Embed Size (px)

Citation preview

PREQIN QUARTERLY UPDATE:

PRIVATE DEBT

Q1 2017Insight on the quarter from the leading provider of alternative assets data

alternative assets. intelligent data.

Content includes:

FundraisingFunds in MarketInstitutional InvestorsDry Powder

© Preqin Ltd. 2017 / www.preqin.com2

PREQIN QUARTERLY UPDATE: PRIVATE DEBT, Q1 2017

FOREWORD - Ryan Flanders, Preqin

Eighteen private debt funds reached a fi nal close in the fi rst quarter of 2017, securing just under $20bn. Capital commitments in the quarter were strong, with $7bn more secured than in the same quarter last year, despite fewer funds closing. Private debt globally is

coming off the strongest three-month period in the history of the asset class, with $50bn secured across 46 funds in Q4 2016.

Investor appetite has held fi rm for North America- and Europe-focused funds, with both regions seeing eight funds close in Q1, although North America-focused funds secured nearly $2bn more than Europe-focused vehicles. Direct lending funds closed the period with the most vehicles (10) and aggregate capital secured ($11.9bn), while distressed debt funds secured $4.2bn, followed by special situations funds closing on $2.6bn in commitments.

2017 is certainly off to a strong start, specifi cally bolstered by the highly active direct lending segment in the US. Fund managers across strategies are seeing increased and sustained investor appetite for access to all parts of the market at this point in the credit cycle, when a hybrid of private debt strategies are poised to return strong results. Finally, with 284 private debt funds in market globally targeting more than $112bn, competition for investor allocations will remain fi erce for the remainder of 2017.

We hope that you fi nd this report useful and welcome any feedback you have. For more information, please visit wwww.preqin.com or contact [email protected].

All rights reserved. The entire contents of Preqin Quarterly Update: Private Debt, Q1 2017 are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in Preqin Quarterly Update: Private Debt, Q1 2017 is for information purposes only and does not constitute and should not be construed as a solicitation or other off er, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of Preqin Quarterly Update: Private Debt, Q1 2017. While reasonable eff orts have been made to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. does not make any representation or warranty that the information or opinions contained in Preqin Quarterly Update: Private Debt, Q1 2017 are accurate, reliable, up-to-date or complete. Although every reasonable eff ort has been made to ensure the accuracy of this publication Preqin Ltd. does not accept any responsibility for any errors or omissions within Preqin Quarterly Update: Private Debt, Q1 2017 or for any expense or other loss alleged to have arisen in any way with a reader’s use of this publication.

p3 Fundraising

p4 Funds in Market

p5 Institutional Investors

p6 Dry Powder

PRIVATE DEBT ONLINE

Private Debt Online is the leading source of data and intelligence on the growing private debt industry and tracks all aspects

of the asset class, including fund managers, fund performance, fundraising, institutional investors and more.

Constantly updated by our team of dedicated researchers, Private Debt Online represents the most complete source of

industry intelligence available today, with global coverage and all fund managers and investors profi led.

Get in touch today to arrange a demo of Private Debt Online: : [email protected] | : www.preqin.com/privatedebt

3

DOWNLOAD DATA PACK: www.preqin.com/quarterlyupdate

FUNDRAISING

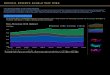

Eighteen private debt funds reached a fi nal close in Q1 2017, totalling just under $20bn in capital commitments (Fig. 1), well

behind the previous quarter, which saw 46 funds close for a record $50bn. Quarterly fundraising since 2013 has seen an average of 38 funds secure around $22bn in aggregate capital; no other quarter since Q1 2013 has had fewer than 26 fund closures.

North America- and Europe-focused funds each had eight closings in Q1, totalling $11bn and $9bn respectively, and two Asia-focused vehicles closed (Fig. 2).

