Embed Size (px)

Citation preview

Private Capital Flows to Developing Countriesand Their Determination: Historical Perspectives,Recent Experience, and Future Prospects

SWP484World Bank Staff Working Paper No. 484

August 1981

Prepared by: Alexander Fleming , jFinancial Policy and Analysis Department g <

Financial Staff 1 U 0 , ;

Copyright ® 1981The World Bank REMOVE1818 H Street, N.W. E MWashington, D.C. 20433, U.S.A.

PUB views and interpretations in this document are those of the authorHG should not be attributed to the World Bank, to its affiliated3881.5 lnizations, or to any individual acting in their behalf. 0 044 -01 0223.W57W67 Feathery Jaffies K.no.484 N 554

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

The views and interpretations in this document are those of the author andshould not be attributed to the World Bank, to its affiliated organi-

zations, or to any individual acting on their behalf.

WORLD BANK

Staff Working Paper No. 484

August 1981

PRIVATE CAPITAL FLOWS TO DEVELOPING COUNTRIESAND THEIR DETERMINATION:. HISTORICAL PERSPECTIVE,

RECENT EXPERIENCE, AND FUTURE PROSPECTS

A Background Study for World Development Report 1981

From an analysis of borrowing experience by oil-importing developing coun-tries (OIDC's), it is concluded that in recent literature on private capi-tal flows too much emphasis has been placed on the constraints on bankingintermediaries. The key determinant of flows through banking markets is

the macroeconomic environment (the orientation of global current accountbalances, the state of domestic loan demands in the industrialized coun-tries, etc.) that influences the supply of funds to the banks. The banksthemselves are strongly motivated to intermediate internationally by adesire to diversify their portfolios and by the profitability of inter-national business broadly defined. Constraints do impinge on particular

banks and particular borrowers at certain junctures, but for the market asa whole these constraints will not be severe as long as there are groups ofbanks--the Middle East banks are a current example--with an abundence of

capital and an undiversified portfolio that are willing to establish a mar-ket presence. Prospects for greater access of the OIDC's to the fixed-rateinternational bond markets will remain bleak so long as high and variable

interest rates persist and the public sectors in the industrialized coun-tries continue to preempt large volumes of fixed-rate funds.

Prepared by: Alexander E. FlemingFinancial Policy and Analysis DepartmentFinancial Staff

Copyright © 1981The World Bank1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

ii

Contents

Page

I. Introduction.1

II. Historical Perspective.3

The 1960s and Early 197s.31973-78: Adjusting to the First Oil Price

Shock.31979 and After: Adjusting to the Second Oil

Price Shock .................................... 5The Evolving Pattern of Financing ................ 7Borrowing in the International Capital Markets... 8

III. The Determination of Flows through the InternationalCapital Makets ........................................ 12

Some Preliminary Questions ....................... 12The Supply of Funds to Banking Markets ........... 13The Demand for Banking Funds ..................... 16The Role of International Banking Intermediaries. 18Conditions in the External Bond Markets .......... 20

IV. Recent Experience and Future Prospects .................. 21

The Macroeconomic Environment, Current andProspective .................................... 21

An Analysis of Recent Bank Lending to theOil-Importing Developing Countries (OIDC's) .... 23

The Impact of Banking Constraints ................ 30Prospects for International Banking Flows ........ 33Prospects for the External Bond Markets .......... 35

Additional References ................................... 37

iii

Tables

Page

1. Global Current Account Balances, 1970-78 .............. 3

2. Medium- and Long-Term External Debt, Outstanding andDisbursed, 1970-80. 6

3. Oil-Importing Developing Countries' Current AccountDeficit and Finance Sources, 1970-80 ................ 7

4. Gross Borrowing in the Medium-Term Eurocurrency CreditMarket by Developing Countries, 1973-81 (lst Half).. 9

5. Terms on Syndicated Eurocredits, 1976-81 (lst Half) ... 10

6. Outstanding International Bank Lending,1976-81 (March) .11

7. Foreign and International Bond Issues, 1973-81(lst Half) .......................................... 12

8. Global Current Account Balances, 1978-80, 1985, 1990.. 22

9. OIDC Current Accounts Volume of Syndicated Lending andLoan Spreads, 1976-81 .24

Charts

Charts 1-5: Supply and Demand for Syndicated Loans to OIDC's,1977 through 1981:

Chart 1: 1977 .. 25

Chart 2: 1978 .. 26

Chart 3: 1979 .. 26

Chart 4: 1980 .. 28

Chart 5: 1981 .. 29

iv

Acronyms and Abbreviations

BIS Bank for International Settlements

CMS Capital Market System (of the World Bank)

CSOEC Capital-surplus oil-exporting country

IMF International Monetary Fund

LIBOR London inter-bank offered rate

ODA Official development assistance

OECD Organisation for Economic Co-operation and Development

OEDC Oil-exporting developing country

OIDC Oil-importing developing country

I. Introduction

This paper examines the recent evolution of private capital flows

to developing countries and seeks to identify those factors which are

likely to be most potent in influencing their size and make-up in the early

1980s. The focus of attention will be almost entirely on the

quantitatively most important flows, specifically those through the

international capital markets to the middle- and low-income oil-importing

developing countries (OIDC's). 1/

The paper will seek to shed light in particular on borrowing

experience by the OIDC's, for it has been argued by some economists,

bankers, and market commentators that the flow of funds through private

markets to these countries might be slowing down--and this at a time when

the OIDC's are having to cope with increasing current account deficits that

require financing. In this scenario of constrained private capital flows,

the strain can be taken in the short term by a run-down in reserve levels.

If, however, no alternative forms of financing are forthcoming, this would

imply a need for domestic policy adjustment and a slowing in the tempo of

economic development.

There is one feature of the methodology of this paper that merits

attention. The most significant development in the world economy over the

last decade has been the increasing interdependence of its component

economies. Increasing trade linkages have brought with them greater

interdependence of real activity both between and within the industrialized

and developing economies. Of particular relevance to this paper, however,

is the increasing financial interdependence in the world economy brought

1/ Developing countries comprise the middle- and low-income OIDC's to-gether with the oil-exporting developing countries (OEDC's). TheMiddle Eastern oil-exporting countries which run large current accountsurpluses are defined as capital-surplus oil-exporting countries(CSOEC' s).

-2-

about by the growth of the international banking and bond markets. The

removal of barriers to capital flows into and out of the industrial

economies has also meant increasing interdependence of financial conditions

within the industrialized economies and in the international markets. The

implication of this observation for the present paper is that the ability

of the developing countries to raise funds in the international markets

will largely depend on conditions in the industrialized countries. The

determination of economic and financial conditions in this latter group of

countries must accordingly be the subject of analysis.

1I. Historical Perspective

The 1960s and Early 1970s

The pattern of developing country financing that existed prior to

1974 was markedly different from that which has since ensued. Foreign

capital financed between 10% and 20% of total investment in ¶these

countries. The bulk of foreign capital took the form of official flows;

that is, grants and loans from official bodies on concessional or market

terms. In 1969, the first year for which comprehensive debt data are

available, 55% of the outstanding debt of developing countries was from

official sources. Of the remainder, the bulk is believed to have been in

the form of officially guaranteed suppliers' credits. The rest took the

form of direct foreign investments.

Two changes began to take place towards the end of the 1960s.

First, private Western banks began to see the benefits of overseas lending

and started to increase their external exposure to, among others, the

developing countries. The banks were strongly motivated to diversify the

risks in their portfolios toward high-yielding overseas loans. Second,

- 3 -

workers' remittances 1/ came to assume an increasing importance for

developing countries as a source of finance, particularly those countries

in Southern Europe and North Africa. This development reflected the

growing mobility of workers from within these two regions.

1973-78: Adjusting to the First Oil Price Shock

A change in pattern of developing country financing had begun to

take place at the end of the 1960s, but in many respects 1973 marked a

distinct turning point. In that year the major oil-producing countries,

after a long period during which they had seen the real price of their main

export fall, took steps to raise the relative price of their oil. The

price adjustment took the form of an abrupt and unexpected price increase

a quadrupling over the 1973-74 period.

The price rise brought about a distinct increase in the size of the

current account surpluses run by the oil-producing countries that had as

its counterpart rises in the deficits (or falls in surpluses) of the

industrialized countries and the oil-importing countries. (See Table 1.)

Table 1: Global current account balances 1970-78(billions of current U.S. dollars)

Regicn.s 1970 1971 1972 1973 1574 1975 1976 :977 :976

OIDC'. -8.6 -10.7 -5.3 -7.3 -33.1 -38.6 -26.1 -22.9 -25.5of vhicrb:

Lo.--ncooe Countries -1.7 -2.5 -1.5 -3. -6.0 -5.4 -2.4 -1.6 -5.1Middle-lncomc Councries -7.0 -d.2 -3.8 -4.2 -27.1 -33.2 -24.4 -21.3 -20.4

OEiC's -2.2 -2.9 -3.6 -2.6 -19.3 -2.5 -0.3 -5.5 -17.6

All Developin, Co011tries a/ -10.9 -13.6 -8.9 -9.9 -13.8 -4:.1 -27.1 -28.5 -43.1

CSOEC-6 2.6 n.a. 1.9 6.7 43.3 30.5 36.3 32.9 18.8

1ndu6cri2ltizcd Coc:3treIe 12.1 15.5 16.0 18.9 -8.5 20.0 3.9 -1.5 29.9

a, OICC- and 0EC's.n.N .So. avallabl .

F,te: lgureG exclude official trLnsEfts.

1/ Gurushri Swamy, International Migrant Workers' Remittances: Issues andProspects, World Bank Staff Working Paper No. 481 (Washington, D.C.,August 1981).

- 4 -

As well as adjusting to the rise in energy prices, the OIDC's had

to contend with the impact of an associated recession in the industrialzed

countries. The consequent fall-off in OIDC exports exacerbated their

payment situations. After the sharp deterioration in current account

positions in 1974, which continued into 1975, there was an improvement that

resulted from a leveling out of the oil price in nominal terms. In real

terms oil prices fell as the decade progressed.

The improvement also reflected a degree of domestic policy

adjustment in the OIDC's. Experience with adjustment was not uniform

across developing countries. Some middle-income OIDC's (in particular the

newly industrialized countries) that had ready access to the fast-growing

international capital markets were able to quicken their export growth or

import substitution strategies. 1/ The growth rates of the middle-income

countries held up remarkably well--an annual GDP growth rate of 5.6% in the

1970s compared with one of 6.2% in the 1960s--given the size of their

current account deterioration in 1974-75. This may be explained in part by

the fact that the oil price rise was construed by many of these countries

as a one-time occurrence. Accordingly, there was a strong incentive to

finance the increased current account burden rather than to undertake swift

economic policy adjustment that would have been very wasteful in economic

resources.

