Embed Size (px)

Citation preview

Prepared for:

CMAG

Lee Shupp

Kathleen Chattin

Leigh Marriner

Joanne Mendel

CheskinGuiding clients to innovative solutions

Date: March 2008

Cheskin Added Value255 Shoreline Dr., Suite 350Redwood Shores, CA 94065650-802-2100

2

© Cheskin 2007

Cheskin is a consulting firm

that guides innovation

through its deep understanding

of people, culture, and change.

Who is Cheskin?

Additional information and several relevant case

studies can be found at www.cheskin.com

3

© 2008 Cheskin Added Value

Cheskin Overview

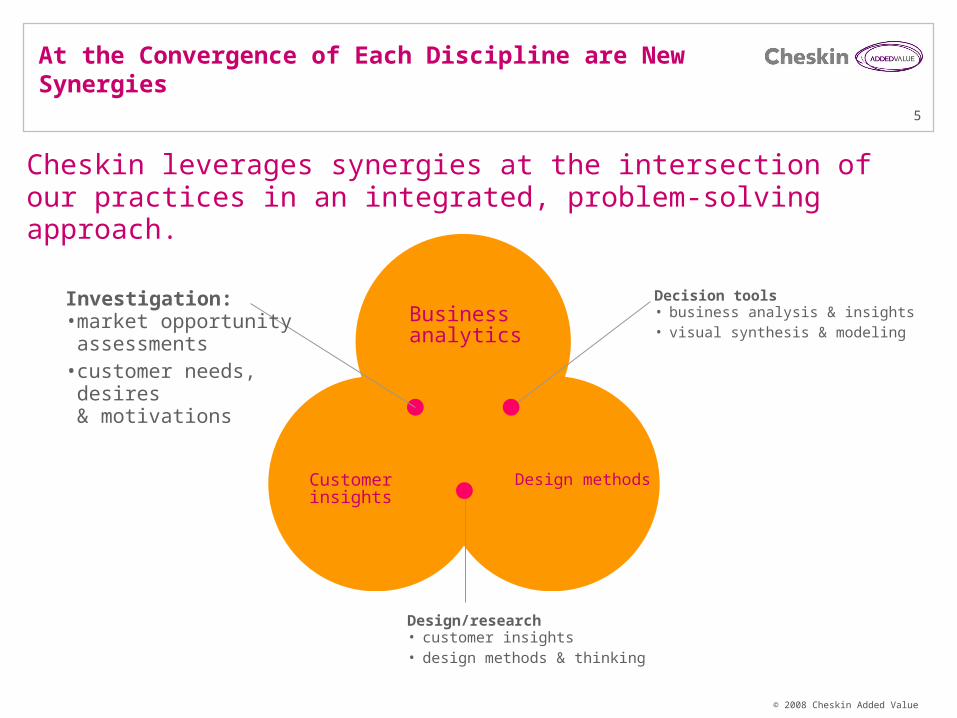

Integrating disciplines for innovative solutionsCheskin is an innovation consulting firm that offers a unique and powerful combination of disciplines and offerings.

As an integrated approach, these synergies deliver results far greater than the sum of their parts.

