Embed Size (px)

DESCRIPTION

A detailed graduate level report on the need and design of prediction markets in currency exchange forecats

Citation preview

Page 1 of 10

Prediction Markets in Currency Exchange Forecasts

SI 679 Research Paper

By,

Aditya Doshi

School of Information, University of Michigan

Page 2 of 10

Introduction:

The paper will give a brief description of the existing system and the need for a market

for determining currency exchange rates for the near future. It will then explain the need and

usefulness of a prediction market in this domain and propose a market design for such a

prediction market based on certain criteria’s such as security design, the trading mechanisms, use

of real money or play money, and interfaces. It then lightly discusses the strategic concerns of

having such a market as well as some ethical issues. The paper ends with a comparison to other

predicting mechanisms and recommendations to implement this market.

Forecasting problem and scope:

Currency values have come a long way from being determined by the actual gold

reserves of a country to having currencies relative to the US$. Most markets today allow for

trading on the currency futures.

Predicting exchange rates is not easy as many factors work at determining these rates. A

few important factors include:

1. Interest rate movements – the national interest rates have a significant effect on the

exchange rate; as this determines the flow of money in a country, hence causing an

appreciation of that currency and in turn the exchange rate.

2. Economic prospects – the economic prospects of an economy depends on the

inflation rates and general economic situation of the country. This in turn affects

interest rates and expectations towards devaluation of a currency.

3. Political policy and government control – policies and political conditions play an

important role in determining the growth prospects of a country and its economy and

affects currency exchange rates.

It is very important for most people specially hedgers to have an accurate knowledge of

this exchange rate movement in advance to cut risks in present international transactions. These

Page 3 of 10

people resort to currency futures markets and trade in currency future contracts1 and currency

forward contracts2 to hedge against volatility in exchange rate prices.

In this paper we shall study one of the many big organizations that gets affected by the

change in currency rates over a period of time. The company under consideration is ‘Infosys’

which is India’s second largest software services company. In the summer of 2007 when the

Rupee appreciated by more than 7% against the Dollar, Infosys made a strategic decision to cut

its dependence on the US market from 63% to 50%; this was a risk mitigating effort. The

company also participates in the recently opened3 currency futures market as a hedging

mechanism4. Hence we herewith analyze the company’s use of a prediction market to make

accurate buys/sells on the currency futures market.

Use of prediction markets:

Since the exchange rate varies according to various factors such as interest rates, political

policies, growth prospects in industry and government control, there are many people possessing

different tidbits of insider knowledge and publicly available knowledge.

This knowledge can be categorized into three groups – firstly, the knowledge that

everyone knows and gives one no competitive advantage, secondly, knowledge that gives no

advantage but not knowing it can be potentially damaging, and thirdly, insider knowledge that is

private and can be exploited to an advantage.

A prediction market mainly provides incentive to seek this knowledge and aggregates a

diverse opinion to project accurate forecasts. Hence prediction markets are also called as ‘strong

form’ efficient markets, where the prices reflect all available information, including private

information. Moreover, these markets are dynamic and factor in continuous time compared to

having polls that are periodic and static.

1 Currency futures contract allow investors to hedge against foreign exchange risk. Investors can exit their obligation to buy or sell the currency prior to the contract’s delivery date. 2 Currency forward contracts obligate the contract holder to buy or sell the currency at a specified price, at a specified quantity and on a specified future date. These contracts cannot be transferred. 3 The currency futures market for trading on $ vs. Rs was opened to residents in India in August, 2008. 4 Infosys was assuming a rate of Rs 40.58 to a dollar in its forecast and has not factored any large deals. It has hedged $925 million at Rs 40.58. Mr. Balakrishnan said adding “if required we will increase the hedging”. – (2007, The Hindu Business)

Page 4 of 10

Hence we see that prediction markets provide investors with a hedging mechanism

against future events, a sort of insurance against volatility that cannot be insured elsewhere; and

is beneficial to exporters and importers who wish to hedge against volatility in currency rates.

