Embed Size (px)

Citation preview

Research Deutsche Bank Jan Schildbach

16 June 2016

Research Deutsche Bank

Non-performing loans in Europe and the US – impact on banks & customers

Brussels, 16 June 2016

Jan Schildbach

Research Deutsche Bank Jan Schildbach

16 June 2016

Agenda

2

1

NPL impact on banks & customers

Macro picture

2

Research Deutsche Bank Jan Schildbach

16 June 2016

High – and often rising – private-sector debt levels in Europe

3

0

20

40

60

80

100

FR DE UK US Euro area

IT ES PT GR IE SE

2005 Q3 2015

Credit to households% of GDP

Source: BIS

0

40

80

120

160

200

FR DE UK US Euro area

IT ES PT GR IE SE

2005 Q3 2015

Credit to non-financial corporations% of GDP

Source: BIS

Research Deutsche Bank Jan Schildbach

16 June 2016

... partly a result of deep crisis (not yet overcome by some countries) – leading to strong policy response

4

75

80

85

90

95

100

105

110

115

Q1 2007

Q1 2008

Q1 2009

Q1 2010

Q1 2011

Q1 2012

Q1 2013

Q1 2014

Q1 2015

Q1 2016

EU-28 EMU-19 DE FRUK IT ES GRPT SE US

2010 = 100

Source: Eurostat

Real GDP

0

1

2

3

4

5

6

7

1999 01 03 05 07 09 11 13 15

US Euroland UK

%Main official interest rates

Sources: Federal Reserve, ECB, BoE

Research Deutsche Bank Jan Schildbach

16 June 2016 5

Bank lending rates: Record lows abound

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

11 12 13 14 15 16

Loans to non-financial corporations, EUR ≤ 1 m

Loans to non-financial corporations, EUR > 1 m

Loans to self-employed & non-corporate businesses

Corporate lending rates in theeuro area, by loan size%, new business

Source: ECB

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

11 12 13 14 15 16

≤ 1 year 1-5 years > 5 years

... by rate fixation period%, loans to non-financial corporations

Source: ECB

Research Deutsche Bank Jan Schildbach

16 June 2016

— Between 2012 and 2015, — bank loan outflows of EUR 302 bn in

the EMU — compensated by inflows of

EUR 323 bn from bond issuance

— Narrow investor base limits further growth potential

— Capital Markets Union a good opportunity to 1. allow for a more active involvement of

pension funds in bond markets 2. reduce the mechanistic reliance on

ratings 3. iron out duplications and overlaps in

disclosure regimes

Nevertheless, corporate borrowing has partly shifted to capital markets – but will it continue?

6

-200

0

200

400

600

0

40

80

120

160

06 07 08 09 10 11 12 13 14 15

Bond issuance (left) Bank loans (right)

EUR bn, Net bond issuance (left), EUR bn, Bank loan flows (right)

Sources: ECB, Deutsche Bank Research

Euro area: Non-financial firms' funding shifts from loans to bonds

Research Deutsche Bank Jan Schildbach

16 June 2016

Agenda

2

1

NPL impact on banks & customers

Macro picture

7

Research Deutsche Bank Jan Schildbach

16 June 2016

Low rates have prevented a surge in delinquencies

8

32.9 32.1 30.1 28.7 26.1 24.0 23.2

53.5 51.1 49.5 59.6 61.0 60.5 61.4

25.2 21.6 22.221.3 18.9 17.7 16.0

19.5 22.0 24.930.0 33.1 31.2 29.5

18.1 17.7 17.419.0 21.1 18.2 15.9

12.3 12.9 12.913.1 12.1

11.5 11.5

21.9 21.3 20.020.0 20.4

19.0 17.5

0

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012 2013 2014 2015

Germany France UK EMU peripherals Benelux Austria/Switzerland Nordics

Corporate insolvencies in Europe

Source: Creditreform

in '000

Research Deutsche Bank Jan Schildbach

16 June 2016 9

... which in turn helped stabilise/improve credit quality at banks

0

4

8

12

16

20

24

28

32

36

40

0

2

4

6

8

10

12

14

16

18

20

Q4 09 Q4 10 Q4 11 Q4 12 Q4 13 Q4 14 Q4 15

France* Germany*UK* USItaly* SpainPortugal Greece (right)Ireland (right)

Non-performing loans as % of total loansNPLs in selected countries

* No data available for Q1 and Q3, data for Germany only available for Q4.

