Embed Size (px)

Citation preview

STUDY ON

PRIVATE INVESTMENT IN THE OIC COUNTRIES BETWEEN STRATEGIC ALLIANCES

AND TRADE PROMOTION

SUBMITTED BY

THE ISLAMIC CENTRE FOR DEVELOPMENT OF TRADE

TO

THE WORKSHOP ON :

"THE PRIVATE SECTOR INVESTMENT IN THE OIC MEMBER COUNTRIES

AND THE ROLE OF IDB"

Istanbul, 14-16 September 2002

1

PRIVATE INVESTMENT IN THE OIC COUNTRIES

BETWEEN STRATEGIC ALLIANCES AND TRADE PROMOTION

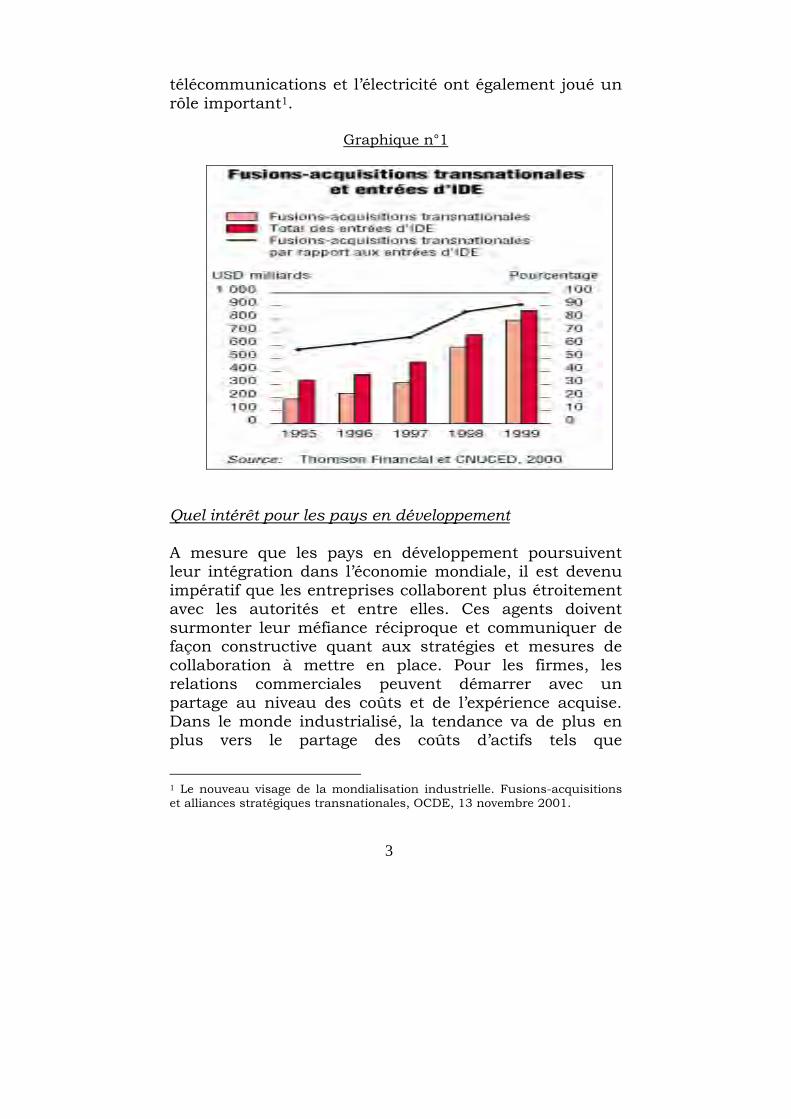

GENERAL INTRODUCTION: Since a few years, the merging of enterprises has been invested with an international dimension to the extent that the transnational merger-acquisition operations have become in 1999 the most important component of the world Foreign direct investment flows (FDI). According to some estimates, these flows have accounted for 92% of total FDI in 1999 against less than 60% in 1995. These groupings have rapidly progressed in the 90’s, their volume increased from 153 billion US dollars in 1990 to about 1000 billion in 2000. They have played a major role in the globalisation and restructuring of activities, with an increasing tendency towards large-scale the operations. The development of merger-acquisitions may be explained by the fact that enterprises are inclined to sell or buy assets abroad instead of investing in the building of new installations. Compared to the building of new installations, the advantage of the acquisition of the existing assets allows to rapidly gaining ground in a market by immediately taking possession of a critical mass of installations and intangible assets in a given industrial sector. Several factors have contributed to the speeding up of such activity in this field worldwide, namely, trade and capital flows liberalisation, the quick technological changes and the rapid progress of information technologies. Privatisations and the reforms of regulations in some sectors and services of public purposes such as financial services, telecommunications and electricity have also played an important role1.

1 Le nouveau visage de la mondialisation industrielle. Fusions-acquisitions et

alliances stratégiques transnationales, OCDE, 13 novembre 2001.

2

Graph n° 1 Transnational mergers acquisitions and FDI inflows

0

200

400

600

800

1000

1995 1996 1997 1998 1999

0%

20%

40%

60%

80%

100%

Transnational Mergers acquisitions (in billion US $)

Total FDI inflows (in billion US $)

Transnational Mergers acquisitionsin comparison with the FDI inflows(in percentage)

Source: Thomson Financial et CNUCED, 2000

What stakes for Developing countries? In so far as developing countries are seeking integration in the world economy, it has become imperative for enterprises to collaborate more closely with authorities and between them. These agents should overcome reciprocal mistrust and set up in concert and harmoniously joint collaboration measures and strategies. As far as companies are concerned, sharing costs and acquired experiences may set up trade relationships. In the industrialised world, companies are more inclined to share the assets costs such as infrastructure, premises, the staff, storing, transport and repairing services, telecommunication systems as well as the common marketing of complementary products. Developing countries should find out their own joint ventures patterns, value added partnership, strategic alliances and cooperation agreements. In fact, in the future the sharing of risks and partnerships are expected to prevail2. Actually, if in the past, Developing countries have led an important import-substitution policy and that technology

2 Forum du commerce international; CCI 01 septembre 1999 page 11.

3

acquisition mainly consisted in imitating techniques used in developed countries, Developing countries are currently more and more focusing on exports oriented policies that require alliances and targeting foreign markets as well as the acquisition of the know-how and technology, which are henceforth established by the world market3. While the life cycles of technology and products are more and more getting shorter, technology and know-how are to a greater extent considered as basic assets that would allow facing competition on national and international markets. For the last two decades, inter-enterprises agreements have considerably developed, contracts by mutual agreement, franchising, concession and sub-contracting contracts are ever more growing. Besides, the recent agreements between air-companies, car manufacturers, information systems companies, insurance companies and Banks are a good evidence of such a development. The impressive merging of Daimler and Chrysler, the buying up of Volvo by Ford, the Renault-Nissan alliance, the attempt of General Motors to take over Daewoo, the absorption of Kia by Hyundai, the buying up of Bentley, Lamborghini and Bugatti by Volkswagen and of Rolls Royce by BMW, in addition to several other merger-acquisitions between manufacturers of components that have started several years ago4 seem to have produced a wave of contacts, negotiations, buyouts and alliances in car industry, which seem more irresistible particularly as similar waves have been noted in other sectors, such as pharmacy, aeronautics, banks insurance, telecommunications, agro food and information technology etc…

3 Renforcement des capacités technologiques : ONUDI, OMC,

IP/C/WW/243/Add2, 16 mars 2001, p 5. 4 Michel Freyssinet fusions acquisitions alliances et internationalisation, quelles

logiques, quelles perspectives?-Université Montesquieu, Bordeaux, éditorial de la lettre du GERPISA (groupe d’études et de recherche permanent sur l’industrie et les salaires de l’automobile), avril 1999, p 1.

4

FIRST PART

STRATEGIC ALLIANCES AND OTHER FORMS OF PARTNERSHIP:

It is generally recognized that partnership agreements are old practices in the industrial world. Garette and Dussage (1995) note the development by the late 60’s of joint ventures (JV)-which constitute the archetype of alliances-within the framework of multinational operations. However, it is the 80’s, which mark the real growth of inter-corporations cooperation. During this period, alliances have grown in number in a context propitious for globalisation and a rapid technological evolution.

Unlike, the previous cooperation forms, which are more properly targeted (licenses, franchising, sub-contracting…), it has been established that strategic alliances allow corporations to build up or acquire in the long run, major strategic skills and to derive benefit from a competitive advantage (Hamel and Pralahad, 1990)5. I. THE NOTION OF ALLIANCE : The several definitions of the concept of alliance are growingly extensive and more or less operational. They can include the most restraining modalities such as the takeover or less constraining ones such as franchising or sub-contracting, transfer of licences or acquisitions.

Strategic alliances consist in long-term agreements concluded between independent companies. These are cooperative arrangements that were set up so as to reach strategic objectives (LORANGE and ROOS, 1982).

5 PERROT Pascal Université de Rennes 2, RUFFIO Philippe , GUILLOUZO

Raymond « Les alliances stratégiques au service du développement des coopératives agroalimentaires (le cas de l’ouest de la France) » 23ème Congrès international du CIRIEC « Economie Sociale et Economie Publique : Nouvelles formes de coopération à l’ère de la mondialisation »13 – 14 juin 2000, Montréal, Québec, Canada.

5

According to the French Standard Association (AFNOR), alliances are: “a frame of mind making possible the establishment of relationships between partners, sharing and seeking the same medium term objectives, in conditions favouring reciprocity of advantages”.

