Embed Size (px)

Citation preview

© 2013 Navigant Consulting, Inc.

Evolution of the Electric Industry

Structure in the U.S. and

Resulting Issues

Prepared for:

Electric Markets Research Foundation

Navigant Consulting, Inc.

1200 19th Street NW

Suite 700

Washington, DC 20036

202.973.2400

www.navigant.com

October 8, 2013

© 2013 Navigant Consulting, Inc.

Copyright This report is protected by copyright. Any copying, reproduction, performance or publication in

any form without the express written consent of Navigant Consulting, Inc. is prohibited.

No Warranties or Representations, Limitation of Liability This report (The “Report”) was prepared for Electric Markets Research Foundation on terms

specifically limiting the liability of Navigant Consulting, Inc. (“Navigant”). Navigant’s conclusions

are the results of the exercise of its reasonable professional judgment based upon information

believed to be reliable. This Report is provided for informational purposes only. Navigant accepts

no duty of care or liability of any kind whatsoever to the reader or any other third party, and all

parties waive and release Navigant for all claims, liabilities and damages, if any, suffered as a result

of decisions made, or not made, or actions taken, or not taken, based on this report. Use of this

Report by reader for whatever purpose should not, and does not, absolve reader from using due

diligence in verifying the Report’s contents.

Electric Markets Research Foundation

Navigant conducted this study for the Electric Markets Research Foundation (EMRF). EMRF was

established in 2012 as a mechanism to fund credible expert research on the experience in the United

States with alternative electric utility market structures – those broadly characterized as the

traditional regulated model where utilities have an obligation to serve all customers in a defined

service area and in return receive the opportunity to earn a fair return on investments, and the

centralized market model where generation is bid in to a central market to set prices and customers

generally have a choice of electric supplier.

During the first few years of restructured markets, numerous studies were done looking at how

these two types of electric markets were operating and the results were mixed. But since those early

studies, limited research has been done regarding how centralized markets and traditionally

regulated utilities have fared. The Electric Markets Research Foundation has been formed to fund

studies by academics and other experts on electric market issues of critical importance.

© 2013 Navigant Consulting, Inc. Page i October 8, 2013

Table of Contents

1. Executive Summary ................................................................................................................ i

History and Development of Traditional Regulation and Competitive Markets .................................. i Today’s Two Broad Models ......................................................................................................................... iii System Reliability ......................................................................................................................................... iv Environmental Issues .................................................................................................................................... v Relative Allocation of Risks over Time ...................................................................................................... vi Responsibilities for Planning and the Types of Planning Performed .................................................... vi Innovation and the Levels of Research and Development Pursued ..................................................... vii State and Federal Government ................................................................................................................. viii

2. Introduction ............................................................................................................................ 1

3. History and Development of Traditional Regulation and Competitive Markets ..... 2

3.1 Development of Traditionally Regulated Markets .............................................................................. 3 3.2 Period of Growth and Declining Costs, 1945‐1970 .............................................................................. 6 3.3 Slowed Growth and Inflation, Seeds of Competition, 1970‐1990 ...................................................... 7 3.4 The Advent of Centralized Markets, 1990‐1999 ................................................................................... 9 3.5 Traditional Regulation and Centralized Markets Today .................................................................. 13

4. Today’s Two Broad Models ............................................................................................... 20

4.1 Current Status of Centralized Wholesale Generating Markets ....................................................... 20 4.1.1 Todays’ Centralized Wholesale Generating Markets .......................................................... 20 4.1.2 Energy Markets ........................................................................................................................ 21

4.2 Bilateral Wholesale Generation ............................................................................................................. 23 4.3 Today’s Retail Choice Status ................................................................................................................ 23 4.4 Cost‐Based Rates and Traditional Utility Regulation ....................................................................... 24 4.5 The Retail Choice Model ....................................................................................................................... 24 4.6 Differences Between the Traditional and Retail Choice Models ..................................................... 26

4.6.1 Retail Choice Markets .............................................................................................................. 26 4.6.2 Pricing for Generation Services .............................................................................................. 27

5. System Reliability ................................................................................................................ 28

5.1 Development of the Mandatory Reliability Standards ..................................................................... 28 5.2 Transmission Reliability ....................................................................................................................... 31

5.2.1 The NERC Standards and Who Must Comply .................................................................... 31 5.2.2 Role of the Registered Entities and States ............................................................................. 33 5.2.3 Compliance Monitoring and Enforcement ........................................................................... 34

5.3 Resource Adequacy ............................................................................................................................... 34

© 2013 Navigant Consulting, Inc. Page ii October 8, 2013

6. Environmental Issues .......................................................................................................... 39

6.1 Impacts of Environmental Regulation ................................................................................................ 39 6.2 Differing Impacts for Different Structures ......................................................................................... 39

6.2.1 Greenhouse Gas Initiatives ..................................................................................................... 40 6.2.2 Renewable Portfolio and Energy Efficiency Resource Standards ..................................... 42 6.2.3 Mercury and Air Toxics Standards ........................................................................................ 44 6.2.4 National Ambient Air Quality Standards ............................................................................. 44 6.2.5 Clean Air Interstate Rule/Cross‐State Air Pollution Rule ................................................... 44 6.2.6 Regional Haze ........................................................................................................................... 44 6.2.7 Cooling Water Intake Structures ............................................................................................ 45 6.2.8 Coal Combustion Residuals .................................................................................................... 45

7. Relative Allocation of Risks over Time ........................................................................... 46

7.1 Traditionally Regulated Model ............................................................................................................ 46 7.2 Centralized Market Model .................................................................................................................... 47

8. Responsibilities for Planning and the Types of Planning Performed ...................... 51

8.1 The Transmission Planning Framework ............................................................................................. 51 8.1.1 Regional Planning and the Inclusion of Non‐Incumbent Transmission Developers ..... 51 8.1.2 Interregional Planning Coordination .................................................................................... 53 8.1.3 Cost Allocation ......................................................................................................................... 54 8.1.4 Planning for Public Policy Requirements ............................................................................. 56

8.2 Transmission Siting and Transmission Grid Expansion .................................................................. 59 8.3 Adequacy Planning and Integrated Resource Planning ................................................................... 60

8.3.1 Integrated Resource Planning and Procurement Plans ...................................................... 60

9. Innovation and the Levels of Research and Development Pursued .......................... 63

9.1 Declining Costs and Increasing Flexibility of Generation Technologies ........................................ 63 9.2 Emergence of Demand Side Alternatives ........................................................................................... 65 9.3 Smart Grid ............................................................................................................................................... 66 9.4 Research and Development Investment ............................................................................................. 67

10. State and Federal Government ........................................................................................ 70

© 2013 Navigant Consulting, Inc. Page iii October 8, 2013

List of Figures and Tables

Figures:

Figure 1. Historical Timeline 1920‐1945 ................................................................................................................ 3 Figure 2. Historical Timeline 1945‐1970 ................................................................................................................ 6 Figure 3. Historical Timeline 1970‐1990 ................................................................................................................ 7 Figure 4. Historical Timeline 1990‐1999 ................................................................................................................ 9 Figure 5. Historical Timeline 1999‐Present ......................................................................................................... 13 Figure 6. Regional Transmission Organizations ................................................................................................ 18 Figure 7. Status of Electricity Restructuring (Retail Choice) by State .............................................................. 19 Figure 8. NERC Regions ........................................................................................................................................ 31 Figure 9. State RPS Policies ................................................................................................................................... 42 Figure 10. State EERS Policies ............................................................................................................................... 43 Figure 11. Forecasted Energy Sales from Alternative Suppliers ...................................................................... 49 Figure 12. States with Integrated Resource Planning (or similar planning process) ..................................... 62

