Embed Size (px)

Citation preview

Organize Productive Conversations With Your Clients

Presented by: Jason E. Lea, CFP ®

The Retirement Challenge:

Some Stunning Statistics

• 14.4% (.144)

• 73.3% (.733)

• 87.6 %

• 11

• 22

• 0.00%

• Red Sox Team World Series Batting Average

• David Ortiz World Series Batting Average

• Likelihood you will stay awake for 1:45 today!

• David Ortiz # hits• Rest of Team- total hits

(not including Ortiz)• Koji Uehara’s W/S ERA

Agenda

• Changing Landscape• Economy, Politics, and Interest Rates• Our Mission Today• 3 Main Client Objectives • 5 Simple Steps• Strategies• Carrier Panel

Thank You To Our Sponsors

Talking to Your Clients

• 1 conversation every day• Work with your BSMG advisors• Have the right tools to present solutions• Understand the risks

• For your clients• To your practice

Retirement Market – It’s Pretty Big

U.S. Total Retirement Market

Trillions of dollars, end-of-period, selected periods $20.9 Trillion

* The Investment Company Institute“The U.S. Retirement Market, Second Quarter 2013.”

DC Plans and IRA’sRetirement Assets by TypeBillions of dollars, end-of-period, 2013:Q1–2013:Q2

* The Investment Company Institute “The U.S. Retirement Market, Second Quarter 2013.”

The Retirement Landscape

• The Financial Crisis – what’s the impact?• A wake up call for clients• Clients realize they need advice on retirement• Clients feel more secure when they work with a

financial professional

A Stunning Opportunity

75% of Clients switch advisors at Retirement1

67% percent of clients want a retirement income plan, only 25% have received it.2

87% of clients who received a retirement income plan moved their assets to that advisor.1

1Source: McKinsey & Co., Cracking the Consumer Retirement Code, 20072Source: Fidelity Investments, Adapting a Practice for Retirement Income Planning, 2006