Sources: IMF, Banco de España, Banco de Portugal,Deutsche Bank Research

0

50

100

150

200

250

300

350

400

Q4 2010

Q4 2011

Q4 2012

Q4 2013

Q4 2014

Q4 2015

France Germany UKUS Italy SpainPortugal Greece Ireland

Total NPLs

Sources: IMF, Banco de España, Deutsche Bank Research

in billions of national currency

Research Deutsche Bank Jan Schildbach

16 June 2016

Provisioning for loan losses remained a drain though, until recently – faster cleanup & recovery in the US

10

0

10

20

30

40

50

60

70

80

06 07 08 09 10 11 12 13 14 15

US banks Large European banks

Loan loss provisionsUSD / EUR bn, up to Q4 15

Sources: FDIC, company reports, Deutsche Bank Research

0.0

2.5

5.0

7.5

10.0

12.5

15.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1 05

Q1 06

Q1 07

Q1 08

Q1 09

Q1 10

Q1 11

Q1 12

Q1 13

Q1 14

Q1 15

Residential mortgages C&ICRE AutoConstruction (right) Credit card (right)

Loan performance in the US:net charge-offs% of outstanding volumes

Source: FDIC

Research Deutsche Bank Jan Schildbach

16 June 2016

Low rates have failed to support/hurt European banks in other areas

11

105

110

115

120

125

130

135

140

H1 09

H2 H1 10

H2 H1 11

H2 H1 12

H2 H1 13

H2 H1 14

H2 H1 15

H2

EUR bn, top 20 European banks

Sources: Company reports, Deutsche Bank Research

Net interest income

-9

-6

-3

0

3

6

9

12

08 09 10 11 12 13 14 15 16

US Euro area

Lending to the private sector% yoy, up to Mar 16

Sources: ECB, FDIC, Deutsche Bank Research

Research Deutsche Bank Jan Schildbach

16 June 2016

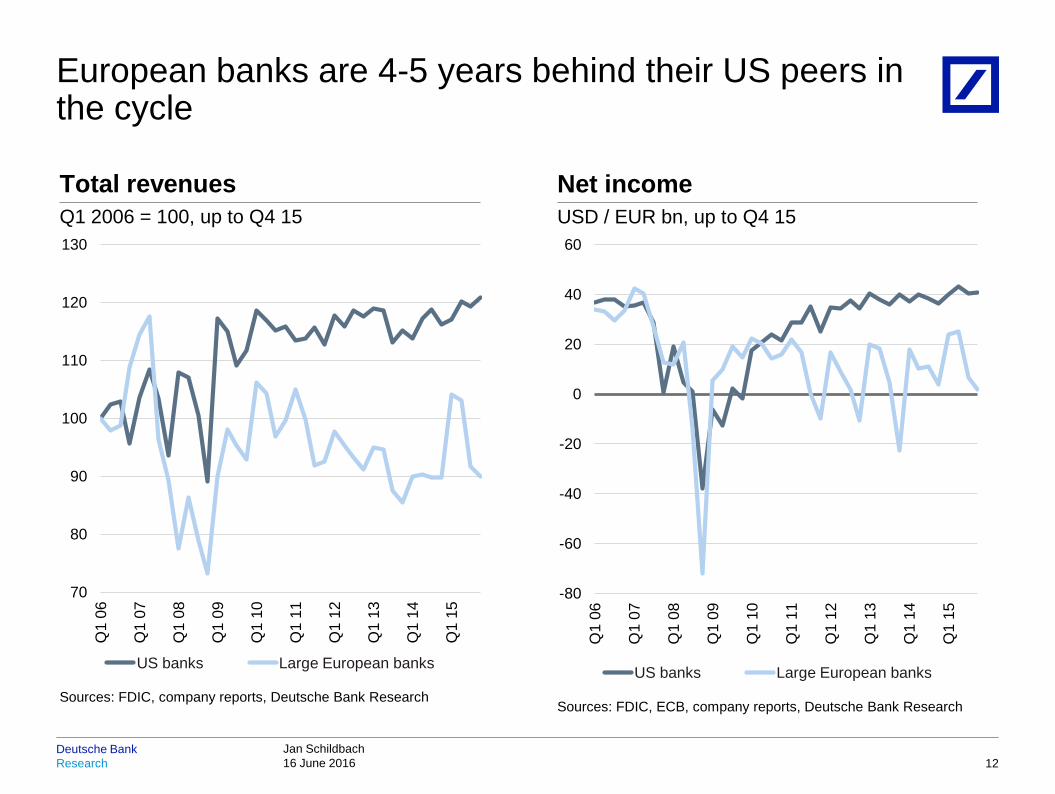

European banks are 4-5 years behind their US peers in the cycle

12

70

80

90

100

110

120

130

Q1

06

Q1

07

Q1

08

Q1

09

Q1

10

Q1

11

Q1

12

Q1

13

Q1

14

Q1

15

US banks Large European banks

Total revenues

Sources: FDIC, company reports, Deutsche Bank Research

Q1 2006 = 100, up to Q4 15

-80

-60

-40

-20

0

20

40

60

Q1

06

Q1

07

Q1

08

