Embed Size (px)

Citation preview

International Income Taxation Chapter 8: TRANSFER PRICING Professors Wells

Presentation:

March 30, 2016

2

Chapter 8 – Transfer Pricing Code §482

Issues re establishing the “arm’s length” price between related parties in the following situations: 1) Loans 2) Sales of tangible personal property 3) Leases of tangible personal property 4) Licensing of intangibles 5) Providing of services

Purpose of these rules is to place a “controlled taxpayer” on tax parity with an “uncontrolled taxpayer.” In this analysis, it is assumed that all the facts are known and both related parties are knowledgeable in the industry.

3

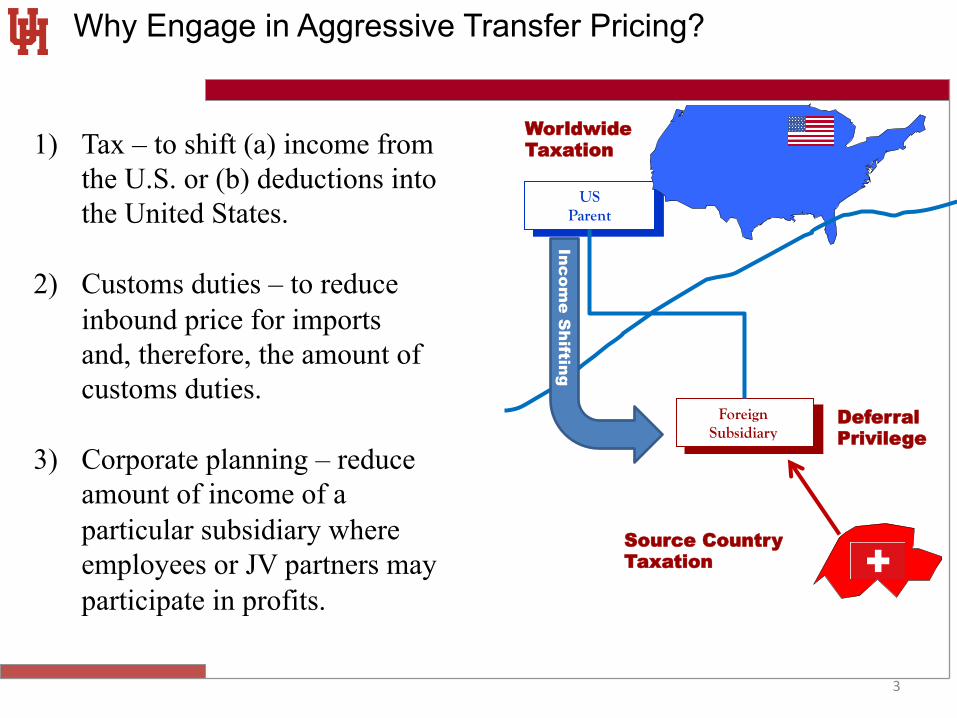

Why Engage in Aggressive Transfer Pricing?

1) Tax – to shift (a) income from the U.S. or (b) deductions into the United States.

2) Customs duties – to reduce inbound price for imports and, therefore, the amount of customs duties.

3) Corporate planning – reduce amount of income of a particular subsidiary where employees or JV partners may participate in profits.

US Parent

Foreign Subsidiary

Worldwide Taxation

Deferral Privilege

Source Country Taxation

Income S

hifting

4

Code §482 Essentials – Arm’s Length Pricing

1) Commonly controlled entities.

2) Apportionment of gross income, deductions, etc. between parties.

3) To “prevent evasion of taxes or clearly to reflect the income . . .”

A tax accounting provision – to facilitate the determination of the true taxable income of a taxpayer.

US Parent

Foreign Subsidiary

Worldwide Taxation

Deferral Privilege

Source Country Taxation

Income S

hifting

5

Challenge to the Pricing Adjustment by Taxpayer

An accounting adjustment – therefore ordinarily more deference to the Service’s position on the adjustment. Taxpayer has the burden of proving that any IRS adjustment is “arbitrary, capricious or unreasonable”. Requirement for correlative allocations and deductions for related parties (if possible).

US Parent

Foreign Subsidiary

Worldwide Taxation

Deferral Privilege

Source Country Taxation

Income S

hifting

6

Defining “Control” for Code §482 Purposes p. 715

No specific ownership attribution rules. What about a 50-50 joint venture, particularly where parallelism of interest exists between the two joint venturers?

Example: a joint purchasing arrangement for raw materials.

Standard: “Control” means “any kind of control, direct or indirect, whether legally enforceable, and however exercised.”

1. Reality rather than formal control is the critical inquiry. A presumption of control exists if income is artificially shifted.

2. Control exists if two or more unrelated taxpayers act in concern for a common goal.

X Y

JV, Inc.

50% 50%

7

Secondary Consequences of Adjustment Under §482

Rev. Rul. 78-83, p. 716 Triangular dividend treatment. Excessive amount transferred is treated as: 1) Dividend distribution (§301) upstream to

the common parent corporation; this assumes “earnings and profits” and

2) Capital contribution downstream to the other entity (including foreign). §351.

P

X Y

Div

iden

d

Contribution

P

X

Y Div

iden

d

Contribution

P

X

Y

Div

iden

d

Variations on Rev. Rul. 78-83

Excess Value

I.L.M. 201349015 (Sept. 16, 2013) (can you guess the FTC issue???)

