Embed Size (px)

Citation preview

Prin

ted

by T

aco

Vis

ions

Pvt

. Ltd

.w

ww

.taco

visi

ons.

com

C C MM YY K

C C MM YY K C C MM YY K

1 1

Board of Directors 02

3600 - The Business of Creation 03

Chairman’s Letter 04

Performance at a Glance 06

Key Highlights 07

Directors’ Report 08

Annexure To Directors’ Report 12

All Round Solutions 14

Management Discussion and Analysis 15

Financial Highlights 25

Corporate Governance 26

Auditors’ Report 37

Balance Sheet 40

Profit and Loss Account 41

Schedule to & Forming Part of Accounts 42

Balance Sheet Abstract 62

Cash Flow Statement 63

Consolidated Financial Statements

Statement Under Section 212 of the Companies Act, 64 1956 relating to subsidiary companies

Auditors’ Report 65

Consolidated Balance Sheet 66

Consolidated Profit and Loss Account 67

Consolidated Schedule to & Forming Part of Accounts 68

Consolidated Cash Flow Statement 88

29th Annual Report and Audited Statement of Accounts for the year ended March 31, 2010

C O N T E N T S

22

E X E C U T I V E M A N A G E M E N T T E A MMr. Kamal K. Jain President & CFO

Mr. Dinesh B. Patel President & CEO (Domestic - TL Projects)

Mr. B. K. Satish President & CEO (Distribution Projects)

Mr. N. Sai Mohan President & CEO (Overseas Projects)

Mr. Gyan Prakash President & CEO (Pipeline Projects)

Mr. M. A. Baraiya Head - HR

Company Secretary Mr. Bajrang Ramdharani

Auditors M/s. Kishan M. Mehta & Co., Ahmedabad M/s. Deloitte Haskins & Sells, Ahmedabad

Legal Advisor M/s. Singhi & Co., Ahmedabad

B A N K E R S Indian BankOriental Bank of Commerce Union Bank of IndiaState Bank of IndiaEXIM Bank ICICI Bank Ltd.IDBI Bank Ltd.Standard Chartered BankBNP Paribas, Abu DhabiCommercial Bank of Kuwait

F A C T O R Y & R E G I S T E R E D O F F I C E Plot No. 101, Part III, G.I.D.C. Estate, Sector 28, Gandhinagar - 382 028, Gujarat, India. Tel No.: 91 - 79 - 23214000 Fax No.: 91 - 79 - 23211966 / 68 / 71 Email: [email protected]

C O R P O R A T E O F F I C E ‘KALPATARU SYNERGY’ , 8th Floor, Opp. Grand Hyatt Hotel Vakola, Santacruz(E) Mumbai - 400 055, India. Tel. No.: 91 - 22 - 30645000 Fax No : 91 - 22 - 30643131

W E B S I T E www.kalpatarupower.com www.jmcprojects.com www.kalpataru.com www.ssll.in

Mr. Mofatraj P. Munot , ChairmanFounder, Promoter and Chairman of Kalpataru Group with over 45 years of experience in the field of Real Estate and Property Development, Civil Contracting & various industries.

Mr. Mahendra G. Punatar, Independent Director (Structural Engineering) from University of Michigan, USA with over 50 years of experience in transmission line towers.

Mr. K. V. Mani, DirectorBachelor of Engineering and MBA. Has 45 years of experience in Transmission industry, mainly Construction, Project Management and Overseas Marketing.

Mr. Pankaj Sachdeva , Managing Director B.E (Hons) degree in Electrical Engineering and has over 26 years of Product Marketing and Project Execution experience in Power Systems Sector.

Mr. Parag Munot, Promoter DirectorMBA, Carnegie Mellon University, USA with 17 years of experience, is responsible for the group Real Estate andProperty Development business. Presently Managing Director of Kalpataru Ltd.

Mr. Manish Mohnot, Executive DirectorChartered Accountant and an ICWA having a rich experience of 15 years in consulting in the field of Oil, Gas, Power and other sectors related to Infrastructure. He is also the Director of JMC Projects (India) Ltd. and Shree Shubham Logistics Ltd.

Mr. Sajjanraj Mehta, Independent DirectorChartered Accountant with over 35 years of experience.A Consultant in the field of Foreign Exchange, Taxation and Corporate Affairs and Strategy.

Mr. Vimal Bhandari, Independent DirectorChartered Accountant with an experience of more than 25 years in Financial Services sector. He was Executive Director of IL&FS Ltd. Presently, he is Country Manager - Aegon India.

Mr. Narayan Seshadri, Independent DirectorChartered Accountant with an experience of 28 years in the field of finance, account, tax and business consulting. Presently, he is the Chairman and CEO of Halcyon Resources and Management Pvt. Ltd.

Mr. S. P. Talwar, Independent Director Certified Associate of the Indian Institute of Bankers and Member of Indian Council of Arbitration. He is a Law Graduate and Arts honors. He is a hard core Banker and retired as deputy Governor, RBI. He is a Senior Advisor of Yes Bank Ltd.

Mr. Shitin Desai, Independent Director (upto 10.05.2010)Experience in excess of 28 years in Financial Services sector.He is currently the Executive Vice Chairman of DSP Merrill Lynch Ltd.

B O A R D O F D I R E C T O R S

diaa

ed Bank Dhabi

k of Kuwait

& R E G I S T E R E D O F F I C E t III, G.I.D.C. Estate, Sector 28, 2 028, Gujarat, India. 23214000

- 23211966 / 68 / 71 patarupower.com

E O F F I C E YNERGY’ , 8th Floor, t Hotel Vakola, Santacruz(E)5, India. - 30645000- 30643131

ower.coms.com om

3 3

E X P E R T I S E A C C R O S S I N F R A S T R U C T U R E V A L U E C H A I N • EPC contracting: › Power transmission and distribution › Oil and Gas Pipeline › Factories and Buildings › Roads and Bridges › Power plant construction › Water Pipeline• Ownership of assets: › Power Transmission › Road › Logistics and Warehousing

O R D E R S• Exceeding Rs. 50 billion ($1billion) - Domestic Rs.35 billion - Overseas Rs. 15 billion - Consolidated Order Book exceeding Rs. 77 billion

I N V E S T I N G F O R F U T U R E• Cummulative last 4 year capex exceeding Rs. 3 billion• Investment in subsidiaries in past 4 years exceeding Rs. 1.25 billion

D I V E R S I F I C A T I O N• JMC projects• Shree Shubham Logistics• Oil and Gas Pipelines• Annuity/Boot projects• Real Estate Development

P R O D U C T I O N C A P A C I T Y• In excess of 108,000 MTs - Main Plant - 78,000 MTs - EOU - 30,000 MTs - Planned addition of 30,000 MTs

T E C H N O L O G Y• Global solutions for design• Automated production lines• Integrated solution (SAP)• Automated testing stations• Facility to demonstrate helicopter simulation at tower testing station

P E O P L E• Work force exceeding 5,000• Dedicated training centre

3 6 0 ° - T H E B U S I N E S S O F C R E A T I O N

It takes a tremendous amount of perseverance, dedication and hard work to find a successful foothold in every sphere of diversification within the infrastructure sector. Over the last 40 years, Kalpataru has excelled at being the leader in infrastructure, simply because of its 3600 - the Business of Creation outlook. This very diversification along with a motto to succeed has been the core reason for propelling the group to greater heights.

The exploratory gene, vision, foresight, an unbreakable team and a dynamic view of the industry round off the check list when it comes to having the attributes that make a winning combination. No stone remains unturned in the quest for maintaining and strengthening our leading position.

44

on revamping the transmission infrastructure to reduce transmission losses through technologically innovations like high voltage Ac transmission networks upto 1200 KV and long distance HVDC lines.

On the distribution side, distribution utilities are looking at outsourcing distribution network in cities to reduce distribution losses and improve customer services.Schemes like Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY) & Restructured Accelerated Power Development & Reforms Programme (RAPDRP) to electrify rural India & strengthen urban areas, have given ample opportunities for growth. Your company will selectively continue to tap these opportunities to enlarge its presence in distribution segment.

In the international arena, both developed and developing countries present attractive business opportunities as power continues to be key drivers for this sustainable growth and future development. Countries in Africa, Middle East and CIS countries continue to invest in power transmission as it holds key to their economic growth & prosperity. We are also witnessing opportunities in America and Europe for upgradation of transmission lines and creation of additional capacity with smart solution grids.We have incorporated overseas subsidiaries to focus on the available opportunities in the respective countries.

We as a Company are moving towards leadership position in majority of T & D sector with annual Tower Manufacturing capacity of 108,000 MT pa and presence in over 28 countries with on time delivery records in last 2 decades. We are on track to expand our manufacturing capacity by 30,000 MT pa to be operational in a year’s time. Our fully equipped design & engineering centre, tower testing station, dedicated export manufacturing facility, time tested safety, quality & environment systems & integrated ERP system are keys for meeting tight delivery schedules for international clients.

