Embed Size (px)

Citation preview

Journal of Multinational Financial Management

11 (2001) 407–426

Price differentials between different classesof stocks: an empirical study

on Chinese stock markets

Clas Bergstrom a,*, Ellen Tang b

a Department of Finance, Stockholm School of Economics, P.O. Box 6051, 11383 Stockholm, Swedenb Standard Chartered Bank, 7/F., 4-4A Des Voeux Road, Central, Hong Kong, China

Received 15 July 2000; accepted 28 February 2001

Abstract

This paper investigates the effect of strict segmentation on pricing in the context of theChinese stock markets. The paper demonstrates that information asymmetry between foreigninvestors and domestic investors, liquidity effects, diversification effects, clientele bias,risk-free return differentials between foreign and domestic investors, and foreign exchangerisks are significant factors in explaining discounts on shares that can only be owned byforeign investors. © 2001 Elsevier Science B.V. All rights reserved.

JEL classification: G12; G15

Keywords: Market segmentation; Asset pricing; Chinese stock markets

www.elsevier.com/locate/econbase

1. Introduction

In the Chinese stock markets, strict ownership segmentation is implemented, andtwo classes of shares — domestic-only shares (A shares) and foreign-only shares (Bshares) — are traded. Bailey (1994) gives evidence of discounts on foreign-only-shares relative to domestic-only-shares. Fernald and Rogers (1998) argue that thelower return required by domestic investors, and little domestic investment oppor-tunities in China contribute to the price discount. Chakravarty et al. (1998) model

* Corresponding author. Tel.: +46-8-7369152; fax: +46-8-312327.E-mail address: [email protected] (C. Bergstrom).

1042-444X/01/$ - see front matter © 2001 Elsevier Science B.V. All rights reserved.

PII: S1042 -444X(01 )00039 -1

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426408

the effect of information asymmetry on the discount on stock prices in a strictlysegmented market. Gordan and Li (1999) argue that legal restrictions create thesegmented market and limit investment opportunities. Thus, domestic investorshave inelastic demands for equity due to insufficient supply, pushing up the price ofclass A shares.

In a related study, Errunza and Losq (1985) argue that in partially segmentedmarkets, securities inaccessible to a subset of investors demand a risk premium.1

Hietala (1989) devise a model that suggests domestic investors pay less under mildsegmentation; and this is verified by empirical data from the Finnish market.Bergstrom et al. (1993) analyze stock pricing when domestic investors face a cap oninvesting in foreign assets, and when foreign investors are restricted to investing indomestic assets. They find that domestic investors pay a premium to invest inforeign assets while foreign investors pay a premium to invest in domestic assets.

In contrast to other stock markets with similar ownership segmentation, theChinese stock markets have substantial, yet persistent, price discounts on foreign-only-shares relative to domestic-only-shares.2,3 Given this special phenomenon, thispaper analyses potential causes that can explain the price discount.4 The paper isstructured as follows: Section 2 presents the institutional setting, Sections 3 and 4perform analysis of cross-sectional and time-series data; and Section 5 presents ourconclusions.

2. Institutional setting

Shanghai Stock Exchange (SHSE) and Shenzhen Stock Exchange (SZSE) startedtrading in the early 1990s.5 Since then, public equity markets have developed

1 Under partial segmentation, one class of shares is available to all investors and the other class isavailable to a subset of investors. However, in the Chinese stock markets, segmentation is strict, underwhich one class of shares is only available to domestic investors while another class of shares is onlyavailable to foreign investors.

2 Examples of other markets that segment ownership are Switzerland, Mexico and the Philippines. Thedegree of segmentation varies between different markets. According to Wo (1997), the Chinese stockmarkets are the only markets covered by the International Finance Corporation that employ strictsegmentation.

3 The phenomenon of discounting foreign-only shares relative to domestic-only shares previouslyappeared in other markets, such as the Stockholm Stock Exchange. However, according to Fernald andRogers (1998), by the end of 1996, only the Chinese stock markets still demonstrated such aphenomenon.

4 The paper is an extension of Tang (1999), a master thesis authored by Tang and supervised byBergstrom.

5 There are other regional Stock Exchanges, e.g. Beijing Stock Exchange and Chengdu StockExchange, offering domestic-only shares. However, only SZSE and SHSE offer both domestic-onlyshares and foreign-only shares.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 409

quickly. In May 1999, total market capitalization of the equity market of the twoexchanges reached US$ 267 billion. In July 1999, the number of listed companieshad risen to 904 from 599 in 1996.

Only a part of the total outstanding shares are traded publicly. Shares that arenot tradable publicly are held by state or government agencies, by the companiesthemselves, and by company employees. In May 1999, the total market capitaliza-tion of freely traded shares amounted to US$ 80.4 billion, i.e. 30% of the totalmarket capitalization.6 There are two classes of tradable shares: A shares and Bshares. Class A shares can only be owned and traded by Chinese citizens, exceptthose who are citizens of Hong Kong and Macau. Class A shares are denominatedand traded in local currency, i.e. Chinese yuan. Class B shares, listed on SHSE andSZSE, can be owned and traded by foreign citizens and by citizens of Hong Kongand Macau as well.7,8,9. Also, B shares carry the same voting and dividend rights asA shares. While B shares are denominated in Chinese yuan, they are traded inHong Kong dollars in SZSE and US dollars in SHSE. Cross trading between Ashares and B shares is prohibited; segmentation is strict and tight.

