Embed Size (px)

Citation preview

Healthy TensionFiguring Out the Auto Scene Dan Dembicki, Business Development Mgr.R. L. Polk & Co.

Healthy TensionFiguring Out the Auto Scene Dan Dembicki, Business Development Mgr.R. L. Polk & Co.

© 2006 R. L. Polk & Co. All rights reserved

Television Bureau of Advertising

Annual Marketing Conference Jacob Javits Convention Center

New York, NYThursday, April 20, 2006

Television Bureau of Advertising

Annual Marketing Conference Jacob Javits Convention Center

New York, NYThursday, April 20, 2006

2

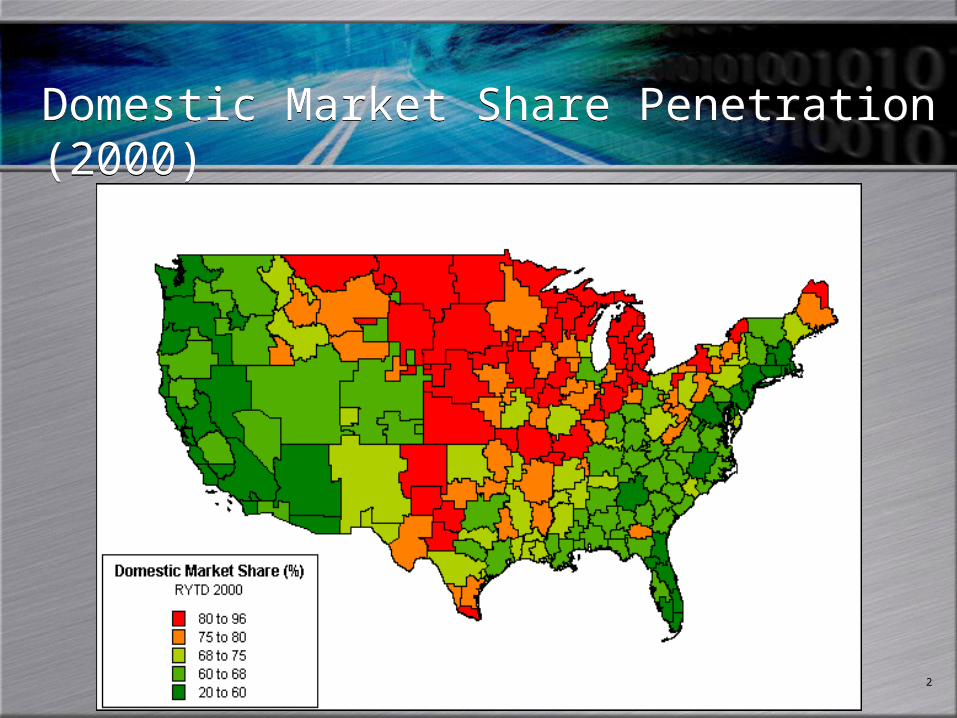

Domestic Market Share Penetration (2000)Domestic Market Share Penetration (2000)

3

Domestic Market Share Penetration (2005)Domestic Market Share Penetration (2005)

