Embed Size (px)

Citation preview

Capturing the Digital Opportunity

Thomas D. Meyer

Country Managing Director

Switzerland’s

Top500:

Copyright © 2016 Accenture All rights reserved. 2

Accenture Digital Strategy Framework

Three Value - Chain Potentials

Source: Accenture Strategy

Value Chain Areas

Digital

Enterprise

Internal Focus

Exte

rnal F

ocus

Digitize the

Business

Digitize the

Customer

Experience

Digital

CustomerDigital

Business

Disrupt Existing

(Sub-) Markets1. Digital Customer:

Use digital technologies for better customer intimacy,

to increase Net Revenue and Profitability

2. Digital Enterprise:

Reduce existing value - chain costs

3. Digital Business:

Redesign of the business models or innovation of a

new models

Copyright © 2016 Accenture All rights reserved. 3

15 different topics with over 60 indicators

First survey about digitalization among

the Swiss population

More than 100 people involved

digital.swiss Indexwww.digital.ictswitzerland.ch

digital.swiss –

Monitoring Digitalization in Switzerland

Copyright © 2016 Accenture All rights reserved. 4

Digital Index 2016 – Accenture & Google Monitor the

Digital Readiness of Industries and Firms

Google industry research

combined with detailed evaluation of

the 100 biggest companies in

Switzerland along 130 tailored

digital benchmarks

Accenture’s Digital Index

Copyright © 2016 Accenture All rights reserved. 5

The Biggest and

the Best

Copyright © 2016 Accenture All rights reserved. 6

Revenues (in CHF mn)

44 of the Swiss Top500 are Growth Champions

They achieved an average annual growth rate of 6.1% in 2010–2014.

Data source: Bisnode/Dun & Bradstreet, S&P Capital IQ, Annual Reports

Note: Chart excludes financial service companies

3177 33663710 3851 3967

50544799 4990 4963 4993

2010 2011 2012 2013 2014

+5,7%

-0,3%

2015 Growth Champions Other Companies

Compared with their

peers, the Growth

Champions are

consistent

outperformers.

Copyright © 2016 Accenture All rights reserved. 7

Return on Sales (%)

44 of the Swiss Top500 are Growth Champions

They achieved an average annual growth rate of 6.1% in 2010–2014.

Data source: Bisnode/Dun & Bradstreet, S&P Capital IQ, Annual Reports

Note: Chart excludes financial service companies

2015 Growth Champions Other Companies

Avg:

4,4%

Compared with their

peers, the Growth

Champions are

consistent

outperformers. Avg:

10,7%10.5%10.0% 9.9%

11.1%11.7%

4.7%3.9%

3.4%4.5%

5.5%

2010 2011 2012 2013 2014

Copyright © 2016 Accenture All rights reserved. 8

Digital Expectations,

Strategies and Practices

Copyright © 2016 Accenture All rights reserved. 9

Digital Transforms Business

The stakes

are high

Copyright © 2016 Accenture All rights reserved. 1010

Are Switzerland’s

best-performing

businesses also

better at being

digital?

Yes

Digital strategies

Digital activities

Better governance

Copyright © 2016 Accenture All rights reserved. 11

Accenture Research

Findings

Copyright © 2016 Accenture All rights reserved. 12

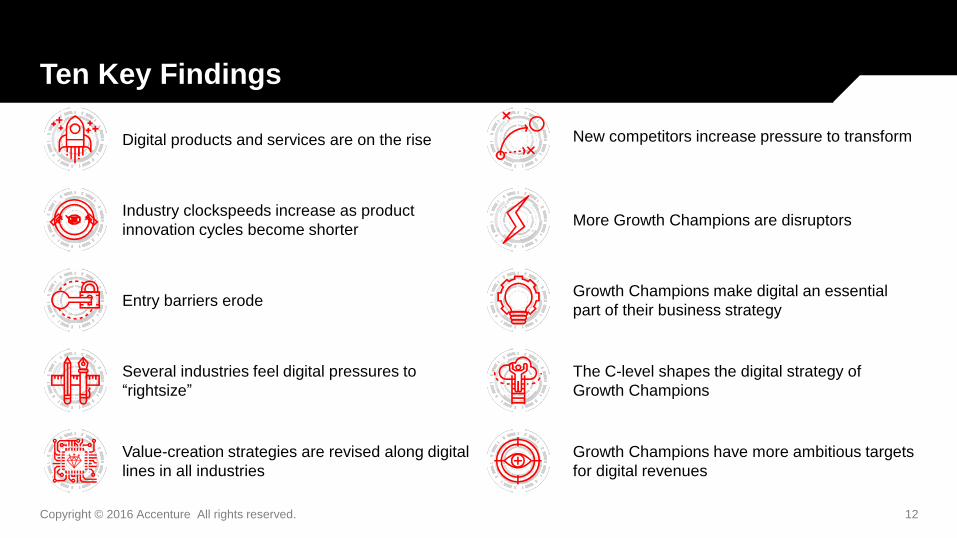

Ten Key Findings

The C-level shapes the digital strategy of

Growth Champions

New competitors increase pressure to transform

Growth Champions have more ambitious targets

for digital revenues

Digital products and services are on the rise

Entry barriers erode

Industry clockspeeds increase as product

innovation cycles become shorter

Several industries feel digital pressures to

“rightsize”