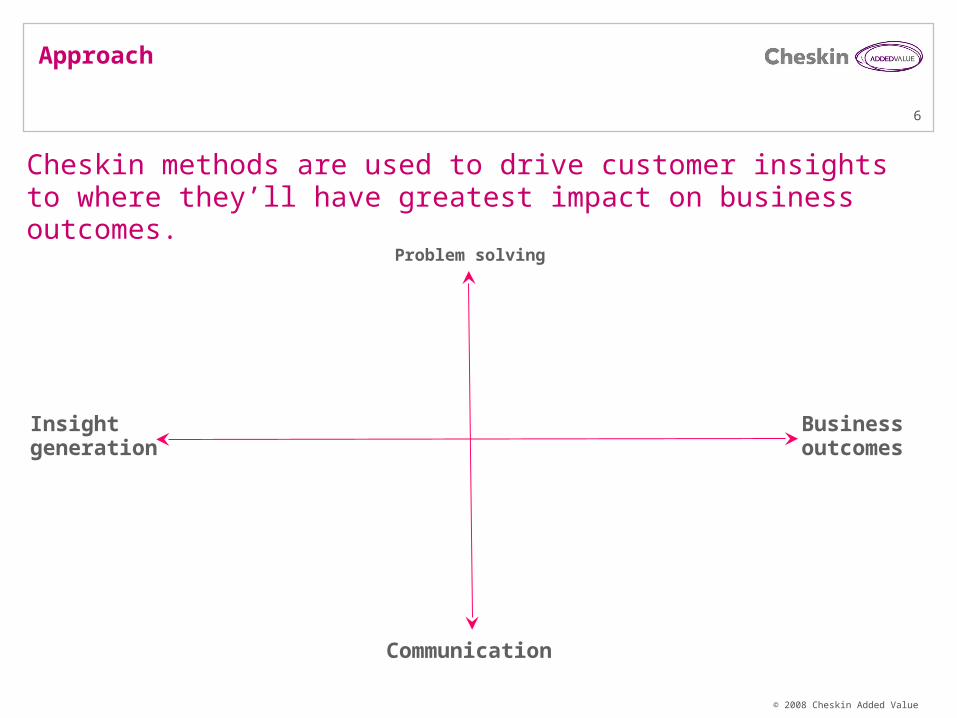

Cheskin methods are used to drive customer insights to where they’ll have greatest impact on business outcomes.

Design methods

Business analytics

Customer insights

Innovation consulting

4

© 2008 Cheskin Added Value

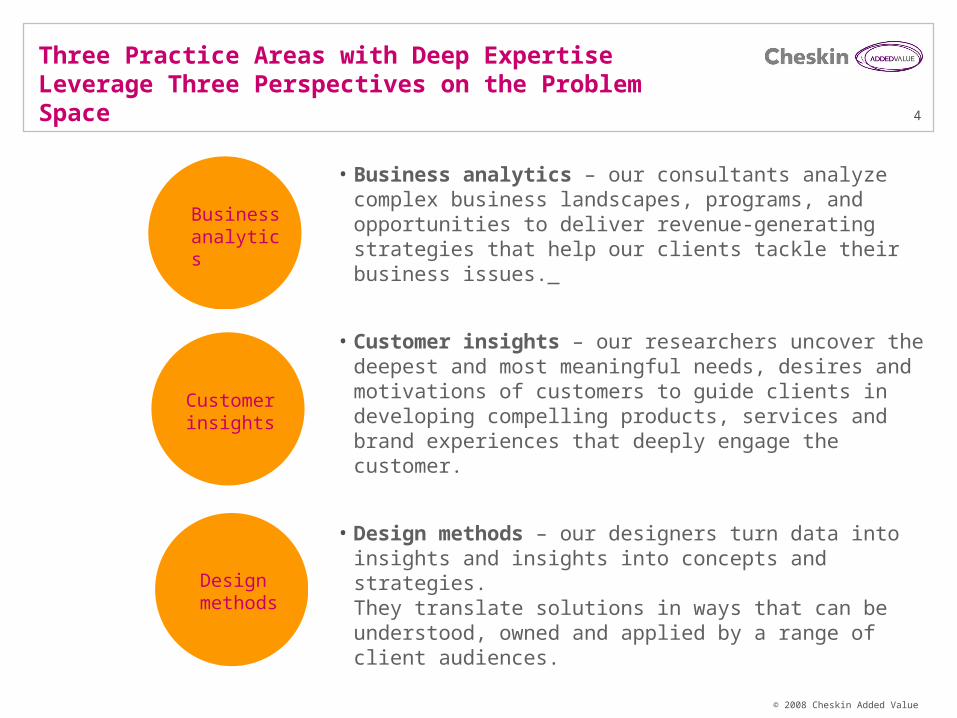

Three Practice Areas with Deep Expertise Leverage Three Perspectives on the Problem Space

• Business analytics – our consultants analyze complex business landscapes, programs, and opportunities to deliver revenue-generating strategies that help our clients tackle their business issues.

• Customer insights – our researchers uncover the deepest and most meaningful needs, desires and motivations of customers to guide clients in developing compelling products, services and brand experiences that deeply engage the customer.

