Embed Size (px)

Citation preview

Equity MarketplaceA Blockchain Implementation

About us

I am Tullio Menga, ICT architect and developer.

I have been working in Capital Market area during last twenty years, specifically in the field of high

performance infrastructures.

I am currently collaborating with ATS, Milano (IT), having its core business in Capital Market.

ATS is Innovation Partner of UCL.

We are currently exploring use cases of blockchain technology in OTC derivatives, non-listed equities

and several other areas.

Blockchain in brief

IMMUTABLEDISTRIBUTED

TRANSACTION LEDGER

• immutable, non-tamperabletransactions

• cryptographic encryption

• consensus

SECURITY

• transactions are etched to the ledger as they are processed

• no need for end-of-day batch processes

NEAR-REAL-TIME

• decentralisation

• data replication on nodes

• no single point of failure

REDUDANCY

• smart contracts to define complex business logics

• complex transactions execute atomically

PROCESS

OPTIMIZATION

Blockchain in Capital Market

t+0

t+x

t+y

t+0

TODAYSeveral back-offices use different technologies and interact at

different times, leading to very complex, slow and non-atomic

transactions, possible human errors and slow reaction to failures.

FUTUREDistributed ledgers handle complex transactions atomically, in near-

real-time, and share updates at transaction time, leading to safer and

faster processes, less human errors and quicker reaction to failures.

• Intracompany settlement

• Loan settlement

• Trade settlement

• Trading

• Collateral management

• Derivatives clearing

• Derivatives agreements

• Cross-border payments

FINANCIAL INSTITUTIONS

• Trade reporting

• Compliance reporting

• Risk visualisation

• Transparency regulation

• Anti-money-laundring

REGULATORS

OTC Derivative Trading NON-listed EQUITY Trading

Market Engine (book, matching) X X

Post-trade settlement X X

Contract issuing (master agreement) X

Contract maturity settlement X

Shares management X X

Collateral management X X

Instrument pricing X

Margination management X

Trade-offs

• Requires more features and

more complex

• More problematic normative

aspects (may involve CCP

obligations)

• Requires less features

• Easier normative aspects

(no CCP obligations)