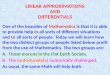

Fig. 1. Price discount over time.

6 Total market capitalization is the market value of all outstanding shares, both tradable andnon-tradable. All the statistics given in this paper relate to SZSE and SHSE only, excluding otherregional exchanges that can only offer domestic-only shares.

7 SHSE and SZSE are the only exchanges in China that offer B shares. There are other foreign-only-shares, H shares and N shares, listed overseas. H shares are listed on the Stock Exchange Hong Kong(SEHK) and are traded in Hong Kong dollars. N shares are listed on the New York Stock Exchange(NYSE) and London Stock Exchange (LSE) and are traded in US dollars.

8 Investors holding a foreign passport are eligible to register as foreign investors.9 In Fernald and Rogers (1998), the authors refer to an analyst in Shanghai who claimed that 40% of

B shares are owned by overseas Chinese or domestic residents who use various means to circumvent thelegal barriers. However, it is purely based on the analyst’s opinion and there is no official estimateavailable regarding patterns of share ownership. We will assume that only eligible investors are engagedin trading B shares.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426410

Class B shares have almost always been traded at a discount to A shares. For asample of 79 companies, the average daily price discount of B shares to A sharesduring the period January 1, 1995 to August 31, 1999 exceeded 69% (with astandard deviation of 10.67%). Fig. 1 reveals that the discount on B shares has beensustained over time, thus suggesting that there exist underlying factors of anongoing character that support it. The discount also demonstrates variability overtime. In the following sections, two models will be constructed to explain theunderlying cross-sectional variations and time variations in the B share discount.

3. Cross-sectional analysis

The cross-sectional model investigates company specific factors related to infor-mation asymmetry, relative liquidity, diversification benefits, company size, andratio of tradable A shares to B shares, as well as the stock exchange on which thecompany is listed. The dependent variable is the average daily price discount forindividual companies, i.e.

discounti=pai−pbi

pai

(1)

where pji is the price of j-shares and j=A, B for company i.

3.1. Hypotheses

3.1.1. Information asymmetry contributes to the discount on B sharesChakravarty et al. (1998) argue that foreign investors demand a risk premium to

compensate for their disadvantage in information relative to domestic investors.They find that the price difference between A shares and B shares is:1. negatively proportional to cov(uai, ubi)/var(P� ai), where cov(uai, ubi) is the covari-

ance between the A-share return and B-share return and var(P� ai) is the varianceof the A-share price; and

2. positively proportional to var(ubi), i.e. the variance of the B-share returns.Intuitively, the first proxy measures the return sensitivity of B shares to A shares.

A high covariance implies that the A-share return is informative of the B-sharereturn. A high covariance implies that foreign investors can more easily infer theB-share price from the A-share price, which incorporates information not accessibleby foreign investors. A high volatility of A shares makes it difficult for foreigninvestors to infer the B-share price. Therefore, the B-share return sensitivity isnegatively related to the discount on B shares. The second variable is the varianceof the B-share return. The larger the volatility of the B-share returns, the moredifficult it is for foreign investors to make predictions. Thus, B-share returnvariance carries a positive relation to the B-share discount. Media coverage oncompanies (REPORTi) is a third proxy for information asymmetry. The moreextensive the media coverage, the more information accessible to foreign investors.Thus, the REPORTi variable is negatively related to the discount.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 411

3.1.2. The B-share discount is related to the relati�e liquidity of B shares to Ashares

Investors demand a liquidity premium if it is costly and time-consuming to liquidatea position. If the B share is illiquid relative to the A share, foreign investors demanda larger liquidity premium on the B shares, creating a price discount on B shares.The first proxy of liquidity is relative spread:

(SPREAD(bi)/pbi)(SPREAD(ai)/pai)

,

where SPREAD(bi) and SPREAD(ai) are bid-ask spreads of B shares and A shares,respectively, each of which is divided by stock price to adjust for higher A-share price.Since spread is a negative measure of liquidity, the relative spread is positively relatedto B-share discount.

The second proxy is relative trading volume (VOL(bi))/(VOL(ai)), where VOL(bi)and VOL(ai) are the trading volumes of B shares and A shares, respectively. Thelarger the ratio, the more liquid the B-share trading is relative to the A-share trading;and the smaller is the discount on B shares.

3.1.3. Di�ersification benefits offered by B shares to foreign in�estors reduce theB-share discount

Foreign investors require a lower return on B shares if these shares providediversification benefits. Portfolio theory suggests that an asset provides diversificationbenefits if its return demonstrates a less than perfect positive correlation with portfolioreturn. The correlation of B-share return, (ubi), with the portfolio return, (umarket),(corr(ubi, umarket)), is a proxy of the diversification benefits and has a positive relationto discount on B shares.

