Embed Size (px)

Citation preview

PPC Hearing on Convergence Bill

August 2005

Parliamentary Portfolio Committee Hearings on the

Convergence Bill

Prof Alison GillwaldLINK Centre

Graduate School of Public and Development ManagementWitwatersrand University

10 August 2005

PPC Hearings on Convergence Bill

August 2005

• Response to ICT policy and regulatory training and research vacuum

• Independent, multidisciplinary ICT policy and regulatory training and research centre

• Professional development training through to post graduate courses - Master of Management ICT PR, PhD

• To satisfy the growing demand for information and analysis needed for appropriate policy formulation and effective regulation •Africa research network – Research ICT Africa! - to build research capacity and inform decision-making and governance structures • Create body of African public domain research and debate and to provide a repository of data, metadata, analysis and knowledge

Research

Learning Information Networking and Knowledge (LINK) Centre

PPC Hearings on Convergence Bill

August 2005

Purpose of presentation

• In policy, like driving, although the windscreen seems to provide the obvious view for where you need to go it is critical to look back through the review mirror before trying to proceed forward.

PPC Hearings on Convergence Bill

August 2005

Is intervention needed?• Why don’t we just carry on as we are?

– Results of first two rounds of reform only partially achieved objectives

• Strong growth: 1994 – 2002 of around 5 billion a year.

• 2003/4: flatter growth - still 14%

• R 74 billion revenues (2004)

• 6% contribution to GDP (2004)

• Fixed line teledensity < middle income countries (excl

Mexico, Morocco)

• Evidence of high costs inhibiting growth

PPC Hearings on Convergence Bill

August 2005

Telecom

• Fixed– Commercial successful fully digitised, partially

privatised, high shareholder value public network

– Social mandate largely failed: little progress on affordable universal service (high retail prices/monopoly rents)

– National economic contribution: high wholesale prices and evidence of anti-competitive behaviour; high input cost to cost of business, disincentive to investment

– De facto monopoly, SNO delays– Not critical mass, no network effects, limited

multipliers

The South African Communications Sector Review

PPC Hearings on Convergence Bill

August 2005

SA: Telephony Access, 2001No access

Fixed & mobile access

Fixed access only

Mobile access only

At a neighbour nearby

Public telephone nearby

Another location nearby

Neighbour not nearby

Household Telephone Penetration – 2001 Census Source: USA

The South African Communications Sector Review

PPC Hearings on Convergence Bill

August 2005

Access remains racially skewed

The South African Communications Sector Review

South Africa: Percentage of households with telecommunications access 2001

12.0

43.2

74.878.6

24.424.631.0

58.9

74.6

32.3

0

10

20

30

40

50

60

70

80

90

Black African Coloured Indian/Asian White Total

Telephone in dw elling Cell-phone

From: RIA! Towards an African e-Index 2005 2001 Census

PPC Hearings on Convergence Bill

August 2005

PSTN Affordability

South Africa: Telephone tariffs 1997 - 2004 (in Rand)

81.949.6

171.0

274.35

227.44

61.80

0306090

120150180210240270300

1997 1998 1999 2000 2001 2002 2003 2004

Residential monthly telephone rental

Residential telephone connection charge

Fix ed line - cost of 10 hours w orth of calls per month (peak rate)

Telkom prices 1997 – 2004 = 21% CAGRTreasury report – telecoms prices excessiveLabour Commission - measurable impact on inflation Productivity factor = 1,5% (UK = 7.5%, USA = 6.5%, Mexico = 3%)Efficiency Research – SA Foundation

