Embed Size (px)

Citation preview

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 1/26

1

BM&F BOVESPA PRESENTATION

Oct 2008

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 2/26

2

Forward Looking Statements

This presentation may contain certain statements that express the management’s expectations, beliefsand assumptions about future events or results. Such statements are not historical fact, being based oncurrently available competitive, financial and economic data, and on current projections about the

industries BM&FBovespa S.A. works in.The verbs “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “plan,” “predict,” “project,” “target”and other similar verbs are intended to identify these forward-looking statements, which involve risksand uncertainties that could cause actual results to differ materially from those projected in thispresentation and do not guarantee any future of BM&FBovespa S.A. performance.

The factors that might affect performance include, but are not limited to: (i) market acceptance of BM&FBovespa SA services; (ii) volatility related to (a) the Brazilian economy and securities markets and (b)

the highly-competitive industries that BM&FBovespa S.A. operates in; (iii) changes in (a) domestic andforeign legislation and taxation and (b) government policies related to the financial and securitiesmarkets; (iv) increasing competition from new entrants to the Brazilian markets; (v) ability to keep upwith rapid changes in technological environment, including the implementation of enhanced functionalitydemanded by BM&FBovespa SA customers; (vi) ability to maintain an ongoing process for introducingcompetitive new products and services, while maintaining the competitiveness of existing ones; (vii)ability to attract new customers in domestic and foreign jurisdictions; (viii) ability to expand the offer of

BM&FBovespa S.A. products in foreign jurisdictions.All forward-looking statements in this presentation are based on information and data available as of thedate they were made, and BM&F Bovespa SA undertakes no obligation to update them in light of newinformation or future development.

This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities,nor shall there be any sale of securities where such offer or sale would be unlawful prior to registrationor qualification under the securities law. No offering shall be made except by means of a prospectus

meeting the requirements of the Brazilian Securities Commission CVM Instruction 400 of 2003, asamended.

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 3/26

3

THE NEW COMPANY

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 4/26

4

Timeline

2007 – Demutualizations and IPOs

Feb May

Oct Nov

Integration

Initiation

Talks

Bovespa

Demutualization

Aug Sep

2008 - Integration

JunAug

28th 20th

BM&F

DemutualizationBovespa´s IPO BM&F´s IPO

19th 8th

General

Meeting

20th

Chairman and

CEO

Nomination

Top Mgmt

Nomination

18th

First Tradingday of the new

ticker: BVMF3

20th 29th

Final Staff

and

Layoffs

26th 30th

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 5/26

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 6/266

Trading, Registration & Clearing Model

FX Cash Market

Open outcry

Electronic trading

OTC registration

FX Clearinghouse

Derivatives

Open outcry

Electronic trading

OTC registration

Derivatives

Clearinghouse

Stocks andCorporate Bonds

Electronic Trading

OTC Registration

CBLC

GovernmentBonds

Electronic trading

OTC registration

Securities

Clearinghouse

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 7/267

Gross Operating Revenues Breakdown

1Q082Q08

OthersBovespa9.2%

Trading andClearingBovespa52.6%

OthersBM&F1.4%

Vendors andOthers

2.8%

Trading andClearing Fees

34.0%

Trading andClearingBovespa55.7%

Trading andClearing Fees

BM&F31.5%

OthersBovespa8.3%Others

BM&F1.8%

Vendors andOthers

2.7%

R$ 437.6 MillionR$ 483.6 Million

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 8/268

Regulation in Brazil demands that all trades carried in exchangesmust be matched at the beneficial owner level

Internalization of orders is not allowed

Our clearing houses act as central counterparty agents and wehave the risk management at the investor level with mark tomarket (margin variation calls) done on daily basis

All trades must be carried through a brokerage house (clearingagent), which is responsible for their clients risk and know yourclient policies

Current regulation requires settlement, clearing and depositoryservices to be provided to third parties on a commercial basis

Regulatory Environment

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 9/269

Risk Management - Collaterals

R$ billions

Clearings Deposited Required

Derivatives 80.8 62.4

Cash Equities 32.7 17.6

FX 3.3 1.0

Fixed Income 1.6 0.3Total 118.4 81.3

Date: Sep 29th, 2008

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 10/2610

Securities Lending Activity

Cl e a r i n g a c t s a s CCP

T r a d i n g s y s t e m o f f e r s r e g i s t r a t i o n

L en d i n g i s a i n v e s t o r ' s d e c i s i o n a n d i t i s d o n e

t h r o u g h a b r o k e r a g e h o u se

Se t t l e m e n t a g e n t s a r e r e sp o n s i b l e b y t h e i r c l i e n t ss e t t l em e n t a n d co l l a t e r a l s

