Embed Size (px)

Citation preview

Prism’s Approach to Modeling Natural Catastrophe Risk

Casualty Actuarial Society

November 12, 2007

Mark Rouck, CPA, CFA

Topics

Background on Prism

Prism’s Catastrophe Risk Component

What Does it Mean for Ratings?

Topics

Background on Prism

Prism’s Catastrophe Risk Component

What Does it Mean for Ratings?

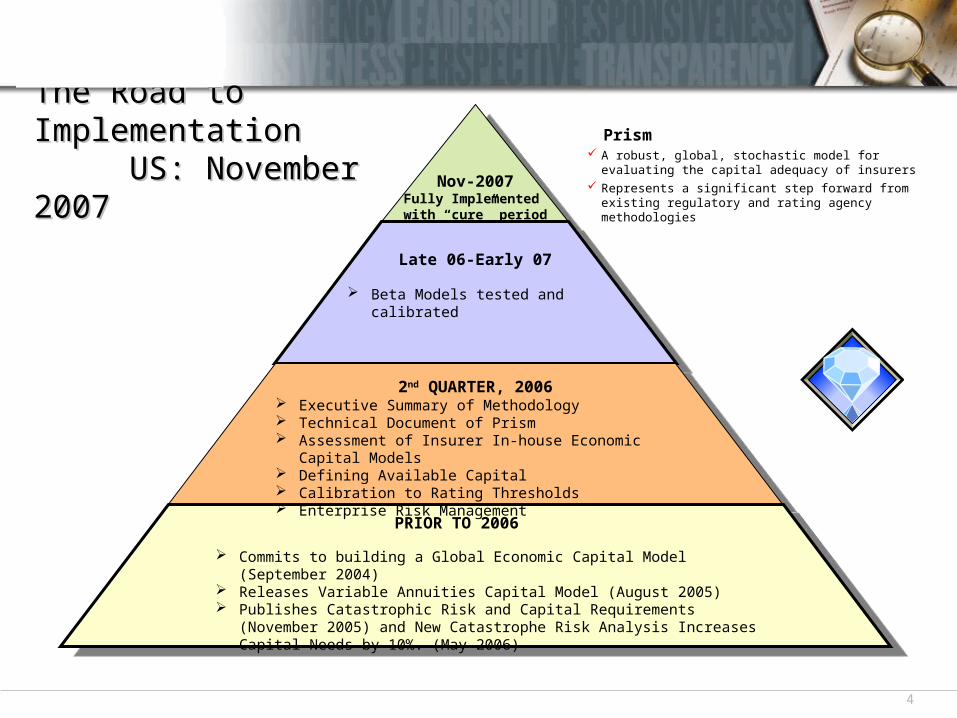

4

Nov-2007Fully Implemented with “cure” period

Nov-2007Fully Implemented with “cure” period

Late 06-Early 07Late 06-Early 07

2nd QUARTER, 20062nd QUARTER, 2006

PRIOR TO 2006PRIOR TO 2006

The Road to ImplementationThe Road to Implementation US: November 2007 US: November 2007

Beta Models tested and calibrated

Executive Summary of Methodology Technical Document of Prism Assessment of Insurer In-house Economic Capital Models Defining Available Capital Calibration to Rating Thresholds Enterprise Risk Management

Commits to building a Global Economic Capital Model (September 2004) Releases Variable Annuities Capital Model (August 2005) Publishes Catastrophic Risk and Capital Requirements (November 2005) and New

Catastrophe Risk Analysis Increases Capital Needs by 10%. (May 2006)

Prism A robust, global, stochastic model for evaluating

the capital adequacy of insurers Represents a significant step forward from existing

