Embed Size (px)

Citation preview

Presentation to the SMA Annual Board of Directors Meeting

February 15, 2007

Ocean Reef Club, Key Largo, FL

“Mini’s in a Maxi World”

www.first-river.com2

3 Parts

Size Industry Structure Growth

www.first-river.com3

…couldn’t respond to the SMALL opportunity

The GAP

It used to be the BIG company…

entrepre

ne

urial

www.first-river.com4

But maybe big is not so bad now

Big organization skills Larger organization good at

– Hiring & developing people– Sharing best practice between

mills– Multi-location customers– One-stop shop products &

services– etc

Economies of scale in:– Manufacturing, maintenance– Purchasing – Financing– Sales & Distribution– R&D

Industry Environment Healthy demand & global growth

– Cost curves relatively flat Resources are critical

– People, materials, equipment Lots of corporate opportunities

– Acquisitions, Joint ventures– International scope– Integration up & downstream

Technical issues to the fore Complex financial matters

– Currencies, futures, indices

www.first-river.com5

And big may not hurt performanceData from 118 global public steel companies

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75

Revs $Bn (LTM)

% E

BIT

DA

(L

TM

)

Source: CapIQ, First River

www.first-river.com6

Is SMALL now a limitation in responding…

The GAP?…to BIG opportunities?

Organiza

tio

nal?

www.first-river.com7

ArcelorMittal radically changed the scale

0

20

40

60

80

100

120

140

Cru

de

Ste

el P

rod

uct

ion

(M

illio

n T

on

ne

s)

Source: IISI, First River

China36%

ArcelorMittal10%

Everybody Else54%

33.7

22.5

www.first-river.com8

How do you manage a company this size?

320,000 employees in 60 countries Strategy focused on three axes

– Geography– Product– Value chain

~2 acquisitions a month in 2007 But organization design goals

– Lean, flat, avoid top-heavy bureaucracies, avoid functional silos– Clear ‘line of sight’ in the decision-making process– Promote/allow inventiveness, allow adaptability– Clear accountability at every level – “…and faster entrepreneurial spirit that will keep AM ahead of

competition”

www.first-river.com9

At the top the CEO + Group Management Board

Flat Long Distribution Mining

Americas

Europe

Asia/Africa/CIS/Stain-less

4

32

1

Combine with ~20 senior executives to form Management Committee

www.first-river.com10

VP Sales & Mktg

VP Operations

GM’s

$23Bn revs

Flat Carbon Americas would be #6 in the world if a separate company

www.first-river.com11

Top heavy layers are inevitable

AM US Steel Nucor SteelDynamics

GM GM GM GM

VP VP EVP VP

CEO-C

CEO-R

CEO

GMB

COO

CEO CEO

COO CEOP&L

www.first-river.com12

Large buildings need more support

>20 stories ~35% floor space for structural elements

Smaller buildings ~20%

www.first-river.com13

Increasing organizational size reflected in SG&A expenses*

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0 5 10 15 20 25 30 35

Revs $Bn

SG

&A

% o

f S

ales

Source: CapIQ, First River*Selected global public steel companies, excluding China

SG&A can add value

Industry structure

www.first-river.com15

When industry structure shifts…NAFTA* steel shipments by company size, 2004 & 2007

0

10

20

30

40

50

60

>20MT 10-20 2-10 <2

Cu

m. S

hip

me

nts

, MT

2007 2004

40% 30% 30%

41% 23% 28%

8%

2

2

12

19

3

10 41

Source: First River, company filings*US & Canada only, producers with meltshop only

www.first-river.com16

It drives product line consolidation…

3 firm share

Source: First River, company filings

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rebar Hot Roll

Top

3 S

uppl

iers

M

arke

t Sha

re (%

)

2001

2006

www.first-river.com17

Improves competitor conduct…

6,000

7,000

8,000

9,000

10,000

11,000

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

60%

65%

70%

75%

80%

85%

90%

95%

100%

FR Inv. (KT - Left Axis) Cap Util (%) - Right Axis

Source: MSCI, AISI, First River

93%98%

SSC FR inventories & capacity utilization

77%75%

www.first-river.com18

Leads to better, converging performanceA predictable function of improved industry structure?