Fu l l d i sc l o s u r e o f t h e o p e n i n t e r e s t p o s i t i o n s b y

c om p a n y o n d a i l y b a s i s Co r p o r a t e A c t i o n s A d j u s t m e n t s

R i s k M a n a g e m e n t

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 11/2611

• Launched in December 2000

• Special listing segment of companies committed to better corporate governance

standards, beyond those already established at current Brazilian regulation

• Instituted with the goal to increase the market credibility and investors’ confidence

– Becoming shareholders in these companies

– Providing better valuation

• Decision of joining NM is voluntary and market driven

Novo Mercado

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 12/2612

Dispersion

Shareholders rights

• maintain at least a 25% free float;

• adoption of special procedures in public offerings to enhance the dispersion of

the company shares.

Transparency

• only common shares;

• tag-along rights extend to all shareholders in the event of disposal of control;

• board of director with at least five members and a minimum of 20%

independent board member;

• public tender offering in case of delisting or cancellation of the NM’s contract

• a statement of cash flows (company’s and consolidated) included in the

quarterly financial reports and annual financial statements;

• annual financial statements in an international standard – IFRS or US GAAP;

• disclose information about the company’s securities traded by the controlling

shareholders and the senior managers.

Novo Mercado Rules

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 13/2613

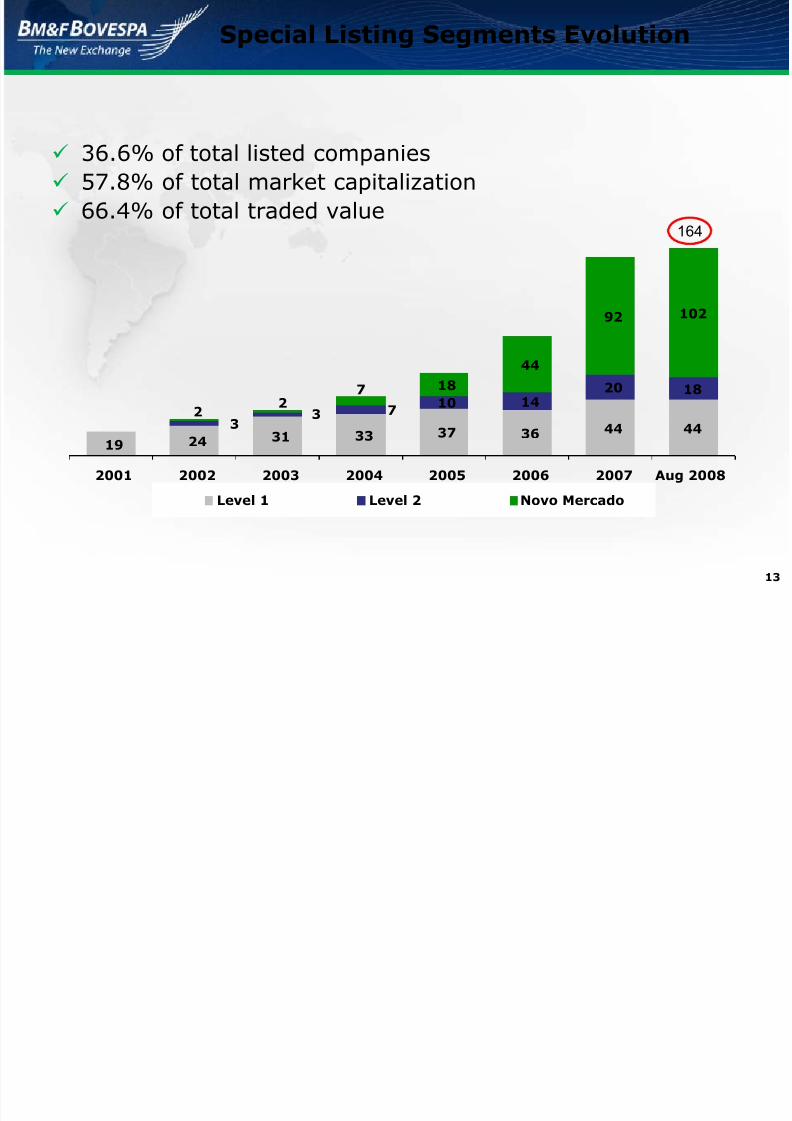

Special Listing Segments Evolution

36.6% of total listed companies

57.8% of total market capitalization

66.4% of total traded value164

19 24 31 33 37 36 44 447

10 1420

92

18

33

7

2

2

18

44

102

2001 2002 2003 2004 2005 2006 2007 Aug 2008

Level 1 Level 2 Novo Mercado

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 14/2614

Market Opportunities

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 15/2615

Number of investors – potential increase in the country andabroad (550 thousand active investors)

