Embed Size (px)

Citation preview

Challenges and constraints

2

Lack of trainingLack of skillLack of informationLack of networkingLack of resources

Proposed interventions

3

Practical hands-on trainingWeekly sessionsFormation of consortia by SMMEsFormation of joint venturesFormation of partnershipsMonitoring and evaluation of submitted

tenders

The Process

4

Identification of tendersRequest for tender documentsIdentification of suppliersRequest for quotationsCompliance –Tax clearance certificatesPricing of documentCalculation of preference pointsCompletion of documentSubmission of tender

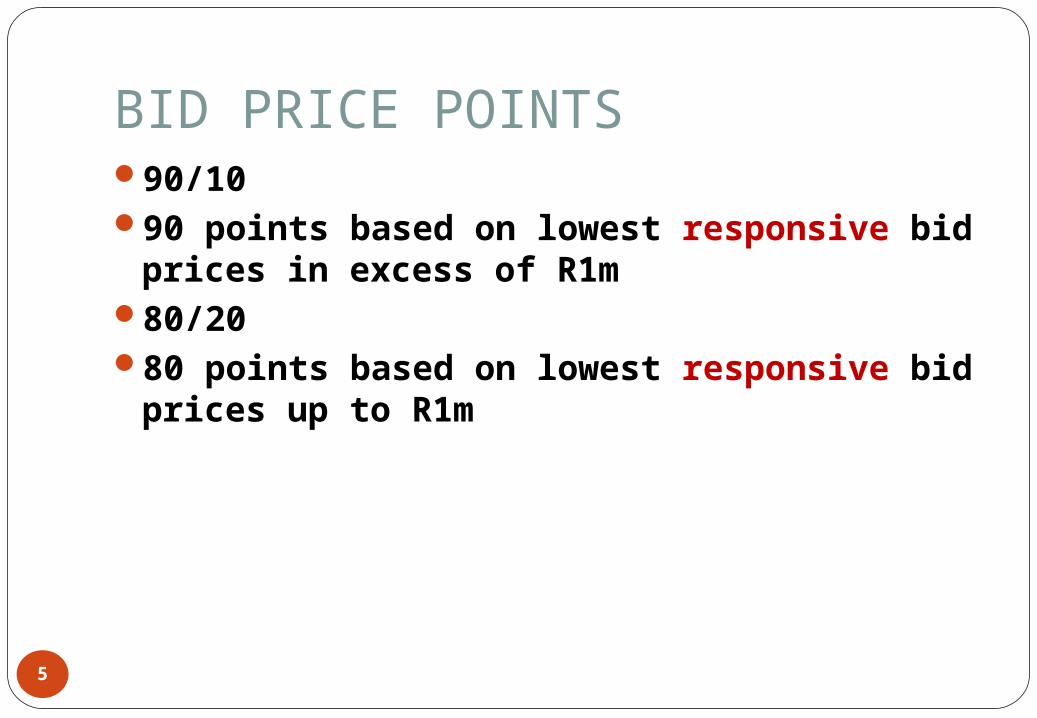

BID PRICE POINTS

5

90/1090 points based on lowest responsive bid

prices in excess of R1m80/2080 points based on lowest responsive bid

prices up to R1m

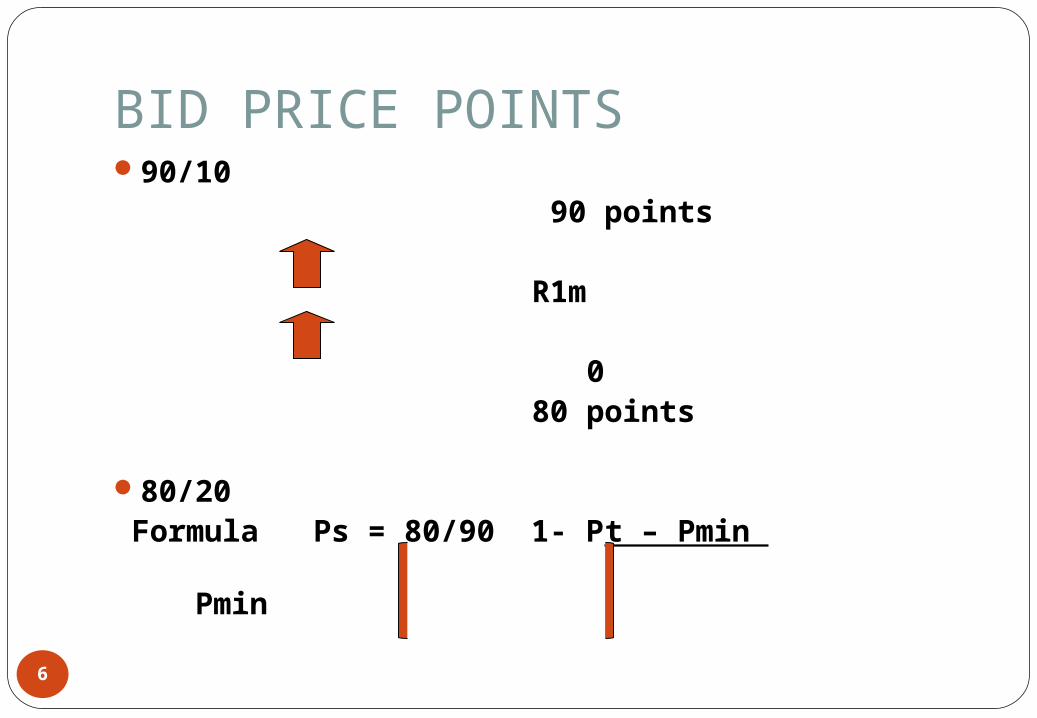

BID PRICE POINTS

6

90/10 90 points R1m 0 80 points 80/20 Formula Ps = 80/90 1- Pt – Pmin Pmin

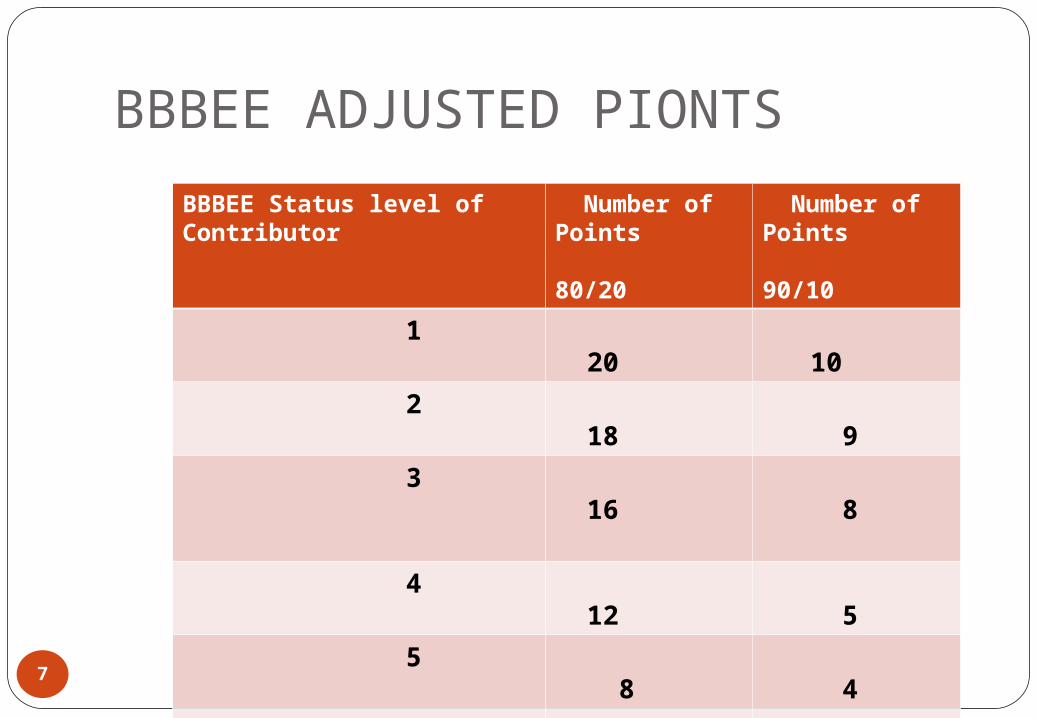

BBBEE ADJUSTED PIONTS

7

BBBEE Status level of Contributor

Number of Points 80/20

Number of Points 90/10

1 20 10

2 18 9

3 16

8

4 12 5

5 8 4

6 6 3

7 4 2

8 2 1