O I L & G A S P I P E L I N E S - A G R O W T H P L A T F O R MIndia is the third largest oil consumer in the Asia - Pacific region after China and Japan. Demand for hydrocarbon is increasing at rapid space. India has inadequate pipeline network compared with most of developed countries, which is used for only 30% of petroleum product in country. We expect that over the next few years 10,000 Kms of pipe laying work is expected from public and private sector companies in India with an investment of over Rs. 450 billion.

Dear Stakeowners,

I’m once again delighted to address all our stake holders thorough this yearly communiqué whereby I appraise you all on our plans going forward.

The Company reported a spectacular all round performance in the year 2009-10. The revenue of the Company grew by 38% to Rs. 25.96 billion, Net Profit registered a strong growth of over 80% to Rs. 1.70 billion. The consolidated revenue of the Company surpassed Rs. 40 billion mark. We have seen significant improvement in operating margins over the previous year with consolidated EPS of Rs. 67.05.

At heart we have a non - negotiable commitment for consistent growth and value creation, with our continued commitments to world class on time delivery of infrastructure by leveraging our core competence & expertise in design, engineering and project management. Our focus will continue to explore avenues/opportunities for creating value from all our infrastructure spectrum which evolves from our strategy to provide end to end solutions to reinforce our model of 360° - the business of creation.

P O W E R – O U R C O R E F O C U S A R E A O F B U S I N E S S & G R O W T HOur country is still power deficit despite quantum jump in capacity in past few years. The government’s thrust in this sector continues & visible from the developments from new business models such as UMPPs and UMTPs to increase private sector engagement. The Country is witnessing huge investment in power generation, transmission and distribution. Power Grid Corporation of India (PGCIL) has recently announced mega investment plans to the tune of Rs 640 billion in the transmission & distribution Sector (T&D) over the next five years. State utilities are also investing in transmission infrastructure, post the SEB unbundling process. The entire focus is

C H A I R M A N ’ S L E T T E R

5 5

We have also created a leadership position in EPCcontracting business of Oil & Gas pipeline business by executing over 1800 kms of pipelines during the last 5 years. We have met all challenges be it tough terrain like rocky & hilly areas for our Panvel - Dhabol Project or highest diameter of pipe laying work in India of 48” under Vijaypur - Dadri Project. We have invested above Rs. 1.15 billion to create large base of equipments. We are exploring opportunities in international market for EPC contracting for Oil & Gas space and also expecting to spread our wings to entire value chain of Oil & Gas pipeline business, be it upstream or downstream.

C I V I L C O N T R A C T I N G - A N A T I O N B U I L D I N G E F F O R TInfrastructure is the back bone of growth of the country and thrust on development of the same by Government is going to create long term opportunities in the country. The Government has also aimed to expedite infrastructure through public-private partnership by implementing requisite changes in policy framework like introducing competitive bidding process, setting up regulatory authority, rationalization of customs and excise duties etc. Government is looking for revamping and developing all round infra-structure like Roads, Bridges, Canals, Dams, Water, Railway Terminals, Ports, Airports, SEZs as well as Rural and Urban Infrastructure.

JMC Projects, our subsidiary, in the last five years has achieved significant presence in various segments of infrastructure sectors namely factories and buildings, power plants, roads, bridges etc. Given its current order book and visible opportunities along with a commitment to deliver, we believe that JMC would continue to achieve greater heights in the future.

P U B L I C – P R I V A T E P A R T N E R S H I P O P P O R T U N I T I E S , C R E A T I N G A S S E T S F O R S U S T A I N A B L E R E V E N U E I N F U T U R E With opening-up of various opportunities under PPP route your company participated in various PPP projects last year and it’s a matter of great pride that Kalpataru Power Transmission, JMC projects and Shree Shubham Logistics Ltd. (SSLL) all have bagged one project each under this route, of which details are as follows:1. The Company in consortium secured a project from Haryana Vidyut Prasaran Nigam (HVPNL) to evacuate power from the upcoming power plant at Jhajjar through 100 Kms, 400 Kv transmission line &

sub-stations. 2. JMC in consortium bagged a project to construct 83 kms of four-lane highway between Rohtak to Bawal, Haryana from NHAI. 3. SSLL has entered into an agreement with Rajasthan State Warehousing Corporation (RSWC) to manage State owned 38 warehouses having capacity of 405,000 Mts across the state.

Some of the other key achievements of the company during the year are highlighted below:1. Engineering excellence in successful testing 1200 KV transmission tower at our testing station.2. Optimum utilization of Plant capacity for fabrication of transmission tower.3. SSLL, now manages more than 590,000 MT of dry and cold storage in the state of Rajasthan and Gujarat4. The Company’s revenue from international operations crossed the Rs. 10 billion mark. This is a phenomenal growth considering that the division is less than six years old.5. Consolidated order book exceeded Rs. 77 billion.

To support our growth plans, in the month of May, 2010,the Company has successfully raised over Rs. 4.50 billion (USD 101 Million) through QIP issue under SEBI (ICDR) Regulation, 2009. This fund shall be used for capital expenditure, expansion of manufacturing capacity (transmission line towers), long-term investment in PPP, BOT, BOOT and BOOM projects, development of EPC services, further investment in existing divisions and subsidiaries and working capital purposes.

While the trends on business growth in power & energy front are bullish in our country & global market, we are also continuously evaluating the perceived outlook on financial uncertainties in European Union which can globally effect the growth story.

As a global player we strive to meet and exceed expectations of our customers, governments, banks, vendors, employees and investors, benchmarking our performance against best in class industry standards and delivering the best against all odds that is what we call 360° - the Business of Creation.

Thanks to everyone for their unstinted support and faith.

MOFATRAJ P. MUNOTChairman

C H A I R M A N ’ S L E T T E R

66

P E R F O R M A N C E A T A G L A N C EK P T L C O N S O L I D A T E D *

* Year Since Consolidation started

7 7

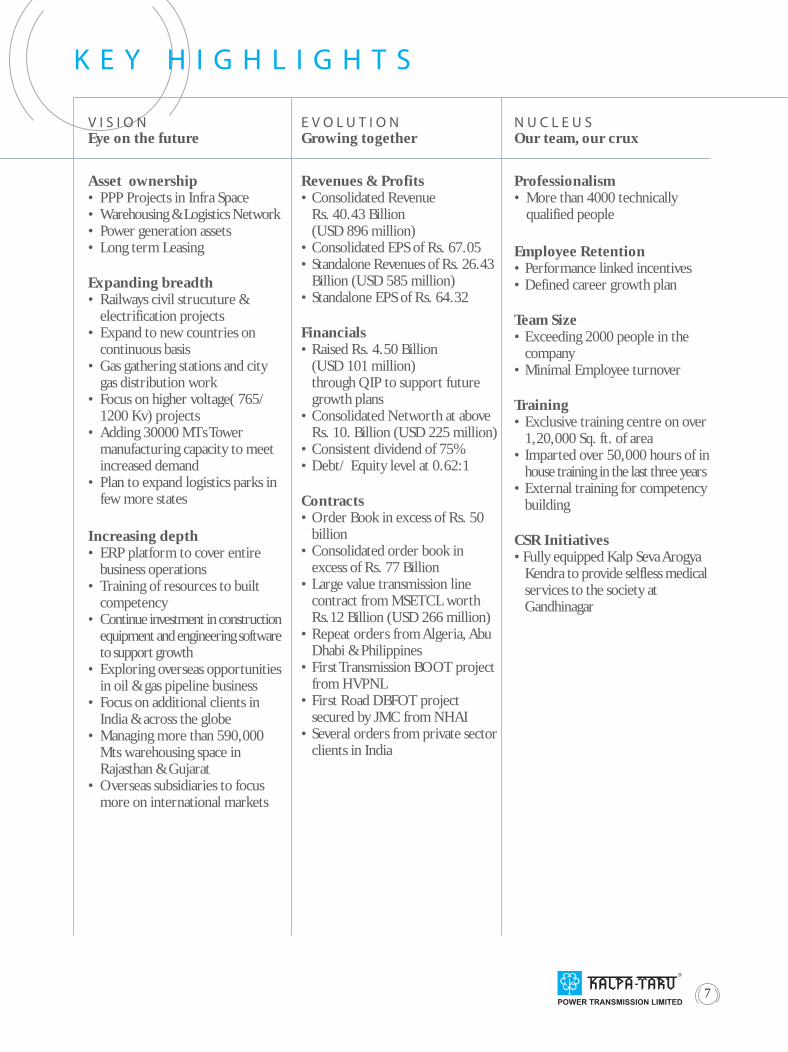

K E Y H I G H L I G H T S

Revenues & Profits• Consolidated Revenue Rs. 40.43 Billion (USD 896 million)• Consolidated EPS of Rs. 67.05• Standalone Revenues of Rs. 26.43 Billion (USD 585 million)• Standalone EPS of Rs. 64.32

Financials• Raised Rs. 4.50 Billion (USD 101 million) through QIP to support future growth plans• Consolidated Networth at above Rs. 10. Billion (USD 225 million)• Consistent dividend of 75%• Debt/ Equity level at 0.62:1