Direct lending vehicles raised more than half ($11.9bn) of all capital secured by private debt funds closed in Q1 2017, followed by $4.2bn from two distressed debt funds (Fig. 3). Mezzanine accounted for the smallest amount of capital, with $1.2bn raised via four funds, while two special situations funds raised $2.6bn. Private debt funds of funds and venture debt vehicles did not see any closings in the fi rst quarter.

Hayfi n Capital Management’s Hayfi n Direct Lending Fund II was the largest fund closed in the fi rst quarter of 2017 (€3.6bn), and Alcentra Group’s Alcentra European Direct Lending Fund II secured €2.8bn; both are targeting European direct lending opportunities (Fig. 4).

30

44

35

56

30

40 38

47

41 39

45 45

26

40

33

46

1815

25 2219 17

22

14

2631

25

32

14 13

22

13

50

20

0

10

20

30

40

50

60

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2013 2014 2015 2016 2017

No. of Funds Closed Aggregate Capital Raised ($bn)

Source: Preqin Private Debt Online

Date of Final Close

Fig. 1: Private Debt Fundraising, Q1 2013 - Q1 2017

8 8

2

11

9

0

2

4

6

8

10

12

North America Europe Asia & Rest of World

No. of Funds Closed Aggregate Capital Raised ($bn)

Source: Preqin Private Debt Online

Primary Geographic Focus

Fig. 2: Private Debt Fundraising in Q1 2017 by Primary Geographic Focus

2

4

10

2

4.2

1.2

11.9

2.6

0

2

4

6

8

10

12

14

Distressed Debt Mezzanine Direct Lending Special Situations

No. of Funds Closed Aggregate Capital Raised ($bn)

Source: Preqin Private Debt Online

Fund Type

Fig. 3: Private Debt Fundraising in Q1 2017 by Fund Type

Fig. 4: Five Largest Private Debt Funds Closed in Q1 2017

Fund Firm Fund Size (mn) Type Geographic Focus

Hayfi n Direct Lending Fund II Hayfi n Capital Management 3,600 EUR Direct Lending Europe

Alcentra European Direct Lending Fund II Alcentra Group 2,807 EUR Direct Lending Europe

Carlyle Strategic Partners IV Carlyle Group 2,500 USD Distressed Debt US

Marlin Equity Partners V Marlin Equity Partners 2,500 USD Special Situations US

Cerberus Levered Loan Opportunities Fund III Cerberus Capital Management 2,050 USD Direct Lending US

Source: Preqin Private Debt Online

© Preqin Ltd. 2017 / www.preqin.com4

PREQIN QUARTERLY UPDATE: PRIVATE DEBT, Q1 2017

FUNDS IN MARKET

As at the start of Q2 2017, there were 284 private debt funds seeking an aggregate $112bn in capital. These fi gures are

roughly the same as they were in Q1 2016, when 260 funds were targeting $123bn globally.

Direct lending vehicles continue to represent the largest proportions of both funds in market and aggregate capital targeted, with 126 funds seeking $43bn (Fig. 5). Thirty-nine distressed debt funds are in market targeting just over $34bn, while 33 special situations funds seek $16bn in capital.

North America-, Asia- and Rest of World-focused funds have each seen a rise in the number of private debt vehicles in market compared to Q1 2016, while there are six fewer targeting Europe (Fig. 6).

More than three-quarters (77%) of private debt funds in market have been on the road for two years or less. The largest proportion (35%) of private debt funds in market have been on the road for 13-24 months, whereas 24% have been fundraising for six months or less (Fig. 7).

The fi ve largest funds in market account for 18% of total capital targeted within the private debt asset class. GSO Capital Solutions Fund III, the largest fund in market, is currently seeking $6.5bn for distressed debt opportunities in North America (Fig. 8).