3.1.4. The discount of B shares is negati�ely related to company sizeInvestors might find it easier to collect information about and trade shares in large

companies. Therefore, company size holds a negative relationship to the discount.Company size is proxied by total market capitalization of both A shares and B shares.

3.1.5. The B-share discount is negati�ely related to the ratio of tradable A sharesto B shares

If, by the impact of price pressure, the supply of A shares is greater relative to thatof B shares, the price of A shares relative to B shares will be lower; and, consequently,the B-share discount will also be lower.10

3.1.6. There exists a bias against stocks listed on SHSE such that discount onSHSE B shares is higher

According to the legal framework, SHSE and SZSE should operate in similarmanner and therefore there should not be a clientele bias against companies listedon any of the two stock exchanges. However, Chakravarty et al. (1998) and Fernald

10 Tradable A shares are used since these reflect the market better than the total number ofoutstanding A shares.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426412

and Rogers (1998) find that investors appear to be biased against the companieslisted on SHSE. We use a dummy with the value of 1 if the shares are listed atSZSE and zero if the shares are traded at SHSE. In line with previous findings, thedummy variable is expected to carry a negative relationship to the discount.

3.2. Data

The data have been collected for the period January 1995 to August 1999 inrespect of 79 companies, 39 of which are listed on SHSE and 40 on SZSE. The testis done on a quarterly basis.11 A sample size of 1213 has been set.12 The data usedare the daily closing prices, with those of B shares being converted into yuan bymeans of daily closing spot exchange rates. Beside covariances and variances, dailynumbers are computed first, and an average is calculated for each quarter for all thevariables. Covariances and variances are computed using daily returns and closingprices for each quarter.

Due to a lack of information, total market capitalization, instead of negotiablemarket capitalization is used as a proxy for company size. Values of tradable Ashares to B shares are yearly based. Trading volume is measured as the number ofshares traded. The REPORTi variable measures the number of times ReutersBusiness Briefing — chosen as the medium for its broad coverage — carries anarticle about that company in each quarter. The Morgan Stanley MSCI index(MSCI) is chosen to represent the market portfolio. An alternative representationof the market portfolio is Hang Seng Index (HSI).13 This index is taken to representthe market portfolio of investors from Hong Kong, whom we believe to be theactive investors in B shares.

3.3. Results

3.3.1. Descripti�e statisticsThe coefficients of variation reveal that the independent variables show a

relatively larger dispersion than the discount. At the beginning of 1995, the B sharesof some companies were traded at a premium. This corresponds to the resultusually found in partially segmented markets where foreign investors pay a pre-mium to invest in domestic stocks.14 However, only a few companies exhibitB-share premiums and over time, these B-share premiums eroded and B-share

11 The authors have also conducted a sensitivity analysis by running a yearly-based test. The resultsdiffer only slightly and are therefore not reported here.

12 Since some of the companies were listed after January 1995, the sample size is 1213, instead of 1501,i.e. 79 companies multiplied by 19 quarters in the period of January 1995 to August 1999.

13 The Hang Seng Index is the tracking index for the main trading board of the Hong Kong StockExchange.

14 Hietala (1989) and Errunza and Losq (1985).

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 413

discounts emerged. This observation supports the methodology for the cross-sec-tional test using quarterly data to capture time variations. The maximum relativetrading volume looks excessive. However, this is due to a few outliners. Trading inB shares is in general thinner than A-share trading, as indicated by the median. Thecorrelation between B-share returns and the returns on MSCI and HSI is very low.A sensitivity analysis has been conducted on weekly and monthly returns, andyields similar low coefficients. This illustrates the diversification benefits that Bshares provide (Table 1).

A strong pair-wise correlation between the independent variables, especially thatof SIZEi, ratio of tradable A shares to B shares and EXCHANGEi with most othervariables, raises concerns about multi-collinearity. (See Table A4 in Appendix A fordetails.) The strong pair-wise correlation is probably attributed to common compo-nents, such as foreign exchange rates, entering into the independent variables.Nevertheless, this alone does not necessarily imply multi-collinearity. First, inde-pendent variables such as EXCHANGEi and the ratio of tradable A shares to Bshares are statistically independent and should not introduce statistical bias.Secondly, the tolerance measure for the independent variables is much larger than0.1, and thus does not support the presence of multi-collinearity. Thirdly, multi-collinearity usually renders estimates insignificant. However, the tests reportedbelow yield significant estimates with expected signs. Finally, the stepwise regres-sion employed assists in rejecting independent variables that demonstrate multi-collinearity with other variables. Thus, multi-collinearity is not a concern.15

The three proxies of information asymmetry are strongly correlated, supportingthe appropriateness of proxies. With respect to the liquidity effect, the correlationbetween relative spread and relative trading volume is not very high. This raisessome suspicion regarding the appropriateness of at least one of them.

3.3.2. Test resultsThe linear regression estimates are summarized in Table 2 Model 1 includes all

independent variables. Model 2 includes the variables that have been foundsignificant by stepwise regression. Model 7 is similar to Model 1, with the MSCIreplaced by HSI. In all models, all independent variables show the expected sign. At5% confidence level, only company size is rejected. The results show that informa-tion asymmetry, illiquid trading of B shares, diversification benefits, ratio oftradable A shares to B shares and clientele bias are significant determinants of theB-share discount. In all models, the constant term is large, indicating that relevantfactors have been omitted.

