Embed Size (px)

Citation preview

Principles of Accounting, 4th edition1

The Journal and the Ledger

4

Principles of Accounting, 4th edition2 Principles of Accounting, 4th edition2

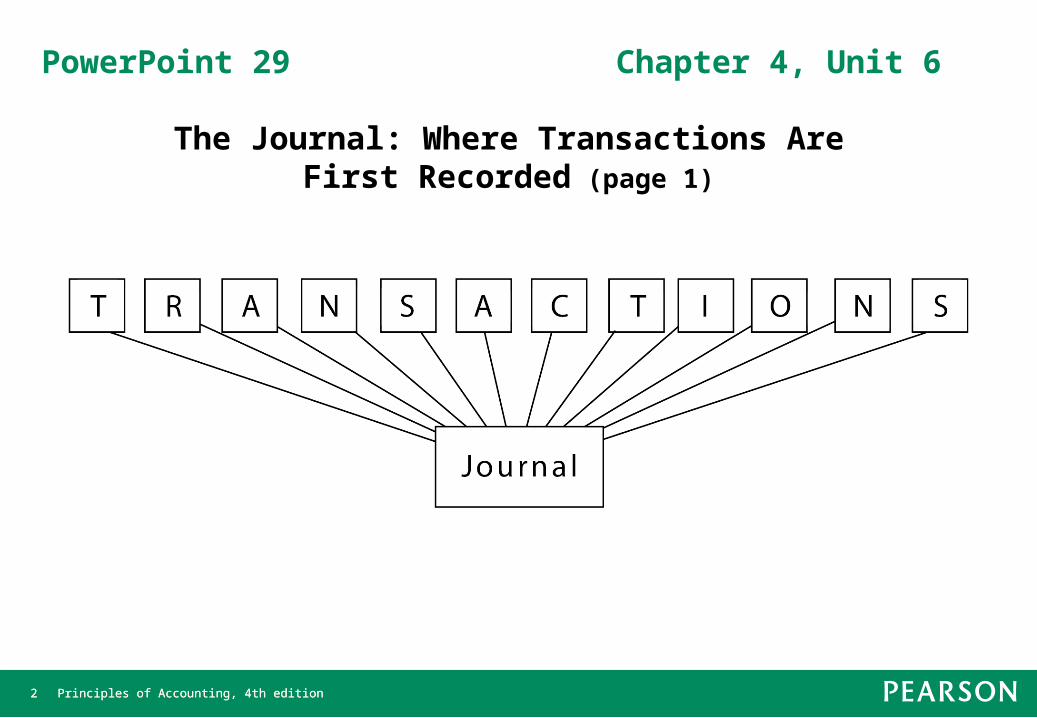

PowerPoint 29 Chapter 4, Unit 6

The Journal: Where Transactions Are First Recorded (page 1)

Principles of Accounting, 4th edition3 Principles of Accounting, 4th edition3

PowerPoint 29 Chapter 4, Unit 6

• Transactions are first recorded chronologically in the journal.

• The journal contains a complete record of each transaction: date,

account debited and amount, account credited and amount, and

explanation.

• Journals may be completed manually in the form of a book.

• Journals may be completed using a computer and take the form of a

computer file.

The Journal: Where Transactions Are First Recorded (page 2)

