Embed Size (px)

Citation preview

"Revisiting Asian Financial Crisis for Envisioning Commodity Market Outlook”

Presented by : Ali Muhammad LakdawalaITC Ltd (Foods Division)

Email : [email protected]

GLOBOIL 2017, Mumbai

Views shared in the paper are author’s view and not to be

considered as company’s view or being endorsed by

company which author represents.Disclaimer

Why Revisiting 1997 Crisis???

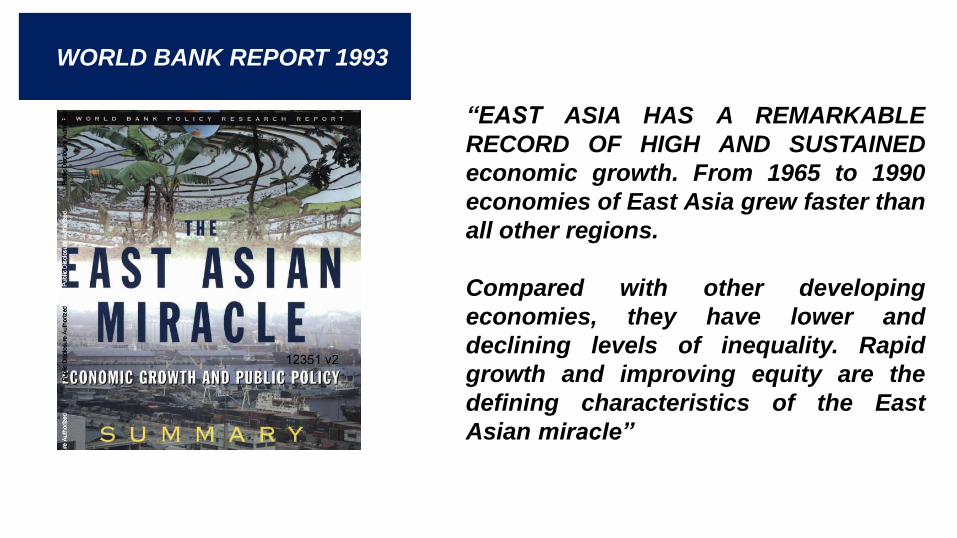

WORLD BANK REPORT 1993

“EAST ASIA HAS A REMARKABLE

RECORD OF HIGH AND SUSTAINED

economic growth. From 1965 to 1990

economies of East Asia grew faster than

all other regions.

Compared with other developing

economies, they have lower and

declining levels of inequality. Rapid

growth and improving equity are the

defining characteristics of the East

Asian miracle”

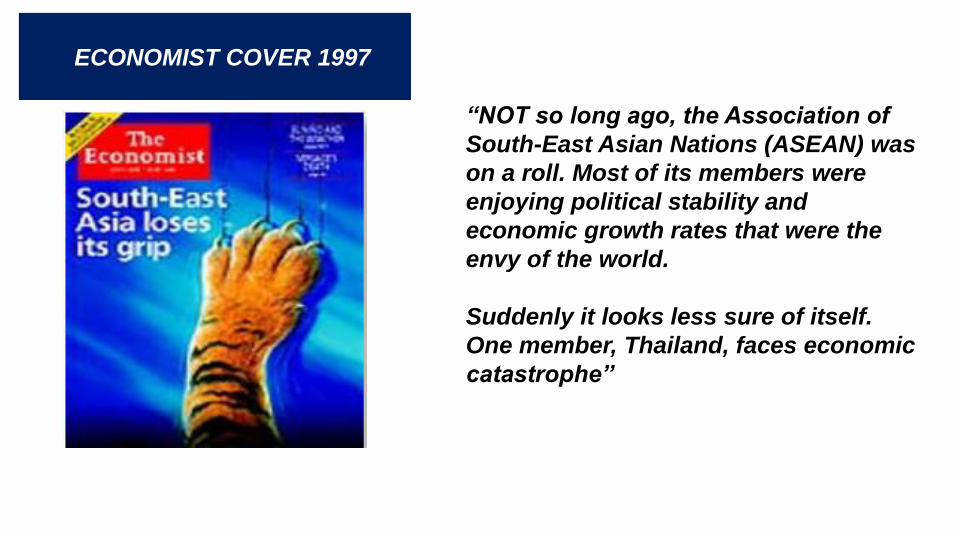

ECONOMIST COVER 1997

“NOT so long ago, the Association of

South-East Asian Nations (ASEAN) was

on a roll. Most of its members were

enjoying political stability and

economic growth rates that were the

envy of the world.

Suddenly it looks less sure of itself.

One member, Thailand, faces economic

catastrophe”

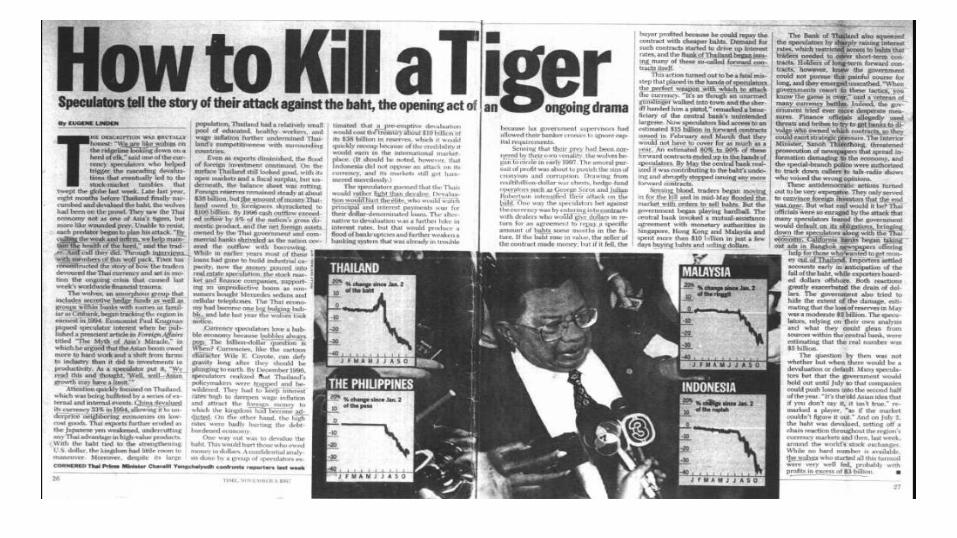

“The crisis takes a much longer time coming than you think, and then it happens

much faster than you would have thought." – Rudiger Dornbusch

The above quote by German Economist holds good while analysing 1997 Asian Financial Crisis, as region

enjoyed decades of buoyant growth, suddenly what started out as a currency crisis (Thai Baht) with large

devaluation of domestic currencies, quickly evolved into a financial crisis in which banks were unable to

repay their foreign debts. In turn, this lead to an economic crisis as domestic firms were starved of credit

and went bankrupt : illiquidity turned quickly into insolvency.

