Embed Size (px)

Citation preview

Corporate Taxation Chapter One: Overview Professors Wells

Presentation:

January 22, 2018

2

Federal income tax planning concerns:

1. Choice of business enterprise form 2. Capital structure, e.g., debt or equity (or both) 3. Dividend/profits distribution policy 4. Compensation policy 5. Disposition of corporate interests 6. Estate planning/wealth transfers

Relevance of this Corporate Taxation Course

3

Business Entity Choices

Corporation – “C” or “S” status

Partnership – general or limited

Limited Liability Company (LLC)

Trust or Estate

Sole Proprietorship

Disregarded Entity (DRE)

RICs & REITS and other flow-throughs

4

Business Tax Reform’s Impact on Choice of Entity

1. Corporate Tax Rate at 21% 2. Individual Tax Rate on QBAI

is 29.6% (37% x 80%).

3. Capital Gains Tax at 23.8% (20% + 3.8% surtax under §1411).

Implication: 1. C corporation and dividend create an all-in corporate and

shareholder tax cost of 39.8% (i.e., 21% corporate tax + 79% after-corporate tax profits x 23.8%). 2. Basic equivalency between deductible compensation to owners versus dividends

(37% plus employment taxes or an all-in 39.8%. 3. Undistributed Business profits earned in a C corporation incur only a 21% tax rate. 4. Business profits of $315,000 earned in a pass-through entity is subject to a maximum

individual tax of 29.6% when the owner is subject to the top individual tax rate. 5. Business profits earned in a pass-through entity in excess of $315,000 may be

subjected to higher tax rates of up to 37%. Thus, if a business owner cannot accumulate income in a C corporation and does not qualify for the 20% pass-through deduction, then it may not matter what business form is used as the tax cost of these

two alternative strategies ranges only between 37% versus 39.8%.

5

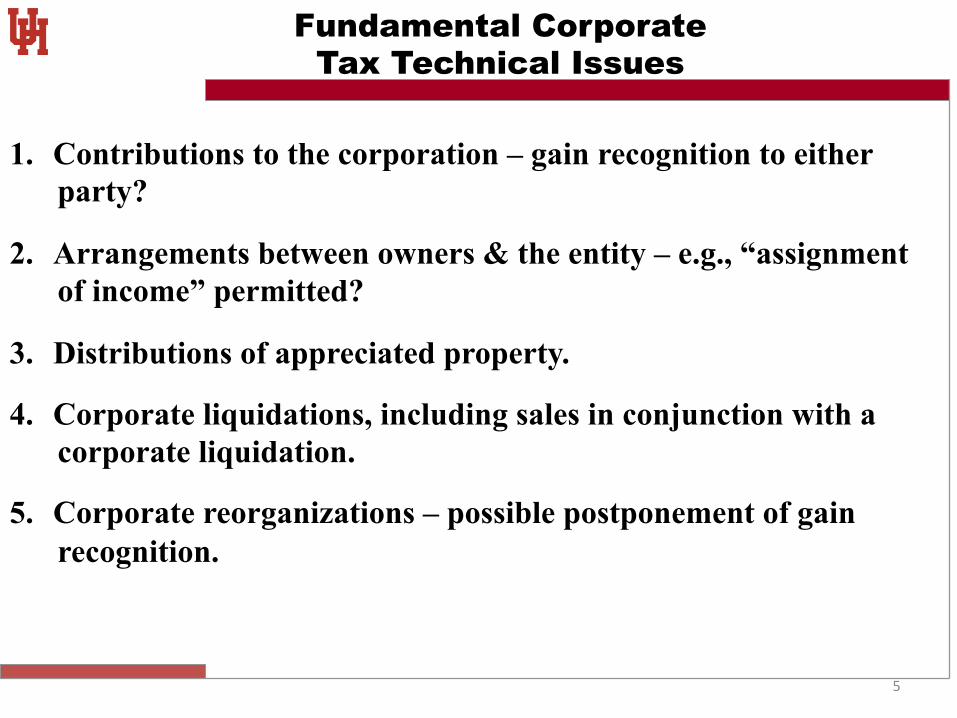

Fundamental Corporate Tax Technical Issues

1. Contributions to the corporation – gain recognition to either party?

2. Arrangements between owners & the entity – e.g., “assignment of income” permitted?

3. Distributions of appreciated property.

4. Corporate liquidations, including sales in conjunction with a corporate liquidation.

5. Corporate reorganizations – possible postponement of gain recognition.

6

“Cradle to Grave” Approach In This Course

1. Formation of Corporations: §351

2. Capital Structure – Debt vs. Equity. Is an interest expense deduction available? Tax-free repatriation of debt available?