Tables:

Table 1. Wholesale and Retail Market Structure by State ................................................................................. 20 Table 2. Centralized Markets and their Attributes ............................................................................................. 22 Table 3. Examples of Market‐Based Resource Adequacy Mechanisms .......................................................... 37 Table 4. Examples of Cost Allocation Approaches Used by Planning Region ............................................... 55 Table 5. Estimated National Average Levelized Cost of New Generation Resources in 2018 ..................... 64 Table 6. EPRI Planned R&D Funding for 2013 and 2014 .................................................................................. 69

© 2013 Navigant Consulting, Inc. Page i October 8, 2013

1. Executive Summary

This paper explores the key policy questions surrounding two broad regulatory/market structures that

currently exist in the United States (U.S.) in varying degrees: traditional utility regulation without

centralized markets on the one hand, and centralized electricity markets, often involving restructured

regulation, on the other.1 The paper is intended as an educational piece for non‐industry experts on how

and why electric utility regulation has evolved and one model has developed in some areas of the

country while not in others. This paper does not provide a critique of the market structures nor a

quantitative comparison between the two models. This paper may also serve as a foundation for

identifying the issues that characterize the key differences between the approaches and help guide

decisions on future research projects for the Electric Markets Research Foundation.

History and Development of Traditional Regulation and Competitive Markets

The evolution of the U.S. electric industry is a history of adaptation to changes in the operating and

regulatory environment. The first chapter traces the history of the two regulatory/market structures. It

begins from the early structure of the electric utility industry as it developed around the concept of a

central source of power with vertically integrated utilities and regulation of these entities by municipal

and state governmental entities.

During the early twentieth century, electric systems grew rapidly. Under the Rural Electrification Act

service was extended to unserved, or underserved, rural areas, which also gave rise to rural electric

cooperatives in many areas of the U.S. Disenchantment with privately owned power spurred the

development of government‐owned utilities, particularly hydroelectric power facilities. During the

presidency of Franklin D. Roosevelt (1933 to 1945), a number of these facilities were built, ushering in the

beginning of publicly owned power.

In 1920, the Federal Water Power Act was passed to coordinate the development of these hydroelectric

projects. This act created the Federal Power Commission (FPC), now the Federal Energy Regulatory

Commission (FERC). In 1935 the law was renamed the Federal Power Act and the FPC’s regulatory

jurisdiction was expanded to include all interstate electricity transmission and sales of power for resale

1 Within the two different general models there are further distinctions. The traditionally regulated model is often

characterized at the wholesale level by bilateral resource transactions while at the retail level the traditional

vertically integrated utility provides / purchases all functions required to provide service to the end users. The

centralized market model generally involves the existence of a Regional Transmission Organization (RTO) or

Independent System Operator (ISO) that administer centralized, bid‐based markets at the wholesale level with some

degree of retail competition where the customer has the right to procure power competitively with transmission and

distribution service provided by a regulated utility. Transmission and distribution under both models remains

governed by a cost of service regulatory approach. Further, the reader should be aware that there may be instances

where regions or entities generally characterized as functioning under a certain broad model may not exhibit all

features of that model. For example, there are regions that have centralized wholesale energy markets that may not

have implemented retail choice in all states within that region. Similarly, there are regions that remain traditionally

regulated but have elements of centralized markets and retail choice.

© 2013 Navigant Consulting, Inc. Page ii October 8, 2013

and formed the basis for federal jurisdiction over the electric and natural gas industries, and the

responsibilities of the FERC. In that same year, after several large holding company systems collapsed,

the Public Utility Holding Company Act of 1935 (PUHCA) was passed, giving the Securities and

Exchange Commission responsibility for regulating utility holding companies. Under Title II, PUHCA

charged the FPC with regulating utilities involved in interstate wholesale marketing or transmission of

electric power. Regulatory administration of the rate case established base rates based on the actual

normal costs of providing service determined by the utility’s revenue requirement.

A number of damaging events occurred in the 1960s and 1970s that interrupted the growth that had

occurred in the prior several decades. First, the Northeast Blackout of 1965 raised concerns about

reliability; then, the passage of the Clean Air Act of 1970 and its amendments in 1977 increased utility

costs to reduce polluting emissions. And, most significantly, the Oil Embargo of 1973‐1974 resulted in

increases in fossil‐fuel prices. In 1978, Congress pursued legislation to address these pressures by

reducing U.S. dependence on foreign oil and developing renewable and alternative energy sources. The

Public Utility Regulatory Policies Act of 1978 ushered in a greater reliance on market forces to set

wholesale energy prices, while requiring utilities to buy power at their “avoided cost” from unaffiliated

alternative energy resources meeting a number of qualifications. Throughout the late 1980s, utility

interest in wholesale transactions grew, prompted by a number of factors. Some utilities found

themselves with excess generation because expected demand growth did not meet projected levels. In

addition, in the wake of aggressive utility construction programs, regulators determined that some costs

were imprudent and refused to allow the utilities to recover them in rates. Utilities sought to sell

electricity in wholesale transactions at market‐based rates, and FERC would grant these requests upon a

showing that the utility could not exercise market power to set prices.

Two significant policy decisions occurred in the 1990s that provided a foundation for energy market

development. The first was the passage of the federal Energy Policy Act of 1992 (EPACT), which created

a number of incentives for market development. The second was the cornerstone in the creation of

competitive wholesale power markets, FERC’s Order No. 888. Order No. 888 strove to eliminate anti‐

competitive practices and undue discrimination in transmission services through a universally applied

open‐access transmission tariff. At the same time these changes were occurring in the wholesale

electricity markets, a growing number of states were also pursuing a reliance on competitive markets for

the retail supply of electric power. This typically required the incumbent utility to divest some or all of

its generation and become a wires‐only distribution utility.

By 2000, FERC was calling for the voluntary formation of regional transmission organizations (RTOs)

through its Order No. 2000. The basis of Order No. 2000 was FERC’s belief that RTOs would facilitate

the continued development of competitive wholesale power markets and would lead to improvements

in reliability and management of the transmission system, eliminating any remaining discriminatory

practices. However, concurrent with FERC’s efforts under Order No. 2000, challenges were arising in

the California markets. In 2001, California suffered from flaws in its power market structure leading to

the insolvency of one of the largest utilities in the state. Following the California energy market crisis

and a blackout that affected a large portion of the northeastern U.S. and Canada in 2003, Congress

enacted the Energy Policy Act of 2005 (EPAct 2005) on August 8, 2005. This legislation provided FERC

greater authority to oversee wholesale electricity markets. FERC subsequently issued Order No. 890 in

© 2013 Navigant Consulting, Inc. Page iii October 8, 2013

early 2007 to correct flaws in its pro forma Open Access Transmission Tariff (OATT) that had been

uncovered during the ten years since Order No. 888 was issued.

During the autumn of 2008, large disruptions in the financial markets also uncovered vulnerabilities in

the electricity markets. In response, FERC issued Order No. 741 proposing extensive revisions to its

policy on RTO/Independent System Operator (ISO) credit practices. Congress took additional actions in

response to the 2008 financial crisis, including enacting the Dodd‐Frank Act, which had the potential to

affect energy trading companies and wholesale energy markets.