Non Compliant contributor

0 0

POINTS ALLOCATION

8

BIDDER

PRICE PRICE POINTS

BBBEE CONTRIBUTOR LEVEL

BBBEE POINTS

TOTAL POINTS

A

B

C

D

E

F

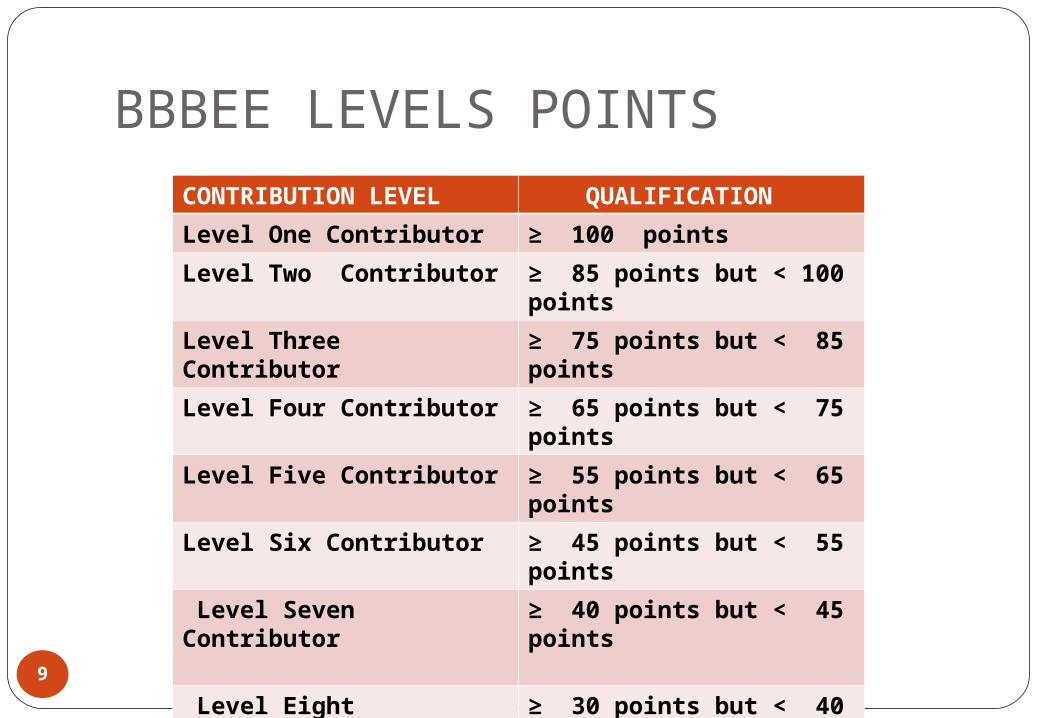

BBBEE LEVELS POINTS

9

CONTRIBUTION LEVEL QUALIFICATION

Level One Contributor ≥ 100 points

Level Two Contributor ≥ 85 points but < 100 points

Level Three Contributor ≥ 75 points but < 85 points

Level Four Contributor ≥ 65 points but < 75 points

Level Five Contributor ≥ 55 points but < 65 points

Level Six Contributor ≥ 45 points but < 55 points

Level Seven Contributor

≥ 40 points but < 45 points