Contracts• Order Book in excess of Rs. 50 billion• Consolidated order book in excess of Rs. 77 Billion• Large value transmission line contract from MSETCL worth Rs.12 Billion (USD 266 million)• Repeat orders from Algeria, Abu Dhabi & Philippines• First Transmission BOOT project from HVPNL• First Road DBFOT project secured by JMC from NHAI• Several orders from private sector clients in India

E V O L U T I O NGrowing together

Professionalism• More than 4000 technically qualified people

Employee Retention• Performance linked incentives• Defined career growth plan Team Size• Exceeding 2000 people in the company• Minimal Employee turnover

Training• Exclusive training centre on over 1,20,000 Sq. ft. of area• Imparted over 50,000 hours of in house training in the last three years• External training for competency building

CSR Initiatives• Fully equipped Kalp Seva Arogya Kendra to provide selfless medical services to the society at Gandhinagar

N U C L E U SOur team, our crux

Asset ownership• PPP Projects in Infra Space• Warehousing & Logistics Network• Power generation assets• Long term Leasing

Expanding breadth• Railways civil strucuture & electrification projects• Expand to new countries on continuous basis• Gas gathering stations and city gas distribution work • Focus on higher voltage( 765/ 1200 Kv) projects • Adding 30000 MTs Tower manufacturing capacity to meet increased demand• Plan to expand logistics parks in few more states

Increasing depth • ERP platform to cover entire business operations• Training of resources to built competency • Continue investment in construction equipment and engineering software to support growth• Exploring overseas opportunities in oil & gas pipeline business• Focus on additional clients in India & across the globe• Managing more than 590,000 Mts warehousing space in Rajasthan & Gujarat• Overseas subsidiaries to focus more on international markets

V I S I O NEye on the future

88

D I R E C T O R S ’ R E P O R T

TO,

THE MEMBERS,Your Directors have the pleasure to present the 29th ANNUAL REPORT on the business and operations of your company together with the Audited Statement of Accounts for the year ended March 31, 2010.

F I N A N C I A L R E S U L T S 2 0 0 9 - 2 0 1 0 2 0 0 8 - 2 0 0 9 (Rs. in billion) (Rs.in billion)

Total Revenue 26.78 19.45

Profit before Depreciation 2.66 1.48

Less: Depreciation 0.38 0.27

Profit before Taxation 2.28 1.21

Less: Provision for Taxation including Fringe Benefit Tax 0.56 0.23

Less: Provision for deferred Taxation 0.01 0.03

Net Profit after Taxation 1.71 0.95

Add: Surplus brought forward from previous year 3.76 3.19

Profit available for appropriation: 5.47 4.14

A P P R O P R I A T I O N S :

Transfer to General Reserve 0.25 0.12

Transfer to Debenture Redemption Reserve 0.09 0.03

Proposed Dividend on Equity Shares 0.23 0.20

Corporate Tax on Proposed Dividend 0.03 0.03

Balance carried to Balance Sheet 4.87 3.76

5.47 4.14

9 9

D I R E C T O R S ’ R E P O R T

Your company has an order book of over Rs. 50 billion excluding fairly placed bills.

S U B S I D I A R I E SJMC Projects (India) Ltd. And its subsidiary (JMC):JMC has reported consolidated revenue of Rs. 13.13.billion (USD 291 million) as against Rs.13.12 billion (USD 180 million) in corresponding period. Profit before tax as well as profit after tax stood at Rs. 531 million and Rs. 396 million as against Rs. 520 million and Rs. 368 million respectively. Abandonment of the major NHAI road project by the client and delay in commencement of few power projects were the bottlenecks in achieving desired growth during the year.

JMC has also received its first DBFOT basis project in consortium for Four Laning of Rohtak to Bawal of NH-71 of 83 kms from NHAI.

JMC has an order book exceeding Rs.26.71 billion (USD 663 million). Your company has strengthened JMC in terms of its capital base and business profile (through diversification) and improved financial discipline which will enable the company to achieve rapid growth. The company has invested Rs.942 million in JMC and holds 53.01% stake in JMC.

Shree Shubham Logistics Ltd (SSLL):In reporting period, SSLL has achieved a turnover of Rs884 million as against Rs.560 million in corresponding period, registering a growth of 58%.SSLL reported loss of Rs. 53 million as against profit of Rs 3.6 million in the corresponding period on account of delay in operation at all warehousing facilities and interest expenses.

SSLL has made significant progess during the reportingperiod on following count:

• All own logistic parks are operational with capacity of above 189,000 metric tons.

• Majority of logistic parks are accredited by NCDEX

• Strategic tie up with Rajasthan Ware Housing Corporation Ltd. to run their 38 warehouses having capacity of more than 405000 Metric Tons.

• Tied up with banks as collateral manager and service provider to expand the base amongst the farmers and trading community

D I V I D E N D Your Directors are also pleased to recommend payment of dividend for the year ended March 31, 2010 @ Rs. 7.50 per equity share of Rs. 10 each on increased equity share capital of 30,692,114 Equity shares on account of allotment of 4,192,114 Equity shares to Qualified Institutional Buyers on May 6, 2010 underSEBI (ICDR) Regulation, 2009.

F I N A N C I A L & O P E R A T I O N S R E V I E WYour company’s strong order book and executioncapabilities can be visualize by noticing an overall strong growth in terms of turnover and profitability. The gross revenue of the Company grew by 38% to Rs. 26.78 billion (USD 593 million) as against Rs. 19.45 billion (USD 431 million) in the previous year. Total Export Turnover (including overseas projects) was Rs. 11.58 billion (USD 256 million) or approx 43% of revenues in 2009-10 as against Rs. 5.19 billion (USD 102 million) in 2008-09.

The company reported growth of 89% in profit before tax of Rs. 2.28 billion in 2009-10 as against Rs. 1.21 billion in 2008-09 on account of better management of material, project and working capital during the year.

Your company has supplied 1,20,760 MTs of Transmission Line Towers as against 89,477 MTs in preceding year, which is higher by 35%.

Your Company has successfully raised Rs. 4.50 billion by issue of further 4,192,114 Equity shares of Rs. 10 each at price of Rs. 1074.20 per shares to Qualified Financial Institutions on May 6, 2010 under Chapter VIII of SEBI (ICDR) Regulation, 2009. The funds shall be used for capital expenditure, expansion of manufacturing capacity (transmission line towers), long-term investment in PPP, BOT, BOOT and BOOM projects, development of EPC services, further investment in existing divisions and subsidiaries and working capital purposes.

Your Company has secured its first Independent Power Transmission Company (IPTC) project inconsortium for Haryana Vidyut Prasaran Nigam Ltd. to undertake development and operation / maintenance of the 100 kms 400 kV / 220 kV transmission system project through Public Private Partnership on Design, Build, Finance, Operate and Transfer basis for the evacuation of electricity from the 2 x 660 MW thermal power plant at Jhajjar, Haryana.

1010

D I R E C T O R S ’ R E P O R T

is a Joint Venture between your company and a local company named as PDNA Industries (Pty) Ltd. who are 25.1% stakeholder in this company. Your company made an initial investment of Rs. 4.9 million towards equitycapital and other expenses.

Kalpataru Power Transmission Nigeria Ltd.:This Company was incorporated as a 100% subsidiary of your Company to explore the Power Transmission market in Nigeria.

Kalpataru Power Transmission (Mauritius) Ltd.:

This company is a 100% subsidiary in which your company has invested Rs. 1.1 million as capital and loan.

Kalpataru Power Transmission-USA, INC. This company was incorporated as a 100% subsidiary of your company during the year to increase its focus on American markets with local presence. Yourcompany has invested Rs. 9.3 million as capital and loan in this company.

During reporting period, all the above stated overseas subsidiaries are yet to commence business activities.

S T A T E M E N T O F D I R E C T O R S ’ R E S P O N S I B I L I T YPursuant to requirement under Section 217(2AA) of the Companies Act, 1956, Directors based on representationsreceived from Operating Management, confirm:

(i) That in the preparation of the annual accounts for the financial year ended March 31, 2010, the applicable accounting standards had been followed;

(ii) That Directors had selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the company at the end of the financial year and of the profit of the company for the year;

(iii) That the Directors had taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of the Companies Act, 1956 for safeguarding the assets of the company and for preventing and detecting fraud and other irregularities;

(iv) That the Directors had prepared the annual

At the year end, investment of your company in SSLL was Rs. 776 million as equity shares, preference share capital and loan. SSLL is an 80% Subsidiary of your company.

Energylink (India) Ltd (ELL):ELL plans to foray in to construction of commercial complexes and integrated township targeting middle and upper middle class income households. ELL has also entered into MOU, for setting up a Multi Product SEZ with Government of Gujarat during “Vibrant Gujarat”, an Investors Meet for Infrastructure development and is in the process of acquiring land near Ahmadabad for the same. During the year company has acquired 100% stake in Saicharan Properties Limited which is in process of implementing commercial cum retail project in Indore.

At the year end, investment of your company in ELL was Rs.1.28 billion as capital and loan. ELL is a Wholly Owned Subsidiary of your company.