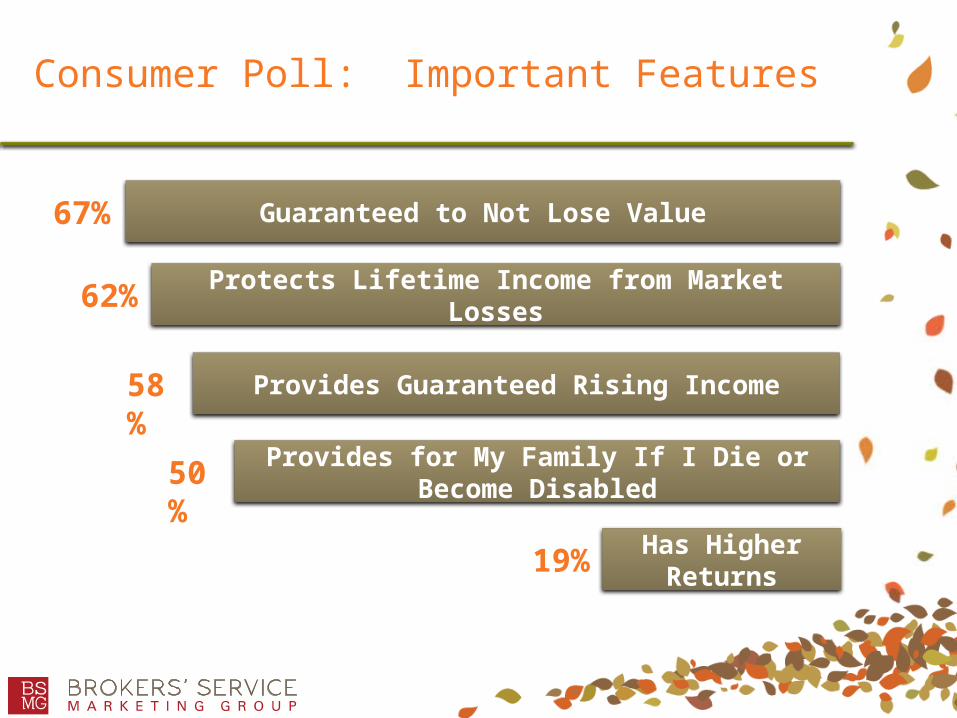

Consumer Poll: Important Features

Guaranteed to Not Lose Value

Protects Lifetime Income from Market Losses

Provides Guaranteed Rising Income

Provides for My Family If I Die or Become Disabled

Has Higher Returns

67%

62%

58%

50%

19%

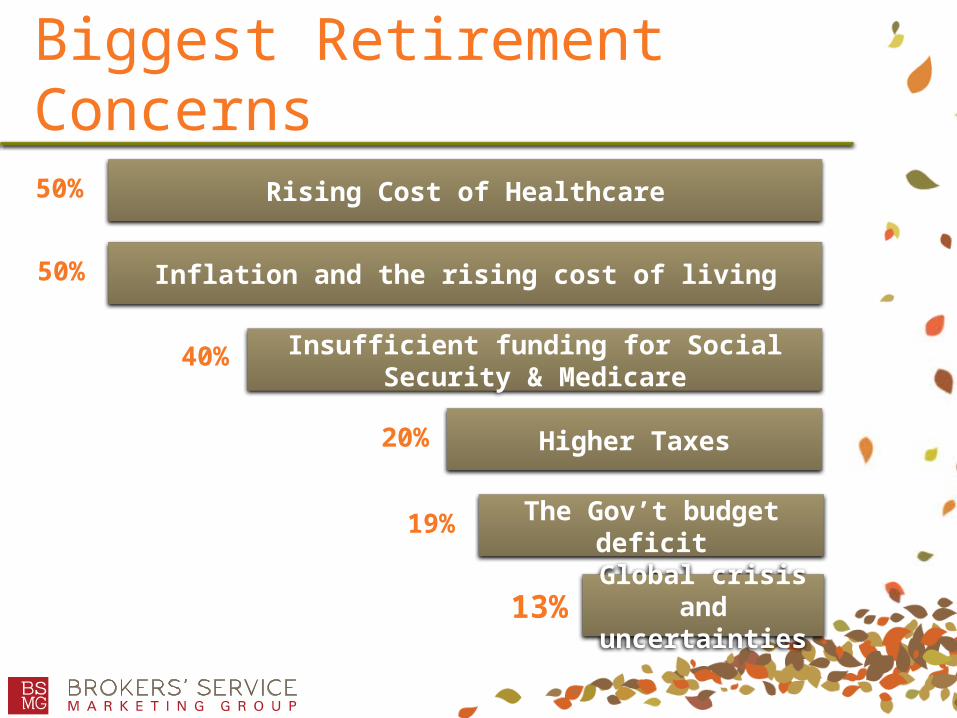

Biggest Retirement Concerns

Rising Cost of Healthcare

Inflation and the rising cost of living

Insufficient funding for Social Security & Medicare

Higher Taxes

The Gov’t budget deficit

50%

50%

40%

20%

19%

Global crisis and uncertainties13%

Taxes

• 3 ways Retirement Income taxed

Ordinary Income

Capital Gains

Tax-Free

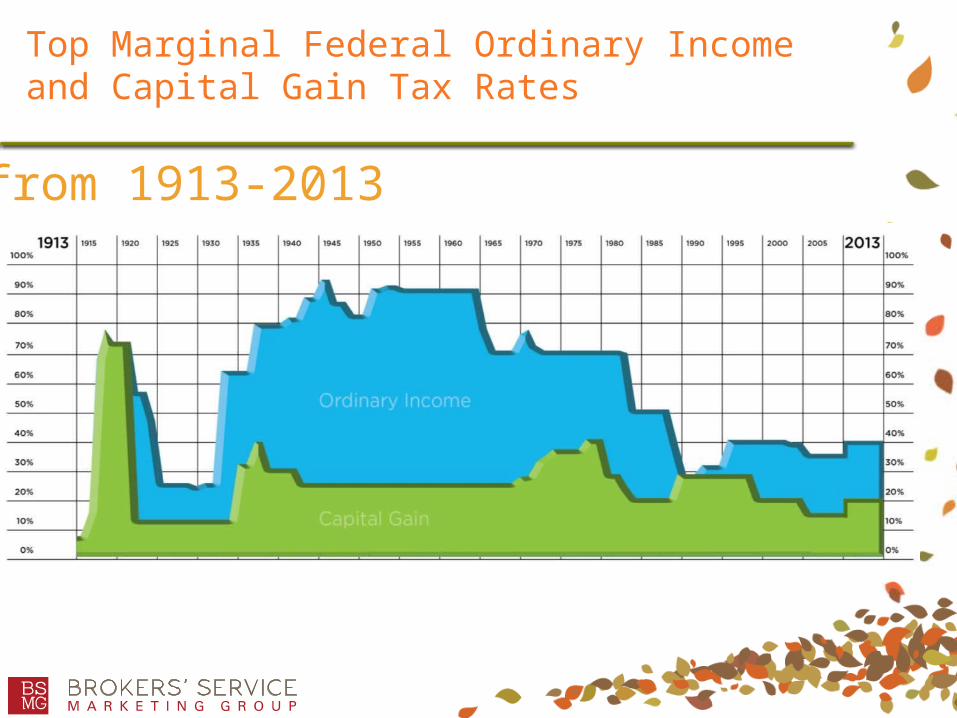

Top Marginal Federal Ordinary Income and Capital Gain Tax Rates

from 1913-2013

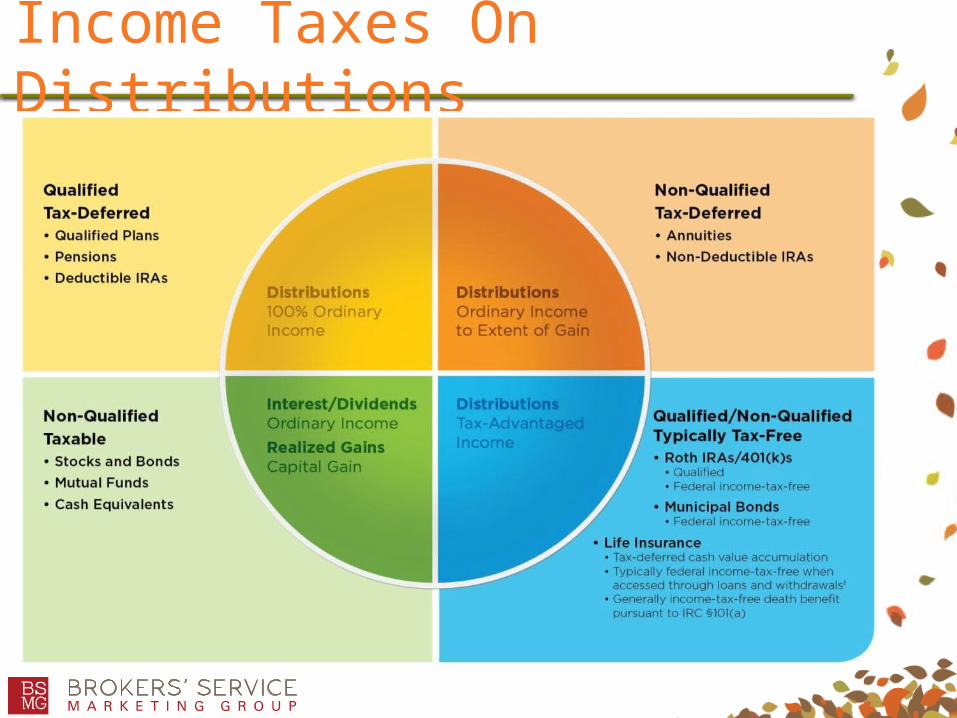

Income Taxes On Distributions

Pain Outweighs Gain

• Which is more impactful to retirees?