• Design methods – our designers turn data into insights and insights into concepts and strategies. They translate solutions in ways that can be understood, owned and applied by a range of client audiences.

Designmethods

Customer insights

Business analytics

5

© 2008 Cheskin Added Value

At the Convergence of Each Discipline are New Synergies

Design methods

Business analytics

Customer insights

Design/research• customer insights• design methods & thinking

Cheskin leverages synergies at the intersection of our practices in an integrated, problem-solving approach.

Decision tools• business analysis & insights• visual synthesis & modeling

Investigation:• market opportunity

assessments• customer needs, desires

& motivations

6

© 2008 Cheskin Added Value

Approach

Cheskin methods are used to drive customer insights to where they’ll have greatest impact on business outcomes.

Business outcomes

Problem solving

Communication

Insightgeneration

7

© 2008 Cheskin Added Value

Approach

Systems thinking

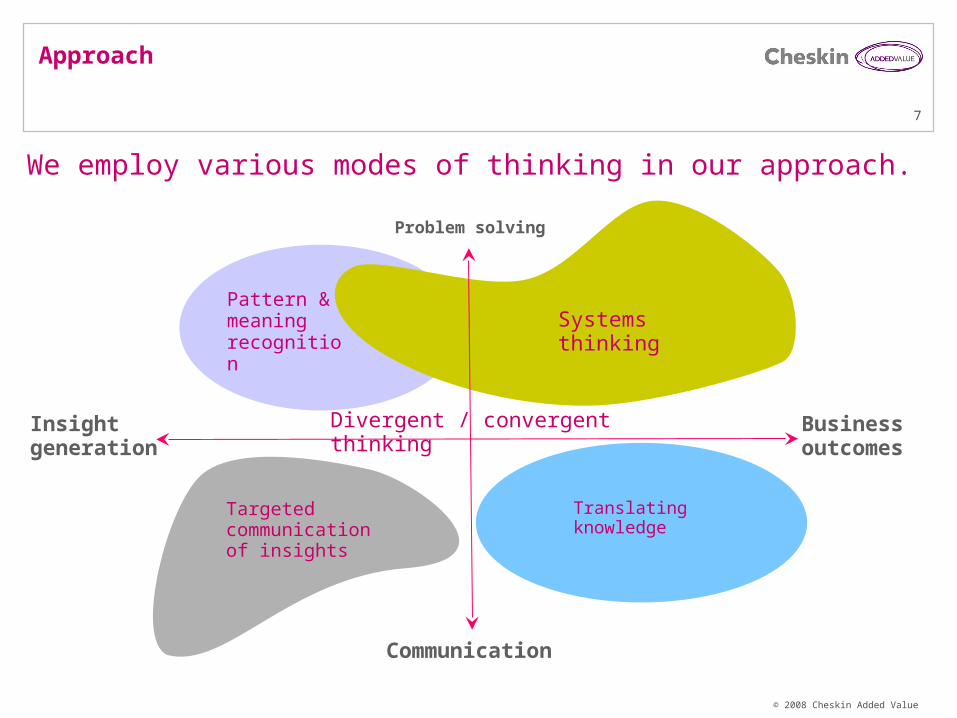

We employ various modes of thinking in our approach.

