Embed Size (px)

Citation preview

Principles of Fundamental Analysis – Day 1

Professor Jacob Cohen

March 2016

2

Introduction – Jake Cohen

• Senior Associate Dean for Undergraduate and Master’s Programs and Senior Lecturer in the Accounting and Law groups

• Former faculty member and Dean of the MBA Program at INSEAD, Senior Teaching Fellow at Harvard Business School, Judge Fellow at University of Cambridge and Research Fellow in Oxford University’s Smith School of Enterprise and the Environment.

• Consulting work with Blackstone, BCG, SAP, Schlumberger, and others

3

Alignment in Action

4

Day 1 Content

• The Corporate Finance Model of the Firm

• The Financial Accounting Model of the Firm

• What is Risk?

• The Fundamental Finance Principle

5

INVESTORS

PROVIDE CAPITAL

MANAGERS

EMPLOY CAPITAL

FINANCIAL MARKETS

VALUE CAPITAL

The Value Loop

THE MARKET VALUE OF THE CAPITAL EMPLOYED

ACCRUES TO THE INVESTORS

MANAGERS MUST MAKE DECISIONS WHICH RAISE THE MARKET VALUE OF CAPITAL ABOVE THE

AMOUNT OF CAPITAL EMPLOYED. THE DIFFERENCE IS CALLED MARKET VALUE ADDED OR MVA:

MVA = Market Value of Capital (Owner’ equity + Debt) – Capital Employed

6

Value Creators & Destroyers in the U.S.

MARKET VALUE

OF CAPITAL

CAPITAL

EMPLOYED

MARKET VALUE

ADDED

US$ Billions

1. GENERAL ELECTRIC

343 97 +246

2. WAL-MART STORES 296 82 +214

3. MICROSOFT GROUP 225 24 +201

4. CITIGROUP INC. 267 133 +134

5. INTEL CORP. 163 31 +132

996. LUCENT TECHOLOGIES INC. 31 62 - 31

997. SBC COMMUNICATIONS INC. 114 151 - 37

998. TIME WARNER INC. 118 161 - 43

999. AT&T CORP. 36 88 - 52

1000. JDS UNIPHASE CORP. 5 70 - 65

12/31/03

7

Source: http://www.ge.com/sites/default/files/ge_pivot_simpler_more_valuable.pdf

8

Jeff Immelt: A simpler, more valuable GE Today, we announced an exciting and promising new chapter for GE, a plan to create a simpler, more valuable industrial company by reducing the size of our financial business. As a first step, we also announced agreements to sell the bulk of GE Capital Real Estate assets for a total value of approximately $26.5 billion.

As the senior management team and Board carefully considered this move, we asked ourselves some key questions: What is going on in the world? Is this the right time? Is this good for customers and investors? What will GE look like going forward?

Coming out of the financial crisis, financial markets have changed for a generation. GE Capital has solid businesses and a great team. However, the business model for large, wholesale-funded financial companies has changed, making it increasingly difficult to generate acceptable returns going forward.

This is a good time to move. Synchrony Financial’s successful IPO and other recent Capital business exits bolstered our confidence that our businesses will be more valuable outside of GE. The market is strong for the businesses we will sell, and I am confident they will thrive elsewhere.

We are also confident that creating a simpler GE will position us to deliver superior outcomes around our core capabilities. Every GE business – including the Capital aviation, healthcare and energy “vertical” financing businesses – will be part of the “GE Store” of technology, process tools and cultural strength. As we build the next industrial era, customer focus is more important than ever.

For investors, we anticipate our high-value industrials to generate more than 90% of our earnings by 2018. And, we expect to return more than $90 billion in cash to investors through dividends, share buybacks and the Synchrony exchange through the end of 2018.

GE today is a premier industrial company with businesses in high-growth industries. We are leaders in technology, well positioned in growth markets and delivering higher margins and lower costs. This transformation positions GE for long-term success as we pair our best-in-class industrials with financial businesses focused on growth.

I know I speak for all of GE and the Board when I say that we are proud of the Capital team, the outstanding businesses that Capital employees have built and how they have delivered for customers and shareholders over many years. The Capital team has displayed great resiliency, facing tough cycles and driving strong results.

This was a hard decision and a big change for GE. However, it is right for the company.

Jeff Immelt Chairman and CEO, GE

9

Market Value of Debt

The market value of debt is usually more difficult to obtain directly, since very few firms have all their debt in the form of bonds outstanding trading in the market.