Level Eight Contributor ≥ 30 points but < 40 points

Non Compliant Contributor

< 30 points

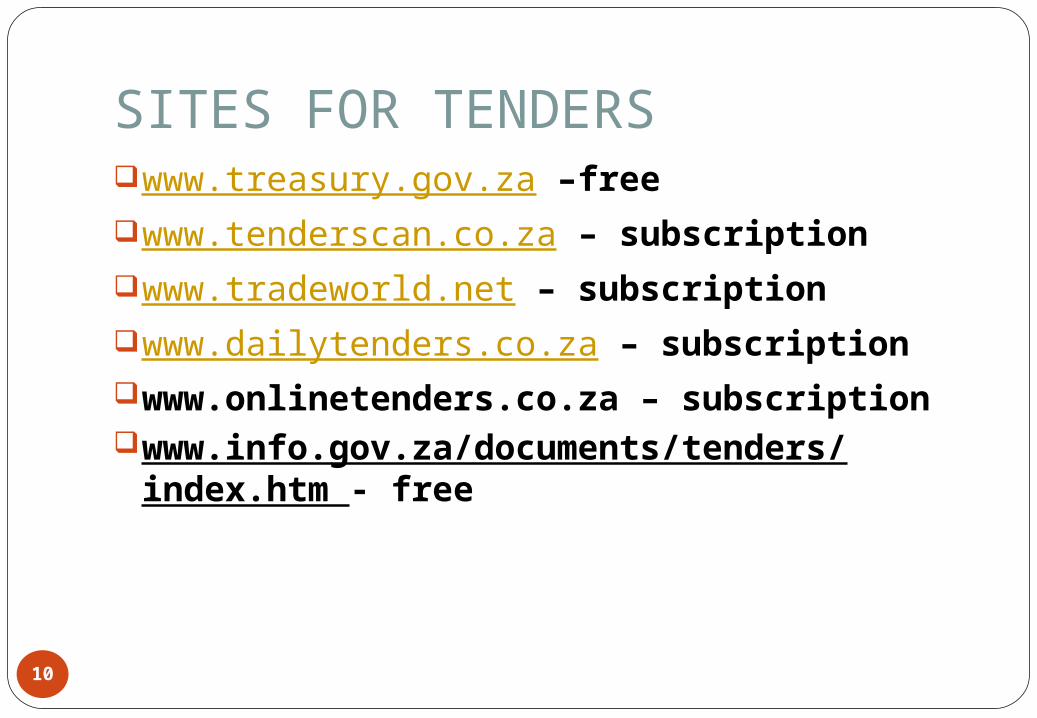

SITES FOR TENDERS

10

www.treasury.gov.za –freewww.tenderscan.co.za – subscriptionwww.tradeworld.net – subscriptionwww.dailytenders.co.za – subscriptionwww.onlinetenders.co.za – subscriptionwww.info.gov.za/documents/tenders/

index.htm - free

SITES FOR SUPPLIERS

11

www.safindit.co.zawww.findsa.co.zawww.sayellow.co.zawww.easyinfo.co.zawww.sabs.co.zawww.specifile.co.zawww.kellysearch.comwww.africatrade.co.zawww.infomine-africa.com