Amber Real Estate Ltd. (Amber):Amber is in process of creating approx. 392,000 sq. feet leasing space for IT/Software Technology park at Thane, Mumbai is expected to be completed by Dec., 2011. At year end, investment of your company in Amber was Rs. 192 million as capital & loan and it is a Wholly Owned Subsidiary of your company.

Saicharan Properties Ltd, 100% Subsidiary of Energylink (India) Ltd.(SAI):SAI is proposing a commercial cum retail project in the heart of city of Indore where it has approximately 12600 sq. meter of free hold land. The project is expected to be completed by March 2013. At the year end, investment of your company in Saicharan was Rs. 1.25 billion as capital and loan through ELL.

Adeshwar Infrabuild Ltd., (Adeshwar):Adeshwar was incorporated during the year as wholly owned subsidiary to venture into new areas of business which can be conveniently or advantageously run by company in the coming year which may include mining, cement, solar power, etc. At the year end, investment of your company in Adeshwar was Rs. 5 million as capital in this company. It is Wholly Owned Subsidiary of your company.

Kalpataru SA (Proprietary) Ltd.:This Company was formed in South Africa to bid for EPC Power Transmission jobs in South Africa. This

11 11

D I R E C T O R S ’ R E P O R T

re-appointment. Auditors comments on your company’s accounts for year ended March 31, 2010 are self explanatory in nature and do not require any explanation as per provisions of Section 217(3) of the Companies Act, 1956.

P A R T I C U L A R S O F E M P L O Y E E SIn terms of provisions of Section 217(2A) of the Companies Act, 1956, read with the Companies (Particulars of Employees) Rules, 1975, as amended, names and other particulars of employees are required to be set out in Annexure to the Directors’ Report. However, as per provisions of Section 219(1)(b)(iv) of the said Act, the Annual Report excluding aforesaid information is being sent to all the Members of company and others entitled thereto. Members who are desirous of obtaining such particulars are requested to write to company.

C O N S E R V A T I O N O F E N E R G Y & T E C H N O L O G Y A B S O R P T I O N A N D F O R E I G N E X C H A N G E I N F L O W & O U T F L O WInformation required under Section 217(1)(e) of the Companies Act, 1956 is annexed hereto and forms part of this Report.

D E P O S I T SYour company has not accepted deposits from the public within provisions of Section 58-A and 58-AA of the Companies Act, 1956.

A C K N O W L E D G E M E N TYour Directors wish to place on record their gratitude to the shareholders of the Company, Banks, Financial Institutions, valued Customers, Suppliers, and Business Associates for their support and confidence in the Company.

Your Directors gratefully appreciate the co-operation and assistance extended by various Central and State Governmental Agencies. Your Directors also place on record their appreciation for overwhelming co-operation and assistance extended to your company by its employees.

On behalf of the Board of DirectorsMOFATRAJ P. MUNOTCHAIRMAN

Place: Mumbai Date: May 29, 2010

accounts for the financial year ended March 31, 2010 on a “going concern” basis.

C O R P O R A T E G O V E R N A N C EAs per Clause 49 of listing agreement with the Stock Exchanges, a separate section on Corporate Governance and Management Discussion and Analysis, confirming compliance is set out in Annexure forming part of this report.

Your company has been practicing principles of good corporate governance over the years. Your Board of Directors supports broad principles of corporate governance. In addition to basic governance issues, Board lays strong emphasis on transparency, accountability and integrity.

D I R E C T O R SIn accordance with provisions of the Companies Act, 1956 and the Articles of Association of your company, Mr. Mofatraj P Munot, Mr. Sajjanraj Mehta and Mr.Parag M. Munot are liable to retire by rotation at ensuing Annual General Meeting and being eligible they have offered themselves for re-appointment.

Mr. Shitin Desai, Independent Director, has resigned from his directorship w.e.f. May 10, 2010 due to hispreoccupation. The Board of Directors records itsappreciation for his valuable services rendered to your Company during his tenure.

C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

Your Directors have pleasure in attaching the Audited Consolidated Financial Statements pursuant to Listing Agreement entered into with the Stock Exchanges and prepared in accordance with Accounting Standards prescribed by the Institute of Chartered Accountants of India.

A U D I T O R S A N D A U D I T O R S ’ R E P O R TBoard of Directors have recommended appointment of M/s. Kishan M. Mehta & Co., Chartered Accountants and M/s. Deloitte Haskins & Sells, Chartered Accountants as auditors of your company who retire at the conclusion of forthcoming Annual General Meeting and are eligible for re-appointment.

M/s. Kishan M. Mehta & Co., Chartered Accountants and M/s. Deloitte Haskins & Sells, Chartered Accountants have given their consent to act as auditors, if re-appointed. Members are requested to consider their

1212

A N N E X U R E T O D I R E C T O R S ’ R E P O R T

Biomass Energy DivisionFollowing measures taken by your company from time to time has helped us in maintaining the auxiliary consumption at optimum level.

1. Use of Energy Efficient Motors for all auxiliaries of the plant has helped in reduction in Auxiliary consumption.

2. High capacity motors like Boiler Feed Pump Motor have been provided with Soft Starters (Electronic Starters) to conserve energy.

3. Variable Frequency Drives (VFD’s) have been provided for majority of continuous running auxiliaries which helps in conserving energy.

B . T E C H N O L O G Y A B S O R P T I O N :We have not imported or used any special technology which fall under this disclosure.

C . F O R E I G N E X C H A N G E E A R N I N G S

A N D O U T G O : ( R S . I N B I L L I O N )

Foreign exchange earnings Rs. 9.22(including overseas projects)

Foreign exchange outgo Rs. 6.41(including overseas projects)

A . C O N S E R V A T I O N O F E N E R G Y :Transmission & Distribution DivisionFollowing measures taken by your Company from time to time has helped us maintaining energy consumption at optimum level:

1. Use of Voltage Stabilizer to regulate fluctuations in voltage of the Ahmedabad Electricity Company supply, which helps to reduce energy consumption and eliminates wastage.

2. Installed enough number of Capacitors at Electrical Control Panel Boards to improve the overall power factor.

3. Implementation of recommendations made by the National Productivity Council while conducting energy audit.

4. Installed differential wound linear regulator, Automatic Voltage Controller with advanced technology for the energy saving.

5. Took PNG Connection, an environment friendly fuel, for galvanizing plant and hot bending machine to conserve the energy.

Our total energy cost is less than 1% of our totalturnover, which reflects success of your company’sefforts in this direction.

Information required under the Companies (Disclosure of Particulars in the Report of the Board of Directors) Rules, 1988.

R E P O R T

ur company from n maintaining the evel.

s for all auxiliaries duction in Auxiliary

Boiler Feed Pumpwith Soft Starters e energy.

VFD’s) have been ontinuous running ving energy.

P T I O N :y special technology

E A R N I N G S

L L I O N )

Rs. 9.22

Rs. 6.41

rd of

13 13

1414

A L L R O U N D S O L U T I O N S

P O W E R T R A N S M I S S I O N• Design Engineering Expertise with latest available technology• Testing facilities upto 1200 KV with helicopter simulation• Integrated Manufacturing with State-of the art CNC Machine with 108,000 Mts capacity and further to be increased to 138,000 Mts by 2011.• Supply management capabilities for on time delivery• Capable team of project execution and site management• Adequate construction equipments to carry out multiple jobs• Strong country management network to meet out country specific project execution requirement

P O W E R D I S T R I B U T I O N• Dedicated team of planning and supply management of executing project spread over longer distances in rural and urban areas with high quality standards• Dedicated site management team managing construction resources with due care of safety and quality.• A competent design team to design optimized distribution system for reduction in distribution losses.

O I L & G A S P I P E L I N E• Dedicated team of accredited fitters / welders capable of delivering quality project.• A dynamic project management site organisation to address complex construction challenges.

Staying ahead of the game requires one to have a presence in every conceivable direction. Providing a product or service is not enough. Kalpataru ensures integrated solutions from the creation of new designs, to their quality fabrication, project execution and commissioning.

• Adequate fleet of construction equipments for timely project completion.• 1,800 Kms of pipe laying work experience in all kind of terrain.

W A R E H O U S I N G & L O G I S T I C S• State of art ultra modern 12 Logistic park are operational with capacity of over 189,000 Mts.• Majority of logistics park are accredited by NCDEX• Managing 38 state owned warehouses of RSWC having capacity of over 405,000 Mts.

C I V I L C O N T R A C T I N G• Present in all sphere of EPC business in infra sector• Huge pool of construction Equipments• Presence across almost all states of India• Ability to execute projects on DBFOT basis

nt design team to design optimizedn system for reduction in distribution

S P I P E L I N Eteam of accredited fitters / weldersdelivering quality project.project management site organisation to

mplex construction challenges.

15 15

Chhattisgarh, Madhya Pradesh, Andhra Pradesh and Tamil Nadu. These corridors will have high-voltage lines i.e. 800 kV with the capacity to withstand variations of surge and decline in power transmission. They will help increase inter-regional power transfer capacity. India currently has an inter-regional power transfer capacity of 20,800MW, and PGCIL plans to increase it to 37,000 MW by 2012. This will require the strengthening of regional grids and building more inter-regional links.