Was Asian economy's growth model flawed or was it due to MULTIPLE EQUILIBRIA : both good and bad

due to which an external event triggered a move from a good to a bad one or was it a Commodity

/Resource Curse???

The purpose of this paper is to shed some light on this questions, post which it will analyse how it

impacted Key Commodities. Followed by understanding the on-going tectonic shift in global growth as

baton gets exchanged between developed & developing nations. Finally concluding with analysing the

market structure for commodities and estimating the price forecasts for next year.

Abstract

Presentation Flow

• Asia Growth Story

• Was it really “Asia” Financial Crisis???

• Impact on Commodities

• Current Scenario

• What NEXT???

• Commodity Market Structure

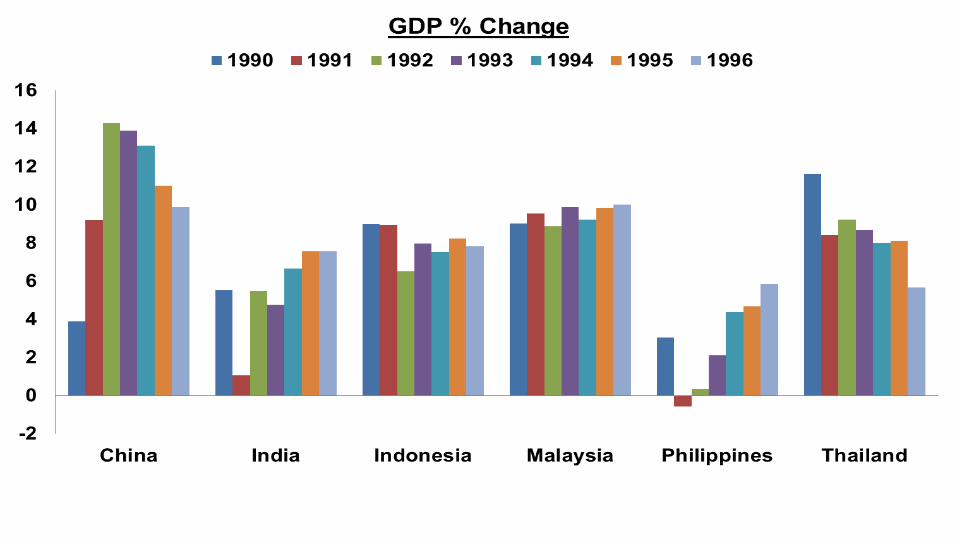

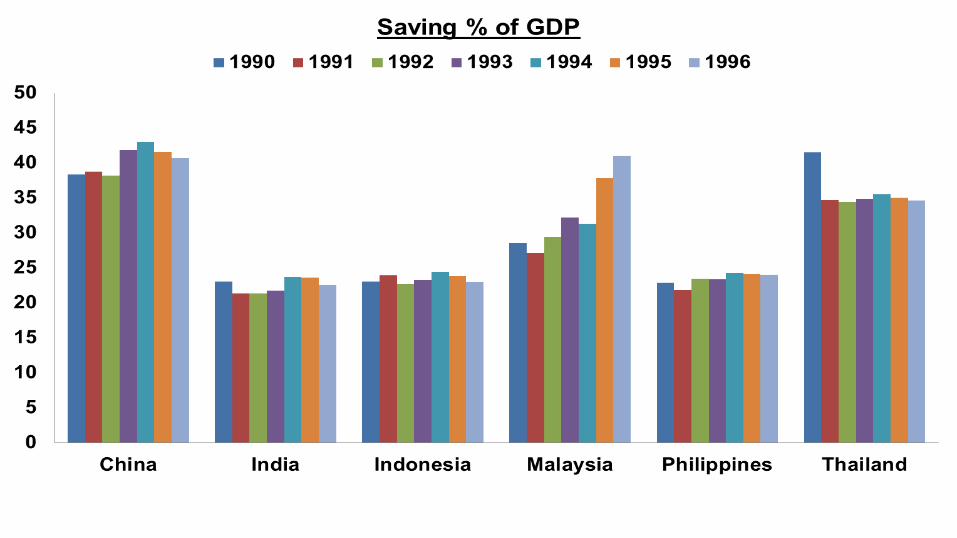

VUCA ASIA GROWTH STORYRapid economic growth, Persistence of rapid economic growth – an unprecedented long period of economic

expansion, Moderate Inflation & Political stability

WMD “Where are they???"

WMD “Where are they???"

WMD “Where are they???"

