Embed Size (px)

Citation preview

Preserving and Protecting

Planning for Individuals With Special Needs

2

Preserving and Protecting

»Special needs planning requires preparation careful research experienced professional guidance

3

Primary objectives

» Protecting the assets of the person with special needs

» Providing additional potential income to facilitate a better quality of life

» Preventing the loss of government benefits, including Supplemental Security Income (SSI)

» Balancing the needs of other family members and beneficiaries

4

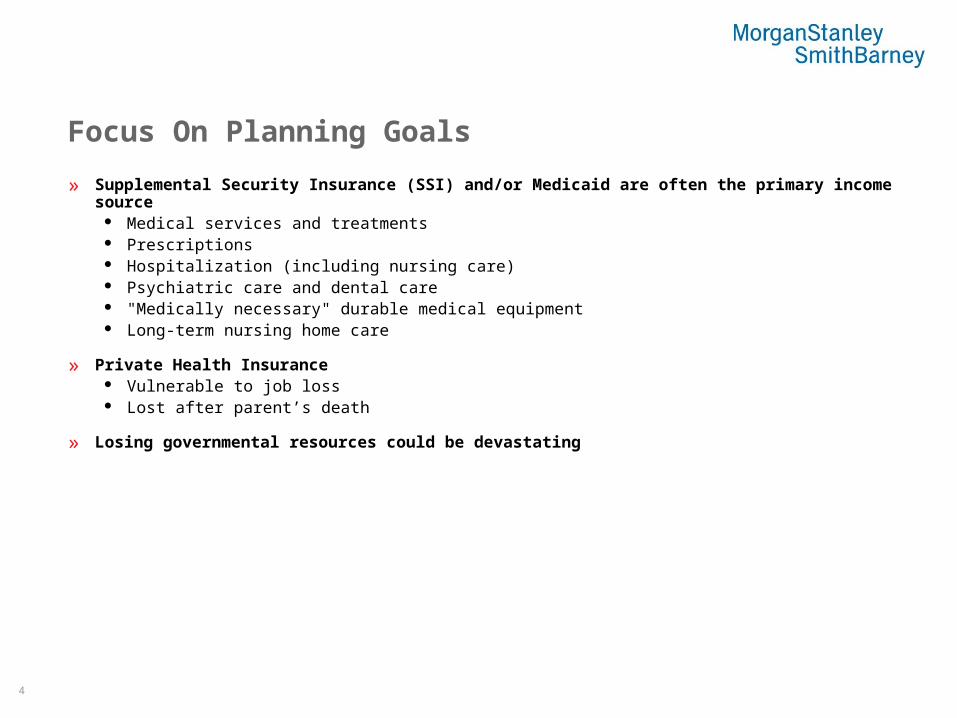

Focus On Planning Goals

» Supplemental Security Insurance (SSI) and/or Medicaid are often the primary income source Medical services and treatments Prescriptions Hospitalization (including nursing care) Psychiatric care and dental care "Medically necessary" durable medical equipment Long-term nursing home care

» Private Health Insurance Vulnerable to job loss Lost after parent’s death

» Losing governmental resources could be devastating

5

Outright Bequests and Gifts

» Direct gifts, or will or trust Available assets for any governmental agency providing need-based benefits, such as SSI or Medi-Cal. Required to be spent for the individual’s care (use of the assets by the beneficiary may be minimal and short-lived) Direct gift in excess of $2,000, could negate all of your planning efforts by disqualifying beneficiary for SSI.*

*Social Security Administration .SSA Publication No. 05-10026 January 2008. al Security Administration .SSA Publication No. 05-10026 January 2008.

