Embed Size (px)

Citation preview

Power of PROSECUTION

under Income Tax Actand remedies thereto

byADV HARDIK VORA

PreparedbyAdvocateHardikVora

INTRODUCTION

PreparedbyAdvocateHardikVora

• ‘Noxiae Poena Par Esto’ is a latin phrase coined by Marcus TulliusCicero which means “let the punishment be equal tooffence”.• Generally, under the taxation laws, levy of monetary penalty is

levied for the default committed by the tax payer. However,upsurge in wilful tax evasions and with a view tostrengthening the tax surveillance led the Parliament to introducestringent provisions for prosecution of the defaulters notcomplying with the provisions of the Income Tax Act.• Recently Income Tax Department has started issuing notices to

the assessees who have either defaulted in the payment of thetax deducted at source within the due date specified under thelaw or who have failed to file the returns of income despite havingtaxable income or filed the returns of income after the due dateeven though the tax payable thereon has been paid with interest.

PreparedbyAdvocateHardikVora

• A Press Release issued by the Ministry of Finance shows that duringthe period April to November 2017, 2225 prosecution complaintswere filed out of which 1052 complaints were compounded and 48 casesresulted in conviction by the courts. A recently notified Central Plan forthe Period April to June 2018 mandates that each range shouldidentify and process atleast 10 cases for prosecution which areliable to prosecution u/s. 276CC of the Act.

• Unfortunately, it has been observed that undue pressures have beenput over the tax payers by the Departmental Authorities forcompounding the offences with a sole intention of meeting the budgetarytargets. It has to be borne in mind that sanctioning prosecution is a veryserious and extreme measure and should therefore be exercisedjudiciously since it violates the fundamental right of freedom granted bythe Constitution.

In wake of the increased pressure by the department for prosecutingthe tax payers, it becomes necessary to understand the provisions ofthe Act which deals with prosecution of the defaulters and the remediesavailable with the tax payers against the same. PreparedbyAdvocateHardikVora

• Principle of double jeopardyØThe principle of double jeopardy is a procedural defence which prevents an

accused person from being tried once again on the same or similar charges andon the same facts following a valid acquittal or conviction.

ØHowever, in case of prosecution u/s. 276B of the Act, the principles of doublejeopardy would not be applicable on the ground that penalty or interest hasalready been imposed for the same offence. This is because prosecution has norelation whatsoever with the penalty or interest as levied as per the provisionsof the Act.

ØThe Bombay High Court had in the case of [ITO vs. Sultan Enterprises & Ors.(2002) 256 ITR 185 (Bom)] held that the assessee is liable both for recovery ofthe amount with interest and penalty so also for prosecution for havingcommitted offence punishable under s. 276B of the IT Act for his failure to paythe amount within the prescribed period. PreparedbyAdvocateHardikVora

Article20inTheConstitutionOfIndia194920.Protectioninrespectofconvictionforoffences(1) Nopersonshallbeconvictedofanyoffenceexceptforviolationofthelawinforceatthetimeofthecommissionoftheact chargedasanoffence,norbesubjectedtoapenaltygreaterthanthatwhichmighthavebeeninflictedunderthelawinforceatthetimeofthecommissionoftheoffence(2) Nopersonshallbeprosecutedandpunishedforthesameoffencemorethanonce(3) Nopersonaccusedofanyoffenceshallbecompelledtobeawitnessagainsthimself

Sec278EPresumption as to culpable mental state

“(1) In any prosecution for any offence under this Act which requires a culpablemental state on the part of the accused, the court shall presume the existenceof such mental state but it shall be a defence for the accused to prove the factthat he had no such mental state with respect to the act charged as an offencein that prosecution.Explanation.—In this sub-section, "culpable mental state" includes intention,motive or knowledge of a fact or belief in, or reason to believe, a fact.(2) For the purposes of this section, a fact is said to be proved only when thecourt believes it to exist beyond reasonable doubt and not merely when itsexistence is established by a preponderance of probability.”

• in any prosecution for any offence under this act• defence can’t be proved by preponderance of probability• Section 278E of the Act presumes the existence of a culpable mental state

unlike the civil or criminal laws which presumes the accused to be innocentuntil found to be guilty. Therefore the increased onus lies on the assessee to provethe absence of a culpable mental state.

PreparedbyAdvocateHardikVora

Whoisliabletobeprosecuted?

PreparedbyAdvocateHardikVora

• Any person, committing the offence is liable to be prosecuted. In thisconnection it is not necessary that the person should be an assesseeunder the Income-tax Act. In the case of an offence committed by aCompany, Firm, Association of Persons or Body of Individuals, every personin charge of or responsible for the conduct of the business of theconcern as well as the concern are deemed to be guilty. Similarly, in thecase of an offence by a Hindu Undivided Family, the karta thereof isdeemed to be guilty of the offence.