• Protection from loses is more important than higher, riskier returns

8x More important!*

• Peace of Mind is 4x more important than wealth**2012 AIG Retirement Reset Study

Gain 20%

Lose 20%

or

Life Expectancy

• Doubled in the last 100 years• Average Length of Retirement for a married

couple age 65?

27 Years! (Age 92)

Economy, Politics, Interest Rates

• Slow recovery, unemployment remains high

• Washington refuses to collaborate

• Persistently low interest rates

• Market Volatility

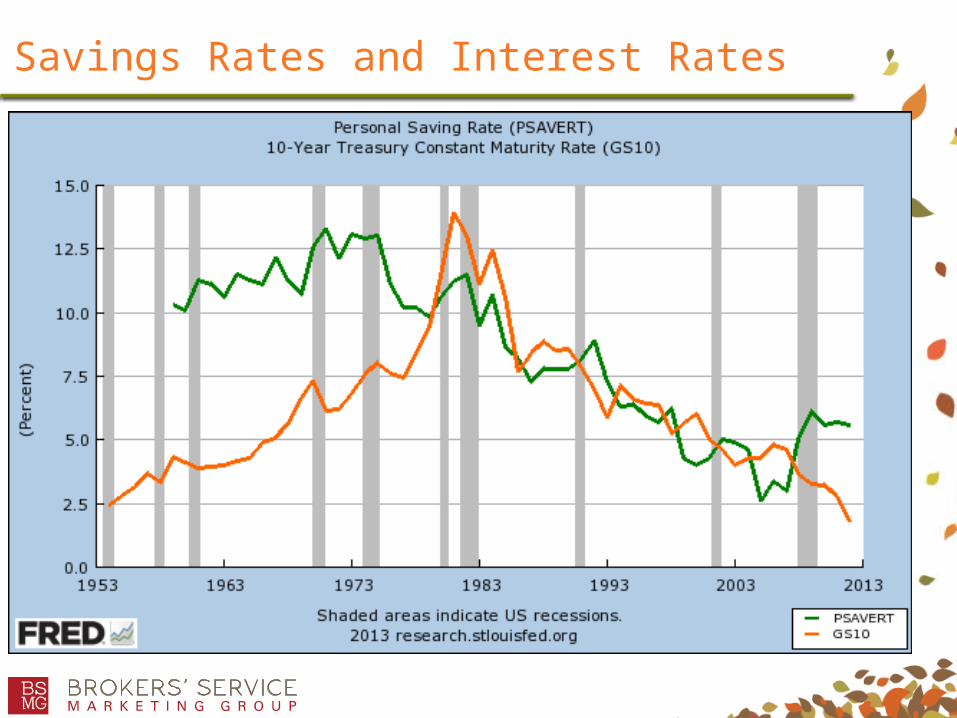

Savings Rates and Interest Rates

The Importance of Saving

Post-retirement expenses

Financial In

dependence

Needs

Wants

Dreams

Legacy

Travel, entertainment, gifts, motorcycle

Food, shelter, clothing

Grandchild’s education, vacation home, RV

Heirs, charities

Freq

uency

Less

More

3 Major Retirement Topics

Retirement Income

Asset Protection

Legacy Planning

There’s Only Three Uses for $…

Income

• Spend it

Assets

• Save it

Legacy

• Give it away

Retirement

Income•Needs (Non-Discretionary)•Wants (Discretionary)

Assets •Emergency Fund•Diversified Portfolio•Protection against Healthcare & LTC Costs

Legacy•Life Insurance death benefits•Assets transfer to spouse/heirs

Make it Personal

Income•Mortgage•Monthly Bills•2nd home•Travel•Gifts

Assets•Emergency fund•Unexpected health-related expenses•Grandkids’ education

Legacy•Surviving Spouse•Kids•Grandkids•Charity

Income

Defined Benefit “Pension Plans”Social Security

Will these be enough for your clients?Clients can create their own personal “pension”

plans

Asset Protection

HealthCare and LTC costs

Market Risks

Interest Rate Risks

Inflation

What’s Your Legacy?

Spend Pennies on the Dollar to:

Take Care of your spouse when you’re gone

Take care of Kids and Grandkids

Give to Charities/Organizations that have

meaning to you

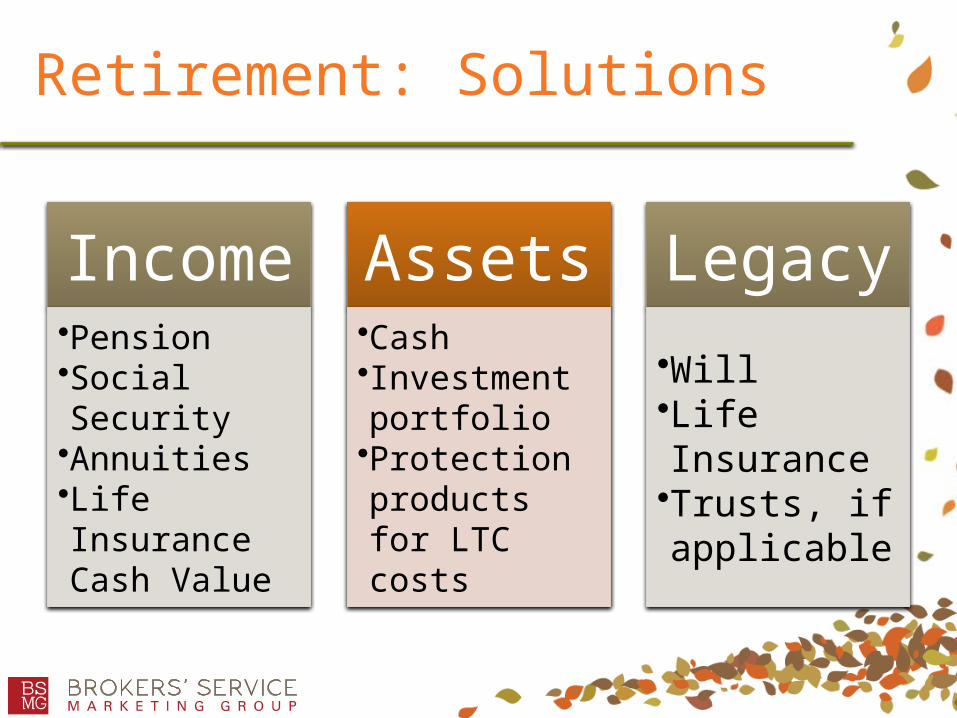

Retirement: Solutions

Income•Pension•Social Security•Annuities•Life Insurance Cash Value

Assets•Cash•Investment portfolio•Protection products for LTC costs

Legacy•Will•Life Insurance•Trusts, if applicable

Our Mission Today

Be able to “Yellow Pad” it with

your clients

6 Simple Steps

1. Define Your Relationship with the client

2. Ask key questions, gather data

3. Evaluate client’s financial status

4. Develop and present your recommendations

5. Implement your plan

6. Yearly or quarterly check-ups

Define The Relationship

• Let them know this is conversation you are looking to have with your clients

• Ask if they are willing to discuss with you, and explain that it’s a very important

• What Retirement goals do they have?

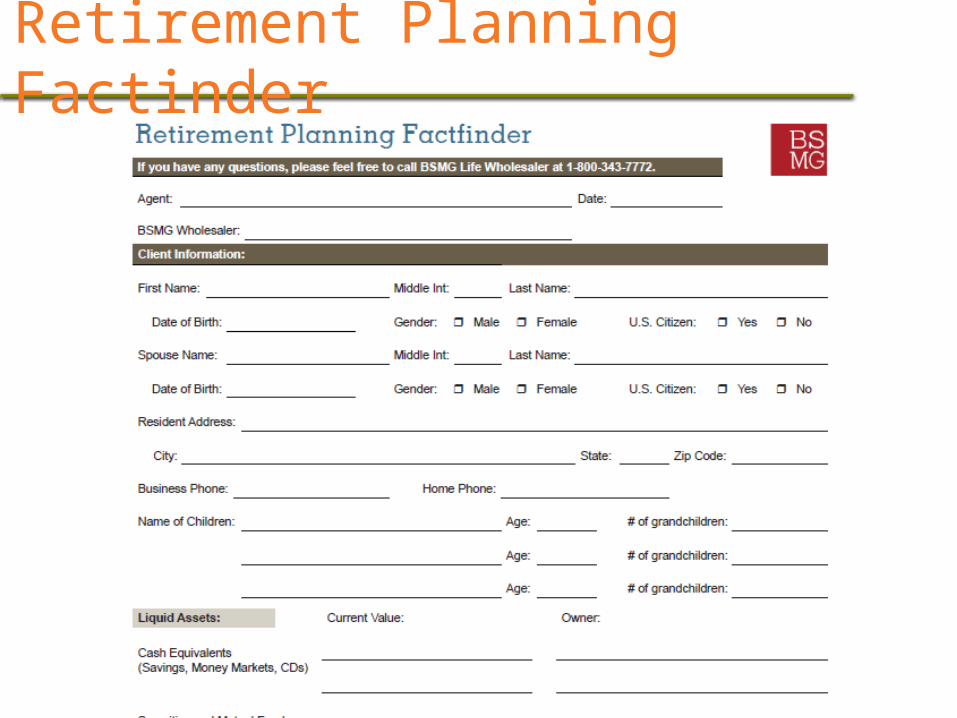

Ask Questions, Gather Data

• Use a Fact Finder• Determine Client goals and priorities for

income, asset protection and legacy• Determine client needs

Retirement Planning Factinder

Retirement Needs Worksheet

Goals vs. Needs

• Client goals often > Client resources • Good fact-finding will reveal their actual needs

and those should be addressed first.• Advising is easier your client once you

understand their needs.• Clients appreciate good homework.

Evaluate Client’s Financial Status

• Do they have adequate:• Cash• Protection from HealthCare and LTC costs• Sources of Retirement Income• Life Insurance

• Do they have an estate planning attorney who has drafted a will, health care proxy, power of attorney, trusts if necessary