44% 38%

14% 31%

22%13%

12%14%

4%2%5% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No. of Funds Raising Aggregate CapitalTargeted ($bn)

Venture Debt

Private Debt Fundof Funds

Special Situations

Mezzanine

Distressed Debt

Direct Lending

Source: Preqin Private Debt Online

Prop

ortio

n of

Fun

ds in

Mar

ket

Fig. 5: Private Debt Funds in Market by Fund Type

143157

75 69

1729 25 29

73 71

4029

6.5 8.6 3.8 3.10

20

40

60

80

100

120

140

160

180

Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017

North America Europe Asia Rest of World

No. of Funds Raising Aggregate Capital Targeted ($bn)

Source: Preqin Private Debt Online

Primary Geographic Focus

Fig. 6: Private Debt Funds in Market by Primary Geographic Focus, Q1 2016 vs. Q1 2017

24%

18%

35%

13%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

6 Months orLess

7-12Months

13-24Months

25-36Months

More than 36Months

Source: Preqin Private Debt Online

Prop

ortio

n of

Fun

ds in

Mar

ket

Time Spent on the Road

Fig. 7: Time Spent on the Road by Private Debt Funds in Market

Fig. 8: Five Largest Private Debt Funds in Market

Fund Firm Target Size (mn) Type Geographic Focus

GSO Capital Solutions Fund III GSO Capital Partners 6,500 USD Distressed Debt North America

Apollo European Principal Finance Fund III Apollo Global Management 3,500 USD Distressed Debt Europe

Centerbridge Special Credit Partners III-Flex Centerbridge Capital Partners 3,500 USD Distressed Debt North America

HPS Specialty Loan Fund IV HPS Investment Partners 3,500 USD Direct Lending North America

Cerberus Institutional Partners VI Cerberus Capital Management 3,500 USD Distressed Debt North America

Source: Preqin Private Debt Online

5

DOWNLOAD DATA PACK: www.preqin.com/quarterlyupdate

INSTITUTIONAL INVESTORS

Preqin’s Private Debt Online tracks more than 2,500 active investors in private debt. The 10 largest investors currently

allocate a combined $76bn to the asset class (Fig. 9). Half of these investors are based in the US, including TIAA, which currently allocates $25.9bn to private debt funds, amounting to 3% of its total assets.

Over the next 12 months, the largest proportion (51%) of active private debt investors will target mezzanine funds, for the second consecutive year (Fig. 10). The proportion of investors targeting direct lending funds over the next 12 months has increased from 36% in Q1 2016 to 42% in Q1 2017, while a slightly larger proportion (46%) of investors will target distressed debt funds.

Over a quarter (27%) of investors are seeking special situations opportunities, followed by smaller groups looking for exposure to venture debt and private debt fund of funds vehicles (5% and 3% respectively).

Europe and North America are likely to remain the most targeted regions for private debt investors over the coming year, as sought by 41% and 38% of investors seeking opportunities respectively (Fig. 11). While North America and Europe attract the majority of investor capital, 18% of investors plan to target private debt investments in Asia over the next 12 months, a two-percentage-point increase from December 2016.

51%46%

42%

27%

5% 3%

0%

10%

20%

30%

40%

50%

60%

Mezzanine DistressedDebt

DirectLending

SpecialSituations

VentureDebt

Fund ofFunds

Source: Preqin Private Debt Online

Prop

ortio

n of

Fun

d Se

arch

es

Strategy Targeted

Fig. 10: Strategies Targeted by Private Debt Investors in the Next 12 Months

38%41%

18%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

North America Europe Asia Rest of World

Source: Preqin Private Debt Online

Prop

ortio

n of

Fun

d Se

arch

es

Region Targeted

Fig. 11: Regions Targeted by Private Debt Investors in the Next 12 Months

Fig. 9: 10 Largest Investors by Current Allocation to Private Debt

Investor Type LocationCurrent Allocation to

Private Debt ($bn)

TIAA Private Sector Pension Fund US 25.9

New York State Teachers' Retirement System Public Pension Fund US 8.8

Partners Group Private Equity Fund of Funds Manager Switzerland 7.0

Netherlands Development Finance Company (FMO) Government Agency Netherlands 6.8

KB Insurance Insurance Company South Korea 5.5

African Development Bank Bank Ivory Coast 5.3

California Public Employees' Retirement System (CalPERS) Public Pension Fund US 5.0

FINEP Government Agency Brazil 4.1

Arizona State Retirement System Public Pension Fund US 4.1

Oregon State Treasury Public Pension Fund US 3.6

Source: Preqin Private Debt Online

© Preqin Ltd. 2017 / www.preqin.com6

PREQIN QUARTERLY UPDATE: PRIVATE DEBT, Q1 2017

DRY POWDER

As at March 2017, private debt managers hold more than $196bn in dry powder, up $200mn from December 2016 (Fig.

