Embed Size (px)

DESCRIPTION

Primary Agent - June 2009 - PA Edition

Citation preview

PENNSYLVANIA

INTHISISSUE_______________5 ways to avoid HR turbulence

How one agency handled absenteeism

Talking shop with an aggregator advocate

G9616_C1 DMPJune2009Covers.qxd 5/14/09 6:46 AM Page P1

www.emcinsurance.com

© Copyright Employers Mutual Casualty Company 2009 All rights reserved

MAKE EMC YOUR CHOICE FOR MAIN STREET BUSINESSWhen you think main street business, start thinking about the EMC Choice® Businessowners Program. Small and midsize businesses will enjoy the flexible coverage options designed to meet their specific insurance needs, the added value of free loss control services, plus the responsive service from an EMC branch office nearby. So if you still think EMC is just for niche programs, think again. Count on EMC ® for your main street commercial lines marketing, too. For more details, contact your local EMC branch office.

I used to think EMC was ju st for niche commercial programs. Then again, I used to think that chocolate milk came from brown cows.

Valley Forge Service Office: 800.362.3620 | Home Office: Des Moines, IA

G9616_C2C3C4June09.qxd 5/14/09 6:40 AM Page 1

800-334-5579www.gotapco.com

The TAPCO Service Pledge

1,000 Strong More than 1,000 classes of P&C businesswritten under binding authority.

Real Time Service with a Real Live Underwriter.

Call. Quote. Bind.

five-minute phone call

Do you remember when Real Time meant a

relationship with a real underwriter? We do!

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 1

FFiivvee wwaayyss ttoo aavvooiidd HHRR ttuurrbbuulleenncceeTake a page from Southwest Airlines and learn how your agency can glidethrough the typically turbulent hiring and managing process with a few high-flying human resources tips.

Page 12

HHooww aann aaggeennccyy hhaannddlleedd aann eemmppllooyyeeee’’ss aabbsseenntteeeeiissmmWhen one of her eight employees started habitually calling off of work, Angela Malizia fretted over what she could do. But with help from IA&B’s HR Solution©, her staff is present and accounted for once again.

Page 18

TTaallkkiinngg sshhoopp wwiitthh aann aaggggrreeggaattoorr aaddvvooccaatteeDon Rumbaugh, an agency owner in his early sixties, is doing the opposite ofmany agency principals his age: He is bringing on sales people and planning todouble the size of his agency in the coming years. Ask him why, and he’ll singthe praises of Best Insurance Group — the cluster he joined four years ago.

Page 22

12

18

22

ContentsP R I M A R Y A G E N T M A G A Z I N E

Copyright 2009. All rights reserved. No material may be reproduced in whole or in part without written consent of the publisher. The information in this publication is general in nature and is not intended to serve as legal, accounting, financial,insurance, investment advisory or other professional advice as to any reader’s particular situation. Users are encouraged to consult withcompetent legal, financial, insurance, investment advisory and or other professional advisors concerning specific matters before makingany decisions and we disclaim any responsibility for any decisions or actions by readers. Statements of fact and opinion in PrimaryAgent are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the IA&B.Participation in IA&B events, activities and/or publications is available on a non-discriminatory basis and does not reflect IA&Bendorsement of the products and/or services.

Subscriptions: Non-member price: $2.25 per copy or $15 per year.

All communications for publications, including news, features, advertising copy, cuts, etc., must reach the editor by 1st of month two monthsprior to publication. Advertising rates furnished upon request.

Address inquiries to:Primary Agent EditorPO Box 2023Mechanicsburg, PA 17055-0763Phone (800) 998-9644 or (717) 795-9100 Fax (717) 795-8347

Periodical postage paid at Mechanicsburg, Pa. and additional entry post office.

Postmaster: Send address changes to above address.Primary Agent (ISSN 1543-3110), Permit # 638-620, Issue # 2009-6) is published monthly by IA&B Service Group Inc., a subsidiary of IA&B.

4 Chairman of the Board’s Message6 State News7 New Members8 Preventing Errors & Omissions9 Member FAQ10 Coverage Corner

15 Glance at Events17 IA&B Partners26 Technology Update28 Advertisers Index28 Classified Ads

In every issue

Mission StatementPrimary Agent delivers ideas to helpInsurance Agents & Brokers’ membersnegotiate their unique position asguardians of trust between insuranceconsumers and companies whilefacing the challenges of maintaining a small business. Primary Agent also supports IA&B’s mission topreserve and advocate the AmericanAgency System.

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 2

We’re one part international. Now part of QBE®, a

multibillion dollar business with the global resources to

support more than 2,000 independent agents in North

America alone. Together we search the world for solutions

to your most complex challenges.

We’re one part regional. Since 1925, General Casualty®

has kept regional offices open and decision-makers in

the field all across this state. We know our agents—and

their clients—because we know the value of personal,

accessible service.

We’re one. General Casualty and QBE, working

together for you.

generalcasualty.com

General Casualty is a registered service mark of General Casualty Company of Wisconsin.

QBE and the links logo are registered service marks of QBE Insurance Group Limited.

All coverages underwritten by member companies of QBE. © 2009 QBE Holdings, Inc.

GLOBAL REACHMEETS LOCALTOUCHPOINT.

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 3

OfficersRobert J. “Buc” Cawley, AAI

ChairmanWexford, Pa.

Kathleen M. Glattly, ChFC, CLU, CPCUVice ChairwomanFactoryville, Pa.

G. Kevin Nemith, CICImmediate Past ChairmanDover, Del.

MembersNorman F. Basso, CPCU

York, Pa.

Vincent D. “Chip” Boylan Jr., CPCURockville, Md.

Timothy P. BurrisThompsontown, Pa.

M. Scott Clemens, CIC, CPCU, CLU, ChFC Souderton, Pa.

John T. “Chip” Colwell Jr., CICCorry, Pa.

Robert B. Hall, CPCU, CLU, ChFC, ARM, ARM-PWest Chester, Pa.

Denise M. Kozel, CPCUNewark, Del.

Linda A. McCann, AAI, CPCU, CPIWSalisbury, Md.

Thomas G. McElhaney State College, Pa.

Michael F. McGroarty Sr.Pittsburgh, Pa.

Scott C. Rogers, CPIAYork, Pa.

David Rosenkilde, CICReisterstown, Md.

Susan A. Sallada, CIC**Ft. Washington, Pa.

William D. Schneider, CPCU, ARM*Pittsburgh, Pa.

Robert A. Walbeck, CICHomer City, Pa.

David B. Wasson Sr., CICState College, Pa.

James M. Watkins*Dover, Del.

King W. “Kip” White, LUTCFFallston, Md.

John S. Yasik, CICNewark, Del.

* IIABA National Director** PIA National Director

Board of Directors

Running a tight ship during a tidal wave of tough times

By now the financial crisis has rippled through just about everysegment of the economy — the independent agency systemincluded. And as agency principals struggle to stay afloat, it’soften office oversight that sails off into the sunset.

Before you drown in human resources headaches, take a fewminutes to review this issue of Primary Agent magazine andgrab onto a few lifesaving tips from people (execs atSouthwest Airlines and at fellow IA&B member agencies)who’ve done it right.

You’ll also find a wealth of legal and managerial material inthe agency-operations information available on iabgroup.com.Association staff recently re-categorized the online content, soyou can quickly and easily find the resources to help you run atight ship.

Of course the IA&B Web site also houses HR Solution©. The collection of members-only HR tools and resources iscontinually updated to reflect compliance and legal changes. If you haven’t registered for HR Solution© yet, it’s time to jump onboard.