Results of Data gathering

• Findings determine:• Income Gap• Asset protection needs• Legacy objectives

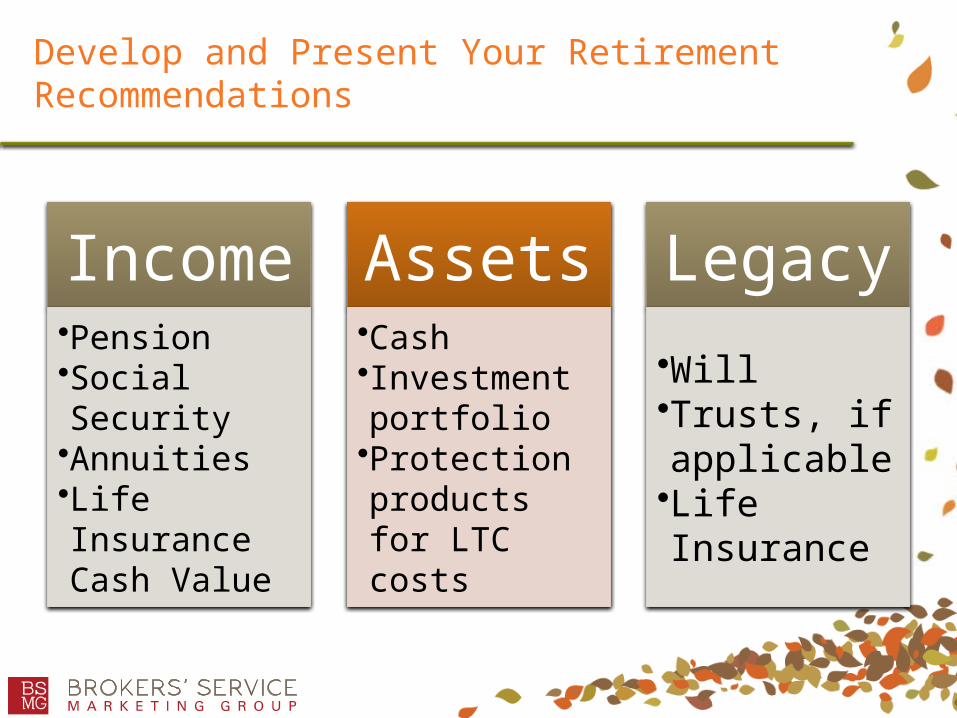

Develop and Present Your Retirement Recommendations

Income•Pension•Social Security•Annuities•Life Insurance Cash Value

Assets•Cash•Investment portfolio•Protection products for LTC costs

Legacy•Will•Trusts, if applicable•Life Insurance

Protection Products Offer…

• Risk Transfer from client to Insurance Co.• Peace of mind• Asset protection from financial risks• …in a word…

Protection

Match-up Solutions to the Needs

• Annuities• Lump-Sum funded Retirement Income• Fixed Asset to protect from market losses

• LTC Products• Lump Sum or Flex-pay funded• Protect assets from largest risk in retirement

• Life Insurance• Lump sum or-Flex pay funded• Provides Death benefit and now access while alive to DB for

LTC expenses• Access cash value for income after 15 years

Implement Plan & ConductYearly or quarterly Reviews

• Build Client Trust over time• Chance to uncover other opportunities• Become a Center of Influence, and develop

retirement referrals

Michael (engineer) & Mary (teacher), age 60

• Retiring in 5 years • Current income = $7.5k / month after taxes• Current expenses • Net Savings $1.5k/month

• ($500 to NQ savings, $1,000 to 401(k))• (2) Children – 28 & 30 years old• (1) Grandchild – 2 years old

Retirement Budget

Housing Costs

Mortgage / Rent

Real Estate Taxes

Maintenance & Repair

Home Insurance

Retirement Budget - @ age 65

• Non-discretionary expenses: $5,000/month (mortgage, bills, food)

• Discretionary expenses: $1,000/month (vacations)• Pension @65 of $2,000/month• Social Security @65 of $2,500/ month

Personal Balance Sheet

• $500,000 qualified plan

• +70,000 in additional (saved from 60-65) = $570,000

• $250,000 NQ assets

• + $30,000 saved (saved from 60-65) = $280,000

• $500k Term Insurance (5 years left), no plan for LTC

• $200,000 Vacation home Mortgage (Florida)

• $20,000 Auto loans

Assumptions• 4% IRR on investments, 3% inflation, 30% income tax rate• Plan to retire in 5 years

A Thought on Reducing Expenses…

• Much more financially powerful than increasing income because the expense reduction (savings) double effect:

• Increases savings each month• Permanently decreases the amount you’ll

need each month for the rest of your life.

Michael and Mary: Goals

• Inflation-protected lifetime income• Keep remaining assets safe• Travel• Help with grandkids’ College• Protect against LTC costs• Leave a legacy for their kids & grandkids

A Snap Shot @Age 65

Income-$5,000 Expenses

-$1,000 Discretionary Expenses.

$2,500 Pension

$2,500 S. Security

$1,000 Income Gap

Assets

$80,000 Cash

$200,000 NQ

$570,000 Q Plan

No LTC Plan

Legacy

$500k Term Life Insurance

Beneficiaries & Charities

Help Grandkids with College

Three Strategies

Retirement Income

• Use a deferred annuity with a guaranteed joint lifetime

withdrawal benefit.

• Client retains control of account value

• Guaranteed withdrawals for life

• Withdrawals can be started when the client wants

• Longer deferral = larger guaranteed w/d!

• Annual fee ranges between 0.65% - 1.25%

Three Lifetime Income “Buckets”

Age 65

$240,000Qualified Funds

Monthly after-tax Income $1,116

Annual Income $13,400

Age 70

$80,000Qualified Funds

Monthly after-tax Income $500

Annual Income $6,000

Age 75

$87,000NQ Funds

Monthly after-tax Income $1,000

Annual Income $12,000

Annuities Create a “Personal Pension”