12). Distressed debt funds hold $66bn in dry powder, the most of any private debt strategy, followed by direct lending ($58bn) and mezzanine ($51bn).

North America-focused funds have $130bn in available capital (Fig. 13). This fi gure is down over $3bn from December 2016, but still accounts for two-thirds of total capital available to the asset class. Funds focused on Europe have added more than $4bn in aggregate dry powder over the same time period, with $55bn currently available for investment. Dry powder levels for Asia- and Rest of World-focused funds declined somewhat, and currently stand at $9.6bn and $1.5bn respectively.

Fig. 14 displays total private debt dry powder versus that of buyout funds since 2008; this puts the private debt market into historical perspective amid recent years of substantial growth. Aggregate dry powder for all private debt strategies remains just under $200bn, and continues to hover at over a third (37%) of the value of global buyout fund dry powder ($530bn).

Oaktree Capital Management still holds the largest amount ($17.0bn) of available capital among private debt managers, followed by GSO Capital Partners ($13.6bn) and Goldman Sachs Merchant Banking Division ($8.3bn, Fig. 15).

111 104 116 131 132

190 176215 196 196

476 477

423388

360

432 447473

535 530

0

100

200

300

400

500

600

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Mar

-17

Private Debt BuyoutSource: Preqin Private Debt Online

Dry

Pow

der (

$bn)

Fig. 14: Dry Powder: Private Debt vs. Buyout, 2008 - 2017

0

20

40

60

80

100

120

140

160

180

200

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Mar

-17

Direct Lending Mezzanine Venture DebtDistressed Debt Special Situations

Source: Preqin Private Debt Online

Dry

Pow

der (

$bn)

Fig. 12: Private Debt Dry Powder by Fund Type, 2008 - 2017

130

55

1020

20

40

60

80

100

120

140

160

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Mar

-17

North America Europe Asia Rest of World

Source: Preqin Private Debt Online

Dry

Pow

der (

$bn)

Fig. 13: Private Debt Dry Powder by Primary Geographic Focus, 2008 - 2017

Fig. 15: 10 Largest Private Debt Fund Managers by Estimated Dry Powder

Firm HeadquartersEstimated Dry

Powder ($bn)

Oaktree Capital Management US 17.0

GSO Capital Partners US 13.6

Goldman Sachs Merchant Banking Division US 8.3

HPS Investment Partners US 7.0

Intermediate Capital Group UK 6.0

Hayfi n Capital Management UK 5.9

Ares Management US 4.8

Fortress Investment Group US 4.6

Cerberus Capital Management US 4.0

Centerbridge Capital Partners US 3.4

Source: Preqin Private Debt Online

Register for demo access to fi nd out how Preqin’s Private Debt Online can help your business:

www.preqin.com/privatedebt

Source new investors for funds

Identify new investment opportunities

Conduct competitor and market analysis

Track fi rms with capital available to invest

Develop new business

alternative assets. intelligent data.

alternative assets. intelligent data.

With global coverage and detailed information on all aspects of the private debt asset class, Preqin’s industry-leading Private Debt Online service keeps you up-to-date on all the latest developments in the

private debt universe.

Find out how Preqin’s range of private debt products and services can help you:

www.preqin.com/privatedebt

PRIVATE DEBT ONLINE

New York ■ London ■ Singapore ■ San Francisco ■ Hong Kong ■ Manila