Embed Size (px)

Citation preview

Presented by:

Business Continuity Planning

Tom Pilkington CA CFP TEP

National Estate and Tax Planning Consultant

Ontario Regional Marketing Centre

Keyperson Protection

Funding Shareholder Agreements

Global Financial2007 Kick-Off Meeting

Wednesday, January 10, 2007

2

Important considerations This material is for information purposes only and should

not be construed as legal or tax advice. Every effort has been made to ensure its accuracy, but errors and omissions are possible.

All comments related to taxation are general in nature and are based on current Canadian tax legislation for Canadian residents, which is subject to change. Persons who are not residents in Canada or who are resident in Canada but are citizens of another country, may be subject to different tax rules in Canada and may also be subject to taxes levied by jurisdictions other than Canada.

For individual circumstances, consult with legal or tax professionals.

This information is current as of January 10, 2007

3

Agenda

Business continuity planning Keyperson protection Funding shareholder agreements

4

Keyperson ProtectionKeyperson Protection

5

The success of a business

The right strategy The right product / service The right market The right price

The right people!

6

Who are the key employees

Key decision makers Financial and operations management Research Technology Marketing Sales Etc.

7

Who are the key employees

The owner-managers Any other employees who have a

financial impact on the success of the business

8

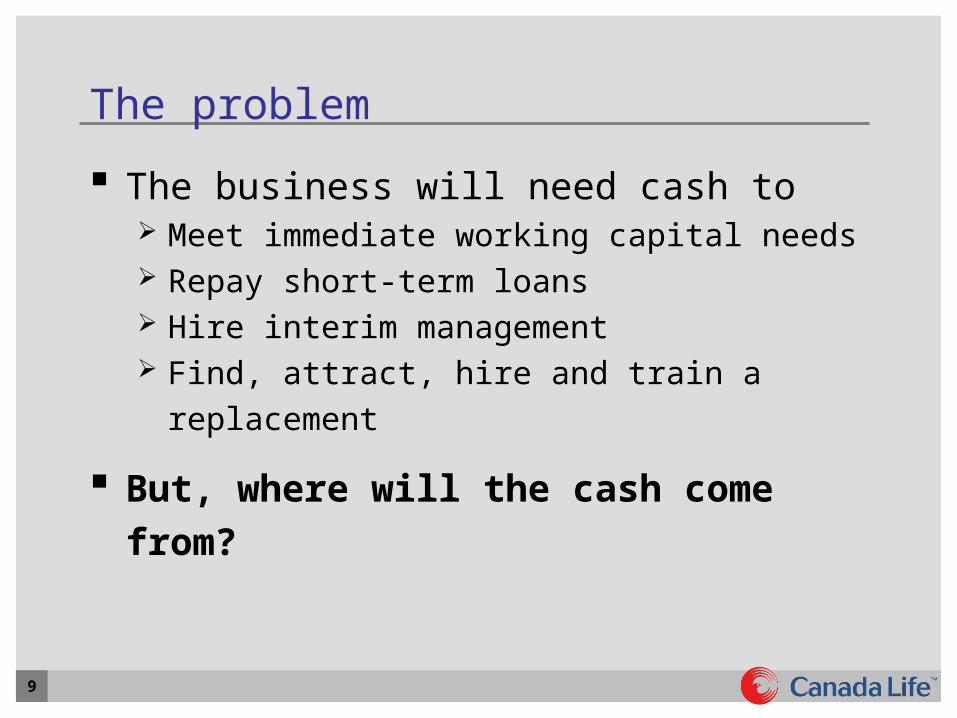

The problem

Premature death of the owner-manager or other key employee: Bankers may call loans Suppliers may not extend credit Customers may not return Employees may seek more secure

employment

Without a source of working capital, the business may not survive!

9

The problem

The business will need cash to Meet immediate working capital needs Repay short-term loans Hire interim management Find, attract, hire and train a replacement

But, where will the cash come from?

10

The solution

Business earnings? The bank? Family? Friends? Investors?

Life insurance!