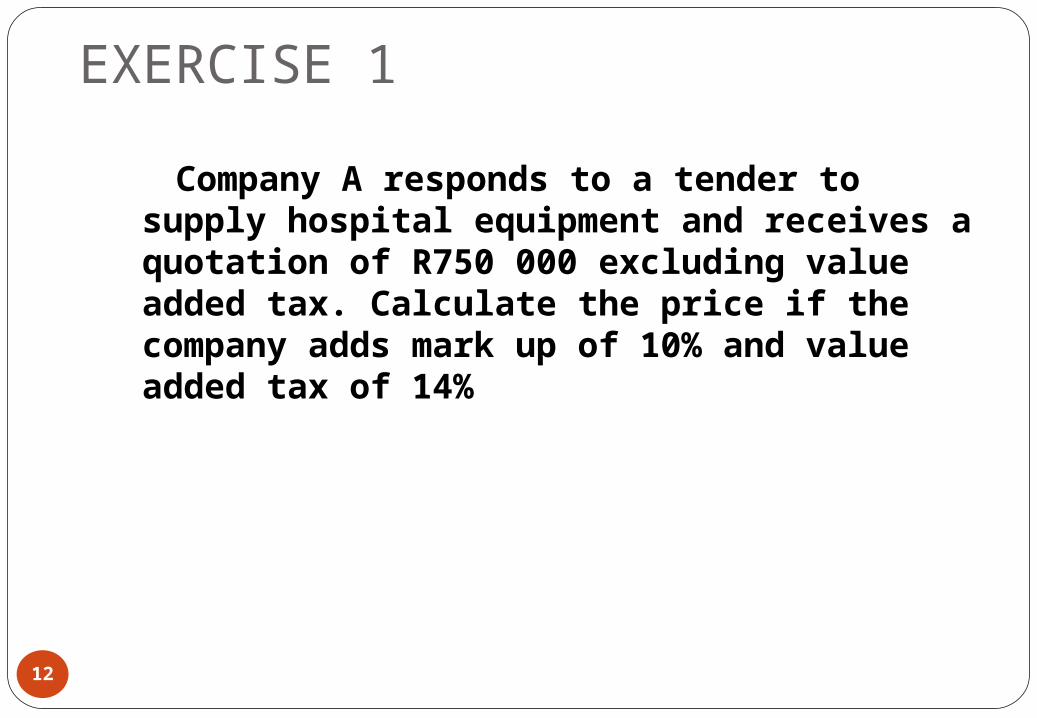

EXERCISE 1

12

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

EXERCISE 1

13

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

Cost price =R750 000,00

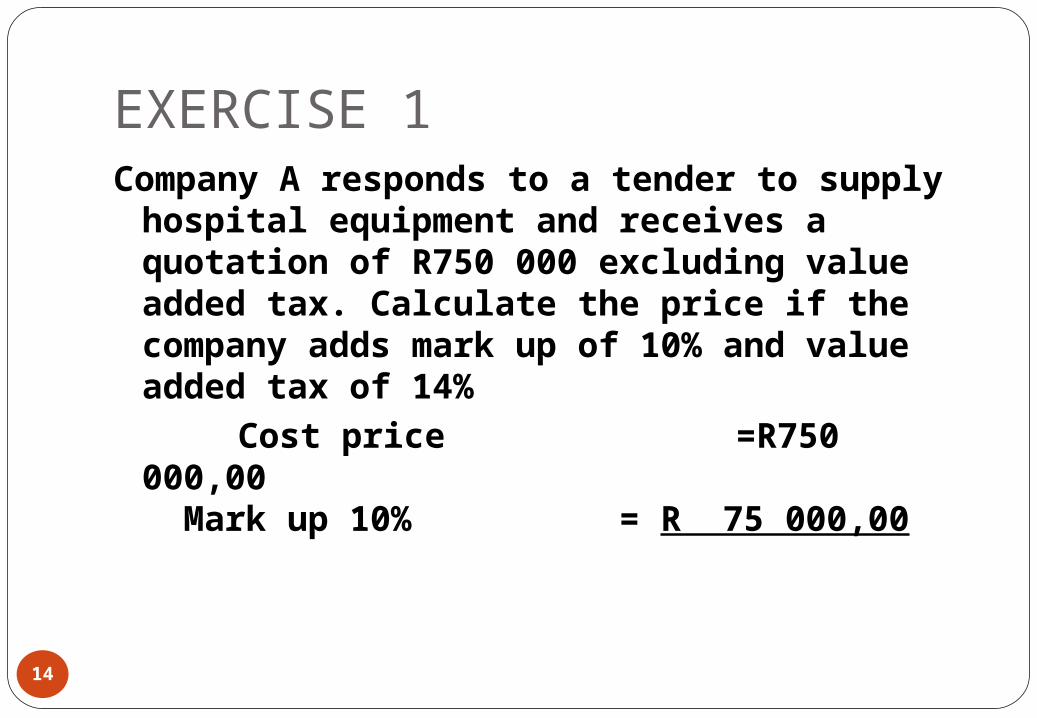

EXERCISE 1

14

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

Cost price =R750 000,00 Mark up 10% = R 75 000,00

EXERCISE 1

15

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

Cost price = R750 000,00 Mark up 10% = R 75 000,00 Total price (exc) = R825 000,00