regulatory and rating agency methodologies

5

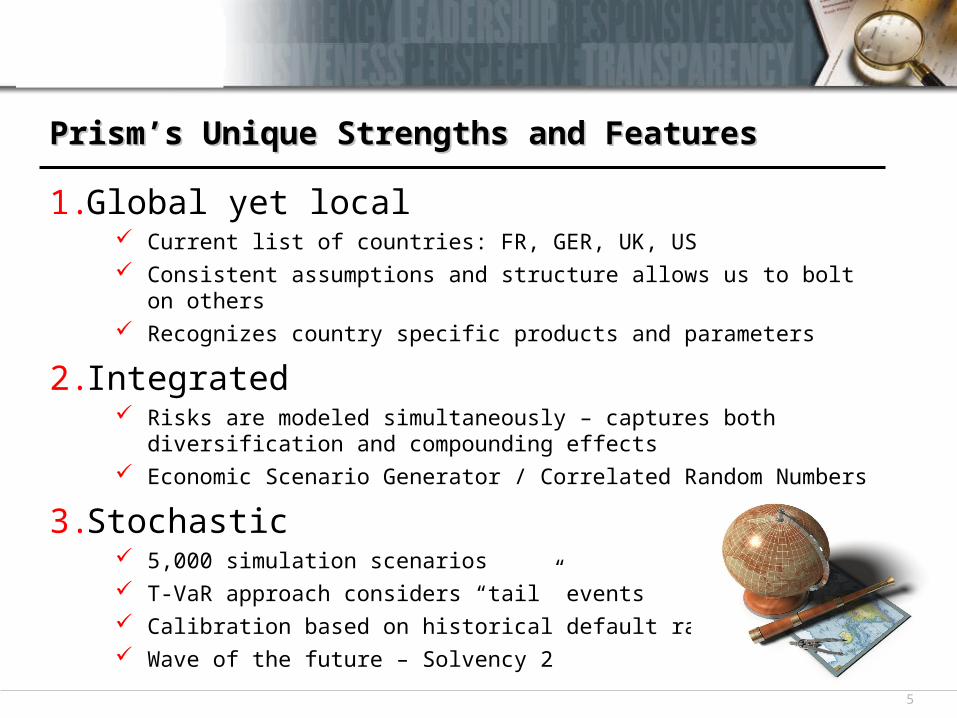

1.Global yet local Current list of countries: FR, GER, UK, US Consistent assumptions and structure allows us to bolt on others Recognizes country specific products and parameters

2. Integrated Risks are modeled simultaneously – captures both diversification and

compounding effects Economic Scenario Generator / Correlated Random Numbers

3.Stochastic 5,000 simulation scenarios T-VaR approach considers “tail” events Calibration based on historical default rates Wave of the future – Solvency 2

Prism’s Unique Strengths and FeaturesPrism’s Unique Strengths and Features

6

Modeling Methods – Risk Elements CapturedModeling Methods – Risk Elements Captured

“Aggregator” Consistent economic scenario set Similar Cat event set Correlated random numbers

Underwriting Risk Use a collective risk

model of frequency and severity of losses.

Relies on ELR, Attachments, Limits

Factors one year of new business.

Underwriting Risk Use a collective risk

model of frequency and severity of losses.

Relies on ELR, Attachments, Limits

Factors one year of new business.

ALM (Market) Risk Incorporates risk-free

yield curve (bonds, mortgages), real estate and equity returns (DAX, FTSE, CAC).

Use a proprietary, integrated scenario generator.

ALM (Market) Risk Incorporates risk-free

yield curve (bonds, mortgages), real estate and equity returns (DAX, FTSE, CAC).

Use a proprietary, integrated scenario generator.

Reserve Risk Incorporates reserve

adequacy analysis Use Mack Method to

Estimate Volatility Utilize several checks

to ensure data integrity

Asbestos & Environmental Losses Evaluated Separately

Reserve Risk Incorporates reserve

adequacy analysis Use Mack Method to

Estimate Volatility Utilize several checks

to ensure data integrity

Asbestos & Environmental Losses Evaluated Separately

Catastrophe Risk Use Company

Provided PMLs Use AIR (Catrader)

software. Consideration of up to

1 in 10,000 event

Catastrophe Risk Use Company

Provided PMLs Use AIR (Catrader)

software. Consideration of up to

1 in 10,000 event

Credit Risk Incorporates defaults,

migration and spread volatility

Use common market indices to establish parameters for asset type and quality

Over 50 asset buckets.

Stochastically model reinsurer default risk

Credit Risk Incorporates defaults,

migration and spread volatility

Use common market indices to establish parameters for asset type and quality

Over 50 asset buckets.