Those low-income OIDC's not benefiting from good harvests and with

only limited access to commercial financing were, in contrast, forced to

cut their oil imports and attain little economic growth (3% in the 1970s

compared with 4.2% in the 1960s) and probably zero growth in per capita

terms.

1/ For further discussion of adjustment in individual countries, see WorldBank, World Development Report 1981 (New York: Oxford University Press,August 1981), chapter 6, and other papers in this series.

- 5 -

1979 and After: Adjustment to the Second Oil Price Shock

As forementioned, the fall in the real price of oil through the

mid-1970s wiped out much of the price adjustment that had taken place in

1973-74. In many respects the world had returned to its pre-1973 position,

with CSOEC's accumulating only small current account surpluses and the

surpluses of the industrialized countries mirrored by deficits in the

developing countries (see Table 1). In 1979 the CSOEC's took further steps

to readjust the oil price. As a result, the price effectively doubled over

the 1979-80 period.

The 1979-80 oil shock accompanied a deeper world recession with

worse unemployment levels, more unused capacity, and higher inflation and

interest rates in the industrialized countries than occured after the shock

of 1973-74. The deflationary policies adopted by many industrialized

countries following the recent shock - particularly the strong predilection

in favor of monetary policy - have compounded the problems facing the

OIDC's. The resulting fall in activity in the industrialized countries -

quantitatively the most important factor - adversly affected the exports of

the OIDC's. With respect to monetary policy, a tight control of the money

supply is seen in certain countries as a necessary (and in some cases

sufficient) condition for controlling inflation. This type of policy

requires for its imposition a willingness to allow short-term interest

rates to fluctuate almost without constraint. As much developing country

debt has been contracted on a floating-rate basis in dollars, 1/ the sharp

upward movements in U.S. short-term rates (which are closely related to

Eurodollar rates) will unfavorably affect the debt-servicing burden of the

developing countries.

1/ The thirty-three largest developing country borrowers held a totalvariable interest-rate debt of about US$180 billion, most of it denomi-nated in dollars. For each percentage point increase in the Eurodollarrate (normally the six-month rate) these thirty-three countries faceextra interest charges of $1.8 billion a year. For further coverage ofthis point, see N.C. Hope, Developments in and Prospects for the Exter-nal Debt of Developing Countries: 1970-80 and Beyond, Staff WorkingPaper No. 488 (Washington, D.C., August 1981).

- 6 -

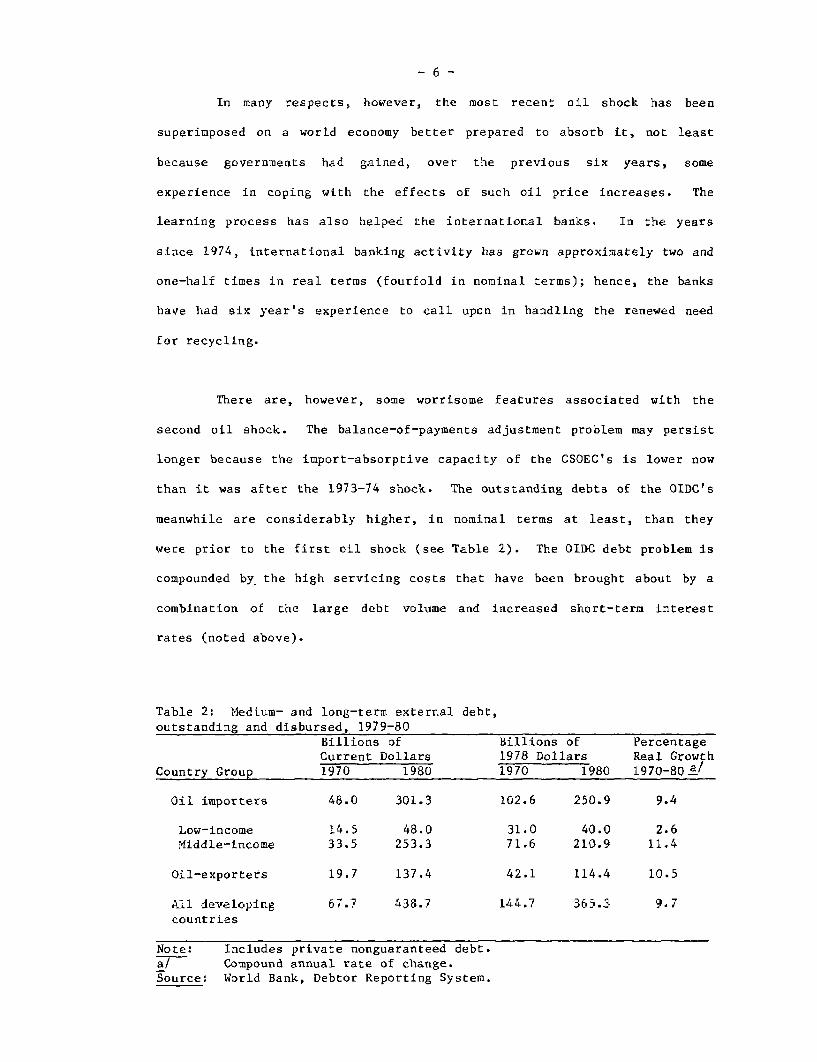

In many respects, however, the most recent oil shock has been

superimposed on a world economy better prepared to absorb it, not least

because governmeats had gained, over the previous six years, some

experience in coping with the effects of such oil price increases. The

learning process has also helped the international banks. In the years

since 1974, international banking activity has grown approximately two and

one-half times in real terms (fourfold in nominal terms); hence, the banks

have had six year's experience to call upon in handling the renewed need

for recycling.

There are, however, some worrisome features associated with the

second oil shock. The balance-of-payments adjustment problem may persist

longer because the import-absorptive capacity of the CSOEC's is lower now

than it was after the 1973-74 shock. The outstanding debts of the OIDC's

meanwhile are considerably higher, in nominal terms at least, than they

were prior to the first oil shock (see Table 2). The OIDC debt problem is

compounded by the high servicing costs that have been brought about by a

combination of the large debt volume and increased short-term interest

rates (noted above).

Table 2: Medium- and long-term external debt,outstanding and disbursed, 1979-80

Billions of Billions of PercentageCurrent Dollars 1978 Dollars Real Growth

Country Group 1970 1980 1970 1980 1970-80 a/

Oil importers 48.0 301.3 102.6 250.9 9.4

Low-income 14.5 48.0 31.0 40.0 2.6Middle-income 33.5 253.3 71.6 210.9 11.4

Oil-exporters 19.7 137.4 42.1 114.4 10.5

All developing 67.7 438.7 144.7 365.3 9.7countries

Note: Includes private nonguaranteed debt.a/ Compound annual rate of change.Source: World Bank, Debtor Reporting System.

-7-

The Evolving Pattern of Financing

The global economic developments that took place during the 1970s

have had direct implications for the nature and volume of financing that

the developing countries have received. The financing of the middle-income

OIDC's has exhibited the most dramatic changes (see Table 3).

Table 3: Oil-importing developing countries' current accountdeficit and finance sources, 1970-80(billions of 1978 dollars)

..o'.-tflnce Middle-incomeIten 19017WT15 i978 :3 190 !937 1975 197ST1990

Current account dEificit a/ 3.6 4.9 7.0 5.1 9.1 14.9 6.7 42.8 20.4 46.9

Financed by

Nat capital flows:ODA 3.4 4.1 6.6 5.1 5.7 3.3 5.3 5.3 6.5 7.9

PrivIte lcect investrent 0.3 0.2 0.4 0.2 C.2 3.4 5.1 3.8 4.6 4.5

L cial .1cls 0.5 0.6 0.8 0.9 0.7 8.9 13.7 21.0 2;.4 27.1

Chanbces in rLs.rve. andsh,rt-term ocrrow,.:,gs b/ -0.5 -1.1 -0.7 -1.1 2.4 -0.8 -11.7 12.7 -20.1 9.5

Memorandun item:

Current Account deficits pcrce>Cage of CNP 1.9 2.4 3.9 2.6 4.5 2.6 1.0 5.5 2.3 5.0

a/ Excljdes net official transfers (grants), shich are included in capitol flows.

b/ A minus aign (-) indicates an increase in reserves.

SoLrce: Wiarld Bank, Economic A:acly.is and Projections Depar;ment.

Although concessional official development assistance (ODA) and

direct private investment grew little over the decade, workers' remittances

played an increasingly important financing role. 1/

1/ Although workers' remittances are conventionally classified as current

receipts and not as a financing item in the balance of payments

accounts.

- 8 -

Perhaps the most remarkable development, however, was the vast

growth in lending by international banks. As much of the surplus of the

CSOEC's had been placed either directly or indirectly with the

international banks, these institutions acted as intermediaries for the

recycling of funds, although many doubts were expressed at the time as to

whether they could cope with such large volume of funds.

For the low-income OIDC's, the pattern of financing has changed

relatively little over the decade. They have had to rely primarily on

ODA. This form of finance reached its peak in 1975 as the industrialized

countries responded to the heavy financing requirements of the low-income

countries. Since then ODA has grown very slowly. The only form of

financing that has exhibited substantial growth over the 1970s is workers'

remittances. Remittances grew to reach 33% of net financial flows to the

low-income OIDC's in 1978.

Borrowing in the International Capital Markets

It has been shown that borrowing through the international capital

markets has become the most important source of financing for the

developing countries, particularly for the middle-income OIDC's. Before

attempting to analyze the reasons for the growth in borrowing, it is

necessary to examine in more depth the nature of the borrowing over the

last decade. To place developing country borrowing in proper perspective,

three sets of data must be examined: (1) gross borrowing commitments in

the syndicated medium-term Eurocurrency credit market and the terms

attached to such loans, (2) net international bank lending, and (3) the

issuance of foreign and international bonds. For (1) and (3), the source

of data is the World Bank's Capital Markets System (CMS); for (2), the Bank

for International Settlements (BIS).

- 9 -

Table 4 shows that total gross borrowing in the syndicated loan market by

developing countries has grown substantially over the last decade.

Table 4: Gross borrowing in the medium-term eurocurrency creditmarket by developing countries, 1973-81 (1st Half)(US$ billions)

lSoO !951Regiols 1973 1974 1975 1976 1977 1978 1979 Ist ;!G 2c Ha,lf 1st iaiaE

All uor.o.ing Countries 2C.8 28.5 20.6 28.7 34.2 71.7 70.2 29.0 41.4 32.8

Developtno1 Counctres 8.6 10.4 13.0 18.1 20.1 38.2 43.2 16.7 21.5 19.2

(' of co::1) (41) (37) (63) (63) (59) (52) (62) (58) (50) (59)

Of C IcH:OIP.C's 4.4 7.7 7.1 11.8 10.4 19.6 26.5 1'.7 '3.4 14.0

(X of toLt1) (21) (27) (35) (4.1) (31) (27) (,3) (40) (22) (43)

Or.CT s 4.2 2.7 5.9 o.3 9.7 18.6 17.2 5.0 7.1 5.2

(.: cf totol) (20) (9) (29) (22) (28) x25) (25) (17) (17) (16)

Source: World BUnk, CMS.