Today’s Two Broad Models

At the wholesale level, bilateral transactions prevail in the Southeast, most of the Southwest, parts of the

Midwest and the West, excluding California. Under this regime, utilities engage in wholesale physical

power transactions through bilateral arrangements ranging from standardized contract packages, to

customized, complex contracts known as structured transactions. This is characterized as a component

of the traditionally regulated model. A centralized market model is the norm in the Northeast, Mid‐

Atlantic, much of the Midwest, the Electric Reliability Council of Texas (ERCOT), and California. In

these markets participants bid/offer resources into a centralized market and are paid a uniform clearing

price.

Similarly, two models are currently employed in the United States to deliver electric power to retail

consumers. The traditional model is the Vertically Integrated Utility, where various services are

“bundled,” meaning that all energy and energy delivery (transmission and distribution) services, as well

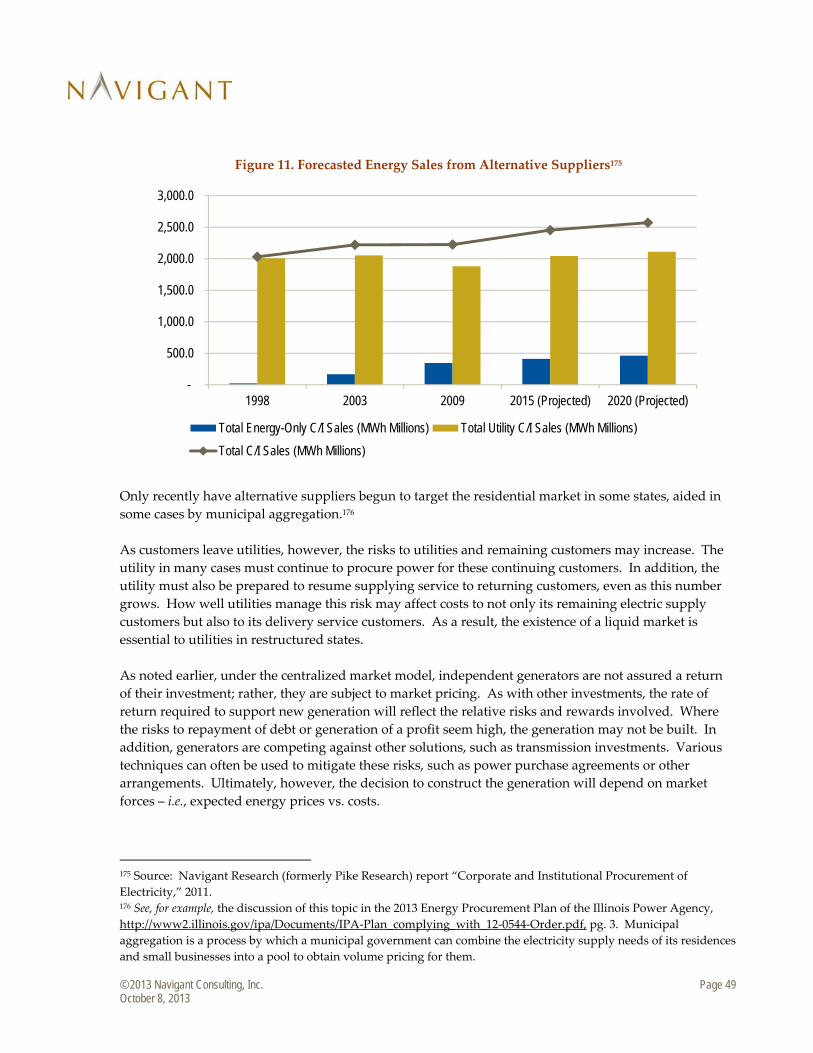

as ancillary and retail services, are provided by one entity.2 Customers do not have the option of

selecting another provider for any of these services, and the utility’s charges are set entirely by the

regulatory authority or governing body in the case of public power. In contrast, under the retail choice

model, customer choice has been partially or fully implemented. In this model, customers may often

select their energy provider, and the utility will deliver the power. Non‐utility energy providers can set

their own pricing for power, but the utility’s charges for delivery and related services are set by the

regulatory authority. Traditional “bundled” pricing may also be available from the utility, for some or

all types of customers.3

In the United States, traditional utility pricing (or ratemaking) is cost‐based, meaning that the utility is

allowed to charge prices that will recover prudent operating costs and provide an opportunity to earn a

reasonable rate of return on the property devoted to the business. Among the historical criticisms of

cost‐based ratemaking are that it creates an incentive to over‐invest in capital‐intensive projects and fails

to provide utilities proper incentives to operate efficiently.

2 Although in the case of Public Power, generation and transmission may be provided by joint authorities and

bundled by the local distribution utility. 3 It is worth noting that the “Retail Choice” model encompasses a spectrum of features that may vary from state to

state. The key features, such as the existence of retail choice for at least some customers and the availability of

organized wholesale energy markets are the same, although there may be differences in the manner and degree to

which these features are implemented.

© 2013 Navigant Consulting, Inc. Page iv October 8, 2013

The customer choice aspect of the Retail Choice model was introduced in the United States in the 1990s

in response to high regulated prices in some regions relative to the cost of wholesale markets. Many

consumer groups found retail competition attractive because the prices in emerging wholesale markets

were significantly below the regulated retail prices charged by utilities.

In contrast to the traditional regulated model, the customer choice feature of the retail choice model

limits the operation of the regulated utility to the transmission and distribution functions, where

traditional cost‐based pricing is implemented and approved by regulators. Generation services are

provided either by competitive service providers or through a default “provider of last resort.” Retail

choice also has its criticisms; among them are that residential participation in some retail markets has

been slow to materialize, in part because retail suppliers have not pursued residential customers as

aggressively as commercial customers due to their relatively small size. Other factors may include a lack

of incentives (i.e., lower prices) or information.

System Reliability

Reliability standards or criteria used for planning and operations are an integral part of the electric

power industry and have been since the very first systems were developed in the late nineteenth

century. There are two principal components to bulk power system (BPS) reliability—resource adequacy

and transmission security.4 The area of transmission security is governed by FERC, the North American

Electric Reliability Corporation (NERC), and the Regional Entities (REs). The states still retain a role in

resource adequacy and in regulating the reliability of local distribution systems.

Over the years, a series of blackouts (the 1965 Northeast Blackout, the blackout on the East Coast in July

1977, the West Coast blackouts in July and August of 1996, and the blackout on August 14, 2003 affecting

the northeastern U.S. and Canada) led to the creation of NERC and its REs. Prior to 2005, compliance

with reliability standards was voluntary. The enactment of EPAct 2005 eliminated the voluntary nature

of the NERC reliability standards. FERC was charged with the ultimate oversight of electric reliability of

the Bulk Power System (BPS). NERC, as the independent Electric Reliability Organization (ERO), along

with its REs develop mandatory reliability standards subject to FERC approval, monitor industry

participants’ compliance with these standards, and can levy penalties for noncompliance up to one

million dollars per day per violation for the most serious violations.

Currently, there are 102 standards with more than 1,300 requirements applicable and mandatory in the

U.S. Within the United States, other than Alaska and Hawaii, all users, owners, and operators of the BPS

must comply with the reliability standards developed by the ERO and regional reliability standards

developed by the REs. This responsibility extends FERC jurisdiction not only to the government‐owned

and other so‐called non‐jurisdictional utilities, but also to utilities in Texas as well as to a wide range of

non‐utility entities that use the transmission grid.