Stochastically model reinsurer default risk

Each Company will potentially have unique risk curves

7

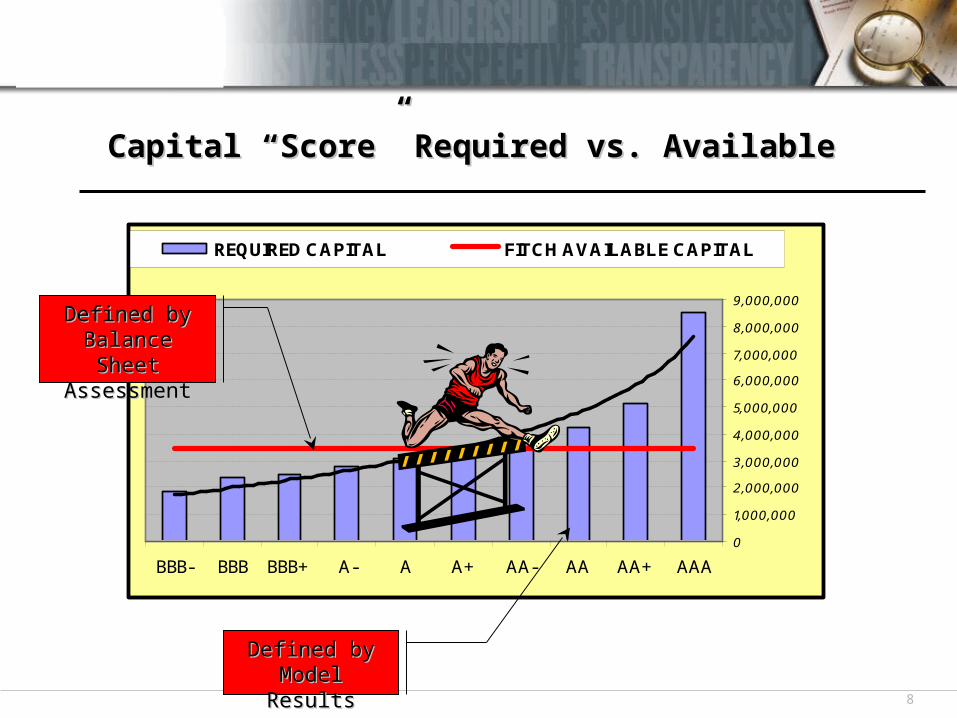

Two Core Outputs Determine Prism ScoresTwo Core Outputs Determine Prism Scores

1. Available Capital or “AC” Economic, not accounting based number

What is amount of liquid capital in a controlled run-off situation

2. Required Capital or “RC” Distribution table produced by the simulation

RC is not a single number but a range of outcomes

Derived by applying the appropriate T-VaR against distribution

Simulation calculates PV of cash inflows and outflows over 30 year balance sheet run-off (with one year of new business) Cash outflows: claims and expenses

Cash inflows: investment earnings and premiums on new business

Prism Score is point where AC intersects RC The highest rating level at which that occurs is your Prism Score

8

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

AAAAA+AAAA-A+AA-BBB+BBBBBB-

REQUIRED CAPITAL FITCH AVAILABLE CAPITAL

Capital “Score” Required vs. AvailableCapital “Score” Required vs. Available

Defined by Defined by Model ResultsModel Results

Defined by Defined by Balance Sheet Balance Sheet AssessmentAssessment

9

Prism: 2006 US Non-Life ResultsPrism: 2006 US Non-Life Results

Confirmed overall existing capital assessment of Fitch universe

Limited (~10% of group’s reviewed) Prism related rating actions

Certain sectors performed better than expected e.g. personal auto

PRISM SCORES: DISTRIBUTION AT YEAREND 2006US: Non-Life Groups

Prism Score# of Non-Life

Insurer GroupsPercent of Total

(%)

AAA 20 47 AA+ 7 16 AA 2 5 AA- 1 2 A+ 6 14 A 3 7 A- 4 9 BBB+ 0 0BBB 0 0BBB- 0 0

Non-investment grade 0 -

Total 43 100

Topics

Background on Prism

Prism’s Catastrophe Risk Component

What Does it Mean for Ratings?

11

Prism’s Catastrophe Risk Component

> Insurer provided modeled annual aggregate catastrophe losses at various return periods – Frequency / Severity Assumptions = Near-term

– Demand Surge = Occurrence base

> AIR Catrader models gross annual aggregate catastrophe losses at various return periods based on by state premium distribution and AIR event sets

> Interpolation generates modeled annual aggregate gross loss distribution ranging from 20-10K year return periods

12

Prism’s Catastrophe Risk Component (cont.)

> Catastrophe reinsurance program applied against gross losses to create annual aggregate modeled net loss distribution– Alternatively will use insurers full net annual aggregate

catastrophe loss distribution if provided

> Alternatives to traditional reinsurance (i.e. catastrophe bonds, ILWs) added to catastrophe reinsurance program based on perils and attachment points

13

Prism’s Catastrophe Risk Component (cont.)