OTC Derivatives and Equities

OTC Derivative Trading NON-listed EQUITY Trading

Market Engine (book, matching) X X

Post-trade settlement X X

Contract issuing (master agreement) X

Contract maturity settlement X

Shares management X X

Collateral management X X

Instrument pricing X

Margination management X

focus of this

presentation

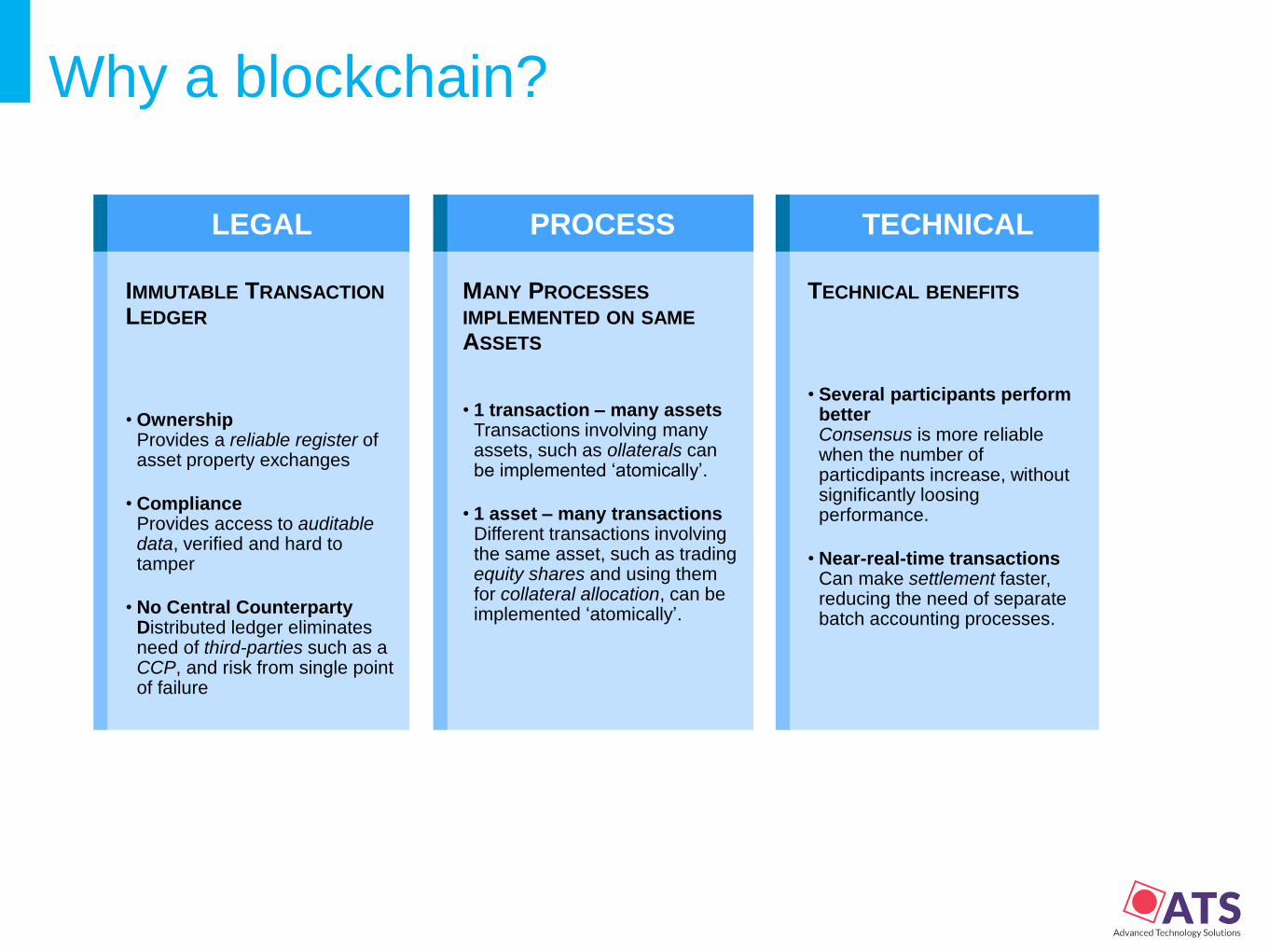

Why a blockchain?

IMMUTABLE TRANSACTION

LEDGER

• OwnershipProvides a reliable register of asset property exchanges

• ComplianceProvides access to auditabledata, verified and hard to tamper

• No Central CounterpartyDistributed ledger eliminatesneed of third-parties such as a CCP, and risk from single pointof failure

MANY PROCESSES

IMPLEMENTED ON SAME

ASSETS

• 1 transaction – many assetsTransactions involving many assets, such as ollaterals can be implemented ‘atomically’.

• 1 asset – many transactionsDifferent transactions involvingthe same asset, such as trading equity shares and using themfor collateral allocation, can be implemented ‘atomically’.

TECHNICAL BENEFITS

• Several participants performbetterConsensus is more reliablewhen the number of particdipants increase, withoutsignificantly loosingperformance.

• Near-real-time transactionsCan make settlement faster, reducing the need of separate batch accounting processes.

LEGAL PROCESS TECHNICAL

Equity Trading Processes

asset:

currency

transactions:

amount transfers

actor:

financial institutions

asset:

equity shares

transactions:

ownership exchanges

actor:

custodians

asset:

collaterals

transactions:

collateral allocations

actor:

central counterparties

CASH

LEDGER

SECURITY

LEDGER

COLLATERAL

LEDGER

blockchain pegging

Equity Trading Ledger

assets:

currency and equity shares

transactions:

trades and collateral allocations

smart contracts:

custodian and central counterparty business logics

actors:

financial institutions only

EQUITY TRADING

LEDGER

OTC Derivatives and EquitiesPrivate – Permissioned Public – Permissionless

Participants Controlled, trusted. Free, trustless.

