Embed Size (px)

Citation preview

PRESENTATION 1

Why do governments tax tobacco products?

Workshop on tobacco prices and tax

World Health Organization (WHO) and International Union Against Tuberculosis and Lung Disease (The Union)

Questions at the end of the session

• Why do governments tax tobacco ?• If people stop smoking in response to

a tobacco tax increase, why do government revenues tend to increase?

• What types of taxes can be applied to tobacco products?

Two main reasons why government tax tobacco

• Generate revenues: to generate additional government revenues and meet annual revenue targets

• Promote public health: to promote health or achieve other social welfare goals

Sugar, rum, and tobacco are commodities which are no where necessaries of life,

which are become objects of almost universal consumption, and which are therefore extremely proper subjects of

taxation.

Adam Smith, Wealth of Nations, 1776

Historically, tobacco has long been the target for government taxation

Tobacco tax has capacity to generate revenues efficiently for governments

Large room for increase: In many countries, the tax rates applied to tobacco products are relatively low

Relatively easy to administer: excise tax is usually applied to a few large cigarette manufacturers

Inelastic demand: consumption falls less than the revenues generated from an increase in price

Promoting public health and social welfare

An increase in the tax applied to cigarettes and

other tobacco products generally results in higher prices at point of sale, assuming that the tax is passed onto consumers

Therefore many governments are also using tobacco tax to increase tobacco prices and reduce consumption.

Promoting public health and social welfare, cont.

Increasing tobacco prices has a stronger

impact on people who are more sensitive to price changes -- including youth, infrequent smokers, and people with lower-incomes.

Higher prices also deter people from starting to smoke and encourage people to stop smoking.

Revenues increase because the demand for tobacco is generally inelastic

People do respond to changes in tobacco prices (particularly those that are price sensitive such as children and infrequent smokers).

However, most people continue to smoke despite increases in tax, although their consumption may decline (they smoke less cigarettes).

The remaining smokers pay a higher tax – therefore government revenues tend to increase from a tobacco tax.

Example: UK: increases in the prices of cigarettes have resulted in increases in tax revenue

Tax revenue

Price

Townsend J.

10

Example South Africa: increasing tobacco taxes results in increased revenues

Source: Van Walbeek, 2003

Inflation Adjusted Cigarette Taxes andCigarette Tax Revenues, South Africa, 1961-2003

0

50

100

150

200

250

300

350

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

Real

exc

ise

rate

(in

con

stan

t 200

0 ce

nts)

0

1000

2000

3000

4000

Real

exc

ise

reve

nue

(R m

illio

n, 2

000

pric

es)

Real excise rate Real excise revenue

However, it also resulted in lower cigarette consumption—thereby

promoting health

This suggests that tobacco taxes are good instruments to achieve both revenue and public health goals.

What types of taxes can be applied to tobacco products?

• Excise tax • Value-added tax (VAT)• Sales tax• Tariff

Excise tax• Usually applied to intermediaries (i.e, tobacco

producers), and is considered relatively easier to administer especially where there are a few large producers

• Applied to products with inelastic demand – that is, products that are not highly responsive to price changes (consumption falls less than the revenues generated from an increase in price):– Products that lack “merit,” and the government

wishes to discourage (tobacco, alcohol, etc.)– Luxury goods (vs basic necessities), i.e., sports cars

Value added tax (VAT) and sales tax• VAT is an indirect consumption tax applied to the

“value added” at the stage of production, when product is sold or resold. Calculated as a proportion of price

• Sales tax: can be single or multi-stage– In example, some countries apply only a sales tax at the

point of sale. – Multi-stage sales taxes are applied at more than one stage

of the production and distribution of a product

Tariff Applied to the movement of goods across country

borders.Usually applied to imported goods but can also be

applied to exports.

They can be used to discourage trade or protect domestic industries (i.e, import tax for cigarettes that result in higher prices compared with domestically produced brands).

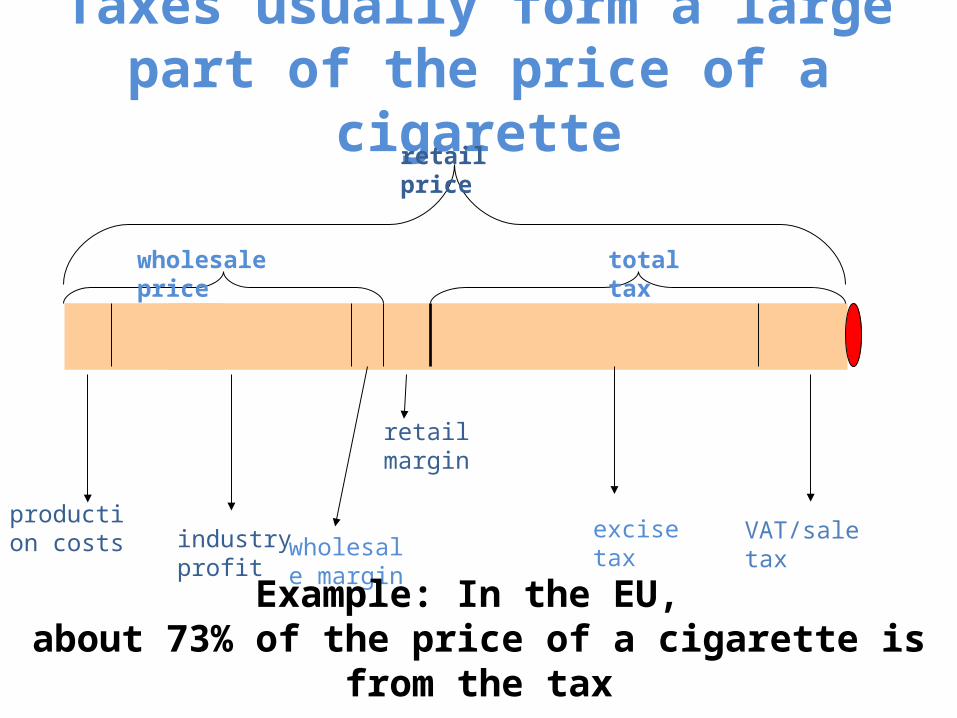

Taxes usually form a large part of the price of a cigarette

wholesale price

retail price

production costs industry

profitwholesale margin

retail margin

excise tax VAT/sale tax

total tax

Example: In the EU, about 73% of the price of a cigarette is from the tax

An increase in the tax applied to cigarettes and other tobacco products

generally results in higher prices at point of sale, assuming that the tax is

passed onto consumers.

Review questions • Why do governments tax tobacco ?• If people stop smoking in response to

a tobacco tax increase, why do government revenues tend to increase?

• What types of taxes can be applied to tobacco products?