Embed Size (px)

Citation preview

Prentice Hall © 2005 1

PowerPoint Slides to accompanyThe Legal Environment of Business

and Online Commerce 4E, by Henry R. Cheeseman

Chapter 24Negotiable Instruments, Credit, and Bankruptcy

Prentice Hall © 2005 2

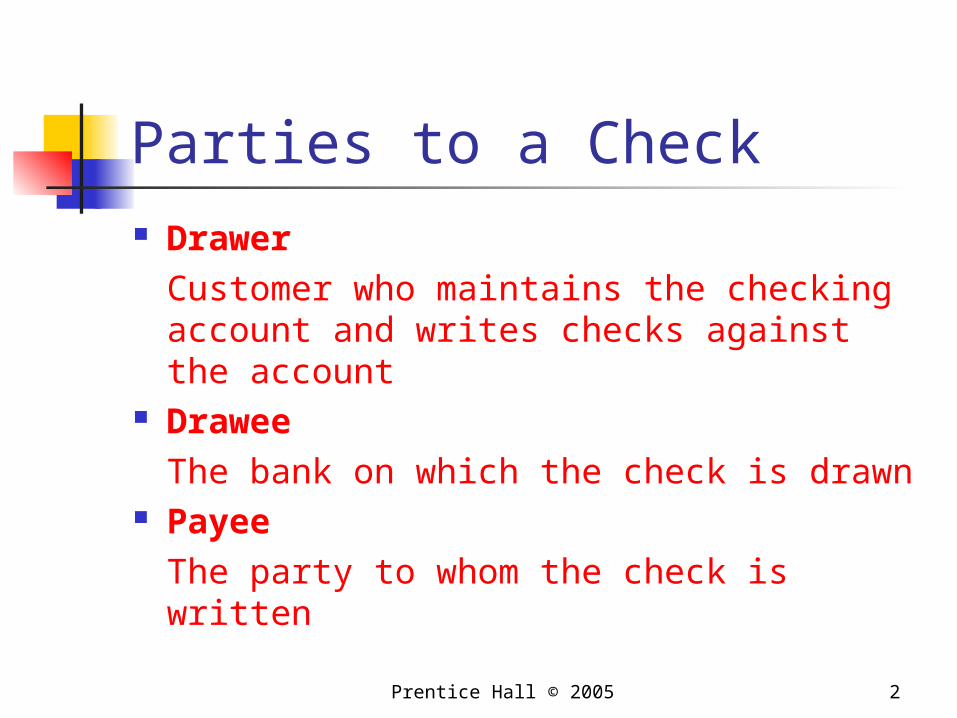

Parties to a Check Drawer

Customer who maintains the checking account and writes checks against the account

DraweeThe bank on which the check is drawn

PayeeThe party to whom the check is written

Prentice Hall © 2005 3

Electronic Funds Transfer Systems Automated teller

machines Point-of-sale

terminals Direct deposits

and withdrawals Pay-by-telephone

systems

Prentice Hall © 2005 4

Special Types of Checks

Certified checks Cashier’s checks Traveler’s checks

Prentice Hall © 2005 5

Honoring Checks Stale checks

A check that has been outstanding for more than six months Incomplete checks Death or incompetence of the drawer Stop-payment orders

An order by a drawer of a check to the payor bank not to pay or certify a check

Overdrafts The amount of money a drawer owes a bank after it has paid

a check despite insufficient funds in the drawer’s account Wrongful dishonor

Occurs when there are sufficient funds in a drawer’s account to pay a properly payable check, but the bank does not pay the check

Prentice Hall © 2005 6

Forged Signatures and Altered Checks

Forged instrument Is wholly

inoperative as the signature of the drawer

Is not properly payable

Altered check A check that has

been altered without authorization that modifies the legal obligation of a party

Prentice Hall © 2005 7

Check Collection Process

Coun tryB an k

C ityB an k

M etroB an k

P ayee

D rawer

Drawer issues a check to Payee drawn on Country Bank

Payee deposits the check into his account at Metro Bank

Metro Bank sends the check to City Bank for collection

City Bank sends the check to Country Bank for collection

Drawer has a checking account at Country Bank

Prentice Hall © 2005 8

Final Settlement Occurs when the payor bank

Pays the check in cash Settles for the check without having a

right to revoke the settlement Fails to dishonor the check within

certain statutory time periods

Prentice Hall © 2005 9

“On Us” v. “On Them” Checks “On us”