Until next time, keep your chin up and your head above water.Sunnier days are ahead!

[ 4 ]

ROBERT J. “BUC” CAWLEYAAI

ChairmanO F T H E B O A R D ’ S M E S S A G E

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 4

©S

IAA

2005

YourBridge to

Success!THE ALTERNATIVE

The Strategic Independent Agents Alliance (SIAA) is the future of insurancedistribution…NOW. Since 1983, SIAA and our Master Agencies have made a business out of

helping local independent agencies stay independent, while helping Captive Agents, DirectWriters, Producers, and Life and Financial Service Agents become independent.

GET INSTANTLY BIGAs soon as you join an SIAA Master Agency, you become instantly BIG by accessing the

companies that you need in order to compete with and win against any agency. Your agency’sincome and value will increase beyond any amount that you can generate on your own.

Over 2,100 agencies like yours have increased their income and value by joining SIAA. Find out more by visiting our website at www.siaa4u.net.

Trouble Get t ing Mar ket s?

Now over 50 agencies

in Pennsylvania

G9616_01-11PrimAgJune09.qxd 5/14/09 5:45 AM Page 5

State NewsPrimary Agent | June 2009

[ 6 ]

Thirty-nine IA&B of Pennsylvaniamembers congregated in Washington,D.C. April 29-30 as part of the annualBig “I” Legislative Conference &Convention. The event broughttogether hundreds of producers fromacross the country to advocate onregulation, licensing, health carereform, the National Flood InsuranceProgram and crop insurance.

“With insurance regulation such a hottopic in Congress, it was especiallyimportant for us to make the trip thisyear,” said Buc Cawley, chairman ofthe IA&B Service Group. “Ourmembers relayed their reservationswith federal regulation and expressedtheir support of state regulation tobenefit the industry and consumers.”

The event began on Wednesdayafternoon with a briefing by Big “I”staff. From there, Pennsylvaniaattendees went to a reception, issuesbriefing and dinner hosted by IA&B.The next morning they traveled to theCapitol, where they met with 17legislators and their staff. (See sidebarfor a complete list.)

“It was a great opportunity for ourmembers to influence change on anational level while representing their local communities,” said Cawley,“and the congressmen andcongresswomen were very receptive to their input and experiences.”

Each year IA&B hosts a limited number of members to attend theconference. Attendance is available ona first come, first served basis.Registration for the March 3-4, 2010event will be announced via AgentHeadlines late next fall.

Independent agents take Washington, D.C. by storm

IA&B members met with the following congressmenand congresswomen and/ortheir staff.

Rep. Jason Altmire

Rep. Chris Carney

Sen. Bob Casey

Rep. Kathy Dahlkemper

Rep. Charlie Dent

Rep. Jim Gerlach

Rep. Tim Holden

Rep. Paul Kanjorski

Rep. Tim Murphy

Rep. Jack Murtha

Rep. Joe Pitts

Rep. Todd Platts

Rep. Allyson Schwartz

Rep. Joe Sestak

Rep. Bill Shuster

Sen. Arlen Specter

Rep. Glenn Thompson

Roger Janes, Ann Truschel, Bill Griffin, Bill Schneider, Mark Christie, Rosann Cusumano Elinsky and Michael McGroarty

Tim Franklin, John Shipman, Rep. Paul Kanjorski, Cinda Hartman, Barbara Jason, Kathleen Glattly

Tim Franklin, Patrick McClure, Allan Boyd, Tim Burris, Henry Brusca, Scott Rogers, John Shipman,

Michael McGroarty, Kim Troast-Singley, Bob Sobel

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 6

[ 7 ]

How to pick a PAC to supportIndependent agents in Pennsylvaniaare represented by three PACs –AgentPAC, InsurPAC and PIAPAC.

IA&B oversees AgentPAC and uses themoney to support friends in thePennsylvania House and Senate. Theother two — InsurPAC, which isassociated with the Big “I,” andPIAPAC, which is associated with PIANational — are national PACs. Bothsolicit contributions from agentsacross the country and use the fundsto support U.S. Congressionalcandidates in Washington, D.C.

IA&B encourages support of all three PACs.

IA&B Political Action CenterThis spring IA&B launched its Web-based Political Action Center to provide members with the latest legislative and political newsand opportunities to make their voices heard. It is updated frequentlyto reflect the most recent actionstaken by the U.S. Congress and state legislature.

By logging on, members can easilycatch up on the federal and stateissues that impact them asindependent agents and small-business owners. Plus, the PoliticalAction Center simplifies involvementby providing a contact directory andtemplate forms for use incommunicating with legislators.

Members can find a link to thePolitical Action Center on the left-handnavigation bar of iabgroup.com.

2009 Agency PAC ChallengeThere is still time to participate in the2009 Agency PAC Challenge — acontest among member agencies toraise money for AgentPAC. The resultwill be a stronger, more viablepolitical action committee (PAC) …and lunch for one winning agency.

In April IA&B concluded a successfulemployee campaign at associationheadquarters that raised $700 forAgentPAC. IA&B encourages memberagencies to hold their own employeechallenge using a similar benchmarkof $20 per employee. The agency withthe highest average contribution rateper employee by June 30 wins.

Additional information, contributionforms and FAQ sheets are available bycontacting IA&B’s Member ServiceCenter toll free at (800) 998-9644 orlocally at (717) 795-9100, option 0.

New MembersW E L C O M E

Lane Agency, LLCAllentown, Pa.

PAC a punch in Harrisburg

Rosann Cusumano Elinsky, Michael McGroarty,Rep. Tim Murphy, Mark Christie

Roger Janes, Rep. Kathy Dahlkemper, Bill Schneider

John Shipman, Kathleen Glattly, Rep. ChrisCarney, Tim Franklin, Jeff Coup

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 7

Underinsured Motorists andUnderinsured Motorists(UIM/UM) coverages are veryimportant. They protectindividuals when they areinjured by uninsured driversor drivers that carry low limitson their vehicles.

But how well is your agencyprotected from an E&O claimrelated to this coverage?

When UIM/UM coverages arein place, injured parties cancollect money from their ownautomobile policy to helpcompensate them for theirphysical and financial lossesfollowing an accident. Themethod by which thiscoverage can be offered willvary from state to state. Infact, some states mandate aninsured execute waivers forUIM/UM coverage andwaivers to disallow stacking oflimits. There is acorresponding reduction inpremium if an insureddecides to waive coverage orstacking. In the past, waiverswere collected by agents andfiled by carriers. In theinterests of budgetcutting/streamlining, carriersnow are mandating theiragents keep waivers on file,which places a burden on

agencies to maintain thosedocuments. Without aproperly executed waiver onfile, the exposure to agencieswhen a UIM/UM claim ismade increases greatly.

Take, for example, the casewhere an agency’s client wasseriously injured and made aclaim for UnderinsuredMotorists following theaccident. There was a signedrejection of UIM in theagency’s file, and the carrierinitially denied coveragebased on the rejection.

The law in that state wasclear: If an insured rejects thecoverage, he cannot collect.However, in this particularcase the injured insureddenied signing the rejectionform, and claimed thesignature was not his. Hesued the carrier for $500,000,alleging there was no properrejection on file.

The law in that state was clearon this issue: Without asigned waiver, coverage isdeemed to be in place. Thecarrier had a handwritinganalysis performed by anexpert, and the expertconcluded it was not theinsured’s signature on the

rejection. The insured’s intentas to whether or not hewanted UIM coveragebecame a moot issue. All hehad to show was that therewas no properly executedrejection on file in order tocollect. The carrier paid$500,000, and sued the agentfor not obtaining a propersignature. The agent claimedhe did not sign the form butcould not say who did signthe form. The form had beenmailed to the insured andreturned with a signature, perthe agent.