In terms of nominal volume of OIDC borrowing there was a pause in

1977 and in the first half of 1980. It was the most recent pause that some

market observers took as an indication that an adverse change in bank

sentiment toward OIDC's might have begun. In the event, rising spreads

appear to have encouraged further bank lending, and loan volume picked up

substantially. In the first half of 1981 the share of OIDC borrowing in

total borrowing had reached a high 43%.

Developing countries' access to the syndicated lending market was

encouraged by a number of factors. The large volumes of funds that could

be mobilized in one operation were attractive to developing countries, as

were such attributes as the speed with which credits could be arranged,

flexibility in their use, etc. Whereas borrowing from the International

Monetary Fund (IMF), for instance, entailed a degree of policy

conditionality, market borrowing did not. This became a potent argument in

favor of the latter at certain junctures.

- 10 -

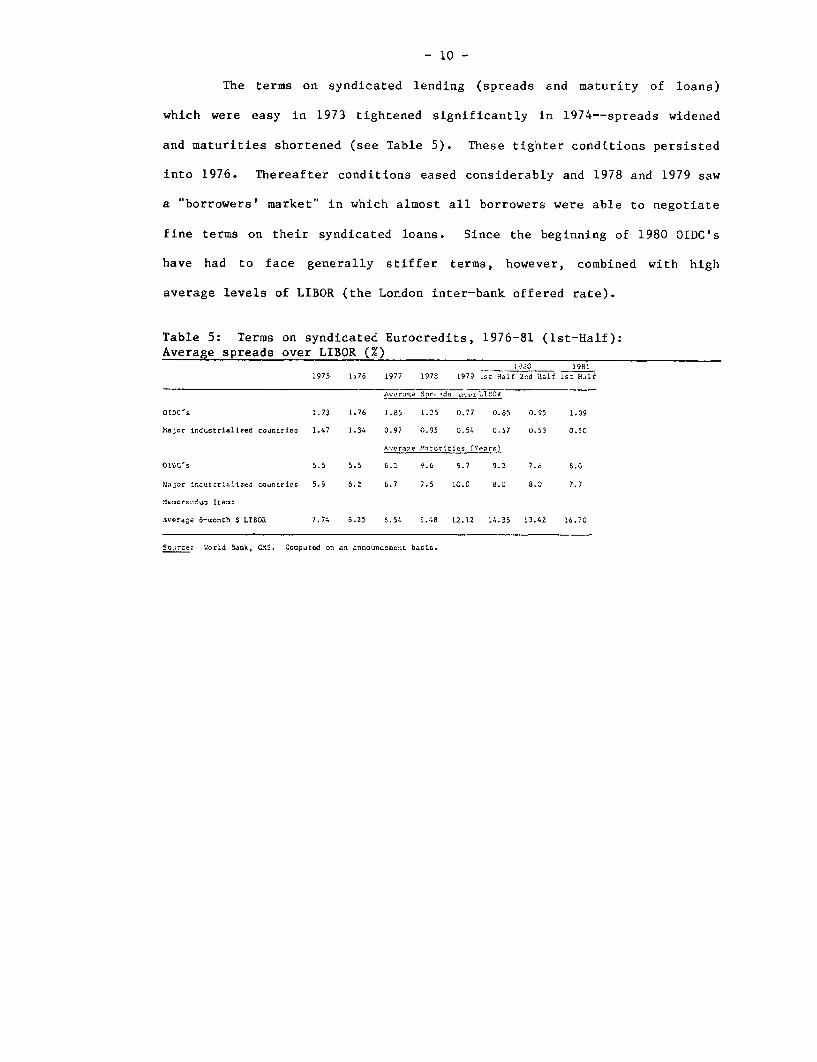

The terms on syndicated lending (spreads and maturity of loans)

which were easy in 1973 tightened significantly in 1974--spreads widened

and maturities shortened (see Table 5). These tighter conditions persisted

into 1976. Thereafter conditions eased considerably and 1978 and 1979 saw

a "borrowers' market" in which almost all borrowers were able to negotiate

fine terms on their syndicated loans. Since the beginning of 1980 OIDC's

have had to face generally stiffer terms, however, combined with high

average levels of LIBOR (the London inter-bank offered rate).

Table 5: Terms on syndicated Eurocredits, 1976-81 (1st-Half):Average spreads over LIBOR (%)

1I.3 19811975 1.76 1977 1978 1979 isr Half 26.d DilE is: Half

A-erae. S: zds d ys- 41I0R

OIDC's 1.73 1.76 1.85 1.25 0.77 0.85 0.95 1.09

iaAer industrialised courtries 1.47 1.34 0.97 0.95 0.54 0.07 0.53 0.50

Average Maturities (rears)

01lC's 5.5 5.5 6.2 9.6 9.7 9.2 7.d 8.0

ulactr indescrlaltzed countries 5.9 6.2 6.7 7.5 10.0 8.C 8.0 7.7

M-oraerdu, Itcem:

Average 6-month $ LIBOR 7.74 6.25 6.54 5.48 12.12 14.35 13.42 16.70

Soarce: World Bank, 01S. Coeputed on an aneouncement basis.

- 11 -

BIS banking data may be distinguished from the syndicated loan data

in that they cover the actual outstanding international lending activity

(including syndicated, non-syndicated, and short-term lending) of all banks

reporting to that institution. 1/ BIS data are thus a broader measure of

international banking flows. Using this measure it can be seen from Table

6 that outstanding lending to the OIDC's has increased two and one-half

times since the end of 1976. It is also notable that the share of OIDC

lending in total international bank lending has increased since the end of

1979. Furthermore, in the post-1979 period such lending has continued to

grow at annual rates in excess of 20%.

Table 6: Outstanding international bank lending, 1976-81 (March)(End-period data; US$ billions)

1 1980 1981

1976 1977 1978 1979 I End-June End-Dec. End-Mar.

All BorrowingCountries 547.6 657.1 893.1 1110.7 I 1205.7 1321.9 1346.6

OIDCBorrowers 143.5 174.7 237.1 296.2 327.7 364.7 384.8(% of total) (26) (27) (27) (27) (27) (28) (29)

Source: BIS. Note data is "net" of loan repayments.

The external bond markets have not been a major source of finance

to OIDC's. Indeed, as Table 7 shows, only in the period 1977-79--good

years generally for bond financing--did the OIDC's secure significant

volumes of funds. Floating-rate notes (effectively, bonds with an

adjustable coupon) have come to assume increasing importance, as have

certain other innovating fund-raising techniques (convertible issues and

warrant issues, for instance). However, it has been mainly the

sophisticated borrowers from the industrialized economies that have

benefited from these innovations.

1/ See BIS quarterly press release for details of coverage of data.

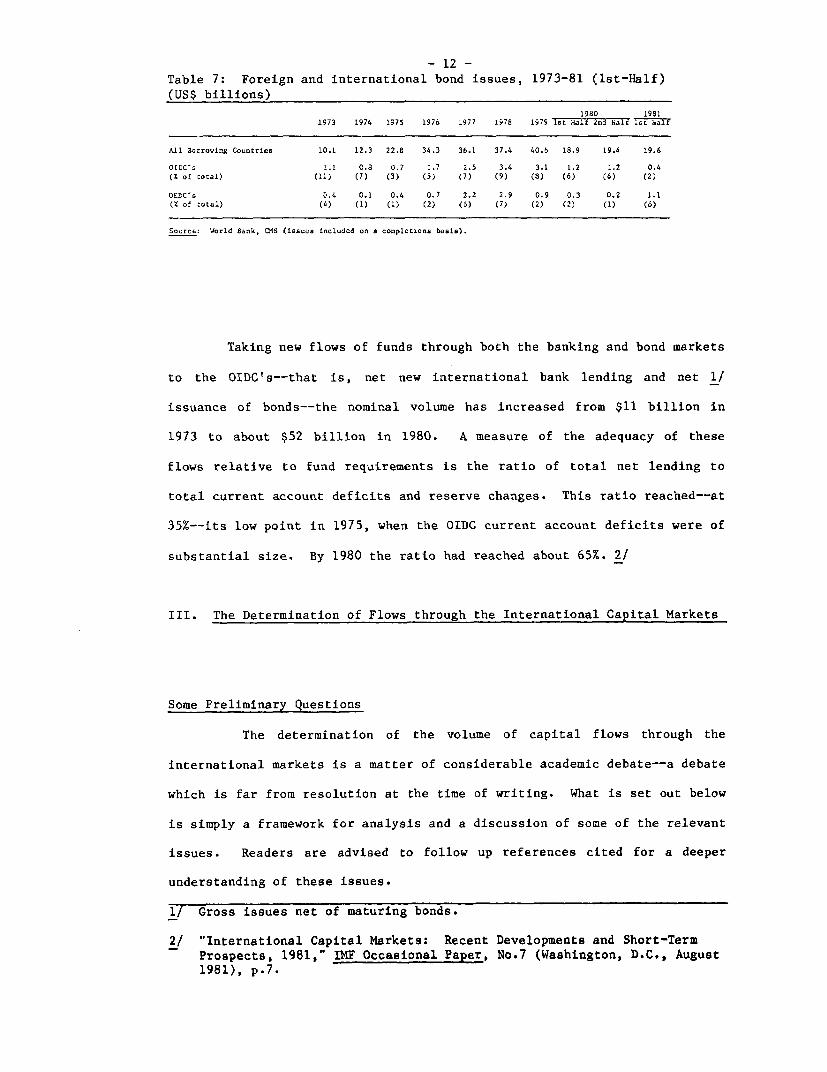

- 12 -Table 7: Foreign and international bond issues, 1973-81 (lst-Half)(US$ billions)

1980 19811973 1974 1975 1976 1977 1978 1979 lot Halj 2nd hiali lst haf

All Borro.ing Countries 10.1 12.3 22.8 34.3 36.1 37.4 40.6 18.9 19.4 19.6

OIDC's 1.1 0.8 0.7 1.7 2.5 3.4 3.1 1.2 1.2 0.4(Z of cotal) (11) (7) (3) (5) (7) (9) (8) (6) (6) (2)

OEDC's 0.4 0.1 0.4 0.7 2.2 2.9 0.9 0.3 0.2 1.1(X of total) (4) (1) (1) (2) (6) (7) (2) (2) (1) (6)

Source: 'World Bank, A1S (issues included on a completions basis).