We can also define an alliance as a new organisation entailing long-lasting and perceptible reductions in costs and generating a higher standard quality and a permanent innovation. Such an organisation is based on three main pillars: The redefinition of the roles of the different actors of the

industrial branch. Internal organisation structures, which rely more on

project logic than on a professional logic. The creation of a supplier’s network, which encourages

and facilitates cooperation between all enterprises that are involved in the implementation of the project.

Therefore, alliances represent a modality that would bring closer two or several companies, legally independent, whose objective is to pool their financial and human resources and know-how with a view to jointly carrying out activities dealing with a strategic field such as research and development (R&D), production, marketing etc. Companies agree on an objective, on means, as well as on sharing and controlling results while resorting to less formal modalities. In most cases, they sign contracts that govern the legal and economic aspects of their alliances, as well as its duration. It also happens that they choose arrangements that are more formal such as joint subsidiary companies or joint ventures.

II. THE DIFFERENT FORMS OF ALLIANCES :

PARTNERSHIP or ALLIANCE: In its broadest sense, partnership may refer to strategic alliances, partnerships, joint ventures, collaboration agreements, enterprises networks and coalitions.

Most of alliances may be gathered under the category of horizontal alliances, or under that of vertical alliances. Yet, it

6

happens sometimes that in view of their scope, certain alliances integrate vertical and horizontal components in their structure6. We may also classify alliances according to an organisational criterion based on the shape taken by the cooperation agreement: Is it only a delegation, a concession for the benefit of an already existing entity (sub-contracting strategy) or would it lead to a new entity (integration strategy)7. A. Sub-contracting strategies :

At present, in all the sectors, we may note an increase in sub-contracting practices (contracting out, joint subcontracting and concession), as concerns, products as well as the services sector. An enterprise may contract out functions or the production of sub-systems and components.

Licensing:

Through licensing, the licensor gives to the licensee the right to derive benefit and exploit fundamental and protected values of the enterprise (brands, devices, production processes, distribution channels…)

Thus, the licensee remains dependent on the licensor, at least from the legal point of view (the awarding by the Swiss chemical industry of licences for the production and sales of medicine to foreign companies whose head office is in the United States). In several cases, the enterprise sells also the production plant to the licensee and gives him the necessary instructions for the organisation of production and sales according to their own pattern.

6 There are four kinds of alliances:

- Horizontal alliances (arrangements between competing enterprises producing similar or identical products with a view to limiting competition);

- Vertical alliances (arrangements between enterprises intervening in the different stages of the production-distribution process);

- Mergers - Acquisitions

7 Marketing course of Geneva university , academic year 1999-2000.

7

Most of the business investments will be borne by the licensee. This way, the national enterprise can develop its line of products (eventually, other brands) on difficult markets and partly lagging behind. This way it can save money and invest solely in research and innovation and in the development of new products.

The overall returns of the product line can be basically improved by the supply of licensed products in cross-border markets.

In spite of being interesting, licensing conventions, dictate to international firms several legal and economic precautions, so as to avoid that the licensee becomes a rival.

The basic difference between the licensing convention and franchising, lies in the fact that the licensee remains in principle free on the way and means to sell its product, while the efforts of its counterpart, the franchiser will be strictly restrained on the market and at the same time stimulated thanks to the concept of international franchising provided by the licensor (ex Mac Donald’s restaurants and/or hotels).8 - Sub contracting :

It is an operation through which an entrepreneur, main contractor or prime contractor) entrusts under his responsibility to another person called sub-contractor, the task of carrying out and fulfilling the terms of all or a part of the contract or the market.

Such a definition allows the distinction of another enterprise’s sub-contactor:

The products of the Sub contractor are in general part of the final product but they do not constitute the whole of the final product;

The sub-contactor has not in general established any direct contact with the final consumer; it is the main contractor who establishes such contact.

8 IBID

8

We may distinguish several kinds of sub-contracting : Standard subcontracting Simple subcontracting Extended subcontracting Strategic subcontracting Sub-contracting in partnership

For the enterprise, subcontracting may be a way of getting known and doing business worldwide (internationalisation), in case the enterprise (the main contractor) is undertaking an international activity. It may also lead to the internationalisation of the main contractor if the latter contracts out all or part of a product abroad.

Special case: The original equipment manufacturers (OEM) contract, the prime contractor is called OEM or sourcer, while the components suppliers are considered as the manufacturers of OEM products, that is to say subcontractors.

In an OEM contract, the negotiating power between both parties is often in the interest of the prime contractor. It is not often the case in prime contractor/subcontractor normal relationship. Sometimes, the subcontractor is provided with a special competence or skill, which gives him a special power vis-à-vis, the prime contractor. This certainly explains partly the development of international subcontracting.

The reasons of such development are numerous. The contractor may wish to concentrate on his basic

skills; He may try to reduce the production costs. Each stage of

the supply chain is heading for international subcontracting;

The subcontractor may through his specialisation, be an innovation source

The potential prime contractor may be confronted with a fluctuating demand.

9

In this order, subcontracting implies an increasingly important coordination degree between both parties as the assigned task is more intricate. - FRANCHISING:

A company in a country (the franchiser) authorises a company in another country (franchisee) to use its trademark, its logo and or its production or marketing techniques against the payment of royalties.

There are several kinds of franchising: - Industrial franchising: In this case, the franchiser is a

manufacturer, who concedes to another manufacturer a licence that allows him to use its method and know-how (coca cola for example).

- Services franchising: in this case, the contract provides for the dissemination of a method and know-how (for example Mac Donald’s or Jean Louis Davis). This form of franchising has developed and currently accounts for 40% of franchised sales outlets.

- Production franchising: the franchiser is a producer, who sells his products in shops, which exploits his brand and its reputation (Yves Rocher or Benetton for example).

- Distribution franchising: In this case the franchiser is a wholesaler, who develops a device and disseminates a collection, which he selected with suppliers or which was designed for him (Manoukian or Pronuptia for example).

Concession and agreement:

1. CONCESSION:

The concession is a contract linking a supplier to a merchant, to whom exclusively sells his products, provided that he accepts a trade, accounting and even financial control of his enterprise and sometimes he undertakes to get his supplies from this sector and exclusively from the licensor. Such definition shows that the concession may be a mode of selective distribution and eventually exclusive.

10

- Selective concession: In this case, the producer carefully chooses his distributors and limits the number of sales outlets where his products will be distributed. The selection takes place according to a criterion taking into account the size, and especially the reception, skills and even advice proposed to customers. As concerns the producer, it results in a reduction in distribution costs and allows a qualitative control of sales outlets. Yet, the market coverage remains limited. No exclusivity is imposed on distributors. - Exclusive concession: It is an exclusive concession coupled with and exclusivity clause. In this case, the enterprise does not any more choose sales outlets but some distributors that have exclusive distribution rights of its products in a determined geographical sector. The objective of such a strategy is to enable the development and strengthening of a brand image. That is why; the exclusive concession is often reserved to luxury products or up-market products. The advantage of such a concession lies in the fact that it allows an excellent quality control of sales; it offers the possibility of a light investment for the producer in terms of sales force and logistics but the disadvantage is that is ensures only a weak market coverage in view of the small number of the selected sales outlets. Besides, the control and recruiting of distributors is not often easy. 2. THE AGREEMENT : It is the less restraining form of agreements between enterprises, because it does not provide for any exclusivity condition. The agreement falls within the framework of an intensive distribution policy that will consists in distributing products in maximum sales outlets. The advantage of the

11

agreement lies in the fact that it allows the coverage of an important geographical sector, to conquer high market shares, and make known products rapidly, whence an increase in the turnover. Yet, in keeping with such a strategy, the enterprise must be able to supply to distributors and in very short time limits large quantities. However, such a strategy is only conceivable for enterprises of a certain size. The major characteristics of the agreement may be summarized as follows:

The licensor should designate other distributors in the zone attributed to the franchise holder

The franchise holder does not undertake not to sell competing products.

Yet, the absence of exclusivity does not prevent the application of the essential principles of the concession contract, namely the possibility for the distributor to benefit from the promotional actions of the licensor. - The setting up of a joint subsidiary company: (joint venture) When it concerns companies of different nationalities. In this event, two companies decide to create a common subsidiary company as legal entity. The legal status is freely chosen.

- In general, the “best” subcontracting operations, in other words the easiest operations that can be assessed without difficulty. Through subcontracting, the major subcontracting enterprise should provide a competitive advantage, either in terms of cost, quality or exclusivity, while keeping its self-autonomy. Only limited strategy operations should be contracted out.