4

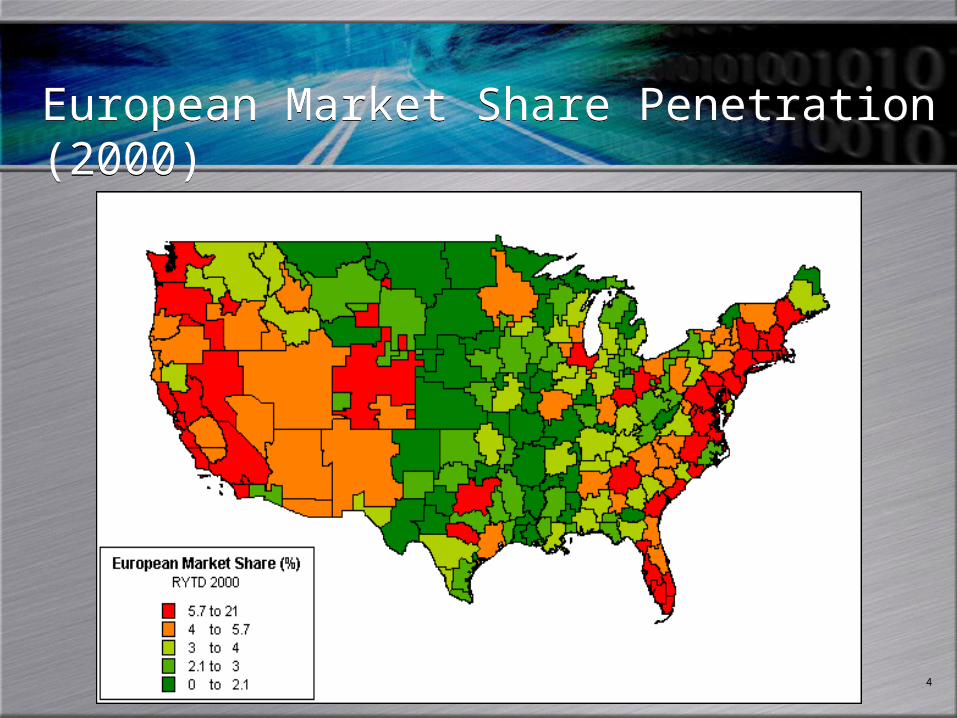

European Market Share Penetration (2000)European Market Share Penetration (2000)

5

European Market Share Penetration (2005)European Market Share Penetration (2005)

6

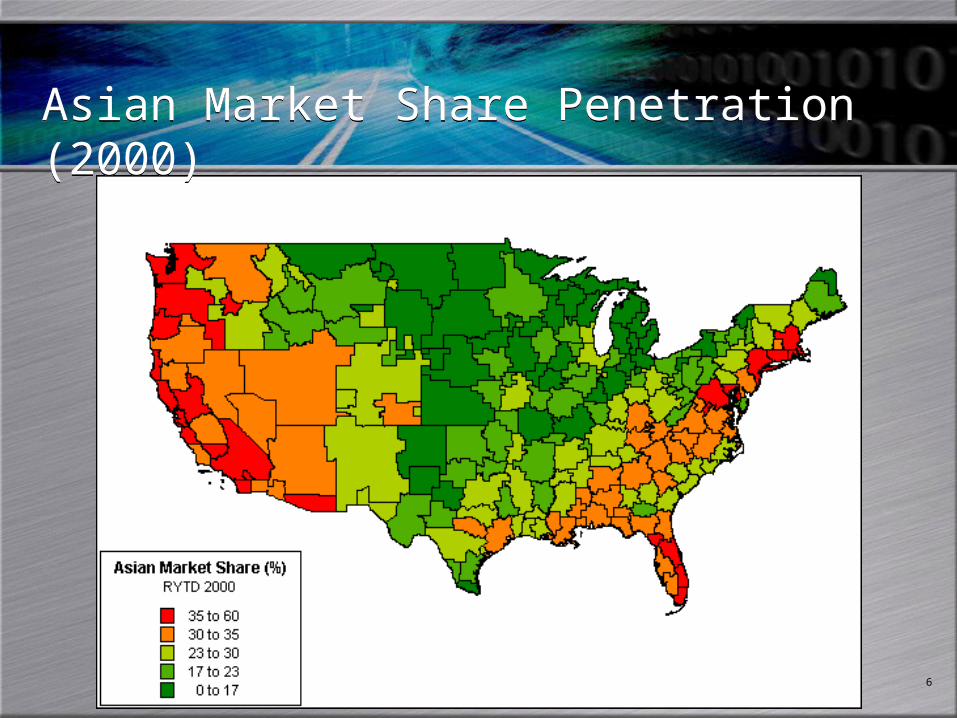

Asian Market Share Penetration (2000)Asian Market Share Penetration (2000)