> Modeled net catastrophe losses combined with other risk components to determine each scenario’s additional capital needs

YearAsset

BalanceNet

PremiumInvestment

Income ClaimsCAT

Losses

Asset Balance Ending

Added Required Capital NPV

1 5,491 2,013 1,245 3,203 152 5,394 - - 2 5,394 - 216 2,017 - 3,593 - - . 485 - 19 388 - 116 . 116 - 4 153 - (33) 33 22

30 - - - 43 - (43) 43 27

Total 49

Topics

Background on Prism

Prism’s Catastrophe Risk Component

What Does it Mean for Ratings?

15

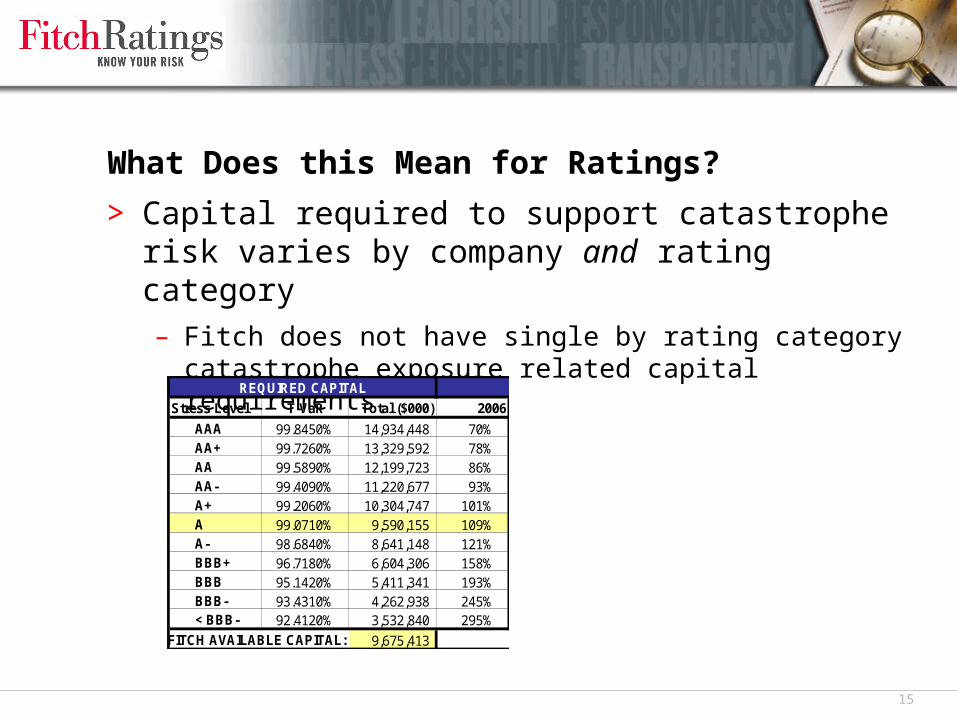

What Does this Mean for Ratings?

> Capital required to support catastrophe risk varies by company and rating category– Fitch does not have single by rating category catastrophe

exposure related capital requirements

Stress Level T-VaR Total ($000) 2006

AAA 99.8450% 14,934,448 70%AA+ 99.7260% 13,329,592 78%AA 99.5890% 12,199,723 86%AA- 99.4090% 11,220,677 93%A+ 99.2060% 10,304,747 101%A 99.0710% 9,590,155 109%A- 98.6840% 8,641,148 121%BBB+ 96.7180% 6,604,306 158%BBB 95.1420% 5,411,341 193%BBB- 93.4310% 4,262,938 245%< BBB- 92.4120% 3,532,840 295%

FITCH AVAILABLE CAPITAL: 9,675,413

REQUIRED CAPITAL

16

What Does this Mean for Ratings? (continued)

> Catastrophe related “stress test” implicitly considered through– Use of annual aggregate modeled catastrophe losses

– T-VaR approach applied to overall required capital distribution

– In unique cases, modeled catastrophe results can also be stressed by shifting company supplied or CATRADER generated loss distributions upward

