Embed Size (px)

Citation preview

Creating a world-class specialtypharma business

Preliminary Results Presentation25 April 2017

2Disclaimer

Neither this presentation nor any verbal communication shall constitute, or form part of, any offer, invitation orinducement to any person to underwrite, subscribe for, or otherwise acquire or dispose of, any shares or othersecurities in Circassia Pharmaceuticals plc (“Circassia”).

Forward-looking statements

This presentation and information communicated verbally to you may contain certain projections and otherforward-looking statements with respect to the financial condition, results of operations, businesses andprospects of Circassia. The use of terms such as “may”, “will”, “should”, “expect”, “anticipate”, “project”,“estimate”, “intend”, “continue”, “target” or “believe” and similar expressions (or the negatives thereof) aregenerally intended to identify forward-looking statements. These statements are based on current expectationsand involve risk and uncertainty because they relate to events and depend upon circumstances that may ormay not occur in the future. There are a number of factors which could cause actual results or developments todiffer materially from those expressed or implied by these forward-looking statements. Any of the assumptionsunderlying these forward-looking statements could prove inaccurate or incorrect and therefore any resultscontemplated in the forward-looking statements may not actually be achieved. Nothing contained in thispresentation or communicated verbally should be construed as a profit forecast or profit estimate. Investors orother recipients are cautioned not to place undue reliance on any forward-looking statements contained herein.Circassia undertakes no obligation to update or revise (publicly or otherwise) any forward-looking statement,whether as a result of new information, future events or other circumstances.

3Period of challenges and new opportunities

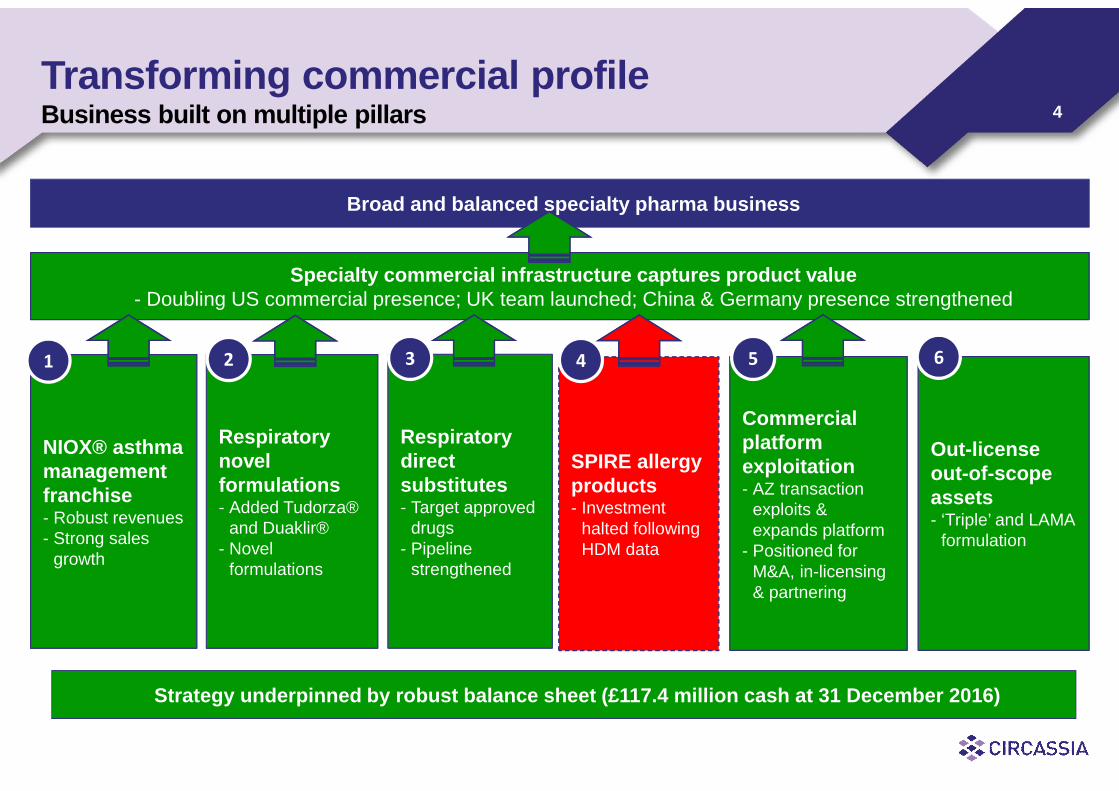

Expanded commercial infrastructure as strategic growth platform

NIOX® revenues continuing robust growth

Exciting collaboration and commercial rights transaction with AZ

Three COPD products added to specialty portfolio

Respiratory pipeline continuing to advance

Rapid action to halt allergy investment following disappointing results

Strong balance sheet (£117.4m cash at 31 December 2016)

Emerging as strong specialty pharma business

4

Respiratorynovelformulations- Added Tudorza®

and Duaklir®- Novel

formulations

Broad and balanced specialty pharma business

Specialty commercial infrastructure captures product value- Doubling US commercial presence; UK team launched; China & Germany presence strengthened

2

Transforming commercial profileBusiness built on multiple pillars

Commercialplatformexploitation- AZ transaction

exploits &expands platform

- Positioned forM&A, in-licensing& partnering

Out-licenseout-of-scopeassets- ‘Triple’ and LAMA

formulation

NIOX® asthmamanagementfranchise- Robust revenues- Strong sales

growth

SPIRE allergyproducts- Investment

halted followingHDM data

1 5 6

Strategy underpinned by robust balance sheet (£117.4 million cash at 31 December 2016)