Without any proof that therejection was properlyexecuted, the claim by thecarrier was settled for$250,000. While it may beeasier to merely send a formto an insured for hissignature, the agency isexposing itself when asignature is challenged wellafter the fact. All UIM/UMwaivers should be signed inthe presence of an agent toavoid any confusion,challenges or claims againstthe agency.

Another UIM/UM scenariothat can lead to claims againstan agency involvescommercial auto policies.

PreventingE R R O R S A N D O M I S S I O N S

[ 8 ]

PAUL E. WALTERS

Paul E. Walters is claims

manager for Utica Mutual

Insurance Company in

Utica, N.Y.

Insurance Agents & Brokers

Service Group Inc. is the

exclusive agent for the Utica

E&O program in Delaware,

Maryland and Pennsylvania.

For questions regarding this

article or your Errors &

Omissions coverage, contact

IA&B at (800) 998-9644 or by

e-mail at [email protected].

UNDERINSURED/UNINSURED MOTORISTS —GETTING IT RIGHT

Primary Agent | June 2009

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 8

Under either coverage, a claim forUIM/UM can only be made by either a named insured or an occupantof the covered vehicle. UIM/UMcoverage will apply to a named insuredeven if that person was injured as apedestrian or was a passenger inanother car. Since many commercialauto policies list a business as thenamed insured, the agent must checkwith the principals of the business andinquire whether or not that person(s)wants to be listed as an additionalnamed insured on the policy. Thereusually is no additional premiuminvolved. Otherwise, the agency isexposed when a principal of a companyis seriously injured.

An example is a case where theagency’s client was a new customer ofthe agency for commercial autocoverage. The policy had $1,000,000

limits for BI and UIM/UM. The clientcompany was owned by two partners,one being Mr. X. When the policy waswritten, neither of the owners was listedas additional named insured on thepolicy. Following the policy inception,Mr. X was killed while jogging. Hisestate made a claim against the UIMportion of the commercial auto policy.The carrier disclaimed based on the facthe did not qualify as an insured, as hewas not in the course of hisemployment and he was not operatingnor was he in a covered auto. Suit wasfiled against both the carrier and theagent. The estate produced a witness,the deceased’s daughter, who said sheoverheard her father discuss with theagent the need to be added to thepolicy. This was denied by the agent.The agency’s counsel had filed for adismissal based on the fact that theagent owed no duty to advise the

partners of the need to be added asadditional insureds. The court deniedthe motion, stating there was aquestion of fact as to the duty owed.The claim against the agency wassettled for $150,000.

Since it is easy to add a businessowner(s) as an additional namedinsured on a commercial auto policy,ask the client(s) if he or she wishes to be added. Then document the discussion.

Agents have been sued by carriers and their clients (personal andcommercial) following auto accidentswhen there is a problem with eitherUM or UIM coverage. Protect youragency! Take steps to witness thesigning of waivers and offer additionalinsured coverage to principals undercommercial auto policies.

?QUESTION:

I work directly with the NFIP (no

Write-Your-Own company). The

NFIP is redoing its flood maps and

when I want to order the maps, I

don’t know which ones have been

updated recently and which have

not. At this point, I have to

“pretend” to purchase a map in

order to see the revision date, but

that procedure is not user-friendly:

I have to go into every little

borough and township.

Is there an “easy button” to know

if the township has had its flood

map updated?

ANSWER:To check the date of the current map,you can access the Community StatusBook from the NFIP Web site. Thislisting, by state, will tell you thecommunity name, number, date of theoriginal map and date of the currentmap. There are quite a few 2008 and2009 map effective dates for PA.

To access this list, go towww.fema.gov/business/nfip andrequest the flood insurance library. Youwill see the community status book as achoice and then select the appropriatestate. This is the “easy button.”

Another source of information is theagent section of www.floodsmart.gov,which has a partial listing ofcommunities for which new maps arecurrently in the proposed status.

Finally, agents generally really benefitby getting aligned with a good Write-Your-Own (WYO) company.

This answer was provided with theassistance of nationally recognizedflood expert M. Rita Hollada.

DO YOU HAVE AQUESTION? E-mail it to us at [email protected] use “Primary Agent FAQ” in the subject line of your message. You can also fax your question to (717) 795-8347. We look forward toanswering your questions!

Member FAQ

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 9

CoverageC O R N E R

[ 10 ]

JERRY MILTON, CIC

Jerry M. Milton teaches

and consults on industry

issues. The legal profession

recognizes him as an

expert on insurance

coverages. He is also the

education consultant for

IA&B, working with CISR,

CIC and continuing

education programs.

I’M CONFUSED — WHO AND WHAT DOES THEHOMEOWNERS POLICY COVER?

Primary Agent | June 2009

When attorneys and thecourts argue over the termsand provisions of a contract,including insurance contracts,they often refer to those terms and provisions as being ambiguous. Thedefinition of ambiguous is“susceptible of multipleinterpretations.” Black’s LawDictionary states, “Language ina contract is ambiguous whenit is reasonably capable ofbeing understood in morethan one sense.”

There are several provisions inthe Homeowners policy thatmay or may not beambiguous. I really don’tknow if they are. But whetherthey are or not, I’m stillconfused by them. Thefollowing are a few examples.

The Homeowners policydefines “business” as:

a. A trade, profession oroccupation engaged inon a full-time, part-timeor occasional basis; or

b. Any other activityengaged in for money orother compensation,except the following: Oneor more activities, notdescribed in (2) through(4) below, for which no“insured” receives more

than $2,000 in totalcompensation for the 12 months before thebeginning of the policy period.

Incidentally, exceptions (2), (3) and (4) refer to volunteeractivities and home day care services.

Now, here is my question.We’re having a yard sale thisweekend. Is that a “business”activity? Before you answerthat question, you must ask ifwe had a yard sale last year. Ifwe did, you must then askhow much we made. If wedidn’t have a yard sale lastyear, then the yard sale thisyear is not a “business”activity. If we did have a yardsale last year, but made$2,000 or less, it’s still not a“business.” The yard sale thisyear is a “business” only if wehad one last year and mademore than $2,000.

If I received compensation of$5,000 for an activity last yearand only $1,000 this year, isthat activity a “business”under my currentHomeowners policy? Yes. But,if I received no compensationlast year and receive $100,000this year, is that activity a“business” under my

Homeowners policy? I don’tthink so. Go figure.

The definition of “insured” in the Homeowners policy is as follows:

a. You and residents ofyour household who are:

1) Your relatives; or

2) Other persons under the age of 21 and in the care of any person named above;

b. A student enrolled inschool full time, asdefined by the school,who was a resident ofyour household beforemoving out to attendschool, provided thestudent is under the age of:

1) 24 and your relative.

Our 26-year-old daughter,Princess, is in graduate schoolat State University. She iscurrently taking 12 semesterhours. Buster, who is our 24-year-old son, has finally madeit to his senior year at thesame university. He’s taking 14hours this semester. StateUniversity defines a full-timestudent as one taking 12 hoursor more.