17

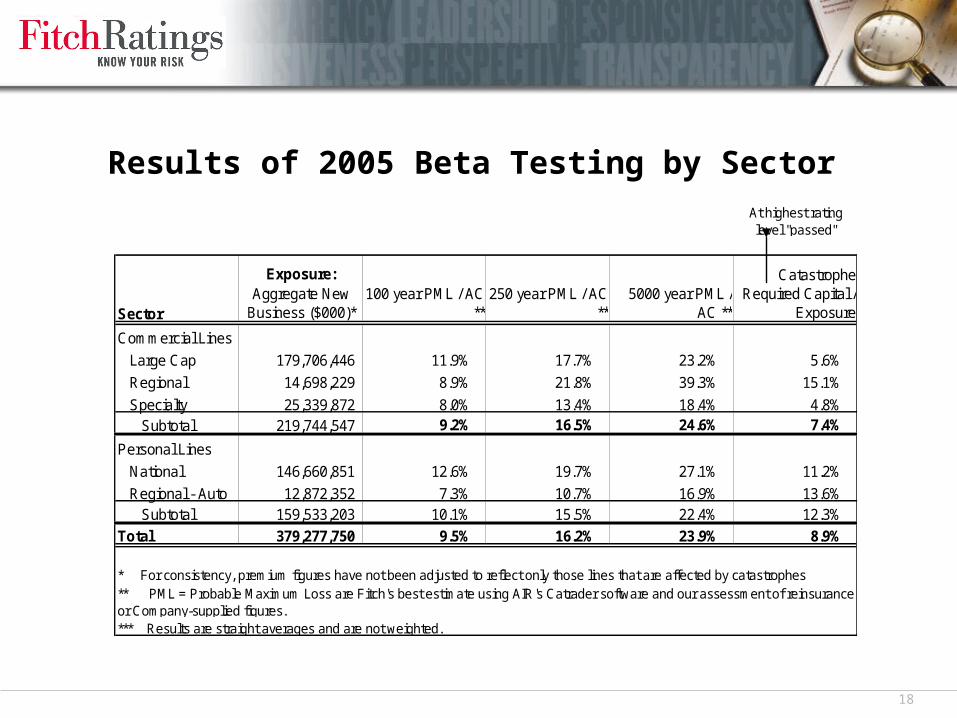

Catastrophe Findings from 2005 Beta Testing

> Insurers with large homeowners or coastal property coverages have tremendous capital exposure to extreme tail events

– For these insurers required capital can materially exceed 100 year and 250 year PML used in factor based models

> Others such as specialty liability underwriters have virtually no catastrophe exposure

> For universe in aggregate, catastrophe related required capital was equal to 8.9% of aggregate exposure

> Ignoring insurers without catastrophe exposure, range of required catastrophe capital / exposure was 6% - 37%

18

Results of 2005 Beta Testing by SectorAt highest rating level "passed"

Sector

Exposure: Aggregate New

Business ($000)*100 year PML / AC

**250 year PML / AC

**5000 year PML /

AC **

Catastrophe Required Capital /

Exposure

Commercial Lines

Large Cap 179,706,446 11.9% 17.7% 23.2% 5.6%

Regional 14,698,229 8.9% 21.8% 39.3% 15.1%

Specialty 25,339,872 8.0% 13.4% 18.4% 4.8%Subtotal 219,744,547 9.2% 16.5% 24.6% 7.4%

Personal Lines

National 146,660,851 12.6% 19.7% 27.1% 11.2%

Regional - Auto 12,872,352 7.3% 10.7% 16.9% 13.6%Subtotal 159,533,203 10.1% 15.5% 22.4% 12.3%

Total 379,277,750 9.5% 16.2% 23.9% 8.9%

* For consistency, premium figures have not been adjusted to reflect only those lines that are affected by catastrophes

*** Results are straight averages and are not weighted.

** PML = Probable Maximum Loss are Fitch's best estimate using AIR's Catrader software and our assessment of reinsurance or Company-supplied figures.

19

Takeaways

> Fitch uses Prism to determine capital requirements for natural catastrophe risk

> Prism considers modeled annual aggregate catastrophe loss distributions rather than select points along the distribution to develop capital requirements

> Capital required to support catastrophe risk varies by insurer and by rating category

> “Stress Tests” implicitly considered through annual aggregate and T-VaR approaches employed by Prism

20

Access to this portion of our

website is free –

requires only a registration.

Dedicated Website: www.fitchratings.com/prismDedicated Website: www.fitchratings.com/prism

The Fitch Group Fitch Ratings Algorithmics Fitch Training

Fitch Ratingswww.fitchratings.com

London101 Finsbury Pavement London EC2A 1RS +44 20 7417 4222

New YorkOne State Street PlazaNew York, NY 10004+1 212 908 0500+1 800 75 FITCH

Singapore7 Temasek Blvd.Singapore 038987+65 6336 6801