8

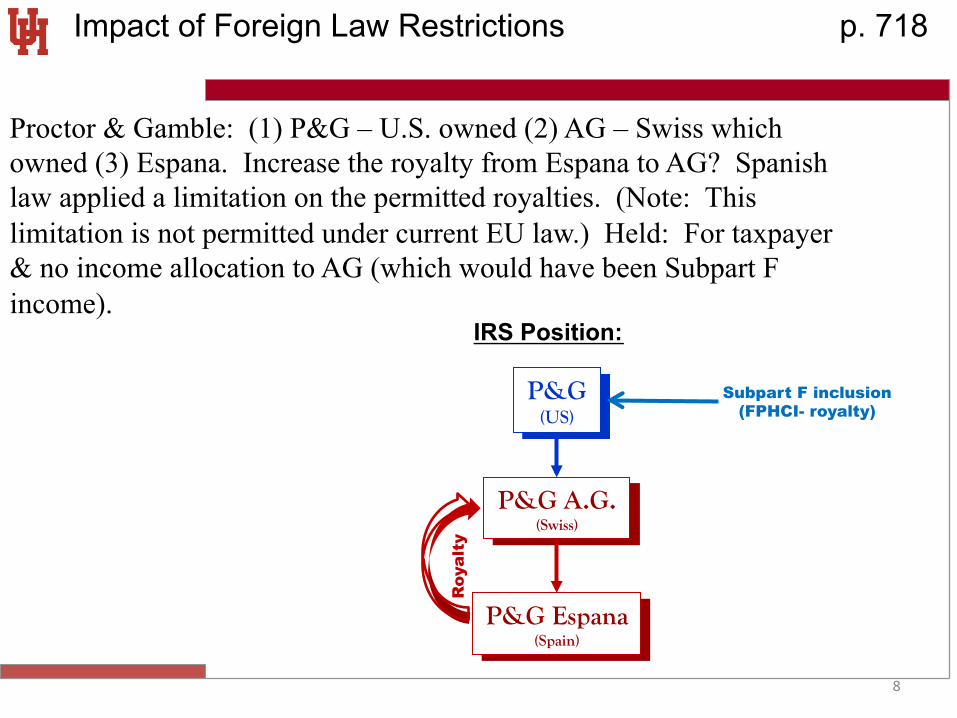

Impact of Foreign Law Restrictions p. 718

Proctor & Gamble: (1) P&G – U.S. owned (2) AG – Swiss which owned (3) Espana. Increase the royalty from Espana to AG? Spanish law applied a limitation on the permitted royalties. (Note: This limitation is not permitted under current EU law.) Held: For taxpayer & no income allocation to AG (which would have been Subpart F income).

P&G (US)

P&G A.G. (Swiss)

P&G Espana (Spain)

Roy

alty

IRS Position:

Subpart F inclusion (FPHCI- royalty)

9

Regs. Concerning Foreign Law Restrictions p.719

1) Must be publicly promulgated and generally applied.

2) Taxpayer must exhaust all available local country remedies in seeking a waiver of these rules.

3) The restrictions must prevent receipt.

4) Related parties must not have engaged in arrangements to circumvent the restrictions.

5) Taxpayers must elect to apply this regulation and identify affected transactions on its tax return.

Reg. §1.482-1(h)(2).

10

Mechanisms to Reduce Double Economic Taxation p. 720

1) Correlative adjustments – if all entities are subject to U.S. income taxation.

2) Competent Authority mechanism to challenge the adjustment where cross-border situations.

See 2006 U.S. Model Income Tax Treaty, Article 25.

X Y

P

$100x (overpriced by $5x)

$100x Sales Price $ 60x COGS $ 40x Reported profit

$100x Sales Price $100x Purchase Price $ 0x Reported profit

$100x Customer

Example: What is the transfer pricing adjustment and correlative adjustments?

11

Concepts of Arm’s Length Pricing Under Code §482 p. 722

“Best method” rule. Reg. §1.482-1(c)(1). Since a range of economic results can occur parties must examine these factors to determine the comparability of uncontrolled transactions to that of the “controlled transaction” that is being tested: 1. Functions. 2. Contractual terms between the parties. 3. Economic risks. 4. Economic conditions. 5. The nature of the property or services.

See Treas. Reg. §1.482-1(d).

12

Interest on Debt Between Related Parties p. 724

Use a safe haven rate based on the “applicable federal rate” – if not in the “business” of making loans. Range of not less than 100% of the AFR nor more than 130% of the AFR. See Treas. Reg. §1.482-2(a)(2) (revised 2009).

13

Rental of Tangible Property p. 724

Establish an arm’s length rental amount based on: 1) The period and the location of use.

2) The owner’s investment in the property.

3) Expenses of maintaining the property.

4) The type of property involved. Reg. §1.482-2(c).

14

Providing Services to a Related Party p. 724

Code §482 – determine that amount which would be charged for similar services in independent transactions between unrelated parties under similar circumstances. Treas. Reg. §1.482-2(b) & Treas. Reg. §1.482-9.