6

Trusts

» Special Needs Trust Allocate resources to help maintain a quality of life Allow disabled person to qualify for SSI, Medi-Cal and other government-funded

programs Provide means of combining resources from government-funded programs with

private resources May help avoid court intervention

» Trust assets supplement medical or custodial care, training and education, or simply improve the individual’s standard of living

Step ThreeEstablish a Trust

8

» A Special Needs Trust (SNT) is a trust, created for a beneficiary with Special Needs

» Supplements government benefits such as SSI and Medi-Cal

» May be funded with proceeds obtained by the disabled person through: court proceeding inheritance life insurance claim settlement of a claim gift

» Two main types – Third Party and Self Settled

Special Needs Trust

9

Third Party Special Needs Trust

» Established for a disabled person with funds from someone other than the disabled person

» Commonly created by parents of an adult disabled child or other person NOT responsible for the disabled child’s care

» Upon the death of the disabled beneficiary – no payback required to the government for benefits provided to the disabled beneficiary

10

Self Settled Special Needs Trust

» Allows a person with disabilities to protect his/her own property received either from a personal injury settlement or other source

» Includes various restrictions on how the money remaining in the trust at the disabled person’s death must be used

» Two types of self-settled trusts Pay Back Trust Not-for-Profit Pooled Trust

11

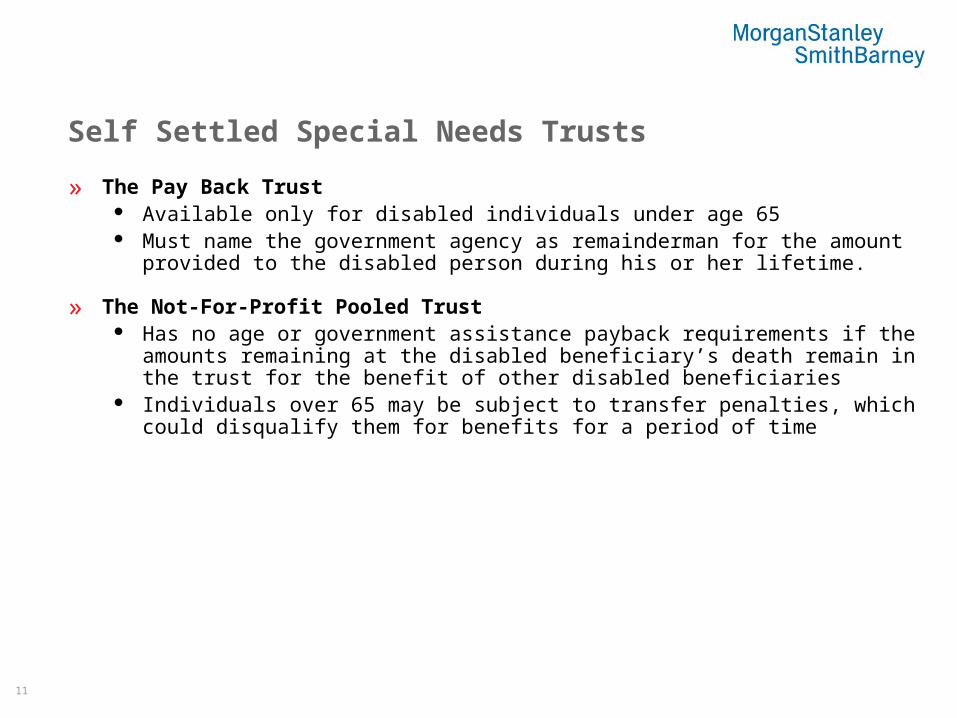

Self Settled Special Needs Trusts

» The Pay Back Trust Available only for disabled individuals under age 65 Must name the government agency as remainderman for the amount provided to

the disabled person during his or her lifetime.

» The Not-For-Profit Pooled Trust Has no age or government assistance payback requirements if the amounts

remaining at the disabled beneficiary’s death remain in the trust for the benefit of other disabled beneficiaries

Individuals over 65 may be subject to transfer penalties, which could disqualify them for benefits for a period of time

12

What Is A Special Needs Trust?