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 10

[ 11 ]

Based on the Homeowners definition of“insured,” neither of our children are an“insured” under our Homeownerspolicy. However, Buster decided to dropa three-hour course. He is no longerfull-time as defined by the university. Ishe now an “insured” under ourHomeowners policy? If he is stillconsidered a resident of our household,I think he is. And, I believe he would beconsidered a resident of our household.After all, we fully support himfinancially, he comes home frequentlyand he uses our home address on hisdriver’s license and other legaldocuments. The Homeowners policy issilent about students who are 24 andolder and are part-time students.

Finally, under Coverage C – Personal Property the following special limits apply:

h. $2,500 on property, on the‘residence premises,’ usedprimarily for ‘business’ purposes;

i. $500 on property, away from the‘residence premises,’ usedprimarily for ‘business’ purposes.However, this limit does not applyto loss to electronic apparatus andother property described inCategories j. and k. below;

j. $1,500 on electronic apparatusand accessories while in or upon a‘motor vehicle,’ but only if theapparatus is equipped to beoperated by power from the‘motor vehicle’s’ electrical systemwhile still capable of beingoperated by other power sources;

k. $1,500 on electronic apparatusand accessories used primarily for‘business’ while away from the‘residence premises’ and not in orupon a ‘motor vehicle.’ Theapparatus must be equipped to beoperated by power from the‘motor vehicle’s’ electrical systemwhile still capable of beingoperated by other power sources.

My personal computer was stolen frommy car. It has a value of $2,500. Howmuch will I be paid? $1,500 if I have acable that allows me to plug it into thecar’s power outlet. $2,500 if it can’t beplugged in because I don’t have a power cable.

My business computer was stolen from a hotel conference room. It has avalue of $3,000. How much will I collectunder my Homeowners policy? $1,500if I have that cable to plug it into thecar’s power outlet. $500 if I don’t havethat power cable.

Sounds like I don’t want the power cable if it’s a personal computer, but Ido want it if the computer is used forbusiness purposes.

As I said earlier, I’m confused aboutcertain Homeowners provisions. I stillam. Now you probably are too.

Y’all take care!

A-Rated Carrier Now AppointingNew Producers in Pennsylvania,

Maryland & Delaware! (More states to be added in the near future.)

� Business Insurance—CPP, BOP Monoline Fire, GL

� Competitive pricing—All LinesMSO rates and policy forms

� Personal lines roll overs will be considered

� Commercial auto for artisan contractors, retailers and wholesalers

� Contractor’s policy rated on number of employees, not payroll

� Internet rating system

� No minimum premium requirement forour producers

� Fast and friendly service for our customersfrom company staff

P.O. Box 62

Dublin, PA 18917

Office: 215-249-1394

Cell: 215-272-1442

Fax: 215-249-1395

E-mail: [email protected]

To get started, please contact Dick Riddle, CPCU

G9616_01-11PrimAgJune09.qxd 5/14/09 5:41 AM Page 11

HUMAN RESOURCES

Take a page from Southwest Airlines and learn how your agency can glidethrough the typically turbulent hiring and managing process with a fewhigh-flying human resources tips.

Five ways to avoidHR turbulence

G9616_12-17June09PrimAg.qxd 5/14/09 5:55 AM Page 12

[ 13 ]

Primary Agent | June 2009

Iam a fan of Southwest Airlines because it is sosuccessful in an industry full of unsuccessfulcompanies. A few years ago, Kevin and Jackie Freibergwrote a book outlining its success: “Nuts! SouthwestAirlines Crazy Recipe for Business and PersonalSuccess.” Besides probably being the funniest business

how-to book, it is still one of the best, and most lessons applyto insurance agencies.

One issue so many agency owners struggle with is hiringemployees who care about the agency. In the book’s words,“What does it take to get employees to assume ownership fora business, to truly take personal responsibility for itssuccess?” Southwest has achieved this extremely well, soagencies may find some words of wisdom in their success.

1. Hire people that think like owners. People that think like owners will focus on the agency’shealth, not just their jobs. As the book points out,ownership is a state of mind as much as a piece of paper.

2. Hire self-starters. This is particularly true of producers. A producer that justwants job security is not going to be successful. Southwestmade potential pilots pay for their own $10,000 trainingwith no promise of even being hired. The pilots had to payfor this training even before Southwest would interviewthem! That way, the training served as a screen. Only self-starters made it to the interview process.

3. Share the profits. Suppose all the people you hire take ownership and are self starters, but then you don’t pay them for their success. I can guarantee the results won’t be positive. If you hire people that think like owners and take responsibilityfor their work and the agency, they must be treated like owners. Make bonuses serious sums so the agency’s interest is closely aligned with the employees’interest. Make the bonuses significant enough to get theemployees’ attention.

4. Listen. Make sure your employees know you want their opinion. Inevery agency I visit, the staff knows more about whathappens daily in the agency than the principals. Therefore,if you want to improve, you need their input. Most peoplewant to make a difference in their jobs. Knowing they doenhances an agency and the employees’ lives. It makesrecruiting good employees easier.

One issue so many agency

owners struggle with is hiring

employees who care about

the agency.

Once an agency begins

successfully hiring good people —

and keeps them — the agency

will begin having a much easier

time hiring even more good

people. Success breeds success.

I

G9616_12-17June09PrimAg.qxd 5/14/09 5:55 AM Page 13

5. Communicate trust.Communicate consistency. Communicate goals. Againand again and again. I visitmany agencies where thestaff and even producershave lost faith in agencymanagement for neverfollowing through on anyinitiatives. In thesesituations, management has violated all three ofthese tenants. They havenot shown trust, they havenot shown any consistency,and the agency’s goals are a mystery.

The most important asset anyagency has is its people. Oncean agency begins successfullyhiring good people — andkeeps them — the agency will begin having a mucheasier time hiring even more good people. Successbreeds success.

This does mean giving upsome freedom because anytime we make a commitmentto anyone, we are giving upsome freedom. For someowners, this loss of freedommay be too much. If this is the case, admit it, and thenstop complaining about theinability to get goodemployees. That is thepotential price for hanging on to your freedom.

However, if you can accept theloss of some freedom, thesefive simple suggestions makegreat sense, and I know everyagency that follows them willenjoy more success.

NOTE: None of the materials in thisarticle should be construed as offeringlegal advice, and the specific advice of legal counsel is recommendedbefore acting on any matter discussedin this article. Regulatedindividuals/entities should also ensurethat they comply with all applicablelaws, rules and regulations.

______________________________

Chris Burand is president ofBurand & Associates, LLC, aninsurance-agency consultingfirm. Readers may contact Chris at (719) 485-3868 or [email protected].

[ 14 ]

HUMAN RESOURCES

DO YOU WORK WITH DENTISTS?That’s all we do.

EASTERN DENTISTS INSURANCE COMPANY

200 FRIBERG PARKWAY, SUITE 2002 • WESTBOROUGH, MA 01581WWW.EDIC.COM • A DENTAL RISK RETENTION GROUP

Eastern Dentists Insurance Company (EDIC), a dental risk retention group,is currently welcoming the opportunity to work with Pennsylvania agentsholding a book of business with dentists. We are a financially sound,growing malpractice insurance company, serving dentists throughout theNortheast. Our agents enjoy outstanding benefits, including:

• New Products• Fair Commissions• Extra Incentive Programs• Exclusive “By Dentists, For Dentists®” Marketing Program

EDIC was established in 1992 and is independently owned by dentists.Our multi-state Board of Directors is comprised of dentists, including arepresentative from Pennsylvania.

Do you consider yourself the best? If so, join the best. Join EDIC.