12

III/ INTEGRATION STRATEGIES : A/ Integration technique of patrimonial kind : There are three categories:

1. Merger 2. Merger-takeover 3. partial business transfer

Merger is a legal operation that consists in regrouping into one company several companies. For instance, if two companies, that is to say A and B, merge, the operation will result in the breaking up of these companies. Their assets will be unified. A new company will be created by incorporating the assets and liabilities of both A and B companies. Merger-takeover: It is characterised by the take over of a company by another one. Through this operation, the assets of the company, which has taken over the other one, increase. The company, which was taken over, breaks up, but without the creation of a new legal entity as in the previous case. The new owner should increase its capital and assign new securities to shareholders of the company, which was taken over. Partial business transfer: In this case, a company brings assets into another business. For example if the company A brings partial assets for the benefit of a company B, the latter will bring in return, securities to the latter. B/ Integration techniques of financial kind: In this case, it is question of the acquisition, takeover and the setting up of a trust. Acquisition: We speak of acquisition when a company becomes owner of a part of securities by another company. It is considered as an acquisition when the held percentage ranges between 10 to

13

50% of the company’s capital (beyond this percentage it becomes a takeover). Takeover: It is characterised by the holding of a percentage higher than 50%. For example if a company A holds more than 50% of a company B, it becomes a subsidiary company of the company A. However, we may speak of takeover even if the acquisition is lower than 50%. Such techniques are often used for the acquisition of enterprises within the framework of a tender offer. The tender offer is a technique through which a company proposes to the partners of a company that is highly sought after to buy their securities at a rate higher than that of the stock exchange for a limited period, with a view to taking over the targeted company. A tender offer might be friendly or unfriendly. Penetration strategies to foreign markets may therefore be limited to financial participations. In the event of venture capital, the adopted strategy consists in making a profitable investment abroad without any particular ambition to control the management of enterprises. In the seventies, the inflow of the Libyan capital in Fiat Company, at a time when the latter was experiencing great difficulties at production level is an eloquent example. After having clarifying the notions of partnership and alliances, we will deal with the stakes and difficulties related to the implementation process.

14

IV/ THE STATE OF ALLIANCES: A/ Sector-based distribution of alliances9: Porter and Alii (1986:353) have recorded a sector-based shifting of strategic alliances from ripe sectors towards high-tech sectors. Such a trend conflicts with the idea according to which alliances started in high-tech sectors before spreading in a second stage to ripe sectors. In the seventies, cooperation agreements mainly concerned metals, minerals, energy and chemical sectors. While cooperation agreements have constantly declined in the seventies, in the two first sectors, they have recorded a development in the energy sector immediately after the two oil crises. On the other hand, according to Porter and alii, increased alliances in the computer sector have increased in the early eighties. They explain the enhancement of cooperation in the chemicals and computer sectors by their technological intensity. In a latest study, Hagedoorn (1996:602-3) confirms this sector-based shifting of alliances. Actually, in the mid-seventies, strategic alliances were almost inexistent in high technologies such as information technologies, biotechnologies and new materials. Until 1979, alliances in the traditional sectors were more numerous than those in the high-tech areas. But since the 80’s, high-tech strategic alliances have prevailed.

9 Mohamed El Filali El Youssefi, under the supervision of Jorge Niosi. Strategic

alliances between in the globalisation era and of the changes of technological paradigms, Journal of Crises collection “Working papers”.

15

Table n°1 Sector-based distribution of alliances (1980-1993)

Distribution Sectors (%)

Biotechnology 16,2 Microélectronics 15,63 Chemicals 9,34 New matérials 9,29 Télécommunication 8,6 Software 8,55 Air-craft industry/defence 6,82 Industrial automation 5,86 computers 5,3 Car industry 4,3 Other Information Technologies 2,26 Heavy electrical industry 2,00 Technical Instruments 1,74 Électronics 1,69 Food and beverages 1,61 consumption 0,83 Others Total 100,00

Source : Hagedoorn et Narula, 1996.

Such results are corroborated by the study of Menguzzato and Reneau (1992:142), which shows the strong tendency to cooperate and its evolution in the 80’s vary according in the different sectors. Actually, in the young sectors (information, biotechnology) by a relatively important growth potential, a higher technological intensity and a higher globalisation degree, the propensity to cooperation is greater. In sectors, such as the information technologies and biotechnologies, technology is very complex and rapidly changing. Furthermore, they are young (biotechnology) and growing (information) sectors in addition of being globalised sectors. Hergert and Morris (1988:105) draw attention to the concentration of cooperation agreements in five major industries, which alone account for 87% of alliances. Such a result is not surprising since all these sectors are characterised by high entry costs, strong globalisation, scales economies, and by a very changing technology and finally they are considered as being high risk sectors. These are telecommunication, aerospace industries, car industry, computer and electrical equipment industries.

16

B/ GEOGRAPHICAL DISTRIBUTION OF STRATEGIC ALLIANCES:

Ohmae (1985) brings out the predominant role of American European and Japanese enterprises in the international strategic partnership in technology, especially in the computer and car industries. The results of the study of Morris and Hergert (1988:102-103), which covers the period between 1975 and 1986, reveal that the major part of international alliances are established between the partners of the European Community (30.8%) or between partners from the EC and the USA (25.8%). American enterprises account for 47% of registered alliances while the Japanese alliances account for only 18%. Europeans account for 74% of partnerships listed by the study. The rest of the world remains the poor relation of alliances with a little more than 10% of partnerships. Most of international alliances are established by the triad’s enterprises (USA, Europe and Japan). Such a statement has been corroborated by the latest studies, especially those of Freeman and Hagedoorn (1994) and Hagedoorn (1996 a: 612). On the other hand, the study of Porter, Fuller and Rawlinson (1986) shows that the geographical distribution of alliances is in favour of the United States followed by Japan and Europe. This difference between the results of the first analyses and those of the latter may be explained by the fact that the first ones overestimate European data and those of Porter and his colleagues are based on American data. Freeman and Hagedoorn (1994:773) show that for the 1980/1989 period, the predominating position of developed countries is also reflected at the level of the different sectors. In fact, in the biotechnology, software and computer industries, cooperation is quasi-exclusive to developed countries. The predominance of Developed Countries is felt at a lesser degree in food and beverages sectors. It may be explained by the attraction of Developed Countries by the new

17

sectors as well as by the relocation of ripe sectors or less dynamic market openings of ripe sectors in non-industrialised countries. The most typical case is the concentration of the United States followed later on by Europeans and Japanese in chemistry and their reorientation towards refined, specialised and value added chemical industry and at a lesser risk and the disengagement of the basic chemical industry and its relocation in DCs that are endowed with cheap raw materials. The 1990/1993 period marks a major change, in so much as the analysis of Hagedoorn reveals (i) a reduction in the percentage of intra-Europe technologic alliances (9%); (ii) the progression of intra-USA alliances and (iii) a more active participation of other countries’ enterprises (other than those of Europe, the United States and Japan), which has doubled between the 1970/1979 and 1991/1993 periods. The international combinations of alliances have changed in view especially of the increase of the agreements with companies of newly industrialised countries, particularly, those of South-East Asia, such as South Korea, Singapore and Hong Kong. Particular case of mergers and acquisitions: Industrial countries are predominating actors in the cross-border mergers-acquisitions. Since the 80’s, 80% of merger-acquisitions (purchases and sales) are carried out by industrialised countries.

The European Union held the first position in 1999 with

70% of acquisition sales and 50% of the sales carried out between industrialised countries. The outstanding imbalance between purchases and sales is due to the important acquisitions made in the United States. In addition to these operations, the remaining operations (75% of sales and 50% of purchases) are composed of intra-community operations, achieved in general in response to deregulations, regional integration and the creation of the Euro.

The United States are the main targets of operations with a record figure of purchases amounting to US$ 233

18

Billion, of which 80% are carried out by the EU’ s companies (while this share was lower than 50% in the mid-nineties). The acquisitions made by the America companies have dropped by 18%; i.e. US$ 112 billion in 1999, in view of their weak participation in mega-mergers concluded in 1999.

On the whole, Japan is somewhat behind M&A operations, probably in view of the absence of liquid assets, as a consequence of bank crises and those of insurance companies.

Emerging or developing countries remain minor actors with respect to purchases (5% of the world flow in 1999), in spite of an increase in the amounts’ value (US$ 41 Billion, i.e. twice more than in 1998). Yet, it should be underlined that such operations play a structural role in a regional context, particularly in Asia (starting from Singapore) and in Latin America, enabling thus some companies to emerge as important actors in their sectors at world level (Cemex in Mexico in the cement sector for example). As far as Mergers-acquisitions inflows are concerned, the share of emerging countries has increased by 20% of total operations, i.e. 9% in value in 1999), owing to privatisation operations in Latin America and of acquisitions in Asia following the crisis (especially in South Korea). The EU remains the main investor with 40% of inflows in the zone followed by the United States10.

10 Mohamed El Filali El Youssefi, under the supervision of Jorge Niosi. Strategic

alliances between the globalisation era and the changes of technological paradigms, op cit.

Todd Evans, monitor of foreign direct investment, Société d’expansion des exportations, Canada, Août 2000.

19

Table n° 2 Cross-border Mergers-acquisitions in percentage of FDI inflows11

Areas Average from 1997 to 1999

(Percentage) North America 91.7 Western Europe 93.9 Japan 100.0 Latin America 60.9 Eastern Europe 32.9 Africa 31.3 Middle-East 26.9 Asia 21.8 Average of developed countries

95.1

Average of developing countries

36.7

World average 77.1 Source: United Nations Conference on Trade and Development,

Report on investment in the world 2000, p 9

V/ ALLIANCES’ STAKES: In a first stage, the alliances’ objectives is to markedly strengthen enterprises at organisational level and in a second stage, it is at the strategic level that enterprises place the main stakes, (especially with regard to SMEs). Such stakes consist in obtaining advantages in order to overcome the constraints imposed by markets. Thus, the main strategy adopted by large enterprises is to focus on their know-how while combining their skills and by simplifying procedures. Such procedures are simplified because suppliers propose global services (it therefore implies the reduction in the number of interlocutors), it also implies the shrinking of the Industrial network. This reduction in the lean conception has three effects:

Reduction in development and industrialisation costs. Quick marketing of new products (gain in time) Allows making up for costly errors resulting from the

conception stages.