Respiratorydirectsubstitutes- Target approved

drugs- Pipeline

strengthened

3 4

5

Product Research Preclinical Phase I Phase IIRegistration study /

SubstituteFiled /

ApprovedMarketed

NIOX VERO® / NIOX MINO®

Tudorza® US*

Duaklir® US

Flixotide® substitute**

Seretide® substitute

Flovent® substitute**

Spiriva® substitute

Cat SPIRE

Grass SPIRE

House Dust Mite SPIRE

Ragweed SPIRE

Birch SPIRE

Novel LABA / LAMA formulation

Novel COPD therapy formulation

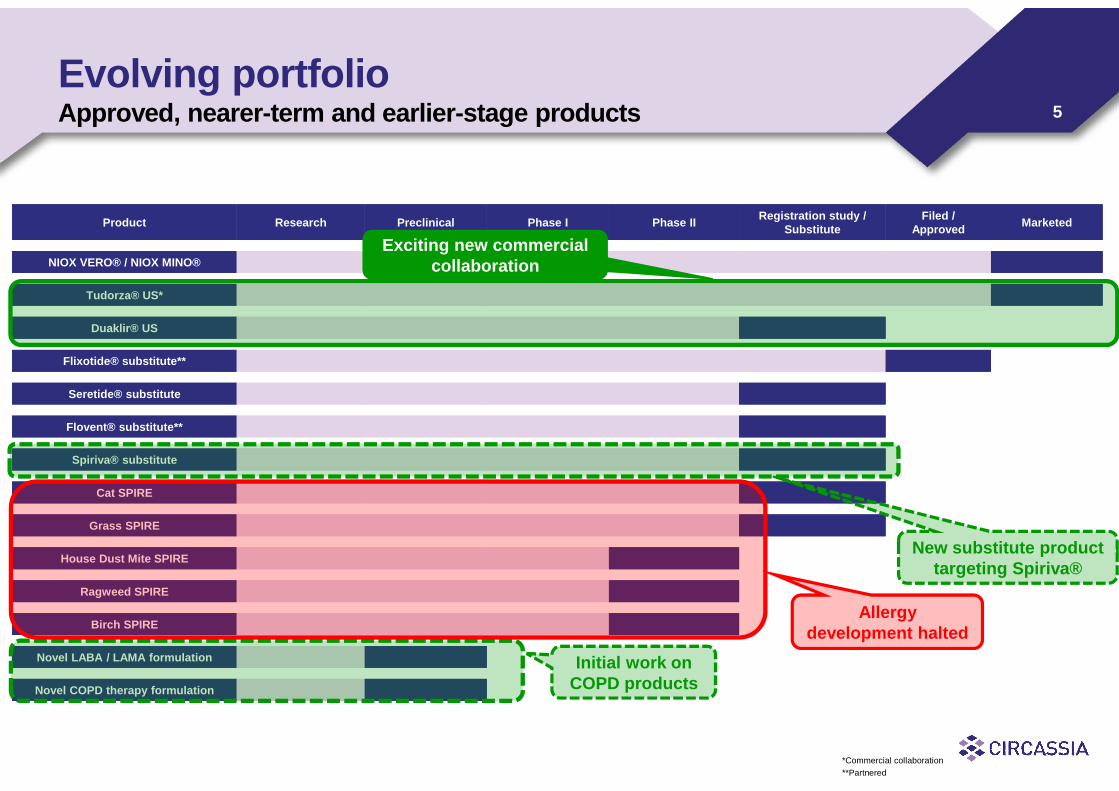

Evolving portfolioApproved, nearer-term and earlier-stage products

*Commercial collaboration

**Partnered

Initial work onCOPD products

Allergydevelopment halted

Exciting new commercialcollaboration

New substitute producttargeting Spiriva®

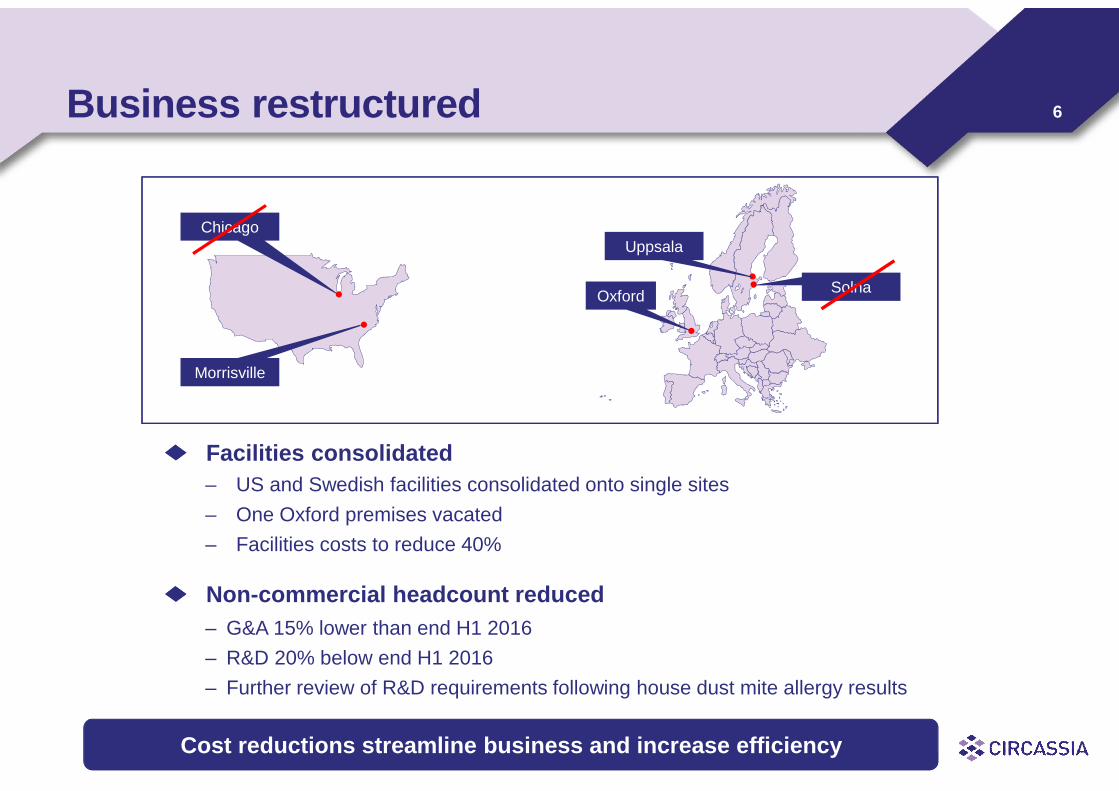

6Business restructured

Facilities consolidated

– US and Swedish facilities consolidated onto single sites

– One Oxford premises vacated

– Facilities costs to reduce 40%

Non-commercial headcount reduced

– G&A 15% lower than end H1 2016

– R&D 20% below end H1 2016

– Further review of R&D requirements following house dust mite allergy results

●

●

Chicago

Morrisville

●●

Uppsala

Solna

●

Oxford

Cost reductions streamline business and increase efficiency

7

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

8

NIOX® is only point-of-care FeNO device available across all major markets

Clinical evidence shows FeNO monitoring improves asthma management

– Improves diagnosis

– Improves determination of inhaled steroid responsiveness

– Improves stepwise dosing of inhaled steroids