3. Liquidating and Nonliquidating distributions -Redemptions & partial liquidations

-Stock dividends & §306 stock

4. Taxable complete or partial liquidation

5. Corporate tax-free reorganizations & divisions

6. Carryover of Corporate Tax Attributes

7. Corporate Affiliated Groups

8. S Corporations

7

Corporation/Shareholder Tax Policy Issues “Slaying Dragons or Tilting At Windmills?” p.4

1) Double taxation 2) Tax rates on ordinary income 3) Preferential capital gains rates. 4) Non-recognition for owner-shifts

Corporation

Shareholder

Corporate Tax

Shareholder Tax D

oubl

e Ta

x

8

Incidence of Corporate Tax p.6

Who bears the burden of the corporate tax? 1) The corporation? 2) Shareholders/owners? 3) Employees? 4) Corporate managers? 5) Consumers of the corporation’s output? 6) Other investors?

9

Concepts of “Tax Common Law” p.14

Non-codified federal income tax rules (particularly relevant in the corporate income tax context): 1) The “sham transaction” rule. 2) “Substance over form” analysis. 3) The “business purpose” doctrine. 4) The “step transaction” doctrine. 5) Codified §7701(o) – re: economic substance

10

Income Taxation of the Corporation p.18-22

1) Code §11 – graduated tax rate structure. -Code §11(b)(1) – no lower initial brackets for personal service companies. 2) Determination of the corporation’s taxable income – no “above

the line” vs. “below the line”; why? - capital gains & losses (no rate benefit but limits) §1211 & §1212 - dividends received deduction is available. §243 p.20 - deduction for domestic production - §199. p.21

Also, no passthrough income deduction under §199A. 3) Accounting period – is the calendar year required? §441(b) & (i) 4) Accrual method of accounting? §448(a). p.22

11

Income Taxation of the Corporation, Cont. p.22 - 31

5) Code §267 – limitations on loss transactions and timing mismatches between corporation and its owners, i.e., potential “gaps”. p. 23

6) Corporate Alternative Minimum (ALTMIN) Tax – p. 24 repealed for small corporations.

7) Multiple corporations - §1561 – p.27 Consolidated tax returns for an affiliated group of corporations - §§1501-1504. 8) The “S” corporation alternative – p.28.

12

Problem (a) C Corporation Scenario p.31

(a) Determining corporate level gross income: Inventory Sales 2,600,000 Capital Gains 200,000 2,800,000

Exclusion under §103 for $10,000 muni-bond interest

continued

13

Problem (a) Deductions Against Gross Income p.31

Operating Expenses 800,000 Depreciation 800,000 Capital Loss (limit $220,000 to gain) 200,000 Total Deductions 1,800,000

continued

14

Problem (a) Determining Tax Liability p.31

§11(b) tax calculation on $1 million taxable income is a flat 21% rate on $1 million of taxable income.

Total Tax Liability 210,000

15

Problem (b) Dividend Distribution p.31

Distribution of $790,000 after-tax profit §61(a)(7) dividend income 20% percent of $790,000 = $158,000 §1411 Surtax (3.8% on $790,000) = $ 30,020 Total taxes: (210+158+30.2) $472,000 Amount for shareholders: $601,980 Effective tax rate: 39.8 percent (Is a 39.8% effective tax rate too much?)

16

Problem (c) Deductible (?) Payments p.31

1) $500,000 salaries each paid – to eliminate all corporate level income. Reasonable compensation amount? Consequences are zero corporate tax but $370,000 individual taxes leaving $630,000 after-tax (compare this to $601,980) in Problem (b)). But not, §162(m) denies deduction for compensation in excess of $1 million.