11 Todd Evans, monitor of foreign direct investment, Société d’expansion des

exportations, Canada, Août 2000.

20

The improvement of the production process may encompass/ quality, deadlines, innovation capacity and the efficiency of the management.

In addition to the costs reduction thanks to the economies of scale, there are reductions in the transport costs (and logistics). Finally, if the large enterprises form an alliance to benefit from a broader negotiation scope, SMEs endeavour to resist the increasingly restrictive market conditions. With respect to SMEs, an alliance is justified by the notion of critical size imposed by suppliers or the market. They must also increase their capacity in terms of financial investments, staff or in terms of equipment. But partner ship is above all for these enterprises a means to ensure their survival and meet competition and ensure their development. Better still, it is also an occasion for these enterprises to benefit from a stable order book.

- Yet, it should be underlined that some alliances merely consist of short-lived encounters, which last only for the time during which one of the partners penetrates the market. Others take place as a prelude to the total merger of technologies and capacities of one or several enterprises. More and more multinational companies adopt the strategic option: inter-regional competitive alliance of enterprises into which two or several international companies that are strongly implanted, and often from different areas, pool their capacities and resources to enter into competition at world level or regional level.

- Empirical studies on the determinant of strategic alliances:

According to the study of Hagedoorn (1993), three main causes play a significant role in the constitution of strategic alliances: technological complementarities with 31% of alliances, the reduction in the deadline of innovation which concerns 28% of agreements and market access as well as market restructuring which accounts for 32% of agreements (P: 378). The first two causes are probably the most important for the firms that get involved in technological cooperation.

21

According to the study, the importance of these motives has increasing for the last ten years.

Results show different motives in the different technological fields and industrial sectors. The same study points out that technological complementarity and the reduction in the innovation deadline are less significant cooperation motivations in sectors such as chemistry, the consumer electronic industry, food and beverages industry and to some extent in the car industry.

With regard to the car industry, cooperation started in the seventies and has since then developed. In this sector, the international cooperation agreements that have multiplied between North American, European and Asian enterprises, as shown by Ohmae (1958:201-6), correspond to a new competitive game allowing in particular to enterprises the access to skills and markets. In view of the FDI and the acquisitions, cooperation is an external increasing formula, use to penetrate foreign markets, to improve productive efficiency and widen the line of products and introduce innovations. (Sachwald, 1993, p. 86-102).

These motives are not the same in all the countries. The penetration of a foreign market is an objective, which concerns all the Japanese enterprises in view of the efficiency of their production process. The main target of the Japanese enterprises is on the one hand, exports in order to reduce costs and risks incurred by the penetration in a new market and to rapidly enter a market on the other. Besides, they also seek to be implanted abroad so as to use the already existing networks and benefit from the knowledge of the market conditions acquired by a future partner (Mitsubishi/Chrysler and Toyota/GM).

The efficiency objective12 is reached through (i) access to production: the European and American enterprises, whose

12 Chesnais (1988), contractor et Lorange (1988). Ohmae (1988). The author has

used the Merit databases-Cooperative agreements and Technology indicators (CATI). It is a relational database, which includes information on more than 1,300 technological cooperation agreements (systematic inventory) involving

22

performance is lower in terms of efficiency and seek to improve their situation through alliances with their Japanese competitors with a view to learning “new quality control processes and techniques” (Chrysler/Mitsubishi) (Ohmae, 1985:205); (ii) the achievement of economies of scale (Renault, Peugeot, Volvo for the V6 engine); the delocalisation of Japanese and European production towards less industrialised countries and the widening of the range of products (GM/Toyota). The chemical industry, which is a complex industry, diversified and capital intensive and cyclical was stricken by a crisis in 1980. With a view to reducing the cyclical effect of this industry, enterprises have adopted a portfolio reorganisation strategy as well as a globalisation one. The first one aims at re-orienting this industry towards refined or specialised chemistry, implying thus a disengagement of basic chemistry. Now, both refined and specialised chemistry require a high capacity for innovation and adaptation to meet demand. These two factors imply internationalisation in order to meet the cost of R&D and produce on the spot to be informed of the potential needs of customers (Sachwald, 1993:259-303). Therefore, cooperation is the ideal tool to achieve such objectives.

- Market access and reorganisation is an important motive in the four ripe sectors (car industry, chemistry, the consumer electronic industry, food and beverages as well as computer and micro-electronic industry. With respect to telecommunications, the importance of this motive is understandable, in view of the prevalence in this sector national monopolies and domestic oligopolistic markets. Even for the large companies, the access to international markets was only possible through alliances with the national producers of this market. For the last few years, this sector has been restructured due to an excess of capacity, an ineffective technologic development and a

about 5,000 parent companies concluded in the 80’s. For some sectors or technological fields, it was possible to collect information on cooperation agreements from 1980 to 1993.

23

sharp competition in which alliances play a great role. The last argument explains the importance of this motive in major sectors such as computer and micro-electronic industry (Hagedoorn, 1993:380).

On the other hand, in the semiconductors industry characterised by the intensification of competition upon the emergence on the world market of new producers and the importance of the technological factor, we are witnessing the setting up of joint ventures and technological development agreements for the acquisition of technology, market access, and the sharing of cost and risks and the strengthening of the productive capacity (Hobbay, 1993:172). VI/ DIFFICULTIES: No matter the different forms that alliances may take, the key to success lies in a careful planning and preparation; partnership cannot take shape overnight, the transformation of partnership speech into concrete and profitable reality goes through an apprenticeship period of cooperation, which is often costly. It is essential to define beforehand the common objectives. The fact of defining common strategies guarantees competitive advantage. But it also requires a deep cultural change. Besides, it is important to share information, to take common decisions and obtain the contribution of each party and not to press on suppliers. If need be, the prime contractor should help the supplier reach the targeted objective by delegating on the spot his technicians in order to improve the working methods. Such a transformation implies of course upstream adequate strategic reflections and a good preparation of collaboration. On the other hand, a difficulty arises from the fact that partners sign contracts concerning their targeted objectives before even starting the design and development process13.

13 J.Mbendé, le 24/11/98 (IUP Management des achats Grenoble).

24

The transnational cooperation agreements between car manufacturers (as attested by the agreement between Fiat and Ford explained by Guiseppe Volpato) can fail for reasons relating to power sharing and difficulties encountered to coordinate and even integrate the different services of “cooperating” enterprises. Furthermore, as pointed out by Koichi Shimokawa and young-suk Hyun, the problems generated by imbalanced alliances within which one of the partners pursues the objectives of his leader collaborator. For instance, thanks to its alliance with Chrysler, Mitsubishi has not succeeded in building up its own brand image in the USA. This ultimate alliance was rather disadvantageous. Actually, when Mitsubishi implanted at the USA its own production activities, it did not manage to make profitable owing to its weak commercial power. As to alliance between Deawoo and GM, we can speak of a “strong path dependency”, since Daewoo has produced for twenty one years from 1972 to 1992 for the American market, patterns designed by (Chevrolet, Rekord, LeMans…), while being confined within the internationalisation strategy of the American giant. Of course, this alliance has enabled Daewoo to follow a path of technological training, but the latter could not result in an autonomous design strategy of new patterns and of an international reorganisation as long as Daewoo remained under the dependency of GM. That is why, Daewoo has really started to follow its own internationalisation path while endeavouring to reconquer its domestic market starting from 1993 after its breaking off with GM14. According to the experience of strategic alliances in the car sector, the global environment of the enterprise contributes also to the success or to the failure of alliances. Actually, the lack of harmonisation of monetary, legislative and tariff systems fit for each country, generates economic risks for enterprises that are difficult to forecast (fluctuation of the

14 Lydie LAIGLE, stratégies et trajectoires d’internationalisation des firmes

Asiatiques et européennes, Actes du GERPISA n° 22, pp 3-5.

25

exchange rate, unsteadiness of the stock exchange and the financial markets). Likewise, one should not underrate the difficulties linked to the evolution of the political, social and macroeconomic situations (saving rates of households, distribution of incomes…) of countries in which the firms with which agreements are concluded, as shown by the agreement between the Soviet Government and fiat.

SECOND PART:

IMPACT OF ALLIANCES AND PARTNERSHIP ON TRADE

A/ Impact on trade: Empiric research works show that up till the mid-eighties, it is the international trade that has generated direct investments. After this period, the causality seems to have reversed and direct investment exerts a major influence on trade. More especially, data show that direct investments abroad stimulate the increase of the country of origin’s exports (investor country) and consequently they are complementary to trade. Through an analysis on a set of 14 countries, it was noted that each invested dollar produces about 2 US dollars of additional exports. On the other hand, most often in the host countries, short-term foreign investments tend to increase imports while the increase in exports is realised only in the long term. Yet, in the short term, the host countries derive several benefits from foreign investments (technological transfers, creation of jobs, local sub-contracting, etc)15. - From the point of view of the investor: the FDI may be

considered as substituting for trade, in so much as exports 15 Lionel Fontagné, Foreign Direct investment and international trade are they

complementary or substitutable? Working document of the DSTI, OECD 1999/3.

26

are replaced by domestic sales on foreign markets, particularly, under the form of finished products. This state of things may be harmful to the industry of the investing country, by reducing its production and employment level. On the other hand, the FDI and trade may be considered as complementary in so far as foreign investments reinforce competitiveness on foreign markets and increase trade in intermediary goods (inputs) and of finished products towards the subsidiary company. These kinds of links are expected to be beneficial for the exports of the investing country and hence for its industry.