11

Key person insurance protection

Planning considerations Type of policy Life insured Owner Beneficiary Premium payer Premiums are not tax deductible Death benefit is tax-free Credit to CDA

12

Prospect profile

Private corporation (small or large) Closely held Owner-manager or other key employees Age 30 - 50, healthy Cash flow to pay premiums

13

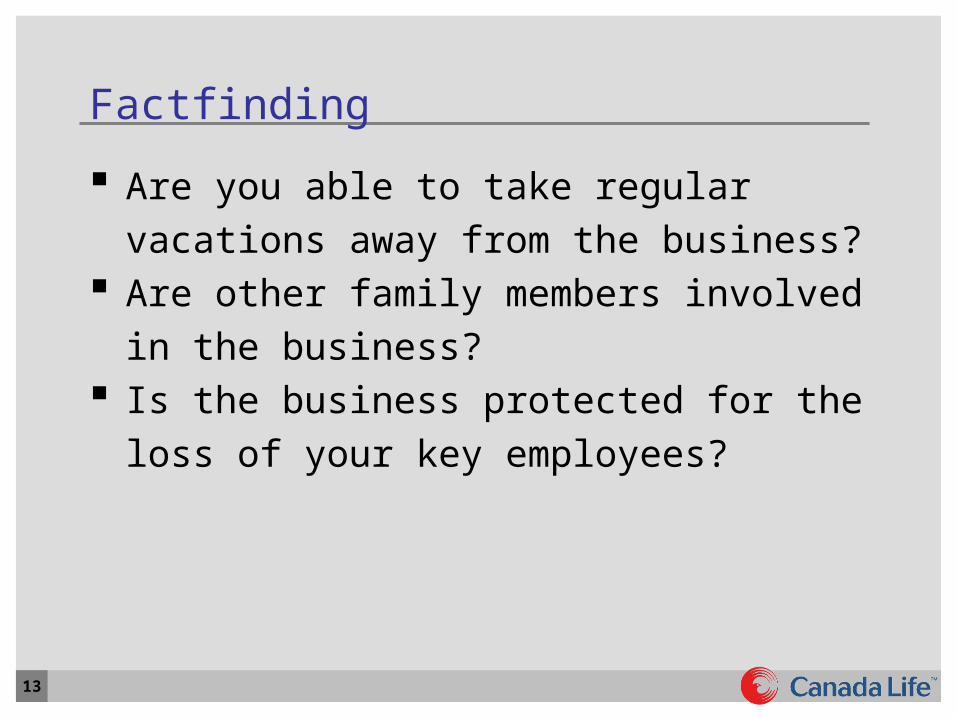

Factfinding

Are you able to take regular vacations away from the business?

Are other family members involved in the business?

Is the business protected for the loss of your key employees?