Business outcomes

Problem solving

Communication

Insightgeneration

Pattern & meaning recognition

Targeted communication of insights

Translatingknowledge

Divergent / convergent thinking

8

© 2008 Cheskin Added Value

Approach

Systems thinking

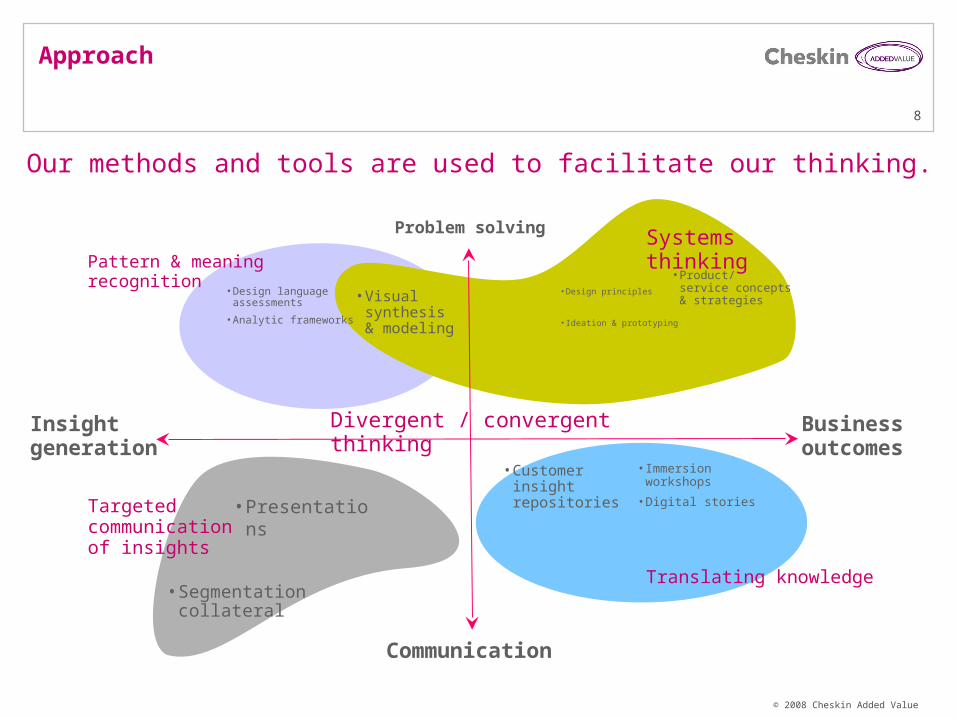

Our methods and tools are used to facilitate our thinking.

Business outcomes

Communication

• Design language assessments

• Analytic frameworks

Insightgeneration

• Segmentation collateral

• Presentations

• Visual synthesis & modeling

• Design principles

• Ideation & prototyping

• Immersion workshops

• Digital stories

• Customer insight repositories

Pattern & meaning recognition

Targeted communication of insights

• Product/service concepts & strategies

Translating knowledge

Divergent / convergent thinking

Problem solving

© 2008 Cheskin Added Value

Case study Should we become a content provider?

24

10

© 2008 Cheskin Added Value

The Challenge

A high tech company came to us to help refine their approach to enter the TV & movie content business• They assumed it was a large market

• And that they could enter it fairly easily

• Our work helped them understand the real size of this opportunity and the barriers to entry

11

© 2008 Cheskin Added Value

Insights from Business Analysis

What’s happening at the broad business level? • Delivery channels & advertisers are battling for

viewership

• Service providers (cable, satellite & telcos) are battling to own connection to the home

• Equipment makers & Service Providers are battling to control the home

Businessanalytics

12

© 2008 Cheskin Added Value

Customer Insights

What’s happening with consumers?

• Companies are battling to establish themselves as the hub, expected to be the focus of consumer attention

• Two audience segments present opportunities for client.

• They discover, evaluate, avoid, select/acquire, watch and store, and return, share, content for different reasons.

Customerinsights

13

© 2008 Cheskin Added Value

“Stories” were created by synthesizing insights from a market opportunity assessment with consumer insights

Partnerships, Competitors, Triple & Quad plays among Cable, Satellite & Telcos

Video: Cable vs. Teleos break into the TV market

MOAp 25

MOAp 24-26

What’s occurring at the broad business level? Service providers (cable, satellite & telcos) are battling to own connection to the home