– Improves monitoring of asthma control and treatment adherence

– Potential to reduce exacerbations

Research sales for use in big pharma clinical studies

− Validates importance; trains physicians; raises profile in asthma community

− Revenues dependent on study numbers and timings

Leadership in FeNO asthma management

NIOX VERO®

Launched in major markets

Ages 4+ EU; 7+ in US

6 and 10 sec test; ~60 sec result

Monitor lasts 5 yrs / 15,000 tests

9

Strong specialty commercial infrastructurePlatform for growth

Sales force expanded to 99territories

Managed markets, key accountsand medical affairs teams in place

Global commercial platform significantly strengthened

Expanding EU presence

UK direct sales team launched

German team strengthened

Beijing-based team managelocal distributors

Team strengthened with marketaccess and medical functions

Field Reps99 Specialty

RepresentativeTerritories

KeyAccounts7 US based

Marketing3 US based

MedicalSupport

3 US based

ManagedMarkets

6 US based

CommercialOperations5 US based1 US trainer

Strong US team

10

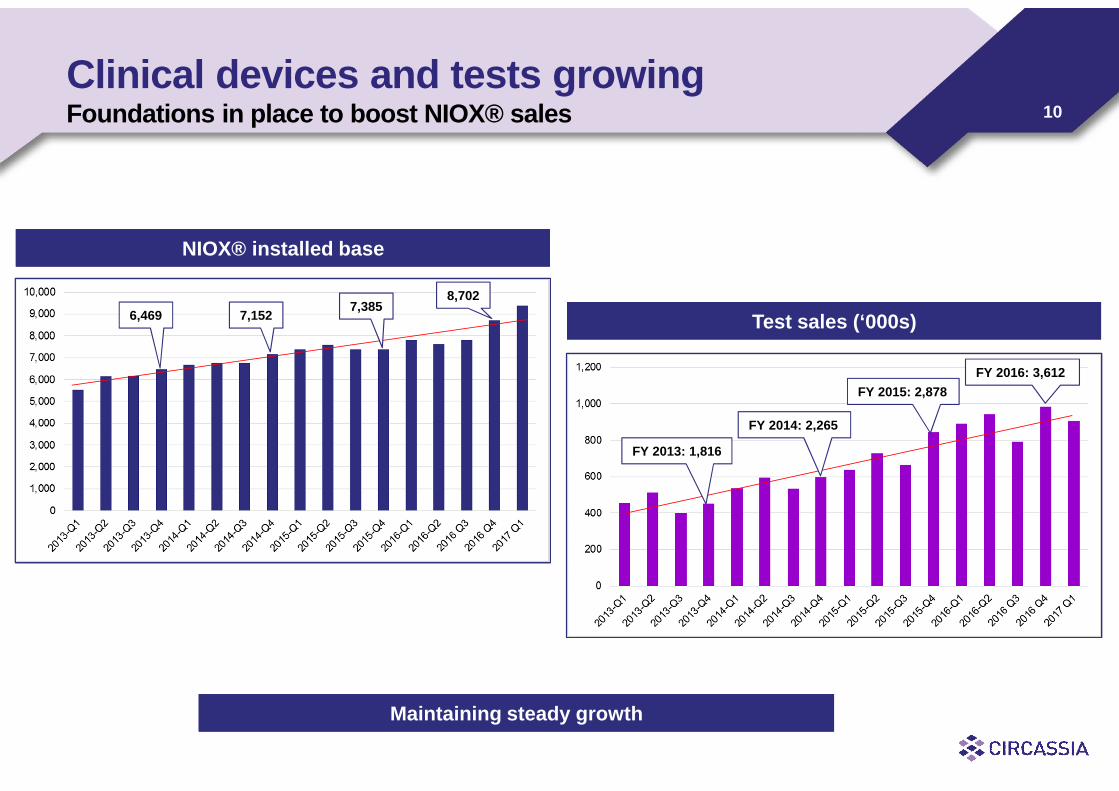

NIOX® installed baseNIOX® installed base

Clinical devices and tests growingFoundations in place to boost NIOX® sales

Test sales (‘000s)Test sales (‘000s)6,469 7,152

8,702

FY 2015: 2,878

FY 2016: 3,612

Maintaining steady growthMaintaining steady growth

7,385

FY 2013: 1,816

FY 2014: 2,265

11Strong NIOX® performance

23% growth vs 2015 (10% CER)

35% increase in clinical sales (21% CER)

6% decrease in research sales (16% CER)