14

Funding Shareholders AgreementsFunding Shareholders Agreements

15

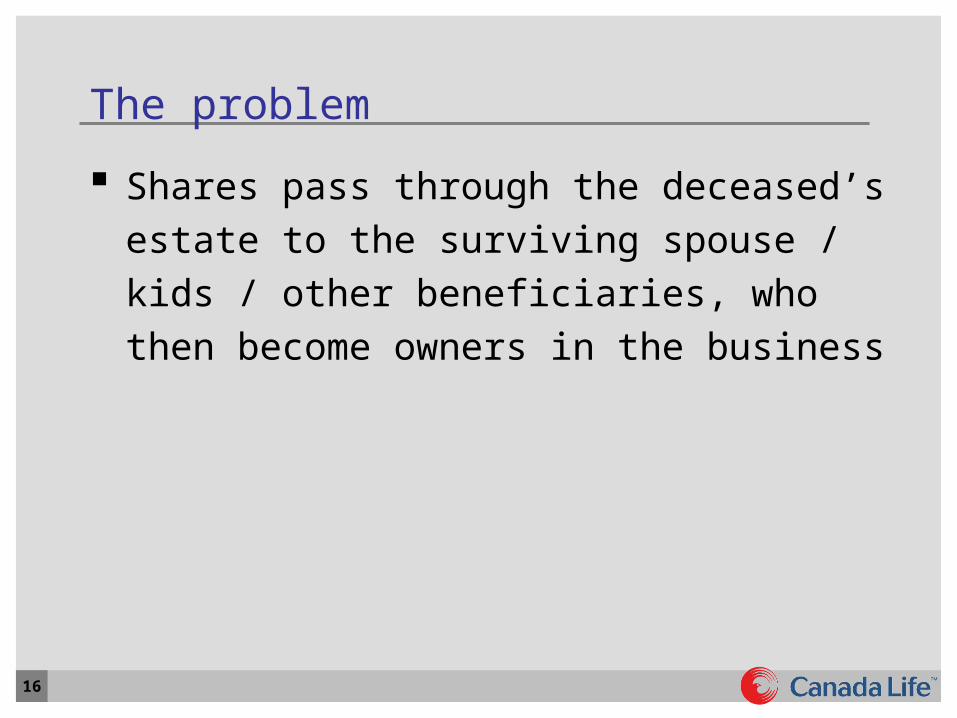

The problem

What happens to the shares of a deceased shareholder if there is no prior arrangement

OPCO

Mr. A Mr. CMs. B

16

The problem

Shares pass through the deceased’s estate to the surviving spouse / kids / other beneficiaries, who then become owners in the business

17

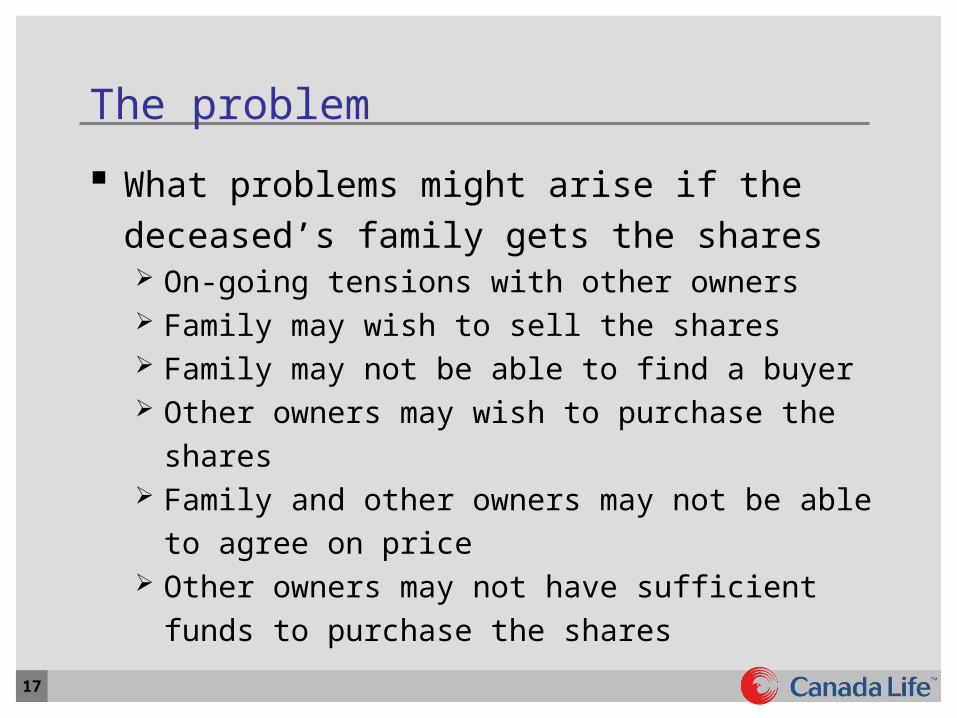

The problem

What problems might arise if the deceased’s family gets the shares On-going tensions with other owners Family may wish to sell the shares Family may not be able to find a buyer Other owners may wish to purchase the