Certain findings are particularly worthy of further discussion. The proxyREPORTi of information asymmetry is not significant in Models 3 to 6. The reasonis probably that the A share and B share prices respond to the news released withvarying degrees of sensitivity. Therefore, REPORTi is a rather rough proxy forinformation asymmetry.

15 Mendenhall and Sincich (1993).

C.

Bergstrom

,E

.T

ang/

J.of

Multi.

Fin.

Manag.

11(2001)

407–

426414

Table 1Descriptive statistics of variables (values are calculated on a quarterly basis)

Low S.D.Variables Coefficient ofMathematical Mean Median Highrepresentation variation

0.18347 0.262070.73271 0.95561 −0.46041Discount pai−pbi

pai

0.70009

0.0039 −0.01611 0.0040547 4.3213B-share return sensitivity 0.091860.000938

cov(uai,ubi)

var(P� ai)

0.0044271 2.10160.002106B-share return variance 0.0154 0.11739var(ubi) 0.00017.9560REPORTi 0.975578.1552 6 58 0.00

13.310386800.00Relative spread 7878467.92542906

SPREAD(bi)/pbi

SPREAD(ai)/pai

2.4677 2.974256.31 0.00Relative trading volume 0.299890.8297

VOL(bi)

VOL(ai)

corr(ubi,uMSCI) 0.43571 −0.42347 0.12970 5.56940.023288Coefficient of correlation of B-share 0.03288return with MSCI return

−0.24243 0.13057 2.0140Coefficient of correlation of B-share corr(ubi,uHSI) 0.064828 0.05005 0.59837return with HSI return

0.50940 0.84540.068452.57470.60253Ratio of tradable A shares to B shares Ri 0.4406.91 3058.8 1.03882944.3 1984.0 35613SIZEI

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 415

In models 1 and 7 the correlation coefficients between B-share return and thereturn on the market portfolio proxy have the expected sign and are significant. Theadjusted R2 is higher with HSI. The reason for this may be that investors in Bshares are active investors in companies listed on the Hong Kong Stock Exchange.When investors price B shares, they take diversification benefits into account.However, foreign investors that are not interested in markets like the Hong Kongmarket are unlikely to be interested in exploiting diversification gains that can beachieved by investing in Chinese B shares. The result also suggests that manyinvestors in B shares might come from Hong Kong. This sheds light on the homebias effect and responds to the suspicion that 40% of B-share trading is carried outby investors from Hong Kong or by overseas Chinese. Although investors fromHong Kong or overseas Chinese face certain information disadvantages relative todomestic investors, this fact suggests that information asymmetry should beof little relevance in explaining the B-share discount. In fact, information asymme-try, although significant, does not demonstrate an overwhelming explanatorypower.16

In line with the studies of Chakravarty et al. (1998) and Fernald and Rogers(1998), there exists a clientele bias against companies listed on SHSE. Both paperssuggest possible explanations for the bias, without providing any empirical tests.One of these is that investors in B shares are active investors in Hong Kong stockswho tend to pick B shares on SZSE due to proximity. Another reason is that thereare underlying differences between stocks listed on SHSE and SZSE. In fact, theEXCHANGEi variable bears a strong correlation with other independent vari-ables.17 However, from a legal perspective, SHSE and SZSE operate in a verysimilar fashion. It might be that the sole clientele bias against B shares on SHSEgives rise to such underlying differences, which are thus self-fulfilling. To resolvethis chicken-and-egg conundrum, a study in micro-market structure is required.

Looking at the increment in adjusted R2 from model 2–6, the variables, the ratioof tradable A shares to B shares, EXCHANGEi and the diversification effect are thestrongest factors in explaining the cross-sectional differences of the discount on Bshares.

3.3.3. Comparison with the Chakra�arty et al. (1998) studyThe Chakravarty et al. (1998) model is based on an investigation of 39 companies

from January 1994 to December 1996, and uses average figures. Independentvariables include the proxies for information asymmetry, beta of B share, companysize, exchange and ratio of outstanding A share to B share.18 Only the B-sharereturn sensitivity and beta are insignificant and the adjusted R2 is 67% (Table 2).

16 With yearly data, the information asymmetry was only weakly significant. This suggests that theinformation disadvantage is reduced when foreign investors have more time to gather information.

17 A regression analysis with EXCHANGEi as the single variable yields an adjusted R-square of13.4%. Although the explanatory power is large, EXCHANGEi does not capture all other factors.

18 The authors use the ratio of tradable A shares to B shares here, as it is a better reflection of the realmarket situation.

C.

Bergstrom

,E

.T

ang/

J.of

Multi.

Fin.

Manag.