Growth Champions make digital an essential

part of their business strategy

More Growth Champions are disruptors

Value-creation strategies are revised along digital

lines in all industries

Copyright © 2016 Accenture All rights reserved. 13

Industry-level Findings (All)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Industry clockspeeds increase as

product innovation cycles

become shorter

Entry barriers erode

Several industries feel digital

pressures to “rightsize”

Value-creation strategies are

revised along digital lines in

all industries

New competitors increase

pressure to transform

Digital products and services are

on the rise

Copyright © 2016 Accenture All rights reserved. 14

Industry-level Findings (#1)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Digital products and services are

on the rise

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 15

Industry-level Findings (#2)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Industry clockspeeds increase as

product innovation cycles

become shorter

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 16

Industry-level Findings (#3)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Entry barriers erode

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 17

Industry-level Findings (#4)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Several industries feel digital

pressures to “rightsize”

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 18

Industry-level Findings (#5)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

Value-creation strategies are

revised along digital lines in

all industries

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 19

Industry-level Findings (#6)

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

External pressure to transform high medium low

New competitors increase

pressure to transform

IT

Automotive

RetailUtilities

Banking

Services

Insurance

Consumer

GoodsEnergy

Pharma & Healthcare

Other Industry

Construction

Engineering & Machinery

Logistics &

TransportChemicals

Electronics & High Tech

Resources/Raw materials (incl. trade of those goods)

Impact of new competitors

Communications

Truly

disruptive

Little to

none

Major

None ManySome

Media & Entertainment

Number of new competitors

Copyright © 2016 Accenture All rights reserved. 20

Company-Specific Findings

More GrowthChampionsare disruptors

The C-Levelshapes the digital

strategy of Growth

Champions

Growth Champions

make digitalan essential part of

their business strategy

Growth Champions set

ambitious digitalnet revenue targets –

and invest more in digitalthan their peers

Copyright © 2016 Accenture All rights reserved. 21

Get Started

Copyright © 2016 Accenture All rights reserved. 22

Becoming a Truly Digital Business

Digitize operations

Develop more

holistic customer-

value propositions

Think beyond the

organization

Do not shy away

from cannibalizing

Ground initiatives

in the advancing

digital technologies

Copyright © 2016 Accenture All rights reserved. 2323

Contacts

Thomas D. Meyer

Frederic Brunier

Markus Schimmer

Christine Wetli

Appendix

Copyright © 2016 Accenture All rights reserved. 25

Digitization of products Industry transformation New Player

Industry

Digital products

and services

Increased product

complexity

Shorter

innovation cycles

Lower entry

barriers

Lower costs and

market prices

Industry

rightsizing

Revision of value

creation logic

Convergence with

other industry

Ecosystems

center/ platform to

others

External pressure

to transform

Automotive 1 2 5 6

Banking 1 4 5 6

Chemicals

Communications 1 2 3 5 6

Construction

Consumer Goods

Electronic & High Tech

Energy 4

Engineerings &

Machinery

Insurance 1 5

IT

Logistics & Transport 5

Media & Entertainment 2 3 5

Pharma & Healthcare

Resources / Raw

materials (incl. trade of

those goods)

Retails 1 3 5 6

Services

Utilities 6

Other Industry

Industry-level Findings

Note: A cell is marked black if more than 66% of the respondents checked the industry effect in

the survey, dark grey if the rate was between 33% and 66%, and light grey if the rate was below

33%; N = 396. For indicating the “external pressure to transform” a different approach was

applied: Cells are marked black if many new competitors with major or disruptive impact entered

an industry, dark grey if some new competitors arrived with major impact, and light grey if only

few competitors entered the industry with little to no impact.

Digital products and services are on the rise

4

3

Product innovation cycles become shorter

1

2

Entry barriers erode

Digital pressures to “rightsize” arise

5

6

Value creation logics become revised

New competitors increase pressure to transform

High

Medium

Low

Copyright © 2016 Accenture All rights reserved. 26

Company-specific Finding #1

More Growth Champions are disruptors.

Copyright © 2016 Accenture All rights reserved. 27

Company-specific Finding #2

Growth Champions make digital an essential part of their business strategy.

86% of Growth Champions see digitization as a more prevalent component of their business

strategies than other companies (75%). Accenture Strategy research

has found that digital leaders

develop strategies that:

• Aim for revenue growth and

new business models

• Actively involve customers

and other stakeholders

• Are supported by an

organizational structure

geared for speed and

adaptability.

Copyright © 2016 Accenture All rights reserved. 28

Company-specific Finding #3

The C-level shapes the digital strategy of Growth Champions.

Accenture research and

experience has shown

that building a digital

culture starts at the top of an

organization by leaders

who serve as digital role

models and promote a

digital mind-set within the

company.

Copyright © 2016 Accenture All rights reserved. 29

Company-specific Finding #4

Growth Champions set ambitious digital net revenue targets —

and invest more in digital than their peers.

Copyright © 2016 Accenture All rights reserved. 30

Digital Showcases

Certain Swiss companies show what digital leadership looks like.

• Axa Winterthur

• SIKA

• SIX GroupAs Switzerland’s largest all-

lines insurer, we consider

digitization to be an opportunity

to learn even more about our

customers’ requirements and

to put them at the center of all

that we do.

- Antimo Perretta,

CEO of AXA Winterthur