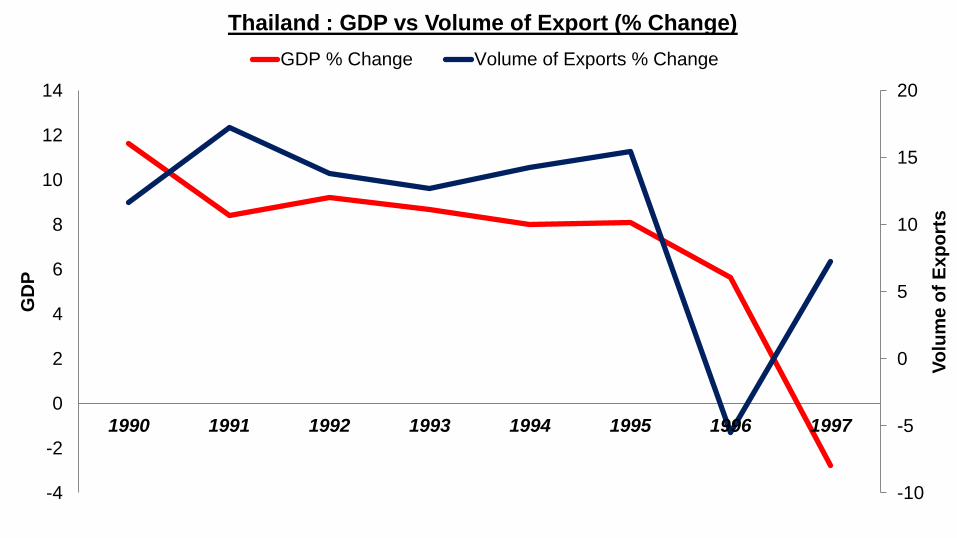

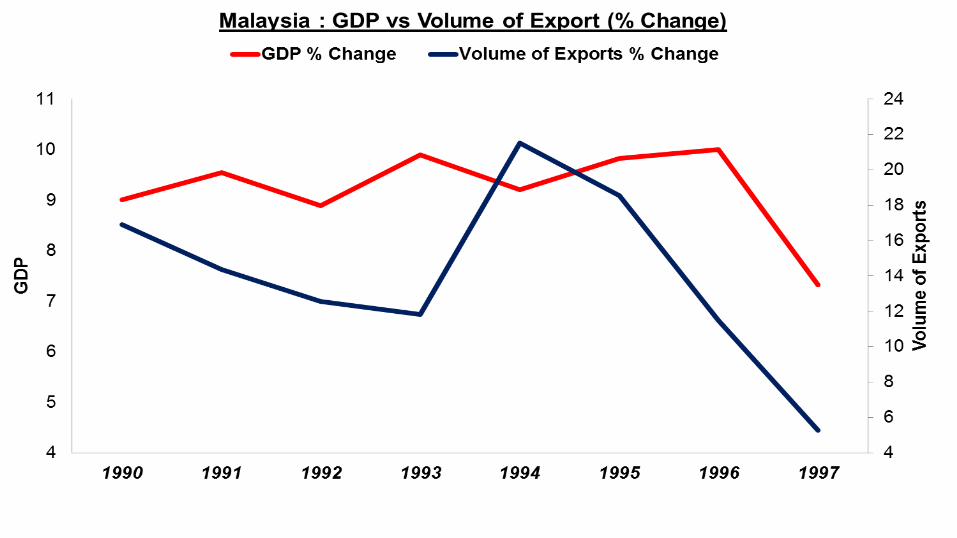

VUCAWas it really “ASIA” FINANCIAL CRISIS???

Capital inflows, especially when volatile, denominated in foreign currencies and not properly hedged against exchange rate

risks, may pose macroeconomic and financial problems in the recipient economy

-10

-5

0

5

10

15

20

-4

-2

0

2

4

6

8

10

12

14

1990 1991 1992 1993 1994 1995 1996 1997

Vo

lum

e o

f E

xp

ort

s

GD

PThailand : GDP vs Volume of Export (% Change)

GDP % Change Volume of Exports % Change

VUCAIMPACT ON COMMODITIES

Most populous region of the world needs resources to feed & fuel its economy : hence key influencer in commodity market

5.00

10.00

15.00

20.00

25.00

30.00

Ja

n-9

6

Fe

b-9

6

Ma

r-9

6

Ap

r-9

6

Ma

y-9

6

Ju

n-9

6

Ju

l-9

6

Au

g-9

6

Se

p-9

6

Oc

t-9

6

No

v-9

6

De

c-9

6

Jan

-97

Fe

b-9

7

Ma

r-9

7

Ap

r-9

7

Ma

y-9

7

Ju

n-9

7

Ju

l-9

7

Au

g-9

7

Se

p-9

7

Oc

t-9

7

No

v-9

7

De

c-9

7

Ja

n-9

8

Fe

b-9

8

Ma

r-9

8

Ap

r-98

Ma

y-9

8

Ju

n-9

8

Ju

l-9

8

Au

g-9

8

Se

p-9

8

Oc

t-9

8

No

v-9

8

De

c-9

8

Brent Crude $/bbl

1200.00

1400.00

1600.00

1800.00

2000.00

2200.00

2400.00

2600.00

2800.00

Ja

n-9

6

Fe

b-9

6

Ma

r-9

6

Ap

r-9

6

Ma

y-9

6

Ju

n-9

6

Ju

l-9

6

Au

g-9

6

Se

p-9

6

Oct-

96

No

v-9

6

De

c-9

6

Ja

n-9

7

Fe

b-9

7

Ma

r-9

7

Ap

r-9

7

Ma

y-9

7

Ju

n-9

7

Ju

l-9

7

Au

g-9

7

Se

p-9

7

Oc

t-9

7

No

v-9

7

De

c-9

7

Ja

n-9

8

Fe

b-9

8

Ma

r-9

8

Ap

r-9

8

Ma

y-9

8

Ju

n-9

8

Ju

l-9

8

Au

g-9

8

Sep

-98

Oc

t-9

8

No

v-9

8

De

c-9

8

Copper ($/MT)