15

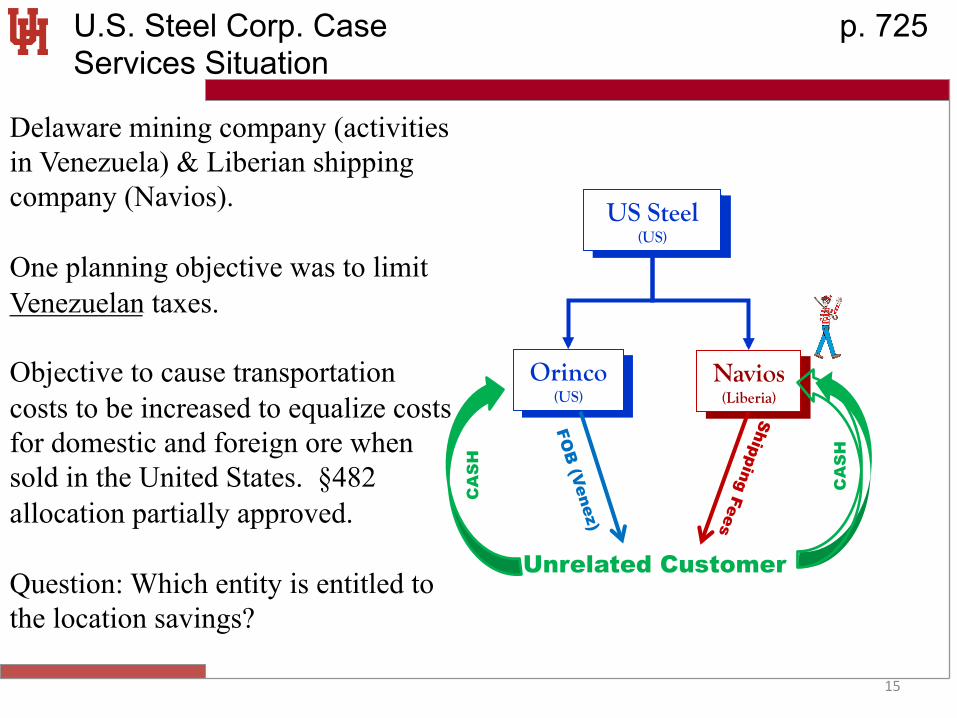

U.S. Steel Corp. Case p. 725 Services Situation

Delaware mining company (activities in Venezuela) & Liberian shipping company (Navios). One planning objective was to limit Venezuelan taxes. Objective to cause transportation costs to be increased to equalize costs for domestic and foreign ore when sold in the United States. §482 allocation partially approved. Question: Which entity is entitled to the location savings?

US Steel (US)

Orinco (US)

Navios (Liberia)

Unrelated Customer

FOB

(Venez)

CA

SH

CA

SH

16

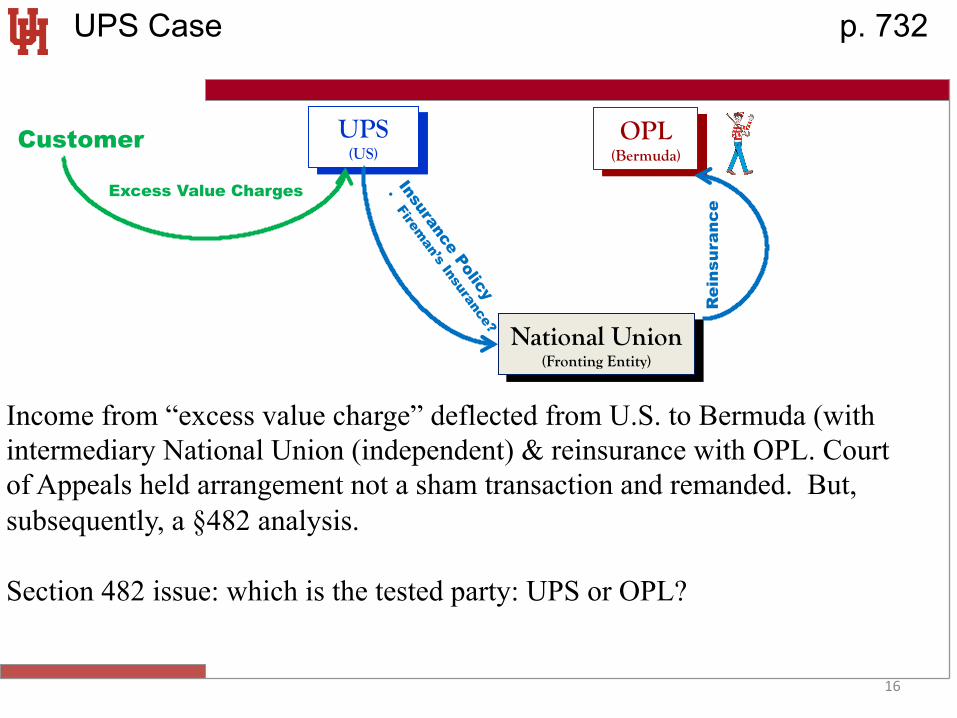

UPS Case p. 732

Income from “excess value charge” deflected from U.S. to Bermuda (with intermediary National Union (independent) & reinsurance with OPL. Court of Appeals held arrangement not a sham transaction and remanded. But, subsequently, a §482 analysis. Section 482 issue: which is the tested party: UPS or OPL?