The ERO’s compliance registry process is used to identify the set of entities that are responsible for

compliance with a particular reliability standard and the applicability section of a particular reliability

standard determines the applicability of each reliability standard. The NERC Functional Model provides

4 Reliability is also dependent at the local level on the reliability of the local distribution system.

© 2013 Navigant Consulting, Inc. Page v October 8, 2013

guidance concerning the type of function for which an entity is registered and, therefore, their role in

maintaining reliability.

Regardless of whether entities are located in regions that have centralized markets and RTOs/ISOs or a

traditional regulation structure, the REs and NERC will identify who must be registered and as what

type of functional entity. The primary difference between functional responsibilities of entities that exist

in RTOs/ISOs and those that do not is that RTOs/ISOs often perform the functional roles of balancing

authority, reliability coordinator, transmission operator, and transmission planner. In regions that do

not have RTOs/ISOs, the electric utility often performs all the functions and is registered as multiple

functional entity types. The states and other governmental entities that have regulatory oversight

functions may participate as non‐voting members in NERC and RE activities, under the government

sector, and may also provide comments in FERC proceedings.

Two approaches have been applied to achieving the resource adequacy goals—market‐based and an

administrative approach. With a capacity market, suppliers receive periodic (i.e., annual or monthly)

payments for providing “reliable” capacity to a system and Load‐Serving Entities (LSEs) are required by

the regulatory standard to purchase the capacity. Examples of capacity markets are PJM, NYISO, and

ISO‐NE. There are also other variations to the market‐based approach; these are energy‐only markets (in

ERCOT) and markets with administrative resource adequacy requirements for LSEs (CAISO and MISO).

One key concern for consumers is price volatility and uncertainty. Questions also remain as to how

current market design will work to ensure capacity adequacy in the long term at economically efficient

levels. Under the administrative approach, resource adequacy is achieved through traditional Integrated

Resource Planning (IRP) and competitive resource solicitation. One key concern with the administrative

approach is increased consumer cost due to uneconomic long‐term investment decisions. Examples of

administrative approaches are the Southwest Power Pool, most of the Western Electricity Coordinating

Council outside the CAISO, and the southeast U.S.

Environmental Issues

Market/regulatory structure plays an important role in whether and how environmental requirements

and policies affect electric entities. Where the traditionally regulated model prevails, the impacts—

whatever they are—fall on the utility and the associated costs flow to its customers through cost‐based

rates. In contrast, where there has been a restructuring of utility regulation and the development of

centralized electricity markets, impacts vary widely. A utility that owns no generation would not incur

the direct expense of complying with environmental rules relating to emissions, although generators

would try to raise prices to recover costs. Similarly, generation‐only entities would not normally be

subject to renewable portfolio standards (RPS) or policies favoring the use of renewable energy

resources.

Independent generators in centralized markets are particularly sensitive to the costs of environmental

regulation, since these generators rely on market pricing rather than cost of service rates. Uneconomic

generation in competitive markets may be retired rather than operated at a loss for any extended period

of time. Under the traditional regulated model, vertically integrated utilities are also sensitive to

environmental regulation, including policies or regulations favoring renewables, since compliance

would increase or decrease its costs.

© 2013 Navigant Consulting, Inc. Page vi October 8, 2013

The costs and risks from proposed environmental regulations will differ by region, largely affecting

those regions of the country with significant amounts of existing coal‐fired generation. Whether

environmental costs end up being passed through in cost‐based rates or result in higher market‐based

rates, the impact on electricity consumers in those regions will be considerable.

Relative Allocation of Risks over Time

Under the traditional regulated model, the allocation of risks is well established. The utility has a

monopoly right to provide electric service to retail customers, who in turn are entitled to electricity at a

“reasonable” cost. The utility’s risk in the traditional model is that its rates will not recover its actual

investment and operating costs or meet the rate of return required for its investors to risk their money.

The utility also risks that its costs will be determined to have been prudently incurred and that it will

receive timely recovery through the regulatory process. The customers face much of the risk of utility

over‐investment or under‐investment (either through bad decision making or out of concern that it will

not recover its costs), and unreliable service and high costs as a result of ineffective operations or bad

decision making; to the extent the regulators allow utilities to recover their costs.

In a centralized market model, the risks for customers and the mechanisms for addressing them are the

same with respect to the transmission and distribution system. Rate cases and regulation are the

principal tools to protect customers from monopoly abuses and to set the utility’s pricing for the delivery

of electricity. However, with respect to generation, the market sets wholesale energy prices. In these

markets, many generators in a region compete with one another to supply electricity. These regions also

rely on market forces to cause needed generation to be added when and where it is needed but some

markets have found that these forces may not be enough incentive. A further complexity in some

centralized markets is customer choice where a utility must be prepared to procure power for a changing

customer base.

Responsibilities for Planning and the Types of Planning Performed

Planning functions encompass adequacy and transmission security planning. State and federal

governments have overlapping responsibilities for these two aspects of planning. The oversight of

resource adequacy planning has traditionally been a state function while transmission security planning,

with the important exception of transmission siting, has now become governed by federal law and

regulation overseen by FERC.

In recent years, two key FERC Orders have encompassed the field of transmission planning. They are

Order No. 890 and Order No. 1000, which apply to entities whether in RTO/ISO regions with centralized

markets or not. Order No. 890 promoted increased open, transparent and coordinated transmission

planning on sub‐regional (local) and regional levels. Order No. 1000 built upon and extended many of

the ideas initially introduced under Order No. 890. Among the changes introduced in Order No. 1000

are requirements for regional and interregional planning, cost allocation, consideration of public policy

requirements, and elimination of the Right of First Refusal in wholesale tariffs to construct new facilities.

In areas where RTO/ISOs have formed, transmission planning often encompasses a larger region than

previously existed and is coordinated around a centralized processes administered by the RTO/ISO. In

areas where traditional regulation remains, planning is coordinated by the vertically integrated utilities

© 2013 Navigant Consulting, Inc. Page vii October 8, 2013

or public power entities within their territory. These territories may also encompass large areas due to

mergers and holding company consolidation. Both traditionally regulated and competitive market

(RTO/ISO) regions have in place processes to coordinate planning with their neighboring entities.

The authority over transmission siting is a patchwork quilt of overlapping and sometimes unclear

divisions of authority. While the majority of siting authority currently lies with the states, there are

instances where federal approvals are required. The Energy Policy Act of 2005 established a limited role

for the U.S. Department of Energy (DOE) and the FERC in transmission siting. The act directed DOE to

create “transmission corridors” in locations with adequate transmission capacity that had “national

interest” implications. The act also granted FERC secondary authority over transmission siting in these

corridors, which may not be exercised by FERC unless the state where the facility would be sited lacks

the authority to issue the permit, the applicant does not qualify for the permit in the state, or the state

has “withheld approval” of the permit for more than one year.

While some regions have moved to develop capacity markets, discussed earlier, to ensure generation

adequacy, many states, particularly in areas where the traditionally regulated model remains, have

retained the IRP approach, which began in the late 1980s. Steps taken in an IRP include forecasting

future loads, identifying potential supply‐side and demand‐side resource options to meet those future

loads and their associated costs, determining the optimal mix of resources taking into account

transmission and other costs, receiving and responding to public participation (where applicable), and

creating and implementing a resource plan.

Innovation and the Levels of Research and Development Pursued

Innovations in the electric industry, technical and economic, have come about through the application of

research and development (R&D) of projects by the electric sector, governments, and other industrial,

communications, and technology sectors.

The expansion of combined heat and power and natural gas‐fired combined cycle plants in the late 1970s

into the 1990s was a strong contributing factor to growth in the class of non‐utility generation. The cost‐

effectiveness of smaller increments of generation has reduced the need for utilities to periodically have

large, “lumpy”, capital‐intensive investments and corresponding large additions to their rate base.