»Life Enhancement Trusts

»Read exactly opposite of what you would expect

»Distributions for Food, Shelter, Medical Expenses, NOT permitted

»Failure to follow trust directives, which are based on government regulations, can result in denial of government benefits

Step FourSelect a Trustee

14

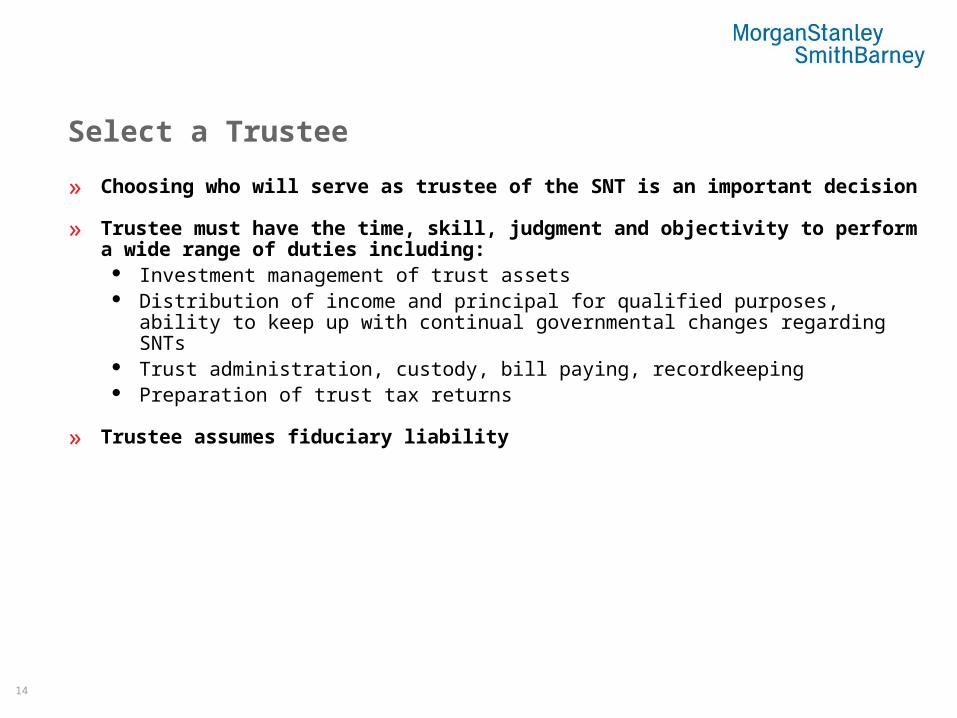

Select a Trustee

» Choosing who will serve as trustee of the SNT is an important decision

» Trustee must have the time, skill, judgment and objectivity to perform a wide range of duties including:

Investment management of trust assets Distribution of income and principal for qualified purposes, ability to keep up with

continual governmental changes regarding SNTs Trust administration, custody, bill paying, recordkeeping Preparation of trust tax returns

» Trustee assumes fiduciary liability

15

Trustee Options

» Personal trustee

» Trust advisory committee Shifts non-financial decisions to other designated advisors

» Trust Protector Monitors the performance of the trustee

» Managing Agent The individual trustee would be responsible for all decisions relating to discretionary distributions and

governmental benefits. The professional trustee would provide professional investment management, as well as full administrative services customized to the specific terms of the trust and the needs of the trustee

» Professional Trustee

Step FiveFund Your Special Needs Trust

17

»Cash

» Investments

»Life insurance

Sources of Funding

18

Life Insurance Requires smaller initial outlay Proceeds usually received income tax free and estate tax free Survivorship life insurance provides one death benefit after the death of the

second spouse» Cost is generally less than buying a separate policy for each parent

Trust can be the beneficiary of the policy, with proceeds used to care for a disabled child after both parents are gone

Step SixBalance Your Family’s Needs

20

»Focus on the financial needs of your entire family

»Ensure that plans for your disabled family member don't interfere with broader family goals or build resentment

»Balance your overall retirement, estate and other planning goals with the needs of your disabled child

Holistic Planning

21

Develop an Estate Plan

» Avoid Probate

» Help reduce estate taxes

» Maintain control over important personal issues such as health care and guardianship