Principles of Accounting, 4th edition4 Principles of Accounting, 4th edition4

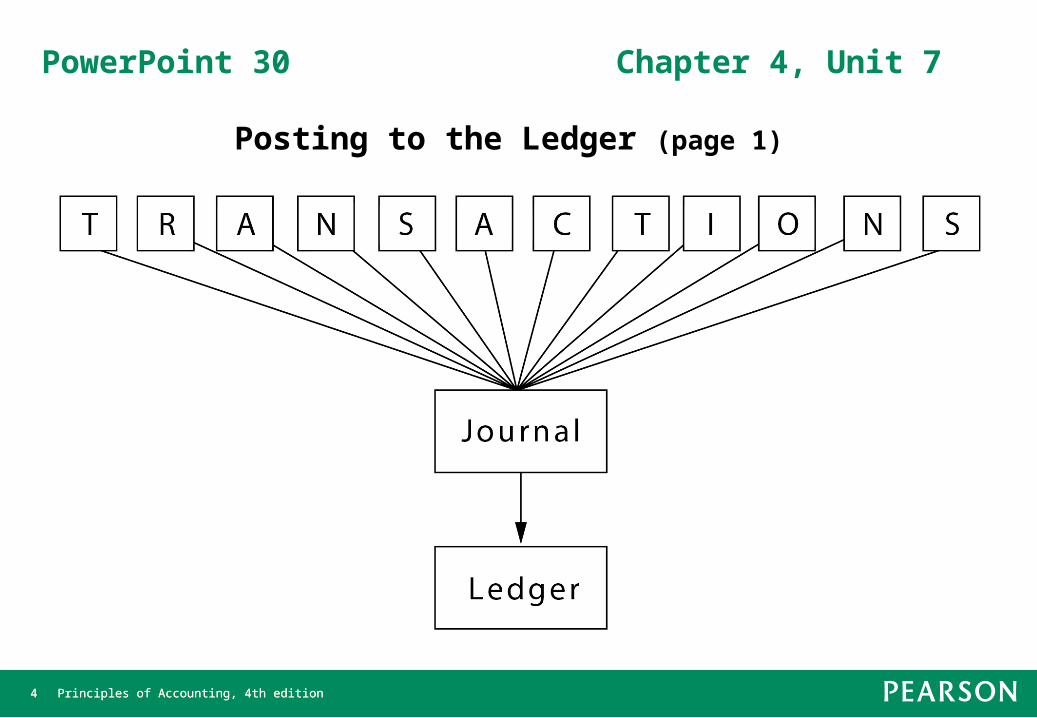

PowerPoint 30 Chapter 4, Unit 7

Posting to the Ledger (page 1)

Principles of Accounting, 4th edition5 Principles of Accounting, 4th edition5

PowerPoint 30 Chapter 4, Unit 7

Posting to the Ledger (page 2)

• The ledger is a group of accounts.

• Each account contains a complete, up-to-date record of all

transactions affecting only that particular account.

• The ledger may be a manually prepared paper record or a set of files

in a computer system.

• Posting is the process of transferring information to the ledger from

the journal.