Moreover, since generation can be added in smaller increments and with lead times closer to the time of

anticipated need, the investment cycle has become smoother. This benefits both traditional and

competitive market entities.

Demand‐side management (DSM)‐induced reductions in load growth reduce or defer the need for new

generation plant investment and the costs of the DSM alternatives may be less than the cost of new

generation. Centralized market regions are gradually implementing market rules that seek to place

supply‐ and demand‐side options on equal footing with respect to bidding into capacity and energy

markets. Traditionally regulated regions seek to maintain equal footing for these two types of options

through integrated resource plans vetted by state regulators.

In the last decade, or less, the Smart Grid has become a hot topic in political and academic circles as well

as other groups not traditionally involved in the regular processes of the electric sector. The expectation

© 2013 Navigant Consulting, Inc. Page viii October 8, 2013

is that Smart Grid implementation will generate potential savings to customers by providing them the

tools to manage their energy consumption habits and costs, as well as providing potential savings to

utilities and their customers through operating efficiencies. Utilities in both models would benefit from

savings. Similarly, customers can benefit from smart meters and usage information under both models.

R&D investment by electric utilities (including their contributions to the Electric Power Research

Institute) is small when compared to other industrial sectors and when observed in the context of the

role electricity plays in our national economy and society. However, historically, electric equipment

manufacturers have provided the majority of the R&D in the sector; this is primarily because utilities

cannot necessarily internalize the benefits of the innovations developed through R&D. No study has

definitively assessed the impact of restructuring efforts on R&D investment in the electricity industry.

However, several studies have noted a decline in R&D investment in some areas and concluded that

utility restructuring is the likely cause. However, there are also studies that have concluded that the

centralized market model encourages more innovation than the traditionally regulated model.5

State and Federal Government

The electric utility industry in the United States is regulated at the state and federal levels. State

regulation extends to most areas of utility operations, rates, and end‐user issues. Federal regulation,

founded on interstate commerce impacts, generally relates to the wholesale side of the utility business,

including interstate transmission and sales of electricity for resale. State and Federal jurisdiction over

transmission siting, resource adequacy and transmission security planning, and electric reliability have

been discussed above.

Investor‐owned utilities are subject to state regulation as to their duties to customers, system

requirements, financing arrangements, and retail rates. Government‐owned utilities and rural electric

cooperatives are not generally subject to regulation under state utility laws, but must follow the

requirements of the ordinance or law establishing them and have governing boards that provide

oversight.

Under both the traditionally regulated model and the centralized market model, interstate transmission

rates are approved by FERC and FERC regulates the interstate transmission and generation activities of

“public utilities.” FERC does not regulate government‐owned utilities or most cooperatives, which are

often referred to as “non‐jurisdictional” entities. In addition, because most of the Texas transmission

grid is not interconnected with the rest of the interstate transmission grid, Texas is not subject to FERC

rate regulation. In Texas, the state regulator is responsible for approving transmission rates (because

Texas transmission is intrastate) as well as regulating all other aspects of the electric utility business in

Texas.

While FERC’s regulatory reach is not absolute, FERC has effectively extended many of its regulations to

non‐jurisdictional utilities through reciprocity. For example, if a non‐jurisdictional utility wants to take

advantage of the terms of a public utility’s Open Access Transmission Tariff (OATT), then it must itself

have an OATT where the terms of service other than rates must comply with FERC requirements.

5 These studies are discussed in greater detail in section 9.4.

© 2013 Navigant Consulting, Inc. Page ix October 8, 2013

Similarly, in order to be part of the regional planning process and to take advantage of proposed cost

allocation mechanisms, FERC has said that non‐jurisdictional entities have to agree to participate in the

FERC‐regulated planning processes and be subject to the outcome of these processes.

© 2013 Navigant Consulting, Inc. Page 1 October 8, 2013

2. Introduction

This paper explores the key policy questions surrounding two broad regulatory/market structures that

currently exist in the United States in varying degrees: traditional utility regulation without centralized

markets on the one hand, and centralized electricity markets, often involving restructured regulation, on

the other. The latter structure also generally involves the existence of a Regional Transmission

Organization (RTO) or Independent System Operator (ISO).

This paper provides a brief history of regulation and competition in the electric industry and identifies

the issues that characterize the key differences between the two major regulatory/market structures,

which for ease of reference are being called a “traditionally regulated” model and a “centralized market”

model.6 The paper is intended as an educational piece for non‐industry experts on how and why electric

utility regulation has evolved and centralized energy markets have developed in some areas of the

country and not in others. It focuses on consumer impacts and discusses how various issues are

addressed under the two broad models as well as identifying ongoing issues and challenges. This paper

does not provide a critique of the models nor a quantitative comparison between the two models.

A secondary purpose of the paper is to serve as a foundation for identifying the issues that characterize

the key differences between the two regulatory/market structures that will help guide decisions on

future research projects for the Electric Market Research Foundation (EMRF) to meet its goal of

informing the public policy debate on the pros and cons of the major market structures.

6 Within the two different general models there are further distinctions. The traditionally regulated model is often

characterized at the wholesale level by bilateral resource transactions while at the retail level the traditional

vertically integrated utility provides / purchases all functions required to provide service to the end users. The

centralized market model generally involves the existence of a Regional Transmission Organization (RTO) or

Independent System Operator (ISO) that administer centralized, bid‐based markets at the wholesale level with some

degree of retail competition where the customer has the right to procure power competitively with transmission and

distribution service provided by a regulated utility. Transmission and distribution under both models remains

governed by a cost of service regulatory approach. Further, the reader should be aware that there may be instances

where regions or entities generally characterized as functioning under a certain broad model may not exhibit all

features of that model. For example, there are regions that have centralized wholesale energy markets that may not

have implemented retail choice in all states within the region. Similarly, there are regions that remain traditionally

regulated but have elements of centralized markets and retail choice.

© 2013 Navigant Consulting, Inc. Page 2 October 8, 2013

3. History and Development of Traditional Regulation and Competitive Markets

The evolution of the U.S. electric industry is a history of adaptation to changes in the operating and

regulatory environment. During times of significant economic and technological change, policymakers

adapted regulatory policy to ensure the public interest continued to be served, economic principles of

efficiency and competition were advanced, and the reliable and efficient delivery of electric service to

consumers was maintained. The decisions made by regulators and policymakers shaped the two

regulatory paths that have emerged—traditional rate making based on cost of service regulation and

centralized market development. Today, both of these approaches co‐exist and continue to evolve to

meet changing economic and technological challenges.

The allocation of regulatory authority between the federal government and the states is distinguished by

what constitutes interstate commerce and what constitutes intrastate commerce.7 Furthermore, there is

the preemptive effect of federal wholesale rate orders on state retail rate authority.8 This dichotomy has

resulted in a number of distinctions among industry participants as to whether they are subject to

federal, state or both federal and state regulation by virtue of how they are organized and whether they

operate within a single state. Further, distinctions as to the applicability of federal vs. state regulation

turn on which specific physical and functional components of the electric system (e.g., generation,

transmission, distribution, and customer service) are in question.

The sections that follow describe, from the early beginning to present day, the key events that

transformed approaches in electric regulation policy and the evolving approaches designed by

regulators and policymakers on both the federal and state levels to meet those challenges.