17 key US accounts signed Q1 2017

6 additional health systems (>2.8m lives) coveringNIOX® Q1 2017

57% growth in US clinical sales Q1 2017 vs Q1 2016

US March 2017 sales best month since launch

Robust revenue growth

12

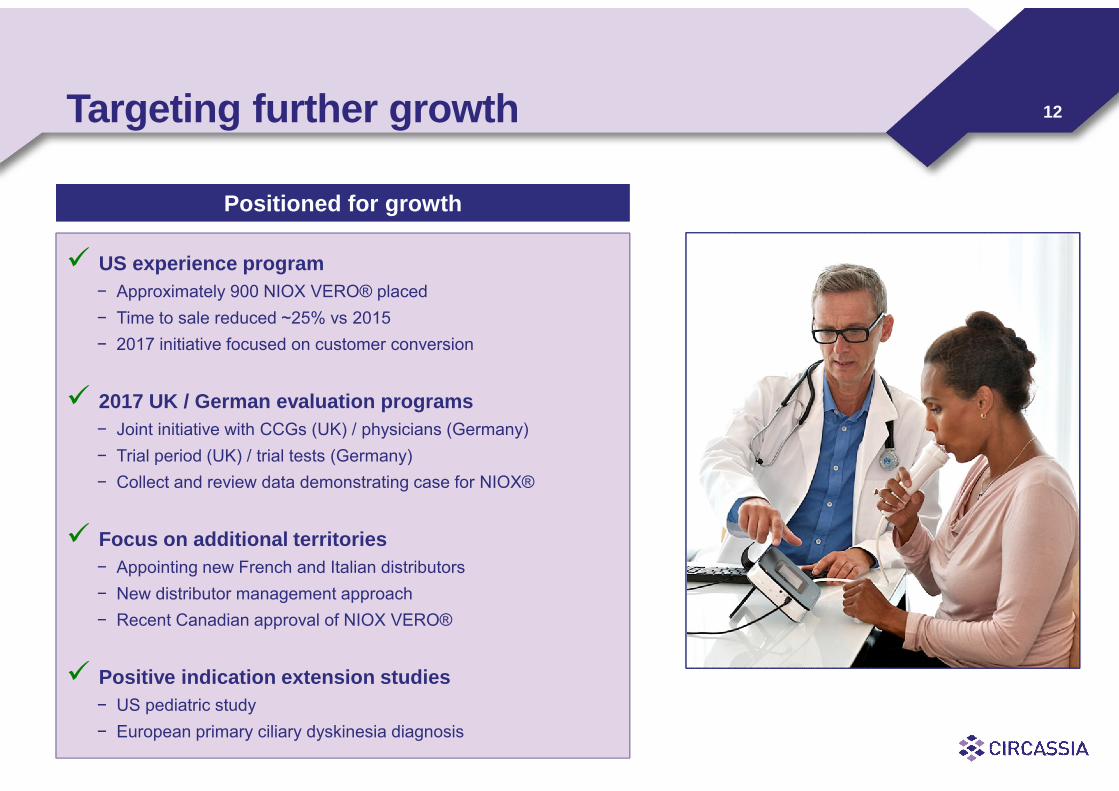

US experience program

− Approximately 900 NIOX VERO® placed

− Time to sale reduced ~25% vs 2015

− 2017 initiative focused on customer conversion

2017 UK / German evaluation programs

− Joint initiative with CCGs (UK) / physicians (Germany)

− Trial period (UK) / trial tests (Germany)

− Collect and review data demonstrating case for NIOX®

Focus on additional territories

− Appointing new French and Italian distributors

− New distributor management approach

− Recent Canadian approval of NIOX VERO®

Positive indication extension studies

− US pediatric study

− European primary ciliary dyskinesia diagnosis

Positioned for growthPositioned for growth

Targeting further growth

13

Positive results in US label extension studyFiling submitted for children aged 4 – 6 and 6 second test mode

Observed FeNO in evaluable population with 2 valid measurement in each mode

4 years (n=9) 5 years (n=27) 6 years (n=32) All (n=68)

Average FeNO 6 sec mode

Mean 14.8 20.7 23.2 21.1

Standard deviation 11.72 14.47 15.61 14.76

Average FeNO 10 sec mode

Mean 14.4 20.1 23.1 20.7

Standard deviation 11.51 14.39 15.34 14.59

Paired difference (average 10s mode - average 6s mode)

Mean -0.4 -0.6 -0.1 -0.4

Standard deviation 0.74 3.28 3.99 3.41

14

Nasal NO measurement from both nostrils

Optimal Cut-Off Specificity Sensitivity

Tidal breathingmethod

171 ppb(AUC 99.8%;PPV 100.0%;NPV 98.9%)

100% 98.0%

Velum closedexpiration againstresistance method

356 ppb(AUC 98.7%;PPV 93.1%;NPV 98.8%)

96.3% 97.8%

AUC = area under curve

NPV = negative predictive value (above optimal cut-off)

PPV = positive predictive value (below optimal cut-off)

TBM = tidal breathing method

ERM = velum closed expiration against resistance method

Positive results in PCD registration studyCertification update in coming months

15Potential to predict response to biologics

FeNO identifies likely (and unlikely)

responders to Xolair® (omalizumab)

- $10,000 - $30,000 per year treatmentfor moderate-to-severe allergic asthma

CI = confidence intervalMean percent reduction (95% CI) in protocol-defined asthma exacerbation rate in low- and high-biomarker subgroups (baseline fractionalexhaled nitric oxide [FeNO], peripheral blood eosinophils, and serum periostin)*Exacerbation reduction P values; omalizumab versus placebo in each biomarker subgroupHanania et al. Am J Respir Crit Care Med. 2013;187:804-811

Asthma exacerbation reduction by biomarkerAsthma exacerbation reduction by biomarker

16FeNO-directed therapy reduces exacerbations

Syk et al. J Allergy Clin Immunol Pract. 2013;1(6):639-648.

FeNO group had reduced time tofirst exacerbation

FeNO group had reduced numberof subjects with exacerbations

17

High FeNO group (>50ppb) n=1,016

Baseline corticosteroid use 852 / 1,016 (83.9%)

Change in corticosteroids based on FeNO 695 / 852 (81.6%)

Stepped down 20 / 695 (2.9%)

Stepped up 668 / 695 (96.1%)

Data presented at 2017 AAAAI‘Real world’ data on FeNO impact on treatment decisions

Effect of FeNO measurement on treatment decisions

Clinical impression match to FeNO

High vs FeNO > 50 ppb

18

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

19

Transformational products

Adds Tudorza® in US

Adds Duaklir® phase III (approved in EU) as market moves towards LAMA / LABAs

Products feature Pressair® potential best-in-class device

Transforms Circassia’s commercial profile

Doubles marketed products with potential to triple in two years

Funds significantly broader commercial infrastructure

Transitioning Circassia into world-class respiratory business positioned for further licensing and M&A

Attractive transaction structure Total consideration $175m - $230m plus Duaklir® deferred royalties

$50m equity upfront with maximum $180m deferred consideration anticipate funded by debt (vendor loan back stop)

Commercial expansion and R&D contribution addressed by profit share collaboration