Principles of Accounting, 4th edition6 Principles of Accounting, 4th edition6

PowerPoint 31 Chapter 4, Unit 7

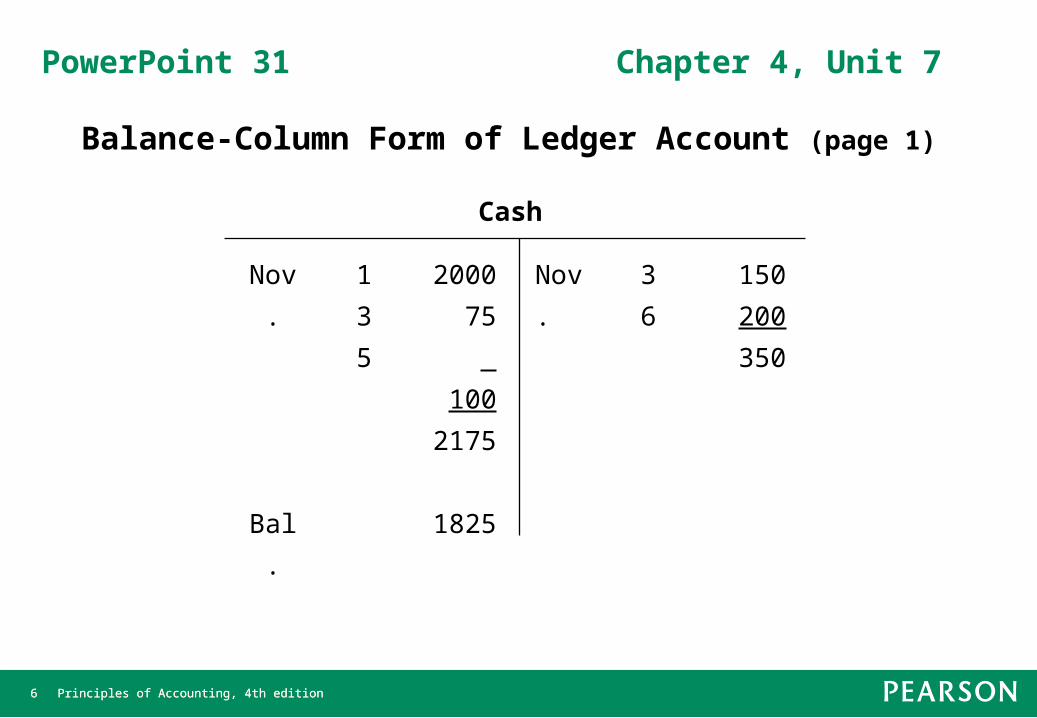

Balance-Column Form of Ledger Account (page 1)

Cash

Nov.

Bal.

1

3

5

2000

75

100

2175

1825

Nov

.

3

6

150

200

350

Principles of Accounting, 4th edition7 Principles of Accounting, 4th edition7

PowerPoint 31 Chapter 4, Unit 7

Balance-Column Form of Ledger Account (page 2)

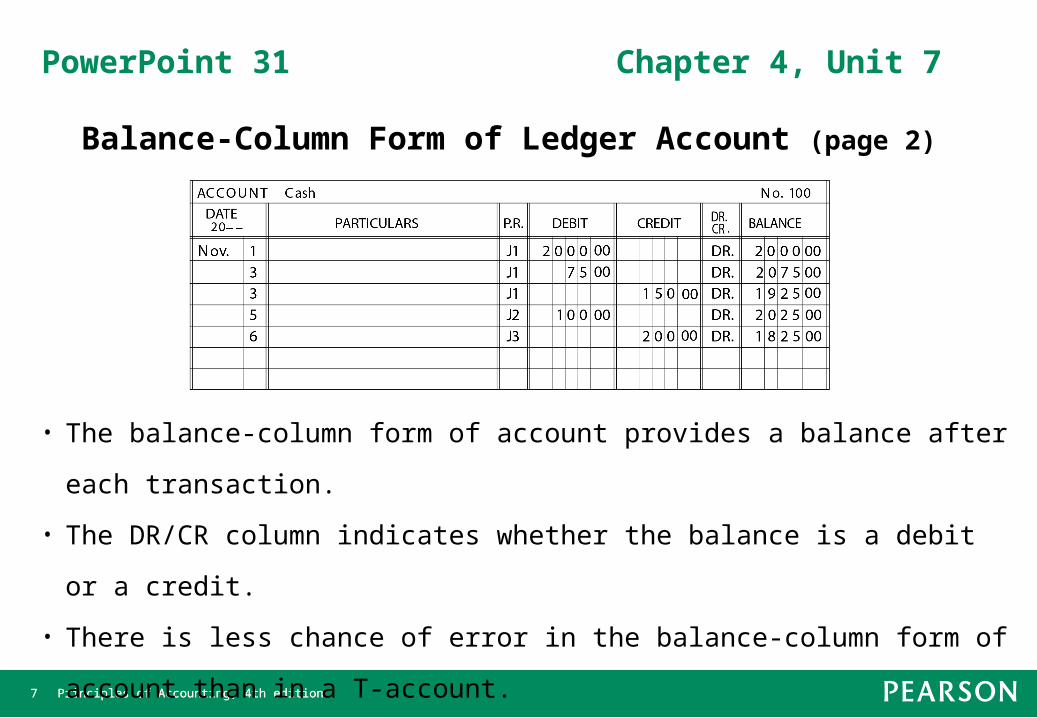

• The balance-column form of account provides a balance after each

transaction.

• The DR/CR column indicates whether the balance is a debit or a credit.

• There is less chance of error in the balance-column form of account

than in a T-account.