2) Other corporate level deductions available for this purpose? §79 - group term insurance §§105 & 106 – health benefits

Creekside

S/H

<Corporate Deduction>

Compensation Income

17

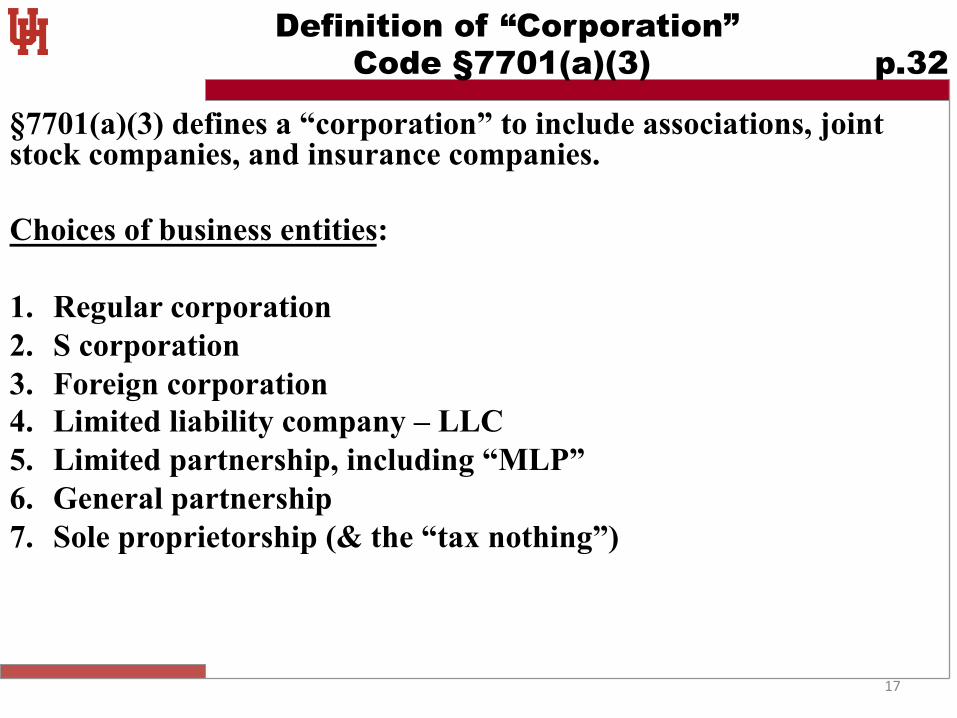

Definition of “Corporation” Code §7701(a)(3) p.32

§7701(a)(3) defines a “corporation” to include associations, joint stock companies, and insurance companies. Choices of business entities: 1. Regular corporation 2. S corporation 3. Foreign corporation 4. Limited liability company – LLC 5. Limited partnership, including “MLP” 6. General partnership 7. Sole proprietorship (& the “tax nothing”)

18

Prior Entity Classification Criteria – Tax Regs. p.32

1) Associates 2) Business objective 3) Continuity of life 4) Centralization of management 5) Limited liability for debts of entity 6) Free transferability of interests – but buy-sell agreement not

limiting transferability. Regs. had bias towards partnership status.