11(2001)

407–

426416

Table 2Test results: the cross-sectional model, quarterly data, sample size: 1213

Expected 2 3 4 5 6 7Factors and 1signproxies/model

0.806Constant term 0.809 0.802(79.565b)(78.978b) (86.539b)

Information asymmetry−6.851−4.834 −7.309 −7.723 −4.657−5.066−4.899cov(uai,ubi)

var(P� ai)−

(−5.821b) (−6.091b) (−4.155b)(3.739b)(−4.328b) (−4.375b) (−5.566b)+ 3.416 3.498 3.697 3.7793.773 3.831var(ubi) 4.124

(3.050b) (3.058b) (3.196b) (3.729b)(3.683b) (−2.572b) (3.936b)−0.000728 −0.0009941 −0.0134−0.000538−0.001035REPORTi −0.001463−0.001398−

(−1.154) (−1.560) (−2.373a)(−2.451b) (−2.572b) (−1.786) (−0.870)

Liquidity0.00000037 −0.000000250.00000040 0.00000041 0.00000046−0.00000025SPREAD(bi)

SPREAD(ai)+

0 54 64 9(3.182b) (2.067a) (2.000a) (4.081b)(3.516b) (3.563b)

−0.01346 −0.0102 −0.0102 −0.0133−0.01326 −0.01324VOL(bi)/MKTCAP(bi)

VOL(ai)/MKTCAP(ai)−

(−5.052b) (−7.404b)(−7.293b) (−7.242b) (−5.170b)(−7.306b)

Di�ersification0.243 0.273corr(ubi, uMSCI) + 0.232 0.229

(7.215b)(6.605b) (6.847b)(6.685b)+ 0.3corr(ubi, uHSI)

(8.444b)

C.

Bergstrom

,E

.T

ang/

J.of

Multi.

Fin.

Manag.

11(2001)

407–

426417

Table 2 (Continued)

Expected sign 3 4 5 6 71Factors and 2proxies/model

Size−0.00000288SIZEi −0.000002199−

(−1.989a)(−1.506)

Ratio of tradable A shares to B sharesRi −0.0659− −0.07178 −0.07142 −0.121

(−5.957b)(−6.438b) (−6.403b) (−13.156b)

Stock exchange−0.115−0.08591EXCHANGEi −0.08543−

(−9.931b)(−7.596b) (−7.552b)5.4% 3.2% 26.2%9.4%20.9%24.6% 24.5%Adj. R2

T-statistics are shown in parentheses.a 5% significant.b 1% significant for 2-tailed test.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426418

The adjusted R2 of 24.6% of the cross-sectional model, which includes theadditional variable relative liquidity and the diversification variable, is relativelylow. However, the authors replicated the Chakravarty et al. (1998) model withdata on 79 companies from January 1995 to August 1999. The results are similarand the adjusted R2 is 60%.19 In the short run, there is probably a considerablelevel of noise influencing the stock prices. In the long run, the noises tend tocancel out and the adjusted R2 is accordingly much greater. ComparingChakravarty et al. (1998) with our model, we find three major differences. First,B-share return sensitivity and beta are insignificant in Chakravarty et al. (1998).It could be that calculating the values over 2 years ignores time-variations incovariances and beta. Second, the variable beta yields a negative coefficient inChakravarty et al. (1998).20 Theoretically, beta is a measure of internationalsystematic risk and should hold a positive relationship with the B-share dis-count.21 In our model, the coefficient of correlation of B-share returns with thereturns on the market portfolio is significant and positive. Third, company size isof strong significance in Chakravarty et al. (1998), but insignificant in ourmodel.22 However, company size is highly correlated with other independentvariables in our model.

In general, the comparison of our results with those of Chakravarty et al.(1998) suggests that different factors are important in different periods. However,clientele bias against companies on SHSE and the ratio of tradable A shares toB shares are major factors in explaining B-share discount in both studies.

4. Time series analysis

The time varying model investigates the effect of risk-free return differenceand foreign exchange risk23 on the time-variations in the B-share discount. Sincethe factors studied are not company-specific (so as to obtain more reliable statis-tics), the tests are performed on the rate of return on a portfolio rather than onindividual shares. The dependent variable is the daily discount of the B-shareindex against the A-share index, i.e.

19 These results are not reported since they offer little new insight. Moreover, the authors believe thattesting the cross-sectional model over a long period introduces bias due to the time varying nature ofdifferent variables.

20 In one of the test models of Chakravarty et al. (1998), beta is significant and positive.21 Although the Beta is not the exclusive source of systematic risk of B shares, it should affect the price

in a negative direction.22 Chakravarty et al. (1998) do not specify whether it is the market value of freely traded shares or the

total market capitalization of outstanding shares that proxy for company size. Nevertheless, in ourreplication of their study, we use both measures and neither is significant.

23 In the original model we included political risk as one of the variables. Since it is not significant, theresults are not reported here.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 419

discounti=Iai−Ibi

Iai

(2)

where Iai and Ibi are the A-share and B-share value weighted indices of companieswith both A and B shares.