Many firms have non-traded debt, such as bank debt, which is specified in book value terms but not market value terms.

Thus, for our purposes, we’ll assume that market value of debt is equal to the book value of debt.

10

THE INVESTORS

And what they get in return

THE SHAREHOLDERS

They get:

• Dividends

• Capital gains

THE DEBTHOLDERS

BONDHOLDERS

They get:

• Coupons

• Capital gains

LENDING INSTITUTIONS

They get:

• Interest payments

• Principal Repayment

Whose Money are the Companies Spending?

11

Credit Ratings

• Credit ratings are opinions about credit risk. Standard & Poor’s ratings express the agency’s opinion about the ability and willingness of an issuer, such as a corporation, to meet its financial obligations in full and on time.

• To form its ratings opinions, the credit analysis of a corporate issuer typically considers many financial and non-financial factors, including key performance indicators, economic, regulatory, and geopolitical influences, management and corporate governance attributes, and competitive position.

• For high-grade credit ratings, Standard & Poor’s considers the anticipated ups and downs of the business cycle, including industry-specific and broad economic factors. The length and effects of business cycles can vary greatly, however, making their impact on credit quality difficult to predict with precision.

Source: S&P

12

Credit Ratings Scale

Investm

en

t

Gra

de

Moody’s S&P

Aaa AAA Strongest

Weakest

No

n-

Inves

tmen

t

Gra

de

Aa1 AA+

Aa2 AA

Aa3 AA-

A1 A+

A2 A

A3 A-

Baa1 BBB+

Baa2 BBB

Baa3 BBB-

Ba1 BB+

Ba2 BB

Ba3 BB-

B1 B+

B2 B

B3 B-

Caa1 CCC+

Fitch

AAA

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

B

B-

CCC+

13

THE PRIMARY MARKET THE SECONDARY MARKET

New

Securities

Cash

THE FIRM INVESTORS Outstanding

Securities

Cash

INVESTORS INVESTORS

The Financial Markets

14

Stocks vs. Bonds Performance

$1

$21

$41

$61

$81

$101

$121

$141

$161

$181

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

Stocks (S&P 500)

T.Bills

T.Bonds

$180.24

$13.22

$32.50

Value of $1 invested in 1960

Source: http://www.stern.nyu.edu/~adamodar/New_Home_Page/data.html

15

Content

• The Corporate Finance Model of the Firm ‒ Is concerned with the investor perspective

‒ Focuses on the value impact of business decisions

‒ Is forward looking

• The Financial Accounting Model of the Firm

• What is Risk?