Principles of Accounting, 4th edition8 Principles of Accounting, 4th edition8

PowerPoint 32 Chapter 4, Unit 7

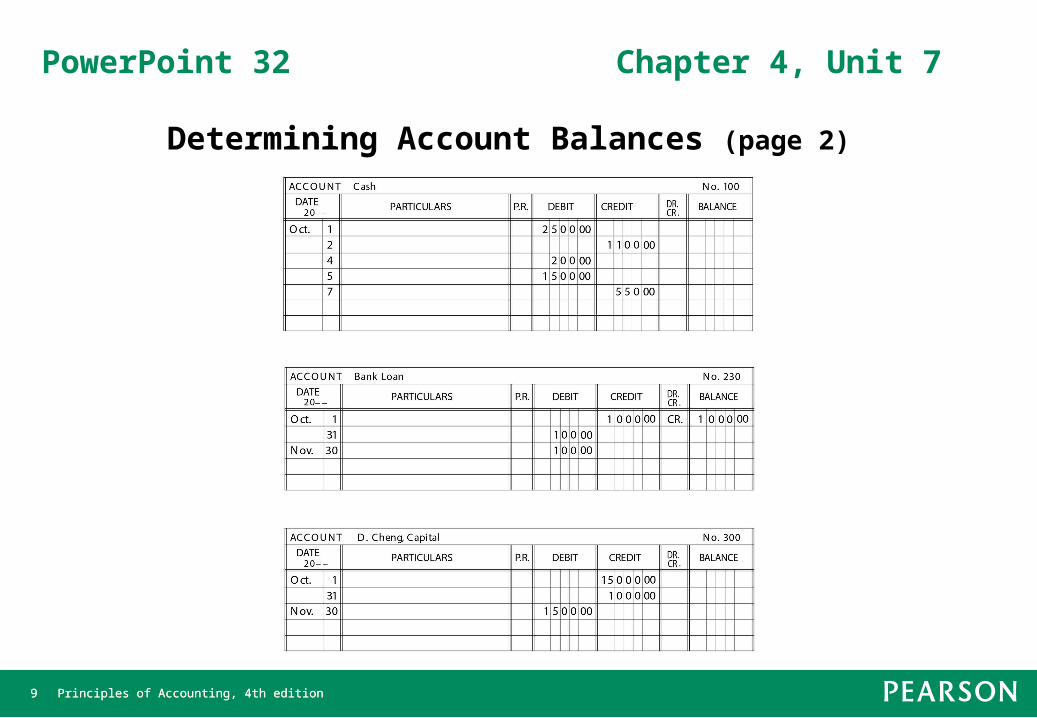

Determining Account Balances (page 1)