EXERCISE 1

16

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

Cost price =R750 000,00 Mark up 10% = R 75 000,00 Total price (exc)= R825 000,00 VAT = R115 500,00

EXERCISE 1

17

Company A responds to a tender to supply hospital equipment and receives a quotation of R750 000 excluding value added tax. Calculate the price if the company adds mark up of 10% and value added tax of 14%

Cost price =R750 000,00 Mark up 10% = R 75 000,00 Total price (exc)= R825 000,00 VAT = R115 500,00 Total price (incl) = R940 500,00

EXERCISE 2

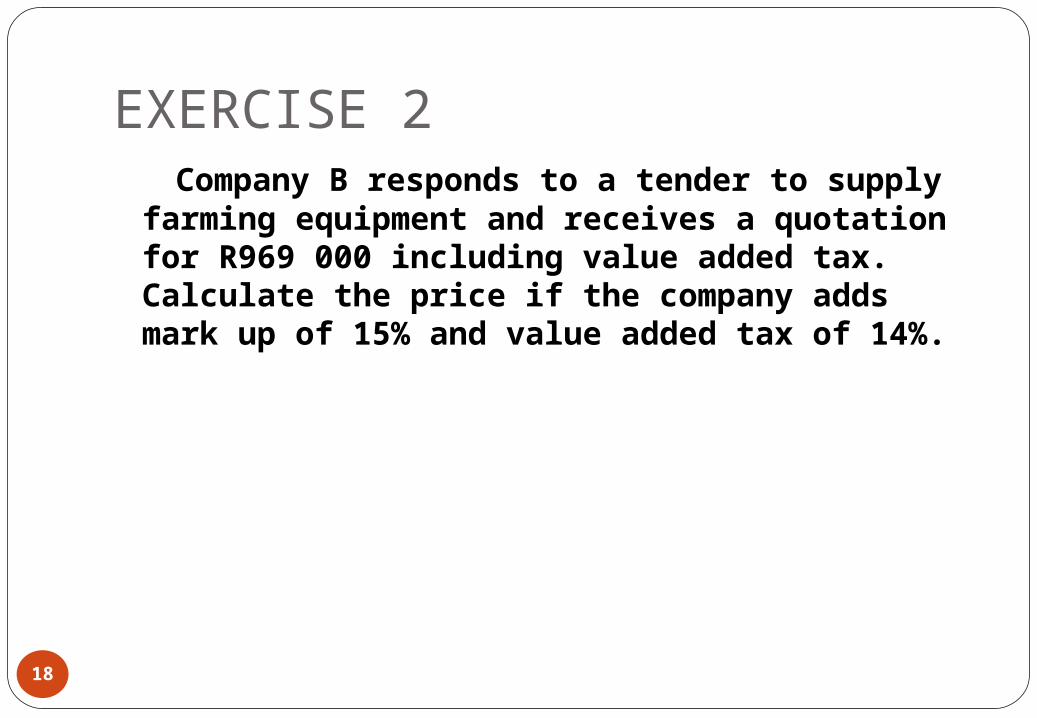

18