shares Family and other owners may not be able to

agree on price Other owners may not have sufficient funds

to purchase the shares

18

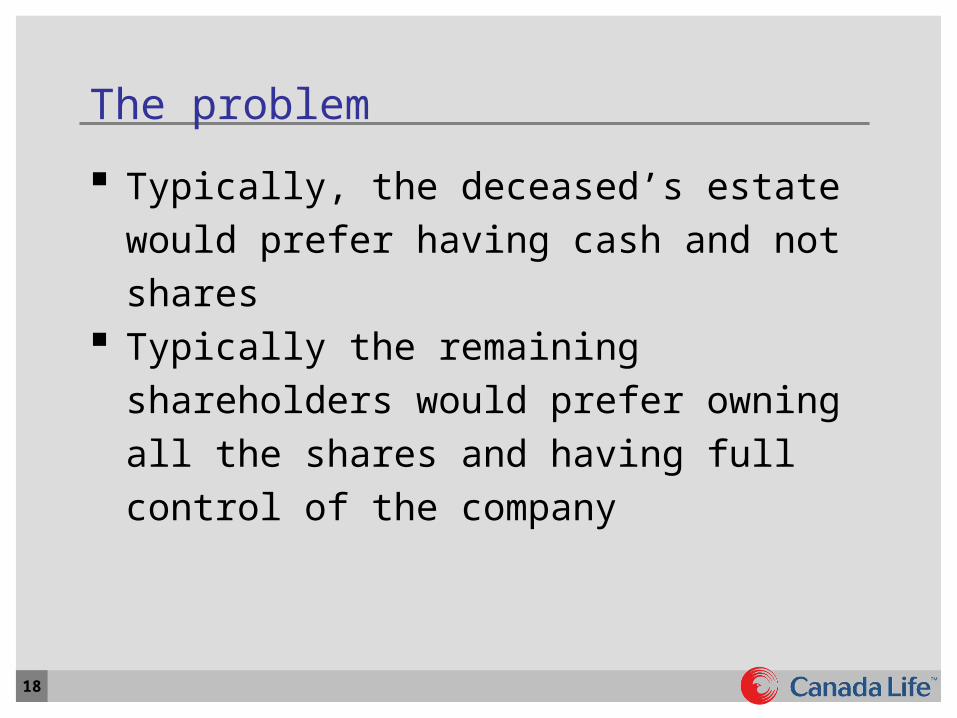

The problem

Typically, the deceased’s estate would prefer having cash and not shares

Typically the remaining shareholders would prefer owning all the shares and having full control of the company

19

The solution

Owners enter into a shareholders agreement Contractual undertaking under which each

shareholder assumes certain rights and obligations

One of the most important business tools Objective is to minimize shareholder disputes Includes buy-sell provisions to help ensure an

orderly transition in the event of the withdrawal of a shareholder for any reason

Pre-funded if possible to reduce financial risk

20

Events covered in an agreement

Dissension between the parties Third party offers Marital breakdown Insolvency Retirement Disability and/or critical illness Death

21

Funding the buy-sell provisions

Funding alternatives Defer the funding obligation until event

occurs- Use corporate or personal cash flow- Use corporate or personal assets- Use bank loans- Use vendor financing