For more information, contact John P. Dombek, Vice President, Sales,at 800-898-3342 or [email protected]

®

G9616_12-17June09PrimAg.qxd 5/14/09 5:58 AM Page 14

[ 12 ]

Glance at EventsDate Topic Location

2 P&C Licensing Mechanicsburg, Pa.

CISR—Commercial Property Altoona, Pa.

3 P&C Licensing Mechanicsburg, Pa.

CISR—Commercial Property Pittsburgh, Pa.

4 P&C Licensing Mechanicsburg, Pa.

8 CIC—Commercial Property Lancaster, Pa.

9 CIC—Commercial Property Lancaster, Pa.

CISR—Commercial Property Philadelphia, Pa.

William T. Hold seminar Mechanicsburg, Pa.

10 CIC—Commercial Property Lancaster, Pa.

James K. Ruble Graduate seminar Annapolis, Md.

CISR—Commercial Property Mechanicsburg, Pa.

11 CIC—Commercial Property Lancaster, Pa.

James K. Ruble seminar Annapolis, Md.

CISR—Commercial Property Frederick, Md.

12 James K. Ruble seminar Annapolis, Md.

Mistakes That Lead to E&O Claims seminar Salisbury, Md.

15 CIC—Agency Management Erie, Pa.

16 CIC—Agency Management Erie, Pa.

17 CIC—Agency Management Erie, Pa.

CIC—Life & Health Allentown, Pa.

CISR—Commercial Casualty Pittsburgh, Pa.

18 CIC—Agency Management Erie, Pa.

CIC—Life & Health Allentown, Pa.

19 CIC—Life & Health Allentown, Pa.

23 P&C Licensing Philadelphia, Pa.

CISR—Commercial Property Reading, Pa.

24 P&C Licensing Philadelphia, Pa.

CISR—Commercial Property Scranton, Pa.

25 P&C Licensing Philadelphia, Pa.

CISR—Commercial Property Baltimore, Md.

Don’t wait for a CISR course to come to you — access it from your desktop! CISR OnLine is an excellent way tocomplete a course you need that may not be scheduled in your area in the timeframe you need it. You can alsomix and match the CISR OnLine course with classroom courses so you can still maximize the benefit ofnetworking and face time with the instructor. Register for courses online at iabgroup.com.

J U N E C A L E N D A R

G9616_12-17June09PrimAg.qxd 5/14/09 5:55 AM Page 15

FEATURED PARTNER:Mutual Benefit Group

CHIEF EXECUTIVE OFFICER:Steven C. Sliver, President and CEO

COMPANY LOCATION:Huntingdon, Pennsylvania

A.M. BEST RATING: “A-” (Excellent)

WEB SITE:www.mutualbenefitgroup.com

Insurance Agents & Brokers proudly recognizes MutualBenefit Group as one of its Platinum Partners. IA&BPlatinum Partners dedicate the highest level of sponsorshipto our organization.

There are 200 reasons why agentssay they like to do business withMutual Benefit Group. Our people.

People they know by name. There’sSally, who has been underwritingbusiness in MBG’s Personal LinesDepartment for 45 years, and Elaine,who’s handled commercial accounts for31. Patsy has 40 years’ experience in theClaims Department; Joyce has beenprogramming computer applications for37 years. For 34 years, Shelby’s beenhandling payments and answeringquestions about billing. Linda’s beenwith the company 32 years, taking morethan 800 calls a day as a receptionist.

Since 1908, Mutual Benefit has nurtureda relationship-driven corporate culturethat provides uncommon support for itsemployees, who in turn deliver anuncommon insurance experience toagents and policyholders alike. Thecompany enjoys a low employeeturnover rate of six percent. Seventy-three percent of employees have beenwith the company five years or more;thirty percent, 15 years or more. MutualBenefit also makes a major commitmentto professional development. In 2007,ninety-three percent of MBG’semployees completed at least onecompany-reimbursed education coursewith 26 earning a professional insurancecredential.

In an industry where expertise is criticaland employee turnover is common,agents have commented on how muchthey appreciate knowing they will reachthe same personable, experiencedprofessional each time they call MutualBenefit. As one agent put it, “In today’s

world, it’s very unusual to see anybusiness have the same excellent staffcontinue to work for them for such anextended period of time as is the casewith Mutual Benefit. The people at MBGoffer prompt, professional service whilenever losing sight of adding a littlefriendly conversation along the way. Icouldn’t imagine working in theinsurance industry without MutualBenefit Group.”

Selecting and retaining top-notchprofessionals is just one of the waysMutual Benefit exhibits its commitmentto its 250 independent agents and itsmore than 80,000 policyholders.Supporting the independent agencysystem for 100 years has given MutualBenefit a unique perspective on theimportance of fostering strong businessties with agents. We understand howcritical it is to remain accessible toagents, and how important it is to listento their needs in order to respond in away that benefits everyone in thebusiness relationship.

As the Insurance Agents and Brokersconducted their third CompanySatisfaction Index Survey in 2008,Mutual Benefit Group for the third time

in a row placed among the top threeinsurance carriers in its area ofoperation, ranking number one overallin commercial lines and number twooverall in personal lines. Mutual BenefitCEO Steve Sliver maintains that thecompany’s combined score for bothcommercial and personal linesdistinguishes it as the best-performingcompany overall. “The survey resultsreflect our staff’s one-of-a-kindcommitment to accessibility andresponsiveness as they provide agentswith the conscientious service, flexibleunderwriting, quality products,exceptional claims handling, andtechnological systems that agentsdemand and deserve.”

As Mutual Benefit enters its secondcentury in the insurance industry with acorporate culture dedicated to buildingstrong relationships, it’s not surprisingthat “You Know Who we ARE(Accessible, Reliable, Experienced.)” Wereaffirm our commitment to a strongrapport with agents, a rapport that elicitscomments like this: “I treasure myrelationship with Mutual Benefit and itsmany fine people. They always travelthe high road.”