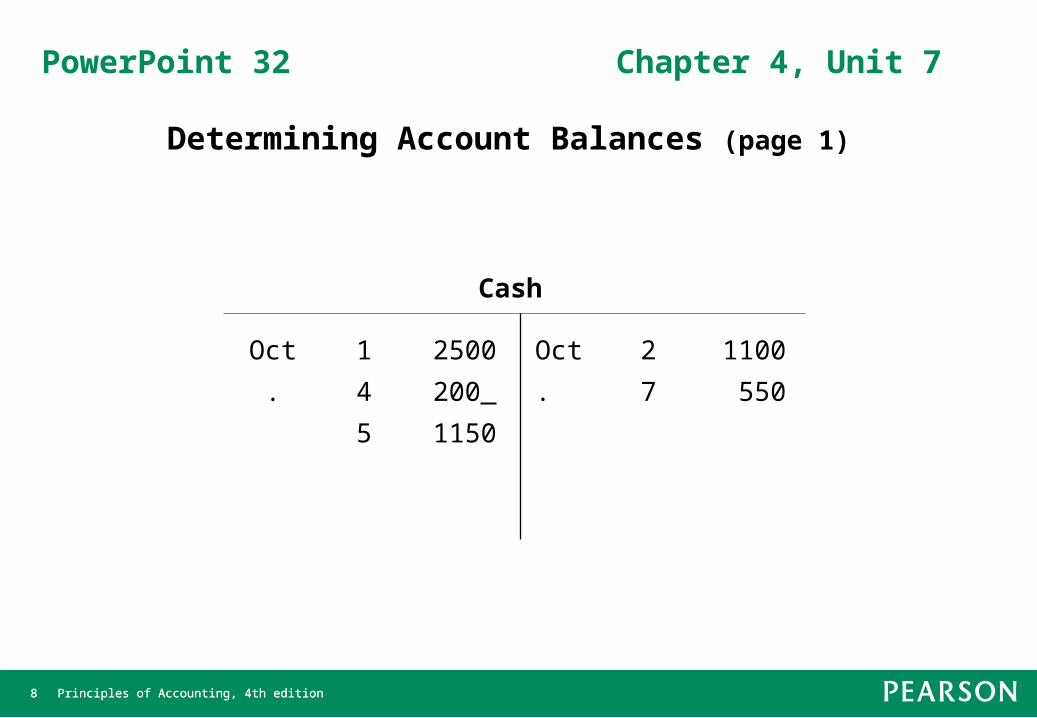

Cash

Oct. 1

4

5

2500

200

1150

Oct. 2

7

1100

550

Principles of Accounting, 4th edition9 Principles of Accounting, 4th edition9

PowerPoint 32 Chapter 4, Unit 7

Determining Account Balances (page 2)