90.0000

95.0000

100.0000

105.0000

110.0000

115.0000

120.0000

125.0000

Jan

-96

Fe

b-9

6M

ar-

96

Ap

r-96

May-9

6Ju

n-9

6Ju

l-96

Au

g-9

6S

ep

-96

Oct-

96

No

v-9

6D

ec

-96

Jan

-97

Fe

b-9

7M

ar-

97

Ap

r-97

May-9

7Ju

n-9

7Ju

l-97

Au

g-9

7S

ep

-97

Oct-

97

No

v-9

7D

ec

-97

Jan

-98

Fe

b-9

8M

ar-

98

Ap

r-98

May-9

8J

un

-98

Ju

l-98

Au

g-9

8S

ep

-98

Oct-

98

No

v-9

8D

ec

-98

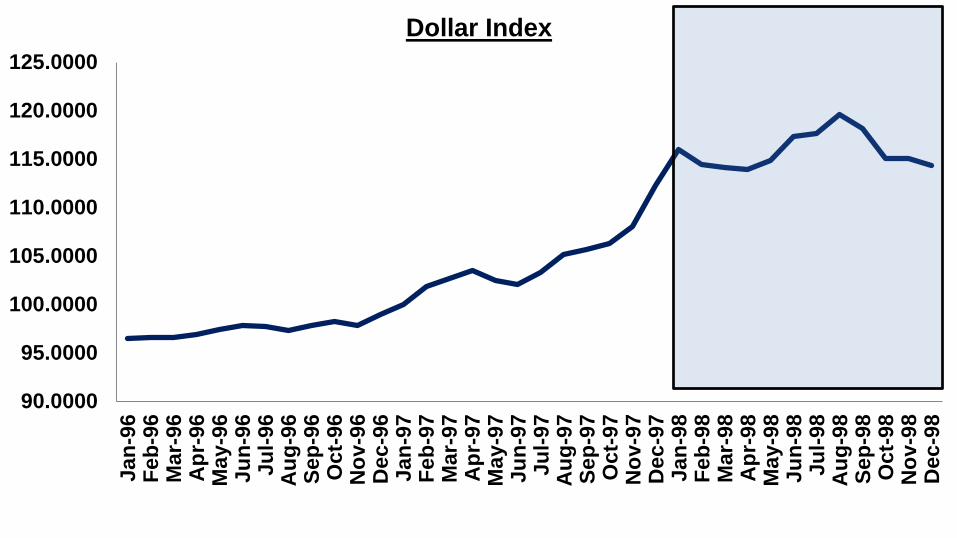

Dollar Index

0

1

2

3

4

5

6

7

1991 1992 1993 1994 1995 1996 1997 1998

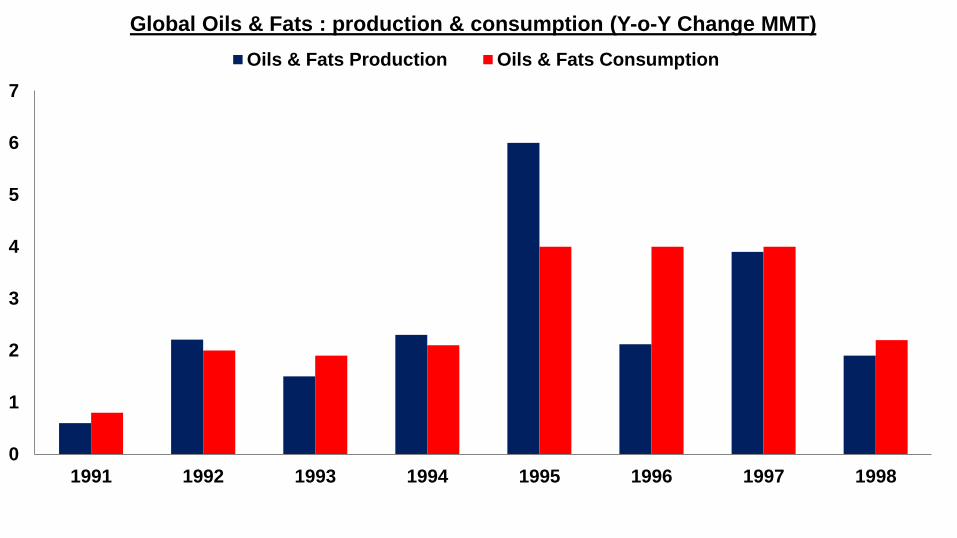

Global Oils & Fats : production & consumption (Y-o-Y Change MMT)

Oils & Fats Production Oils & Fats Consumption

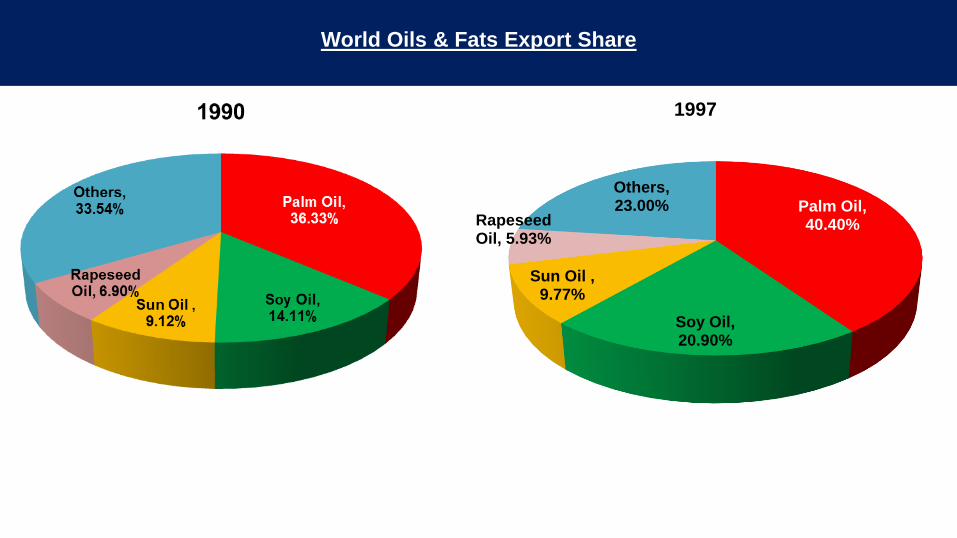

Palm Oil, 40.40%

Soy Oil, 20.90%

Sun Oil , 9.77%

Rapeseed Oil, 5.93%

Others, 23.00%

1997

World Oils & Fats Export Share

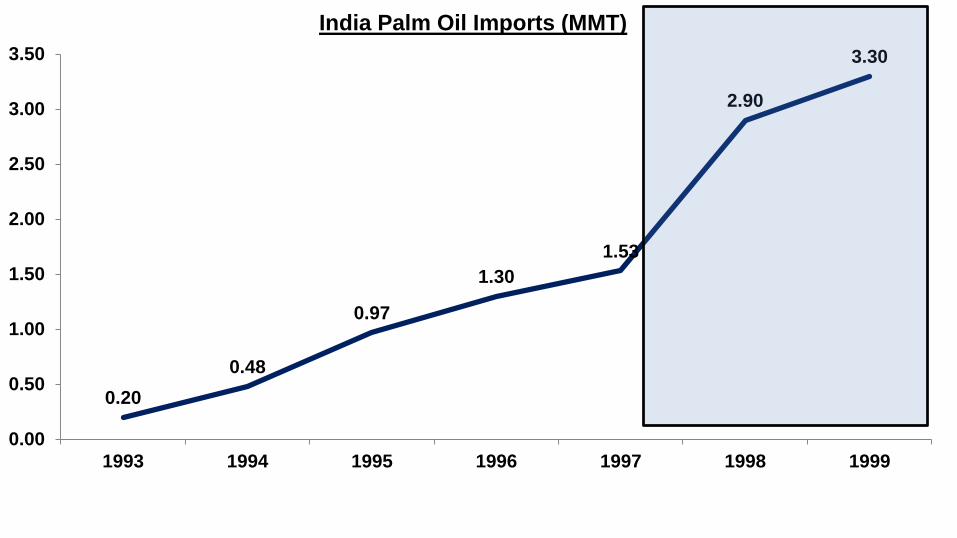

0.20

0.48

0.97

1.30

1.53

2.90

3.30

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1993 1994 1995 1996 1997 1998 1999