A check that is presented for payment where the depository bank is also the payor bank, i.e., the drawer and payee or holder have accounts at the same bank

“On them” A check presented

for payment by the payee or holder where the depository bank and payor bank are not the same bank

Prentice Hall © 2005 10

“Four Legals” that Prevent Payment of a Check

Receipt of a notice affecting the account Receipt of service or a court order of other

legal process that freezes the customer’s account

Receipt of a stop-payment order from the drawer

Payor bank’s exercise of its right of setoff against the customer’s account

Prentice Hall © 2005 11

Types of Credit Unsecured credit

Credit that does not require any security (collateral) to protect the payment of the debt

Secured credit Credit that

requires security (collateral) to secure payment of the loan

Prentice Hall © 2005 12

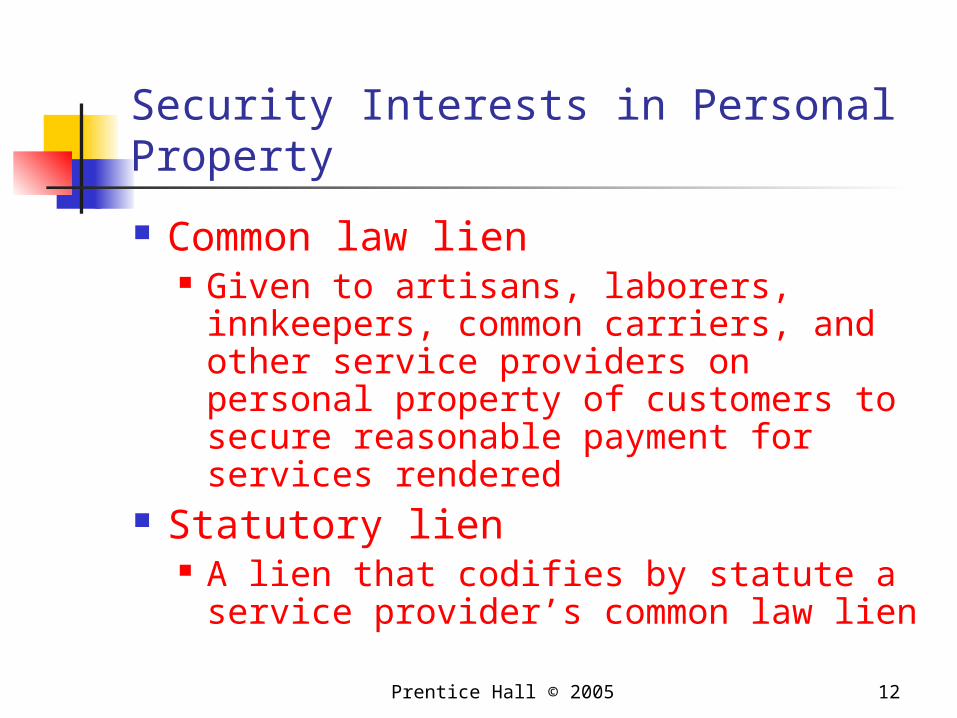

Security Interests in Personal Property

Common law lien Given to artisans, laborers, innkeepers,

common carriers, and other service providers on personal property of customers to secure reasonable payment for services rendered