• Where an offence under this Act has been committed by a person, being acompany, and the punishment for such offence is imprisonment and fine,then, such company shall be punished with fine and every person, referredto in sub-section (1) of section 278B, or the director, manager, secretary orother officer of the company referred to in sub-section (2) of section 278Bshall be liable to be proceeded against and punished in accordance with theprovisions of this Act.

PreparedbyAdvocateHardikVora

• Section 279A of the Act clearly specifies that offence u/s. 276B; 276C;276CC; 277 or 278 of the Act are non-cognizable offence. In thecase of a non-cognisable offence, a police officer does not have theauthority to make an arrest without a warrant and an investigationcannot be initiated without a court order. The police can file a FirstInformation Report (FIR) only for cognisable offences.

• Section 279: Prosecution for offences under section 275A, section275B, section 276, section 276A, section 276B, section 276BB, section276C, section 276CC, section 276D, section 277, section 277Aandsection 278 to be instituted with previous sanction of PrincipalDirector General/Principal Chief Commissioner/PrincipalCommissioner/Director General/Chief Commissioner/Commissioner,except where prosecution is at the instance of the Commissioner(Appeals) or the appropriate authority.

PreparedbyAdvocateHardikVora

Sections relating to Prosecution

• Sections 275A to 280 of the Income Tax Act, 1961 provides for varioustypes of offences for which the Department can prosecute an assessee.

• Prosecution can be launched only at the instance of the PrincipalCommissioner of Income Tax or Commissioner of Income Tax orCommissioner of Income Tax (Appeals).• Balwant Singh (70 ITR 89)(SC); Gopal (279 ITR 510)(SC) – no

opportunity is required to be given to assessee before lodgingcomplain.

PreparedbyAdvocateHardikVora

Sec275AContravention of order made under section 132(1)

(Second Proviso) or 132(3) in case of search seizure “Whoever contravenes any order referred to in the secondproviso to sub- section (1) or sub-section (3) of section132 shall be punishable with rigorous imprisonment whichmay extend to two years and shall also be liable to fine.”

• Not to part with valuables, books found during search and notseized.• (1993) 201 ITR 315 (Bom) Narayan Champalal Bajaj – Almirah