4.1. Hypotheses

4.1.1. The risk-free return differential of domestic in�estors o�er that of foreignin�estors gi�es rise to a discount on B shares

The risk-free rate is regulated and relatively low in China.24 Domestic investorshave limited investment opportunities and accept a low, risk-free return. Hence,foreign investors demand a higher rate of return on the B shares, creating a (ceterisparibus) discount on B shares. The larger the difference of the inverse of therisk-free return of domestic investors (1/r f

d) over that of foreign investors (1/r ff), the

larger is the discount.

4.1.2. Expected de�aluations of the Chinese yuan contribute to the discount of Bshares

According to the international CAPM (e.g. Solnik, 1973)25, the expected riskpremium demanded by a foreign investor on a domestic asset depends on both thebeta of the domestic asset and the expected devaluation of the currency in whichthe asset is denominated. The second component is the foreign exchange riskpremium. Since the dividends of A shares or B shares are the same and denomi-nated in yuan, foreign exchange risk is present.26 All else being equal, if the yuandevaluates, the price of A shares is not affected. However, the B-share price, withearnings translated into foreign currency, is lowered by the devaluation. Thisgenerates a discount on B shares. Fernald and Rogers (1998) calibrate the Gordongrowth model, and find that B-share discount is positively related to the expectedrate of devaluation of the yuan.27

The expected devaluation rate equals the expected future foreign exchange rate,which is commonly proxied by future or forward exchange rates, divided by spotforeign exchange rate (Fig. 2).

The proxy for foreign exchange risk is thus the expected devaluation rate �et+1/et

of Chinese yuan, i.e. the forward foreign exchange rate (�et+1) divided by spotforeign exchange rate (et) and holds a positive relationship to discount.

24 Gordan and Li (1999) argued that the Government kept it low to subsidize SOEs financing. Due tocapital controls, interest rates can be kept at a low level without affecting the foreign exchange rate ofthe yuan.

25 Solnik (1973, 1974).26 Dividends on B shares are denominated in yuan but paid in foreign currency equivalents.27 Fernald and Rogers (1998) commented that although the model might approximate price poorly, it

captures most of the price difference between A and B shares.

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426420

Fig. 2. Discount, devaluation and risk free rate differential over time.

4.2. Data

We use stock return data from 68 companies with both A shares and B shareslisted from January 1997 to August 1999.28 Of these 68 companies, 36 are listed onSHSE, while 32 are listed on SZSE. The data series started from January 1997, asnon-delivery forwards did not begin trading until then. The sample size is 3425.

The A-share index is the value-weighted sum of daily closing prices of the Ashares of the 68 companies. The B-share index is calculated in a similar way, butconverted into Chinese yuan with daily closing foreign exchange rates. Risk-freereturn for foreign investors is proxied by the US 3-month T-bill rate. Unfortu-nately, short-term debt issued by the Chinese Government is very thinly traded andnot available to individual domestic investors. Instead, current deposit rates areused. However, these rates are only available on a monthly basis. Nonetheless, thedeposit rate does not change frequently. While no organized futures market foryuan exists in China, there is an offshore non-delivery forward market.29 Since Bshares are settled in foreign currency, there is no physical delivery of yuan.Non-delivery forwards serve well for hedging purposes and thus are the bestavailable estimate of expected future foreign exchange rate. The non-deliveryforward rate is the daily middle closing 3-month forward price of yuan to the USdollar. This rate is divided by the daily closing spot exchange rate. There are no

28 The data are collected from January 1997 instead of January 1995 since non-delivery forwardsstarted trading on January 15, 1997.

29 Due to currency controls, forwards can only be non-delivery.

C.

Bergstrom

,E

.T

ang/

J.of

Multi.

Fin.

Manag.

11(2001)

407–

426421

Table 3Descriptive statistics of variables (the variables are calculated on a quarterly basis)

High Low S.D. Coefficient. of variationVariables MeanMathematical representation Median

0.0943 0.1279Discount 0.7570 0.87427 0.524210.73710

Iai−Ibi

Iai

0.1658 0.36960.448571/rfd−1/rf

fDifference of inverse risk-free rates 0.39248 0.80930 0.29929

1.0112 0.99578 0.01127 0.01111.0103Devaluation rate 1.05942�et+1

et

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426422

non-delivery forwards for yuan versus Hong Kong dollar. Although it is possible tocalculate the cross rate, it does not add value, as the expected devaluation of yuanrelative to US dollar can capture the market expectation of foreign exchange risk ofinvesting in China. For non-delivery forward rate, missing data is computed usinginterpolation.

4.3. Results

4.3.1. Descripti�e statisticsThe discount shows a relatively larger dispersion than the devaluation rate but

less than the difference of the inverse risk-free rates. Since the exchange rate of theyuan is closely monitored and controlled, a significant devaluation is not expectedand thus its spread is rather small. One interesting point is that devaluation issometimes lower than 1, indicating that the market sometimes expects the yuan torevaluate.

Again, pair-wise correlation difference of inverse risk-free rates and devaluationrate is strong. One might be prompted to think that the devaluation rate is relatedto the risk-free rates by interest rate parities. However, the yuan is not fullyconvertible and therefore interest rate parities cannot hold. As with the cross-sec-tional analysis, the tolerance measure and the fact that the independent variablesare significant and have the expected sign do not suggest presence of multi-collinearity (Table 3).