Pre-fund the obligation- Sinking fund (reserve)- Insurance

22

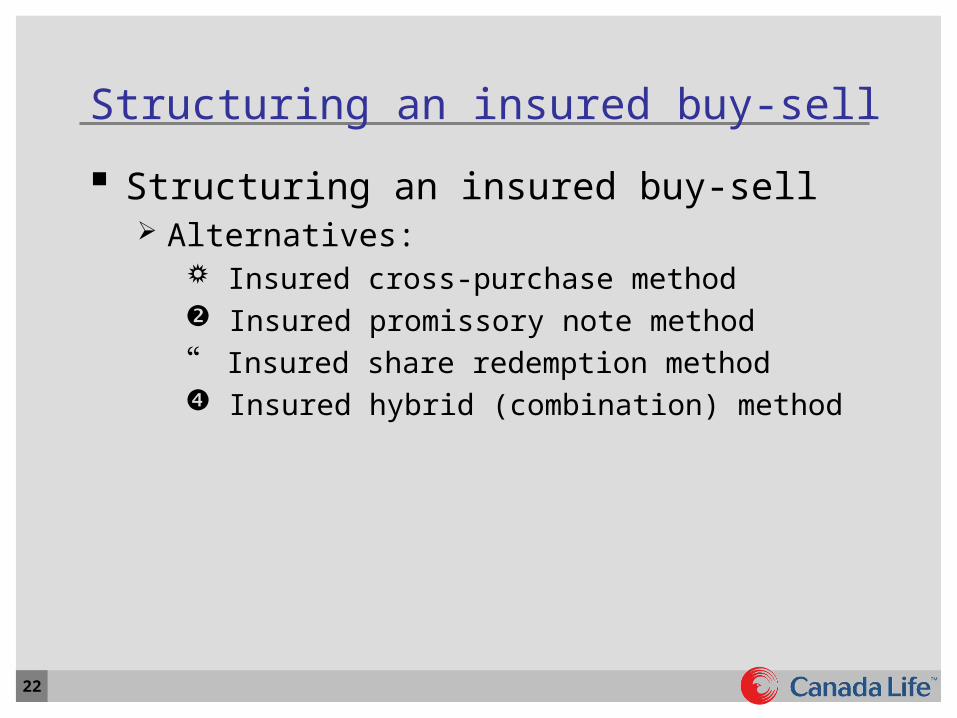

Structuring an insured buy-sell

Structuring an insured buy-sell Alternatives:

Insured cross-purchase method Insured promissory note method Insured share redemption method Insured hybrid (combination) method

23

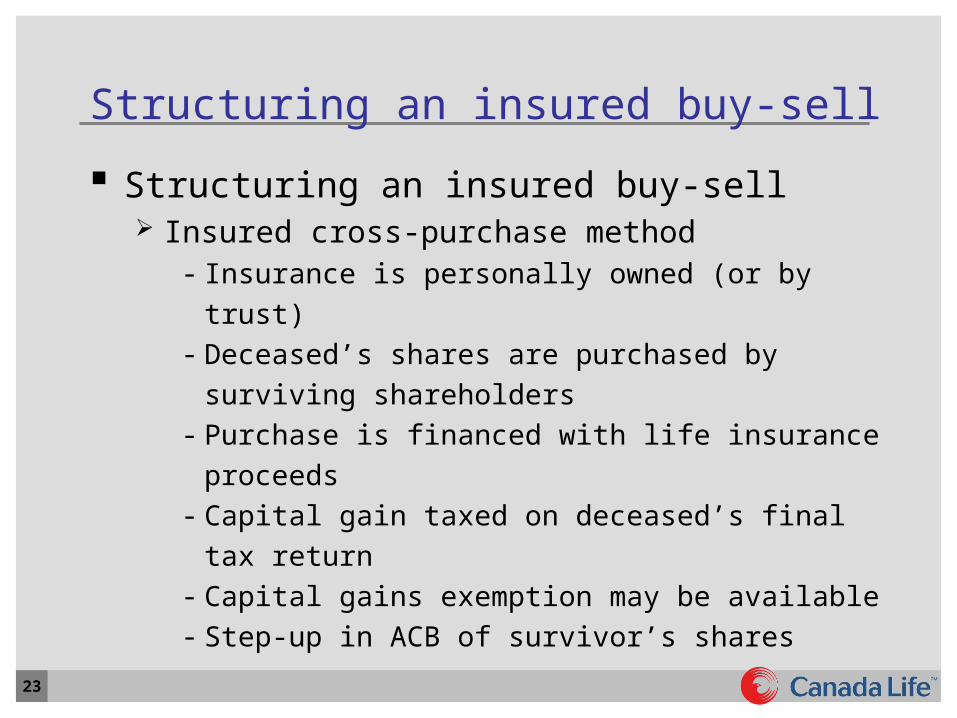

Structuring an insured buy-sell

Structuring an insured buy-sell Insured cross-purchase method

- Insurance is personally owned (or by trust)- Deceased’s shares are purchased by

surviving shareholders- Purchase is financed with life insurance

proceeds- Capital gain taxed on deceased’s final tax

return- Capital gains exemption may be available- Step-up in ACB of survivor’s shares