India Palm Oil Imports (MMT)

VUCACURRENT SCENARIO

Fast Forwarding from 1997 to 2017

Era of VUCA : Volatility, Uncertainty, Complexity, and Ambiguity—reflecting an unstable

and rapidly changing economic environment

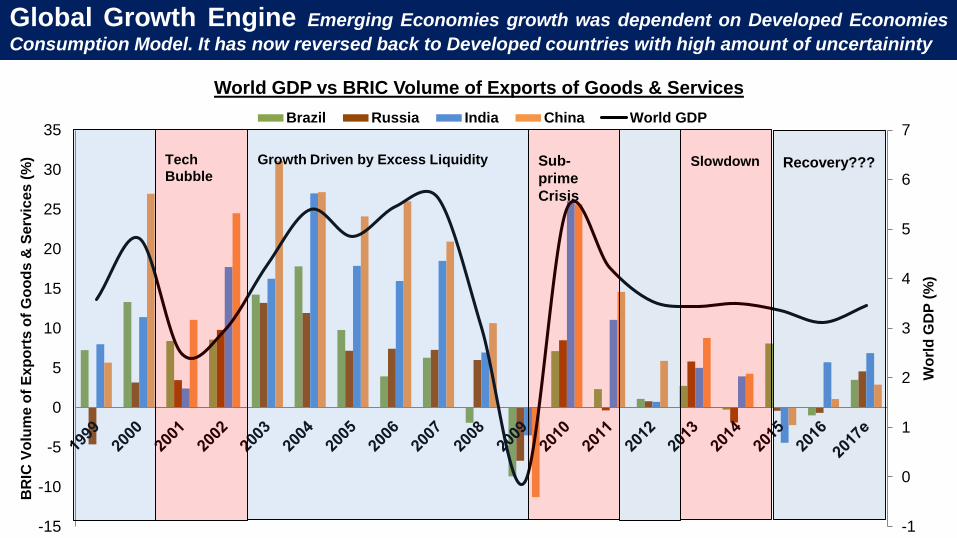

Global Growth Engine Emerging Economies growth was dependent on Developed Economies

Consumption Model. It has now reversed back to Developed countries with high amount of uncertaininty

-1

0

1

2

3

4

5

6

7

-15

-10

-5

0

5

10

15

20

25

30

35

Wo

rld

GD

P (

%)

BR

IC V

olu

me

of

Ex

po

rts

of

Go

od

s &

Se

rvic

es

(%

)

World GDP vs BRIC Volume of Exports of Goods & Services

Brazil Russia India China World GDP

Tech

BubbleSub-

prime

Crisis

Growth Driven by Excess Liquidity Slowdown Recovery???

THE ONLY GAME IN TOWN (by) CENTRAL BANKERS : are we getting ready to live

in an era of rising interest rates??? Within the year’s time we have started to see significant change in

interest rates movement across the globe & FED looks more aggressive compared to others

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

US Japan Sweden Denmark Switzerland

Interest Rates %

2016 2017

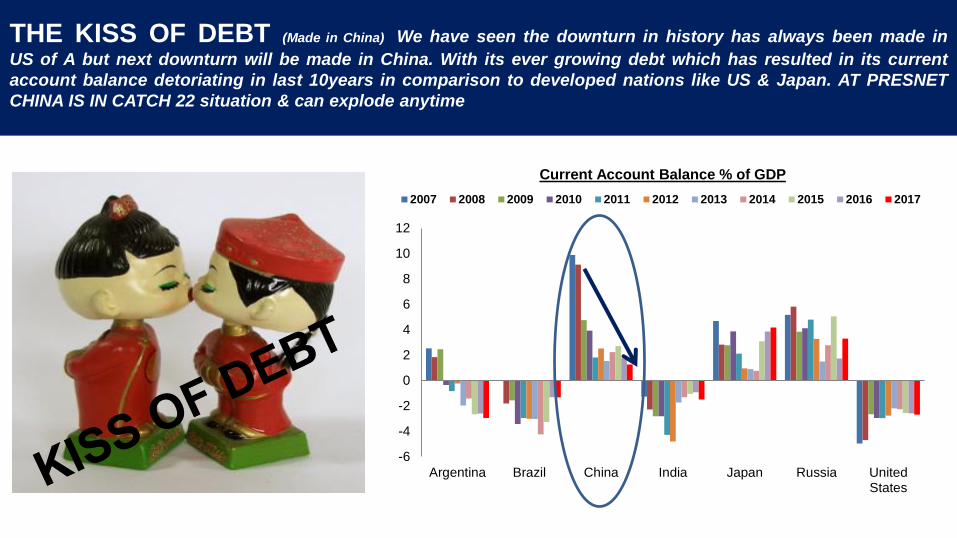

THE KISS OF DEBT (Made in China) We have seen the downturn in history has always been made in

US of A but next downturn will be made in China. With its ever growing debt which has resulted in its current

account balance detoriating in last 10years in comparison to developed nations like US & Japan. AT PRESNET