Potential market liquidity Controlled by participants. All the circulating crypto-currency.

Performance (current) Higher (1 block <3s). Low (1 block in minutes).

SecuritySame as any common private

network.

Relies on anonymous accounts,

must be analysed in details.

Ledger permissioningEmbedded, rules defined by

stakeholders.

Harder to control (participants can

be anonymous).

Regulator / normative implications

Rules can be defined to meet

regulatory compliance.

Regulatory institutions can be

participants themselves

Harder to meet regulator

compliance requirements (it is a

natively cross-border platform).

Our choice

Private – Permissioned Public – Permissionless

Participants Controlled, trusted. Free, trustless.

Potential market liquidity Controlled by participants. All the circulating crypto-currency.

Performance (current) Higher (1 block <3s). Low (1 block in minutes).

SecuritySame as any common private

network.

Relies on anonymous accounts,

must be analysed in details.

Ledger permissioningEmbedded, rules defined by

stakeholders.

Harder to control (participants can

be anonymous).

Regulator / normative implications

Rules can be defined to meet

regulatory compliance.

Regulatory institutions can be

participants themselves

Harder to meet regulator

compliance requirements (it is a

natively cross-border platform).

Trade-offs

• greater performance

• finer permissioning control

• more normative-oriented

(CSDs plays a role)

• more normative oriented

• consensus basis must be built

• greater potential penetration

• greater consensus basis

• slow performance

• hardly controlled permissioning

• harder to meet compliance

rules (no CSDs)