Platinum Profile

G9616_12-17June09PrimAg.qxd 5/14/09 7:41 AM Page 16

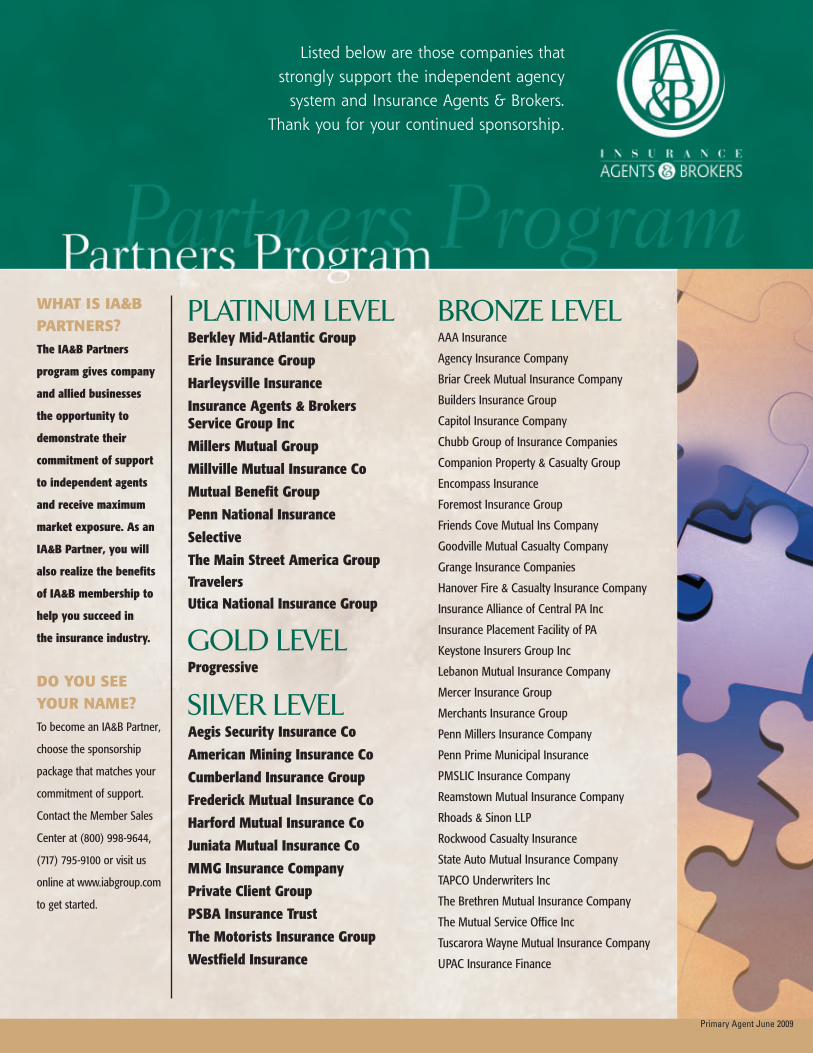

WHAT IS IA&BPARTNERS?The IA&B Partners

program gives company

and allied businesses

the opportunity to

demonstrate their

commitment of support

to independent agents

and receive maximum

market exposure. As an

IA&B Partner, you will

also realize the benefits

of IA&B membership to

help you succeed in

the insurance industry.

DO YOU SEEYOUR NAME?To become an IA&B Partner,

choose the sponsorship

package that matches your

commitment of support.

Contact the Member Sales

Center at (800) 998-9644,

(717) 795-9100 or visit us

online at www.iabgroup.com

to get started.

Listed below are those companies that strongly support the independent agency

system and Insurance Agents & Brokers.Thank you for your continued sponsorship.

PLATINUM LEVELBerkley Mid-Atlantic Group

Erie Insurance Group

Harleysville Insurance

Insurance Agents & BrokersService Group Inc

Millers Mutual Group

Millville Mutual Insurance Co

Mutual Benefit Group

Penn National Insurance

Selective

The Main Street America GroupTravelersUtica National Insurance Group

GOLD LEVELProgressive

SILVER LEVELAegis Security Insurance Co

American Mining Insurance Co

Cumberland Insurance Group

Frederick Mutual Insurance Co

Harford Mutual Insurance Co

Juniata Mutual Insurance Co

MMG Insurance Company

Private Client Group

PSBA Insurance Trust

The Motorists Insurance Group

Westfield Insurance

BRONZE LEVELAAA Insurance

Agency Insurance Company

Briar Creek Mutual Insurance Company

Builders Insurance Group

Capitol Insurance Company

Chubb Group of Insurance Companies

Companion Property & Casualty Group

Encompass Insurance

Foremost Insurance Group

Friends Cove Mutual Ins Company

Goodville Mutual Casualty Company

Grange Insurance Companies

Hanover Fire & Casualty Insurance Company

Insurance Alliance of Central PA Inc

Insurance Placement Facility of PA

Keystone Insurers Group Inc

Lebanon Mutual Insurance Company

Mercer Insurance Group

Merchants Insurance Group

Penn Millers Insurance Company

Penn Prime Municipal Insurance

PMSLIC Insurance Company

Reamstown Mutual Insurance Company

Rhoads & Sinon LLP

Rockwood Casualty Insurance

State Auto Mutual Insurance Company

TAPCO Underwriters Inc

The Brethren Mutual Insurance Company

The Mutual Service Office Inc

Tuscarora Wayne Mutual Insurance Company

UPAC Insurance Finance

Primary Agent June 2009

G9616_12-17June09PrimAg.qxd 5/14/09 7:41 AM Page 17

HUMAN RESOURCES

How an agency handledan employee’sabsenteeism with helpfrom HR Solution©

G9616_18-21June09PrimAg.qxd 5/14/09 6:17 AM Page 18

[ 19 ]

Primary Agent | June 2009

IssueWhen one of her eight employees started habitually calling offof work, Angela Malizia fretted over what she could do.

“She said that she didn’t want to use vacation time and thatwe should just dock her pay,” said Malizia, vice president ofThe Lunar Agency Inc. in Newtown Square, Pa., “but wecouldn’t afford to have someone away from that desk.”

To further complicate the issue, after each time the employeemissed a series of days, she returned to the office with adoctor’s note. Malizia wondered what — if any — recourseshe had.

“I didn’t know what I was allowed to say or do,” she said. “Wewere afraid of getting sued.”

SolutionMalizia referred to the HR Solution© and enlisted the help ofthe on-call consultation service. From there a humanresources professional walked Malizia through her options.

“I learned that I couldn’t refuse her requests without making itan agency policy that employees must use vacation time first,”she said. “Then, because her excuses were not illnessesprotected under the disability act, I could write her up.”

Malizia confided that initially she was fearful of therepercussions and probably wouldn’t have addressed theabsenteeism without being able to rely on advice from thehuman resources consultant.

“When you’re a small-business owner, it’s hard to keep upwith laws and changes and what you are and aren’t allowedto do,” she said. “It’s comforting to have these resources.”

ResultToday The Lunar Agency’s new employee handbookaddresses absenteeism as well as a host of other issues. It’sthe backbone of the agency’s human resources function …and it pleases Malizia’s EPLI carrier.

“Our EPLI carrier has been on our case to get an employeehandbook,” she said. “The template included with the HRSolution© is great. If it hadn’t been for the template, ourhandbook would still be on the back burner.”

Malizia also completed the HR Solution© audit and waspleasantly surprised to learn about the areas in which heragency was already compliant.

“It reinforced what we are doing right,” she said.

Malizia plans to rely on the HR Solution© when she hires newemployees as well, citing how overwhelming the number of

Each agency’s primary member

(labeled as the Agency

Administrator in IA&B’s

database) can access HR

Solution© by logging onto

iabgroup.com, selecting Agency

Operations from the left-hand

navigation bar and then clicking

the Employee Management link.

Questions about re-assigning the

primary member status or

accessing HR Solution© can be

addressed with the IA&B

Member Service Center, available

by calling (800) 998-9644,

Option 0.

G9616_18-21June09PrimAg.qxd 5/14/09 6:17 AM Page 19

state and federal forms are andhow even lawyers aren’t always ontop of human resources practices.

“The HR Solution© is a greatresource,” said Malizia. “I’mthrilled.”

[ 20 ]

HUMAN RESOURCES

You can’t put a price on reliability.For 35 years, Shelby Metz has been tallying premium checks and answering billing questions every Monday through Friday. Her accuracy, availability, and personal attention come included with each policy. That’s reliability. That’s the MBG Experience.

come included with eachh policy.That’s reliability. That’s tthe MBGExperience.

www.mutualbenefitgroup.com

MUTUAL BENEFIT GROUP

Huntingdon, PA

You know who we ARERERE

IA&B’s HR Solution© is a collection

of human resources products

and services available exclusively

to members.

◗ HR audit: questionnaire to identify andprovide guidance on areas of HR non-compliance

◗ HR handbook: template to create alegally compliant employee handbook

◗ HR administrative guide: guidance forimplementing the employee handbook

◗ HR administrative tools: collection offorms and tools from the administrativeguide in an easy-to-access format

◗ On-call consultation: access to HRprofessionals for base-level support

◗ Discounted professional services: 15%discount on professional services fromHuman Resources ManagementAssociates, Inc.