7

Asian Market Share Penetration (2005)Asian Market Share Penetration (2005)

8

TodayToday

Factory & DealerShifts

Consumer Shifts

Staying Relevant

9

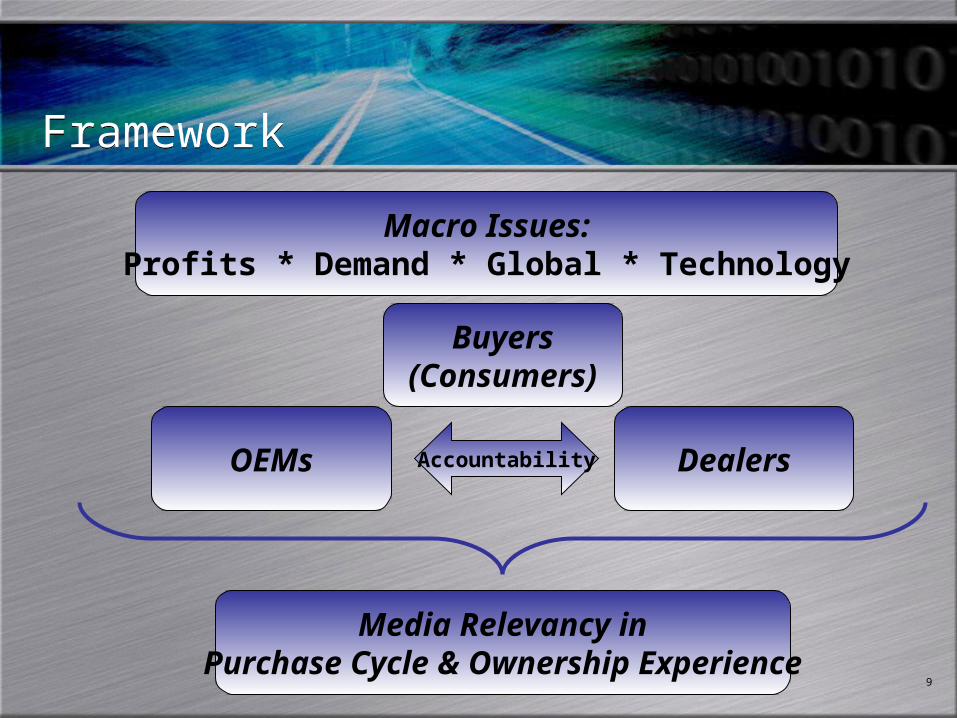

FrameworkFramework

Macro Issues:Profits * Demand * Global * Technology

OEMs

Buyers(Consumers)

Dealers

Media Relevancy inPurchase Cycle & Ownership Experience

Accountability

10

“60 Second Cheat Sheet”“60 Second Cheat Sheet”

Profits– Domestics: “Recovery”– Asians: “Feelin’ Fine”– Europeans: “It’s Not Necessarily Luxury Living”

U.S. New Vehicle Demand– 2005 3rd best year ever, but it doesn’t feel like it– Crowded product lineup– Used & Certified Used keeping buyers interested

Global– China, China, China…

Technology– Hybrids, E85, Fuel Cell– Telematics

Factory & Dealer ShiftsFactory & Dealer Shifts

12

Top 10 Brand Leaders (2005 CYE, U.S.)Top 10 Brand Leaders (2005 CYE, U.S.)