65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 900

6,000

12,000

18,000

24,000

30,000

36,000

Income yrs 15+Income yrs 10+Income yrs 5+

Earning 3% every Year

65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 950

50000

100000

150000

200000

250000

300000

350000

400000

450000

AssetIncome

Earning 4% Every Year

65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 950

50000

100000

150000

200000

250000

300000

350000

400000

450000

AssetIncome

Pension & Social Security Income

65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 900

1200024000360004800060000720008400096000

108000120000132000

Social Security

Pension

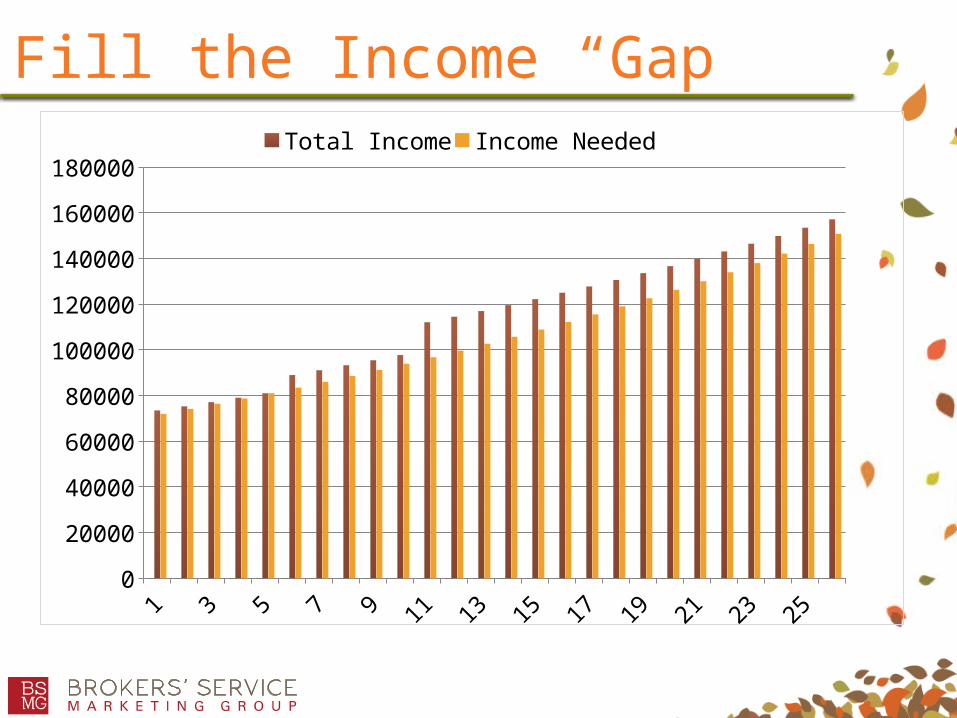

Fill the Income “Gap”

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 260

20000

40000

60000

80000

100000

120000

140000

160000

180000Total Income Income Needed

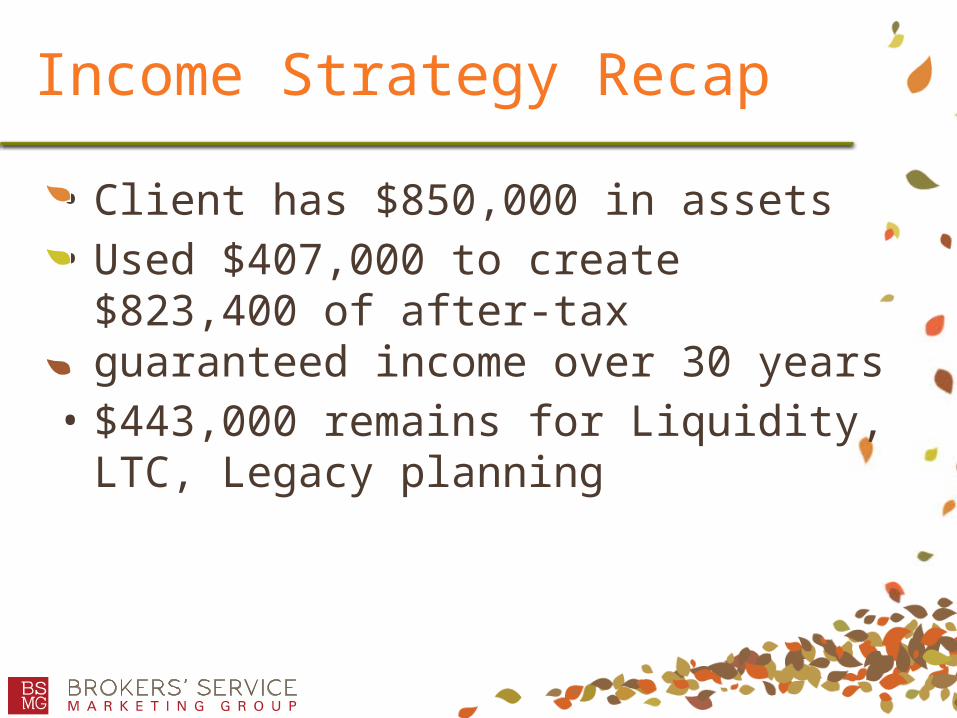

Income Strategy Recap

• Client has $850,000 in assets• Used $407,000 to create $823,400 of after-tax

guaranteed income over 30 years• $443,000 remains for Liquidity, LTC, Legacy

planning

Asset Protection – LTC “Linked Benefit”

• LTC protection goals• Legacy benefits if LTC not needed• Transfers risk of LTC “Health Event” to

Insurance Company• Not an Expense, an “Asset Reposition”• Once policy on each spouse

$200,000 LTC solution

$5,000 per month in LTC benefits

6 year min. benefit period

Zero day elimination

100% Liquidity (return of Premium)

Death benefit = $120k

Linked Benefit GraphicOther

Life insurance tocreate a legacy

Portion of savings

Cashsavings

Investments &retirement income

$75,000Premium

$360,000Income tax-free long-termcare reimbursements$120,000

Income tax-free deathbenefit for beneficiaries

$75,000Money back guarantee

OR OR

LTC “Linked Benefit” Recap

$443,000 remains after retirement income funding

Use $150,000 of Qualified assets($110,000 after taxes)