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

EXERCISE 2

19

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00

EXERCISE 2

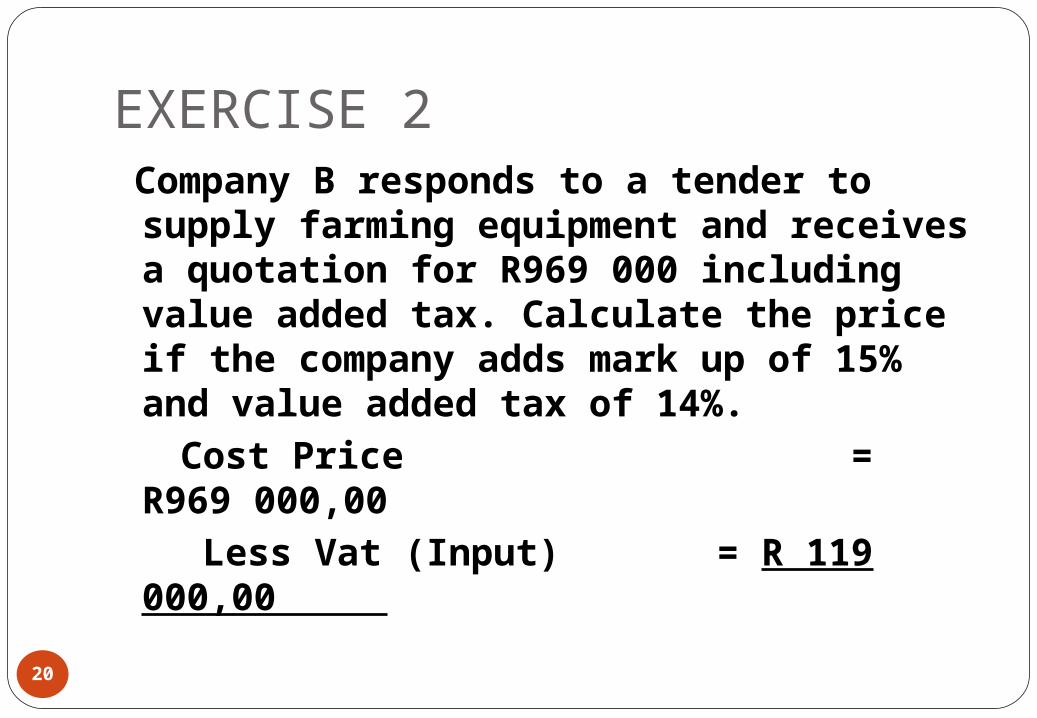

20

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00 Less Vat (Input) = R 119 000,00

EXERCISE 2

21

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00 Less Vat (Input) = R 119 000,00 = R850

000,00

EXERCISE 2

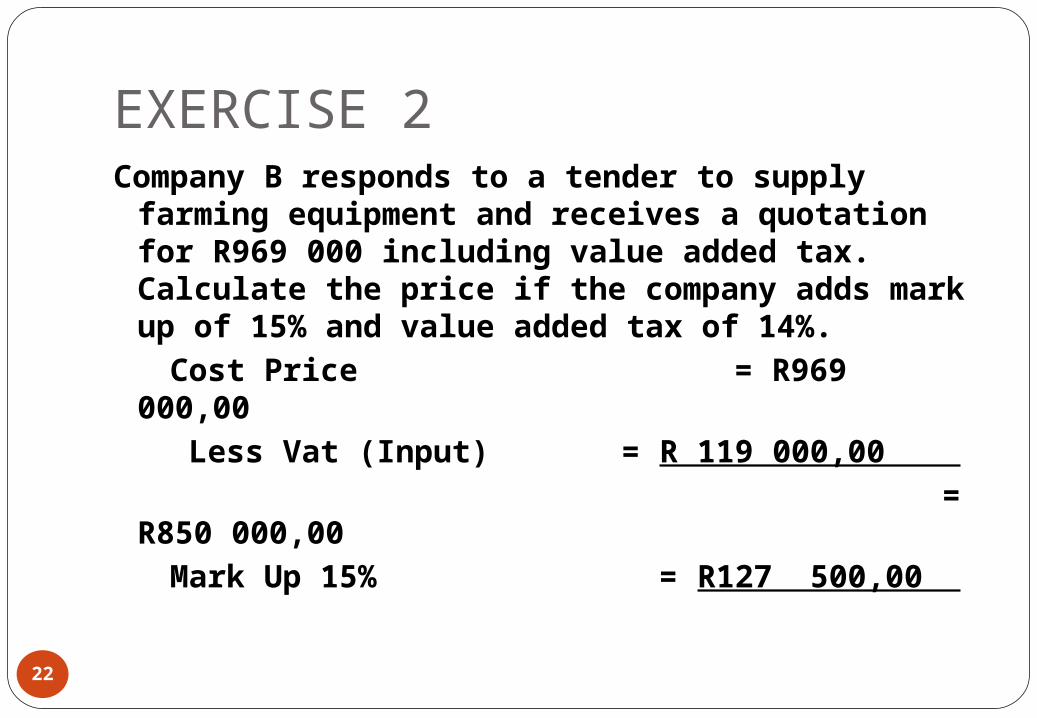

22

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00 Less Vat (Input) = R 119 000,00 = R850 000,00 Mark Up 15% = R127 500,00