G9616_18-21June09PrimAg.qxd 5/14/09 6:17 AM Page 20

G9616_18-21June09PrimAg.qxd 5/14/09 6:17 AM Page 21

AGENCY MANAGEMENT

Don Rumbaugh credits his involvement with the Best Insurance Group for advancing his agency.

Talking shop with anaggregator advocate

G9616_22-25June09PrimAg.qxd 5/14/09 6:21 AM Page 22

[ 23 ]

Primary Agent | June 2009

Don Rumbaugh entered the industry in 1972 andopened his own agency, Rumbaugh Insurance,in Hanover, PA, in 1982. Now in his early sixties,Rumbaugh is doing the opposite of manyagency principals his age: He is bringing onsales people and planning to double the size of

his agency in the coming years.

Ask him why, and he’ll sing the praises of Best InsuranceGroup — the cluster he joined four years ago.

Clusters, also known as aggregators, are groups of agenciesthat combine their production volume while maintainingindividual ownership. While their individual terms andarrangements vary significantly, the concept as a whole iscatching on. According to the 2006 Future One AgencyUniverse Study, 19 percent of respondents said they wereinvolved in an aggregate arrangement, with the largestpercentage having annual revenues of under $1-2 million.

“In today’s world, how do you have a $1 million agency andmove on to the next level?” asks Rumbaugh, who points to thebenefits of clustering for helping his agency do just that.

Inner workingsBest Insurance Group can most accurately be described as awell-functioning family. There are the occasionaldisagreements, but the members look out for each other’s bestinterests. Instead of competition, there is genuine teamwork.

We complement each other the best we can,” says Rumbaugh.As proof, he tells the story of a female member of the groupwho ran across a good-old-boy network when quoting newbusiness. She countered by taking along a fellow (male) cluster member to pitch the policy, and she walked away withthe business.

Rumbaugh also points to the benefits of a pooled knowledgebase. From knowing where to go with a particular risk toupdating his phone system, he relies on suggestions from the group.

“It’s so demanding,” he explains. “A principal is supposed toknow everything and be knowledgeable about HR, finance,training and dealing with insurance companies. You can get alot of information from the group, including how to run aninsurance agency.”

Various aggregation models are structured differently, butmembers of Best Insurance Group each maintain their autonomy.

“We’re spokes on a wheel,” explains Rumbaugh. “We run ouragencies how we want to and come together for productionand maximizing contingencies.”

Clusters began in the 1970s and,

by the 1980s, allowed

aggregators to offer services

across state lines.

“In today’s world, how do you

have a $1 million agency and

move on to the next level?” asks

Rumbaugh, who points to the

benefits of clustering for helping

his agency do just that.

D

G9616_22-25June09PrimAg.qxd 5/14/09 6:21 AM Page 23

However, they haveconsidered merging theiraccounting efforts and are inthe initial planning stages ofadopting the same agencymanagement system.

“Our Philipsburg member e-mailed to say he wasclosing at noon due to an icestorm,” he recalls. “If we wereon the same system, he couldhave redirected his agency’scalls to another member ofthe cluster.”

Carrier responseBest Insurance Group holdstwo meetings per month –one for owners and anotherfor producers. During thecourse of conversation,members will share their

recent experiences withcarriers. When a company’sstory does not match up orwhen multiple agencies areexperiencing a similarproblem, the group invites acarrier representative toattend a meeting andaddresses the issue head on.

“We don’t want special deals,” says Rumbaugh, “but collectively, we can make changes.”

While an aggregator’s fewercontracts and additionaldistribution points benefitcarriers, not all clustersbehave as nicely as BestInsurance Group, and somecompanies are gun shy as a result.

[ 24 ]

AGENCY MANAGEMENT

Aggregate arrangements varyconsiderably, depending on theirpurpose, revenue streams, ownershipand involvement with member agencies’ structures. They can becategorized into four models:

◗ agency franchise operations,

◗ agency platform operations,

◗ managed agency organizations and

◗ market access cooperatives.

G9616_22-25June09PrimAg.qxd 5/14/09 6:21 AM Page 24

“Some aggregators have throwntheir weight around, andcompanies begin to think that allclusters are bad,” he explains.Recently he was approached bya carrier who would not write fora cluster.

Escape planAggregate arrangements havebeen known to cause problemsfor agency members as well —particularly when one memberchooses to leave. In fact,according to the Big “I” VirtualUniversity report “EvolvingOptions for IndependentInsurance Agent & BrokerDistribution: Aggregators,Alliances, Franchises &Networks,” separation from acluster is the most commonchallenge for agencies.

However, Best Insurance Groupis structured more simply thansome.

“It’s selective to get in but easyto get out,” explains Rumbaugh.“There is no penalty for leaving,and I don’t get dictates from the group.”

ConsiderationsPrincipals who consider enteringa cluster are encouraged toresearch the opportunities andconsequences thoroughly andtalk with their legal counsel, tax advisors and carrierrepresentatives. For those whofind an ideal arrangement, thepayoffs can be great.

“I’m sold on this,” Rumbaughoffers. “I believe it’s the way to go for smaller agencies to grow.”

[ 25 ]

G9616_22-25June09PrimAg.qxd 5/14/09 6:21 AM Page 25

ANGELYN S TREUTELCPA

Angelyn Treutel is treasurer, vice

president, and chief information

officer of Treutel Insurance

Agency, as well as chair of the

Agents Council for Technology

(ACT). Angelyn can be reached

Available online at

www.independentagent.com/act,

ACT is part of the Independent

Insurance Agents & Brokers of

America. For more information

about ACT, contact Jeff Yates,

ACT Executive Director at

[email protected]. This article

reflects the views of the author

and should not be construed as

an official statement by ACT.

Primary Agent | June 2009 TechnologyU P D A T E

[ 26 ]

A disturbing reality is that theinsurance industry is aging,with the average age ofagency principals at 51 andthe average age of the agencycustomer base at 53. Currentstatistics indicate that there are2.3 million workers in theinsurance industry, and morethan 1.0 million of theseworkers will reach retirementage in the next 10 years.Where are all of the youngpeople? How do we attractthem to our industry? Andhow do we position ouragencies to succeed in the future?

Out of the mouths of babesLast fall, ACT sponsored atechnology forum at the IIABA

Young Agents LeadershipInstitute to discussgenerational differences and technology preferencesfrom the perspective of young agents. The group ofmore than 70 young peoplewas predominately made upof Generation X (under age46) and Millennials (under age 28).

In the young agents’ opinion,Boomers (over age 44) aremotivated differently from theyounger generations andmeasure their success in lifeby their career achievementsand seem to assess theproductivity of theiremployees by the number ofhours they put in. The X’ersbelieve they are more willing

to try new things, are moreimpatient than Boomersbecause they want everythingnow and measure productivityby “getting the job done.”

The Millennials are the mosttech savvy with digitaleverything and are even moreimpatient than the X’ersbecause they don’t just want itnow, they wanted it yesterday!The young agents suggestedthat the best way to describethe generations was to listento how they greet theirfriends: Boomers will ask“How’s your job?” X’ers willask “How’s your family?” AndMillennials will ask “What didyou do this weekend?”

YOUNG AGENTS SPEAKOUT ON GENERATIONDIFFERENCES ANDTECHNOLOGY NEEDS

G9616_26-28June09PrimAg.qxd 5/14/09 6:26 AM Page 26

[ 27 ]

Intermingling While everyone in the room smiled at the distinct differencesbetween the generations, there was no dispute that thedifferent generations need to understand one another and workeffectively together. Some of the agents said they had been verysuccessful in addressing the natural friction between producersand CSRs (particularly when the differences are generational)by taking the CSRs on client visits, so the CSRs have a betterunderstanding of what the producers do and the support theyneed. Likewise, the producers discussed the CSRs’ workflowwith them in order to gain a better understanding of theirparticular needs and frustrations.