CHINA IS IN CATCH 22 situation & can explode anytime

-6

-4

-2

0

2

4

6

8

10

12

Argentina Brazil China India Japan Russia UnitedStates

Current Account Balance % of GDP

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

VUCA WHAT NEXT???It’s Gonna be 4D World

DEGLOBALISATION increasing PROTECTIONISM & TECHNOLOGICAL ADVANCEMENT will

inflict pain in GLOBAL TRADE

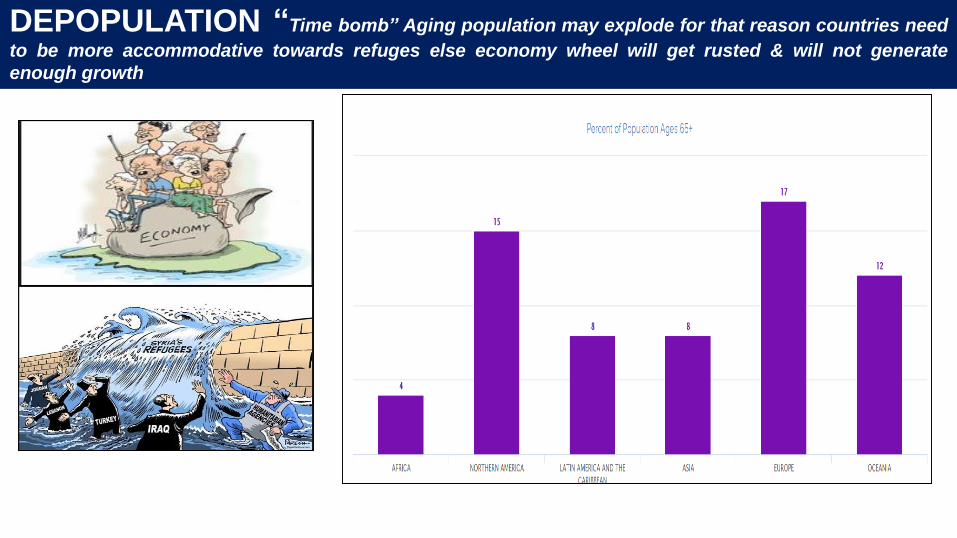

DEPOPULATION “Time bomb” Aging population may explode for that reason countries need

to be more accommodative towards refuges else economy wheel will get rusted & will not generate

enough growth

DEMONITISATION a sudden shift towards demonetisation would slow down growth engine