Taking new flows of funds through both the banking and bond markets

to the OIDC's--that is, net new international bank lending and net 1/

issuance of bonds--the nominal volume has increased from $11 billion in

1973 to about $52 billion in 1980. A measure of the adequacy of these

flows relative to fund requirements is the ratio of total net lending to

total current account deficits and reserve changes. This ratio reached--at

35%--its low point in 1975, when the OIDC current account deficits were of

substantial size. By 1980 the ratio had reached about 65%. 2/

III. The Determination of Flows through the International Capital Markets

Some Preliminary Questions

The determination of the volume of capital flows through the

international markets is a matter of considerable academic debate--a debate

which is far from resolution at the time of writing. What is set out below

is simply a framework for analysis and a discussion of some of the relevant

issues. Readers are advised to follow up references cited for a deeper

understanding of these issues.

1/ Gross issues net of maturing bonds.

2/ "International Capital Markets: Recent Developments and Short-TermProspects, 1981," IMF Occasional Paper, No.7 (Washington, D.C., August1981), p.7.

- 13 -

The volume of funds flowing through the international capital

markets is the result of three factors: the primary supply of funds to the

markets, the demand for market funds, and the willingness of private

institutions to act as intermediaries in the process. As far as the supply

of funds to the market is concerned, it is important to ask what real

economic conditions in the world economy and what financial conditions

within the major industrial countries create the conditions for a flow of

funds to the external markets.

Furthermore, since the developing countries are imporant borrowers

in the international markets, the question of which factors determine

private capital flows to them can be subsumed initially in the question of

which factors determine market conditions in general.

In what follows, the banking markets will be considered separately

(in the next three sections) from the bond markets, although there is clear

substitutability between the suppliers of funds to each market.

Substitutability also exists on the borrowers' side of the markets.

The Supply of Funds to the Banking Markets

In the 1970s one of the main determinants of the volume of net

capital flows has been the size and distribution of worldwide current

account surpluses and deficits. The larger the absolute size of ex-ante 1/

surpluses and deficits, the larger the volume of the flows that might be

expected to take place through the international banking markets. Accord-

1/ Ex post the resulting levels of surpluses and deficits will tend to besmaller. Their size depends largely on the degree of economic activityin the surplus countries and the chosen balance between adjustment andfinancing in the deficit countries.

- 14 -

ing to this view, the large surpluses accumulated by the CSOEC's in the

wake of the two oil shocks would tend to be placed in the international

banking markets, thereby increasing market liquidity and encouraging

lending to those countries - in particular the OIDC's - which carry the

counterpart current account deficits. One of the reasons why the

"recycling" process took place so smoothly after the first oil shock was

that much of the surplus of the CSOEC's was placed directly with the

international banks. These banks, in turn, were prepared to carry both the

resulting maturity transformation risk - the CSOEC's typically placed their

funds at short-term while lending demand was for longer-term money - and

the country risk attached to loans.

One of the intriguing questions raised in the context of the

present round of recycling is the implications for the nature (and cost) of

capital flows to the OIDC's of greater placements by the surplus countries

outside the international banking system. Wherever such funds are placed,

however, it is clear that much, will eventually find its way back into the

international banking markets through a chain of interest-rate-induced

financial substitution and eventual switching (or arbitraging) by the

Eurobanks.

As far as the world current account configuration is concerned, the

U.S. current account position may be of particular significance. A U.S.

deficit, rather than absorbing funds from international markets, actually

provides funds as the dollar is voluntarily held as a reserve currency.

The unique role of the U.S. dollar, it has been argued, 1/ adds an

assymetry to the system which is perhaps important in influencing

conditions in international markets. A more potent argument, however, is

that Euromarket conditions are influenced not by the U.S. deficit per se,

1/ K. Inoue, "Determinants of Market Conditions in the EurocurrencyMarket - Why a Borrowers Market?" BIS Working Paper No. 1 (April 1980).

- 15 -

but by central bank intervention to support the dollar. The dollar pro-

ceeds of the intervention tend to find their way back into the Euromarket.

These theories offer an explanation of why banking flows were strong to the

OIDC's in those years - 1977, and 1978 - when the CSOEC surplus was fall-

ing.

A further factor influencing the volume of flows through the inter-

national capital markets is the level of activity in industrial economies,

although this is slightly ambiguous in its effect. Higher economic activ-

ity within the industrial economies may encourage increased exports from

the developing economies and by so doing improve the creditworthiness of

these countries. This might encourage flows from the international capital

markets. Such flows might also take place - and this is perhaps a more

potent argument - when activity in the industrialized countries is low.

Low economic activity will have as its counterpart a low level of domestic

loan demand from the banks. If this coincides with periods when there is a

high degree of liquidity in domestic banking markets, then banks may seek

alternative portfolio outlets for their surplus funds by lending intern-

ationally. The upturn in international bank lending after the first oil

shock can be attributed in part to this cause.

It might be expected, ceteris paribus, that easy monetary con-

ditions 1/ in the major industrialized economies will spill over into the

Euromarkets, causing easy conditions there which would be conducive to

larger banking flows to the developing countries. Paradoxically, however,

in those countries which have non-interest-bearing reserve requirements on

bank liabilities (notably the United States), tighter monetary conditions

1/ The question of liquidity creation in the Eurocurrency market is dealtwith very comprehensively by H. Mayer in "Credit and Liquidity Creationin the International Banking Sector," BIS Working Paper No. 1 (November1979).

- 16 -

(implying high nominal interest rates) can encourage banks to book deposits

through offshore subsidiaries and thereby foster external intermediation.

The net effect of domestic monetary conditions in the industrialized econo-

mies on the flow of funds to the Euromarkets will ultimately, however,

depend (as discussed above) upon the state of domestic loan demand.

U.S. monetary policy has a clear and direct impact on the cost of

borrowing in the Euromarkets, for the Eurocurrency reference rate - LIBOR -

closely follows movements in U.S. domestic money-market rates due to the

arbitrage activities of the major international banks.l/ The best indi-

cator of conditions in the longer-term segment of the Eurocurrency market -

the syndicated loan market - are contractual loan spreads and not LIBOR it-

self. In fact, historically the average level of spreads and LIBOR appear

to have moved inversely. 2/

The Demand for Banking Funds

A wide range of countries - industrialized, centrally planned,

capital-surplus oil-exporting, as well as developing - tap the inter-

national banking markets for funds. The industrialized countries - the

main fund raisers - tend to borrow in these markets to the extent that they

are unable to attract to their own relatively sophisticated financial mar-

kets requisite volumes of funds to finance their payments imbalances.

1/ R.B. Johnston, "Some Aspects of the Determination of EurocurrencyInterest Rates," Bank of England Quarterly Bulletin (March 1979).

2/ For a more thorough discussion of this issue and the determination ofmarket conditiong,; see A.E. Fleming and S.K. Howson, "Conditions in theSyndicated Medium-Term Euro-credit Market," Bank of England QuarterlyBulletin (Sept. 1980), and Laurie S. Goodman, "The Pricing ofSyndicated Eurocurrency Credits," Federal Reserve Bank of New YorkQuarterly Review, Vol. 5, No. 2.

- 17 -

Industrial, commercial and financial entities within these coun-

tries also tap the markets from time to time to supplement their domestic

funding sources. Furthermore, in the event of a tightening of conditions

in the international banking markets, heavy demands on the part of the

industrialized countries will tend to crowd out other borrowers, partic-

ularly developing country borrowers.

In the developing countries, much of the borrowing through private

markets that took place in the pre-1973 period was directly for development

purposes. The first oil shock in 1973-74, however, brought with it. a

demand for funds of a different order. In the first place, funding was

required to cover the increased costs of needed oil imports. Second, the

developing countries had to cover a shortfall in export earnings brought

about by the depth of the global recession which ensued. Third, the

borrowing itself had to be serviced while the higher inflation rates that

accompanied the shock brought higher nominal rates that exacerbated the

servicing burden (as noted in Section II).

If an individual developing country identifies a potential financ-

ing requirement, there are several factors that will determine when an

approach to the market will be made, and for how much this will be. 1/

The adequacy of the existing level of foreign currency reserves

will be an important determinant. Furthermore, even if the existing level

of reserves were sufficient to cover any projected financing requirements,

it might be rational for a developing country to take advantage of easy

Eurocurrency market conditions to borrow and bolster its resources (perhaps

temporarily reinvesting them in the Eurocurrency market) if it anticipates

a deterioration in conditions.

_/ Assuming that the country has already chosen an appropriate balance be-tween domestic policy adjustment and financing.

- 18 -

An important constraint on borrowing, however, will be the existing

and prospective level of debt outstanding combined with the likely extra

debt-servicing costs that will be involNed. In summary, each "market-

eligible 1/ developing country will have its own unique borrowing strategy

that will be formulated against the background of movements in the costs of

borrowing as well as the size of prospective borrowing requirements and

their outstanding level of debt.

The Role of International Banking Intermediaries

The international banks have not been passive intermediaries

between the suppliers and demanders of funds. They have, for instance,

been active in switching funds from domestic to international use when

domestic demand or returns have been low. What is more, there has been a

marked tendency during the 1970s for banks to seek to internationalize

their business. Aided by the relaxation of capital controls, banks have

been diversifying their portfolios by increasing their international lend-

ing at short-term and longer-term, denominating loans in their own and

other currencies, and lending through branches and subsidiaries in offshore

markets. The adjustment of bank portfolios in this direction has been

helped by innovations such as the development of the Eurocurrency inter-

bank market and the technique of syndication. The international markets

have broadened, deepened, and become more competitive - with the result

that the innovations themselves have encouraged faster growth. This

longer-run process of internationalizaticn was probab)ly under way well

before the first oil shock.

The high returns on offer in the international banking markets have

encouraged banks of different nationalities to enter these markets from

1/ Market-eligible developing countries-are primarily those in the middle-income group, although certain low-income countries (India is a recentexample) with low volumes of private debt outstanding have been able tosecure market access.

- 19 -

time to time. Conversely, as returns have fallen relative to those

available in domestic markets different nationality groups of banks have

dropped out of international lending. It is the inward and outward

mobility of banks in this market that makes it so distinctive. American

banks dominated the market in the 1960s and in the early to mid-1970s. The

international lending momentum was continued by the European banks and in

particular by the Japanese banks, which added a strong competitive fillip

to the market in 1972-73 and 1978-79 (although the Japanese Ministry of

Finance limited their market access at certain junctures). During the

1977-78 period when international bank lending as a whole was accelerating,

the market share of American banks began to fall sharply. This reflected

both the preponderance of new market entrants and the low levels of spreads

that many American banks found unattractive. More recently, there has been

a partial withdrawal from the market by German banks, whereas Middle East

banks 1/ have been increasing their presence substantially.

To summarize, the factors determining the market entry and exit of

banks are relative returns in domestic and international markets 2/ and,

closely associated with this motive, an underlying desire to expand

internationally to gain the benefits of portfolio diversification.

Government policy is also important whether it is imposed for banking

prudential purposes or for balance-of-payments reasons - that is, where the

banks' activities may undermine a country's external financial position.