Q1

09

Q1

10

Q1

11

Q1

12

Q1

13

Q1

14

Q1

15

US banks Large European banks

Net income

Sources: FDIC, ECB, company reports, Deutsche Bank Research

USD / EUR bn, up to Q4 15

Research Deutsche Bank Jan Schildbach

16 June 2016

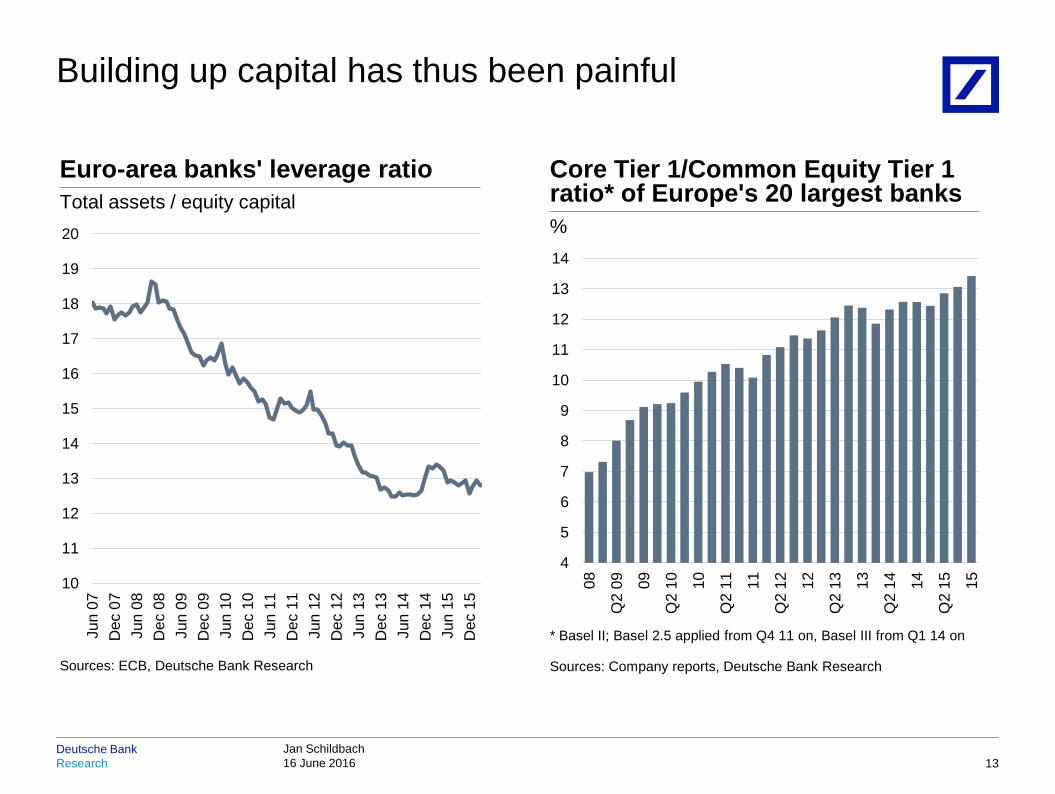

Building up capital has thus been painful

13

4

5

6

7

8

9

10

11

12

13

14

08

Q2

09 09

Q2

10 10

Q2

11 11

Q2

12 12

Q2

13 13

Q2

14 14

Q2

15 15

%

Core Tier 1/Common Equity Tier 1ratio* of Europe's 20 largest banks

* Basel II; Basel 2.5 applied from Q4 11 on, Basel III from Q1 14 on

Sources: Company reports, Deutsche Bank Research

10

11

12

13

14

15

16

17

18

19

20

Jun

07D

ec 0

7Ju

n 08

Dec

08

Jun

09D

ec 0

9Ju

n 10

Dec

10

Jun

11D

ec 1

1Ju

n 12

Dec

12

Jun

13D

ec 1

3Ju

n 14

Dec

14

Jun

15D

ec 1

5

Total assets / equity capitalEuro-area banks' leverage ratio

Sources: ECB, Deutsche Bank Research

Research Deutsche Bank Jan Schildbach

16 June 2016

With more tightening to come: Regulatory timeline

14

Source: Deutsche Bank

Research Deutsche Bank Jan Schildbach

16 June 2016

Extraordinary macro environment: − Private-sector indebtedness has even deteriorated since the financial crisis − Deep crisis not yet overcome in Europe – US back on track, except for

monetary policy

Positive impact on borrowers: − Extremely low lending rates in Europe − Declining number of business insolvencies

Mixed impact on banks: − Benefiting from improving asset quality & shrinking non-performing loans − However, still elevated level of problem assets and loan loss provisions in

Europe − In addition, no pickup in lending and increasing interest margin pressure –

in an ever tighter regulatory environment − Contrast to US: fall in margins more than compensated for by strong growth

in credit volume

Conclusion: Low rates helped customers, but EU banks still suffering from high level of non-performing loans

15

Research Deutsche Bank Jan Schildbach