7 See also, New York v. FERC, 535 U.S. 1 (2002). The court acknowledged that FERC correctly could choose not to

regulate the transmission component of bundled retail sales. Bundled sales are sales that combine energy and

transmission service as a single unit. 8 Under the Narragansett line of cases, Narragansett Elec. Co. v. Burke, 381 A.2d 1358 (1977), cert. denied, 435 U.S. 972

(1978), comprising what is now called the ʺfiled rate doctrine,ʺ state regulators must treat a utilityʹs FERC‐approved

wholesale power costs as reasonable operating expenses in the companyʹs retail cost of service. In other words, the

retail regulator cannot, in its retail rate hearing, question the reasonableness of the wholesale rate that the FERC has

fixed.

© 2013 Navigant Consulting, Inc. Page 3 October 8, 2013

3.1 Development of Traditionally Regulated Markets

Figure 1. Historical Timeline 1920‐19459

The early structure of the electric utility industry developed around the concept of a central source of

power supplied by efficient, low‐cost utility generation, transmission, and distribution. Regulation of

utilities began in the late nineteenth century, with municipalities issuing franchises, often overlapping,

as a method of regulation, promoting competition between utilities. This regulatory oversight derived

from a series of nineteenth century court decisions in the U.S. that held industries such as grain

elevators, warehouses, and canals were “monopoly” providers of service “affected with the public

interest”7 and that their rates and terms of service could therefore be regulated.10 Municipal regulation

gave way to state regulation following the passage of laws in New York and Wisconsin developing

powerful state commissions.11

In the early part of the twentieth century, the electric industry evolved quickly through the creation,

growth, and consolidation of vertically integrated utilities. A rapid increase in electricity generation

encouraged growth and consolidation of the industry to achieve economies of scale, which resulted in an

expansion into more and more cities across wider geographic areas.12 During this period, vertically

integrated electric utilities produced approximately two‐fifths of the nationʹs electricity.13 Over time,

states granted these consolidated utilities monopoly franchises with exclusive service territories in

exchange for an obligation to serve customers within that territory at rates for service based on state‐

regulated, cost‐of‐service ratemaking.14 As utility service territories grew throughout the 1900s, state

9 Source: Navigant Consulting, Inc. 10 See Munn v. Illinois, 94 U.S. 113, 126 (1877). 11 There are alternative views of why the municipal regulation ended. The natural monopoly view is that state

regulation was necessary to distance the regulator from the local level and to enforce uniform regulation throughout

the jurisdiction. This view assumes that one firm can serve the market more cheaply than two or more firms and can

keep out rival firms by expanding output and lowering price when threatened. The alternative view was that the

move from municipal to state regulation was in the public interest. See R. Richard Geddes, A Historical Perspective

on Electric Utility Regulation, CATO REVIEW OF BUSINESS,

http://www.cato.org/sites/cato.org/files/serials/files/regulation/1992/1/v15n1‐8.pdf, at pp. 75‐77. 12 See U.S. Electric Power Industry ‐ Context and Structure, Analysis Group for Advanced Energy Economy

(November 2011) (“AEE Context and Structure”). 13 Energy Information Administration, The Changing Structure of the Electric Power Industry 2000: An Update

(October 2000) Part I, Chapter 2, pg. 5 (“EIA Changing Structure”). 14 See AEE Context and Structure.

© 2013 Navigant Consulting, Inc. Page 4 October 8, 2013

regulation of privately owned electric utilities increased. Among the first states to regulate electric

utilities were Georgia, New York, and Wisconsin, which established state public service commissions in

1907.15 These states were soon followed by more than 20 other states. Part of the justification for

exclusive service territories was that a single distribution system in an area was more efficient due to

economies of scope; competing distribution facilities on thoroughfares and in communities would

require redundant capital investment and expenditures.

Despite the lure of exclusive franchises, some areas were inevitably less attractive than others. This was

particularly true with respect to rural areas, where the progress of electrification was much slower than

in urban areas. The Rural Electrification Act was enacted to provide power to unserved, or underserved,

rural areas and gave rise to the advent of rural electric cooperatives in many areas of the U.S.

During the 1920s and the early years of the Depression, the public became disenchanted with privately

owned power and began to support the idea of government ownership of utilities, particularly

hydroelectric power facilities. This disenchantment resulted primarily from abuses imposed by holding

companies on utilities, and ultimately on their customers, causing the price of electricity to increase. A

fierce debate at the time was whether government‐owned hydroelectric power facilities could produce

power cheaply and sell it to publicly owned utilities for distribution. During the presidency of Franklin

D. Roosevelt (1933 to 1945), a number of these facilities were built, ushering in the beginning of publicly

owned power.16

The development of hydroelectric projects in the United States was coordinated under the Federal Water

Power Act in 1920. The act created the Federal Power Commission (FPC), now the Federal Energy

Regulatory Commission (FERC), as the licensing authority for these plants. The FPC also regulated the

interstate activities of the electric power and natural gas industries. The responsibility of the FPC was to

maintain just, reasonable, and nondiscriminatory rates to the consumer. In 1935 the law was renamed

the Federal Power Act (FPA), and the FPC’s regulatory jurisdiction was expanded to include all

interstate electricity transmission. The FPC was also given authority to regulate nonfederal hydropower

projects. The Federal Power Act is the core legislation providing federal jurisdiction over the electric and

natural gas industries and defining the responsibilities of the FERC.17 However, the FPA exempts

15 Energy Information Administration, Annual Outlook for U.S. Electric Power 1985, DOE/EIA‐0474(85) (August 1985),

pg. 3. 16 EIA Changing Structure, Part I, Chapter 2, pg. 6. As part of the program, President Roosevelt proposed that the

government build four hydropower projects and, within a year after his proposal, his administration began to

implement the projects.

Hoover Dam began generation in 1936, followed by other large projects.

Grand Coulee, the nation’s largest hydroelectric dam, began operation in 1941.

Under the Tennessee Valley Authority Act of 1933, the federal government supplied electric power to

states, counties, municipalities, and nonprofit cooperatives.

The Bonneville Project Act of 1937 pioneered the federal power marketing administrations.

From 1933 to 1941, one‐half of all new capacity was provided by federal and other public power installations. Public

power contributed 12 percent of total utility generation, with federal power alone contributing almost 7 percent. See

Id. It should be noted that the federal power generating entities were not subject to regulation by States. 17 See AEE Context and Structure.

© 2013 Navigant Consulting, Inc. Page 5 October 8, 2013

certain entities from many provisions of the Act, including entities in the state of Texas, which is a

single‐state Interconnection with no interstate transactions, as well as certain non‐public utilities (i.e.,

Municipal Utilities, Cooperatives, Power Marketing Administrations, and state authorities).18

After several large holding company systems collapsed, an investigation by the Federal Trade

Commission was ordered, leading eventually to the passage of the Public Utility Holding Company Act

of 1935 (PUHCA). PUHCA was aimed at breaking up the unconstrained and excessively large trusts

that then controlled the nationʹs electric and gas distribution networks.19

PUHCA gave the Securities and Exchange Commission (SEC) responsibility for regulating utility

holding companies. Under Title II of PUHCA, the FPC also regulated utilities involved in interstate

wholesale marketing or transmission of electric power.20 One of the most important features of the Act

was that the SEC was given the power to break up the large interstate holding companies by requiring

them to divest their holdings until each became a single consolidated system serving a circumscribed

geographic area. Another important feature of the law permitted holding companies to engage only in

business that was essential and appropriate for the operation of a single integrated utility.21