24

Structuring an insured buy-sell

Structuring an insured buy-sell Insured promissory note method

- Insurance is corporate owned- Deceased’s shares are purchased by

surviving shareholders- Purchase is financed with life insurance

proceeds- Capital gain taxed on deceased’s final tax

return- Capital gains exemption may be available- Step-up in ACB of survivor’s shares

25

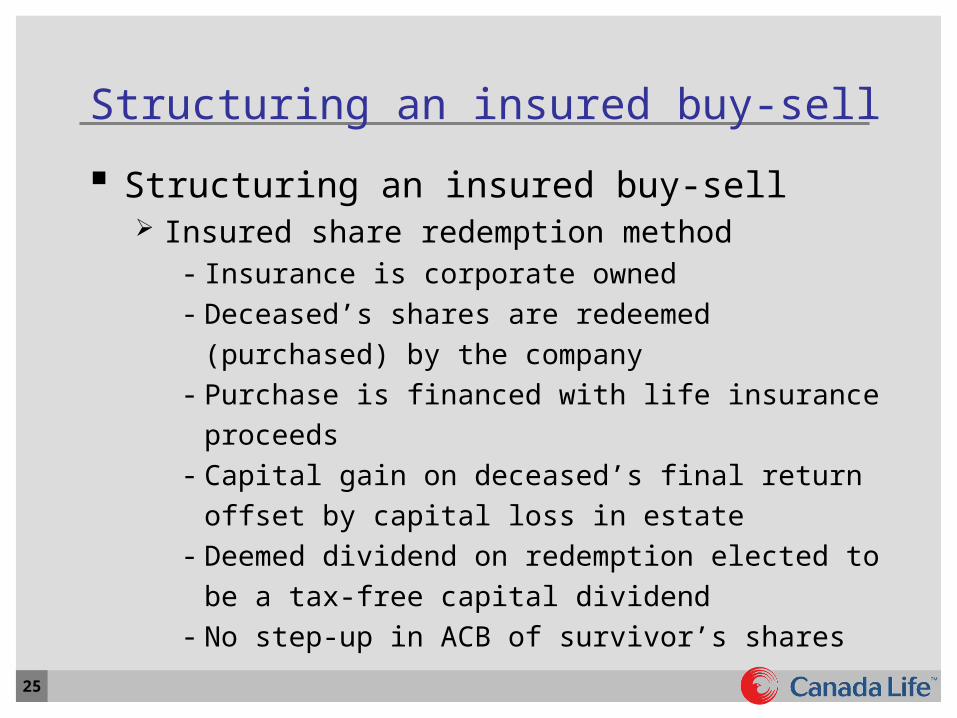

Structuring an insured buy-sell

Structuring an insured buy-sell Insured share redemption method

- Insurance is corporate owned- Deceased’s shares are redeemed (purchased)