Use $50,000 of NQ assets

Net After taxes = $160,000

$243,000 Remains after LTC Funding

….Or buy a UL policy w/ LTC rider

• Buy (2) $250,000 Death Benefit UL Policies

• LTC Rider or Chronic Illness Rider

• 100% of DB available for LTC needs, tax free

• Guaranteed Lifetime DB

• Fully Underwritten, More DB than Linked

• Guaranteed DB = Max LTC Benefit

…UL with LTC/CI rider

$5,000 per month in LTC benefits

50 Month Benefit Period

90 day elimination period

Return of Premium… available with some Carriers

Death benefit = $250,000LTC benefit = $250,000

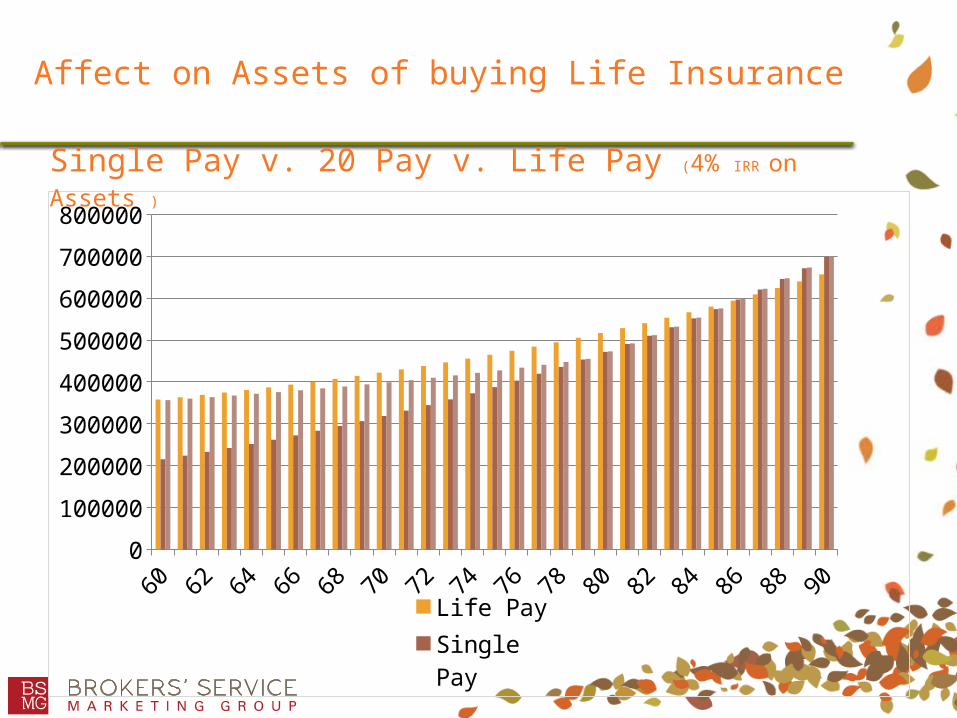

20 Pay Mary $5,000

Michael $5,700Total = $10,700 Single Pay

Mary $68,000Michael $78,000Total = $146,000

$146k funding a Life Pay vs. 20 Pay (4% IRR)

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 900

20000

40000

60000

80000

100000

120000

140000

160000

Life Pay20 Pay

Affect on Assets of buying Life Insurance

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 900

100000

200000

300000

400000

500000

600000

700000

800000

Life PaySingle Pay20 Pay

Single Pay v. 20 Pay v. Life Pay (4% IRR on Assets )

Single Pay v. 20 Pay v. Life Pay (3% IRR on Assets )

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 900

100000

200000

300000

400000

500000

600000

700000

800000

Life PaySingle Pay20 Pay

Affect on Assets of buying Life Insurance

Results of UL with LTC Rider

$443,000 remains after retirement income funding

Use $130,000 of Qualified assets($100,000 after taxes)

Use $46,000 of NQ assets

Net After taxes = $146,000

$267,000 Remains after UL with LTC Rider

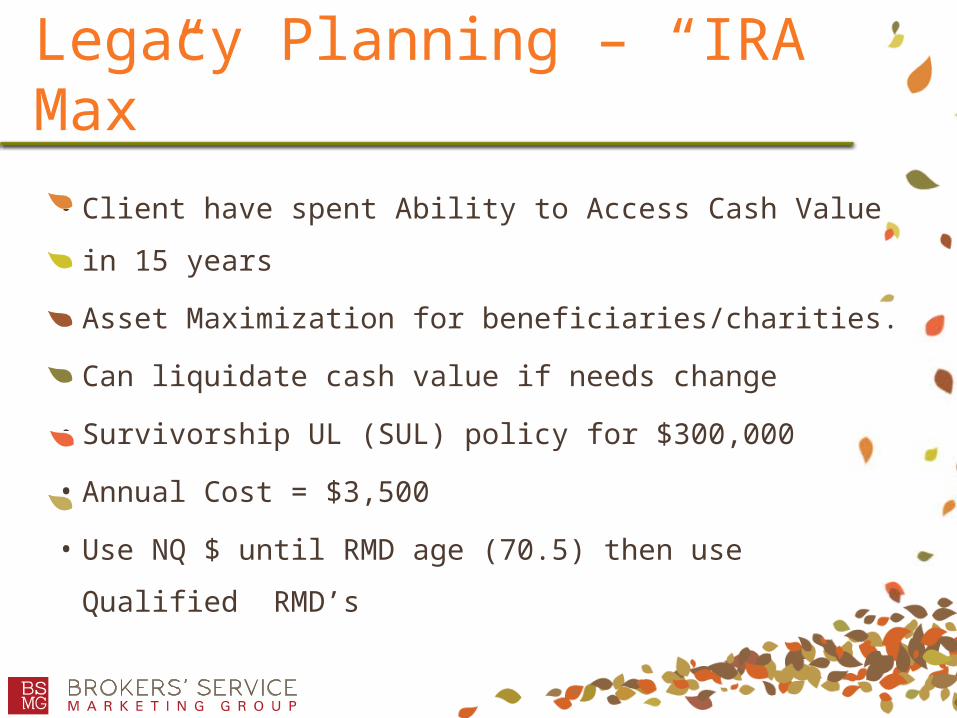

Legacy Planning – “IRA Max”

• Client have spent Ability to Access Cash Value in 15 years

• Asset Maximization for beneficiaries/charities.