In the Supreme Court case of FPC v. Hope, the Court stated: “[t]he rate‐making process … i.e., the fixing

of ― just and reasonable rates, involves a balancing of the investor and the consumer interest.”22 This

balancing of consumer and investor interests evolved into what has become known as the regulatory

compact.23 In addition, Hope gave rise to an End Results Doctrine relating to rates. Under this doctrine,

only the end result – not the methodology – matters in determining whether rates are just and

reasonable.24

The regulatory compact is premised on the existence of a set of rights, obligations, and benefits that are

shared between utilities and their customers.25 In return for the grant of a franchise and the right to

recover its costs plus a market‐determined profit equal to the cost of debt and equity capital, the

18 Section 201(f) of the FPA generally exempts the United States, a state or any political subdivision of a state, an

electric cooperative that receives financing under the Rural Electrification Act of 1936 (7 U.S.C. 901 et seq.) or that

sells less than 4,000,000 megawatt‐hours of electricity per year from Part II of the FPA. However, it should be noted

that the reliability section of the FPA added under EPACT 2005 extends to entities that were described under 201(f)

of the FPA. See Federal Power Act § 215(b), 16 U.S.C §844o(b). 19 EIA Changing Structure, Part I, Chapter 4, pg. 29. 20 Ibid., Part I, Chapter 2, pg. 5. 21 Ibid., Part I, Chapter 4, pg. 29. 22 Federal Power Commission v. Hope Natural Gas Co., 320 U.S. 591, 603 (1944). 23 The concept of a regulatory compact is not that there is a formal agreement between the utility and government

but rather that the legal obligations of regulators and utilities have evolved through a long series of court decisions,

See RAP Publications, Electricity Regulation in the US: A Guide (March 2011) ,

www.raponline.org/document/download/id/645 , pp. 4-5. 24 Dr. Karl McDermott, Cost of Service Regulation In the Investor‐Owned Electric Utility Industry (June 2012), pg. 3

(“Cost of Service Regulation”). 25 Cost of Service Regulation, pg. vii.

© 2013 Navigant Consulting, Inc. Page 6 October 8, 2013

investor‐owned utility must submit to rate regulation and provide service efficiently.26 “The regulatory

compact has a two‐fold focus: (1) establish prices based on the actual prudent costs (i.e., avoid monopoly

pricing); and (2) provide incentives to maintain a reasonable level of efficiency in serving the

customers.”27

Under traditional utility regulation, this determination of the appropriate cost of service that can be

charged by the utility is determined through what developed as the rate case process, which examines

the prudency of costs after they are incurred.28 This form of regulation serves as an administrative

replacement for market mechanisms in determining what costs were efficient.29

3.2 Period of Growth and Declining Costs, 1945‐1970

Figure 2. Historical Timeline 1945‐197030

From the 1940s through the 1960s the industry saw extensive growth and increasing electricity

consumption. Economies of scale increased as new, larger generating units were built which drove

down costs, and stimulated an increased demand for electricity.31

Regulatory administration of the rate case process described above became routine during this period

and established the normal course of utility operations and funding. Utilities would provide service to

all customers in their franchise area and in return were guaranteed a reasonable return on their

investments determined through the rate case process. Both utilities and customers have benefited from

this relationship; utilities received a guaranteed service territory with a return on investment (ROI) and

customers received protection from monopoly pricing.

The rate case would establish rates based on the normal costs of providing service determined by the

revenue requirement. The utility had to work within a framework of regulatory lag, demand growth,

and cost instability in real‐time operations. Exposure to real‐time operations provided both a risk and

26 See Ibid. “The utility was obligated to supply service efficiently, but had the right to recover its costs, including an

opportunity to earn a return/profit equal to its market‐determined cost of debt and equity capital.” Ibid. 27 Ibid., pg. vii. 28 A rate case is a formal administrative process in which the utility provides support for its proposed cost of service

and the public, including the regulatory body, is provided the opportunity to scrutinize the data, policy arguments,

and any other relevant information. Ibid., pg. 12. 29 Ibid., pg. viii. 30 Source: Navigant Consulting, Inc. 31 Cost of Service Regulation, pg. ix.

© 2013 Navigant Consulting, Inc. Page 7 October 8, 2013

incentive. If the original assumptions remained fairly accurate, utilities would be able to operate fairly

successfully; however, if the assumptions proved to be incorrect, either the utility or the regulator would

seek adjustments.32

This worked well for most of this period, although the Northeast Blackout of 1965 raised pressing

concerns about reliability.

3.3 Slowed Growth and Inflation, Seeds of Competition, 1970‐1990

Figure 3. Historical Timeline 1970‐199033

A number of damaging events occurred in the 1970s that interrupted the growth that occurred in the

prior several decades. After the Northeast Blackout of 1965, state and regional power pools were created

or took on expanded roles. Many of these are the predecessors to today’s Regional Transmission

Organizations. In addition, regional, voluntary reliability councils were formed by the utilities in an

effort to enhance reliability and stave off regulation.

The passage of the Clean Air Act of 1970 and its amendments in 1977 required utilities to reduce their

emission of pollutants, raising their operating costs, particularly for utilities operating coal‐fired

generation. Probably the most significant event was the Oil Embargo of 1973‐1974, which resulted in

burdensome increases in fossil‐fuel prices due to transportation costs. Although the embargo lasted only

until March 1974, its effects increased public awareness of energy issues, resulted in higher energy

prices, and contributed to inflation.

The accident at Three Mile Island in 1979 led to higher costs, regulatory delays, and greater uncertainty

for companies pursuing nuclear generation. In general, inflation caused interest rates to more than

triple. The escalating fuel costs, reduction in demand growth, and accompanying unprecedented

inflation in labor, capital costs, and construction materials meant that utilities were not realizing the

incremental cash flows that had helped finance new construction in the past.34

In 1978, Congress pursued legislation intended to reduce U.S. dependence on foreign oil, develop

renewable and alternative energy sources, sustain economic growth, and encourage the efficient use of

32 Ibid., pg. 16. 33 Source: Navigant Consulting, Inc. 34 Cost of Service Regulation, pg. ix.

© 2013 Navigant Consulting, Inc. Page 8 October 8, 2013

fossil fuels.35 A greater reliance on market forces to set wholesale power costs was introduced through

the Public Utility Regulatory Policies Act of 1978 (PURPA), which adopted avoided cost pricing for

energy purchased by utilities from certain types of third‐party suppliers.36 PURPA became a catalyst for

competition in the electricity supply industry, because it allowed nonutility facilities that met certain

ownership, operating, and energy efficiency criteria established by FERC (referred to as “qualifying

facilities” or “QFs”), to enter the wholesale market.37 Utilities did not initially welcome this forced

competition.38 The QFs themselves are not subject to cost‐of‐service regulation, and the prices paid to

them are not based on their cost of producing the electricity.39 Instead, the prices they are paid reflect

the avoided cost of the purchasing utility (generally determined by the utility’s regulatory authority),

that is, the cost the utility avoided by not producing the electricity received from the QF or purchasing it

from another source.40 In some cases utility regulatory authorities set an avoided cost that was very high

leading to financial problems for utilities that were forced to pay these high prices.

The economic challenges of the 1970s fed directly into the 1980s. Demand growth continued to be slow.