The regional grids will be gradually integrated to form a national grid, whereby power in a region of surplus can be transferred to another, resulting in the optimal utilization of capacity generation. With the proposed addition of 16,630 MW, the total inter-regional transmission capacity is expected to be 37,200 MW by the end of the XIth FYP.

Thus the demand for engineering, procurement and construction services in the power transmission lines and power distribution businesses will continue to exist.

Private Investments in TransmissionIn 1998, the Central Government enacted the Electricity Laws (Amendment) Act, which recognized transmission as an independent activity (distinct from generation and distribution), and allowed private investment in the sector.

According to Government policy, the state transmission utilities (STUs, SEBs or their successor entities) and the central transmission utilities (CTU, PGCIL) will identify transmission projects for the intrastate and inter-state/inter-regional transmission of power respectively. The STUs and CTU will invite private companies to implement these projects through an IPTC or on a joint venture basis on BOOT, BOT, BOOM, BOO style.

DistributionTo further strengthen the pace of rural electrification and improving urban distribution and with an objective to electrify all villages and rural households and modernizetion in urban areas in five years, the Central Government launched Rajiv Ghandhi Grameen Vidyutikaran Yojna (“RGGVY”), APDRP and RAPDRP. These schemes aim to create rural electricity distribution backbone through providing for sub-stations, distributiontransformers and decentralized distribution generationsystem where grid supply is not feasible. The RGGVY scheme identified that 112,400 villages and over 56% of rural households were still to be electrified which required huge investment and also to help urban areas in better distribution of power.

Forward Looking Statement:

Company presents its performance for year 2009-10 andoutlook for future based on current Business environment which may vary due to future Economic, Political and other developments in India as well as overseas

E C O N O M I C S C E N A R I OThe growth of Gross domestic product (GDP) slowed from a four year average of 9% for the F.Y 2005-2008 to 6.7% for the year 2009 and expected to be 7.2% for the year 2009-10.

After unprecedented slow down in major economies around the world in mid September, 2008, the Indian economy is showing the sign of stabilization, largely led by Government spending and backed by strong domestic demand, rise in private consumption, investment, trade and positive capital inflow.

The continuous thrust on agriculture, power, infrastructure, urban & rural development and focus on inclusive growth will unlock much of the economy growth potential in the medium term. Keeping this in view, it is expected that the positive and forward looking budget 2010-2011 should provide a perfect platform of a return to the growth trajectory from which the global crisis had momentarily diverted India and will help in attaining projected growth rate of 8.2% and 9% in 2010-2011 and 2011-2012 respectively with an ambitious but achievable target of double digit growth of GDP.

O U T L O O K A N D O P P O R T U N I T I E STransmission And DistributionIndian Scenario As the Central Government plans to increase installed power generation capacity to 224,906 MW by 2012 from the present level of 157,229 MW, this would facilitate an expansion of the regional transmission network and inter-regional capacity to transmit power. Inter-regional transmission networks are required because powergeneration sources are unevenly distributed in India and power needs to be carried over large distances to areas where load centers and demand exist.

State-owned electricity transmission company Power Grid Corp. of India Ltd (PGCIL) plans to float tenders valued at around Rs. 640 billion in the 12th Five year plan for nine high-capacity corridors that will transmit power from new projects in Orissa, Sikkim, Jharkhand,

M A N A G E M E N T D I S C U S S I O N A N D A N A L Y S I S

1616

C I R C U M N A V I G A T I N G T H E G L O B E

9 C O U N T R I E SYear 1995 - 1999

1 9 C O U N T R I E SYear 2000 - 2005

2 8 C O U N T R I E SYear 2006 - 2010

One of the most remarkable chapters in Kalpataru’s story is its far reaching presence across the world. Already in 28 countries and showing no signs of slowing down, Kalpataru has its sights set clearly in all directions. Exploring new avenues and leaving its mark on new soil is just one reason why it is an all round winner.

16

17 17

petroleum, in absolute terms, is expected to be 195 million tons for the years 2011-12. Pipelines transport only 30% of the petroleum products consumed by Indian industry, in spite of being cheaper than railway, coastal tanker and road transportation which account for 40%, 12% and 18%, respectively.

R I S K , C O N C E R N S & T H R E A T SEach enterprise has its own risk and can’t remain isolated to the fullest extent except properly managing the risk. The Company foresees following areas of risk, concerns and threats:

• The Company is exposed to variation in prices of commodities, foreign exchange and interest rate.

• The project execution always largely depends upon skilled and unskilled manpower. Hence deployment, retention and competency growth of employees is also an area of concern.

• The Company is exposed to risk of delay in execution due to external factors like right of way, shortages of skilled/semi skilled manpower, etc.

• The Company business is exposed to unpredicted risk of changes in policies of Government and countries where it operates.

• Bio-mass Power Division is exposed to risk of availability and pricing of its critical fuel i.e agriculture residue/waste and availability of water in the area.

These risks are managed with proper mix of orders across various countries, timely and adequate hedgingof commodity and exchange exposure, optimizationof working capital limits and efficient inventorymanagement. The management keeps close watch on global developments and keeps on reviewing the risk and addresses the concerns for appropriate actions from time to time.

S E G M E N T - W I S E O P E R A T I O N A LP E R F O R M A N C ECompany has four primary business segments constituting Power Transmission & Distribution, Real Estate, Bio-mass Energy and Infrastructure.

Revenue of company can further be divided geographically in two different segments-sales within India and sales outside India considering location of customers. Out of

M A N A G E M E N T D I S C U S S I O N A N D A N A L Y S I S

Company is actively exploring the opportunitiesavailable in power distribution franchises which is beinginvited by State Utilities on competitive bidding basis. These opportunities on being successful will certainlyadd long term consistent revenue stream for the company.

InternationalAs a part of your company’s growth strategy, your company is actively looking at the international market including developed markets such as U.S. and Canada and new countries in CIS where there is need for system up gradation and/or new expansion.

The Company continues to seek growth from the above markets on account of huge investment planned by the countries in power transmission sector. To tap the opportunities in these regions, Company has already made local presence through its subsidiaries in USA, South Africa and Nigeria.

Looking to huge opportunities in transmission &distribution sector in India as well as overseas T&D industry is expected to witness robust order inflow on continuous basis for some time.

Oil and Gas Pipeline SectorThe strong growth of the Indian economy and infrastructure and the resulting increased demand in the energy industry has resulted in the need to develop an efficient distribution network for oil and natural gas transportation. The use of natural gas in the energy industry is also expected to increase significantly. The current low per capita usage of pipes in India, the discovery of large oil and gas reserves in various parts of India, the Central Government’s decision to permit oil retailing by the private sector and the national pipeline grid formulated by GAIL and infrastructure development projects of other major players in the energy industry in India are expected to increase engineering construction activity in the Indian energy sector.

The demand for and the supply of natural gas in India isalso expected to increase in the next several years. Increased demand for natural gas in India is also expected to result in the need for an extensive gas transportation pipeline infrastructure.

India’s regime permitting 100% foreign direct investment in exploration, refining, petroleum and gas pipelines and marketing is favorable for our business.

India is currently the third largest oil consumer in the Asia-Pacific region after China and Japan. Demand for

1818

D R O P S O F E X C E L L E N C E

P O W E R T R A N S M I S S I O N• Successfully tested 1200 KV tower at our testing station• Secured large value contract of Rs.12 billion from MSETCL • Successfully tested over 200 towers at our testing station• Over 5,900 Foundations in year 2009-10• Over 1,500 Kms of Stringing in year 2009-10• 15,000+Mts power transmission towers supplied to USA• Secured orders above Rs. 20 billion from SEBs/ Private Parties• Repeat orders from clients in Algeria, Abu Dhabi & Philippines• Successfully strung special kind of conductors to with stand in temperature upto 210° for a client in middle east

P O W E R D I S T R I B U T I O N• More than 6,500 transformers erected• More than 500 Feeders completed• More than 9,000 circuit kms of conductor stringing

O I L & G A S P I P E L I N E• Completion of 1st 48” Pipeline Project• Entry into city gas distribution • Successfully completed over 1,800 Kms of pipe laying work in India

W A R E H O U S I N G & L O G I S T I C S• All 12 logistics park are operational• MOU with Govt. of Rajasthan to operate their 38 warehouses with 405,000 Mts of capacity• Majority of owned Logistic park are accredited by NCDEX• Spot Exchange and auction platform facilities to arrange best prices to farmers / traders• Quality testing and certification services• Collateral management services

J M C P R O J E C T S ( I N D I A ) L T D .• Significant growth in order book to Rs. 26.70 billion• Focus on power plant civil construction, presently executing civil work for more than 10,000 MW of power plants• Three stadiums for the Common Wealth Games in Delhi• Secured Bangalore metro rail project

In the vast expanse of Kalpataru Infrastructure, we have made it mandatory to always surpass expectations and keep the bar high. Aiming higher ensures sand is turned to pearls. Creating something we can be proud of and better each time.