The young agents encouraged agency principals to support adiscussion of generational differences within the agency andadopt flexible employee policies that are results driven andreflect the needs of the different generations. After all,generations are evolutionary, and each will change theirperspectives based upon their life cycles of graduating fromcollege, getting their first job, getting married, starting a family,buying a home, becoming absorbed in their careers andbeginning preparations for retirement. The same is true of our customers.

AdvancingYoung people are well suited for the insurance industry because they enjoy working in teams and working with people.They also have a keen insight into how other young peoplethink and are more adept at soliciting young people as clients.With the profound changes in marketing that we are starting tosee from the emergence of the Social Web (Facebook, Twitter,LinkedIn, etc.), the younger generations can teach establishedagencies how to be visible in cyberspace where the young andyoung-at-heart do their research, purchase products andnetwork. What a wonderful opportunity we have as agents tobegin to use these tools, not only to learn about new ways tocommunicate and network, but to establish a marketingpresence to attract new clients.

The young agents pointed out that the Social Web enables them to do virtual networking in a similar way to the in-personnetworking Boomers have excelled at in their communities. Infact, social networking is putting the person back into theInternet which promises to put relationship-oriented agents into a stronger position than when the Internet was dominatedby large corporate direct-writing companies.

Targeting younger consumers may be a longer term investmentbecause the Millennials may not yet have a need for complexinsurance products. But haven’t we discussed capturing theseemerging customers when they are young, just as ourcompetitors have done for years? Now we have the competitiveinsurance products to do it. We need to look at the lifetimevalue of these insureds because soon they will be startingfamilies, purchasing homes and establishing businesses. If we

have a presence on the Internet forums where they arecomfortable and if we are capable of doing business their way,they will recognize us for what we are — their trusted advisor.

Internet customers are known to lack loyalty, but agents stillneed to reach out to these customers, work to developrelationships and add value to their purchasing process. If aconsumer gets a quote and a policy with no counseling, there isno value added and that customer is likely to change carriersfrequently. But if an agent is able to insert herself into theprocess offering additional quotes, optional coverage andinsurance advice, we can change the customer into a loyalclient. As they become familiar with our services, they will seekour advice for their more complex coverage needs. Muchresearch has shown that consumers may do their research onthe Internet, but most people still want to do business withpeople and buy insurance from them.

VentingTurning to the technology in the agency office, the youngagents expressed extreme frustration with continued processinginefficiencies and voiced the immediate need for all carriers andagencies to embrace Real Time. Consumers demand a real-timeresponse today, and we need to implement the tools to provideit. With Real Time, agents are able to work with their multiplecarriers through their agency management systems and

Penn Millers Insurance Company1.800.233.8347 • www.pennmillers.com

PennEdge is Penn Millers’ platform to provide property,crime, liability, umbrella and automobile coverages

for targeted middle-market insureds. PennEdge is tailored to provide special coverage features to

our target market customers.

Target Markets: Hospitality Providers, Laundries & Dry Cleaners, Manufacturers, Printers, and Wholesalers

To be a successful business you need an edge.

Policies manufactured specifically for your clients’ needs.

G9616_26-28June09PrimAg.qxd 5/14/09 6:26 AM Page 27

[ 28 ]

comparative raters, rather than having tolog on and enter data into multiplecarrier Web sites.

Today’s consumers are bombarded withthe advertising claims of direct-writercompetitors who can provide quotes inonly 15 minutes, and without Real Timeprocessing, independent agents areunable to meet these consumerexpectations because our archaicprocesses are too slow. Unfortunately,there is still far too much clerical effortrequired in the agency office, the youngagents added. Agents need to demandReal Time from their carriers and MGAs,so they can provide direct value-addedservice to their clients and use their timeto create relationships and make sales.

The young agents said that carriers, too,need to be able to provide more of apersonal touch and supply dedicatedunderwriters, rather than taking a 1-800-UNDERWRITER approach, as manycarriers currently do. To be most effective,the young producers said they need theircarriers to work with them to assist withcomplex coverage issues and risks thatdo not quite fit into the “black box.” Andthe young agents added: please let usknow with whom to work if ourunderwriter is out of the office so that wecan handle the risk promptly!

ForecastingWhat new competition does the futurehold? The young agents feel that Internetdistributors, niche marketers and largercluster agencies will be the forces to bedealt with over the next three years. Withnew technology emerging at exponentialrates, the agency of the future will havegreat opportunities to leverage these newapplications to expedite sales andservicing. Agencies that stay on top oftechnology by keeping up with thecurrent versions of their systems and

implementing available tools (such asReal Time, Commercial Lines Downloadand electronic information management)will be best positioned to take advantageof these new opportunities. Technologyenables our machines to do the clericaland mundane work to free agents andCSRs to do what they do best — workwith people and make sales.

The young agents raised severaladditional useful and energizing ideas to add value for agency clients, such as offering chat capability on the Website, creating specialized Web sites forniche marketing, providing customeraccess portals on Agency Web sites, using virtual meetings through theInternet with small business clients andresearching and communicating withclients using social networks.

What is the message? We need tocontinually reach out to youth, via theInternet and the Social Web, in ouradvertising and in our communities.Young employees are best positioned toattract young prospects. And agencieswhich are innovative with technology and have flexible employee policies thatare results driven will be most likely toattract young employees.

A perfect way to introduce young peopleto our industry is through IIABA’s ProjectInVEST. The Trusted Choice brand,likewise, offers agencies a modern andvalue-added identity that positions themwell to attract the future generations ofconsumers and employees.

TECHNOLOGY UPDATE

Commonwealth Insurance Co . . . . . . . . . . . . .21

EMC Insurance Compannies . . . . . . . . . . . . .IFC

Eastern Dentists Insurance Co . . . . . . . . . . . . .14

General Casualty . . . . . . . . . . . . . . . . . . . . . . . .32

IA&B Series Ads . . . . . . . . . . . . . . . . . . . . .24, IBC

IA&B Partners Program . . . . . . . . . . . . . . . . . . .17

Interstate Insurance Mngmnt. . . . . . . . . . . . .OBC

KnightBrook Insurance Co . . . . . . . . . . . . . . . .11

Millers Mutual Group . . . . . . . . . . . . . . . . . . . .25

Mutual Benefit Group . . . . . . . . . . . . . . . . . . . .20

Penn Millers Insurance Co . . . . . . . . . . . . . . . .28

Preferred Property Program . . . . . . . . . . . . . . .20

Susquehanna Ins Agents Alliance . . . . . . . . . . . .5

TAPCO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

ClassifiedA D V E R T I S E M E N T S

Ad Index

SOUTHEAST PA PRODUCERS & AGENCIES

Professional agency located inFeasterville, Bucks County, Pa. Call for confidential information and a review of our services. Contact Ray Reinard at (215) 375-8600, Ext. 119.

If you would like to place a

Classified Advertisement, simply

fax your ad on company letterhead

to (717) 795-8347, and we will take

care of the rest.

G9616_26-28June09PrimAg.qxd 5/14/09 6:26 AM Page 28

G9616_C2C3C4June09.qxd 5/14/09 6:40 AM Page 2

G9616_C2C3C4June09.qxd 5/14/09 6:40 AM Page 3