• The Fundamental Finance Principle

16

17

Financial Transactions

FINANCIAL ACCOUNTING PROCESS

BALANCE SHEET

THE FIRM THE REST OF

THE WORLD

INCOME STATEMENT

The Financial Accounting Database

The Red Bearded Baron Case

19

ASSETS

CURRENT ASSETS • Cash

• Accounts receivables

• Inventories

• Prepaid expenses

NONCURRENT ASSETS • Financial assets & intangibles

• Property, plant & equipment

• Gross value

• Accumulated depreciation

OWNERS’ EQUITY = ASSETS – LIABILITIES

ASSETS = LIABILITIES + OWNERS’ EQUITY

LIABILITIES & OWNERS’ EQUITY

CURRENT LIABILITIES • Short-term debt

• Owed to banks

• Current portion of long-term debt

• Accounts payable

• Accrued expenses

NONCURRENT LIABILITIES • Long-term debt

OWNERS’ EQUITY

The Balance Sheet

20

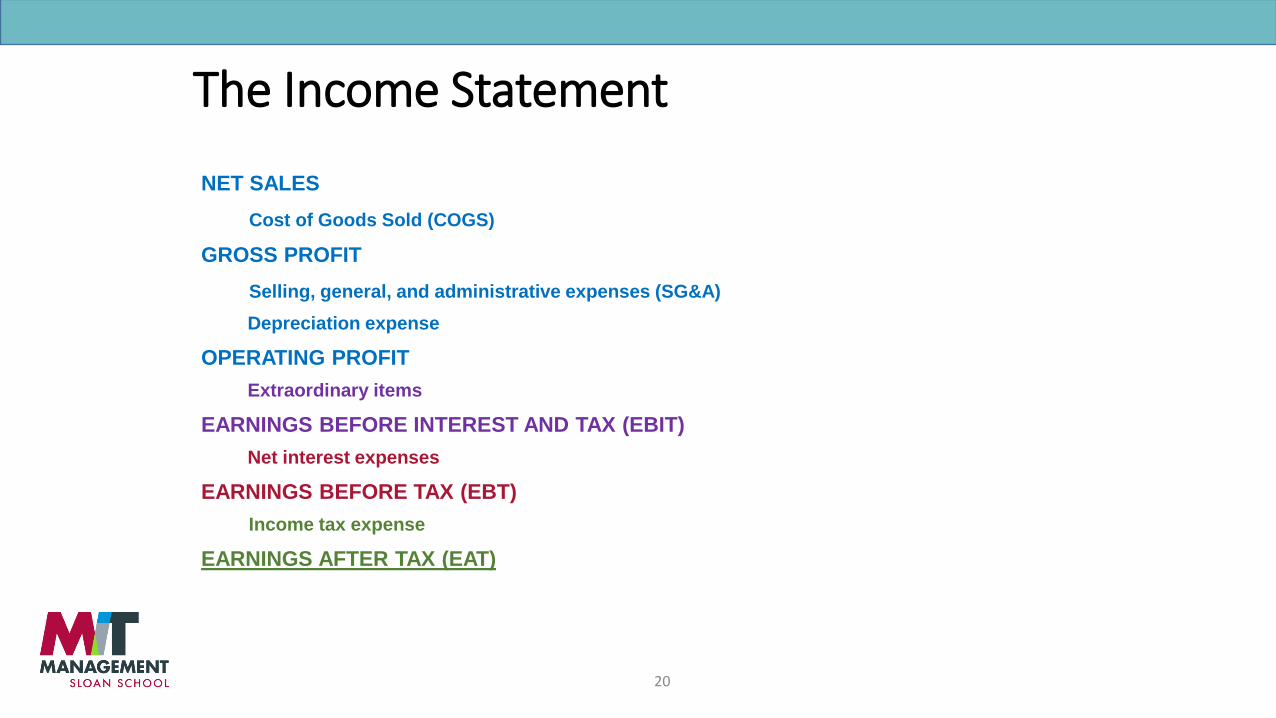

The Income Statement

NET SALES

Cost of Goods Sold (COGS)

GROSS PROFIT

Selling, general, and administrative expenses (SG&A)

Depreciation expense

OPERATING PROFIT

Extraordinary items

EARNINGS BEFORE INTEREST AND TAX (EBIT)

Net interest expenses

EARNINGS BEFORE TAX (EBT)

Income tax expense

EARNINGS AFTER TAX (EAT)

21

CHANGE IN OWNERS’ EQUITY

= EARNINGS AFTER TAX

– DIVIDENDS

+ $ RAISED BY NEW SHARE ISSUANCE

– $ PAID FOR SHARE REPURCHASE

Retained

earnings

The Statement of Retained Earnings

22

These accounts are not

financial accounts

ASSETS

CURRENT ASSETS • Cash

• Accounts receivables

• Inventories

• Prepaid expenses

NONCURRENT ASSETS • Financial assets & intangibles

• Property, plant & equipment

• Gross value

• Accumulated depreciation

LIABILITIES & OWNERS’ EQUITY

CURRENT LIABILITIES

NONCURRENT LIABILITIES • Long-term debt

OWNERS’ EQUITY

• Short-term debt

• Owed to banks

• Current portion of long-term debt

• Accounts payable

• Accrued expenses

The Balance Sheet: The BU’s View

23

THE FIRM’S INVESTMENTS THE ACCOUNTING ESTIMATES

INVESTMENT IN

FIXED ASSETS

NET

FIXED ASSETS

The Firm’s Investments

24

THE FIRM’S INVESTMENTS THE ACCOUNTING ESTIMATES

INVESTMENT IN

FIXED ASSETS

NET

FIXED ASSETS

The Firm’s Investments

INVESTMENT IN

CASH CASH

25

WORKING CAPITAL REQUIREMENT (WCR)

=

[RECEIVABLE’S + INVENTORIES + PREPAID EXPENSES]

– [PAYABLE’S + ACCRUED EXPENSES]

CASH

PROCUREMENT

SALES

PRODUCTION

The Working Capital Requirement (WCR)