Designmethods

14

© 2008 Cheskin Added Value

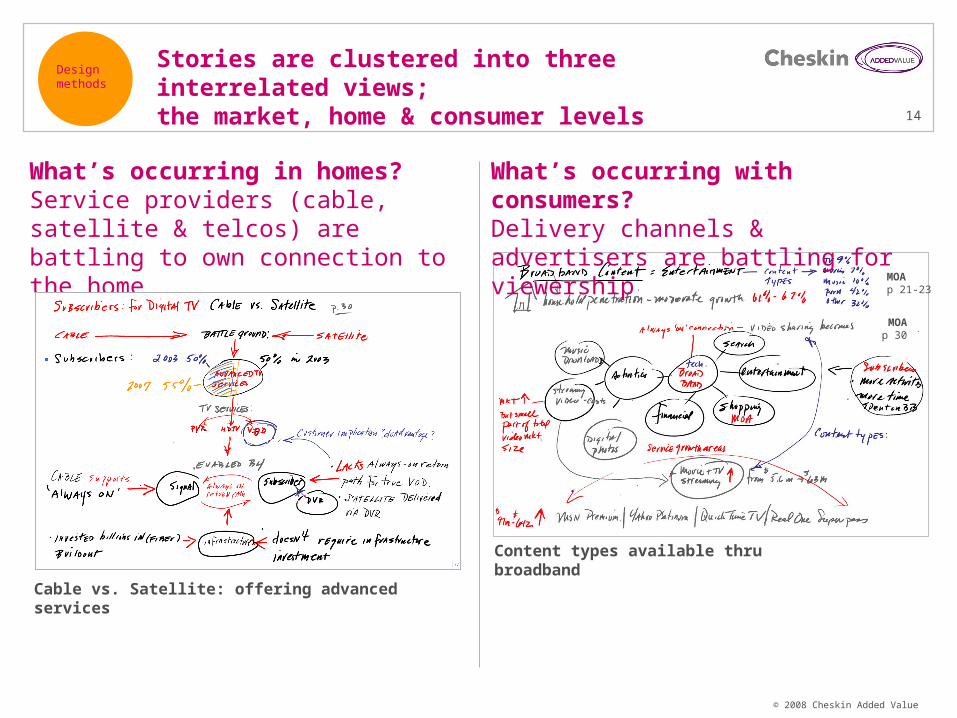

Stories are clustered into three interrelated views; the market, home & consumer levels

Content types available thru broadband

MOAp 21-23

What’s occurring with consumers?Delivery channels & advertisers are battling for viewership

What’s occurring in homes?Service providers (cable, satellite & telcos) are battling to own connection to the home

Cable vs. Satellite: offering advanced services

MOAp 30

Designmethods

15

© 2008 Cheskin Added Value

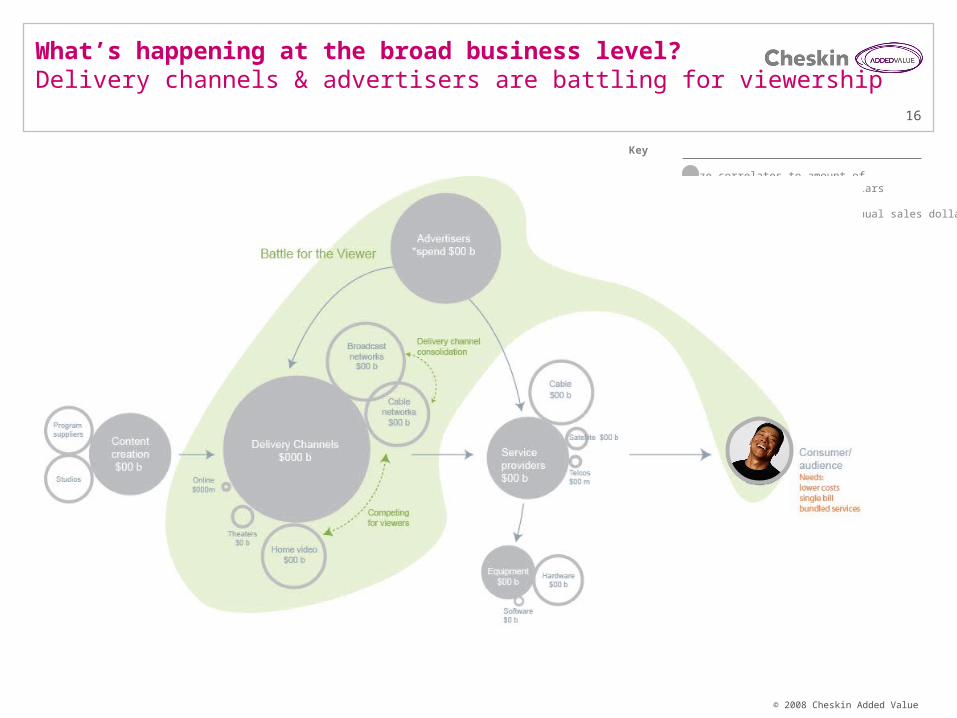

TV Movies landscape From content creation through delivery to the consumer

Key

Size correlates to amount of aggregated annual sales dollars

Size correlates to amount annual sales dollars

* Advertising dollars spent

Designmethods

Businessanalytics

Customerinsights

16

© 2008 Cheskin Added Value

What’s happening at the broad business level? Delivery channels & advertisers are battling for viewership