also it opens up major risk of Cyber Crime

DEBT GLUT is rising across

VUCACOMMODITY MARKET STRUCTURE

100

120

140

160

180

200

220

240

260

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

Q1-2

011

Q2

-20

11

Q3

-20

11

Q4

-20

11

Q1

-20

12

Q2

-20

12

Q3

-20

12

Q4

-20

12

Q1

-20

13

Q2

-20

13

Q3

-20

13

Q4-2

013

Q1

-20

14

Q2

-20

14

Q3-2

014

Q4

-20

14

Q1

-20

15

Q2

-20

15

Q3

-20

15

Q4

-20

15

Q1

-20

16

Q2

-20

16

Q3

-20

16

Q4

-20

16

Q1

-20

17

Meta

l In

dex

Ch

ina

GD

P

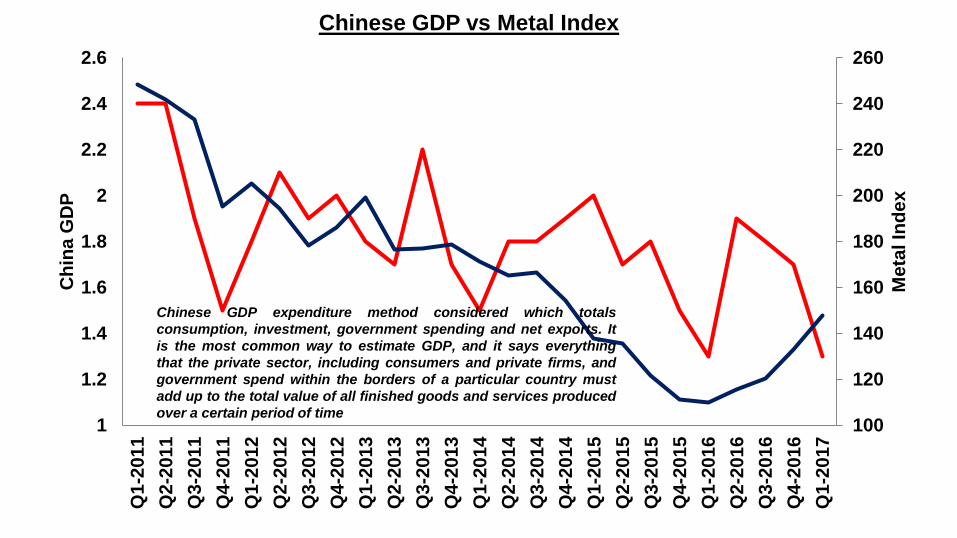

Chinese GDP vs Metal Index

Chinese GDP expenditure method considered which totals

consumption, investment, government spending and net exports. It

is the most common way to estimate GDP, and it says everything

that the private sector, including consumers and private firms, and

government spend within the borders of a particular country must

add up to the total value of all finished goods and services produced

over a certain period of time

80.00

100.00

120.00

140.00

160.00

180.00

200.00

220.00

240.00

5.0000

6.0000

7.0000

8.0000

Jan-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-0

9

Dec-0

9

Ma

y-1

0

Oct-

10

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

Nov-1

2

Ap

r-1

3

Se

p-1

3

Fe

b-1

4

Ju

l-1

4

De

c-1

4

Ma

y-1

5

Oct-

15

Ma

r-1

6

Au

g-1

6

Ja

n-1

7

Jun-1

7

Co

mD

ex

Yu

an

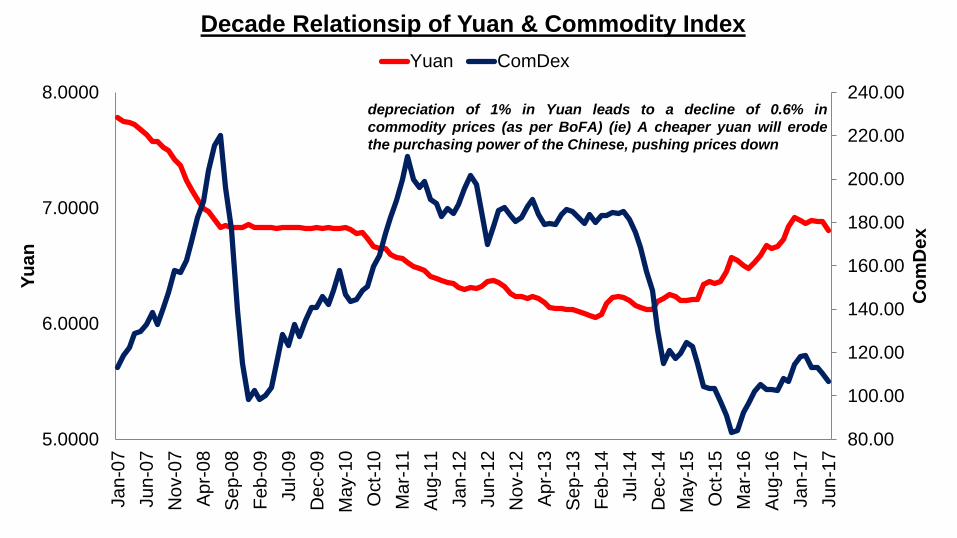

Decade Relationsip of Yuan & Commodity Index

Yuan ComDex

depreciation of 1% in Yuan leads to a decline of 0.6% in

commodity prices (as per BoFA) (ie) A cheaper yuan will erode

the purchasing power of the Chinese, pushing prices down

80

90

100

110

120

130

140

150

160

0.00

1.00

2.00

3.00

4.00

5.00

6.002

00

7-0

1-0

1

2007-0

6-0

1

20

07

-11

-01

20

08

-04

-01

20

08

-09

-01

2009-0

2-0

1

20

09

-07

-01

20

09

-12

-01

20

10

-05

-01

2010-1

0-0

1

20

11

-03

-01

20

11

-08

-01

20

12

-01

-01

2012-0

6-0

1

20

12

-11

-01

20

13

-04

-01

20

13

-09

-01

2014-0

2-0

1

20

14

-07

-01

20

14

-12

-01

20

15

-05

-01

2015-1

0-0

1

20

16

-03

-01

20

16

-08

-01

20

17

-01

-01

US

Liq

uid

ity I

nd

ex

Fe

d F

un

d R

ate

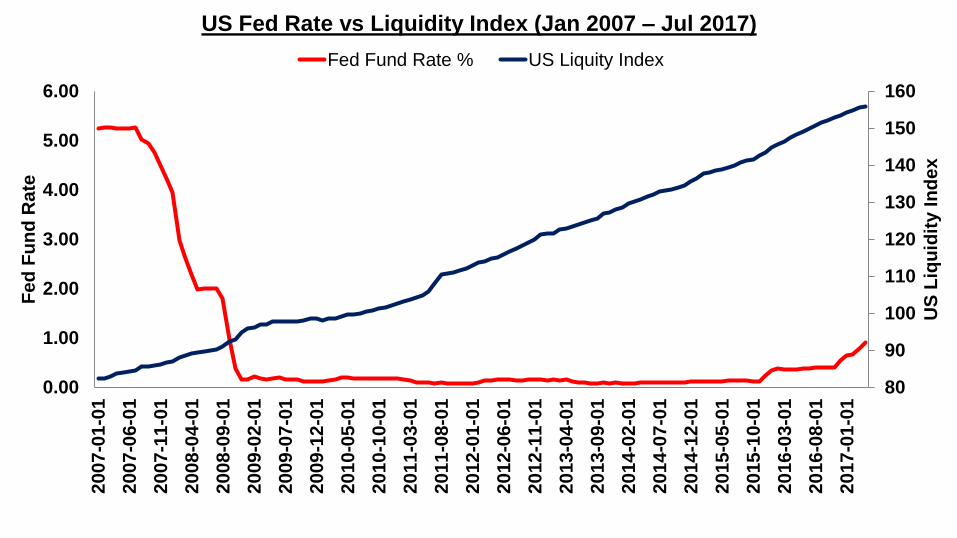

US Fed Rate vs Liquidity Index (Jan 2007 – Jul 2017)

Fed Fund Rate % US Liquity Index

80.00

100.00

120.00

140.00

160.00

180.00

200.00

220.00

240.00

90.00

95.00

100.00

105.00

110.00

115.00

120.00

125.00

130.00

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-09

De

c-0

9

Ma

y-1

0

Oc

t-1

0

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

Ap

r-1

3

Se

p-1

3

Fe

b-1

4

Ju

l-1

4

De

c-1

4

May-1

5

Oc

t-1

5

Ma

r-1

6

Au

g-1

6

Ja

n-1

7

Ju

n-1

7

Co

mD

ex

DX

YDecade Relationsip of Dollar Index & Commodity Index

DXY ComDex

40.00

60.00

80.00

100.00

120.00

140.00

160.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Feb

-09

Ju

l-0

9

De

c-0

9

May-1

0

Oc

t-1

0

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

Ap

r-1

3

Se

p-1

3

Fe

b-1

4

Ju

l-1

4

De

c-1

4

Ma

y-1

5

Oc

t-1

5

Mar-

16

Au

g-1

6

Ja

n-1

7

Ju

n-1

7

Ed

ible

Oil

In

de

x

En

erg

y I

nd

ex

Energy Index vs Edible Oil Index (Jan 2007-Aug 2017)

Energy Index Edible Oil Index

VUCAWHAT’s IN STORE FOR OIL COMPLEX???

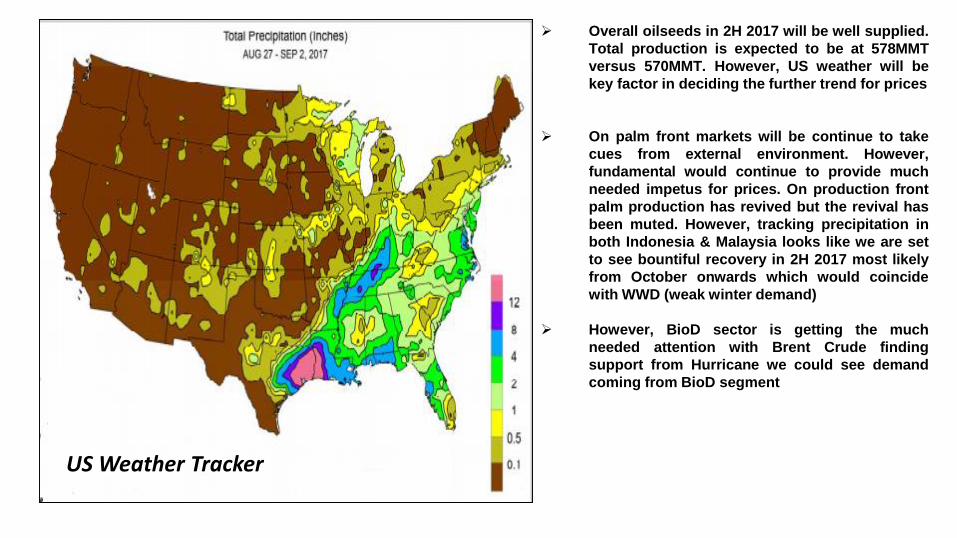

Indonesia Current Precipitation at Key Growing Areas

(as on 10th Sep 2017)SUMATRA

KALIMANTAN RIAU

Malaysia Current Precipitation at Key Growing Areas

(as on 10th Sep 2017)

Overall oilseeds in 2H 2017 will be well supplied.