18

19 19

Infrastructure DivisionDuring reporting period, Division has completed and commissioned pipe laying of Vijaipur Dadri Pipeline Project of Gail India Limited and Chennai Bangalore Pipeline Project of Indian Oil Corporation Limited. So far Company has successfully completed pipe laying work of over 1,800 Kms.

In the previous year, Division has booked a revenue of Rs.3.61 billion as against Rs.1.72 billion in corresponding period.

The division is presently executing a prestigious pipeline job of 48”/30”/28”, 544 Kms Mundra Bhatinda Pipeline project for HPCL-Mittal JV, apart from small jobs for other clients. Division has secured its first city gas distribution order from Gail Gas Ltd for the city of Kota to gain experience in this area as the India has great potential for gas distribution.

After the wholesome domestic experience, division is appropriately considering the overseas opportunities and have been getting pre qualification criteria cleared to bid for these jobs. The required business development team is in place to ensure that we achieve this at earliest.

F I N A N C I A L R E V I E WNet sales and service revenue of the company for 2009-10 was at Rs.25.97 billion. This represents a growth of 38% over 2008-09. Revenue of Power Transmission and Distribution segment grew by 31%, Infrastructure segment grew by110% and Bio-mass Energy segment grew by 6.25%.

Exports revenue (including overseas projects) earnings during this year were at Rs. 11.58 billion representing approx. 45% of your company’s gross revenue.

Company’s profit before tax has increased to Rs. 2.28 billion from Rs. 1.21 billion. Profit after tax stood at Rs. 1.71 billion as against Rs. 0.95 billion. Increase in profit is attributable to increase in turnover, favorable commodity & forex market condition and improved working capital management.

Net fixed assets (including capital work in progress) as at March 31, 2010 was Rs. 3.38 billion as compared toRs. 2.68 billion in previous year, indicating increase ofRs. 0.7 billion, mainly for addition in execution related equipments and tools at domestic and international T&D sites to meet increased construction volume, purchase of pipe laying equipments for Infrastructure

M A N A G E M E N T D I S C U S S I O N A N D A N A L Y S I S

total revenue (Net of Excise Duty) of Rs. 25.97 billion of the Company, revenue within India is 14.39 billion (55%) and outside India is Rs. 11.58 billion (45%).

Transmission & Distribution Division (T & D)Division’s revenue was higher by 31% at Rs. 21.85 billion.

The largest international contract of Company withMEW, Kuwait is progressing well and expected to be over during the current financial year. The Company has also received a domestic large value contract for MSTCL worth Rs. 12 billion for laying power transmission and sub-station line for them. Company has successfully received repeated orders from Algeria, Philippines and UAE.

Most of the rural distribution projects have been successfully completed and the balance are on the verge of completion during the year including GFSS-II project and inflows from these projects will help to improve our working capital.

Company has successfully tested its first 1200 KVpower transmission tower during the year and alsosecured supply order for the same from PGCIL.

The Company is able to achieve this growth on account of its ability to focus on right order mix, expanded geographical reach, improve productivity and optimizing cost in all its activities.

Real Estate DivisionThere has been no major activity in this division during the year 2008-09.

Bio-mass Energy DivisionCompany’s two power generation plants of 7.8MW each at Sri Ganganagar and Tonk District of Rajasthan, generating power from non conventional energy resources i.e. using agricultural waste as fuel, registered a revenue of Rs. 508 million as against Rs. 476 million in corresponding period showing growth of 6.25% over last year. Both plants have run at 97% PLF (excluding shut down) and generated 118 million units out of which 108 million units were exported. Generated power is being sold to RVVNL and company also has option to sell it to private parties under PPAs. Due to water scarcity in the region, Tonk plant was shut in the month of April,10 and expected to be operational again in the month of July, 2010.

2020

W H E E L S O F C H A N G E

222220222222200000002020002022222222222200202020000000022222222222202000000002222222222222202020000200000222222222220000002222222222220000022222222200020002222222222002222222220200020222222200222222200022222220000222222202200022222222200000222222000022222220000222220000022222220000002222222220022222200000

E R P S O L U T I O N S

• Integration of all processes across organization name

› Production & Planning

› Projects & Execution

› Procurement & Inventory

› Finance & Risk Management

R A T I N G S

• Rated by CRISIL & CARE in India

• Business rating by Dun & Bradstreet

O I L & G A S P I P E L I N E S

• Enrty into city gas distribution work

Q U A L I T Y C E R T I F I C A T I O N

• ISO 9001:2008 for Main Plan & Infrastructure Division

• ISO 14001:2004 for EOU Division

• ISO 9001:2008 for EOU Division & DMS Division

S A F E T Y

• Received runner-up safety award from Gujarat safety council for EOU plant

A well oiled operation can only run smoothly if its core is constantly tuned and improved upon. Dynaic and ever evolving systems and processes are a necessity to maintain a perfect engine. We are perennially working to better ourselves and keep the accolades pouring in. Quality comes first and that shows through all ourendeavours, big or small.

20

21 21

C O R P O R A T E S O C I A L R E S P O N S I B I L I T YSafetyCompany gives utmost importance to safety standards at all working locations of company. At manufacturing units, power plants and all project sites, necessary procedures are in place to ensure safety of personnel and equipments. Specially to ensure safety and health of work force and create awareness, company undertakes the following activities.

a. Internal safety audits

b. Safety week celebration to create awareness about safety

c. Mock drills are conducted to access emergency / disaster management preparedness, etc.

EnvironmentPreservation and promotion of environment is of fundamental concern in all our business activities. Company has installed flux regeneration plant, acid and white fume extractors, eco-ventilator fans, etc at its manufacturing facilities to maintain good working condition and to make it more environmental friendly. As specific requirement of customer, Company has started fumigation of its export supplies, dull finishing of products to avoid reflection when it is installed at site, etc. Company does a lot of plantation and green area development for GIDC and GUDA.

Company has been accredited with ISO 14001 for Environment Management Systems by Intertek Quality Registrar, PLC, U.K., for its EOU Division.

Community DevelopmentCompany exhibits concern for society in order to be good corporate citizen, undertakes various community welfare measures and environment friendly initiatives.Primary focus of social welfare and community development measures of your company is focused on healthcare, child development and promoting cultural activities.

Company undertakes community development programmes by way of sponsoring the programme of government and non-government organizations like Rotary Club of Gandhinagar, Gandhinagar Cultural Forum, Kalrav etc. in field of healthcare, child development programme, cultural activities, women empowerment programme etc. Company also donated

M A N A G E M E N T D I S C U S S I O N A N D A N A L Y S I S

Division and purchase of additional land and building in Gandhinagar to meet our increased storage and administrative requirement.

Net current assets as at March 31, 2010 saw an insignificant increase to Rs. 11.68 billion as against Rs. 11.09 billion over previous year. Current assets level of company were managed at same level inspiteof 38% of growth on account of better working capital management. The focused efforts on realization from rural distribution jobs have also helped us in managing current assets levels. Thus Bank working capital limits utilization was almost at the same level as the previous year.

During this year, company has issued 9.55% Non-Convertible Debentures (NCD) of Rs. 0.7 billion for ongoing capex.

The total Debt/Equity ratio is at 0.60 and Long Term Debt/Equity ratio is at 0.18. Company enjoys PR1 + and AA rating for its short term and long term borrowing from CARE Ltd.

The operating cash flow of the company stood at Rs. 4.16 billion as against the negative operating cash flow of Rs. 1.59 billion during the previous year.

Internal ControlCompany has an adequate systems of internal controls implemented by management towards achieving efficiency in operation, optimum utilization of company’s resources and effective monitoring thereof and compli-ance with applicable laws and regulations.

Company’s internal audit department and independent Internal Auditors conduct regular audits to ensure adequacy of internal control systems, adherence to management instructions and compliance with laws and regulations of the country as well as to suggest improvements.

Audit plans, internal/external auditors’ observations and recommendations, significant risk areas assessments and adequacy of internal controls are also periodically reviewed by Audit Committee.

Company has across the board implemented global ERP system-SAP, to have better internal control systems and flow of information.

Company has adhered to stringent rules and regulations of ISO guideline also.

222222

S H E L T E R I N G O U R W O R L D

• W E L F A R E T R U S T

• C O R P O R A T E T O U R N A M E N T S I N A I D O F V A R I O U S N G O ’ S

• B L O O D D O N A T I O N C A M P S

• D I S P E N S A R Y

• Y O U T H / W O M E N E M P O W E R M E N T P R O G R A M M E

• P R O M O T I N G C U L T U R A L A C T I V I T I E S

• T R E E P L A N T A T I O N C A M P

• H E A L T H C A M P S

• C A R B O N E M I S S I O N R E D U C T I O N

A business can only call itself a true powerhouse when it extends its growth into every nuance of development. And this includes sustaining and developing our society. Propagating the importance of renewable development andenvironment protection for future generations is our promise and responsibility.