Number of companies – potential increase of the Brazilianand Latin America listed companies (Around 450 Braziliancompanies are listed and 7 foreign through BDRs)

Turnover ratio – low ratio compared with the otherexchanges

Derivatives – new accessing gates will broad the investorbasis

Revisiting the pricing policy

Opportunities

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 16/2616Source: World Federation of Exchange (WFE)

Exchanges Ranking

1 NYSE Group 13.6 1 NYSE Group 23.0

2 Tokyo SE 3.8 2 Nasdaq 7.4

3 Nasdaq 3.7 3 London SE 5.0

4 Euronext 3.3 4 Tokyo SE Group 3,95 London SE 3.1 5 Euronext 3.2

6 Hong Kong Exchanges 2.0 6 Shanghai SE 2.0

7 TSX Group 1.9 7 Deutsche Börse 1.9

8 Shanghai SE 1.9 8 BME Spanish Exchanges 1.8

9 Deutsche Börse 1.7 9 TSX Group 1.2

10 BME Spanish Exchanges 1.5 10 Hong Kong Exchanges 1.2

11 BM&FBovespa 1.2 11 Borsa Italiana 1.2

12 Austral ian SE 1.1 12 Swiss Exchange 1.1

13 Swiss Exchange 1.1 13 OMX Nordic Exchange 1.0

14 Bombay SE 1.1 14 Austral ian SE 1.0

15 National Stock Exchange India 1.0 15 Shenzhen SE 1.016 OMX Nordic Exchange 1.0 16 Korea Exchange 0.9

17 Borsa Italiana 0.8 17 Cyprus SE 0.9

18 Korea Exchange 0.8 18 Taiwan SE Corp. 0,7

19 JSE 0.7 19 BM&FBovespa 0.6

20 Taiwan SE Corp. 0.6 20 National Stock Exchange India 0.6

Market Cap - US$ Trillions Traded Value* - US$ Trillions

*From Jan to Aug, 2008

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 17/2617

Exchanges Ranking

Millions of contracts – from Jan to Jun 2008

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 18/2618

Turnover

BM&FBovespa´s turnover is 60%

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 19/2619

New Listings Turnover

2005

2006

Total

2004

2007

ADTV of JULY 08

R$ millions

AnnualizedTurnover (Avg.

Market Cap)

62.6%

98.0%

104.5%

67.9%

121.7

115.0

162.7

387.2

IPOs

2008 129.4%137.9

2004-2008 924.5 80.8%

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 20/2620

NovoMercado

Período de 2004 a 2007Fonte: BM&FBOVESPA.