The beginning of the decade saw high inflation in the cost of construction materials and labor along with

double‐digit financing rates. This led to dramatic cost overruns in coal and nuclear plants under

construction. In the wake of the Three Mile Island accident in 1979, the cost to complete nuclear plants

under construction soared as new safety requirements came into play. Some plants (nuclear and non‐

nuclear) were cancelled before completion. These factors led to increased utility costs for plants that

were ultimately cancelled and substantial rate shocks for plants that were completed and entered the

rate base. Regulators responded to the challenge of construction cost overruns by expanding their

oversight of the prudence of project costs. The number of rate cases expanded dramatically from the few

dozen major prudence cases between 1945 and 1975 to over 50 during the 1975 through 1985 period.41

In addition, regulators, public interest groups, and utilities began to recognize in the late 1970s and early

1980s that actions taken to promote conservation and demand‐side management (DSM) could be less

costly under some conditions than construction of new power plants. While the economic conditions

that supported the premise that incremental costs of DSM could be less than the incremental costs of

new generation were reversed during an era of lowered natural gas prices later, new state and federal

35 EIA Changing Structure, Part I, Chapter 2, pg. 8. 36 Cost of Service Regulation, pg. 24. 37 EIA Changing Structure at Part I, Chapter 2, pg. 8. 38 Ibid., Part I, Chapter 2, pg. 8. PURPA defined a new class of energy producers called qualifying facilities. These

producers are either small‐scale producers of commercial energy who normally self‐generate energy for their own

needs but may have surplus energy, or incidental producers who happen to generate usable electric energy as a by‐

product of other activities. When a facility of this type meets the requirements for ownership, size and efficiency,

utility companies are obliged to purchase their energy based on a pricing structure referred to as avoided cost rates.

These rates tend to be highly favorable to the producer, and are intended to encourage more production of this type

of energy as a means of reducing emissions and dependence on other sources of energy. See AEE Context and

Structure. 39 EIA Changing Structure, Part I, Chapter 4, pg. 32. 40 Ibid. at Part I, Chapter 4, pg. 32. 41 Cost of Service Regulation, pg. 25.

© 2013 Navigant Consulting, Inc. Page 9 October 8, 2013

regulations or conservation programs introduced the retail customer class to much greater involvement

in utility planning than had existed before.

An immediate impact on regulators‘ thinking was that there was a need to plan to avoid these situations

and to search for smaller increments of supply or demand reductions. The least cost utility planning and

Integrated Resource Planning (IRP) processes were part of the response to this need.42

These processes were designed to take into account a broad range of information and alternatives,

produce demand forecasts in a public process, and attempt to evaluate supply and demand options on

an equal footing. Much of the late 1980s saw efforts to establish more effective formal planning

frameworks in an attempt to avoid the mistakes that occurred in the 1970s. Regulators embraced this

process to varying degrees, attempting to integrate the planning and rate case sequences together in a

way that reinforced both from an information and implementation perspective.

Another significant development in the late 1980s was an increased utility interest in selling their

generation in wholesale transactions. This was prompted by excess capacity in the early 90s that

occurred because load growth did not meet projected levels. FERC began allowing utilities to sell power

at market based rates (as compared to cost‐based) if the utility could show it had no power to set prices

in the market, would cap the rates at avoided cost, or would provide non‐discriminatory transmission

access to competitive generators.43 This form of regulatory rate treatment was viewed by many in the

industry as superior to the risk of building a new unit under traditional regulation at the state level.44 By

1991, FERC had received 40 of these market‐based pricing requests.45

3.4 The Advent of Centralized Markets, 1990‐1999

Figure 4. Historical Timeline 1990‐199946

42 Ibid., pg. 26. 43 Ibid., pg. 30‐31. 44 Cost of Service Regulation, pg. 31. “The move to greater reliance on markets was accelerated by FERC‘s 1988 pre‐

construction rate approval in Ocean States Power as well as the notice of proposed rulemakings on market based

pricing of electricity. All of these factors were layered on top of the incentive provided for non‐utility generation by

PURPA.” Ibid., pg. 30. 45 Ibid., pg. 31. 46 Source: Navigant Consulting, Inc.

© 2013 Navigant Consulting, Inc. Page 10 October 8, 2013

Passage of the federal Energy Policy Act of 1992 (EPACT) was a significant enabler of market

development. First, it created a new class of electric suppliers, the exempt wholesale generator (EWG),

extending the trend started by FERC with the market‐based rate policy and open access to the

transmission system.47

Like QFs, EWGs were wholesale producers that did not sell electricity in the retail market and did not

own transmission facilities.48 Unlike the non‐utilities that qualified under PURPA, EWGs were not

regulated and could charge market‐based rates.49 The growth of EWGs marked another step toward

increasing the level of competition in the wholesale electricity market.

Marketing of EWG power was facilitated by transmission provisions in EPACT 1992 that gave FERC the

authority to order utilities to provide access to their transmission systems to utilities and non‐utilities.50

In addition, EPACT 1992 required states to conduct an IRP process and evaluate the impact of purchased

power contracts on the local distribution company.51 Some states took this even further, taking steps to

break up the vertical integration of utilities within those states, to introduce retail competition.52

The second cornerstone in the creation of competitive wholesale power markets came in 1996 through

FERC’s Order No. 888.53 At that time, Order No. 888 was considered the most far‐reaching and

ambitious project undertaken by FERC to eliminate impediments to wholesale competition in the electric

power industry.54 Order No. 888 had two basic goals: (1) to eliminate anti‐competitive practices and

undue discrimination in transmission services through a universally applied, open‐access transmission

47 Cost of Service Regulation, pg. 32. 48 EIA Changing Structure, Part I, Chapter 2, pg. 8. The Commission ceased making case‐by‐case determinations of

exempt wholesale generator status following the enactment of EPACT 2005 calling for the repeal of PUHCA. See

Repeal of the Public Utility Holding Company Act of 1935 and Enactment of the Public Utility Holding Company

Act of 2005, Docket No. RM05‐32‐000, (Sept. 2005) at P 21. 49 49 EIA Changing Structure at Part I, Chapter 2, pg. 8. 50 Ibid., Part I, Chapter 4, pg. 33. 51 Cost of Service Regulation, pg. 32. 52 See AEE Context and Structure. 53 The actions taken by the Commission in Order No. 888 paralleled and in many instances were guided by Gas

Restructuring, Order No. 636, open‐access transport in gas. 54 EIA Changing Structure, Part II, Chapter 7, pg. 64.

© 2013 Navigant Consulting, Inc. Page 11 October 8, 2013

tariff, and (2) to ensure the recovery of stranded costs55 a utility might accrue in the transition to

competitive markets.56

Another equally important component of Order No. 888 was the requirement for transmission owners to

functionally unbundle their services. Functional unbundling required the transmission owner to take

transmission service under the same tariff as other transmission users under a comparability standard.

They were required to separate rates for wholesale generation, transmission, and ancillary services and

to rely on the same electronic information network that its transmission customers relied on to obtain

information about prices and available capacity of the transmission system. The concept of unbundling

was to preclude the appearance of possible favoritism and discriminatory practices within a vertically

integrated utility by separating its transmission services functions from other business activities in the

company and by requiring utilities to provide transmission service to others for wholesale transactions

in the same manner as they provide it to themselves.57

Accompanying the requirement for non‐discriminatory access to the transmission system, timely and

accurate day‐to‐day information about transmission was also made available to all transmission users.58

Order No. 889 required all investor‐owned utilities (IOUs) to participate in the Open Access Same‐Time

Information System (OASIS), which facilitated the functioning of competitive power markets.59 At the same time these changes were occurring in the wholesale electricity markets, a growing number

of states were also pursuing a reliance on competitive markets for the retail supply of electric power.

Retail choice was introduced in the United States in the 1990s in response to high regulated prices in

some regions. As noted, excess generation capacity was triggered by the generation construction cycle

that began in the 1960s and continued into the 1970s. Consumer groups in some regions found retail