The South African Communications Sector Review

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

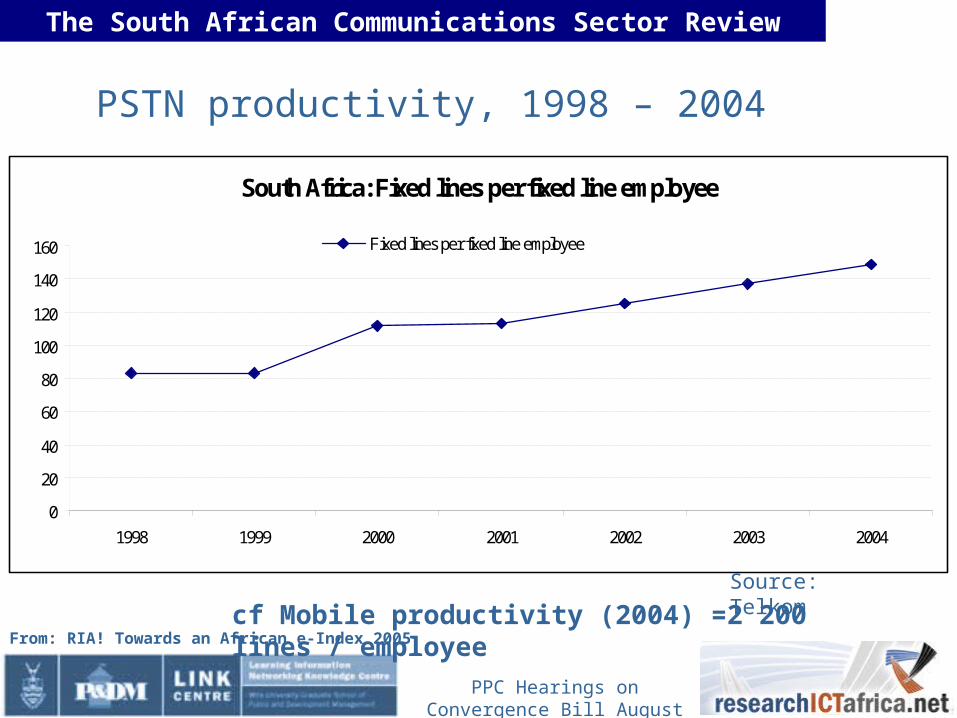

PSTN productivity, 1998 – 2004

South Africa: Fixed lines per fixed line employee

0

20

40

60

80

100

120

140

160

1998 1999 2000 2001 2002 2003 2004

Fixed lines per fixed line employee

Source: Telkomcf Mobile productivity (2004) =2 200 lines / employee

The South African Communications Sector Review

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

Why is intervention needed? 2

• Mobile– Major contributor to universal access– Relatively unregulated– High prices (SA Foundation & ICASA regs)– Price setting characteristic of duopolies– Critical threshold for network effects to kick in – Economic and social multipliers

• USALs- Unenabling regulatory environment, stripped of

business case, essentially mobile franchisees – no innovation around ownership, technology, and access.

PPC Hearings on Convergence Bill

August 2005

Telephony rollout, SA (1997 – 2004)

Sources: Telkom, Vodacom, MTN, Cell C

The South African Communications Sector Review

South Africa: Mobile and Fixed Line Growth 1997 - 2004

0

10

20

30

40

50

60

1997 1998 1999 2000 2001 2002 2003 2004

Total mobile subscribers per 100 inhabitants

Total f ixed-line telephone lines per 100 inhabitants

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

Mobile Telephony Tariffs

The South African Sector Review

South Africa: Mobile operator peak rate charges in Rands - 2003 & 2004

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2003 2004

Contract av erage cost per minute Prepaid av erage cost per minute

Sources: MTN, Vodacom & Cell C w ebsites and LINK SPR Report 2003

Note: Tariffs are based upon calls to other netw orks

From: RIA! Towards an African e-Index 2005

PPC Hearing on Convergence Bill

August 2005

PRE-PAID STANDARD PLANS (2005)