1/ A.E. Fleming, "New Entrants in the Recycling Process: the Middle EastBanks" (World Bank; internal circulation only).

2/ See J.F. Sterling, Jr., "Competitive Advantage in Bank EurocurrencyLending,t' Ph.D. dissertation, Johns Hopkins University, 1980, and R.B.Johnston, "Banks' International Lending Decisions and the Determinationof Spreads on Syndicated Medium-term Eurocredits," Bank of EnglandDiscussion Paper No. 12 (Sept. 1980).

- 20 -

The allocation of bank lending between competing borrowers depends

upon the risk associated with the borrower relative to the return available

on the loan. Differing spreads between borrowers will tend to reflect

differences in the banks' perceived creditworthiness of them. 1/ Some

developing countries may be limited in the amount they can obtain from the

banks, which may operate rationing 2/ in the form of self-imposed credit

ceilings.

Conditions in the External Bond Markets

Conditions in the foreign and international bond markets are rather

more susceptible to world economic, and particularly financial, events than

are the Eurocredit markets. When conditions are not right for the launch-

ing of bond issues, an increase in international bank lending activity is

sometimes observed.

One of the key economic factors determining conditions in these

markets is the level of short-term interest rates relative to the yield on

bonds. 3/ When short-term rates exceed bond yields, there is a tendency for

bond issuance to fall off and even to dry up entirely. The reasoning

behind this is that as short-term interest rates rise non-bank bond inves-

tors have an incentive to place funds in banks rather than take up bonds.

Banks, meanwhile, also hold bonds, but as short-term rates rise it becomes

unprofitable to finance bond holdings through their now more expensive

deposit liabilities.

1/ For a survey of empirical work on the determination of risk premia, seeAngelini, Eng, and Lees, International Lending, Risk and the Euromar-kets (Macmillan, 1979), Ch. 4.

2/ See Isham Kapur, "The Supply of Eurocurrency Finance to DevelopingCountries," Finance and Development, Vol. 14, No. 2. (Sept. 1977).

3/ This is only true for fixed-coupon bonds. As noted early in Section IIbonds with floating rates - floating-rate notes - are assuming increas-ing importance in the market.

- 21 -

Market conditions are also determined to a large extent by the

financial authorities. At times when the country concerned is experiencing

a current account surplus and inflows of capital, the, authorities will

often liberalize foreign access to their bond markets to encourage an out-

flow. The converse is also true.

The access of developing countries to the external bond markets is

determined largely by their credit ratings. Bond investors typically tend

to wish to invest in good-quality paper and only invest in higher-risk

names if an appropriately high coupon is set on the issue. At certain

times developing countries will be crowded out of the bond markets by the

better-risk industrialized borrowers. It is also the case, however, that

when market conditions are coducive to bond issuance and industrialized

country borrowers take advantage of the availability of fixed-rate funds,

there is greater scope for the developing countries to secure banking

finance.

IV. Recent Experience and Future Prospects

The Macroeconomic Environment, Current and Prospective

The second major oil price rise fed through into the industrialized

and OIDC economies toward the end of 1979 and into 1980 and 1981. As shown

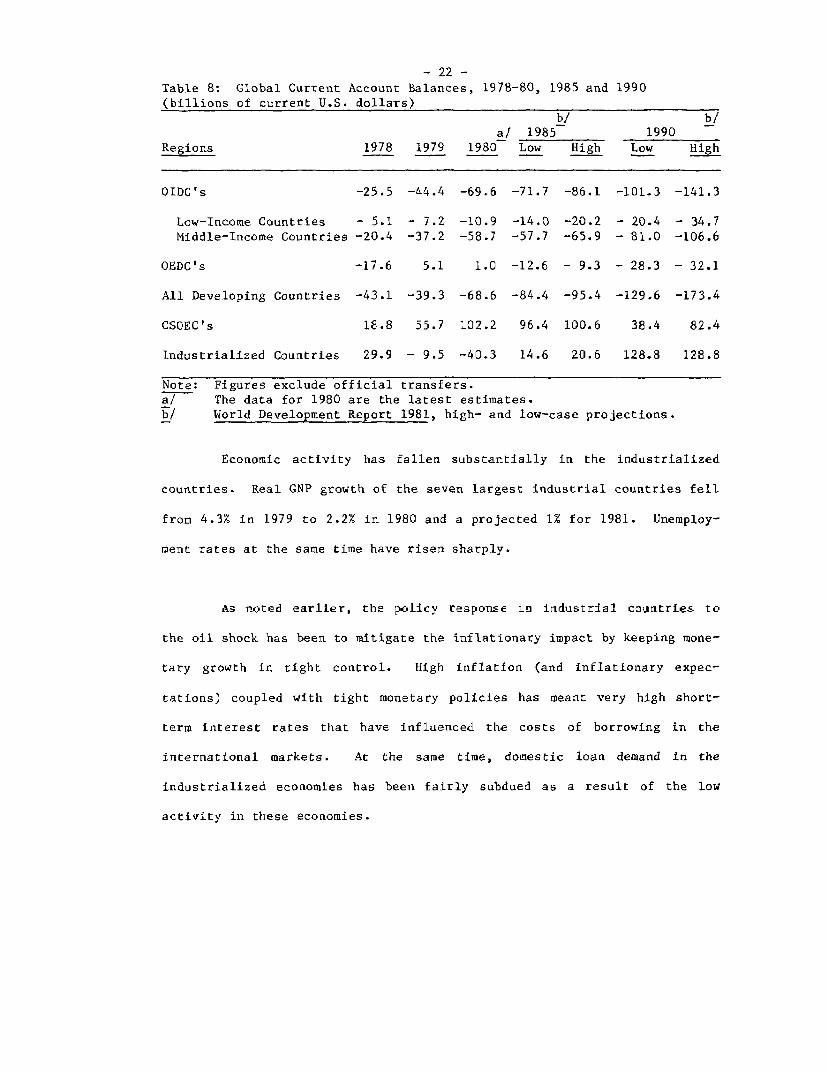

in Table 8, there was a notable swing from current account surpluses to

deficits for the industrialized economies and a widening deficit for the

OIDC's that reflected the sharp increase in the surplus of the CSOEC's.

The direct effect on the OIDC current account position of the oil price

rise was worsened by the indirect effect of slower economic activity in the

industrialized countries, which dampenend demand for OIDC exports. It is

noteworthy that the U.S. current account improved in 1979 and swung into

surplus in 1980, remaining there in 1981.

- 22 -Table 8: Global Current Account Balances, 1978-80, 1985 and 1990(billions of current U.S. dollars)

by b7a/ 1985 1990

Regions 1978 1979 1980 Low High Low High

OIDC's -25.5 -44.4 -69.6 -71.7 -86.1 -101.3 -141.3

Low-Income Countries - 5.1 - 7.2 -10.9 -14.0 -20.2 - 20.4 - 34.7Middle-Income Countries -20.4 -37.2 -58.7 -57.7 -65.9 - 81.0 -106.6

OEDC's -17.6 5.1 1.0 -12.6 - 9.3 - 28.3 - 32.1

All Developing Countries -43.1 -39.3 -68.6 -84.4 -95.4 -129.6 -173.4

CSOEC's 18.8 55.7 102.2 96.4 100.6 38.4 82.4

Industrialized Countries 29.9 - 9.5 -40.3 14.6 20.6 128.8 128.8

Note: Figures exclude official transfers.a! The data for 1980 are the latest estimates.bl World Development Report 1981, high- and low-case projections.

Economic activity has fallen substantially in the industrialized

countries. Real GNP growth of the seven largest industrial countries fell

from 4.3% in 1979 to 2.2% in 1980 and a projected 1% for 1981. Unemploy-

ment rates at the same time have risen sharply.

As noted earlier, the policy response in industrial contries to

the oil shock has been to mitigate the inflationary impact by keeping mone-

tary growth in tight control. High inflation (and inflationary expec-

tations) coupled with tight monetary policies has meant very high short-

term interest rates that have influenced the costs of borrowing in the

international markets. At the same time, domestic loan demand in the

industrialized economies has been fairly subdued as a result of the low

activity in these economies.

- 23 -

Looking into the future, World Development Report 1981 predicts

that by 1985 the current account surpluses of the CSOEC's will be in the

order of $100 billion (see Table 8). Some considerable improvement in the

current account position of the industrialized countries is expected over

the same period, with the result that the OIDC's will be unable to improve

their own current account positions in nominal terms.

Growth is expected to remain sluggish in the industrialized econo-

mies - between 2.6% and 3.3% during the 1980-85 period. The period up to

1985 is also likely to be characterized by continued high inflation,

although the inflation rate may fluctuate about a marginally lower mean

than that observed in the latter half of the 197 0s. This implies a con-

tinuation of historically high interest rates in the world's main money

and capital markets.

An Analysis of Recent Bank Lending to the OIDC's

This subsection draws upon the recent economic developments set out

thus far to explain movements in the data for bank lending to the OIDC's

(Tables 4 through 6). The analysis is carried out with reference to a

simple supply and demand model. It is assumed that the market is amenable

to conventional partial equilibrium analysis. 1/

Lending through the syndicated Eurocurrency credit market is the

most important form of private finance for the OIDC's, although the data

themselves are not entirely comprehensive 2/ and should be treated with

caution. 3/

1/ See A.E. Fleming and S.K. Howson, "Conditions in the Syndicated Medium-term Eurocredit Market," Bank of England Quarterly Bulletin (Sept.1980).

2/ Data only cover publicized lending. The increasing importance of un-published lending when market conditions tighten probably leads to anunderestimation of loan volume at such times.

3/ The data contain some stand-by credits (which may never be drawn) andrefinanced credits (which arguably impart a degree of double countingto the data).

- 24 -

A key question in the analysis is the nature of the clearing

price. To the borrower, both LIBOR and spread will be important in deter-

mining the level of demand. For the lending bank, it is the spread which

is of prime importance because this is the return on the banks' inter-

mediary services. Accordingly, the spread is taken as the clearing price,

and large changes in LIBOR are assumed to shift the curves rather than to

bring about movements along them. Readers are advised that the simple

model described below is purely a characterization of events and is not

derived from a rigorous analysis based upon econometric investigation.