2.8

2.8

3.2

3.5

6.1

6.1

9.0

13.1

13.4

13.7

0.0 3.0 6.0 9.0 12.0 15.0

Hyundai

Jeep

Chrysler

GMC

Dodge

Nissan

Honda

Toyota

Ford

Chevrolet

U.S. Market Share - New Retail Registrations

Top 10 accounts for nearly 75% of all new retail units

Chrysler & Jeep are only domestics in this list who did not lose sharefrom 2004

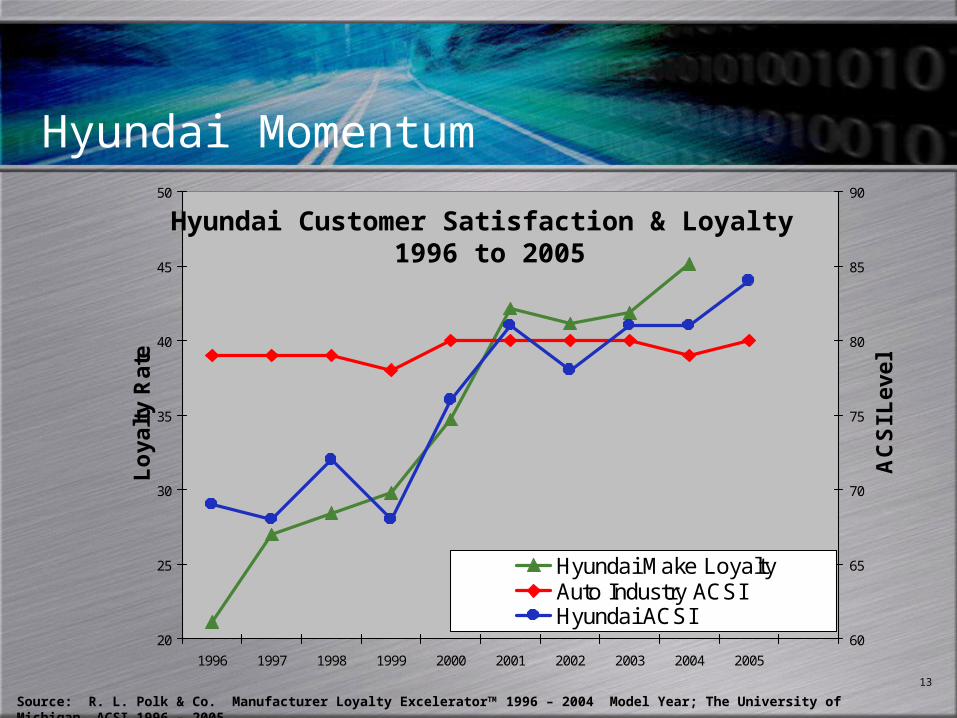

Hyundai - 20 years of U.S. presence starting to payoff!

13

20

25

30

35

40

45

50

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Lo

ya

lty

Ra

te

60

65

70

75

80

85

90

AC

SI

Le

ve

l

Hyundai Make LoyaltyAuto Industry ACSIHyundai ACSI

Hyundai Customer Satisfaction & Loyalty 1996 to 2005

Hyundai Momentum

Source: R. L. Polk & Co. Manufacturer Loyalty ExceleratorTM 1996 – 2004 Model Year; The University of Michigan, ACSI 1996 – 2005.

14

GM cuts $200 million from ad budgetAutomaker will concentrate on product launches (2/6/06)

Auto Company PrioritiesAuto Company Priorities

GM: More non-traditional advertising approach planned

Ford: Fewer nameplates get ad dollars,dealer bonuses & incentives– Ford Division: F-Series, Fusion, Escape, Mustang– Lincoln Division: Zephyr, Navigator– Mercury Division: Milan, Mariner

Chrysler Group:– Jeep lineup expansion– Heavy focus on

production excellence

15

Auto Company PrioritiesAuto Company Priorities

Toyota & Nissan: Winning the “Heartland”– Tundra / Titan Full-size Pickup Battle with Ford / Chevy

– Toyota in NASCAR Nextel Cup with Camry

European brands: “Quiet confidence”– Audi, Jaguar, Volvo, Volkswagen struggling

– BMW continues to set U.S. sales records

Korean brands: Impatient and aggressive– Leadership changes

– Last into U.S. market and taking full advantage of it

16

Auto Company PrioritiesAuto Company Priorities

Toyota, Nissan, Honda: “B-Segment”