UPS (US)

OPL (Bermuda)

Customer

Excess Value Charges

National Union (Fronting Entity)

Rei

nsur

ance

17

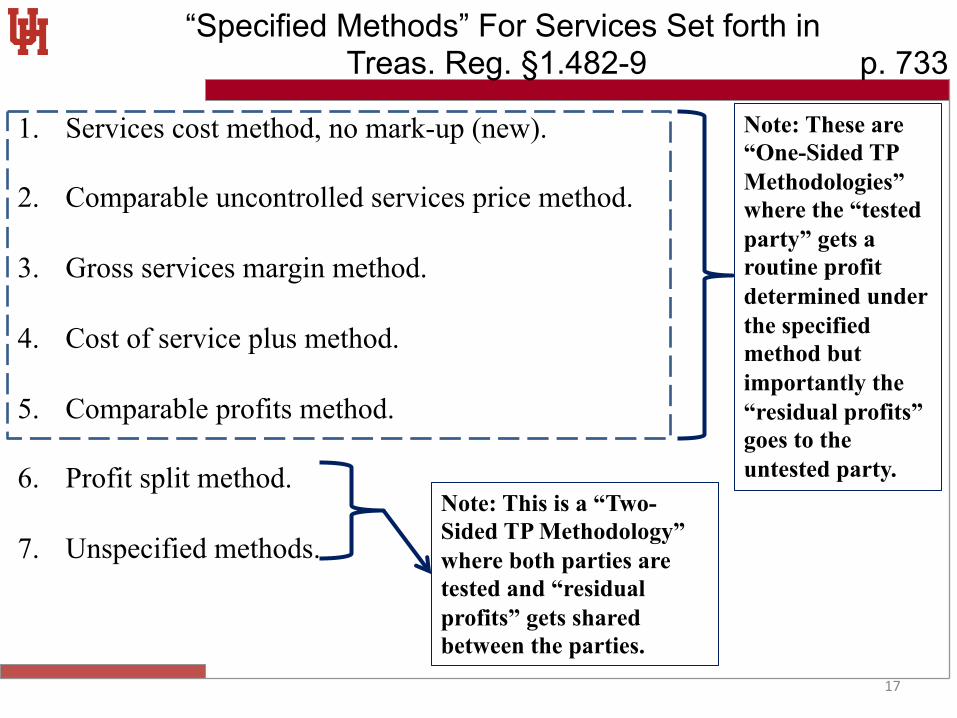

“Specified Methods” For Services Set forth in Treas. Reg. §1.482-9 p. 733

1. Services cost method, no mark-up (new).

2. Comparable uncontrolled services price method.

3. Gross services margin method.

4. Cost of service plus method.

5. Comparable profits method.

6. Profit split method.

7. Unspecified methods.

Note: These are “One-Sided TP Methodologies” where the “tested party” gets a routine profit determined under the specified method but importantly the “residual profits” goes to the untested party.

Note: This is a “Two-Sided TP Methodology” where both parties are tested and “residual profits” gets shared between the parties.

18

Supervisory / Stewardship Expense p. 734

Cf., the cost for management services provided for the benefit of the related/parent corporation. Young & Rubicam case – p. 734 No §482 allocation required, since for the benefit of the parent corporation. Compare Treas. Reg. §1.482-9(l)(3) with Treas. Reg. §1.861-8(e)(4)

19

Rev. Rul. 87-71 p. 736 Compare in Same Market

Foreign sub sells product to (i) Parent corporation and (ii) unrelated purchasers. 1) Sub can sell product to

unrelated purchasers at a higher price because of market conditions in one jurisdiction as contrasted with another jurisdiction.

2) Higher price to parent corporation than to unrelated purchasers in the same jurisdiction - not an arm’s length price.

P (US)

S

B Market Customer X+Y

A Market Customer

A Market Customer

Price?

20

Bausch & Lomb Irish Mfg. Sub. p. 738

Irish sub was organized to manufacture and sell contact lenses. Product sold to Parent for $7.50 but the manufacturing cost was only $1.50. Sub also paid royalty to Parent of 5 percent to use the spin cast manufacturing process developed by the parent. Held: OK to use Irish subsidiary and $7.50 was an acceptable market price. But, the court then looked at royalty rates and engaged in a profit split approach.

B&L (US)

B&L (Various)

B&L (Ireland) $7.50

CUPS • Lombart • American Hydron • American Optical • Hydrocurve

$1.50 cost

21

Current Pricing Rules for Tangible Personal Property p. 746

“Best method” rule (Reg. §1.482-1(c) and -8) Reg. §1.482-3 choices: 1) Comparable uncontrolled price method;

2) Resale price method;

3) Cost plus method;

4) Comparable profits method (or CPM); based on profit level indicators;

5) Profit split method.

Note: These are “One-Sided TP Methodologies where the “tested party” gets a routine profit determined under the specified method but importantly the “residual profits” goes to the untested party.

Note: This is a “Two-Sided TP Methodology where both parties are tested and “residual profits” gets shared between the parties.