- For the host countries, the link between the FDI and trade may be considered as symmetrical to the one observed in the investing country. The domestic sales and purchases made by foreign subsidiary companies replace imports from the investing country and thereby improve the situation of the current balance, the domestic production and the employment level. If the FDI leads to the imports of inputs, it can result in a weakening of the current balance of the host country, such a conclusion is corroborated by some studies. Thus, the progression by 28% in 1997 of foreign investments in the Caribbean and in Latin America, mainly in Brazil and in Mexico has led to a deterioration of the current balance in all the area.

As a general rule, the impact of alliances and investments relating to it generates the following effects: The outflows of FDI lead to imports in case of upstream vertical integration and/or the delocalisation abroad of labour intensive activities from capital-intensive countries. The inflows of FDI lead to exports if foreign enterprises are established in the host country in order to reexport to their own countries or supply a regional market. The outflows of FDI generate exports if competitiveness on foreign markets improves or if they give rise to a reduction in exports in the opposite case.

27

The inflows of FDI give rise to imports if competitiveness of foreign enterprises on domestic market improves but they can generate exports when the host country improves its competitiveness. 1- Impact on imports: In general, the impact of the FDI (mergers and acquisitions in particular) on the balance of payments of the host country is especially exercised through trade flows that are related to it. Apart from a completely secluded country, any FDI results in an increase in imports, owing only to its effects on the level of the domestic economic activity. More often, the FDI itself creates a new sources or demand for imports like national enterprises that develop around the activities of foreign subsidiary companies16. A project of the FDI entirely new in a developing country will undoubtedly require an initial supply with machinery and tools as well as with imported intermediary goods and services. After the establishment stage, a good number of factors are likely to intervene in order to determine to what extent a foreign subsidiary company will continue to import goods and services. These factors are notably the sector where the production sector of the host country’s economy in which the FDI operates (the FDI in agriculture, the mining sector and several services sectors, for example tend to have an import coefficient globally lower than the FDI in the manufacturing sector) and the age of the project (when a project is ready, the foreign subsidiary countries tend to become less dependant on imported inputs, because suppliers of components and domestic subcontractors are developing). The UNCTAD quotes a study based on a survey conducted in 1995 where it can be noted that with regard to 18 of the largest foreign companies belonging to the electrical and

16 According to the UNCTAD even if the recourse to national suppliers is

increasing, there can be an increase in imports to satisfy the demand from the suppliers of national components. Refer to the World Investment Report, 1997 quoting the UN Centre on the transnational companies (1981).

28

electronics sectors in Malaysia, the value of imported materials and components has accounted for 78% of total inputs, which is more than the average for the whole manufacturing industries17. Yet, as observed by the UNCTAD, it is question of an international and very competitive sector, which depends on specialised inputs meeting the standards of a precise quality. The UNCTAD also quotes studies where encouraging signs were observed of foreign subsidiary companies establishing upstream links and replacing imported inputs by domestic products18. The UNCTAD indicates in comparison that the FDI in the Malaysian extractive industries requires relatively less imported inputs and yields a high national value added per production unit19. In the study mentioned here above, the UNCTAD explains in its analysis that the high increase of the import share in the GDP, which rose from 25% in 1985 to 40% in 1991, was mainly the result of a strong dependency on imports, in addition to the increasing role of the FDI. Foreign investors imported 90% of machinery and equipments and 50% of raw materials required by the projects. Likewise, several studies tend to show that the import needs of the foreign subsidiary companies per production unit tend to reduce over time thanks to the increase in domestic supplies. McAleese and McDonald have noted such decrease in Ireland for the 1952-1974 period, ORR noted such tendency for the Japanese foreign subsidiary companies in the USA for the 1967-1989 period and was confirmed by FRY for the host

17 Ariff Mohamed and Yew Sieng Yong (1996), Transnational corporations and

industrial restructuring in developing countries. The case of Malaysia” ( Kuala Lumpur: University of Malaysia), lecture handout quoted in the UNCTAD (1997), op. cit.

18 Athukorala, Premachandra and Jayan Menon (1995), developing with foreign investment: Malaysia”, The Australian Economic Review, 1st semester, pages 9 to 22; and Sivalingham, M and Siew-Peng Yong (1993), TNCs and industrialisation in Malaysia: organisational behaviour and local and egional impacts”, Regional development dialogue, 14, 4 (hiver), pages 40 to 64, quoted in the UNCTAD (1997)n op, cit, page 91.

19 UNCTAD quotes Sivalingham et Yong (1993) op. cit., which have noted that in the sector of resources exploitation in Malaysia, the FDI content of input of national origin amounted to 76% in 1883.

29

countries of the Asia-Pacific region during the 80’s20. The UNCTAD has noted that the local purchases of the Japanese subsidiary companies in Asia increased from 27% of the global purchases in 1981 to 44% in 1988, and decreased to 34% during the 1994 financial year21. In Latin America, it noted that this share had regularly increased, going up from 28% in 1981 to 39% during the financial year 199422. South Korea had supplied to the WTO working group on “Trade and investment” the following indicative elements of such tendency23: In the early eighties, the stimulation effect of imports was felt significantly, because the foreign subsidiary companies were tending to buy raw materials, production and capital goods in the country of origin. Yet, the replacement effect of imports gradually enhanced in view of the integration at local level of foreign subsidiary companies offsetting thus the effect of the afore mentioned stimulation effect of imports”. - One of the measures that were used to reduce the import

output ratio of the FDI and hence to attenuate the “negative” effects of the FDI on the balance of payments in the host countries consists in requiring from subsidiary companies to respect a certain proportion of elements of national origin24.

In conclusion, it can be noted that in the long term the direct effects of the FDI’s flows on trade balance tend to be unfavourable for host countries25. Similarly, the negative impact can disappear in the long term, in view of the favourable implications of the technological progress and growth. This evolution seems to be all the more likely, 20 ORR James (1991), the trade balancing effects of Foreign trade Investment in

U.S. Manufacturing”, FRBNY Quarterly review, summer, pages 63 to 76; Fry, Maxwell (1993 and 1996), op.cit.

21 UNCTAD (1997), op.cit. note 63, page 104. 22 IBID. 23 WTO, WT/WGTI/W/16. 24 Investisssement étranger direct et balance des paiements, OMC,

WT/WGTI/W95, 2 Février 2001. 25 Lionel Fontagné, l’investissment direct étranger et le commerce international:

sont-ils compléméntaires ou substituables? Document de travail de la dsti, OCDE 1999/3, p 24.

30

especially as pointed out by Drabek (1988), the short effect is associated to induced imports of intermediary and capital goods, which are at the origin of a large part of favourable implications. Yet the final result will depend on the relevance of followed policies and other environmental conditions in which enterprises operate.

Table n° 3 The effects on trade of the prescriptions of required results26

Input Imports

per unit of local production

Imports competing with the local

production unit

Export of finished products per local production unit

Content in national products

(Dropping) (Increasing) (Dropping)

Export results ? (Increasing) (Increasing)

Trade balancing (Dropping) (Increasing) (Increasing)

Restrictions on foreign participation

? ? ?

Technological transfer

? ? ?

Note : Indirect effects are mentioned between brackets. The interrogation sign means that the effects on trade are not obvious.

Source : WTO 1998

2. Impact on exports: According to several reports and studies of several inter-governmental organisations, the composition of the FDI realized in the Developing countries has progressed: after having been motivated by the search for markets (often with a view to overcoming obstacles to import), investment is at present more motivated by the search for efficiency. The basic concern being the implantation of each stage of production or the final processing intended for the world market or for a regional market, in the country where its completion will be the most profitable thanks to the existence of useful products, natural resources, labour and technology27.

26 Effets des incitations à l’investissement et des prescriptions de résultats sur le

commerce international note du Secrétariat de l’OMC, document n° WT/WGTI/W/56 30 Septembre 1998, p 14.

27 WTO, W/8/Add.1, pages 9-12.

31

Foreign investors facilitate thus, directly the access of hosting countries to international markets, because they not only subdivide production between several countries and link the different stages to the flows of international trade, but also because they are provided with international distribution channels for the final product and in some cases with services provided by their foreign subsidiary companies. The supplied indications show that because they better know the world markets and that they can accede to international marketing channels, foreign enterprises deal with international trade more than national enterprises28. Likewise, the data on the export share of the host country, which is imputable to foreign subsidiary companies, show empirically the effects produced by the FDI on the export results of the host country thanks to the activity of these foreign enterprises29. The information collected from reports submitted by intergovernmental organisations to the WTO working group on “trade and investment”, show that the direct contribution of multinational enterprises to the exports performances recorded in the host country are not resulting only from the exports achieved by the foreign subsidiary companies; there is also an indirect contribution, in so far as these foreign enterprises boost the exports carried out by other enterprises in the host country. Actually, the driving effects established thanks to the distribution channels of the multinational companies, which facilitated the access to international markets are favoured by a range of intra-group contractual measures, under the shape, for example, of subcontracting agreements, licence granting, agreements on the splitting up of production30. Besides, it has been proved that the presence 28 WTO, W//8/Add.1, pages 27; W/7 paragraph 58. 29 According to one of the studies made in 1994 the exports of subsidiary foreign

companies with American capitals accounted for about 10% of Argentina, Brazil, Chile, Indonesia, Malaysia and Philippines, but if we add other foreign subsidiary companies, the share of these foreign enterprises in the total exports of some countries may be higher than 50%. In some sectors such as micro electronic components and micro processors this export share is sometimes higher than 90% (W/26, p. 34). According to a study on the FDI in China, the share of the foreign subsidiary companies in total exports increased from 17% in 1991 to 31,3% in 1995 (WTO, W/8/Add.2, p. 25).