Principles of Accounting, 4th edition10 Principles of Accounting, 4th edition10

PowerPoint 33 Chapter 4, Unit 7

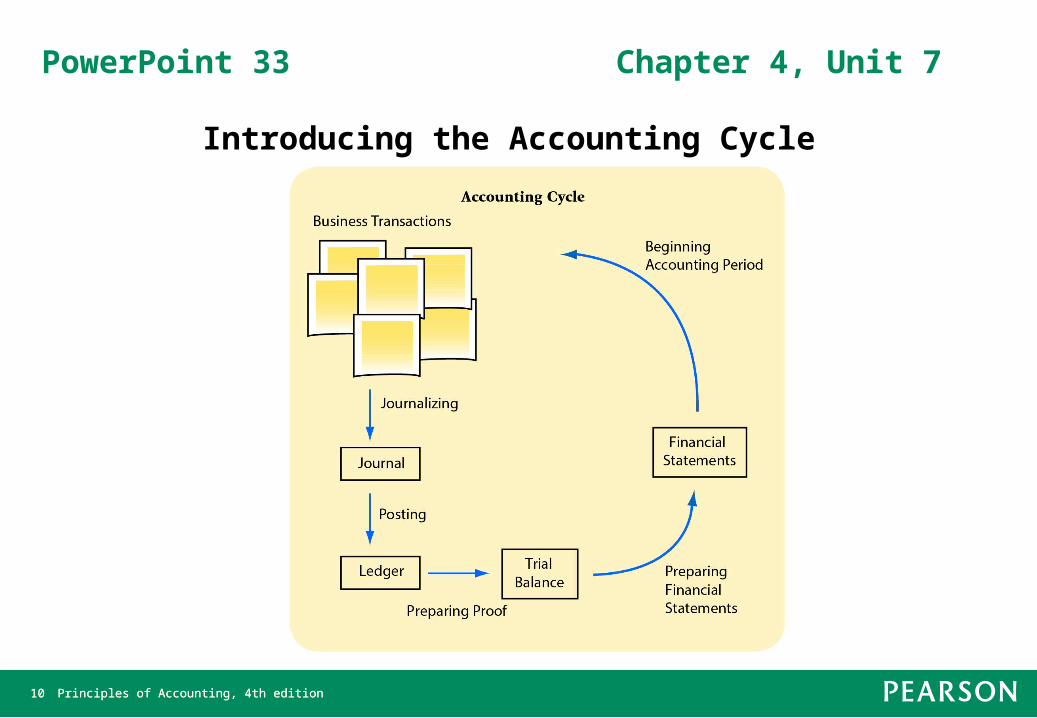

Introducing the Accounting Cycle

Principles of Accounting, 4th edition11 Principles of Accounting, 4th edition11

PowerPoint 34 Chapter 4, Unit 8

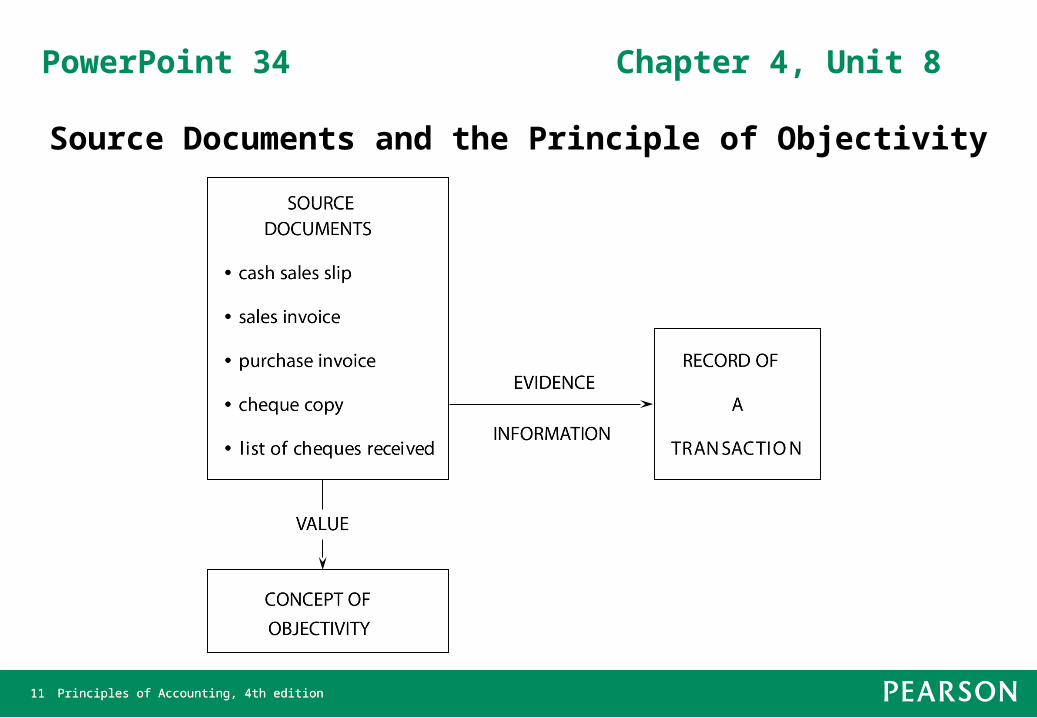

Source Documents and the Principle of Objectivity

Principles of Accounting, 4th edition12 Principles of Accounting, 4th edition12

PowerPoint 35 Chapter 4, Unit 8

