Embed Size (px)

Citation preview

Production and Cost

Production FunctionInputs Output (s)

Cost Function

At Given

Output Level Inputs Unit InputNeeded Price

Based on ProductionFunction

TotalCost

Total Product

Look at theslope

TotalProduct Q

Input (Labor)

TP

Total Product

TotalProduct Q

Input (Labor)

TP

Deriving the Average Product Curve

Total Product Q

Input (Labor)

TP

APL

L

APL

Q3

Q2

Q1

P1 P2 P3

TotalProduct Q

Input (Labor)

TP

MPL

L

MPL

Deriving the Marginal Product Curve

Critical Points in Average and Marginal Product

TotalProduct Q

Input (Labor)

TP

MPL

LMPL

APL

AB

C

Stages of Production

Stage III

MPL

L

MPL

APL

A

B

C Stage I Stage II

Economic vs. Accounting Profit

Economic profits from good (service) =Revenue from good (service) – Total Cost of making good (service) – Value of next best alternative

Value of good (service)

Value of next best alternative(aka “opportunity cost”)

Accounting profits from good (services) = Revenue from good (services) – Total cost of making good (services)

Topics in Costs

Estimating cost functions:Identifying Fixed from Variable Costs

Short run costsLong run costs – scale economiesLearning economies (“experience

curves”)Economies of scope

Cost Functions

In any tactical (short run) setting, some production drivers of a company are “fixed” while others are “variable”

What is fixed and what is variable depends on the company, contracts drawn up, and the industry

The Prestige Telephone Company case is (partially) an exercise in identifying fixed from variable costs. Also illustrates importance of accounting in economic decision making

Examples of Fixed and Variable Costs

Fixed CostDriver

Variable Costs Driver

Auto manufacturers

Physical Capital Labor

Materials

Universities Tenured Faculty Power (portion)

Power (portion) Non-tenured faculty Staff

Cost Function

Form of cost function depends on whether we are dealing with the short run or the long run

Short run, some cost drivers are “fixed” (also to be shown in PTC example). Thus cost function is:C = Fixed Costs + Variable Costs

Equation which relates total costs to outputC = f(Q)

Estimating Cost Function

Done by examining cost data (typically from income statements) and extrapolating cost function

Some Fixed Costs are easily identifiedSome Variable Costs are also easily

identified– the real issue is to determine the relationship between TVC and Q (linear or non-linear?)

The trickiest items are “quasi-fixed-variable” costs: these have a fixed and variable component which must be separated

Quick notes about Costs

C = 100 + 38QWhat does F = 100 represent?What does AVC = 38 represent?What is cost of producing an additional

chip, and what does it cover?Any insights into the production technology

which may be gleaned from the cost function?

What is Average Cost (AC)? Know what is C, F, TVC, AVC, AFC, and AC

Separating Fixed and Variable Costs

Argued that some items have a fixed and variable component. How to identify each component?

We must now make assumptions about the form of the cost function: linear, non-linear? “Constant” will be Fixed Cost

Note how scatter plot suggests that a linear cost function seems appropriate

Cost Functions in general

Can be either linear or non-linearIf non-linear, MC depends on level of

productionExample: C = 20,000 + 200Q + 0.5Q2

MC = 200 + QHow to tell if your company has a

linear or a non-linear cost function?►Scatter plot of costs vs. output►Run regressions►Run a battery of test to test functional form

Total Cost

Total Cost = Total Variable Cost + Total Fixed CostTVC,TC

Q

TVC

TC

TFC

Deriving Average Fixed Cost

TFC

Q

TFC

AFC

Q

AFC

Deriving Average Variable Cost

TVC

Input (Labor)