4.3.2. Test resultsIn the linear stepwise regression, no independent variable is rejected. Both the

difference in the inverse risk-free rates facing domestic and foreign investors and theforeign exchange risk are highly significant with expected sign and similar explana-tory power. The adjusted R2 equals 38.3%. The constant term is negative, indicat-ing that variables that are negatively related to the B-share discount are left out(Table 4).

Table 4Test results: the time-series analysis

Expected signFactor and proxies/model 1 2

Constant −2.479(−9.382**)

Risk-free return difference1/rf

d−1/rff 0.228+ 0.291

(12.73**) (15.548**)

Foreign exchange risk3.079�et+1

et

+(11.684**)

Adj. R2 26%38.3%

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426 423

5. Conclusion

Ever since their introduction, B shares have shown a substantial discount againstA shares. This phenomenon is unique compared to other stock markets that segmentdifferent classes of shares by ownership. From the cross-sectional analysis, we findthat information asymmetry between domestic investors and foreign investors, illiquidtrading of B shares, diversification benefits from investing in B shares, and clientelebias against stocks on SHSE are significant determinants in explaining the cross-sec-tional variations in the discount on B shares. The significance of informationasymmetry and clientele bias confirms the findings of Chakravarty et al. (1998). Theclientele bias against B shares listed on SHSE is strong in all model specifications.However, the puzzle that contributes to the clientele bias remains unsolved. Thecross-sectional analysis identifies two more determinants of the discount on B shares:the relative illiquidity of B shares and the diversification benefits of B shares. Thelater result suggests that investors in B shares are likely to be active investors in theHong Kong stock markets. However, the list of determinants is far from exhaustiveas adjusted R2 is 24.6% and the constant term is large.

The time-series analysis confirms the explanatory power of risk-free returndifference and foreign exchange risk for the time-variations in the discount. The highlynegative constant term suggests that there exist other factors influencing thetime-variations. The explanatory power of the model should improve with a rigoroustreatment of political risk. A further improvement would occur if a risk-free return,which is directly comparable to the US T-bill rate, could be located for domesticinvestors.

A merger of A and B shares has long been desired. However, at present no concreteplan exists for the implementation of such a merger30. If a merger were eventuallyimplemented, it would be of great interest to study the resulting price dynamics.

Appendix A

Table A1. Trading summarya

Shanghai Stock MarketUS Billion Shenzhen Stock Market

97 9898 99, Jan – 99, Jan–MayTotal mar- 96 9796Mayket capital-

ization

30 At the time this study was conducted, there were no concrete plans to merge A shares and B shares.However, on the 19th February 2001, it was officially confirmed that domestic investors would be allowedto trade in B shares from June 1st 2001. Thus, the markets were reshuffled from strict segmentation topartial segmentation. This paves way for full merger of A shares and B shares. Trading was halted between19th February 2001 and 27th February 2001 for the new policy announcement. The Shanghai B Shareindex surged 9.7% and Shenzhen B share index surged 12.4% on February 29th when trading resumed,to speculate the new funds flooding in from 1st June 2001. Luo and Jiang (2001) and Ong and Tang (2001).

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426424

9850 106 117 64 109 127 147A share1B share 23 2 2 1.2 22

107 119 66 111 128.2100 149Total 53

Total negotiable market capitalization33 37 15 28A share 3415 4031

1 1 2 22 1B share 22Total 3418 38 17 30 35 4233

Turno�er145 202 134 40 109 164 148 47A share

1 0 1 33 1B share 02135 40 110 166 145Total 48148 205

aChina Securities Market Year Book (1995), China Statistical Yearbook (1998),Shanghai Stock Exchange Statistics Annual (1997, 1998, 1999), Shenzhen StockExchange Fact Book (1997, 1998).

Table A2. Distribution of daily average price discount (Jan 1995–Aug 1999)

Daily average discounts SHSE (n=39) Whole sample (n=79)SZSE (n=40)

0 0 00�Discount�20%1020%�Discount�40% 1

40%�Discount�60% 1310 3502260%�Discount�80% 28

141 1580%�Discount75.2%64.06% 69.58%Mean Discount

Table A3. Pearson correlation between variables, time-series analysis (Pearsoncorrelation coefficient is shown on the first line and significance on the second line)

Discounti 1/r fd−1/r f

f

Tolerance measure�et+1

et

Discounti 1.000.

0.911.0001/r fd−1/r f

f 0.454**0.000

1.000 0.910.300*�et+1

et

0.388**.0.000 0.000

C.

Bergstrom

,E

.T

ang/

J.of

Multi.

Fin.

Manag.

11(2001)

407–

426425

Table A4. Pearson correlation between variables, cross-sectional model, quarterly data (2-tailed test) (Pearson correlationcoefficient is shown on the first line and significance on the second line. The correlation between different diversificationfactors are not shown as they are entered into the model one at a time.)

Discounti REPORTi Ri Tolerancecorr(ubi, uHSI) SIZEicorr(ubi, uMSCI)SPREAD(bi)/pbi

SPREAD(ai)/pai

var(ubi)cov(uai, ubi)

var(P� ai) measureVOL(bi)VOL(ai)

1.000 0.930−0.148**

cov(uai, ubi)var(P� ai) 0.000 .