Statutory lien A lien that codifies by statute a service

provider’s common law lien

Prentice Hall © 2005 13

Parties to a Mortgage

Owner-DebtorMortgagor

CreditorMortgagee

Loan of funds

Security interest in real property

Prentice Hall © 2005 14

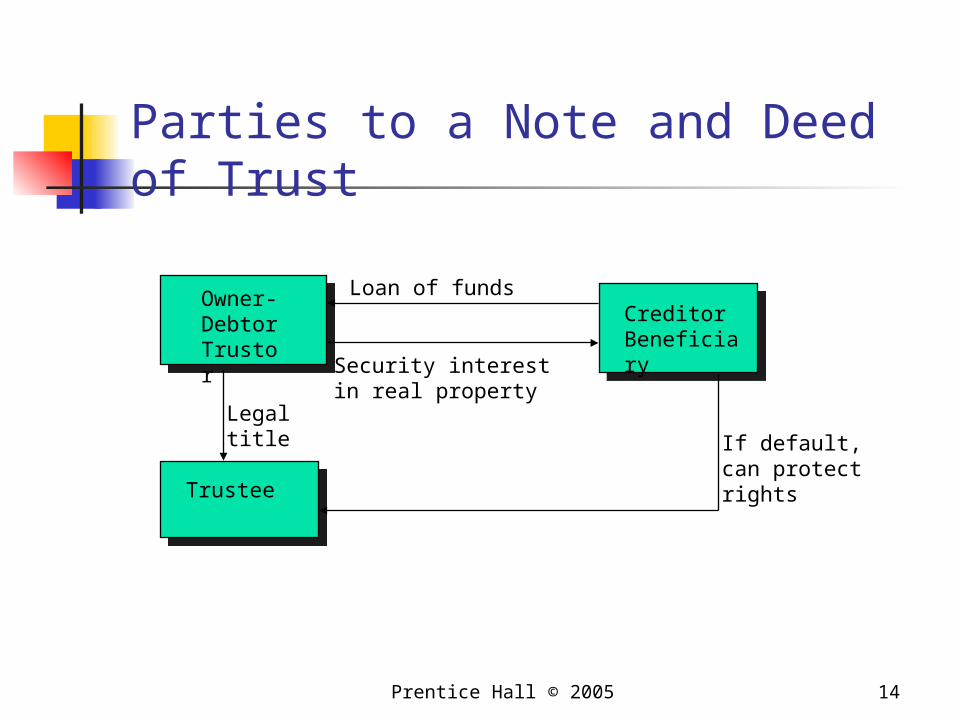

Parties to a Note and Deed of Trust

Owner-Debtor Trustor

Trustee

Creditor Beneficiary

If default,can protectrights

Legaltitle

Loan of funds

Security interestin real property

Prentice Hall © 2005 15

Right of Redemption The mortgagee has the right to

redeem real property after default and before foreclosure

Prentice Hall © 2005 16

Material Person’s Lien A contractor’s and laborer’s lien

that makes the real property to which improvements are being made become security for the payment of the services and materials for those improvements

Prentice Hall © 2005 17

Surety and Guaranty Arrangements

Surety arrangement An arrangement

where a third party promises to be primarily liable with the borrower for the payment of the borrower’s debt

Guaranty arrangement An arrangement

where a third party promises to be secondarily liable for the payment of another’s debt