by the company- Purchase is financed with life insurance

proceeds- Capital gain on deceased’s final return offset

by capital loss in estate - Deemed dividend on redemption elected to

be a tax-free capital dividend - No step-up in ACB of survivor’s shares

26

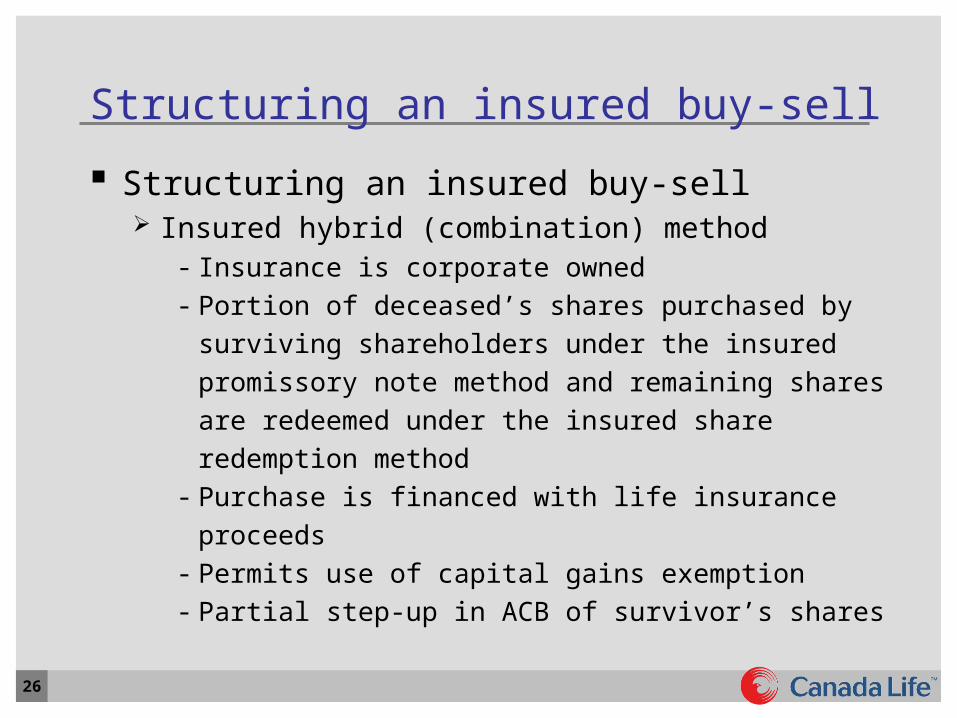

Structuring an insured buy-sell

Structuring an insured buy-sell Insured hybrid (combination) method

- Insurance is corporate owned- Portion of deceased’s shares purchased by

surviving shareholders under the insured promissory note method and remaining shares are redeemed under the insured share redemption method

- Purchase is financed with life insurance proceeds

- Permits use of capital gains exemption- Partial step-up in ACB of survivor’s shares

27

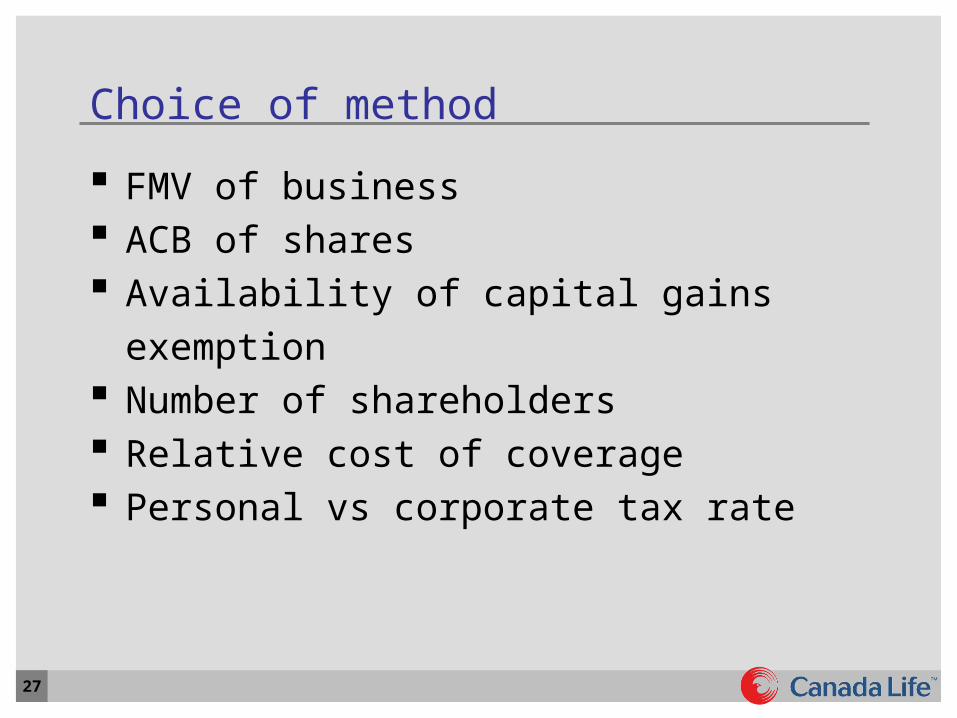

Choice of method

FMV of business ACB of shares Availability of capital gains exemption Number of shareholders Relative cost of coverage Personal vs corporate tax rate