0.063* 0.211** 1.000var(ubi) 0.9500.027 0.000 .

REPORTI −0.020 −0.083** −0.028 1.000 0.9710.497 0.004 0.331 .

−0.012 −0.004 −0.021 1.000 0.9920.062*

SPREAD(bi)/pbi

SPREAD(ai)/pai 0.030 0.676 0.898 0.477 .0.9730.048 −0.024 0.072* −0.023 1.000

−0.144**VOL(bi)VOL(ai) 0.000 0.092 0.412 0.013 0.416 .

0.194** −0.049 0.000 −0.038 −0.002corr(ubi, uMSCI) −0.005 1.0000.000 0.087 0.995 0.193 0.945 0.872 .0.125** −0.036 −0.006 −0.074* −0.040corr(ubi, uHSI) −0.019 1.000 0.9890.000 0.214 0.838 0.011 0.162 0.505 .0.010 −0.062* −0.049 0.089** −0.037 0.006SIZEI 0.060* 0.082** 1.0000.732 0.031 0.087 0.002 0.206 0.827 0.037 0.004 .

RI −0.333** 0.125** 0.076** −0.087** 0.074* −0.136** −0.064* 0.089** −0.071* 1.000 0.6170.000 0.000 0.008 0.003 0.010 0.000 0.026 0.002 0.013 .−0.367** 0.098** 0.019 −0.131** 0.077**EXCHANGEI −0.075** −0.075** 0.252** −0.077** 0.611** 0.6240.000 0.001 0.515 0.000 0.008 0.009 0.009 0.000 0.007 0.000

C. Bergstrom, E. Tang / J. of Multi. Fin. Manag. 11 (2001) 407–426426

References

Chakravarty, S., Sarkar, A., Wu, L., 1998. Information asymmetry, market segmentation and the pricingof cross-listed share: theory and evidence from Chinese A and B shares, Research Paper No. 9820,Federal Reserve Bank of New York.

China Securities Market Year Book, 1995. China Judiciary System Publishing House.China Statistical Yearbook, 1998. China Statistical Publishing House.Bailey, W., 1994. Risk and Return on China’s new stock markets: Some preliminary evidence.

Pacific–Basin Finance Journal, 2, 243–260.Bergstrom, C., Rydqvist, K., Sellin, P., 1993. Asset Pricing within and Outflow Constraints: Theory and

Empirical Evidence from Sweden. Journal of Business Finance and Accounting 20, 865–879.Errunza, V., Losq, E., 1985. International asset pricing under mild segmentation: theory and test. The

Journal of Finance 40, 105–124.Fernald, J., Rogers, J.H., 1998. Puzzles in the Chinese Stock Market, International finance discussion

paper No. 619, Board of Governors of the Federal Reserve System.Gordan, R.G., Li, W., 1999. Government as a Discriminating Monopolist in the Financial Market: the

case of China, NBER working paper No. 7110, National Bureau of Economic Research.Hietala, P.T., 1989. Asset pricing in partially segmented markets: evidence from the Finnish market. The

Journal of Finance XLIV (3), 697–718.Luo, J., Jiang, J., 2001. Chinese B share rally may frizzle after today: Taking Stock, Bloomberg.Mendenhall, W., Sincich, T., 1993. A Second Course in Business Statistics: Regression Analysis, Dellen

Macmillan.Ong, J., Tang, E., 2001. As China’s B shares rally, Buyers Overwhelm Sellers, Bloomberg.Shanghai Stock Exchange Statistics Annual, 1997. Shanghai People’s Publishing House.Shanghai Stock Exchange Statistics Annual, 1998. Shanghai People’s Publishing House.Shanghai Stock Exchange Statistics Annual, 1999. Shanghai People’s Publishing House.Shenzhen Stock Exchange Fact Book, 1997. China Financial Publishing House.Shenzhen Stock Exchange Fact Book, 1998. China Financial Publishing House.Solnik, B.H, 1973. An equilibrium model of the international capital markets. Journal of Economic

Theory 8, 500–524.Solnik, B.H., 1974. The international pricing of risk: an empirical investigation of the world capital

market structure. Journal of Finance 29, 365–377.Tang, E., 1999. Price differentials on different classes of stocks: Empirical study on the Chinese stock

market, Master Thesis, Stockholm School of Economics.Wo, C.S., 1997. Chinese Dual-class Equities: Price differentials and information flows, Emerging

Markets Quarterly, Summer 1997, 47–62.

6. Further reading

Chiao, Xiao Ping, 1998, China Stock Markets Statistics and Analysis 1990 December–1998 June, ChinaFinancial Economics Publisher.

Dongwei, S., Fleisher, B.M., 1997. Risk, Return and Regulation in Chinese Stock Markets, Workingpaper No. 5, Department of Economics, Ohio State University.

Yao, Chengxi, 1998. Stock Market and Futures Market in the People’s Republic of China, OxfordUniversity Press, Oxford.