Total production is expected to be at 578MMT

versus 570MMT. However, US weather will be

key factor in deciding the further trend for prices

On palm front markets will be continue to take

cues from external environment. However,

fundamental would continue to provide much

needed impetus for prices. On production front

palm production has revived but the revival has

been muted. However, tracking precipitation in

both Indonesia & Malaysia looks like we are set

to see bountiful recovery in 2H 2017 most likely

from October onwards which would coincide

with WWD (weak winter demand)

However, BioD sector is getting the much

needed attention with Brent Crude finding

support from Hurricane we could see demand

coming from BioD segment

US Weather Tracker

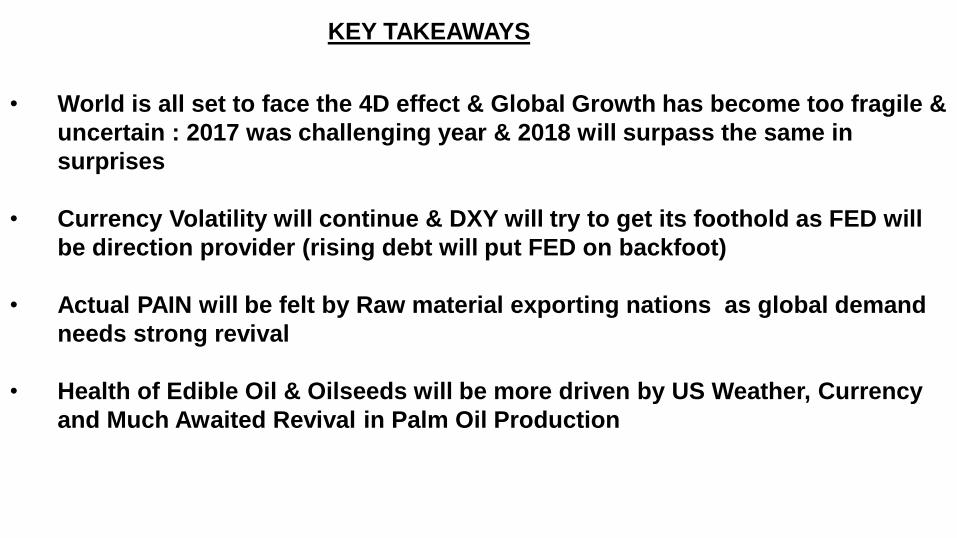

• World is all set to face the 4D effect & Global Growth has become too fragile &

uncertain : 2017 was challenging year & 2018 will surpass the same in

surprises

• Currency Volatility will continue & DXY will try to get its foothold as FED will

be direction provider (rising debt will put FED on backfoot)

• Actual PAIN will be felt by Raw material exporting nations as global demand

needs strong revival

• Health of Edible Oil & Oilseeds will be more driven by US Weather, Currency

and Much Awaited Revival in Palm Oil Production

KEY TAKEAWAYS

VUCAOUTLOOK

“THE Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil.”

Sheikh Zaki Yamani

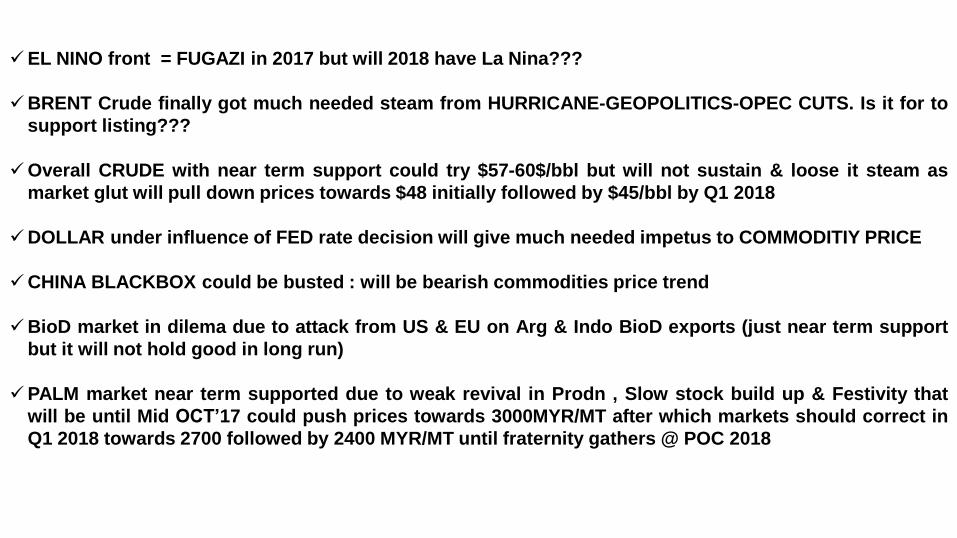

EL NINO front = FUGAZI in 2017 but will 2018 have La Nina???

BRENT Crude finally got much needed steam from HURRICANE-GEOPOLITICS-OPEC CUTS. Is it for to

support listing???

Overall CRUDE with near term support could try $57-60$/bbl but will not sustain & loose it steam as

market glut will pull down prices towards $48 initially followed by $45/bbl by Q1 2018

DOLLAR under influence of FED rate decision will give much needed impetus to COMMODITIY PRICE

CHINA BLACKBOX could be busted : will be bearish commodities price trend

BioD market in dilema due to attack from US & EU on Arg & Indo BioD exports (just near term support

but it will not hold good in long run)

PALM market near term supported due to weak revival in Prodn , Slow stock build up & Festivity that

will be until Mid OCT’17 could push prices towards 3000MYR/MT after which markets should correct in

Q1 2018 towards 2700 followed by 2400 MYR/MT until fraternity gathers @ POC 2018

VUCA Thank You

Disclaimer : Views shared in the paper are author’s view and not to be considered ascompany’s view or being endorsed by company which author represents.