» Provide the liquidity needed for estate taxes and expenses

» Specify philanthropic wishes

» Reduce the likelihood of family disputes

» Protect privacy and avoid distribution delays

22

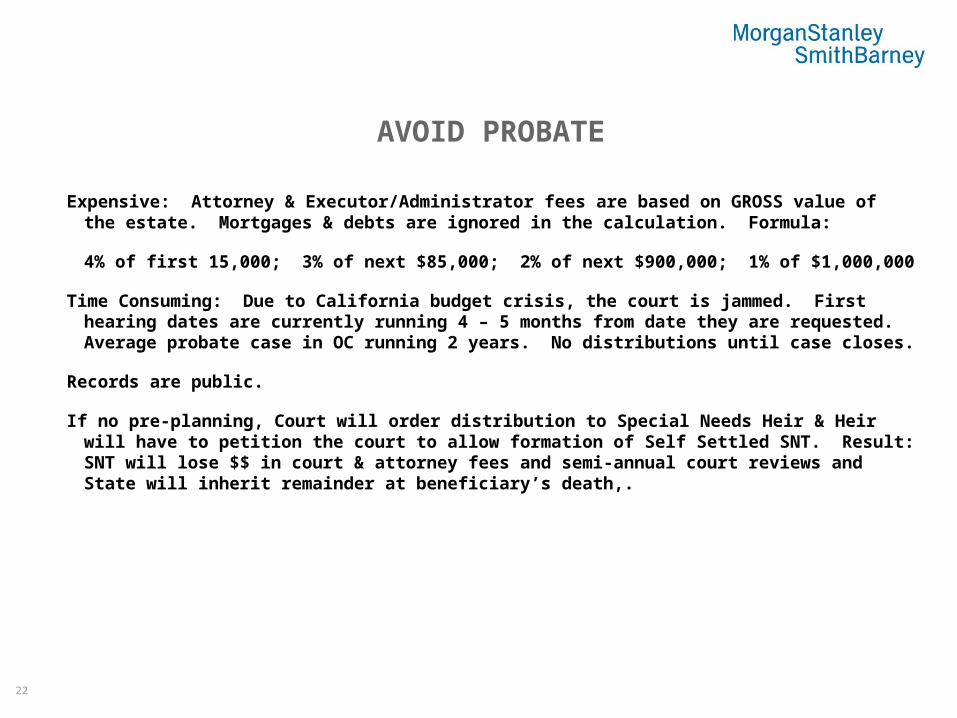

AVOID PROBATE

Expensive: Attorney & Executor/Administrator fees are based on GROSS value of the estate. Mortgages & debts are ignored in the calculation. Formula:

4% of first 15,000; 3% of next $85,000; 2% of next $900,000; 1% of $1,000,000

Time Consuming: Due to California budget crisis, the court is jammed. First hearing dates are currently running 4 – 5 months from date they are requested. Average probate case in OC running 2 years. No distributions until case closes.

Records are public.

If no pre-planning, Court will order distribution to Special Needs Heir & Heir will have to petition the court to allow formation of Self Settled SNT. Result: SNT will lose $$ in court & attorney fees and semi-annual court reviews and State will inherit remainder at beneficiary’s death,.

23

Common Estate Planning Strategies

» Create a trust, pour-over will, durable power of attorney and advance health care directive

» Maximize estate tax deductions and exclusion

» Retitle assets as necessary to maximize benefits – California limit for probate: $150,000 GROSS for assets not in trust, joint tenancy or beneficiary designated

» Review beneficiary designations

» Gifting what you don’t need

» Ensure sufficient estate liquidity

» Know what you have and where you have it

Step SevenCommunicate With Family

25

» Discuss plans with all family members

» Well-meaning relatives could make gifts that jeopardize your well thought out plans

Direct gift in excess of $2,000, for example, could negate all of your planning efforts1

» Encourage family members to make gifts to the special needs trust where appropriate

» Ease siblings’ fears of being left out of the planning process

Communicate With Family

1 In order to qualify for SSI, the limit for countable resources is $2,000 for an individual and $3,000 for a couple. Source: Social Security Online, the official website of the U.S. Social Security Administration.