30 WTO, W/26, pages 35.

32

of subsidiary foreign companies specialised in exports, is favourably felt owing to the demonstrations and information they provide, which contribute to building up the export capacities of the host country31. Likewise, in the note on “the linkages between trade and foreign direct investment”, the WTO secretariat, after having reviewed some concrete studies, has concluded that the FDI carried out in Developing Countries directly favour the exports of all these countries, owing to the export activities of multinational companies, and indirectly by reducing for national companies financial obstacles or by making up for the lack of information which prevented them from exporting or developing their exports32. On the basis of their national experience, a number of countries confirm the positive direct and indirect effects of the FDI inflows on the volume and the structure of their exports in the reports submitted to the WTO33. The FDI was sometimes strongly stimulated by the creation or the extension of some regional economic integration measures, which broaden the “national” market and guarantee that the host country will henceforth seek stability in its trade relations. If this form of FDI is often motivated mainly by the search for markets, it nevertheless favours often the intensification of trade within the area once production is restructured at regional level34.

31 WTO, W/8/ADD.2, page 27. 32 WTO, W/7, paragraphs 10 and 56-60. (see also the document n° 71712 of the

WTO which followed the observations formulated, by second meeting of the working group on Trade and Investment, on the conclusions made in the document W/7 on the linkages between the FDI and the exports results).

33 Refer to the papers within the WTO committee on trade and investment: of Japan (W/11, pages 2-3), of Poland (W/13, page 3) of Korea (W/16, pages 5-6 and of Costa Rica (W/31, pages 2-3.

34 The FDI and foreign portfolio investments are in general carried out by two kinds of different investors, which neither have the same motivations nor the same anticipations as to the advantages of their investments. On the whole, the FDI are made by enterprises involved in the production of goods and services, wishing to develop their commercial activities. The portfolio investors are either financial institutions, institutional investors (such as pension funds, insurance companies or investments funds) or individuals that are motivated by the financial profitability of their investments (increase in values or

33

B/ Portfolio investment and exports35: According to the WTO, foreign portfolio investments in Developing Countries are in general a more recent phenomenon than the FDI. They have therefore formed the subject of less research and analysis and for the moment, they are little empiric studies on this subject. Data collection and statistics on foreign Portfolio investment is also not very advanced and rises more conceptual problems than data collection and statistics on the FDIs. 1- General impact: Case of mergers and acquisitions.

According to a survey conducted by the UNCTAD for example, the data of the balance of payments for the 1990/1997 period show that for the two thirds of a sample of 30 developing countries and economies in transition, the FDI were on an average more important than the foreign portfolio investments36. According to some empiric studies, the profitability of the enterprises, which were subjected to a merger or acquisition, have in the best cases kept the same rate of profitability in the short term. Actually, the sales profit rate is not immediately likely to be sensitive to a takeover. Yet, the intensity of R&D expenditure is positively affected by the influence of the takeover.

Foreign interests do not positively affect the short-term profitability of enterprises during a takeover. Actually, the sales profitability rate highly reduces immediately after the takeover.

dividends) and who do not expect at first to have a sustainable interest in the enterprise or to directly intervene in its management

35 The recent meeting of the UNCTAD’s experts on the portfolio investments flows has concluded among others: “Given the importance of the foreign portfolio investments, countries should boost their efforts to establish accurate statistics of these flows for the purpose of analysis and for the orientation of the governmental action”. (TD/B/COM.2/EM.6/L.1, paragraph 2).

36 IBID, page 8.

34

The enterprises, which were subjected to a takeover, seemed to have intensified their investment activities in physical capital or in R&D37.

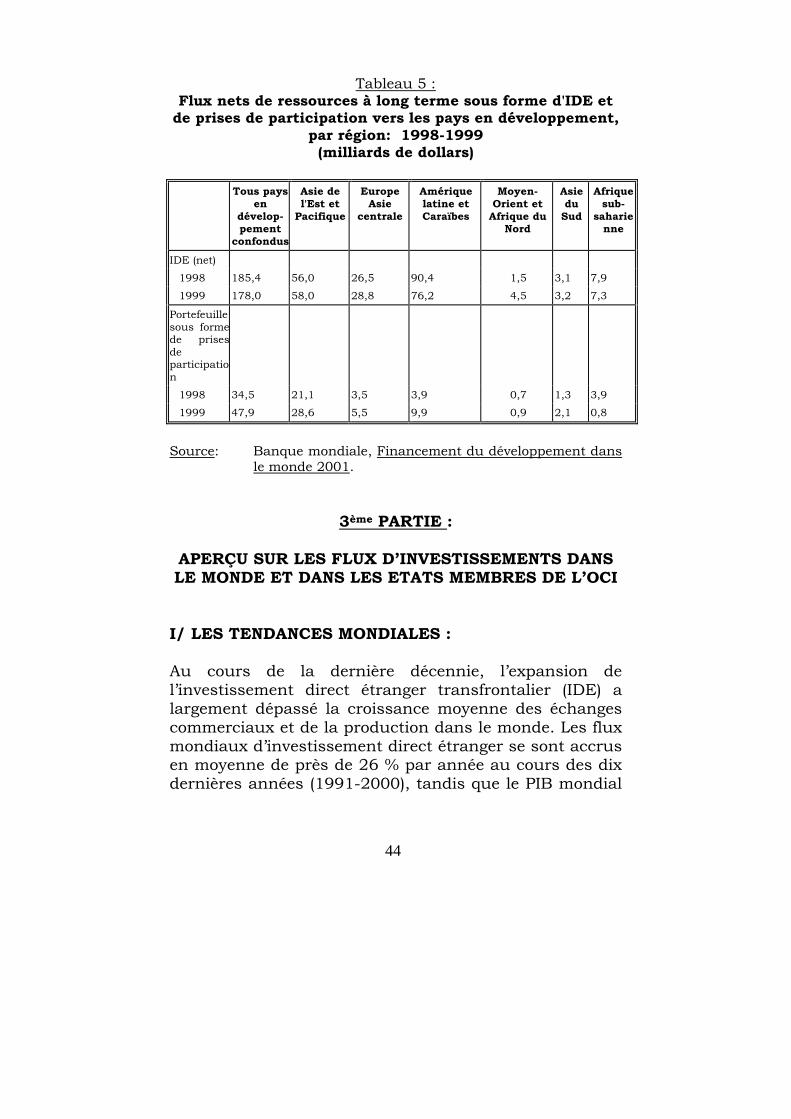

Table n°4

Main net flows of resources in the long term towards Developing countries, 1991/2000 (Billion US dollars)

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Total 123.0 155.8 220.4 223.7 261.2 311.2 342.6 334.9 264.5 295.8

Of which:

Private flows 62.1 99.3 166.8 175.7 206.1 279.3 299.8 280.3 219.2 257.2

Of which

FDI 35.7 47.1 66.6 90.0 107.0 131.5 172.6 176.8 185.4 178.0

FPI 18.5 25.2 87.6 73.4 66.9 111.7 79.2 56.5 59.9 78.1

(Participations) (7.6) (14.1) (51.0) (35.2) (36.1) (49.2) (30.2) (15.6) (34.5) (47.9)

(Obligations) (10.9) (11.1) (36.6) (38.2) (30.8) (62.5) (49.0) (40.9) (25.4) (30.3)

Bank loans 5.0 16.2 3.4 8.7 30.5 33.7 45.2 50.0 24.6 0.7

Source: Word Bank, Financement de développement dans le monde 2001, tables 2&3

The World Bank for example tends to show that merger and acquisitions activities made in developing countries in the 90’s have opened new possibilities because they intervened in activity areas that produced non-tradable goods and services, contrary to the entirely new FDI, which for the major part concerned the manufacturing sector38. According to the World Bank, half of the merger-acquisitions made in East Asia for the last few years concerned non-exporting sectors, such as wholesale and Retail, real estate and the financial sector. Initially, we may therefore conclude that foreign investments under the form of mergers-acquisitions are less centred on exports than the FDI. Anyhow, once the enterprise is under the control of foreign investors, it is the latter who decide if it stay or not in the non-tradable goods sector.

37 The economic impact of the mergers and acquisitions activities on Gilles

Mcdougall enterprises, division of the microeconomic policy analysis, Canada Industry. Working document n°4, February 1995.

38 World Bank, Financement du développement dans le monde 2001 (Washington D.C.), page 36.

35

Table n° 5 Net resources flow under the form of FDI and takeovers

towards developing countries per area: 1998/1999 (Billion US dollars)

Including all Developing Countries

East Asia and Pacific

Europe Central

Asia

Latin America and Caribbean

Middle East and North

Africa

South Asia

Sub Saharan Africa

FDI (net)

1998 185.4 56.0 26.5 90.4 1.5 3.1 7.9

1999 178.0 58.0 28.8 76.2 4.5 3.2 7.3

Portfolio investment (Case of Takeover)

1998 34.5 21.1 3.5 3.9 0.7 1.3 3.9

1999 47.9 28.6 5.5 9.9 0.9 2.1 0.8

Source: Banque mondiale, Financement du développement dans le monde 2001.