Toyota Yaris

Honda Fit

Nissan Versa

3 Things You Must Do3 Things You Must Do

Knowledge is Power

18

Must Do #1: Know Regions IntimatelyMust Do #1: Know Regions Intimately

Auto Companies want to push marketing to the regions

Regional marketing agencies are growing and dealers can choose who they want

Promote ability to deliver on minority buyers

Understand the personality of the DMAs

19

Orlando: Top Growth Brands**2004 to 2005 CYE New Retail Registrations - Among Brands w/ 500+ Units in 2004

Orlando: Top Growth Brands**2004 to 2005 CYE New Retail Registrations - Among Brands w/ 500+ Units in 2004

Top… Brand

Changein Retail

Volume (%)

Was Growthin Orlando

Stronger than U.S.?

…Overall Brand Subaru 28.1 Yes

…GM Brand Cadillac 13.5 Yes

...Ford Brand Ford 1.8 Yes

…DCX Brand Dodge 17.4 Yes

…Asian Brand Subaru 28.1 Yes

…European Brand Mercedes-Benz 19.8 Yes

Orlando Retail Growth:

9.6%

20

San Francisco: Top Growth Brands**2004 to 2005 CYE New Retail Registrations - Among Brands w/ 500+ Units in 2004

San Francisco: Top Growth Brands**2004 to 2005 CYE New Retail Registrations - Among Brands w/ 500+ Units in 2004

Top… Brand

Changein Retail

Volume (%)

Was Growthin San Francisco

Stronger than U.S.?

…Overall Brand HUMMER 44.5 No

…GM Brand HUMMER 44.5 No

...Ford Brand Mercury 10.5 Yes

…DCX Brand Chrysler 19.7 Yes

…Asian Brand Toyota 7.5 No

…European Brand Land Rover 35.4 Yes

San Francisco Retail Growth:

0.8%

21

Must Do #2: Talk About LoyaltyMust Do #2: Talk About Loyalty

Ask if / how programming can support loyalty strategies

Note where integrated programming ties to repeat buying behavior

Take a stab at estimates on gains from growing loyalty

Make Number of Returning Owners*

Overall Make

Loyalty

Revenue from LoyalOwners ($)

Lost Revenue from Defectors

($)

Ford 1,109,796 57.4% $19.6B $14.6B

Volkswagen 120,277 30.5% $1.6B $3.6B

Toyota 547,110 52.2% $7.7B $7.1B

*Base: Vehicle Owning Households with a Retained Vehicle Acquired New Under 10 Years Old (10/03 – 9/04).R. L. Polk & Co. 2004 Model Year Manufacturer Loyalty ExceleratorTM

Assumed average MSRP of 2005 MYr. vehicles: $30,798 (Domestic), $43,303 (European), $27,079 (Asian). Average MSRPs provided by Edmunds.com

22

Must Do #3: Anticipate Auto Companies’Marketing Strategy Must Do #3: Anticipate Auto Companies’Marketing Strategy

GM: “Incentive Insomnia”; Defend truck markets still

Ford: “Red, White and Bold” Be profitable in N. Am.

DCX: Product and Styling Rule; Watch Jeep efforts

Toyota: Hyundai is the new Honda to them– Price may force their positioning on some entry models

Nissan: Expect growing dependence on interactive and highly specialized, niche marketing

Hyundai: Make friends with these franchises

All: Compact car segment will draw from youthand mature buyers find growing demand

23

Your Fit?Your Fit?

Macro Issues:Profits * Demand * Global * Technology

OEMs

Buyers(Consumers)

Dealers

Media Relevancy inPurchase Cycle & Ownership Experience

Accountability

![Oracle Enterprise Manager with 12c - Hearing the Oracle · PDF fileMicrosoft PowerPoint - Managing Oracle Database 12c with Oracle Enterprise Manager 12c.pptx [Read-Only]](https://img.dokumen.tips/doc/110x75/5a7a7a2f7f8b9a05348bfd4a/oracle-enterprise-manager-with-12c-hearing-the-oracle-powerpoint-managing-oracle.jpg)