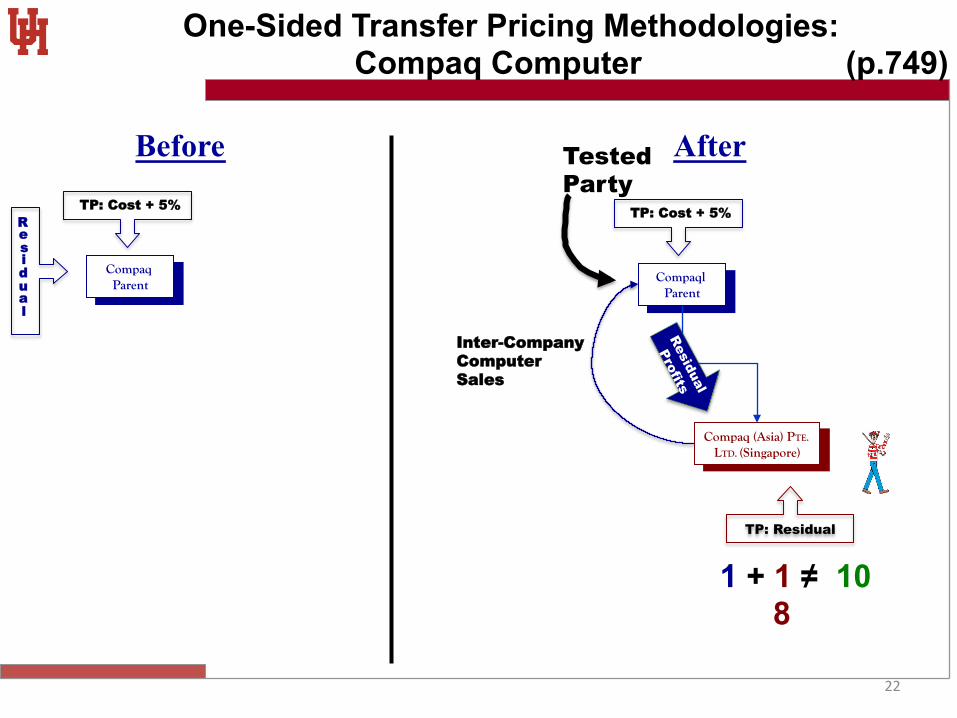

22

Compaql Parent

Compaq (Asia) PTE. LTD. (Singapore)

After

One-Sided Transfer Pricing Methodologies: Compaq Computer (p.749)

TP: Residual

Compaq Parent

Before

R e s i d u a l

TP: Cost + 5% TP: Cost + 5%

1 + 1 ≠ 10 8

Tested Party

Inter-Company Computer Sales

23

Speakerhouse Problem p. 749

Basic tax planning issue: What is the best pricing method when taxpayer wants the lowest possible price that can withstand examination by the IRS? 1) Comparable uncontrolled price ($150 if US Distributor sales are comparable) 2) Resale price method ($150 gives Swisterco a 25% GPM- the same GPM as on its

RT3000 sales) 3) Cost Plus ($150 sales price less $120 cost gives 25% GPM to Speakerhouse- the same

GPM as it earns on its S24 sales to US distributors) 4) Comparable profits (we don’t have profitability information for Soundsgood) 5) Profit split (50:50 profit split gives $155 price, but split is unclear)

Speakerhouse (US)

Swisterco (Switzerland)

S24 @ $150 US Distributors

Price?

S24 @ $200 US Customers

• RT3000 Net Profit $75 • $10 Extra Cost for Packaging S24 & Advertising S24

S24 @ $200 European Distributors

24

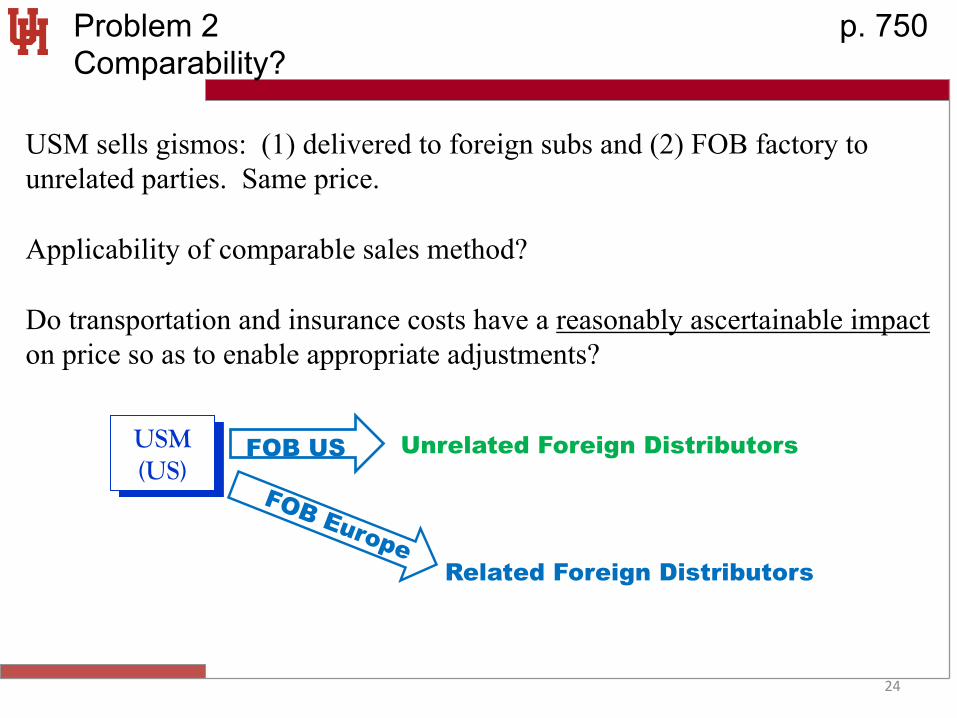

Problem 2 p. 750 Comparability?

USM sells gismos: (1) delivered to foreign subs and (2) FOB factory to unrelated parties. Same price. Applicability of comparable sales method? Do transportation and insurance costs have a reasonably ascertainable impact on price so as to enable appropriate adjustments?

USM (US)

Unrelated Foreign Distributors FOB US

Related Foreign Distributors

25

Problem 3 p. 750 Impact of Trademark?