19

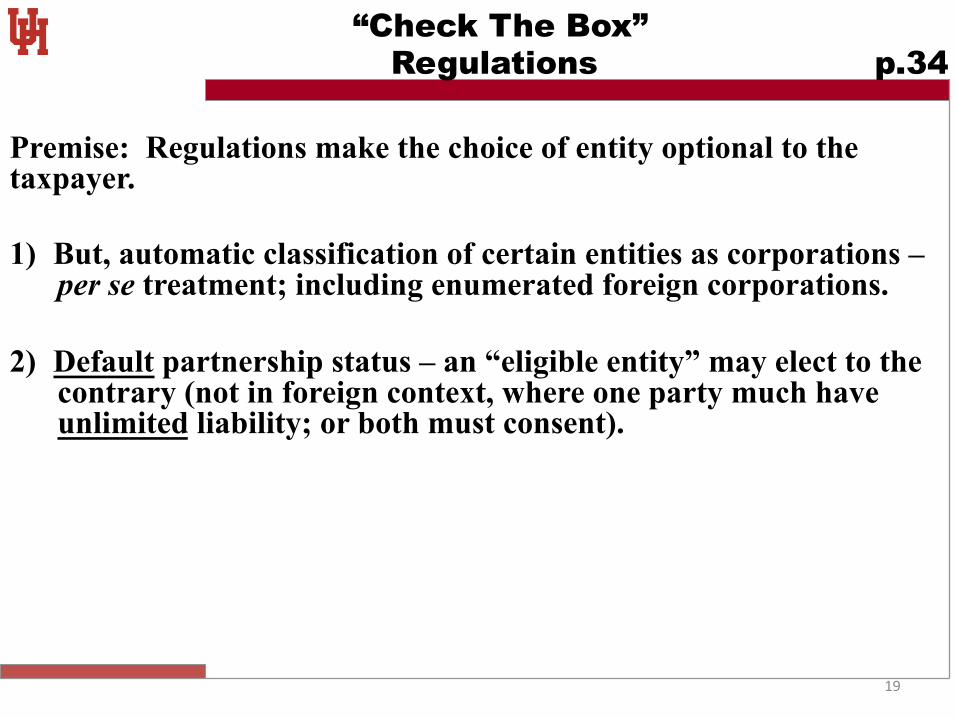

“Check The Box” Regulations p.34

Premise: Regulations make the choice of entity optional to the taxpayer. 1) But, automatic classification of certain entities as corporations –

per se treatment; including enumerated foreign corporations.

2) Default partnership status – an “eligible entity” may elect to the contrary (not in foreign context, where one party much have unlimited liability; or both must consent).

20

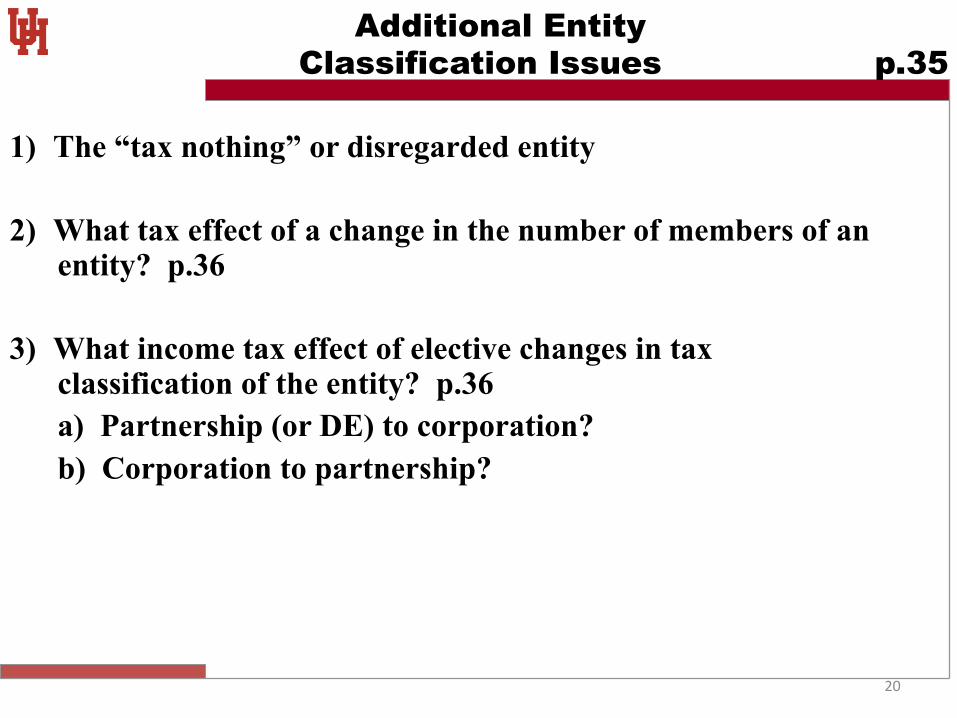

Additional Entity Classification Issues p.35

1) The “tax nothing” or disregarded entity

2) What tax effect of a change in the number of members of an entity? p.36

3) What income tax effect of elective changes in tax classification of the entity? p.36

a) Partnership (or DE) to corporation? b) Corporation to partnership?