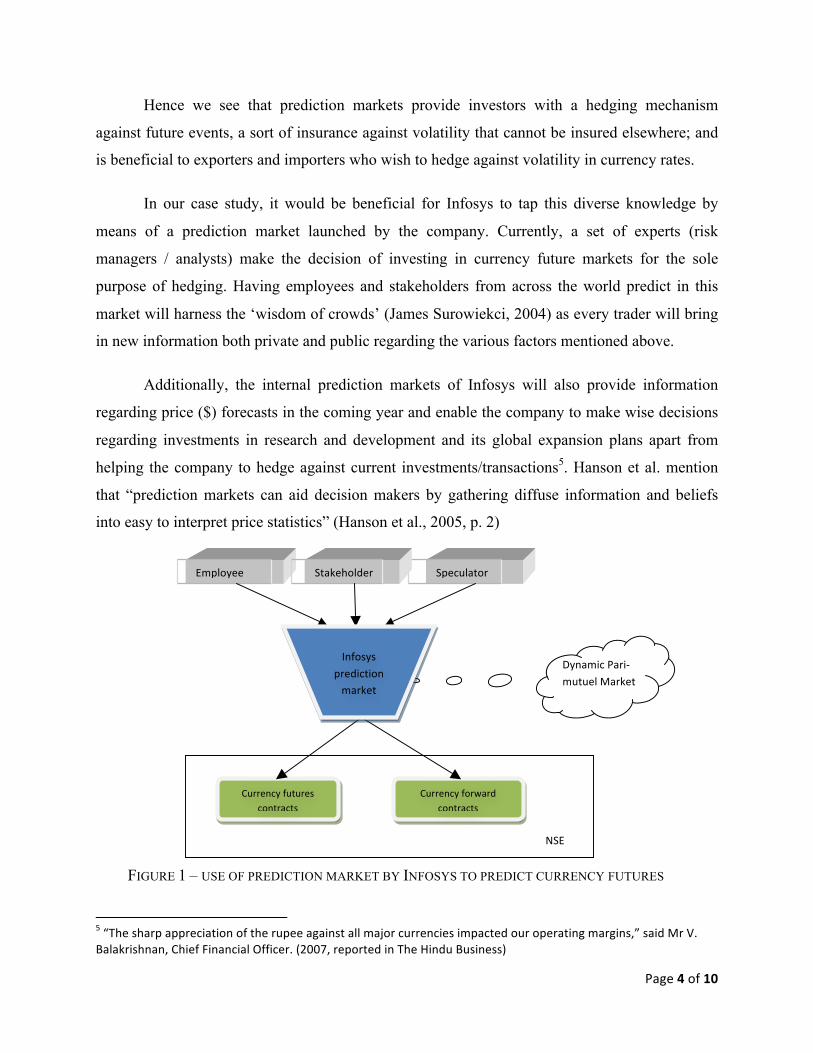

In our case study, it would be beneficial for Infosys to tap this diverse knowledge by

means of a prediction market launched by the company. Currently, a set of experts (risk

managers / analysts) make the decision of investing in currency future markets for the sole

purpose of hedging. Having employees and stakeholders from across the world predict in this

market will harness the ‘wisdom of crowds’ (James Surowiekci, 2004) as every trader will bring

in new information both private and public regarding the various factors mentioned above.

Additionally, the internal prediction markets of Infosys will also provide information

regarding price ($) forecasts in the coming year and enable the company to make wise decisions

regarding investments in research and development and its global expansion plans apart from

helping the company to hedge against current investments/transactions5. Hanson et al. mention

that “prediction markets can aid decision makers by gathering diffuse information and beliefs

into easy to interpret price statistics” (Hanson et al., 2005, p. 2)

FIGURE 1 – USE OF PREDICTION MARKET BY INFOSYS TO PREDICT CURRENCY FUTURES

5 “The sharp appreciation of the rupee against all major currencies impacted our operating margins,” said Mr V. Balakrishnan, Chief Financial Officer. (2007, reported in The Hindu Business)

Employee Speculator Stakeholder

Dynamic Pari-‐mutuel Market

NSE

Currency futures contracts

Currency forward contracts

Infosys prediction market

Page 5 of 10

Market design:

Security Design

The event that would be traded on would have a question such as “What would the

foreign exchange rate for $ vs. Rs be for the month of ‘X’?” where X would be a month in the

next 12 months6. This means that the company would have 12 markets running at the same time,

one for predicting the price for each month. The trade would be open 24x7 and last for a month

or until the company has locked its futures contracts on the NSE (National Stock Exchange) for

that month depending on the prediction in its own market. This monthly time frame allows for

information gathering and trading in respectable volumes.

The security traded on the Infosys prediction market will be a type of Index contract

where the trader will get Rs. X in the future if the price of the Dollar is X. The trading price

initially will be the current price of the $ equal to the Reference Rate for the day, as set by the

Reserve Bank of India. In equilibrium, the market would converge at the best forecast of the

future rate which can then be used to make a decision by the company to buy/sell on the futures

exchange of currency futures.