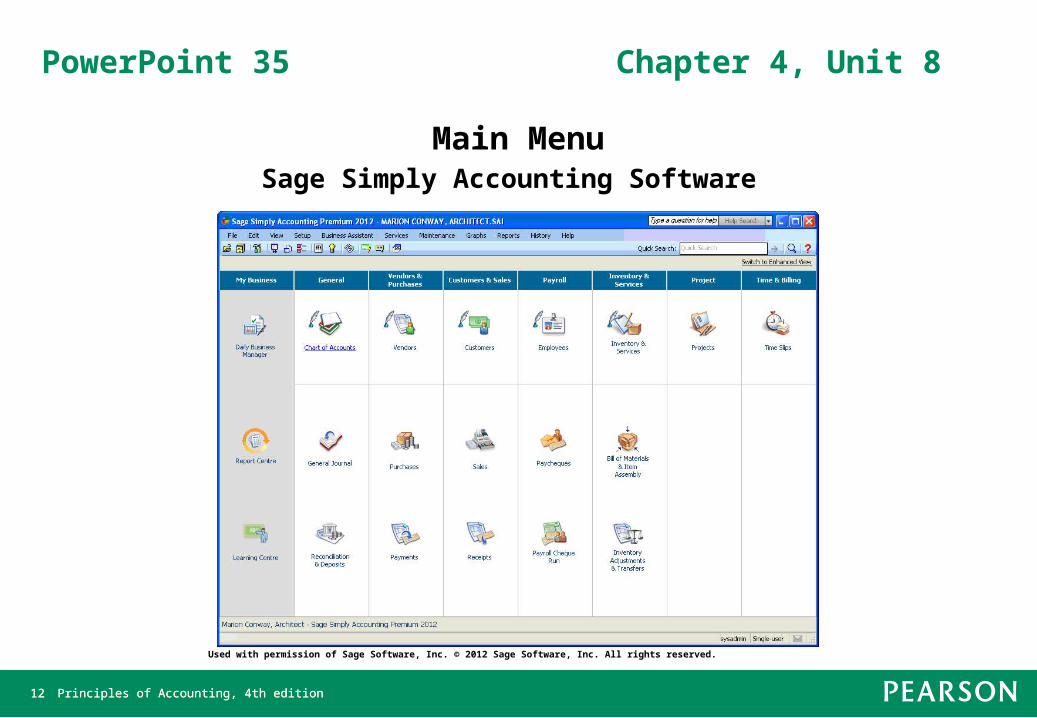

Main MenuSage Simply Accounting Software

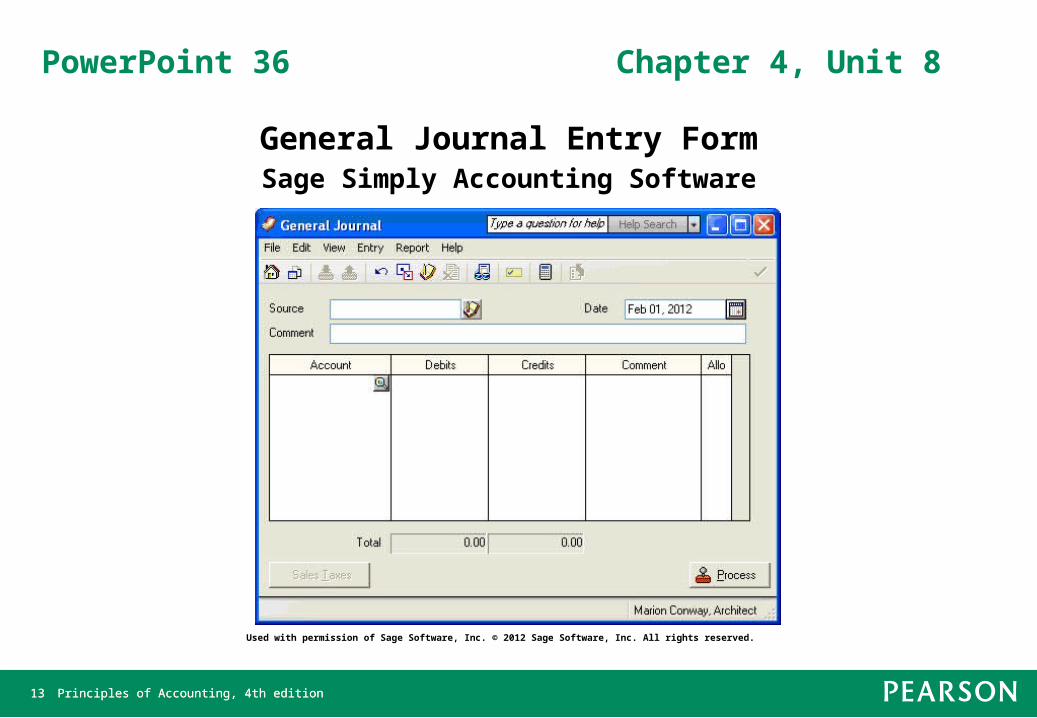

Used with permission of Sage Software, Inc. © 2012 Sage Software, Inc. All rights reserved.

Principles of Accounting, 4th edition13 Principles of Accounting, 4th edition13

PowerPoint 36 Chapter 4, Unit 8

General Journal Entry Form Sage Simply Accounting Software

Used with permission of Sage Software, Inc. © 2012 Sage Software, Inc. All rights reserved.