TVC

AVC

Q

AVC

Minimum AVC

AVC decreasing

AVC increasing

Average Total Cost

Q

AFC

ATC AVC AFC

AVC

ATC

AFC

AVC

ATC

Deriving the Marginal Cost Curve

TVC

Q

TC

MC

Q

MC

Minimum MC (Diminishing marginal returns

to variable input) MC declining

MC increasing

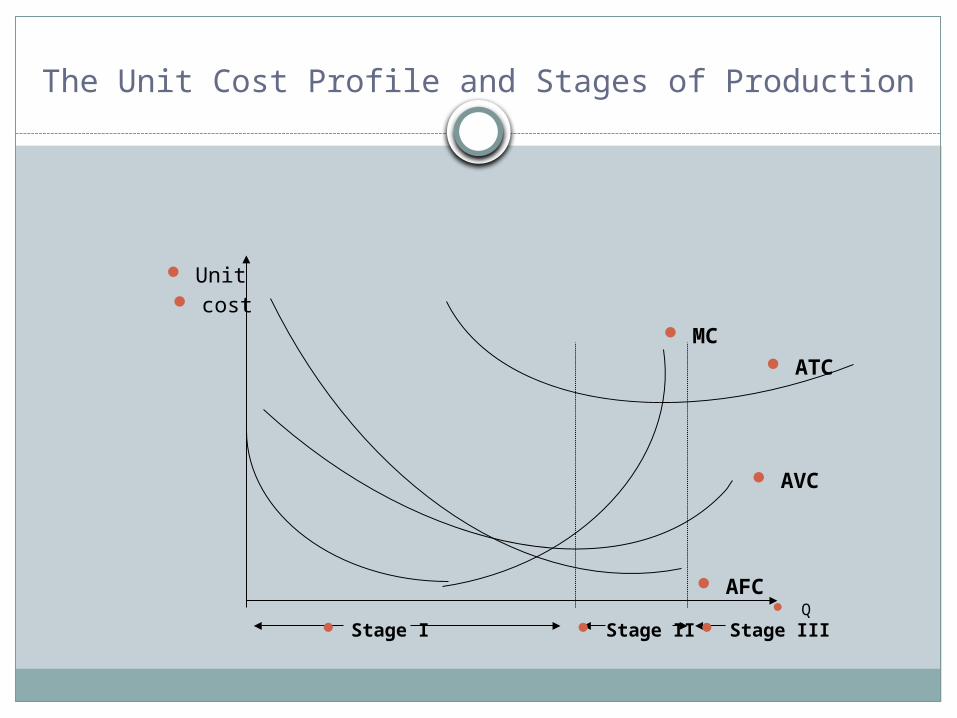

The Unit Cost Profile and Stages of Production

Unit cost

Q

AFC

AVC

ATC

MC

Stage I Stage II Stage III

Why does AC rise/fall? Short Run

Reasons for AC rising/falling are very different depending on whether we are dealing with the short or the long run

In the short run, at least one input is fixed

Output rises from increase in variable inputs

How variable inputs interact with the fixed input determines the shape of the Short run cost functions

Relation between Production and cost

The production function implies the cost functions

Diminishing marginal returns is the reason for increasing MC

The profile of ATC, AVC, AFC and MC is very important for managerial decisions; learn to draw these curves accurately!

Quantity of labor

Co

sts

(d

olla

rs)

Ave

rag

e p

rod

uct

an

dm

arg

inal

pro

du

ct

Quantity of output

MP

MC

Productivity & Cost Curve Relationship

Quantity of labor

Co

sts

(d

olla

rs)

Ave

rag

e p

rod

uct

an

dm

arg

inal

pro

du

ct

Quantity of output

MPAP

MCAVC

Productivity & Cost Curve Relationship

Un

it C

ost

s

Output

For every plant capacity size... there is a short-run ATC curve

and every ATC has a minimum cost

Long-run Production Costs

Un

it C

ost

s

Output

An infinite number of such costcurves can be constructed...

Long-run Production Costs

The Long-run ATC just “envelopes”all of the short-run ATC curves

Un

it C

ost

s

Output

Long-run Production Costs

Long-run ATCUn

it C

ost

s

Output

Long-run Production Costs

Un

it C

ost

s

Output

Long-run ATC

Economiesof scale

Long-run ATC Curves

Un

it C

ost

s

Output

Long-run ATC

Economiesof scale

Constant returnsto scale

Long-run ATC Curves

Un

it C

ost

s

Output

Long-run ATC

Economiesof scale

Diseconomiesof scale

Constant returnsto scale

Long-run ATC Curves

Un

it C

ost

s

Output

Where extensiveeconomies of

scale exist

Long-run ATC Curves

Long-run ATC

Un

it C

ost

s

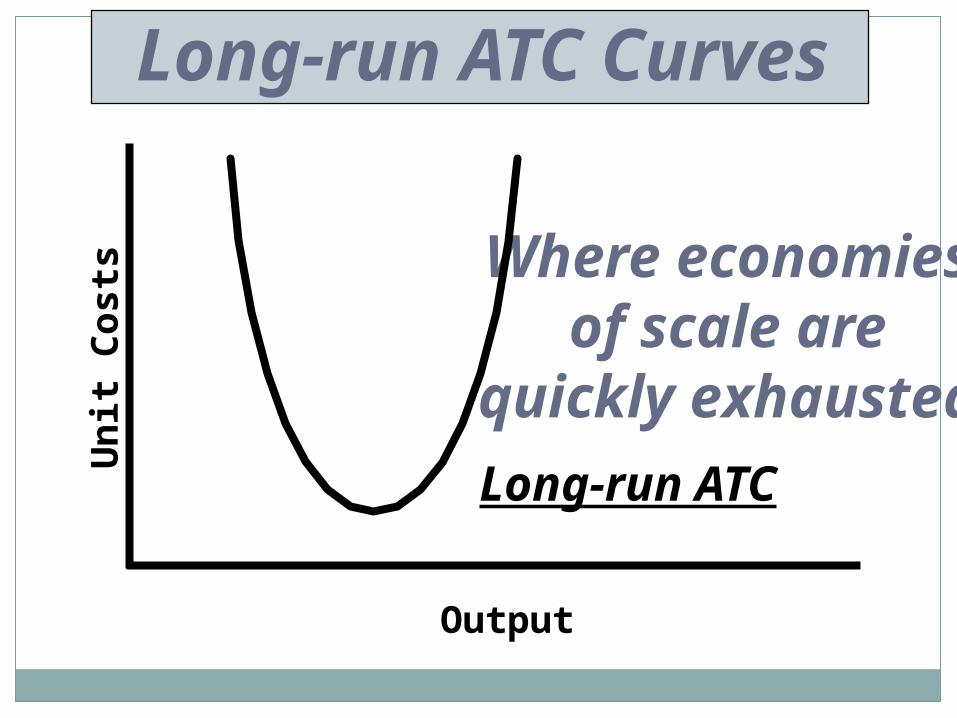

Output

Where economiesof scale are

quickly exhausted

Long-run ATC Curves

Long-run ATC

A last word about...

Minimum Efficient Scale - MESDecision on plant size should relate to the expected demand for the product

Plant Size Expected Demand LRTC LRAC A 10000 $50000 $5.00 B 20000 90000 4.50 C 30000 120000 4.00Although Plant C has lower cost per unit than plant A or B, you do not want to build the plant A or C if your estimated demand is 20000 units.