23 23

M A N A G E M E N T D I S C U S S I O N A N D A N A L Y S I S

Cautionary StatementStatement in the Management Discussion and Analysis describing the Company’s objectives, expectations or predictions may be forwarded looking within the meaning of applicable securities, law and regulations.The Company assumes no responsibility to publicly amend, modify or revise forward looking statement, on the basis of subsequent event or development. Actual results may differ materially from those expressed in the statement. Important factors that cloud infl uence the Company’s operations affecting selling price of fi nishedgoods, input availability and price, changes in government regulations, tax laws, economic development within the country and outside the country and other factors such as litigation and industrial relations.

a vehicle to Akhshya Patra, a foundation to provide food to under privileged children of the Gandhinagar district.

Company is very much committed to improving quality of life in communities in which it operates and to contribute the overall development of society.

As a part of its social responsibility, your company has opened KALPA-SEVA AROGYA KENDRA, a multi specialty dispensary with ultra modern facilities and latest equipments in its Pathological Lab, which will be helpful to cater the medical needs of the people in and around Gandhinagar at a very nominal fee. The Company has organized camp for artificial limb for physically handicapped people.

Human Resource“Making People Our Most Important &Valuable Asset” – Success of a business is directly linked to performance of those who work for that business. Now, properly managing a workforce is a lot more complicated than, maintenance of a company’s material capital such as machinery, computer systems, etc. Indeed, mechanistic approach to employee relations has often failed. Fortunately, this failure has prompted close study into how to effectively see that human capital is treated right and is able to reach its full potential.

Employee loyalty continued and succeeded in retaining the talent while adding 500 + new family members. Employees Welfare Trust is operational and needy people were supported.

At Kalpa-Vriksha Learning Centre, we make sure that freshers abilities are correctly and optimally nurtured and their competencies are enhanced, through a rigorous 35-day induction program. A demo area - a virtual site - has been created to give them the practical knowledge before they go to the site. We also take care to improve their behavioural aspects such as personality development, communication skills etc. We also provide a platform to our employees to upgrade their competencies, knowledge, skills and attitudes through various courses.

We continue to conduct programmes for our employees and their families like camps for kids, sports for family and employee. Annual Day celebration, rewarding long service associates, arranging picnics, gathering and involving each employees etc. Medical check-up for employees is being done periodically.

2424

T H E C O R E

R E C R U I T M E N T• Over 800 technical persons recruited in the last 5 years

T R A I N I N G H O U R S• In house training of more than 50,000 hours imparted to employees in the last 3 years.

T R A I N I N G C E N T R E S• Kalpa-Vriksha 1,20,000 sq. feet dedicated state of the art learning centre

Our most treasured asset has to be our unfailing work force that excels as a team. Nurturing their professional and personal growth is part and parcel of the Kalpataru ethic. We look at how a day to day job can develop into a rewarding career for every single family member here. The end result is sheer excellence.

24

T R A I N I N G C E N T R E S• Kalpa-Vriksha 1,20,000 sq. feet dedicated state of

the art learning centre

S P E C I A L I S E D E D U C A T I O N• Sponspored management courses in IIM, ISB & Kellogg’s Management Institute

K A L P A T A R U P A R I V A A R• 1233 qualified Technicians• 1638 qualified Managers

W O R K F O R C E• > 5,000 people

25

F I N A N C I A L H I G H L I G H T S

2005-06 2005-06 2006-07 2007-08 2008-09 2009-10 2009-10

RS. IN BILLION USD IN MILLION

• Production in MTs 62,452 78,404 79,531 93,484 * 121,483 * 121,483

• Gross Revenue 8.71 15.67 17.68 19.14 26.43 585.49

• Sales Growth 53.7% 79.9% 12.8% 8.2% 38.1% 38.1%

• International Revenue 1.43 4.01 5.01 5.19 11.58 256.54

• Total Expenditure 7.57 13.18 15.27 17.28 23.22 514.42

• Operating Profit (PBDIT & other income) 1.14 2.49 2.42 1.86 3.21 71.07

• Other Income 0.05 0.12 0.21 0.31 0.35 7.68

• Interest 0.16 0.28 0.40 0.68 0.90 19.85

• Profit before depreciation & tax (PBDT) 1.03 2.33 2.23 1.48 2.66 58.89

• Depreciation 0.09 0.17 0.22 0.27 0.38 8.47

• Profit before Tax 0.94 2.17 2.02 1.21 2.28 50.42

• Provision for Taxation (Incl. FBT & Deferred Tax) 0.28 0.57 0.52 0.26 0.57 12.66

• Profit after Tax (PAT) 0.67 1.59 1.50 0.94 1.70 37.76

• Equity Share Capital 0.11 0.27 0.27 0.27 0.27 5.87

• Net Wor th (excluding Revaluation Reser ve & Debenture Redemption Reser ve) 1.67 6.42 7.67 8.33 9.76 216.24

• Total Borrowings 2.33 3.37 3.26 6.54 6.04 133.88

• Capital Employed (Net Wor th + Term Borrowings) 2.66 7.29 8.38 9.68 11.57 256.33

• Debt Equity Ratio 1.39:1 0.52:1 0.43:1 0.79:1 0.62:1 0.62:1

• Debt Equity Ratio (Long Term) 0.59:1 0.14:1 0.09:1 0.16:1 0.19:1 0.19:1

• Book Value Per Equity Share (Rs) (excluding revaluation Reser ve & Debenture Redemption Reser ve) 153.93 242.18 289.52 314.51 368.34 8.16

• Earning per Equity Share (Rs.) 61.26 65.31 56.59 35.63 64.32 1.42

• Operating Profit 13.1% 15.9% 13.7% 9.7% 12.1% 12.1%

• Profit before Tax 10.8% 13.7% 11.3% 6.2% 8.5% 8.5%

• Profit after Tax 7.6% 10.1% 8.4% 4.9% 6.4% 6.4%

Consolidated**:

• Gross revenue NA 16.41 27.05 32.77 40.43 895.66

• Profit after Tax(PAT) NA 1.63 1.80 1.28 1.96 43.32

• Earning per equity share(Rs) NA 66.06 62.22 41.87 67.05 1.49

* The quantity includes production, on job work basis and purchased from/got processed from third par ties.

** Year since consolidation star ted 1 USD = Rs.45.14

26

REPORT ON CORPORATE GOVERNANCE

COMPANY’S PHILOSOPHY ON CORPORATE GOVERNANCE

Company’s philosophy of corporate governance steams from its belief from transparency, integrity and accountability towards all stock holders. Corporate Governance helps to achieve excellence to enhance stakeholders’ value by focusing on long-term stakeholder value creation without compromising on integrity, social obligations and regulatory compliances.

At Kalpataru Power, our continuous endeavor is to achieve good governance, by way of a conscious and conscientious eff ort whereby ensuring the truth, transparency, accountability and responsibility in all our dealings with our employees, stakeholders, consumers and the community at large.

Th e Board of Directors represents the interest of the Company’s stakeholders, for optimizing long-term value by way of providing necessary guidance and strategic vision to the Company. Th e Board also ensures that the Company’s management and employees operate with the highest degree of ethical standards.

We, at Kalpataru Power, believe that the constant eff ort to improve operational performance, guided by our values, forms the basis for good Corporate Governance. Corporate Governance is strongly driven by our values such as quality, commitment, customer orientation and integrity.

I. BOARD OF DIRECTORS

A. Composition of the Board

Th e Board of directors consists of 11 Directors as on March 31, 2010 of which 9 are Non-Executive and 2 are Executive Directors. Th e Chairman is a Non-Executive Promoter Director, apart from him there is 1 Promoter Director and 6 Non-Executive Independent Directors. Th e Board structure is in compliance with Clause 49 of the Listing Agreement.

B. Meetings of Board of Directors

5 Board Meetings were held during the year ended on March 31, 2010 and the gap between any two meetings did not exceed four months. Th e dates on which the Board Meetings were held are May 30, 2009, July 29, 2009, October 26, 2009, January 29, 2010 and February 22, 2010.

C. Directors’ attendance and Directorship held

Th e names and category of Directors on the Board, their attendance at the Board meetings held during the year and also at the last Annual General Meeting, the number of Directorships and Committee Memberships held by them in other companies are given below:

Name of the Directors Category Attendance at No of Directorships and Committee Memberships / Chairmanship (Other than KPTL)**

Board Meetings

Last AGM

Directorship# Committee Chairmanship

Committee Membership

Mr. Mofatraj P. Munot Non – Executive (Promoter) Chairman

5 Yes 101 - -

Mr. Pankaj Sachdeva Managing Director ( w.e.f. June 1, 2009)

Dy. Managing Director( till May 31, 2009)

4 Yes 1 - -

Mr. Parag M. Munot Non – Executive (Promoter)

4 No 110 - -

Mr. Manish Mohnot Executive Director 5 Yes 7 - -

Mr. Sajjanraj Mehta Non - Executive (Independent)

4 Yes 2 - -

Mr. Vimal Bhandari Non - Executive (Independent)

5 Yes 7 1 3

Mr. Shitin Desai Non - Executive (Independent)

3 No 5 - 2

Mr. Narayan Seshadri Non - Executive (Independent)

4 No 10 1 3

27

Name of the Directors Category Attendance at No of Directorships and Committee Memberships / Chairmanship (Other than KPTL)**

Board Meetings

Last AGM

Directorship# Committee Chairmanship

Committee Membership

Mr. Mahendra G. Punatar

Non – Executive(Independent)

(w.e.f. May 30, 2009)

4 Yes 1 - 2

Mr. K. V. Mani Non – Executive(w.e.f. June 1, 2009)Managing Director (upto May 31, 2009)

3 Yes - - -

Mr. S. P. Talwar Non - Executive (Independent)

3 No 12 2 -

Mr. Sanju Ahooja Non - Executive (Independent)

(up to May 31, 2009)

Nil No - - -

**Represent Memberships / Chairmanships of Audit Committee and Shareholders’ Grievance Committee only

# Including Private Limited Companies

None of the Directors of Board is a member of more than 10 Committees and no Director is the Chairman of more than 5 committees across all the companies in which he is a Director. Th e necessary disclosures regarding Committee positions have been made by all the Directors.