USM sells gismos: Trademark on gismos sold to subsidiaries but not when sold to unrelated distributors. Is the effect on price of the trademark probably material and, therefore, not reasonably estimated? Therefore, the CUP method is probably not reliable here.

USM (US)

Unrelated Foreign Distributors FOB US

Related Foreign Distributors

26

Problem 4 p. 750 Different Area Markets

USM sells gismos: Subsidiaries sold to European customers but unrelated distributors sold in Asia. If geographic differences have definitive and reasonably ascertainable effects for which adjustments can be made the CUP method may be acceptable.

USM (US)

Unrelated Asian Distributors FOB US

Related European Distributors

27

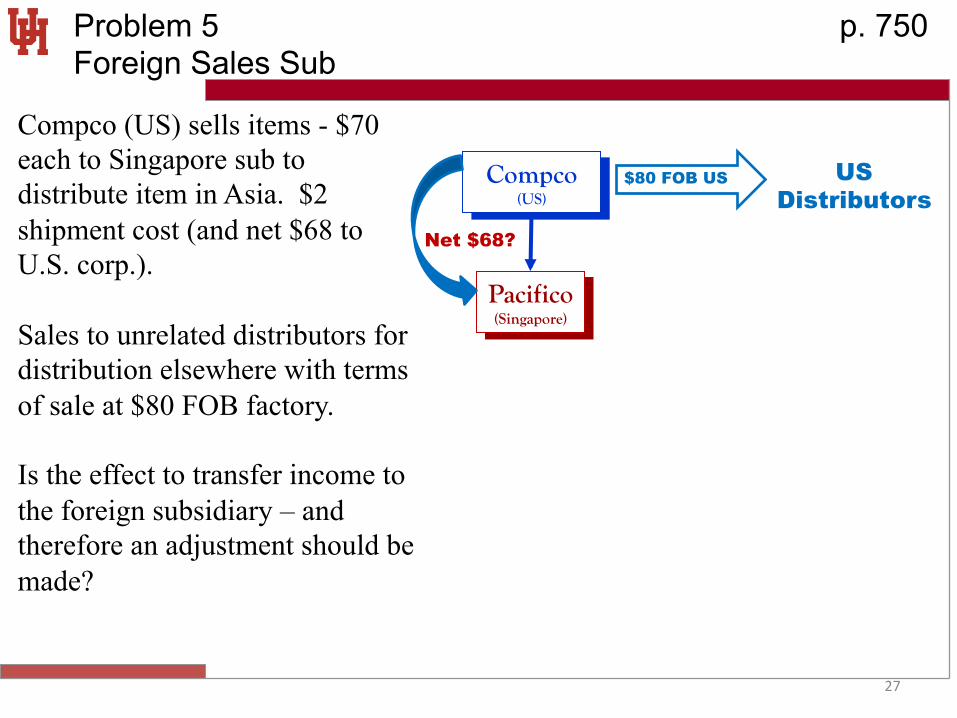

Problem 5 p. 750 Foreign Sales Sub

Compco (US) sells items - $70 each to Singapore sub to distribute item in Asia. $2 shipment cost (and net $68 to U.S. corp.). Sales to unrelated distributors for distribution elsewhere with terms of sale at $80 FOB factory. Is the effect to transfer income to the foreign subsidiary – and therefore an adjustment should be made?

Compco (US)

Pacifico (Singapore)

$80 FOB US US Distributors

Net $68?

28

Problem 6 p. 750 Foreign Sub Pays Too Much?

U.S. corp. sells items for $70 each to Singapore sub to distribute item in Asia. $2 shipment cost (and net $68). Sales to unrelated distributors for distribution elsewhere with terms of sale at $60 FOB factory. Taxpayers cannot invoke §482 to make an adjustment. File an amended income tax return based on different prices?

Compco (US)

Pacifico (Singapore)

$60 FOB US US Distributors

Net $68?

29

Problem 7 p. 683 Foreign Sub Adds Its Own Trademark to Products

Comco affixes its valuable trademark on the products sold to Pacifico but none of its US distributor sales have a trademark. Issue: What is the result now?

Compco (US)

Pacifico (Singapore)

$80 FOB US US Distributors

Price?

30

Intangible Property Transfers p. 751

Definition: Patents, copyrights, trademarks, confidential know-how, trade secrets. Transfer accomplished either by sale or licensing. Licensing can be either co-extensive with the life of the property or for a shorter period.