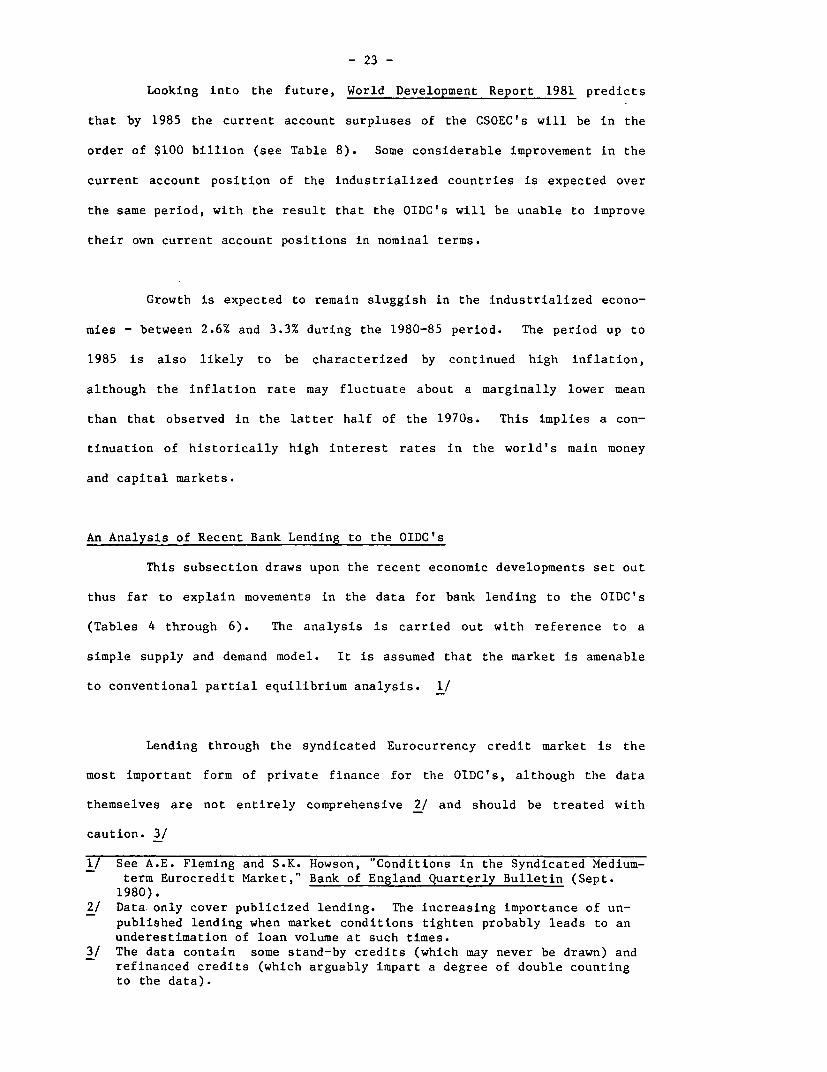

Table 9 summarizes the movements in the volume of and spreads on

lending as well as the main determinant of OIDC borrowing demand, their

current account positions.

Table 9: OIDC Current Accounts, volume of syndicated lending and loanspreads, 1976-81 (US$billions)

1976 1977 1978 1979 1980 1981 a/

Current AccountPosition -26.8 -22.9 -25.5 -44.4 -69.6 -85.0

SyndicatedLending 11.8 10.4 19.6 26.5 25.1 28.0

Average LoanSpread (%) 1.76 1.85 1.25 .77 .90 1.10

a! Estimates.Source: World Bank, CMS.

The starting point for analysis is 1977. Chart 1 depicts the

supply and demand for syndicated loans 1/ and the resulting spread (s )

and loan volume (q 7) in that year.

1/ In nominal terms.

- 25 -Chart 1: Supply and demand, for syndicated loans to OIDC's, 1977.

Spread=s Demand Supply

77

77 q=quantity ofq lending

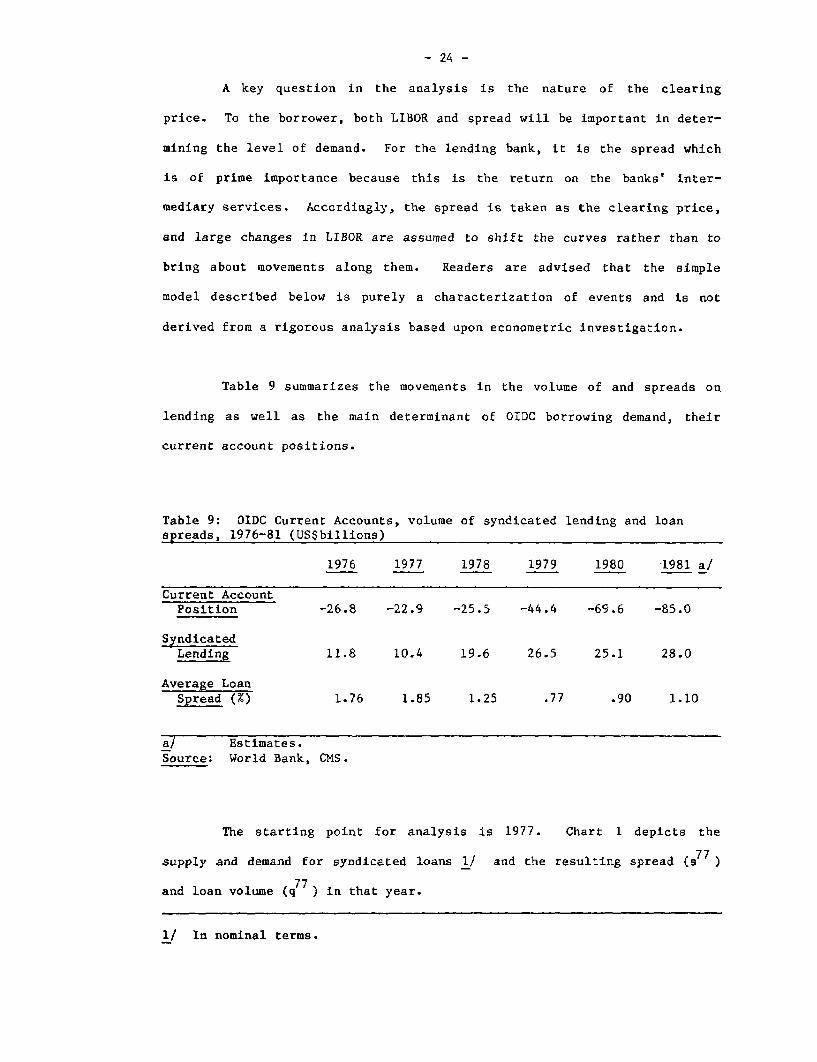

The situation that evolved in 1978 is depicted in Chart 2. On the

demand side of the market there was probably little increase in the

underlying demand for funds (the demand curve shifted outward only

slightly) because the current account deficits increased imperceptively.

On the supply side, however, there was a substantial increase in the

liquidity of the international banks, which shifted the supply curve

outward. As noted in Section III, one explanation that has been offered

was the liquidity-creating effects of a U.S. current account deficit. A

more potent explanation, however, may be the low level of domestic loan

demand in the industrialized countries. The result was an increase in the

quantity of borrowing (q 77 q ) and a fall in spreads (s -Es 7 ). An

interpretation of the 1978 outcome is that the OIDC's were actively

encouraged to borrow much more than their current needs by the banks, which

were flush with funds. There was, consequently, a substantial build up in

OIDC borrowed reserves in 1978.

- 26 -

Chart 2: Supply and demand, for syndicated loans to OIDC's, 1978.

Spread=s Demand Supply

775

78 S

q77 78 q=quantity ofq q 'lending

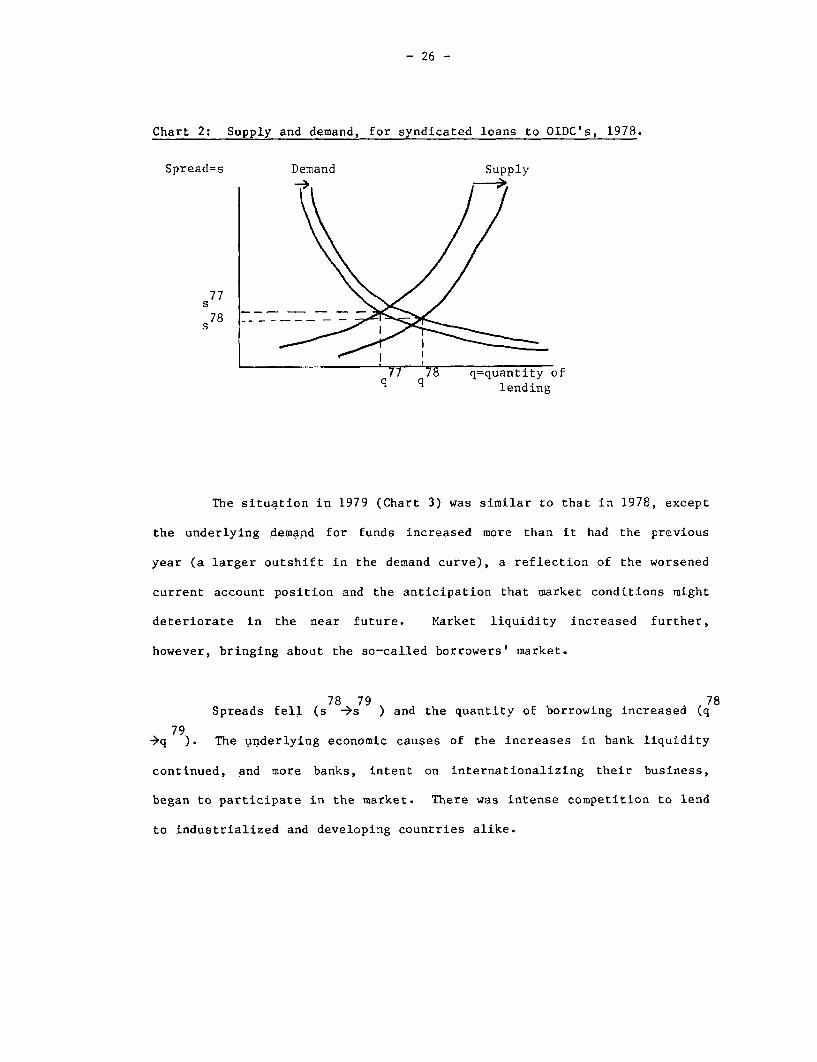

The situation in 1979 (Chart 3) was similar to that in 1978, except

the underlying demand for funds increased more than it had the previous

year (a larger outshift in the demand curve), a reflection of the worsened

current account position and the anticipation that market conditions might

deteriorate in the near future. Market liquidity increased further,

however, bringing about the so-called borrowers' market.

78 79 78Spreads fell (s -3s ) and the quantity of borrowing increased (q

79-*q ). The underlying economic causes of the increases in bank liquidity

continued, and more banks, intent on internationalizing their business,

began to participate in the market. There was intense competition to lend

to industrialized and developing countries alike.

- 27 -

Chart 3: Supply and demand, for syndicated loans to OIDC's, 1979.