16 June 2016

Contact

Jan Schildbach

Deutsche Bank Research

Head of Banking, Financial Markets and Regulation

Taunusanlage 12

D-60325 Frankfurt/Main

Phone: +49 69 910-31717

E-mail: [email protected]

Internet: www.dbresearch.com

Research Deutsche Bank Jan Schildbach

16 June 2016

© Copyright 2016. Deutsche Bank AG, Deutsche Bank Research, 60262 Frankfurt am Main, Germany. All rights reserved. When quoting please cite “Deutsche Bank Research”. The above information does not constitute the provision of investment, legal or tax advice. Any views expressed reflect the current views of the author, which do not necessarily correspond to the opinions of Deutsche Bank AG or its affiliates. Opinions expressed may change without notice. Opinions expressed may differ from views set out in other documents, including research, published by Deutsche Bank. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. No warranty or representation is made as to the correctness, completeness and accuracy of the information given or the assessments made. In Germany this information is approved and/or communicated by Deutsche Bank AG Frankfurt, licensed to carry on banking business and to provide financial services under the supervision of the European Central Bank (ECB) and the German Federal Financial Supervisory Authority (BaFin). In the United Kingdom this information is approved and/or communicated by Deutsche Bank AG, London Branch, a member of the London Stock Exchange, authorized by UK’s Prudential Regulation Authority (PRA) and subject to limited regulation by the UK’s Financial Conduct Authority (FCA) (under number 150018) and by the PRA. This information is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. and in Singapore by Deutsche Bank AG, Singapore Branch. In Japan this information is approved and/or distributed by Deutsche Securities Limited, Tokyo Branch. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product.

Disclaimer