THIRD PART:

OVERVIEW OF THE INVESTMENTS FLOWS IN THE WORLD AND IN THE OIC MEMBER STATES

I/ WORLD TRENDS : For the last decade, the growth of cross-border foreign direct

investment (FDI) has to a large extent exceeded the average growth of trade and production in the world. The flows of foreign direct investments have increased on an average by about 26% per year during the last ten years (1991/2000); while the GDP has increased by 4% and trade by 7% on an average. In the past, the FDI served to counter trade barriers, to accede foreign markets and profit by cheap labour and general governmental incentives. Even if these factors are still playing a role, the decision in the field of the FDI are more aiming at making the most from the competitive advantage of an enterprise by establishing production in the sector where it is the most efficient.

The world flows of the FDI reached a record amount of 1150 billion US dollars in 2000 after having reached 865 Billion US

36

dollars in 1999. The growth rate reaching +27%, even it is though lower than in 1998 (+80%) it remains exceptional). - The cross-border mergers-acquisitions (M&A) consist the

main factor, which explains the recent increases of the FDI. The surplus capacity of a good number of industries in the world and the accruing necessity to rationalise production and reduce costs, contribute to the increase of the cross border merger-acquisitions. Actually, it is much easier for a multinational company to buy some of the existing assets than invest in the construction of new infrastructures or manufacturing plants.

The cross-border M&A have increased from less than 75 billion US dollars in 1987 to 1.14 billion US dollars in 2000. The monetary value of the international M&A has increased by 49.3% in 2000. But the international M&A accounted for 90% of the FDI flows in the world in 2000, comparatively to 50% only in 199139. The steady economic growth of industrialised countries and the recovery on emerging markets have also boosted the FDI in the long term. The privatisation of the States enterprises stimulate the foreign capital flows towards several developing or transitional economies, despite of the slowing down of the flows linked to privatisation on some markets (such Latin America) recorded last year. Besides, the ongoing liberalisation is removing the obstacles to cross-border investment in the telecommunications and financial services (Banking services and insurance). Prevalence of industrialised countries : Industrialised countries account for 91.5% of the FDI outflows and hold 90% of the world stocks; they have also received 73.5% of the FDI inflows and hold 68% of the world stocks. - Western Europe is to a large extent the major source of FDI

in 1999 accounting for 65% of FDI outflows, followed by the NAFTA with 21%, Asia 8.3%, Latin America 6%, Africa,

39 Moniteur de l’Investissement Direct Etranger, op cit, pp 3-8.

37

the Middle East and East Europe account respectively for 0.5% and 0.3%.

- With respect to FDI inflows, West Europe and the NAFTA are on the lead of the attractive zones of the FDI accounting for 36% of the flows each, followed by Asia with 14% (5% of which for China), Latin America with 10% of flows. And then East Europe, Africa and the Middle East with respectively 3% and 2%.

Minority share of Developing countries: The relative share of Developing countries in the FDI dropped slightly in 1999, thus, developed countries received 75% of the inflows of the FDI against 71.5% in 1998. Asia receives more than half of these flows (106 billion US dollars+9%) confirming thus at the end of the crisis, but with geographical disparities. China remains the most attractive (63.5 Billion US dollars of which 23 billion for Hong Kong) followed by the Newly Industrialised Countries, except for Thailand whose flows are diminishing while keeping a relatively high level. Finally, Indonesia has experienced massive disinvestments (-3 billion US dollars in 1999 that followed political instability. Africa accounting for 1.2% (10 Billion US dollars), remains on the whole neglected in spite of an increase by 28% benefiting Angola (Oil investments) Egypt (In response to important deregulations), South Africa, Morocco, Tunisia and Nigeria (traditionally, the most important recipient country). II/ INVESTMENT FLOWS IN THE OIC MEMBER COUNTRIES: The OIC Member Countries received 0.42% of FDI inflows against 4% in 1996 and approximately 0.23% of Portfolio investment against 1% in 1996.

38

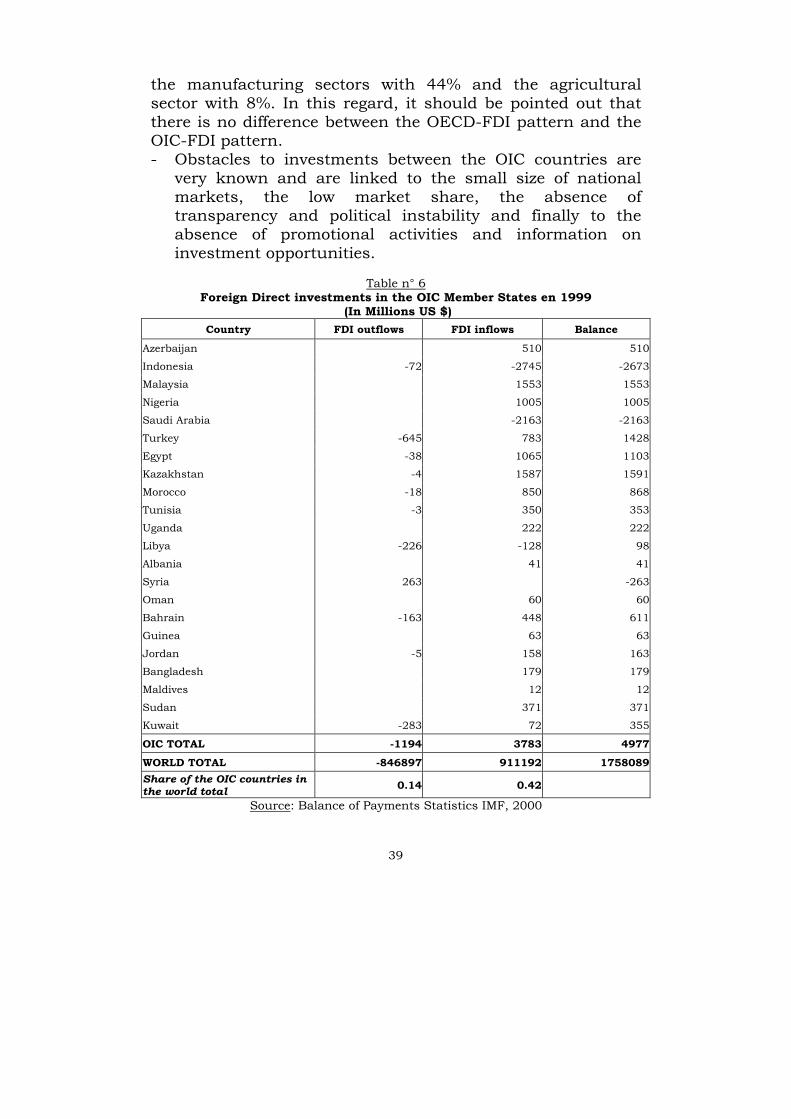

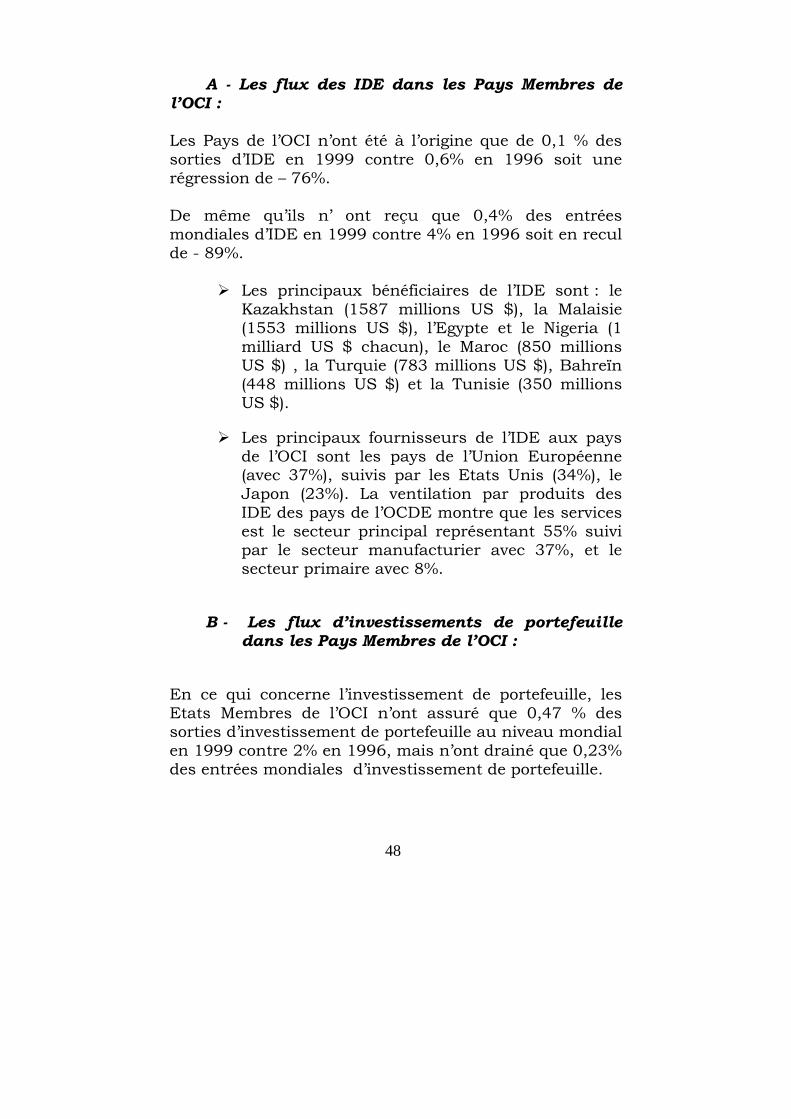

A/ FDI flows in the OIC Member States:

- The OIC Member States accounted for 0.1% of the FDI outflows in 1999 against 0.6% in 1996; i.e. a decrease by –76%.