For example, if the current reference rate is 44.567 for the month of December and

traders feel that the rate would be 45.567 in February, they would buy the contracts @ 44.567 (or

at any amount till 45.566 rationally) and on maturity if the rate is more than the trading price

today they stand to make a profit. Hence rational traders drive the current prediction market rate

towards 45.567 and hence the company can trade on a futures market to buy contracts for

45.567.

The size of each such security / contract shall be $100 and these contracts will be quoted

and settled in Indian Rupees when the futures contract is settled in the respective month. The

prices will reflect up to the fourth decimal digit of the rate (0.000X) and rounded off thereafter,

this would reduce any exchange rate arbitrages. These contracts shall be traded on the Infosys

prediction market, an internal exchange run by the company.

6 The Reserve Bank and SEBI have set guidelines for the trade on currency futures with maturity of contracts within 12 months. Hence only futures for within the next 12 months are traded upon.

Page 6 of 10

Trading Mechanism

The Infosys prediction market should implement the Dynamic Pari-mutuel Market

(DPM) which is a hybrid between a pari-mutuel and a Continuous Double Auction (CDA)

market. Since the Infosys prediction market is a company market and would have lesser volumes

being traded by lesser traders, it would be wise to implement a DPM which provides infinite

buy-in liquidity and has zero risk for the market institution (Infosys). The pari-mutuel market

overcomes the problem of having thin markets by allowing for buy-in trade continuously, thus

encouraging traders to share their new information immediately. Moreover it incorporates the

advantages of a CDA by allowing users to take out profit/loss before the event is resolved. This

helps as most employees are marginal players and would like an option to limit losses.

Additionally, as the prediction market is for the sole purpose of decision making by the company

and not meant for making profits from it, the DPM is the correct choice. In DPM the market pays

out exactly the amount taken in; that is the money is only redistributed amongst the traders. The

market maker makes no profit or loss.

Real money or Play money

The prediction markets with real money and play money give similar accurate results of

forecasts. This was proved by the experiments of Servan-Schreiber and Slamka et al. Servan-

Schreiber further mention that real money markets gave better incentive for information

discovery. Since the currency futures depend on so many varied factors and the company would

encourage the traders to discover information in each field to provide more than the public

knowledge available to everyone, the use of real money is preferred in this market design. It also

encourages speculators by providing them incentive to trade in the market and bringing in more

traders thus reducing the problems of thin market. Moreover, the traders have incentive for

truthful revelation of facts, as they stand to gain or lose real money and this can be a mechanism

to handle the effects of information cascades and manipulation. Play money markets would be

better if the company wanted to predict an internal forecast from employees only, for example

the company sales or sentiments regarding an issue. But as the information required is at a global

level and people outside the company, i.e. people from banks, government administration, US

citizens, financial brokers and market watchers, take part in the prediction; real money would be

a good choice for this market.

Page 7 of 10

Specific Interface Design / Implementation Concerns

Since the prediction market is used mostly in-house and by non-experts and experts alike,

we would keep the interface simple with explanations and cause-effect panels. These panels

would show the results of potentially choosing to buy or sell a certain amount of shares. Also

would be included is an option to limit order. Since we are using a DPM which has a sort of

automated market maker for buy-in, it would be wise to provide trader with a limit order option

to check buy/sell prices. Also on the lines of limited trading the system would check a trader

from not trading more than a certain amount (say $500) on a single day, this would be a good

check for manipulation and reduce the risk of one trader having major influence on the market

(considering smaller marginal employees are also trading on the same market). Moreover the

system would maintain an order book and display the current holdings of a given trader in his

screen to aid long term memory. Lastly, the most important display on the screen would be a

dynamic price chart which would show the price fluctuations every 30 secs and would also have

a sidebar showing digital price fluctuations (a combination of what is shown below).

FIGURE 2 – ELEMENTS OF SPECIFIC INTERFACE DESIGN FOR INFOSYS PREDICTION MARKET

Page 8 of 10

Strategic concerns

Hanson et al. mention that prediction markets are “susceptible to price manipulation by

agents who wish to distort decision making”. Some individuals who wish to control the policy of

a company indirectly can be willing to make some monetary loss for this purpose. Thus a

company implementing prediction markets for decision making purposes needs to be aware of

such manipulation activities. The experiment carried out by Hanson et al. showed that when the

market agent suspects the presence or is aware of the presence of manipulators or the direction of

manipulation, manipulation is ineffective. Strong mechanisms to check manipulation thus need

to be in place. A step towards controlling this is to have a limit on each trader’s activity as

mentioned above. This reduces the influence of a single trader in a single day and gives time for

rational players in the market to drive the price back to rational equilibrium. Other steps such as

checking for irrational behavior, out of bound predictions can also be implemented. Furthermore,

the trading interface hides other trader’s detailed activities so as to prevent information cascade.