Prentice Hall © 2005 18

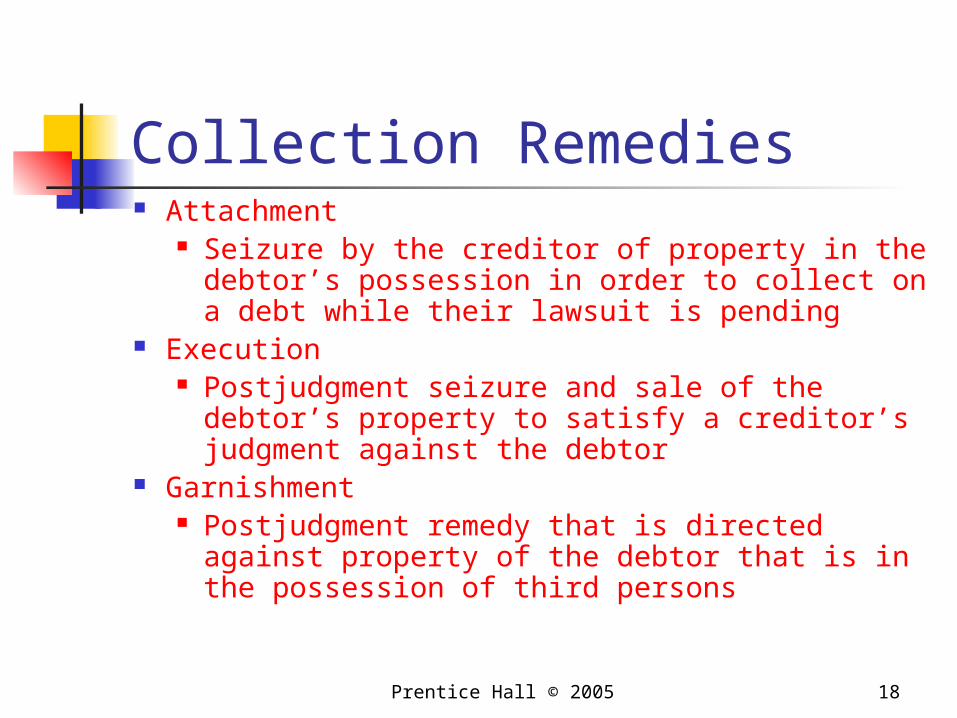

Collection Remedies Attachment

Seizure by the creditor of property in the debtor’s possession in order to collect on a debt while their lawsuit is pending

Execution Postjudgment seizure and sale of the

debtor’s property to satisfy a creditor’s judgment against the debtor

Garnishment Postjudgment remedy that is directed

against property of the debtor that is in the possession of third persons

Prentice Hall © 2005 19

Fresh Start in Bankruptcy The goal of federal bankruptcy law

is to discharge the debtor from the burdensome debts and allow him or her to begin again

Prentice Hall © 2005 20

Chapter 7 Bankruptcy Liquidation Debtor’s nonexempt property is sold

for cash Cash is distributed to creditors Unpaid debts are discharged Any person, including individuals,

partnerships, and corporations may be debtors in a Chapter 7 proceeding

Debtor gets a fresh start

Prentice Hall © 2005 21

Federal Exemptions from the Bankruptcy

Estate Exemptions include:

Homestead exemption—interest up to $15,000 in property used as a residence and burial plots

Interest up to $2,400 for one motor vehicle

Interest up to $400 per item for household goods

Prentice Hall © 2005 22

Voidable Transfers The bankruptcy code prevents debtors

from making unusual payments or transfers of property on the eve of bankruptcy that would unfairly benefit the debtor or some creditors at the expense of others Preferential transfers within 90 days before

bankruptcy Preferential liens Preferential transfers to insiders Fraudulent transfers

Prentice Hall © 2005 23

Priority of Creditors Secured creditors have priority

over unsecured creditors Unsecured creditors claims are

satisfied out of the bankruptcy estate in order of their statutory priority

Prentice Hall © 2005 24

Nondischargeable Debts Nondischargeable debts include:

Claims for taxes accrued within three years prior to bankruptcy filing

Certain fines and penalties payable to federal, state, and local government units

Alimony, maintenance, and child support Claims based on the consumer-debtor’s

purchase of luxury goods of more than $1000 from a single creditor

School loans

Prentice Hall © 2005 25

Chapter 11 Bankruptcy Reorganization Reorganizes the debtor's financial affairs

under the supervision of the Bankruptcy Court to give the debtor a new capital structure so that it will emerge from bankruptcy as a viable concern

Available to individuals, partnerships, corporations, unincorporated associations, and railroads

May be filed voluntarily by the debtor or involuntarily by its creditors

Prentice Hall © 2005 26

Rejection of Collective Bargaining Agreements

Companies that file for Chapter 11 reorganization sometimes argue that agreements with labor unions may be rejected in bankruptcy

The U.S. Supreme Court has upheld the right of companies to reject contracts in bankruptcy if necessary for the successful rehabilitation of the debtor

Prentice Hall © 2005 27

Confirmation Acceptance method

The bankruptcy court must approve a plan of reorganization if

The plan is in the best interests of each class of claims and interests

The plan is feasible At least one class of

claims votes to accept the plan

Each class of claims and interests is nonimpaired

Cram-down method A method of

confirmation of a plan of reorganization where the court forces an impaired class to participate in the plan of reorganization

Prentice Hall © 2005 28

Chapter 13 Bankruptcy Consumer Debt Adjustment

Permits the courts to supervise the debtor’s plan for the payment of unpaid debts by installments

Debtor retains more property than is exempt under Chapter 7

Less expensive and complicated than Chapter 7

Creditors may recover a greater percentage of debts than under Chapter 7

Prentice Hall © 2005 29

Chapter 12 Family Farmer Bankruptcy

Chapter 12 allows family farmers to file for a special type of reorganization bankruptcy that gives them added protection not available under Chapter 11 of the Bankruptcy Code