21

The “Publicly Traded Partnership” p.37

Corporate treatment of a “publicly traded partnership”? IRC §7704. What is “publicly traded”? Purpose of the exception from corporate status where 90% or more of entity’s income is “passive”, including income from natural resource activities? See §7704(d)(1)(E).

22

Corporations vs. Partnerships vs. Trusts p.38

Reg. §301.7701-4 – Purpose of a trust is to “protect or conserve” property, but not to conduct business. If so, partnership or corporate status. Types of trusts: - Personal wealth management - Oil royalty trusts - Equipment leasing/airplane trusts

23

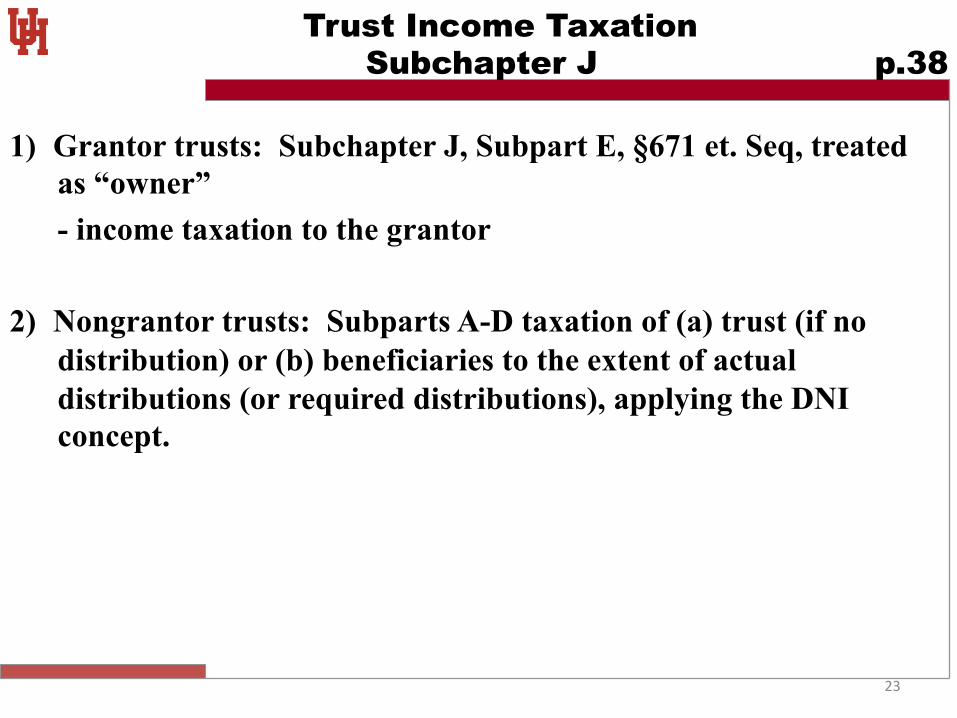

Trust Income Taxation Subchapter J p.38

1) Grantor trusts: Subchapter J, Subpart E, §671 et. Seq, treated as “owner”

- income taxation to the grantor 2) Nongrantor trusts: Subparts A-D taxation of (a) trust (if no

distribution) or (b) beneficiaries to the extent of actual distributions (or required distributions), applying the DNI concept.

24

Commissioner v. Bollinger p.39

FACTS: Corporation holding title to real property.

Issue: Is the corporation the earner of the income or is it merely the shareholder’s “agent”?

Holding: Agency status permitted &, therefore, losses were directly allowable to the individual investors as individuals – (also being shareholders of the corporate agency).

National Carbide Factors 1) Corporation operates in the name and

for the account of the principal; 2) Corporation binds the principal; 3) Transmits money to the principal; 4) Income attributable to services of the

employees of the principal: 5) Relations with the principal must not be

dependent upon the fact that it is owned by the principal; (See Bollinger case discussion) and,

6) Business purpose must be the carrying on of the normal duties of an agent.

Creekside

Bollinger

Creekside Apts

Citizen’s Fidelity / Mass. Mutual Life

Loan (as agent for B)

25

Corporation/Shareholder Tax System Integration p.43

U.S. has a classical tax system, i.e., taxation both on (1) corporation and (2) shareholder.