28

Case study

Smith Jones

OPCO

50Shares

50Shares

Fair Market Value = $1,000,000Fair Market Value = $1,000,000

FMV = $500,000ACB = $0PUC = $0

FMV = $500,000ACB = $0PUC = $0

29

Case study

Solution (in this case study) Insured promissory note method

- $500,000 life insurance coverage on each owner (at least!)

- Opco owns the policy, pays premiums and is the beneficiary

- Premiums are not tax deductible!

30

Case study

Steps Insured promissory note method

- $500,000 life insurance pays tax-free death benefit to Opco following death of shareholder

- Excess of proceeds over policy ACB credited to capital dividend account

- Survivor purchases shares from deceased’s estate in return for promissory note

- Opco distributes insurance proceeds to survivor as tax-free capital dividend

- Survivor uses cash to pay off the promissory note

31

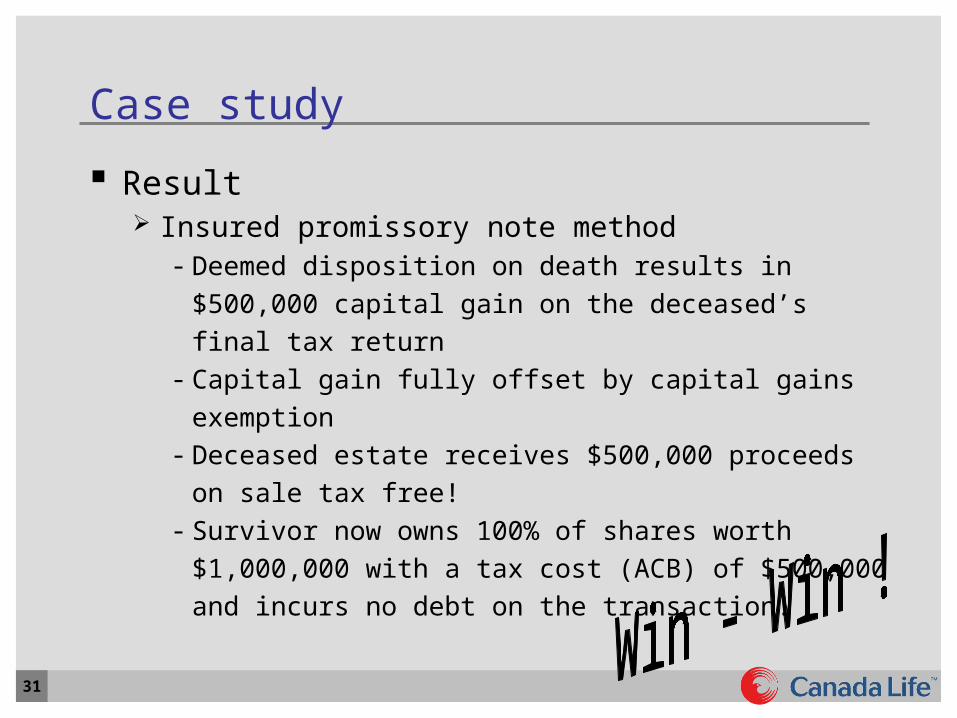

Case study

Result Insured promissory note method

- Deemed disposition on death results in $500,000 capital gain on the deceased’s final tax return

- Capital gain fully offset by capital gains exemption

- Deceased estate receives $500,000 proceeds on sale tax free!

- Survivor now owns 100% of shares worth $1,000,000 with a tax cost (ACB) of $500,000 and incurs no debt on the transaction!

32

Questions?

Thank You!