Likewise, they only received 0.4% of the world inputs of FDI in 1999 against 4% in 1996, i.e. a decrease by –89%.

The main beneficiaries of the FDI are Kazakhstan (1587 million US dollars), Malaysia (1553 million US dollars), Egypt and Nigeria (one Billion US dollars each), Morocco (850 million US dollars), Turkey (783 million US dollars), Bahrain (448 million US dollars) and Tunisia (350 million US dollars).

The main providers of the FDI to the OIC countries are the European countries (with 37%), followed by the United States (34%), Japan (23%). The breaking down per product of the FDI to the OECD countries shows that services is the main sector accounting for 55% followed by the manufacturing sector with 37% and the primary sector accounting for 8%.

B/ The Portfolio investment flows in the OIC Member Countries:

As far as the portfolio investment is concerned, the OIC Member States accounted for 0.47% only of the outflows of portfolio investments at world level in 1999 against 2% in 1996, but they attracted 0.23% of the world inflows of portfolio investment. The main beneficiaries of portfolio investments are Turkey with 4 billion US dollars and Malaysia with 800 million US dollars. Among the OIC Member States, Saudi Arabia was the main supplier of portfolio investments in 1999 accounting for 11.7 billion US dollars.

With respect to intra-OIC investments, it can be noted that in spite of lack of adequate information, the total flows of the FDI are estimated at about 3 billion US dollars and the main targeted sectors are as follows: services accounting for 48%,

39

the manufacturing sectors with 44% and the agricultural sector with 8%. In this regard, it should be pointed out that there is no difference between the OECD-FDI pattern and the OIC-FDI pattern. - Obstacles to investments between the OIC countries are

very known and are linked to the small size of national markets, the low market share, the absence of transparency and political instability and finally to the absence of promotional activities and information on investment opportunities.

Table n° 6

Foreign Direct investments in the OIC Member States en 1999 (In Millions US $)

Country FDI outflows FDI inflows Balance

Azerbaijan 510 510

Indonesia -72 -2745 -2673

Malaysia 1553 1553

Nigeria 1005 1005

Saudi Arabia -2163 -2163

Turkey -645 783 1428

Egypt -38 1065 1103

Kazakhstan -4 1587 1591

Morocco -18 850 868

Tunisia -3 350 353

Uganda 222 222

Libya -226 -128 98

Albania 41 41

Syria 263 -263

Oman 60 60

Bahrain -163 448 611

Guinea 63 63

Jordan -5 158 163

Bangladesh 179 179

Maldives 12 12

Sudan 371 371

Kuwait -283 72 355

OIC TOTAL -1194 3783 4977

WORLD TOTAL -846897 911192 1758089

Share of the OIC countries in the world total 0.14 0.42

Source: Balance of Payments Statistics IMF, 2000

40

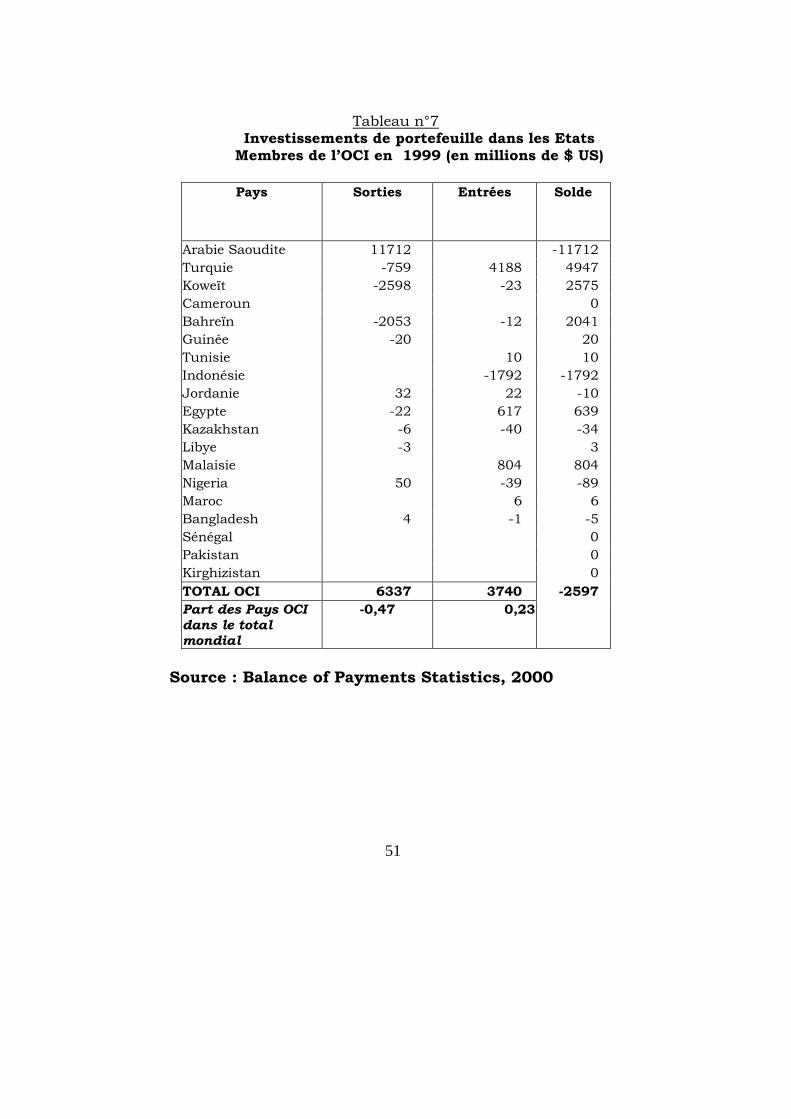

Table n° 7 Portfolio Investments in the OIC Member States in 1999 (in million US

dollars)

Country PI inflows PI outflows Balance Saudi Arabia 11712 11712

Turkey -759 4188 4947

Kuwait -2598 -23 2575

Cameroon 0

Bahrain -2053 -12 2041

Guinea -20 20

Tunisia 10 10

Indonesia -1792 -1792

Jordan 32 22 -10

Egypt -22 617 639

Kazakhstan -6 -40 -34

Libya -3 3

Malaysia 804 804

Nigeria 50 -39 -89

Morocco 6 6

Bangladesh 4 -1 -5

TOTAL OCI 6337 3740 -2597 The OIC share in the world total

-0,47 0,23

Source: Balance of Payments Statistics IMF, 2000

41

FOURTH PART:

THE TEACHINGS OF THE PILOT EXPERIENCES IN THE OIC MEMBER STATES AND IN THE OTHER DEVELOPING COUNTRIES IN THE FIELD OF

PROMOTION, PARTNERSHIP AND INVESTMENT40

Promoting SMEs clustering and networking means stimulating competition and cooperation among firms, creating specific locational advantages, an supporting businesses to make the best of a highly competitive environment ultimately, transforming small individual firms into integrated systems of firms. Some conclusions can be distilled from the examples of best practices: 1. In general, the target should not be a single enterprise, but a network of enterprises. Providing “collective” services has two main advantages: (i) it has lower transaction costs than assistance to individual enterprises; (ii) it helps generate relationships between enterprises, improving their efficiency and maximizing the potential of the group through the development of mutual learning. Given that competitiveness is not a static goal, but consists in the ability to attain and sustain a market position, firms should be stimulated to achieve continuous improvement through self-help and become less dependent on external

40 These information were drawn from the UNCTAD's report which are based on

case studies : 11 cases for the 1st report and 26 cases for the second, of which six OIC Member States (Burkina Faso, Indonesia, Malaysia, Nigeria, Pakistan, Uganda).

- "La promotion et soutien des groupements et réseaux de PME pour le développement", thematic document prepared by the UNCTAD's secretariat TD/B/COM.3/EM.5/26 june 1998.

- "Amélioration de la compétitivité des PME par l'établissement de liens", basic document established by the UNCTAD's secretariat, submitted to the expert meeting on the relationships between the SMEs and transnational companies with a view to promoting the SME's companies. TD/LB/COM.3/EM.11/27 September 2000.

42

support, thus developing a “cumulative” capacity to upgrade. In addition, interventions should be demand driven (“customer oriented”) and not wholly focused on supplying a set of generic services (i.e. training, credit, raw materials and technology). In particular, the formation of networks should be driven by the idea of serving a specific market, and clusters should be stimulated to conquer niche markets and compete on the basis of quality, design, speed of innovation and speed of response to customers’ changing needs. Product innovation should be guided continuously by feedback from their customers. There are many examples demonstrating how the sharing of credits and orders, advanced machines, taking common laboratory tests and quality control certification processes, or participating jointly in training courses, awareness-building workshops (on subjects such as quality, flexibility or efficiency), or trade fairs can stimulate the initial processes of inter-firm dialogue and begin the construction of a relationship of trust and reciprocity among entrepreneurs. 2. Clear priority should be given to the direct provision of innovative, value-adding services. This is based on the assumption that small firms are unlikely to pay for services that address needs, which are still latent, or where the pay-off is in the medium term. In principal, support to SMEs should be provided by the private sector. The public sector should intervene in the case of an initially unfavourable cost/benefit ratio or in cases of 'free riders' (where public goods are concerned). In any event, mechanisms and structures should be conceived in a business-like manner. 3. Increasing concerns about the cost and impact of the interventions are promoting an examination of BDS (business

43