EXERCISE 2

23

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00 Less Vat (Input) = R 119 000,00 = R850 000,00 Mark Up 15% = R127 500,00 Total = R977 500,00

EXERCISE 2

24

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R969 000,00 Less Vat (Input) = R 119 000,00 = R850 000,00 Mark Up 15% = R127 500,00 Total = R977 500,00 Add Vat (Output) = R136 850,00

EXERCISE 2

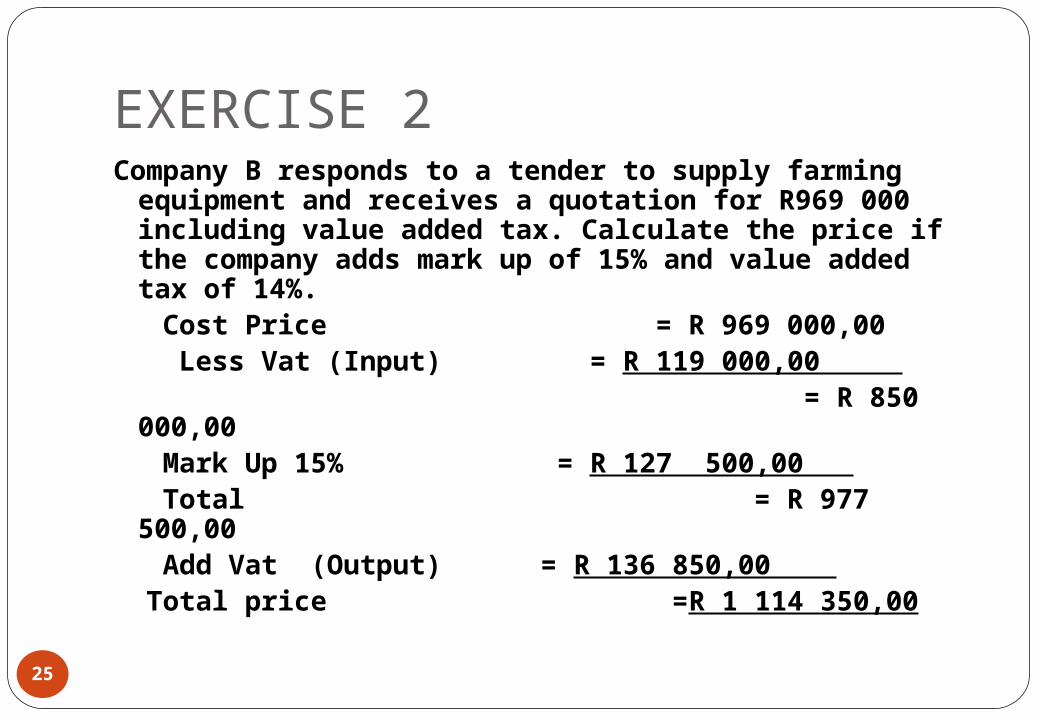

25

Company B responds to a tender to supply farming equipment and receives a quotation for R969 000 including value added tax. Calculate the price if the company adds mark up of 15% and value added tax of 14%.

Cost Price = R 969 000,00 Less Vat (Input) = R 119 000,00 = R 850 000,00 Mark Up 15% = R 127 500,00 Total = R 977 500,00 Add Vat (Output) = R 136 850,00 Total price =R 1 114 350,00

Vat Payable

26

Vat payable = Output tax less Input tax

Formula = Price x rate/ 100 + rateOutput = R 1114350,00 x 14 114 R 136 850,00Input = R 969 000,00 x 14 114 R 119 000,00Vat payable = R 136 850,00 - R 119

000,00 R 17 850

Tools required

27

LaptopAccess to internet – 3G data cardData projectorTraining venueWill to learn

28

Thank You

29

Sello & Associates [email protected]

www.facebook.com/tender.opportunities www twitter.com/BooksySello

Mobile : 0847976212 Fax : 0865152849

f