D. Code of Conduct

Th e Board has laid down code of conduct for all Board Members and Senior Managerial Personnel of the Company. Th e Code of Conduct is available on the website of the Company at www.kalpatarupower.com .

All Board Members and Senior Managerial Personnel have affi rmed compliance with the Code of Conduct and a declaration to this eff ect signed by the Chief Executive Offi cer (CEO) has been obtained.

II. Audit Committee:

Th e Company has complied with the requirements of Clause 49 (II) (A) of the Listing Agreement relating to composition of Audit Committee.

Th e terms of reference of the Audit Committee are broadly as under:

Oversight of the company’s fi nancial reporting process and the disclosure of its fi nancial information to ensure that the fi nancial statement is correct, suffi cient and credible.

Recommending to the Board, the appointment, re-appointment and, if required, the replacement or removal of the statutory auditor/s and the fi xation of audit fees.

Approval of payment to statutory auditors for any other services rendered by the statutory auditors.

Reviewing, with the management, the annual fi nancial statements before submission to the board for approval, with particular reference to:

• Matters required to be included in the Director’s Responsibility Statement to be included in the Board’s report in terms of clause (2AA) of section 217 of the Companies Act, 1956.

• Changes, if any, in accounting policies and practices and reasons for the same.

• Major accounting entries involving estimates based on the exercise of judgment by management.

• Signifi cant adjustments made in the fi nancial statements arising out of audit fi ndings.

• Compliance with listing and other legal requirements relating to fi nancial statements.

• Disclosure of any related party transactions.

• Qualifi cations in the draft audit report.

28

Reviewing, with the management, the quarterly fi nancial statements before submission to the board for approval.

Reviewing, with the management, performance of statutory and internal auditors and adequacy of the internal control systems.

Reviewing the adequacy of internal audit function, if any, including the structure of the internal audit department, staffi ng and seniority of the offi cial heading the department, reporting structure coverage and frequency of internal audit.

Discussion with internal auditors regarding any signifi cant fi ndings and follow up there on.

Reviewing the fi ndings of any internal investigations by the internal auditors into matters where there is suspected fraud or irregularity or a failure of internal control systems of a material nature and reporting the matter to the board.

Discussion with statutory auditors before the audit commences, about the nature and scope of audit as well as post-audit discussion to ascertain any area of concern.

To look into the reasons for substantial defaults in the payment to the depositors, debenture holders, shareholders (in case of non payment of declared dividends) and creditors.

Reviewing with the management, the statement of uses/application of funds raised through an issue ( public issue, right issue and preferential issue etc.), the statement of funds utilized for purposes other than those stated in the off er document/prospectus/notice and the report submitted by the monitoring agency monitoring the utilization of proceeds of a public or right issue and making appropriate recommendations to the Board to take up steps in the matter.

Approval of appointment of CFO ( i.e. the whole time Finance Director or any other person heading the fi nance function or discharging that function) after assessing the qualifi cations, experience & background etc. of the candidate.

Th e Audit Committee comprises of 4 Non-Executive Directors out of which 3 are independent directors. Th e Committee met 4 times during the year on May 29, 2009, July 29, 2009, October 26, 2009 and January 29, 2010 and the attendance of members at the meetings were as follows :

Name of Member Category Status No. of Meetings attended /held

Mr. Sajjanraj Mehta

Mr. Mofatraj P. Munot

Mr. Vimal Bhandari

Mr. Narayan K. Seshadri*

Non Executive-Independent

Non Executive-Promoter

Non Executive-Independent

Non Executive-Independent

Chairman

Member

Member

Member

3 / 4

4 / 4

4 / 4

2 / 2

* Mr Narayan K. Seshadri was inducted as member of audit committee on July 29, 2009.

Th e President & CFO is a regular invitee, Statutory & Internal Auditors are invited as and when required. Th e Company Secretary is the secretary of the committee.

Th e Audit Committee has reviewed fi nancial condition and results of operations forming part of the management discussion and analysis and other information as mentioned in para II (E) of Clause 49 of the Listing Agreement.

III. Subsidiary Company:

Th e company has the following subsidiaries:

1. JMC Projects (India) Ltd. (53.01% Subsidiary), Listed Company

2. JMC Mining & Quarries Ltd. (100% Subsidiary of JMC Projects (India) Ltd),

3. Energylink (India) Ltd. (100% Subsidiary),

4. Shree Shubham Logistics Ltd. (80% Subsidiary),

5. Amber Real Estate Ltd. (100% Subsidiary),

6. Kalpataru Power Transmission (Mauritius) Ltd. (100% Subsidiary),

7. Kalpataru SA (Proprietary) Ltd. (74.9% Subsidiary),

8. Kalpataru Power Transmission Nigeria Ltd. (100% Subsidiary),

9. Saicharan Properties Ltd. (100% Subsidiary of Energylink (India) Ltd),

29

10. Kalpataru Power Transmission USA INC. (100% Subsidiary) and

11. Adeshwar Infrabuild Ltd. (100% Subsidiary),

Except JMC Projects (India) Ltd., all other subsidiaries are non-material non listed subsidiaries of the Company. Th e review of annual fi nancial statement and investments, if any, made by these unlisted subsidiary companies is done by Audit Committee. Th e minutes of Board Meetings of unlisted subsidiary companies are being placed before the Board of Directors of the Company.

IV. Nomination and Compensation Committee:

Although non mandatory in terms of the listing agreement, the Company has Nomination & Compensation Committee to review, assess and recommend the appointment of executive directors from time to time, to periodically review the remuneration package of the executive directors and recommend suitable revision to the Board.

Remuneration of employees largely consists of base remuneration, perquisites and performance incentives. Th e Components of the total remuneration vary for diff erent cadres and are governed by industry pattern, qualifi cation and experience of the employee, responsibilities handled by him, individual performance etc.

Th e objectives of the remuneration policy are to motivate employees to excel in their performance, recognize their contribution, and retain talent in the organization and reward merit.

Th e Committee comprises of 3 Non-Executive Directors.

Th e Committee met on May 29, 2009 to determine the appointment/re-appointments of Executive Directors and revision of remuneration/promotion of top executives of the Company. Th e meeting was attended by following members of committee:

Name of Member Category Status No. of Meetings attended/held

Mr. Mofatraj P. Munot Non Executive-Promoter Chairman 1/1

Mr. Sajjanraj Mehta Non Executive-Independent Member 1/1

Mr. Vimal Bhandari Non Executive-Independent Member 1/1

Remuneration paid or payable to Directors for the year 2009-2010(Rs. In Lacs)

Name of Director Sitting Fees Commission Salary Contribution to PF

Perquisites Total

Mr. Pankaj Sachdeva# - 31.00 138.12 11.88 7.35 188.35

Mr. Manish Mohnot # - 80.00 96.00 8.16 0.55 184.71

Mr. K. V. Mani# 0.60 39.75 30.00 2.40 0.27 72.42

Mr. Mofatraj P. Munot 1.20 - - - - 1.20

Mr. M. G. Punatar 0.80 3.00 - - - 3.80

Mr. Parag M. Munot 0.80 - - - - 0.80

Mr. Sajjanraj Mehta 0.95 4.25 - - - 5.20

Mr. Vimal Bhandari 1.20 3.75 - - - 4.95

Mr. Shitin Desai 0.60 3.00 - - - 3.60

Mr. Narayan Seshadri 0.90 3.50 - - - 4.40

Mr. S. P. Talwar 0.40 3.00 - - - 3.40

# Mr. K. V. Mani till May 31, 2009 as Managing Director was entitled to 2.5% of the profi ts of the Company as commission which was Rs. 36.75 lacs and Rs. 3 lacs is payable in capacity as non executive director thereafter. In terms of agreement/appointment approved by members, commission/incentive to Mr. Pankaj Sachdeva, Managing Director & Mr. Manish Mohnot, Executive Director has been decided by Board of Directors on recommendation of Remuneration Committee.

30

Information of Directors as on March 31, 2010 is as under:

Name Age Designation Date of initial appointment

Nature of employment

Shares held

Mr. Mofatraj P. Munot. 65 Chairman 27.06.1989 1,964,186

Mr. K. V. Mani 66 Director 24.01.2001 Nil

Mr. Pankaj Sachdeva 48 Managing Director 09.07.2008 Contractual Nil