• public code, easier hacker

attacks

Ⓒ2014 ATS

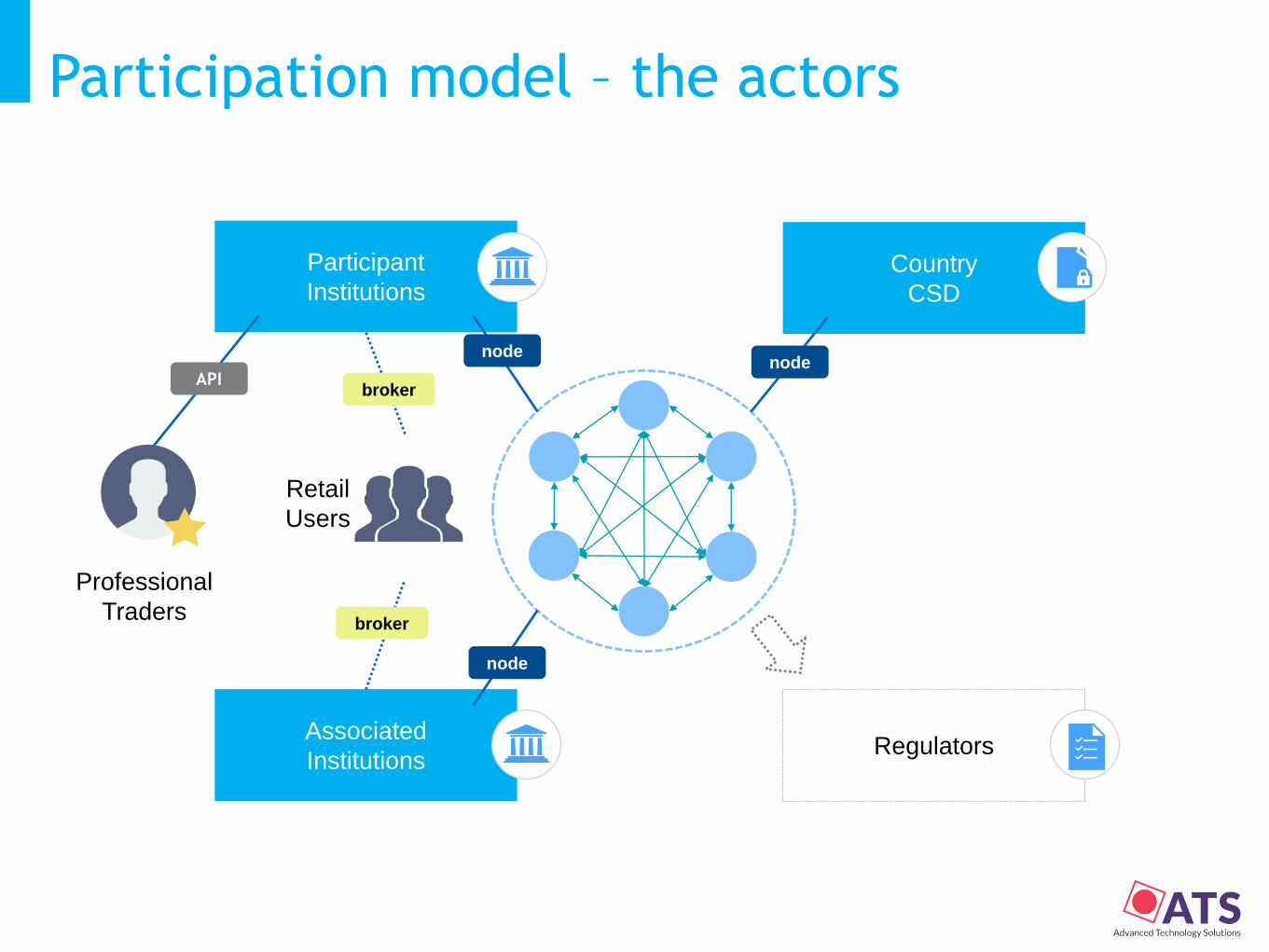

Today

Our Model – who does what• are the user participants of

the platform

• do trading transactions

• do collateral allocationtransactions

• manage updating of balances on real-world bankaccounts

Financial Institutions

Bank Accounts

• are the owner participantsof the platform

• are responsible for normative compliance

• read security ownershipexchanges

• manage updating of theirsecurity accounts

CSD(s)