Step EightReview Your Plans As Needed

27

» Life is full of change Marital status, the birth of a child, purchase or sale of a home, a new business

venture, relocation to a different state, a sizable charitable gift, tax law changes,capital markets developments

» Planning is a dynamic process Review your plans now Assess type of insurance you have and the amount of coverage Conduct annual reviews of life insurance policies used to fund a special needs

trust Protect against unpleasant surprises Evaluate performance of your trustee

Ongoing Review

28

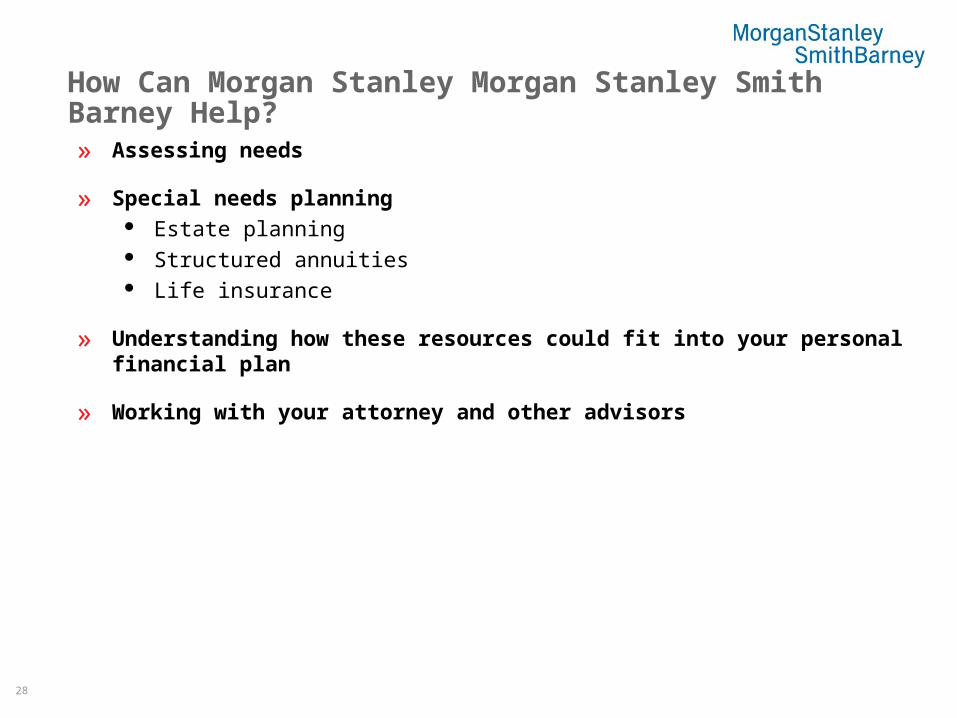

How Can Morgan Stanley Morgan Stanley Smith Barney Help?» Assessing needs

» Special needs planning Estate planning Structured annuities Life insurance

» Understanding how these resources could fit into your personal financial plan

» Working with your attorney and other advisors

29

This material is based on generally available public information and is provided free of charge for general informational and educational purposes only. The information contained in this material is subject to change without notice. Morgan Stanley Morgan Stanley Smith Barney LLC undertakes no obligation to update this material. This material does not take into account your personal circumstances and we do not represent that this information is complete or applicable to your situation.

Morgan Stanley Smith Barney LLC, its affiliates and Morgan Stanley Smith Barney Financial Advisors do not provide tax or legal advice. This material was not intended or written to be used for the purpose of avoiding tax penalties that may be imposed on the taxpayer. Clients should consult their tax advisor for matters involving taxation and tax planning and their attorney for matters involving trust and estate planning and other legal matters.

Since life insurance is medially underwritten, you should not cancel your current policy until your new policy is in force. A change to your current policy may incur charges, fees and costs. A new policy will require a medial exam. Surrender charges may be imposed and the period of time for which the surrender charges apply may increase with a new policy. You should consult your personal tax advisor regarding your potential tax liability on surrenders.

© 2010 Morgan Stanley Morgan Stanley Smith Barney LLC. Member SIPC.

![Protecting LLC Owners While Preserving LLC Flexibility · 2018] Protecting LLC Owners While Preserving LLC Flexibility 2131 INTRODUCTION Limited liability companies, or LLCs, have](https://img.dokumen.tips/doc/110x75/5d647e9888c99309728bbe5a/protecting-llc-owners-while-preserving-llc-flexibility-2018-protecting-llc.jpg)