Key

Size correlates to amount of aggregated annual sales dollars

Size correlates to amount annual sales dollars

* Advertising dollars spent

17

© 2008 Cheskin Added Value

Key

Size correlates to amount of aggregated annual sales dollars

Size correlates to amount annual sales dollars

* Advertising dollars spent

What’s happening at the broad business level? Service providers (cable, satellite & telcos) are battling to own the connection to the home

18

© 2008 Cheskin Added Value

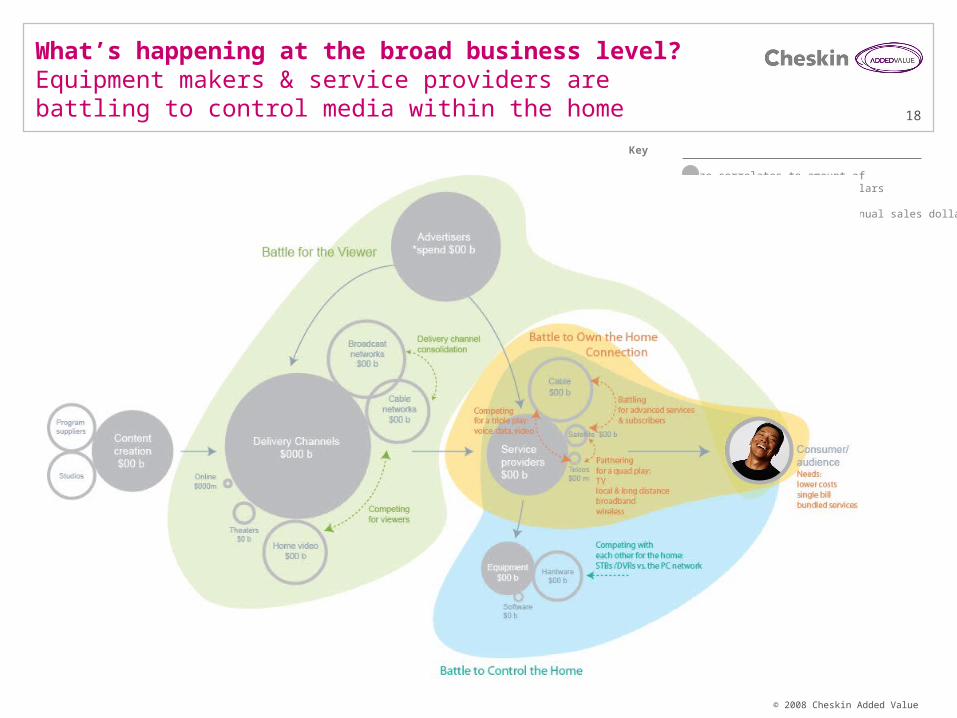

What’s happening at the broad business level? Equipment makers & service providers are battling to control media within the home