Spread=s De Suppl

785

79

q78 q79 q=quantity oflending

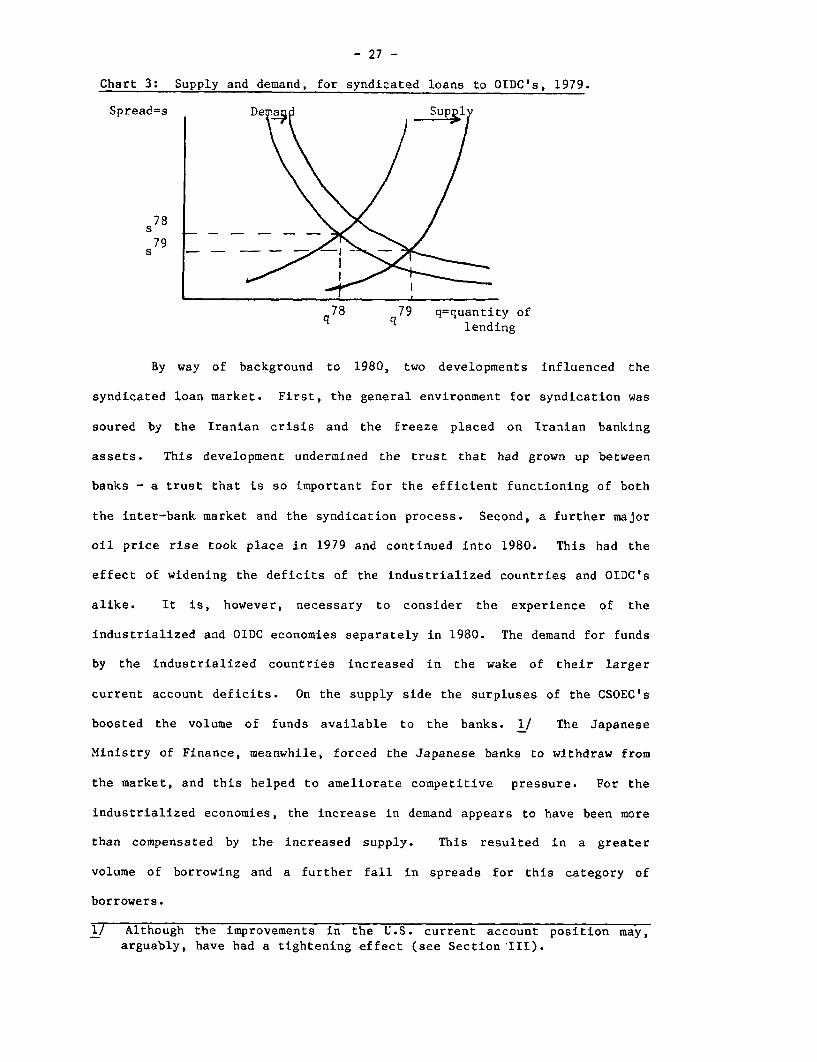

By way of background to 1980, two developments influenced the

syndicated loan market. First, the general environment for syndication was

soured by the Iranian crisis and the freeze placed on Iranian banking

assets. This development undermined the trust that had grown up between

banks - a trust that is so important for the efficient functioning of both

the inter-bank market and the syndication process. Second, a further major

oil price rise took place in 1979 and continued into 1980. This had the

effect of widening the deficits of the industrialized countries and OIDC's

alike. It is, however, necessary to consider the experience of the

industrialized and OIDC economies separately in 1980. The demand for funds

by the industrialized countries increased in the wake of their larger

current account deficits. On the supply side the surpluses of the CSOEC's

boosted the volume of funds available to the banks. 1/ The Japanese

Ministry of Finance, meanwhile, forced the Japanese banks to withdraw from

the market, and this helped to ameliorate competitive pressure. For the

industrialized economies, the increase in demand appears to have been more

than compensated by the increased supply. This resulted in a greater

volume of borrowing and a further fall in spreads for this category of

borrowers.

1/ Although the improvements in the U.S. current account position may,arguably, have had a tightening effect (see Section 'III).

- 28 -

For the OIDC's the situation was slightly different. On the demand

side several factors - in addition to the OIDC current account deficits -

were at work. Several of these may have moderated demand. The high level

of reserves - accumulated during the easy market phase of 1978-79, when

much anticipatory borrowing took place - may have encouraged these coun-

tries to hold back from the market. In any case, unused borrowing commit-

ments were high, and this meant that there would have been less need for

recourse to the markets. The high level of LIBOR may have also discouraged

many borrowers from approaching the market. There was also another impor-

tant factor working on the supply side. The heightened fears of country

risk, fueled by the high OIDC current account deficits, encouraged the

banks to reappraise their country lending limits. Against this background

the industrialized countries looked a more attractive lending proposition.

As a result, it seems reasonable to assume that there was little shift in

the demand curve, while the supply curve probably shifted backwards for the

OIDC-s as depicted in Chart 4.

Chart 4: Supply and demand for syndication loans to OIDC's, 1980.

Demand SupplySpread=s i-

80s

79 _ _ _S

. ~~~~~~~~~~I I80 79 q=quantity ofq q lending

79 80The result was a fall-off in the volume of lending 1/ (q 7-q ) and a rise

in average spreads (s794s 0).

1/ Although some OIDC borrowing may have been diverted to non-publicizedsources.

- 29 -

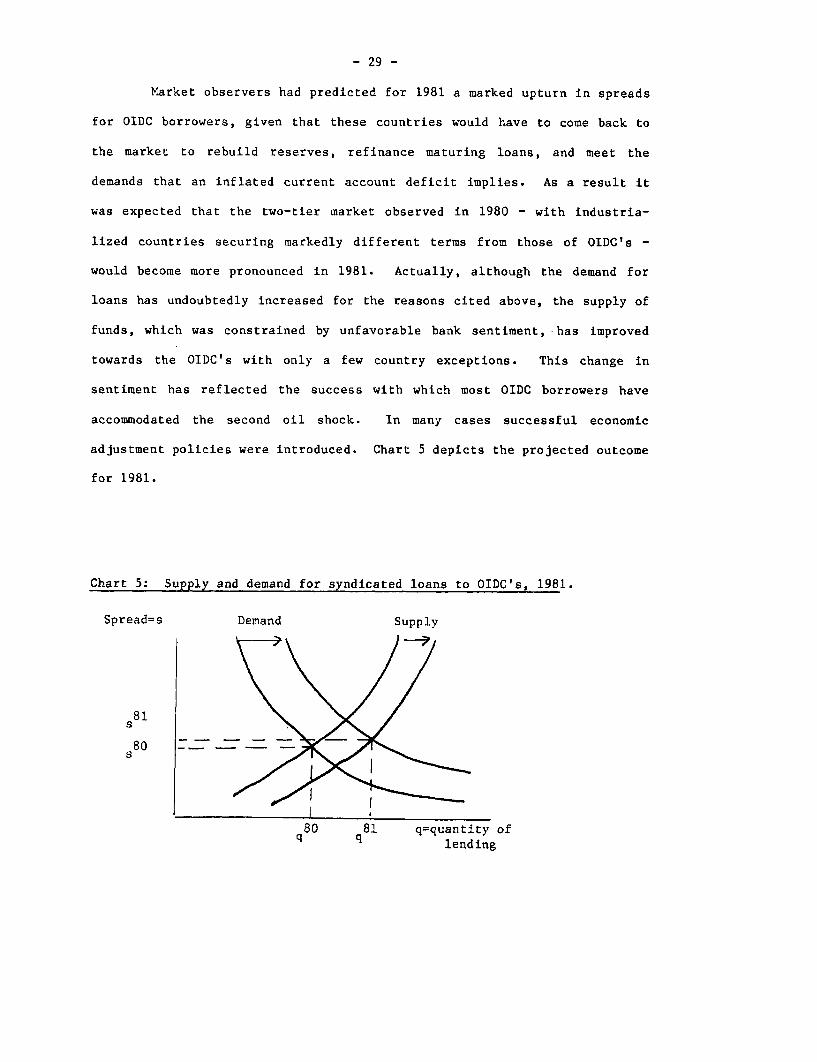

Market observers had predicted for 1981 a marked upturn in spreads

for OIDC borrowers, given that these countries would have to come back to

the market to rebuild reserves, refinance maturing loans, and meet the

demands that an inflated current account deficit implies. As a result it

was expected that the two-tier market observed in 1980 - with industria-

lized countries securing markedly different terms from those of OIDC's -

would become more pronounced in 1981. Actually, although the demand for

loans has undoubtedly increased for the reasons cited above, the supply of

funds, which was constrained by unfavorable bank sentiment, *has improved

towards the OIDC's with only a few country exceptions. This change in

sentiment has reflected the success with which most OIDC borrowers have

accommodated the second oil shock. In many cases successful economic

adjustment policies were introduced. Chart 5 depicts the projected outcome

for 1981.

Chart 5: Supply and demand for syndicated loans to OIDC's, 1981.

Spread=s Demand Supply

81

80 -7-

80 81 q=quantity ofq q lending

- 30 -

Spreads rise slightly (s 8-s ) as does the volume of lending (q -3

q ), resulting from the greater shift in demand than in supply.

The Impact of Banking Constraints

Before considering the outlook for banking flows into the mid-

1980s, it is necessary to examine whether there are any upcoming con-

straints likely to impinge upon the banks' willingness or ability to lend

to the OIDC's.

It is suggested that the falling profitability of international

banking, or more specifically the declining returns available relative to

risk, is one factor that may cause banks to hold back from the market.

Although the long-term trend in spreads may be downward, 1/ and although

low spreads are mitigated only in part by high short-term interest rates

(which endow them with a high return on their capital), it is clear that

the long-term profitability of a bank's entire relationship with an OIDC

may be the factor of key importance. The entire relationship takes in such

profitable business as foreign exchange dealing, trade financing, etc.

Although the loan loss record has been very good in the past on

international lending (compared with domestic lending), concerns have been

expressed that the exposure of some banks overseas is becoming excessive

relative to domestic lending. In the short term some banks heavily

involved in international lending have reportedly found their share prices

quoted at a discount, which hampers any attempt to raise new equity. There

1/ A.E. Fleming and S.K. Howson, "Conditions in the Syndicated Medium-termEurocredit Market," Bank of England Quarterly Bulletin, (Sept. 1980).

- 31 -

is evidence to suggest, however, that whereas overall bank exposure to

OIDC-s is large, the lack of structural uniformity of the countries within

the OIDC category ensures that lending risk is well diversified. 1/

Declining capital ratios have been cited as another possible con-

straint on banks. Inflation has had a significant impact on capital ratios

in some countries. 2/ This is probably the least potent of influences on

bank lending in the short term, although it is perhaps of more significance

in the long run. Ascertaining whether capital is adequate for banks has

different meanings in different banking systems. 3/ The possible relevance

of capital adequacy to OIDC borrowing stems from two important balance-

sheet relationships. The first of these is on the assets side, between

country lending limits (either internally set or externally imposed) and

capital. On the liability side, banks are concerned about their total

liability growth relative to capital as well as the relationship between

their potentially volatile deposits (deposits from, say the CSOEC's) and

capital.