Transaction expected to deliver profits after one year

US infrastructure crucial for transformationaltransaction with AstraZeneca

Commercial collaboration, option and sub-license of US product rights

20

Tudorza® Pressair®

LAMA – maintenance bronchodilatorfor adults with COPD

$80m sales in US

Broad clinical database

– Three pivotal studies

– H2H vs Spiriva®

Aclidinium bromide (400µg twice daily)

Comparison vs market leading LAMA (tiotropium; Spiriva®)

*p<0.05 vs tiotropiumBoth treatments statistically significantly higher than placebo at all time pointsBeier et al COPD 2013

21

Duaklir® Pressair®

LAMA / LABA fixed dose combination

Approved in ~50 countriesincluding EU for adults with COPD

Broad clinical database

– Two pivotal studies

– Study vs Seretide®

Identical product in phase IIIdevelopment for US market

Aclidinium / formoterol (400µg / 12µg twice daily)

The Duaklir® trademark is registered in the United States;the mark is not currently approved for use by FDA

*p<0.05****p<0.0001Adapted from Singh et al BMC Pulm Med 2014; D’Urzo et al Respir Res 2014

FEV1 1hr post-morning doseFEV1 1hr post-morning dose FEV1 morning pre-dose (trough)FEV1 morning pre-dose (trough)

Study1

Study2

22

Pressair® inhaler offers significant advantagesPotential best in class mDPI used for both Tudorza® and Duaklir®

p<0.0001 vs comparator

Strong patient preference

Van der Palen et al. Expert Opin Drug Deliv 2013;Chrystyn et al. ERS 2014; LAC39: data on file

Groups more likely to report COPD:

Current / former smokers

Aged over 65

Women

History of asthma

More likely among COPD patients:

Activity limitations

Unable to work

Require equipment such as portableoxygen tanks

Increased hospital stays

Other chronic diseases

US COPD patient profileUS COPD patient profile

23

GOLD COPD guidelines updated for 2017Support LAMA and LABA / LAMAs as preferred treatments

LAMA + LABA LABA + ICS

LAMA

Furtherexacerbation(s)

Group C Group D – most severeConsider roflumilast ifFEV1 < 50% pred. and

patient has chronicbronchitis

Consider macrolide (informer smokers)

LAMA + LABA+ ICS

LAMA LAMA + LABA LABA + ICS

Furtherexacerbation(s)

Furtherexacerbation(s)

Persistentsymptoms / further

exacerbation(s)

Group A - least severe

Continue, stop or tryalternative class of

bronchodilator

A bronchodilator

evaluate effect

Group B

LAMA + LABA

A long-actingbronchodilator

(LABA or LAMA)

Persistentsymptoms

From the Global Strategy for the Diagnosis, Management and Prevention of COPD, Global Initiative for Chronic Obstructive Lung Disease (GOLD) 2017.Available from: http://goldcopd.org.

PreviouslySAMA or

SABA

PreviouslyICS + LABA

or LAMA

PreviouslyICS + LABA

and / orLAMA

24

Market # HCPs Annual Annual

Decile # HCPs % Reach Reached Calls/HCP Calls

10 129 50% 65 18 1,165

9 424 50% 212 18 3,816

8 1,191 50% 596 18 10,722

7 3,011 50% 1,505 12 18,064

6 5,717 0% - - -

5 9,148 0% - - -

4 13,724 0% - - -

3 21,029 0% - - -

2 36,690 0% - - -

1 167,111 0% - - -

TOTAL 258,174 1% 2,378 14 33,766

*Excludes prescribers reached in left table

Tudorza # HCPs Annual Annual

Decile # HCPs % Reach Reached Calls/HCP Calls

10 248 95% 236 36 8,482

9 525 95% 499 36 17,955

8 837 95% 795 36 28,625

7 1,242 95% 1,180 24 28,318

6 1,786 95% 1,697 18 30,541

5 2,538 95% 2,411 18 43,400

4 3,496 95% 3,321 12 39,854

3 4,788 95% 4,549 12 54,583

2 7,675 0% - - -

1 23,444 0% - - -

TOTAL 46,579 32% 14,687 17 251,758

Focused call plan reaches major prescribers

Expanded sales force to target top 8 Tudorza® prescriber deciles

~15k prescribers responsible for 80% of Tudorza® prescriptions

Complement with top 4 deciles of COPD prescribers (non-Tudorza®) in areas with positive payer coverage

Targeting top Tudorza® prescribers Targeting top COPD prescribers (non-Tudorza®)

Data sourced from IMSHCP = healthcare professional

+

{Top40%Top

80%

25Significant progress executing plan

US sales force expansion by 100− Over 2,000 applied; 44 already recruited with remainder in final stage

Strong support team– 8 regional sales managers – 6 positions filled– Area sales director – position filled– Marketing director – offer stage– 5 medical science liaisons – 3 positions filled– Sales training manager – position filled– Senior analyst – position filled

Existing sales force training this week

Use AstraZeneca training, marketing materials and data

Circassia Tudorza® promotion to begin 8 May

First expansion wave (~75) training from 8 May begin promotion 22 May

Rapid expansion to 200 with full promotion starting 5 June

Tudorza® #1 in sales call & higher frequency increases intensity

26

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

27

Particle-engineered respiratory productsNear-term pipeline & longer-term novel formulations

73.5% of pre-entry brand

price for first to market

generic in US during

exclusivity1

Significant pricing potential

1 Bureau of Economics, Federal Trade Commission, Working Paper No 317. The effect of generic drug competition on generic drug prices during the Hatch-Waxman 180-day exclusivity period. April 2013.