26

27

THE FIRM’S INVESTMENTS THE ACCOUNTING ESTIMATES

INVESTMENT IN

FIXED ASSETS

NET

FIXED ASSETS

The Firm’s Investments

INVESTMENT IN

CASH CASH

INVESTMENT IN

THE OPERATING CYCLE

WORKING CAPITAL REQUIREMENT

WCR

28

CASH

WORKING CAPITAL

REQUIREMENT

NET FIXED ASSETS

SHORT-TERM

DEBT

LONG-TERM

DEBT

OWNER’S

EQUITY

INVESTED CAPITAL CAPITAL EMPLOYED

The Managerial Balance Sheet

29

Cash

Working Capital

Requirement

Net fixed assets

Short-Term

Debt

Long-Term

Debt

Owner’s

Equity

Invested Capital Capital Employed

Cash

Operating Assets

Net Fixed Assets

Short-Term

Debt

Long-Term

Debt

Owner’s

Equity

Assets Liabilities & Equity

Operating Liabilities

Accounting vs. Managerial Balance Sheet

30

Invested Capital

Debt

Owner’s Equity

Revenues

Expenses

Net Profit

Invested Capital

Debt

Owner’s Equity

DIVIDENDS

RETAINED EARNINGS

The Accounting Model of the Firm

31

Content

• The Corporate Finance Model of the Firm ‒ Is concerned with the investor perspective ‒ Focuses on the value impact of business decisions ‒ Is forward looking

• The Financial Accounting Model of the Firm ‒ Is concerned with transactions between the firm and the world ‒ A formidable database to analyze the firm’s strengths and weaknesses ‒ The managerial balance sheet: invested capital & capital employed ‒ Is backward looking

• What is Risk?

• The Fundamental Finance Principle

32

EXPECTED SALES DOWN 10%

SALES UP 10%

SALES $1,000 $900 -10% $1,100 +10%

less variable operating expenses (380) (342) -10% (418) +10%

less fixed operating expenses (380) (380) same (380) same

EBIT (Earnings before interest & tax) $240 178 -26% $302 +26%

less fixed interest expenses (40) (40) same (40) Same

EBT (Earnings before tax) $200 $138 -31% $262 +31%

less variable tax expenses (50%) (100) (69) -31% (131) +31%

EAT (Earnings after tax) $100 $69 -31% $131 +31%

RISK IS RELATED TO THE PROBABILITY OF NOT GETTING WHAT IS EXPECTED.

Risk

33

Economic, social & political conditions

Competitive position

+ 10%

- 10%

+ 26%

- 26%

+ 31%

- 31%

ECONOMIC RISK OPERATIONAL RISK

BUSINESS RISK FINANCIAL RISK

OPERATING

PROFIT

NET PROFIT SALES

Risk

34

Content

• The Corporate Finance Model of the Firm ‒ Is concerned with the investor perspective ‒ Focuses on the value impact of business decisions ‒ Is forward looking

• The Financial Accounting Model of the Firm ‒ Is concerned with transactions between the firm and the world ‒ A formidable database to analyze the firm’s strengths and weaknesses ‒ The managerial balance sheet: invested capital & capital employed ‒ Is backward looking

• What is Risk? ‒ Relevant risks are:

• Business risk • Financial risk

• The Fundamental Finance Principle

35

Glossary of Select Financial Terms

CAGR – Compound Annual Growth Rate. CAGR is the mean annual growth rate of an investment over a specified period of time. DCF – Discounted Cash Flow. DCF analysis uses future free cash flow projections and discounts them to arrive at a present value estimate, which is used to evaluate the potential for investment. EBIT – Earnings Before Interest and Taxes. EBIT is a measure of a firm’s profit that includes all operating income and expenses except interest and income tax. It is often also referred to as operating profit. EBITDA – Earnings Before Interest, Taxes, Depreciation and Amortization. EBITDA is used to analyze and compare profitability between companies and industries because it eliminates the effects of financing and accounting decisions. EV – Enterprise Value. EV is an economic measure reflecting the market value of a whole business. It is a sum of claims of all claimants: creditors (secured and unsecured) and equity holders (preferred and common). IRR – Internal Rate of Return. IRR is the interest rate at which the NPV of all the cash flows (both positive and negative) from a project or investment equal zero. Market Capitalization – the aggregate valuation of a company based on its current share price multiplied by the total number of shares outstanding. MVA – Market Value Added. MVA is the difference between the current market value of a firm and the capital contributed by investors. If MVA is positive, the firm has added value. If it is negative, the firm has destroyed value. NPV – Net Present Value. NPV is the difference between the present value of cash inflows and the present value of cash outflows. WACC – Weighted Average Cost of Capital. WACC is the rate that a company pays on average to all its security holders to finance its assets.