On the assets side there is a question of "country limits." 4/

There is no formal definition of what these limits should be, although in

the United States regulators have a ruling that loans to one borrower must

I/ Laurie S. Goodman, "Bank Lending to Non-OPEC LDC's: Are RisksDiversified?" Federal Reserve Bank of New York Quarterly Review,(Summer 1981).

2/ Jack Revell, "Costs and Margins in Banking: An International Survey,"Organisation for Economic Co-operation and Development Study (Paris,1980).

3/ See also "International Capital Markets - Recent Developments andShort-term Prospects," IMF Occasional Paper, No.7 (August 1981), Table3.

4/ For a thorough coverage of this issue, see Richard O'Brien, "PrivateBank Lending to Developing Countries," World Bank Staff Working Paper,No. 482 (Washington, D.C., August 1981).

- 32 -

not exceed 10% of captial surplus plus retained earnings; this does not,

however, apply to countries. Banks' internal country limits are not

published, and there is no way of analyzing how far the market itself is

"up to its limit." Undoubtedly limits are being reached for some banks

with some countries, and further extensive borrowing by those countries

would require an expansion of the number of banks wishing to take on their

exposure. Some banks may have reached limits for certain countries in

specific categories of lending (to a specific type of entity, for instance)

or maturity of loan, which brings with it the possibility of heavier

concentrations of lending at short term. Concentration of OIDC debt in the

shorter maturity range could of itself be a worrisome development.

Overall, however, there is no strong evidence to suggest that "country

limits" are either a general or lasting constraint on banks' activities.

A further set of constraints emanate from the monetary authorities

in the industrialized economies. The first of these relate to proposals to

control the growth of the Eurocurrency markets through the introduction of,

say, reserve requirements on Eurocurrency deposits. This would involve a

very high degree of international cooperation in an area where there is

considerable international disagreement on the usefulness and feasibility

of such controls. The intellectual underpinnings of the need for

Euromarket controls were weakened by the fact that recycling has proceeded

very smoothly in the wake of the second oil shock, as it did after the

first. Attempts by the United States to get agreement to a form of reserve

requirement have accordingly been shelved.

- 33 -

There does seem to be some measure of agreement among the central

banks in the industrialized countries that there is a need for greater

transparency in international banking flows and closer prudential surveil-

lance. Moves have been made in the Cooke Committee 1/ towards requiring

banks to report their activities on a consolidated basis, thereby permit-

ting closer scrutiny of a bank's entire operations by banking supervisors.

Some analysts have argued that in the long run this might place some con-

straint on the ability of banks to extend international loans. 2/

Recent moves by the U.S. authorities to establish an offshore bank-

ing zone in New York may be construed as an attempt to encourage the repat-

riation to the United States of dollar banking business and hence in the

longer run permit closer surveillance of banking business.

Prospects for International Banking Flows

In much of the literature the possible constraints on banking

intermediaries are overemphasized. Whereas some of the constraints

undoubtedly do constrain certain banks and impinge on specific country

borrowers at particular times, it is misleading to suggest that there will

be a' general constraint on banks that will act so as Ito cut off abruptly

the supply of funds to the OIDC's. Even a prospect of default that, it

might be thought, would ensure a cessation in the flow of funds need not

prove unduly worrisome, for banks have quite profitably rescheduled the

borrowings of countries that have run into financial difficulties. Pruden-

tial controls, meanwhile, by creating a more stable environment for banking

business, could encourage, not discourage, flows of funds to the OIDC's.

1/ For a brief history of international banking supervision, see Develop-ments in Cooperation among Banking Supervisory Authorities," Bank ofEngland quarterly Bulletin (June 1981).

2/ The German authorities, for instance, are gaining greater control overthe activities of German banks in Luxembourg.

- 34 -

Although the data for gross medium-term syndicated lending to

OIDC's has shown some fluctuation over time, net Euromarket lending 1/

(which includes short-term Lending) has exhibited a steadier annual rate of

growth in excess of 20% a year over the past four years, and this at a time

when many commentators had expected banking constraints to become binding.

OIDC borrowers are becoming more sophisticated, too, recognizing that the

best time to borrow is not when the need is greatest 2/ (for bankers' risk

perception is at its greatest then) but when market conditions are easiest.

The prime determinants of banking flows are not the constraints

discussed above, for there is a strong propensity for banks - unconstrained

by county limits or capital considerations - to enter or reenter this mar-

ket and thereby overcome the market constraints. Experience over the past

year suggests that when market conditions are tighter a small rise in

spreads may be sufficient to encourage potential lenders to the market. 3/

The key determinants of banking flows are the macroeconomic ones,

and as far as future developments are concerned the persistence of large

surpluses among the CSOEC½s - together with relatively sluggish growth and

hence slack loan demand in the major industrialized countries - means that

banking intermediaries will continue to have a major role to play in

channeling funds to the OIDC's. The strong desire by banks to inter-

nationalize their business as a means to diversifying their portfolios

ensures that the banking intermediation process becomes effective. The

Middle East banks have entered the international banking markets and have

1/ BIS data - see Table 6.

2/ See Stanyer and Whitley, "Financing World Payments Balances," Bank ofEngland Quarterly Bulletin (June 1981).

3/ See "International Capital Markets; Recent Developments and Short-term

Prospects, 1981," IMF Occasional Paper, No. 7 (August 1981), pp. 17-18.

- 35 -

become very active in injecting new capital into the systems, while banks

from the developing countries themselves are waiting in the wings. Until

such time as the world's banks have restructured their portfolios and

attained the "desired" balance of OIDC exposure in their portfolios, it is

possible to envisage increases in net bank lending of the order of 20% a

year. In terms of the simple supply and demand model explored above, this

would imply continuous outshifts in the supply and demand curves until such

time as portfolio balance has been reached. Thereafter spreads might rise

more permanently for OIDC borrowers as the demand shift exceeds the supply

shift.

Prospects for the External Bond Markets

As shown in Table 7, very little external finance has been

obtained by the OIDC's in the foreign and international bond markets in

recent years despite efforts to provide greater access to these markets. 1/

There has been very little overall growth, and that issue volumes have held

up reflects innovations in the market: the growth of floating-rate notes,

convertible bonds, and numerous other hybrid instruments. Although

international interest rates could decline from the historical peaks

registered recently, prospects for a permanent return to low interest rate

levels is bleak. The prospective interest rate environment therefore seems

likely to make access to international fixed-rate markets sporadic.

Domestic bond markets will continue to be dominated by the demands of the

industrialized country governments themselves, which will be seeking

non-money-creating finance to square their high levels of expenditure with

monetary stringency.

1/ The World Bank/IMF Development Committee set up a working group in June1975 to examine the impediments to developing country access to thecapital markets and to suggest ways in which access might be promoted.See the Secretariat of the Development Committee document, "DevelopingCountry Access to Capital Markets" (Washington, D.C., November 1978).

- 36 -

It therefore seems likely that the OIDC's will have to rely

heavily, in the period up to 1985, on financing from the private banks if

concessional financing does not respond sufficiently to cover the large

current account deficits likely to ensue.

No. TITLE OF PAPER AUTHOR

486 Adjustment in Low-Income Africa R. Liebenthal

487 A Comparative Analysis of Developing Country C. WallichAdjustment Experiences in the 1970s: Low-IncomeSouth Asia

488 Developments in and Prospects for the External N. HopeDebt of the Developing Countries: 1970-80 andBeyond

489 Global Energy Prospects B.J. ChoeA. LambertiniP. Pollak

- 37 -

Additional References

R.Z. Aliber "The Integration of the Offshore andDomestic Banking System," The Journal ofMonetary Economics (1980).

G. Dennis and D. Llewellyn Trends in International Capital Markets(formerly published by The Banker, London).

G. Dufey and I. Giddy The International Money Market, New York,Prentice-Hall (1978).

S.F. Frowen (ed). A Framework of International BankingGuidford, England: Guidford EducationalPress (1979).

R.J. Herring and National Monetary Policies and Inter-R.C. Marston national Financial Markets, Amsterdam,

North Holland (1977).

R.B. Johnston "Banks' International Lending Decisionsand the Determination of Spreads on Syndi-cated Medium-term Eurocredits," Bank ofEngland Discussion Paper, No. 12 (Sept.1980).

M.S. Mendelsohn Money on the Move: The Modern InternationalCapital Market, New York,, McGraw-Hill (1980).

Morgan Guaranty Trust World Financial Markets, New York (monthly).

OECD Financial Market Trends, Paris (monthly).

COMPANION PAPERS IN THIS SERIES

No. TITLE OF PAPER AUTHOR

449 Policy Experience in Twelve Less Developed Countries B. Balassa

470 Industrial Country Policy and Adjustment to Imports J.M. Fingerfrom Developing Countries

471 The Political Structure of the New Protectionism D. Nelson (consultant)

472 Adjustment to External Shocks in Developing Countries B. Balassa

473 Food Policy Issues in Low-Income Countries E. Clay (consultant)

474 Energy, International Trade, and Economic Growth A. Manne (consultant)

475 Capital-Importing Oil Exporters: Adjustment Issues A.H. Gelband Policy Choices

476 Notes on the Analysis of Capital Flows to Developing R.C. Bryant (consultant)Nations and the 'Recycling' Problem

477 Adjustment Experience and Growth Prospects of the F. JaspersenSemi-Industrial Countries

478 Trade Policy Issues for the Developing Countries I. Frank (consultant)in the 1980s

479 Trade among Developing Countries: Theory, Policy 0. HavrylyshynIssues, and Principal Trends (consultant)

M. Wolf

480 Trade in Services: Economic Determinants and A. Sapir (consultant)Development-Related Issues E. Lutz

481 International Migrant Workers' Remittances: Issues G. Swamyand Prospects

482 Private Bank Lending to Developing Countries R. O'Brien (consultant)

483 Development Prospects of the Capital Surplus R. HablutzelOil-Exporting Countries

484 Private Capital Flows to Developing Countries and A. FlemingTheir Determination

485 International Adjustment in the 1980s V. Joshi (consultant)

No. TITLE OF PAPER AUTHOR

486 Adjustment in Low-Income Africa R. Liebenthal

487 A Comparative Analysis of Developing Country C. WallichAdjustment Experiences in the 1970s: Low-IncomeSouth Asia

488 Developments in and Prospects for the External N. HopeDebt of the Developing Countries: 1970-80 andBeyond

489 Global Energy Prospects B.J. ChoeA. LambertiniP. Pollak

PUB HG3881.5.W57 W67 no.484Fleming, Alexander.Private capital flows todeveloping countries andtheir dete

PUB HG3881.5 .W57 W67 no.484Fleming, Alexander.Private capital flows todeveloping countries andtheir determination :

DATE NAME AND EXTENSION NUROOM1- z ~~~~NUMBER