Who pays the corporate tax: The corporation or shareholders?

The full integration option: complete flow-through, e.g., the ALI proposal of: (1) Imputation and (2) withholding (for U.S. Treasury cash flow

acceleration).

In December 2014, the staff of Senator Hatch released “Comprehensive Tax Reform for 2015” that sets forth an extended discussion and endorsement of corporate integration efforts.

26

Partial Corporate Shareholder Integration

1. Shareholder credit for tax previously paid on the dividend amount-subject to an income “gross-up” requirement.

2. Deduction available to the distributing corporation for the dividend paid.

3. Shareholder gross income exclusion for all or part of corporate dividend.

2003 Act – reduce individual dividend tax to 20% +3.8% surtax under §1411

Dividends from certain foreign corporations located in treaty jurisdiction are eligible for reduce dividend rate. See §1(h)(11)(C)(i)(II)

27

Special Concerns About Integration Proposal p.46-47

1. Extension of corporate tax preferences to shareholders.

2. Treatment of tax-exempt shareholders (e.g., §401 deferred compensation plans).

3. Treatment of foreign shareholders (only through tax treaty?) – under 2003 Act.

4. Treatment of foreign taxes paid by the U.S. corporation. Not creditable?

28

Historic Distortions Tilting Towards Non-Corporate Status

1) Higher effective income tax rate on corporate taxable income motivates pass-through entities

2) Higher corporate tax rate motivates finance with debt (since deductible interest reduces net tax amount).

6

distributions of income from the C corporation, while ventures organized as S corporations and

partnerships are not subject to tax at the entity level. The income of S corporations and

partnerships passes through to the owner or partner in whose hands it is subject to tax.

Figure 2, below, reports the trend over the past 32 years of the number of C corporation

returns filed compared to the sum of S corporation and partnership returns.8 1986 was the last

year in which the number of C corporation returns exceeded the number of returns from

passthrough legal entities. As Figure 2 reports, while the number of C corporations has generally

declined in the United States since 1986 by a third, the number of passthrough entities has nearly

tripled.

Source:��Internal�Revenue�Service,�Statistics�of�Income,�published�and�unpublished�data.

8 The data reported in this section comparing C corporations and partnerships are derived from entity-level

returns filed with the Internal Revenue Service. Some partnerships are partnerships of C corporations, some are

partnerships of other partnerships, and some are partnerships of individuals and C corporations or other partnerships.

For this reason subsequent comparisons based either on asset size or gross receipt size includes some double

counting of assets or gross receipts as such items would be passed through to the returns of a C corporation partner

or partnership partner.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Numb

er�of

�Returns

Year

Figure�2.íNumber of C Corporation Returns Compared to the Sum of S Corporation and Partnership Returns, 1978-2009

PassthroughEntities

C�Corporations

TRA 1986

3) Higher corporate tax rate motivates not paying dividends but distribute earnings as salary or some other form of deductible payment. Taxing qualified dividends at same rate as capital gains takes away advantage of using excess cash for stock buy-backs.

29

Business Tax Reform’s Impact on Choice of Entity

1. Corporate Tax Rate at 21% 2. Individual Tax Rate on QBAI

is 29.6% (37% x 80%).

3. Capital Gains Tax at 23.8% (20% + 3.8% surtax under §1411).

Implication: 1. C corporation and dividend create an all-in corporate and

shareholder tax cost of 39.8% (i.e., 21% corporate tax + 79% after-corporate tax profits x 23.8%). 2. Basic equivalency between deductible compensation to owners versus dividends

(37% plus employment taxes or an all-in 39.8%. 3. Undistributed Business profits earned in a C corporation incur only a 21% tax rate. 4. Business profits of $315,000 earned in a pass-through entity is subject to a maximum

individual tax of 29.6% when the owner is subject to the top individual tax rate. 5. Business profits earned in a pass-through entity in excess of $315,000 may be

subjected to higher tax rates of up to 37%. Thus, if a business owner cannot accumulate income in a C corporation and does not qualify for the 20% pass-through deduction, then it may not matter what business form is used as the tax cost of these

two alternative strategies ranges only between 37% versus 39.8%.