Device types

DPIpMDI

Directly substitutable products

– Limited development

– Abbreviated route to market

– No requirement for significant promotion

– Challenging to achieve for respiratory products

Novel formulations

− Longer more extensive development

− Develop specialty products

Novel technology controls API properties

28

Fliveo® EU rightsTargeting direct substitution of GSK’s Flixotide® pMDI

1 Partner rights: USA, Canada, Australia and New Zealand, India, Europe (including the EU and EFTA states (Iceland, Liechtenstein, Norway and Switzerland)), Turkey, Russia and CIS

Originator pMDI / DPI sales $866m (~60%US)

Partnered with Mylan1

Main market US

Discussions initiated for return of EU rights H2 2016

Product approved in all three strengths in UK

Smaller EU market potential opportunity for Circassia

Plan to determine EU approach in coming months

Targeting EU roll-out

29

Seriveo® targets Seretide® pMDI substitutionOriginator pMDI / DPI sales $4.7bn

Salmeterol (Seriveo® vs originator)

Fluticasone (Seriveo® vs originator)

Marked improvement vs previous study

Plan to reiterate pharmacokinetic study

UK filing anticipated H1 2019

3030

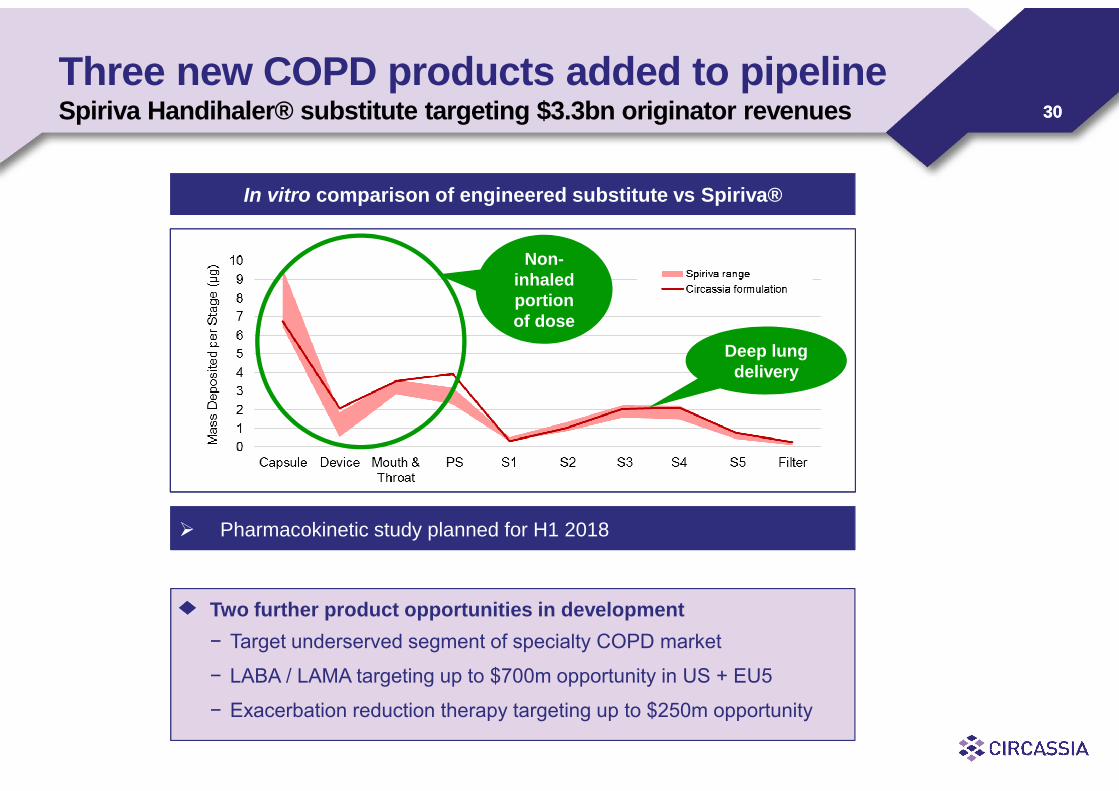

Three new COPD products added to pipelineSpiriva Handihaler® substitute targeting $3.3bn originator revenues

Pharmacokinetic study planned for H1 2018

In vitro comparison of engineered substitute vs Spiriva®

Deep lungdelivery

Non-inhaledportionof dose

Two further product opportunities in development

− Target underserved segment of specialty COPD market

− LABA / LAMA targeting up to $700m opportunity in US + EU5

− Exacerbation reduction therapy targeting up to $250m opportunity

31

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

32House dust mite SPIRE phase IIb study

Robust study designRobust study design

Double-blind, randomized, multi-center field study

― Four arms (4 x 12nmol; 8 x 12nmol; 4 x 20nmol; placebo)

― Large population (4 x 12nmol n=180; 8 x 12nmol n=178; 4 x 20nmol n=178; placebo n=178)

Primary endpoint: difference in combined TRSS / rescue medication use

score one year after start of treatment vs placebo

― Same endpoint as previous cat SPIRE phase III field study

Inclusion criteria minimize confounding factors

― Moderate to severe allergy: baseline TRSS ≥12

― Subjects with laboratory confirmed house dust mite allergy

33

Mean Combined Score 50-52 weeks after treatment initiation

HDM SPIRE results mirror cat SPIRE phase IIIPrimary endpoint - efficacy

Primary endpoint: combined TRSS (0-24 scale) and rescue medication use (RMS) score (0-3 scale)

- Combined Score (0-6 scale) = (TRSS / 8) + (RMS)

ITT populationPlacebo(n=178)

4 x 12 nmol(n=180)

4 x 20 nmol(n=178)

8 x 12 nmol(n=178)