Only the current price in digital form and an analog graph of past activity is shown.

Policy and ethical concerns

Since prediction markets are a recent domain it is not yet differentiated from gambling

markets that are illegal in India. Many laws under the IPC prohibit lottery and any form of

gambling. But taking cue from arguments for prediction markets elsewhere (Europe, USA)

policy makers can allow for prediction markets for non-profit and decision making purposes. As

in-company markets are generally small scale markets and have no clear speculative interests,

soon a policy should be in place to make such markets legal. Arrow et al. argue in their paper

that regulators should lower barriers to create small stake markets which help private firms

manage economic risks. They also mention that these markets need to be separated from

regulations that govern gambling markets. As on today, Infosys being a global company can start

an online prediction market whose exchange is based offshore in Europe (or some parts of USA).

This will allow for traders to legally trade in the market until Indian policies change. Moreover

as they implement a DPM trading mechanism; wherein the exchange stands to make no profit

from the transactions apart from having access to valuable information for decision making

purpose; it would be regarded as a non-for profit market and bypass American gambling laws.

Page 9 of 10

Strengths and weaknesses w.r.t alternative forecasting methods

Currently decision making takes place with the consensus of a panel of experts also

called risk managers within the company or by analysts in a professional risk management and

consulting firm. They follow techniques such as Nominal Group technique or the Delphi process.

These techniques specially the Delphi allow for accountability and justification of predictions

which is not possible in prediction markets that are completely anonymous, hence there is chance

of manipulation in prediction markets. It is also said that prediction markets work best by

“deriving their power from aggregating the information of a diverse group of participants.”

[Buckley, P. Managing prediction markets, in proceedings of MIS’s 47th conference, (2009),

ACM, pg.217-220.] Hence when the advising body size is small or there is a thin market or few

traders, there are chances of manipulation or polarization.

One of the strengths of prediction markets is its capability to factor in new information

almost instantaneously and at all times. Also in real money prediction markets there is incentive

for truthful revelation of information and to search for newer information when the stakes are

high enough. Hence, making the information and the process more credible.

Overall recommendations / Conclusion

Hence we see that under proper policies and by implementing a good market design for

the prediction market, a company such as Infosys can be benefited by being able to aggregate

diverse opinions of people, both within and outside the company, and this in turn would help

them in decision making regarding hedging funds in the currency futures market as well as

company policy formulation for the near future. A play money prediction market might also

accurately enough help small exporters and importers to hedge against currency volatility. With

better evaluation and trading mechanisms prediction markets would turn to be great information

sources and decision-making systems in the near future.

Page 10 of 10

References

1. Prediction Markets, Wolfers and Zitzewitz, The Journal of Economic Perspectives 18(2), 2004 2. Comparing Face-‐to-‐face Meetings, Nominal Groups, Delphi and Prediction Markets on an Estimation

Task, Graefe and Armstrong. 3. Information Markets: A New Way of Making Decisions -‐ Chapter 4: Deliberation and Information

Markets, Cass R. Sunstein. 4. Buckley, P. Managing prediction markets, in proceedings of MIS’s 47th conference, (2009), ACM,

pg.217-‐220. 5. Combinatorial Information Market Design, Hanson, Information System Frontiers (5), 2001. 6. Dynamic Parimutuel Markets, Pennock, ACM EC'04 7. Information Aggregation and Manipulation in an Experimental Market , Hanson, Oprea, and Porter,

Journal of Economic Behavior and Organization 2006. 8. The Promise of Prediction Markets, Arrow et al, Science (320), May 2008. 9. Prediction Markets as Decision Support Systems, Joyce E. Berg and Thomas A. Rietz. (2003) 10. Currency future. (2009, December 16). In Wikipedia, The Free Encyclopedia. Retrieved 19:23,

December 17, 2009, http://en.wikipedia.org/w/index.php?title=Currency_future&oldid=331967748 11. http://www.banknetindia.com/banking/80816.htm 12. https://dealbookweb.demo.gftforex.com/