R 0.00

R 0.50

R 1.00

R 1.50

R 2.00

R 2.50

R 3.00

PEAK OFF-PEAK PEAK OFF-PEAK PEAK OFF-PEAK

ON-NET CALLS (/Telkom Local) CALLS TO OTHER MOBILE CALLS TO FIXED LINE

Cell C MTN Vodacom

ICASA Mobile Pricing Discussion Paper August 2005

PPC Hearings on Convergence Bill

August 2005

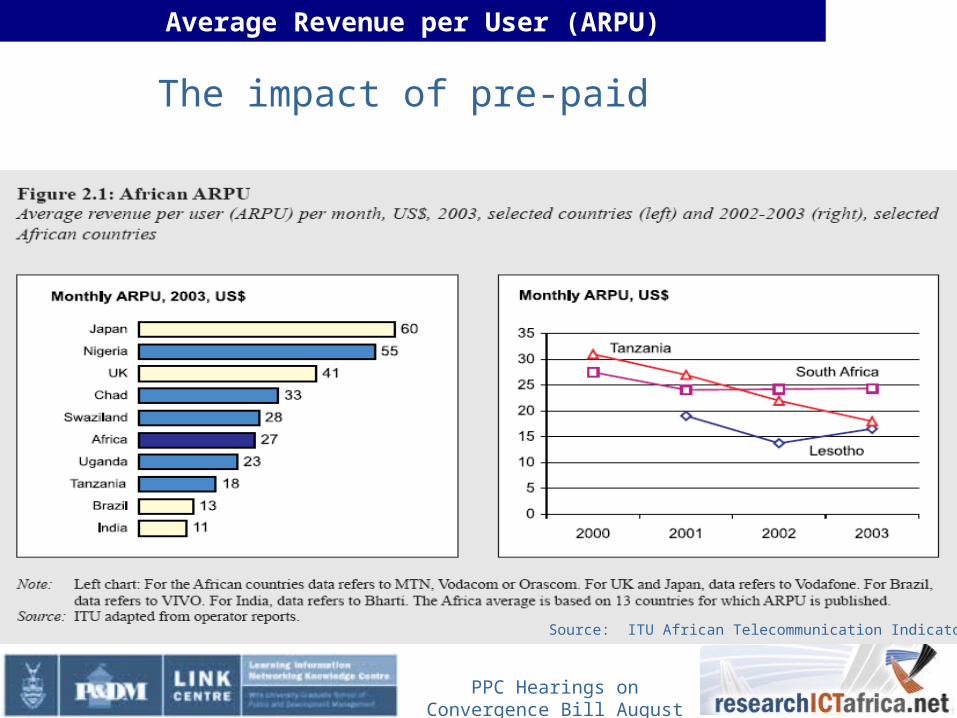

Source: ITU African Telecommunication Indicators 2004

Average Revenue per User (ARPU)

The impact of pre-paid

PPC Hearings on Convergence Bill

August 2005

Is intervention needed? 3

• VANS– Telkom’s dominance of this competitive segment of

the market and requirement to acquire facilities by competitors from Telkom chilling effect.

– Ministerial directives good, claw back on self-provisioning in monopoly environment negative.

• Internet– 80% of ISP costs directly to Telkom– Internet penetration plateaued– Purposes of Electronic Communications Transactions

Act undermined

-

PPC Hearings on Convergence Bill

August 2005

Cost of Internet Access

South Africa: Average ISP costs vs. fixed line cost of 20 hours internet access vs. % growth of total internet subs.

R 124 R 154 R 184R 252 R 252

R 396R 446 R 455

R 80R 80

R 88

R 90

R 94

R 100 R 104

R 89

0

100

200

300

400

500

600

1997 1998 1999 2000 2001 2002 2003 2004

Average ISP costs (Rands)*Fixed line - cost of 20 hours worth of calls per month (peak rate) % growth of total internet subscribers

The South African Communications Sector Review

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

Internet Growth (1997 – 2004)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1997 1998 1999 2000 2001 2002 2003 2004

Corporate users Dial-up subscribers Academic users

The South African Communications Sector Review

Source: RIA! Towards an African e-Index 2005

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

Broadband• 656 000 ISDN subscribers (2004)• 60 000 ADSL subscribers (2005)• Vodacom & MTN - 3G (2005)• SA lags other middle-income countries

Such as: – Brazil: 600,000 (2002)– Argentina: 65,000 (2002)– Poland: 193,000 (2003)– Malaysia: 110,000 (2003)

Comparative broadband charges 2004

0

100

200

300

400

500

600

CzechRepublic

Malaysia Turkey Poland Argentina SouthAfrica

0

20

40

60

80

100

120kbit/s Monthly charge US$

The South African Communications Sector Review

From: RIA! Towards an African e-Index 2005

PPC Hearings on Convergence Bill

August 2005

•The pressure on ISP fees can also be illustrated by examining the pricing of ADSL broadband. The monthly Telkom fee on a business ADSL connection is R699. •In addition, the subscriber must acquire an ISP connection, at an average monthly cost of R250. •The ISP pays Telkom R190 for bandwidth and R40 to conclude peering arrangements with South African Internet Exchange (SAIX) (needed to deliver email rapidly). •Thus, on a product which costs a total of R949, Telkom keeps R929, leaving the ISP with R20 in revenue.

The South African Communications Sector Review

Source: SA Foundation 2005

PPC Hearings on Convergence Bill

August 2005

Broadcasting• SABC – comprehensive PBS in radio and TV• E-TV - free to air competitor• Community radio – widespread but marginal• Subscription service among the most

advanced in the world, operating globally• Sentech multimedia and international

gateway licence• Orbicom, other SD competitors

PPC Hearings on Convergence Bill

August 2005

Regulatory environment• Broadcasting reasonably effective:

– Relatively successful privatisation of SABC regional radio stations and licensing of greenfield licences

– Widespread community radio licensing facing issues of sustainability

– Local content music and TV increased and in demand– Independent production still requiring further

transformation but gains made– Wider use of official language across free-to-air

channels and stations• Achieved under relatively unfettered

regulatory conditions but looking primarily at domestic investment

• Challenges: Digital broadcasting policy – benefits and dangers of delays

PPC Hearings on Convergence Bill

August 2005

Regulatory environment 2 - telecom

• Mechanism in law to deal with the anticipated market failure – absence of access, inefficiencies, monopoly rents, interconnection and facilities disputes, anti-competitive practice

• Regulator under-resourced and under-skilled and structurally compromised by law .