Security Accounts

• Interested in information from the ledger

• In practice, may receive red information from participants

• ideally, can be participantswith read-only access to the ledger

Regulator

• implement the market engine

• business logic of CSDs, ‘atomically’ to tradingtransactions

• business logic of CCPs, ‘atomically’ to collateralallocation transactions

Smart Contracts

Participation model – the actors

Associated

Institutions

Participant

InstitutionsCountry

CSD

Regulators

Professional

Traders

APIbroker

broker

node

node

node

Retail

Users

Participation model – the actors

Associated

Institutions

Participant

InstitutionsCountry

CSD

Regulators

Professional

Traders

• Trader pays transaction

fees

• Participant forwards part of

the fee to the platform

Retail

Users

• Associated pays own

transaction fees to the

Platform

• CSD receives part of

transaction fees collected

by the Platform

• Participant pays

transaction fees (own or

Trader’s) to the Platform

• Platform forwards part of

collected transaction fees

to each Participant

Ⓒ2014 ATS

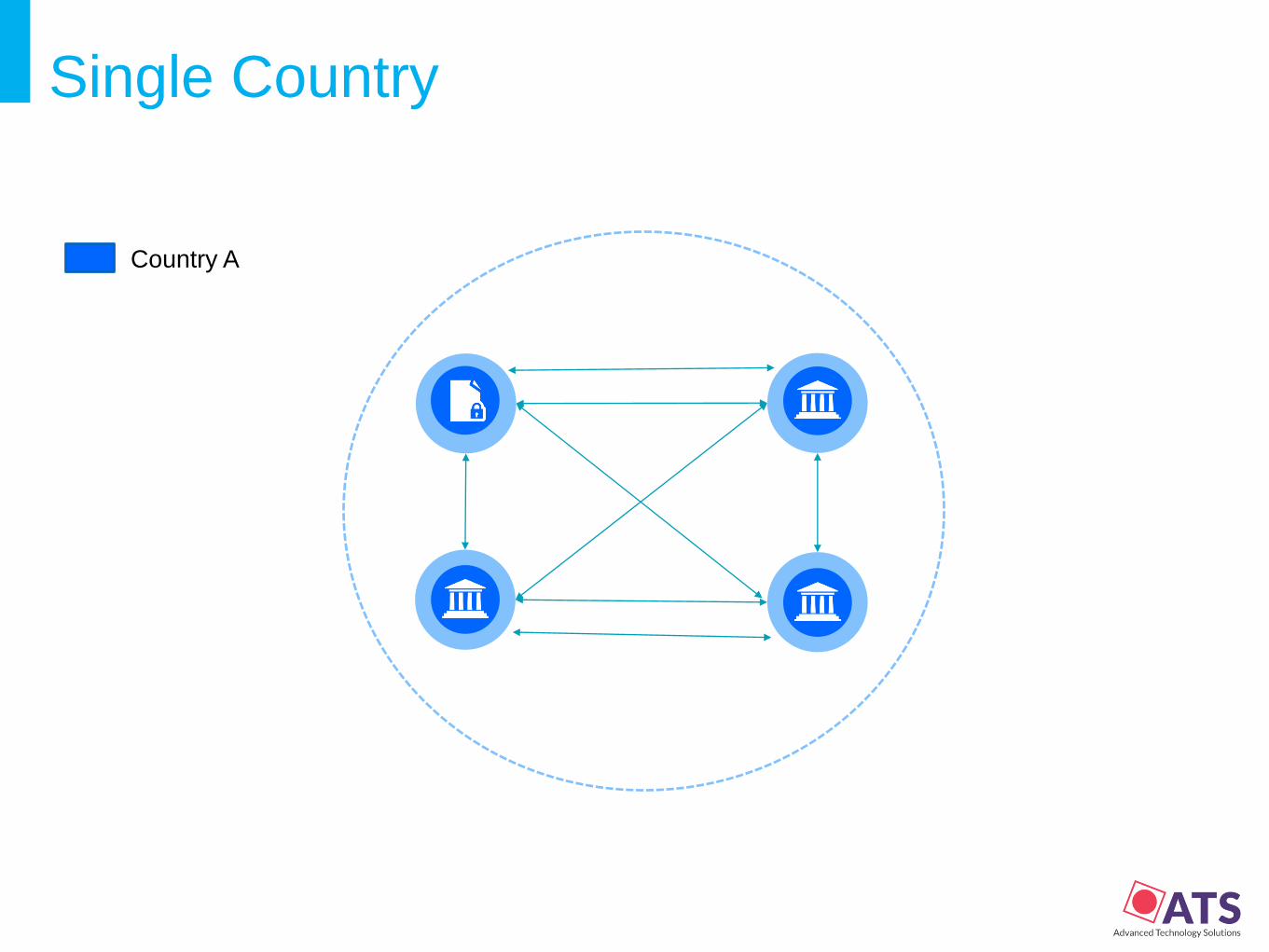

Tomorrow

Single Country

Country A

Multi Country

Country A

Country B

Multi Currency

Country A

Country B

Country C

Currency 1

Currency 2

Ⓒ2014 ATS

Road map

Road map

• Developed

• Performance-tested (>100 transactions/s on 10 nodes)

MARKET ENGINE

• Will be released on October 1st 2016

WHITE PAPER

• Will be released on November 1st 2016

• Using Intelledger®, part of Hyperledger project of Linux Foudation

FULL IMPLEMENTATION

• Currently building network

• Involving Banks, Brokers, Institutions

PARTICIPANT INSTITUTIONS