IPO evolution

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 21/2621

2002 2003 2004 2005 2006 2007

4.9

2.4

1.2

0.80.6

1.6

2008Jan-Sep

5.9

R$ Billions

Bovespa s trading evolution

7/30/2019 Presentation - Rosenblatt - October 2008

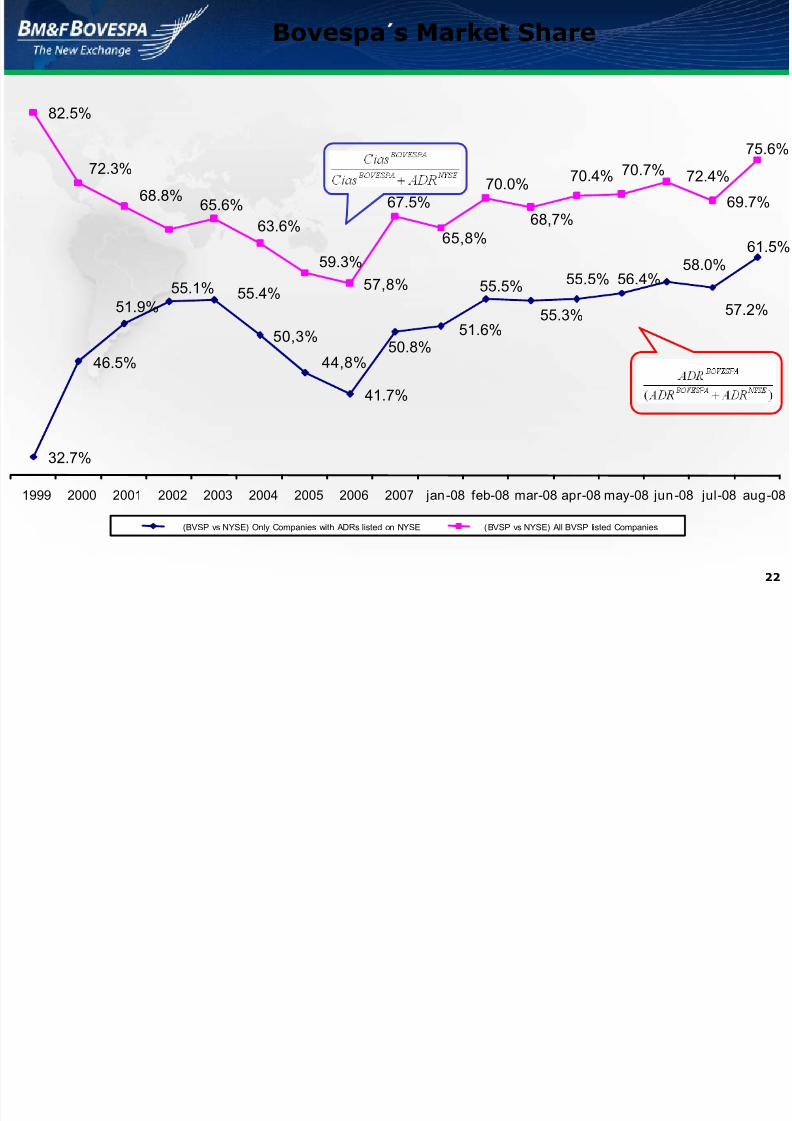

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 22/26

22

Bovespa s Market Share

32.7%

46.5%

51.9%

55.1%

50,3%

44,8%

41.7%

51.6%

55.5%

55.3%

55.5% 56.4%

61.5%

82.5%

72.3%

68.8%

59.3%

57,8%

67.5%

65,8%

70.0%

68,7%

70.4%

69.7%

75.6%

1999 2000 2001 2002 2003 2004 2005 2006 2007 jan-08 feb-08 mar-08 apr-08 may-08 jun-08 jul-08 aug-08

(BVSP vs NYSE) Only Companies with ADRs listed on NYSE (BVSP vs NYSE) All BVSP listed Companies

57.2%

58.0%

72.4%70.7%

65.6%63.6%

55.4%

50.8%

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 23/26

23

Pricing Policy

BM&F’s former Discount Policy terminated on Aug 25th

25% discount for trading and clearing fees applied to investors

that held at least 10,000 BMEF3 shares

New Pricing Policy will be implemented within 60 days

Based in traded volume

Potential pricing review in the following services

Software Licensing

Indexes Licensing

Market Data

Depository

CME O d R ti A t d

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 24/26

24

CME Order Routing Agreement andDMA Timeline

Aug

3Q08

Sep

traditional DMA

IMPLEMENTED

29th

CME Order Routingagreement

implementation(Order flow)

Globex GTS Globex GTS

4Q08

Oct Nov Dec

DMA via directconnection

Q109

2009

DMA viaa provider

FIRST PHASE

SECOND PHASETHIRD PHASE

FOURTH PHASE

(For cash markets

unti l the end of 09)

1ST HALF 09

Co-location

30th

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 25/26

25

Reconciliation of 1H08 Adjusted Results

Minority Interest (607)(607)

Reported

Income Before Taxes

Operating Result

A d j u s t e d N e t M a r g i n b y Go o d w i l l

Adjusted Net Income by Goodwill

Income Tax and Social Contribution

Non-Operating Income

Financial Income, netGoodwill Amortization

EB I T D A M a r g i n

EBITDA

O p e r a t i n g M a r g i n

Operating Expenses

Net Revenues

5 7 . 6%3 9 . 8%

547,649457,244

563,349472,944

6 8 . 1%5 7 . 2%

476.584-

(236,336)(212,174)

10,84210,842

155,036155,036(81,105)

(279,250)(369,655)

826,899826,899

R$ Thousands

55.3% 66.2%

(81,105)

542,017 632,422

Non

RecurringAdjusted

N e t M a r g i n

Net Income

4 7 . 8%3 9 . 8%

395,479329,236 66,243

90,405

66,243

(24,162)

90,405

90,405

90,405

90,405

90,405

90,405

(24,162)

66,243

147,348

7/30/2019 Presentation - Rosenblatt - October 2008

http://slidepdf.com/reader/full/presentation-rosenblatt-october-2008 26/26

BM&F Bovespa Investor RelationsSite: www.bmfbovespa.com.br

Phone numbers: 55 11 3233 2490/ 2847

E-mail: [email protected]