Mean Combined Score (baseline) 2.89 2.78 2.76 2.80

Mean Combined Score (50-52 weeks) 1.76 1.81 1.63 1.56

Combined Score improvement from baseline 39.1% 34.9% 40.9% 44.3%

LS mean difference vs placebo (50-52 weeks) 0.12 -0.05 -0.16

p value vs placebo 0.2641 0.6539 0.1356

34

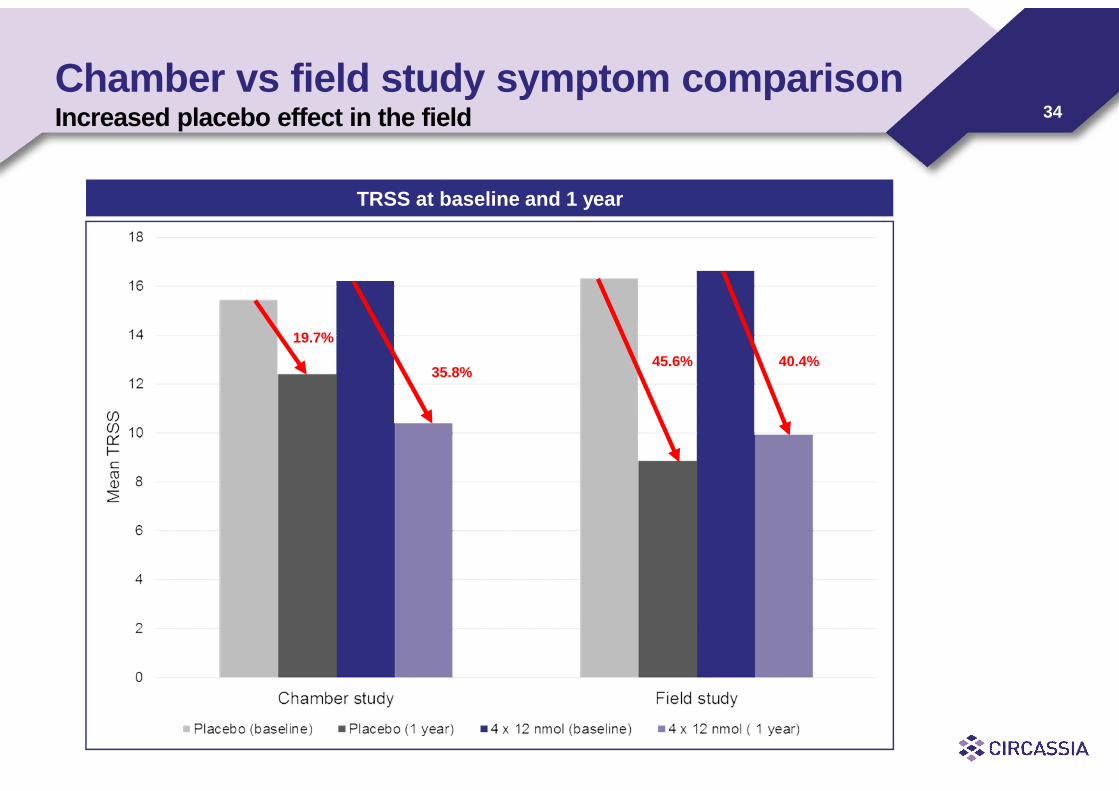

Chamber vs field study symptom comparisonIncreased placebo effect in the field

TRSS at baseline and 1 year

45.6%35.8%

19.7%

40.4%

35

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Phase IIb Phase III

Mea

nT

RS

S

Placebo (baseline) Placebo (1 year) 4 x 6 nmol (baseline) 4 x 6nmol (1 year)

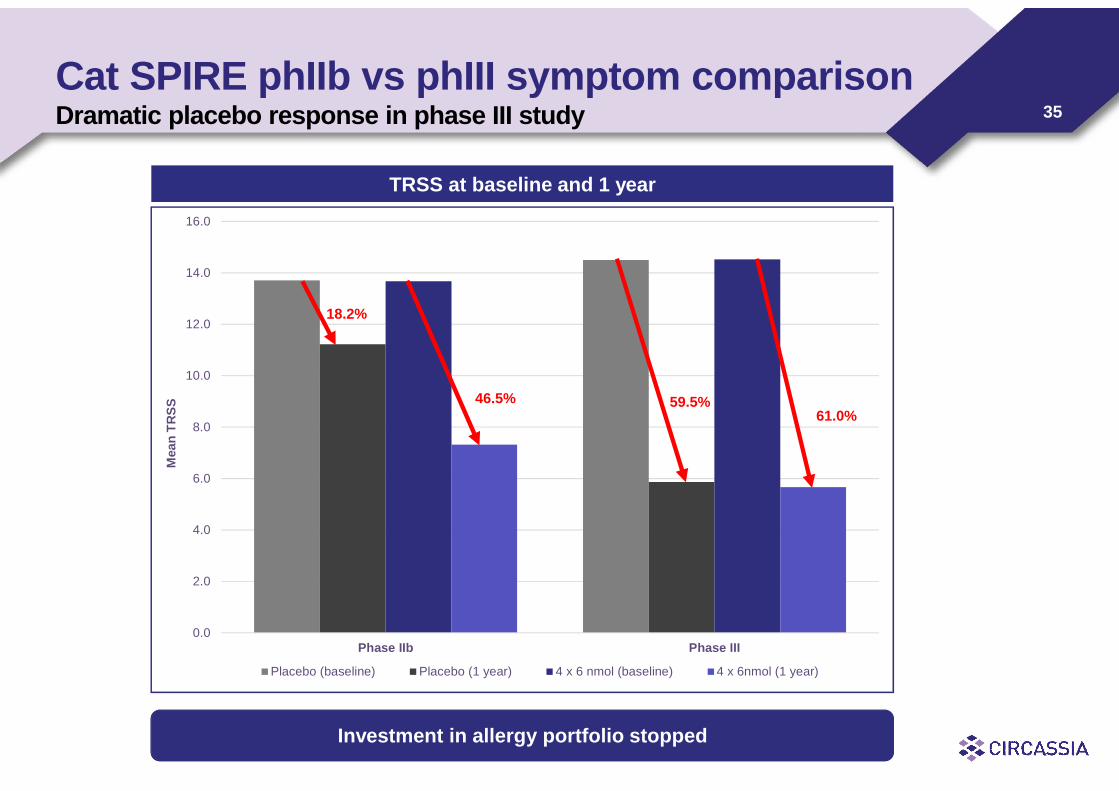

Cat SPIRE phIIb vs phIII symptom comparisonDramatic placebo response in phase III study

TRSS at baseline and 1 year

61.0%59.5%46.5%

18.2%

Investment in allergy portfolio stopped

36

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

37

Financial highlightsYear ended 31 December 2016

Full year results for 2016 differentiated from 2015 by two main factors

– Goodwill impairment allocated to allergy franchise for potential future benefit of acquiredAerocrine sales infrastructure

– Contributions from NIOX® and respiratory business for full year 2016

Underlying loss for 2016 £57.4m (2015: £50.0m)

– Provisions and impairment of allergy portfolio goodwill and other intangibles £77.2 million

– Restructuring costs and provisions for closure of Chicago and Solna offices £2.8m

– Allergy R&D expenditure £19.1m (2015: £30.5m) of which £5.3m in H2

Cash at 31 December 2016 £117.4m (31 December 2015 £203.8m; 30 June 2016: £138.0m)