Key

Size correlates to amount of aggregated annual sales dollars

Size correlates to amount annual sales dollars

* Advertising dollars spent

19

© 2008 Cheskin Added Value

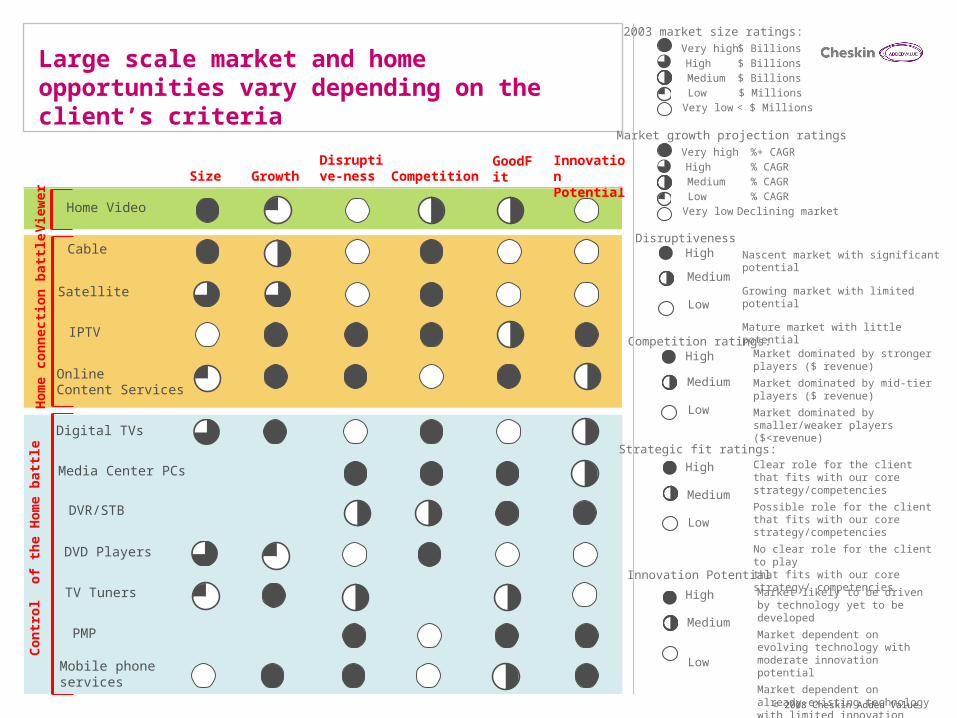

Large scale market and home opportunities vary depending on the client’s criteria

IPTV

Home Video

DVD Players

Mobile phone services

TV Tuners

DVR/STB

Size GrowthGoodFit

Disruptive-ness

Innovation PotentialCompetition

Cable

Satellite

Online Content Services

Digital TVs

Media Center PCs

PMP

2003 market size ratings:Very high $ BillionsHigh $ BillionsMedium $ BillionsLow $ MillionsVery low < $ Millions

Market growth projection ratingsVery high %+ CAGRHigh % CAGRMedium % CAGRLow % CAGRVery low Declining market

DisruptivenessHigh Nascent market with significant potential

Growing market with limited potential

Mature market with little potential

Medium

Low

Competition ratings:High Market dominated by stronger players

($ revenue)

Market dominated by mid-tier players ($ revenue)

Market dominated by smaller/weaker players ($<revenue)

Medium

Low

Strategic fit ratings:

High Clear role for the client that fits with our core strategy/competencies

Possible role for the client that fits with our core strategy/competencies

No clear role for the client to play that fits with our core strategy/ competencies

Medium

Low

Innovation Potential

High Market likely to be driven by technology yet to be developed

Market dependent on evolving technology with moderate innovation potential

Market dependent on already-existing technology with limited innovation potential

Medium

Low

Co

ntr

ol

of

the

Ho

me

bat

tle

Ho

me

con

nec

tio

n b

attl

eV

iew

er

20

© 2008 Cheskin Added Value

Opportunity generation framework used in an executive work session

21

© 2008 Cheskin Added Value

Value to Client – Saved $MM!

These integrated insights directly guided client’s decision to forego this space, saving hundreds of millions in development costs• Saved $$ that would have been spent to enter this

market

• Re-focused team on better opportunities

• Re-directed engineering resources to more profitable areas

© 2008 Cheskin Added Value

Contacts

24

23

© 2008 Cheskin Added Value

Contacts

Lee ShuppEVP Technology PracticeOffice: 650.596.6218Cell: 415.336.3558 [email protected]

Kathleen ChattinDirector, Account ManagementOffice: 650.802.2100Cell: [email protected]

24

© 2008 Cheskin Added Value

Contacts

Leigh MarrinerSr. Director, Business ConsultingOffice: 650.802.2100Cell: [email protected]

Joanne MendelDesign Methods Studio LeaderOffice Phone: 650.802.2100Cell: 415.637.4492Email: [email protected]

Cheskin website www.Cheskin.com

© 2008 Cheskin Added Value

Thank You

24

© 2008 Cheskin Added Value

Appendix

24