31

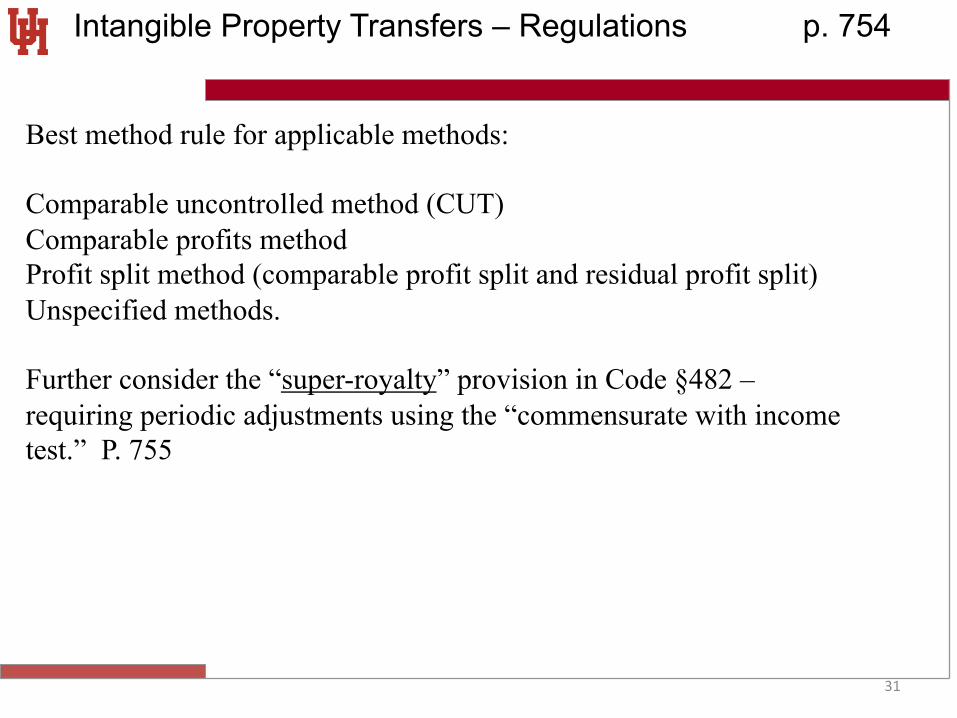

Intangible Property Transfers – Regulations p. 754

Best method rule for applicable methods: Comparable uncontrolled method (CUT) Comparable profits method Profit split method (comparable profit split and residual profit split) Unspecified methods. Further consider the “super-royalty” provision in Code §482 – requiring periodic adjustments using the “commensurate with income test.” P. 755

32

Cost Sharing Arrangements p. 755

Reg. §1.482-7T Agreement to share costs and risks of research and development.

US-Owned MNE Apple

TP: Residual

Foreign-Owned MNE Nestlé

Tested Party

Parent (US)

TP: Cost + 5%

Products

Customers

Owner/Developer (Ireland)

US Domestic Subsidiary

Foreign-Owned Parent

TP: Cost + 5%

TP: Residual

No royalties paid since each participant in the cost-sharing arrangement is an “owner.” No Code §482 adjustments if the arrangement is a “qualified cost sharing arrangement.”

33

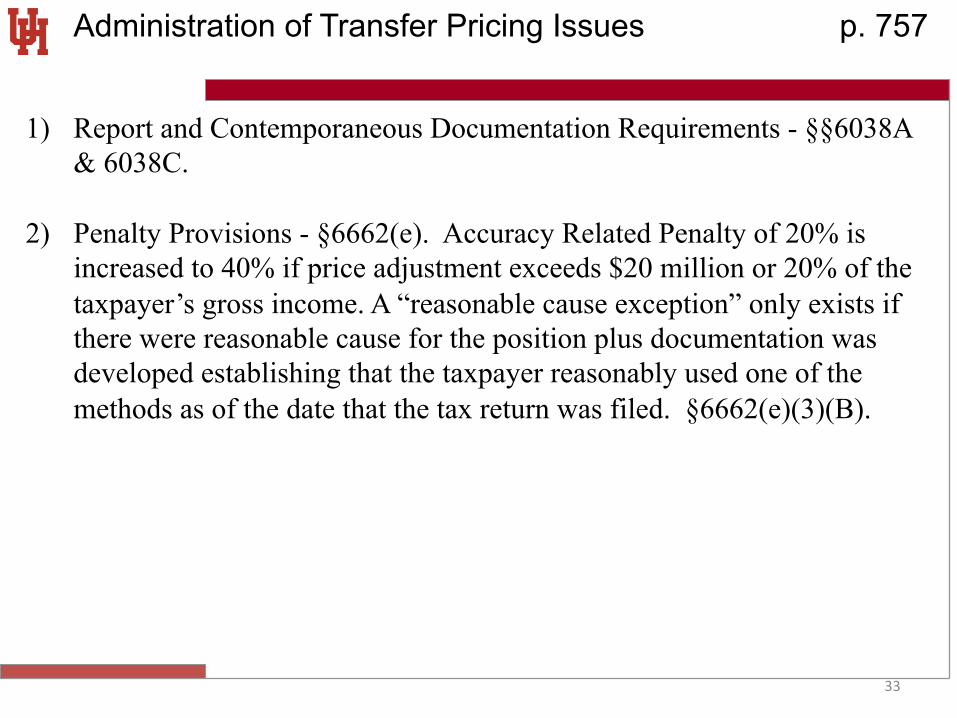

Administration of Transfer Pricing Issues p. 757

1) Report and Contemporaneous Documentation Requirements - §§6038A & 6038C.

2) Penalty Provisions - §6662(e). Accuracy Related Penalty of 20% is increased to 40% if price adjustment exceeds $20 million or 20% of the taxpayer’s gross income. A “reasonable cause exception” only exists if there were reasonable cause for the position plus documentation was developed establishing that the taxpayer reasonably used one of the methods as of the date that the tax return was filed. §6662(e)(3)(B).