• Can liquidate cash value if needs change

• Survivorship UL (SUL) policy for $300,000

• Annual Cost = $3,500

• Use NQ $ until RMD age (70.5) then use Qualified RMD’s

Legacy - Add a Survivorship UL

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 900

100000200000300000400000500000600000700000800000900000

1000000

$300k SULAssets @ 4%

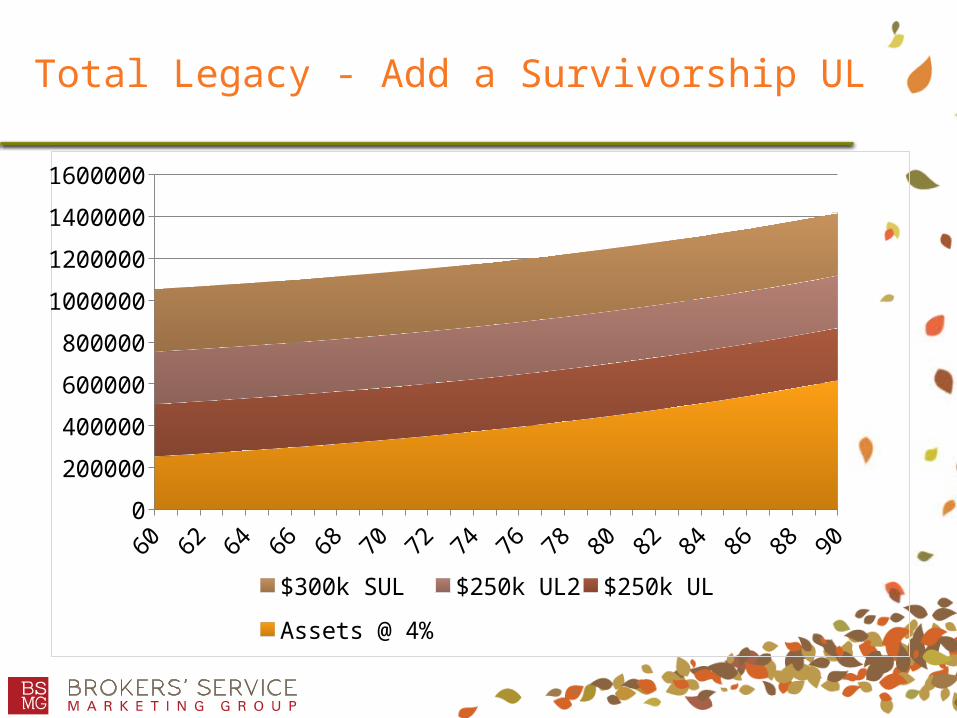

Total Legacy - Add a Survivorship UL

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 900

200000

400000

600000

800000

1000000

1200000

1400000

1600000

$300k SUL $250k UL2 $250k UL

Assets @ 4%

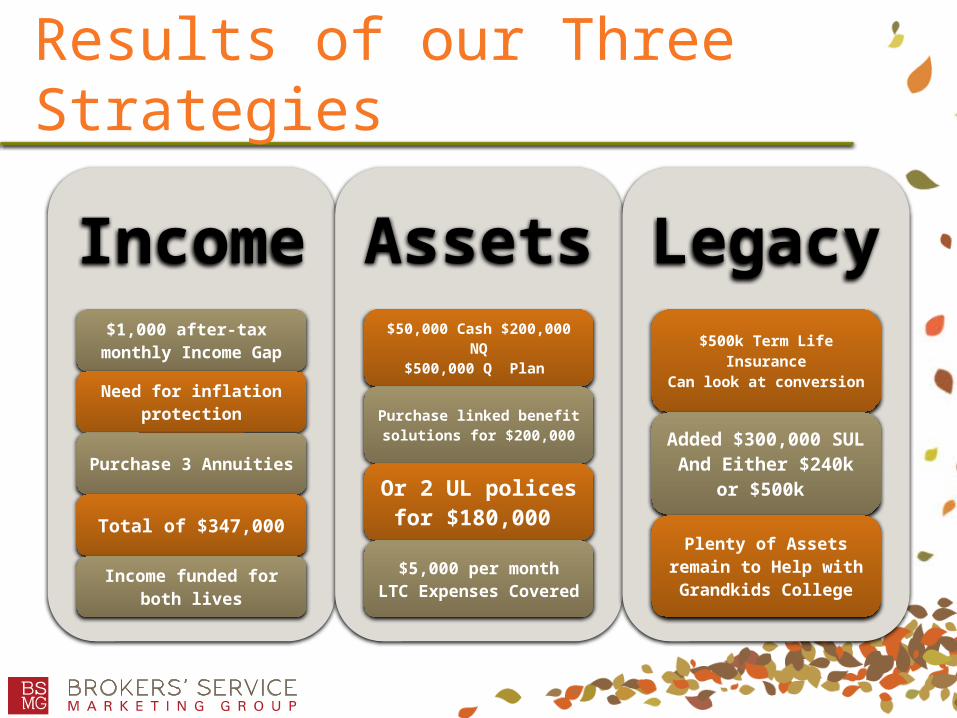

Results of our Three Strategies

Income$1,000 after-tax

monthly Income Gap

Need for inflation protection

Purchase 3 Annuities

Total of $347,000

Income funded for both lives

Assets$50,000 Cash $200,000

NQ$500,000 Q Plan

Purchase linked benefit solutions for $200,000

Or 2 UL polices for $180,000

$5,000 per monthLTC Expenses Covered

Legacy$500k Term Life

InsuranceCan look at conversion

Added $300,000 SULAnd Either $240k or

$500k

Plenty of Assets remain to Help with Grandkids College

Thank You!

![img.mlbstatic.com · Cleveland 1954 Indians batting - Pitching for Kansas City 1985 Royals : LHP nanny Jackson Batting: SHB page-Phil]ey Batting: RHB Wally-Westlake Batting: RHB George](https://img.dokumen.tips/doc/110x75/5f7e059d1e17b7025b240fae/img-cleveland-1954-indians-batting-pitching-for-kansas-city-1985-royals-lhp.jpg)