-5%

0%

5%

10%

15%

20%

25%

30%

2003 2004 2005 2006 2007

EB

ITD

A %

AKS USS NUCOR STLD

Source: CapIQ, First River

www.first-river.com19

Some say structure can be predictedZipf’s law – frequency inversely proportional to rank

Distribution of 47K online document requests, Boston Univ. 1995

Distribution of 4M firms size in the US, 1997

Predicted line slope = -1.0

www.first-river.com20

If AM didn’t exist, you’d have to invent itWorld’s largest steel producer distribution 2000 & 2007

2007

y = -0.8312x

-2

-1

0

1

2

3

4

5

6

0 2 4 6 8

l N(Rank)

lN(T

on

nes

)

2000

y = -0.7089x

-1

-0.50

0.5

11.5

22.5

3

3.54

4.5

0 2 4 6 8

l N(Rank)

lN(T

on

ne

s)

ArcelorMittal

Source: IISI, First River

www.first-river.com21

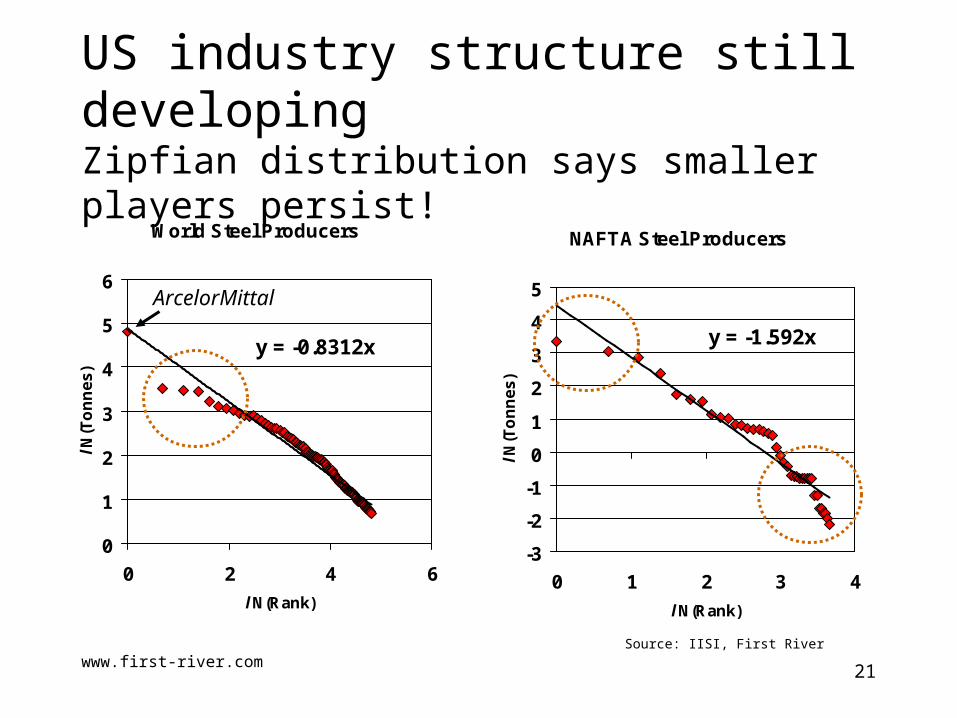

US industry structure still developingZipfian distribution says smaller players persist!

World Steel Producers

y = -0.8312x

0

1

2

3

4

5

6

0 2 4 6

l N(Rank)

lN(T

on

ne

s)

NAFTA Steel Producers

y = -1.592x

-3

-2

-1

0

1

2

3

4

5

0 1 2 3 4

l N(Rank)

lN(T

on

ne

s)

ArcelorMittal

Source: IISI, First River

Growth

www.first-river.com23

0%

5%

10%

15%

20%

25%

30%

0 5 10 15 20 25 30 35 40

Small has greater range of performance Tons liquid steel production v. EBITDA %*

*60 global steel companiesSource: CapIQ, IISI, First River

…reflects variety of positions,

growth strategies & resources

www.first-river.com24

0%

5%

10%

15%

20%

25%

30%

0 5 10 15 20 25 30 35 40

Growth choice to size or quality Tons liquid steel production v. EBITDA %*

*60 global steel companiesSource: CapIQ, IISI, First River

www.first-river.com25

You know how to grow against big – you’ve done it before

Not because you were ‘mini’ – but because you could manage

Let loose the energy of small groups of people Took risks on new technologies & deployed them rapidly Went where the growth was – regions, products Innovated in many areas Took more not less risk

Bring those skills to reinventing the steel corporation

www.first-river.com26

Organize for growth…

If you aspire to size Overhead is useful ‘Extra’ resources will find ways to add value in today’s industry Experiment with organizational structure

If you aspire to quality Not a hiding place from competitive realities Needs skill scaling to global market from smaller resource base And it still means growth…

www.first-river.com27

2007 Production: ~500 2007 Production: 100K

Porsche

The dangers of niche confinement

Morgan

Thank you!

Big or small less important to performance

than leadership

Mini’s in a maxi world?