– Contingent £30.0m consideration paid January 2016 to Prosonix ex-shareholders

– £3.2m payment for remaining 2.1% of Aerocrine issued share capital

– Cash decrease H2 2016 £20.6m

– Business remains well funded

38

Income statementYear ended 31 December 2016

Underlying Non-underlying Total Total Change

operations items 2016 2015

£m £m £m £m £m

Revenue 23.1 - 23.1 10.8 12.3

Cost of goods (8.0) - (8.0) (4.3) (3.7)

Gross profit 15.1 0.0 15.1 6.5 8.6

Sales and marketing (28.9) (75.8) (104.7) (13.5) (91.2)

Research & development (42.3) (3.9) (46.2) (46.8) 0.6

Administrative expenditure (15.4) (0.3) (15.7) (13.7) (2.0)

Other gains - - - 1.1 (1.1)

Operating loss (71.5) (80.0) (151.5) (66.4) (85.1)

Finance income net 6.0 - 6.0 3.5 2.5

Share of profit of joint venture 0.6 - 0.6 0.1 0.5

Loss before tax (64.9) (80.0) (144.9) (62.8) (82.1)

Taxation 7.5 - 7.5 12.8 (5.3)

Loss for the financial year (57.4) (80.0) (137.4) (50.0) (87.4)

39

Income statementYear ended 31 December 2016

Revenues

– Sales increased 23% from £18.7m (10% CER)

– Clinical sales increased 35% to £18.0m (21% CER)

– Device sales grew to £1.7m (CER 2015: £1.3m, 31%)and tests to £16.1m (CER 2015: £13.3m, 21%)

– Steady growth continued over first quarter 2017

– Research sales decreased 6% (16% CER)

Sales and marketing

– £74.5m allergy franchise goodwill impairment

– Increase in field force

Net finance income

– Includes £5.2m fx gain due to sterling weakening

Taxation

– Includes R&D tax credit £8.6m (2015: £10.3m)

– Lower qualifying R&D spend

– Deferred tax movements

2016 2015 Change

£m £m £m

Revenue 23.1 10.8 12.3

Cost of goods (8.0) (4.3) (3.7)

Gross profit 15.1 6.5 8.6

Sales and marketing (104.7)* (13.5) (91.2)

Research & development (46.2) (46.8) 0.6

Administrative expenditure (15.7) (13.7) (2.0)

Other gains - 1.1 (1.1)

Operating loss (151.5) (66.4) (85.1)

Finance income net 6.0 3.5 2.5

Share of profit of jointventure 0.6 0.1 0.5

Loss before tax (144.9) (62.8) (82.1)

Taxation 7.5 12.8 (5.3)

Loss for the financial year (137.4) (50.0) (87.4)

* Includes £74.5m allergy franchise goodwill impairment

40

Research & developmentYear ended 31 December 2016

H2 allergy expenditure £5.3m limited to three areas

– Completion of house dust mite allergy field study

– Drug product and stability programs

– Committed costs including cat allergy two-year follow-up

Remaining allergy expenditure in 2017 ~£6m

Respiratory programs

– Seriveo® and Spiriva® substitute programs

Non-allergy R&D £20.5m (inc £2.0m amortization)

Impairment and provisions

– Impairment of allergy licences and patents

– Production termination for cat, HDM & grass allergy programs

– UK restructuring and provisions for closure of Solna site

2016 2015 Change

£m £m £m

Allergy 19.1 30.5 (11.4)

Respiratory 6.9 6.1 0.8

NIOX 5.3 2.0 3.3

Costs not specific toprojects 11.0 8.2 2.8

Underlying R&D costs 42.3 46.8 (4.5)

Allergy contractterminations 2.4 - 2.4

Intangible assetimpairment 0.3 - 0.3

Restructuring costs 1.2 - 1.2

Total R&D costs 46.2 46.8 (0.6)

41Summary and outlook

Cost reduction

– Immediate halting of allergy investment (£19.1m in 2016)

– Consolidation of Chicago, Solna and Oxford facilities expected annual costs savings ~£6m

Collaboration with AstraZeneca

– Commercial infrastructure investment crucial to attracting AstraZeneca

– Focus on increasing field force to 200

– Expect some disruption in Tudorza® and NIOX® sales in 2017

– Expense most of $62.5m collaboration R&D contribution in 2017

– Payment of $17.5m R&D costs to AstraZeneca December 2017

– Anticipate earnings enhancing after 1 year, broadly cashflow neutral for 3 years then cash generative

Well positioned with robust balance sheet

– Focus on AstraZeneca collaboration to grow sales of Tudorza®

– Progress broader respiratory portfolio; continue investment in earlier-stage new products

42

NIOX® asthma management

AstraZeneca partnership

Respiratory pipeline

1

2

3

SPIRE allergy therapies4

Summary6

Financial results5

43

Building world-class specialty pharma business

− Robust infrastructure established for specialty and direct substitute product commercialisation

− NIOX® revenues increasing strongly

− Collaboration with AstraZeneca brings Tudorza® and Duaklir®

Strong and balanced growth platform

− Commercial platform expanded as growth engine

− Respiratory pipeline broadened with addition of three new COPD programmes

− Allergy investment curtailed with broader focus on cost containment

− Robust balance sheet and funded to deliver (£117.4m cash at 31 December 2016)

Good progress despite allergy set back

Contact us

Office Investors Financial and CorporateCommunications

CircassiaNorthbrook HouseRobert Robinson AvenueOxford Science ParkOxford OX4 4GAUnited Kingdom

W: www.circassia.comE: [email protected]

Steven Harris, CEOJulien Cotta, CFO

T: +44 (0) 1865 405560

FTI Consulting200 AldersgateAldersgate StreetLondon EC1A 4HDUnited Kingdom

T: +44 (0) 20 3727 1000E: [email protected]

![Preliminary Design Reviewelegantly organizing uses, creating great places and developing cost conscious design strategies are the basis of [au]workshop’s mission. [au]workshop’s](https://img.dokumen.tips/doc/110x75/6001d07a2f96f375481e3ec0/preliminary-design-review-elegantly-organizing-uses-creating-great-places-and-developing.jpg)