• But even experienced regulators unable to deal with inherent asymmetries of information, particularly in case of vertically integrated monopoly.

• Creates anti-competitive incentives by playing across competitive and non-competitive elements

• Access regulation associated with this highly resource intensive

• Together with pressures of licensing new entrants, regulator ineffective system failure delays in introduction of competitors, anti-competitive practice, high retail and wholesale prices.

• Conflict of interest for Minister as major shareholder of incumbent, policy maker for sector and licensor of competitors -

PPC Hearings on Convergence Bill

August 2005

Does the bill address these issues?Main fault lines:

– Absence of policy, no common vision, like to lead to conflicting expectations and challenges

– market structure – creates licensing framework for converged market but does not indicate how market will be horizontally restructured so retains industrial silo approach to telecoms with vertically integrated companies with multiple horizontal licences

– No attention to de facto monopolies at either end of the system – LLU and undersea cable essential facilities or at core – self provisioning.

– Critical regulatory framework absent, essentially futile exercise without the accompanying ICASA Act – omnibus legislation and inclusion of process provisions aligned to Administrative Justice.

– potentially tensions between consumer welfare and investment, policy and regulation, new entrants and incumbents on network and equipment supply, content and infrastructure.

• Essentially COMMUNICATIONS ACT of which convergence is one aspect

• Broadcasting Act with all content matters in that or all broadcasting issues effectively integrated into Communications Act

PPC Hearings on Convergence Bill

August 2005

Objects of the Act• Convergence of telecommunications and

broadcasting (signal distribution)X

• Broadcasting – public, commercial, community √• Connectivity for all – quality, affordable X• Investment and innovation X• Efficient radio spectrum usage X• Competition X• Open network access & interoperability X√• Information security & network reliability √• Multi-channel distribution systems X• BEE, HDI, R&D X• Distinguish policy and regulation X

– Ministerial powers (substantive and process) vs regulatory powers (process)

PPC Hearings on Convergence Bill

August 2005

Some specifics of the Bill requiring attention

• Licensing framework, questions of categories (especially appropriateness of application and content services and location of spectrum licence) and types (individual, class, exempt)

• Continued co-jurisdiction on major licences and spectrum planning between Ministry and ICASA

• Process requirements: Ministerial directives and regulations

• Interconnection required at service and network level.• Competition: in not fully liberalised environment anti-

competitive behaviour requires sectoral knowledge and experience that seldom resides in a general competition agency, who are better suited to deal with issues of mergers and acquisitions than technical sector specific anti-competitive practices.

• Consumer code of practice strengthened by penalty clauses for infringing code of practice.

PPC Hearings on Convergence Bill

August 2005

Intergrated information policy

• Access

• Pricing

• Quality

Broadcasting – content Public broadcasting Genres Local content Independent production

IP

• Internet

Information policy

•Industrial policy

•Innovation policy

• Regulated competition

• IPR

• Privacy

• Surveillance

Sector regulation - public utility - consumer welfare

Competition – perfect markets

Telecommunications - infrastructure

International governance

National policy

PPC Hearings on Convergence Bill

August 2005

What is to be done?• Information society initiatives across the globle – Europe

described as messy, contradictory and uncritical• Recognise tensions between objectives of consumer welfare,

investment, industrial policy - prioritise and create tools to manage them

• Integrate information policy across line ministries – communications, trade and industry, science and technology, arts and culture

• Human capital development - Specialised decision-making agencies require specialised owned knowledge – PPC, DOC, ICAS, USA.

• Without highly skilled, realistically resourced, politically and commercially unfettered, transparent and publicly accountable regulation, the objectives of this bill will not be met:

• Complete package to be effective – degree of market failure inevitable, regulatory failure can destroy market.– No consumer welfare – access or affordably– No investment– No effective competition– No pervasive, seamless affordable integrated infostructure for

national economy• Regulation engine of policy, licensing framework, transmission

system.

PPC Hearings on Convergence Bill

August 2005

More information on..

http://link.wits.ac.zahttp://www.researchictafrica.net

or contact:

Wits LINK Centre,011 - 7173913

![Page 1 Vodafone presentation to the Parliamentary Portfolio Committee on Communications Convergence Bill [B9-2005] 17 August 2005](https://img.dokumen.tips/doc/110x75/56649f015503460f94c16c1f/page-1-vodafone-presentation-to-the-parliamentary-portfolio-committee-on-communications.jpg)