34

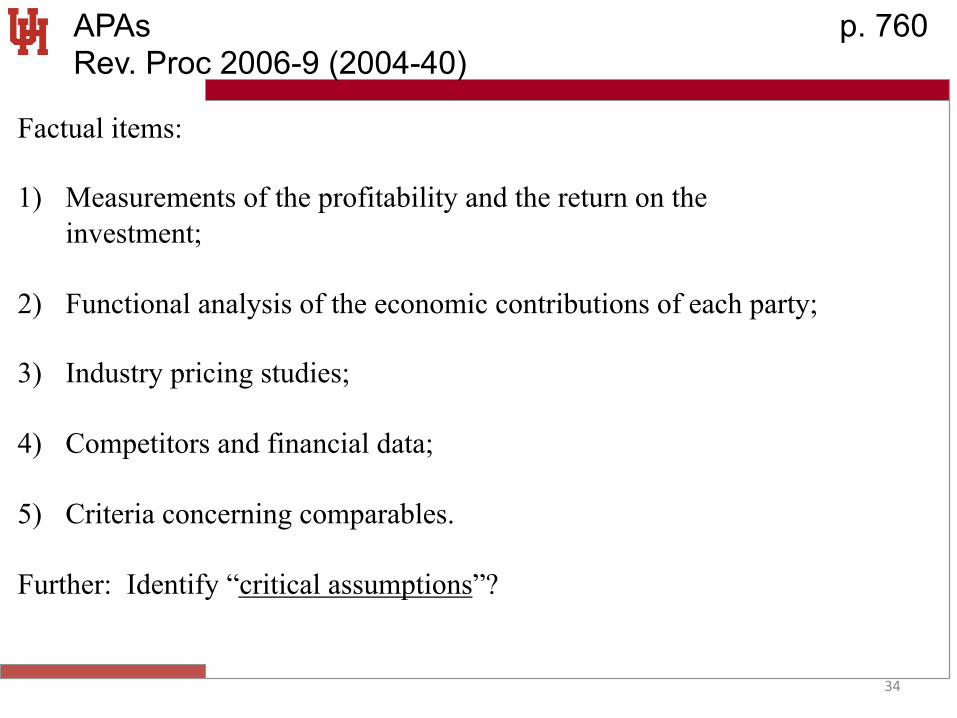

APAs p. 760 Rev. Proc 2006-9 (2004-40)

Factual items: 1) Measurements of the profitability and the return on the

investment;

2) Functional analysis of the economic contributions of each party;

3) Industry pricing studies;

4) Competitors and financial data;

5) Criteria concerning comparables.

Further: Identify “critical assumptions”?

35

Alternatives for Apportionment p. 761

1) Formulary approach State taxation – apportion on the basis of three factors: (i) labor costs, (ii) asset values, and (iii) sales receipts.

2) Production sharing arrangements in the natural resource context.

Each party is entitled to a quantity of the product produced.

36

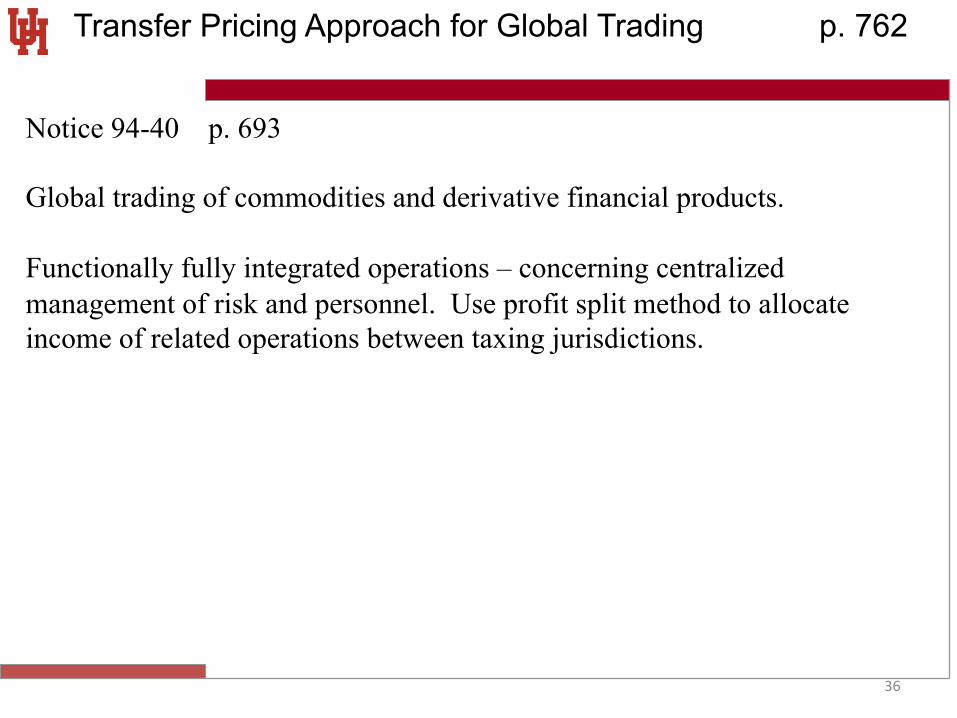

Transfer Pricing Approach for Global Trading p. 762

Notice 94-40 p. 693 Global trading of commodities and derivative financial products. Functionally fully integrated operations – concerning centralized management of risk and personnel. Use profit split method to allocate income of related operations between taxing jurisdictions.

37

Arbitration of Intercompany Pricing Disputes p. 767

1) In the U.S. – between the IRS and the taxpayer. Using “baseball arbitration”? Tax Court Rule 124.

2) Between the taxing authorities of several countries – e.g. Germany, Netherlands, Canada & Belgium treaties, and other newer treaties.