cut open.• Accused was not entrusted with responsibility of guarding seal-

[1995] 80 TAXMAN 539 (DELHI magistrate court) Rajesh Agarwal

PreparedbyAdvocateHardikVora

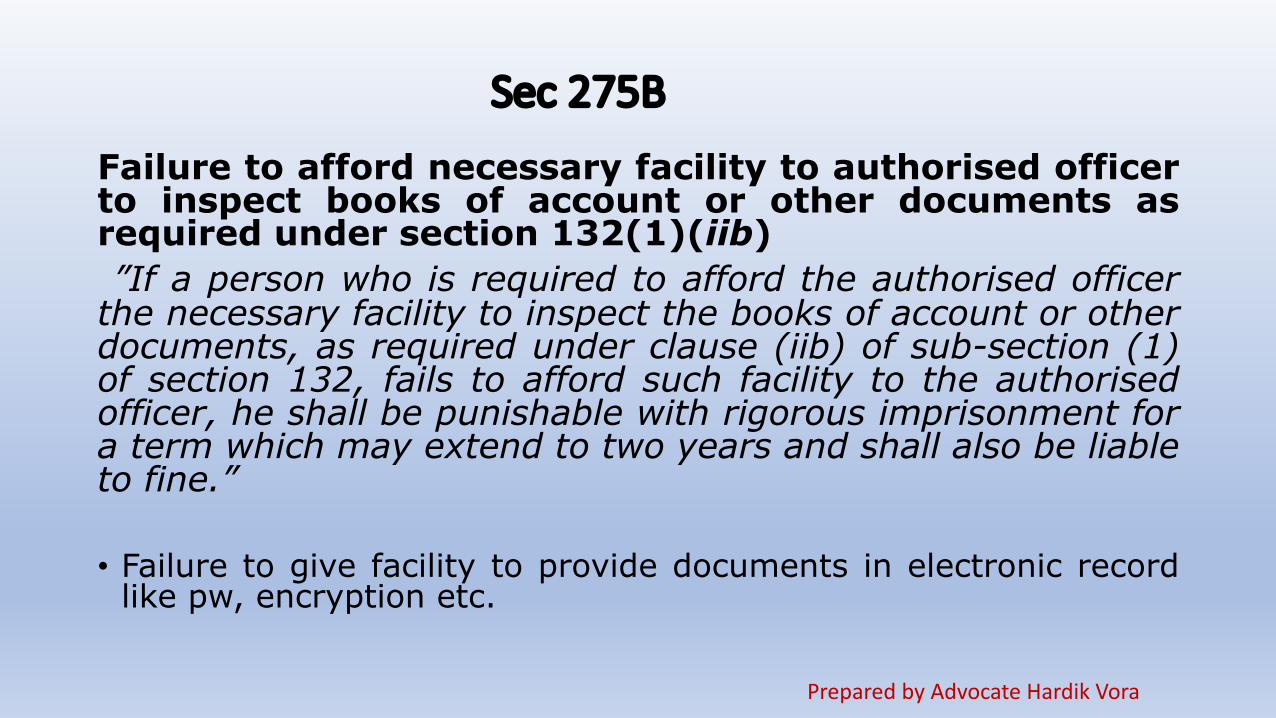

Sec275B

Failure to afford necessary facility to authorised officerto inspect books of account or other documents asrequired under section 132(1)(iib)”If a person who is required to afford the authorised officer

the necessary facility to inspect the books of account or otherdocuments, as required under clause (iib) of sub-section (1)of section 132, fails to afford such facility to the authorisedofficer, he shall be punishable with rigorous imprisonment fora term which may extend to two years and shall also be liableto fine.”

• Failure to give facility to provide documents in electronic recordlike pw, encryption etc.

PreparedbyAdvocateHardikVora

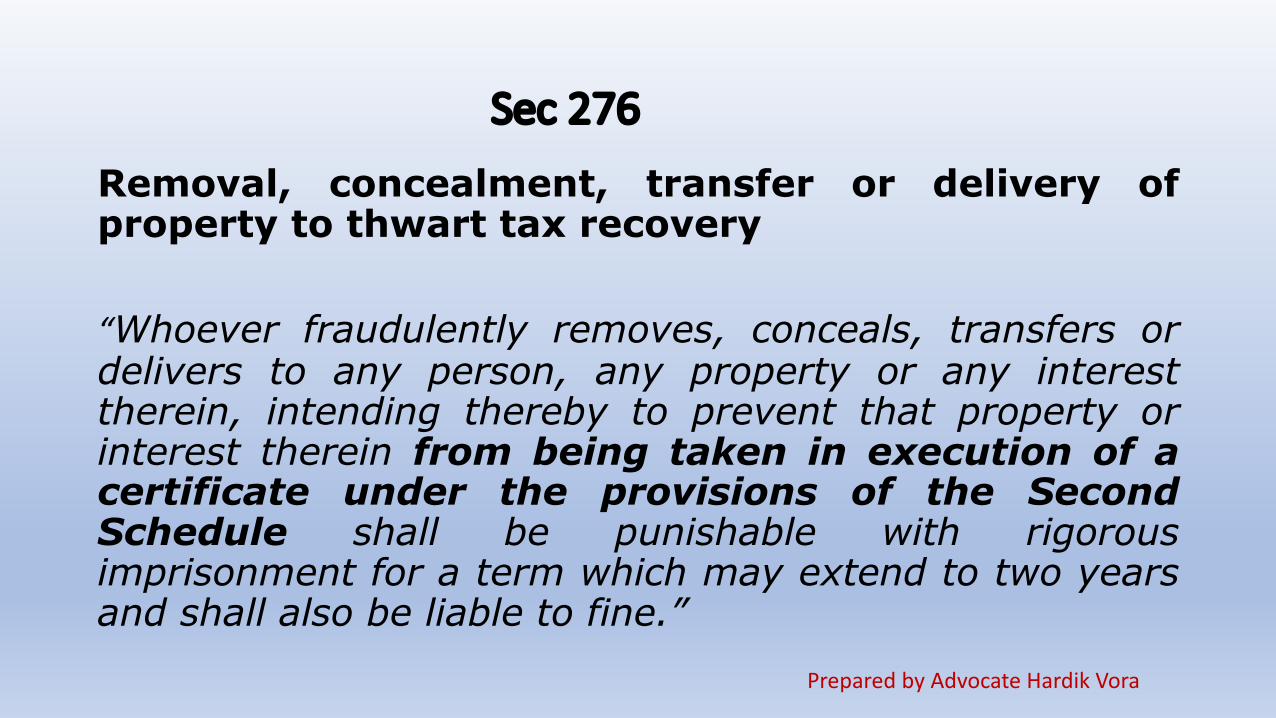

Sec276

Removal, concealment, transfer or delivery ofproperty to thwart tax recovery

“Whoever fraudulently removes, conceals, transfers ordelivers to any person, any property or any interesttherein, intending thereby to prevent that property orinterest therein from being taken in execution of acertificate under the provisions of the SecondSchedule shall be punishable with rigorousimprisonment for a term which may extend to two yearsand shall also be liable to fine.”

PreparedbyAdvocateHardikVora

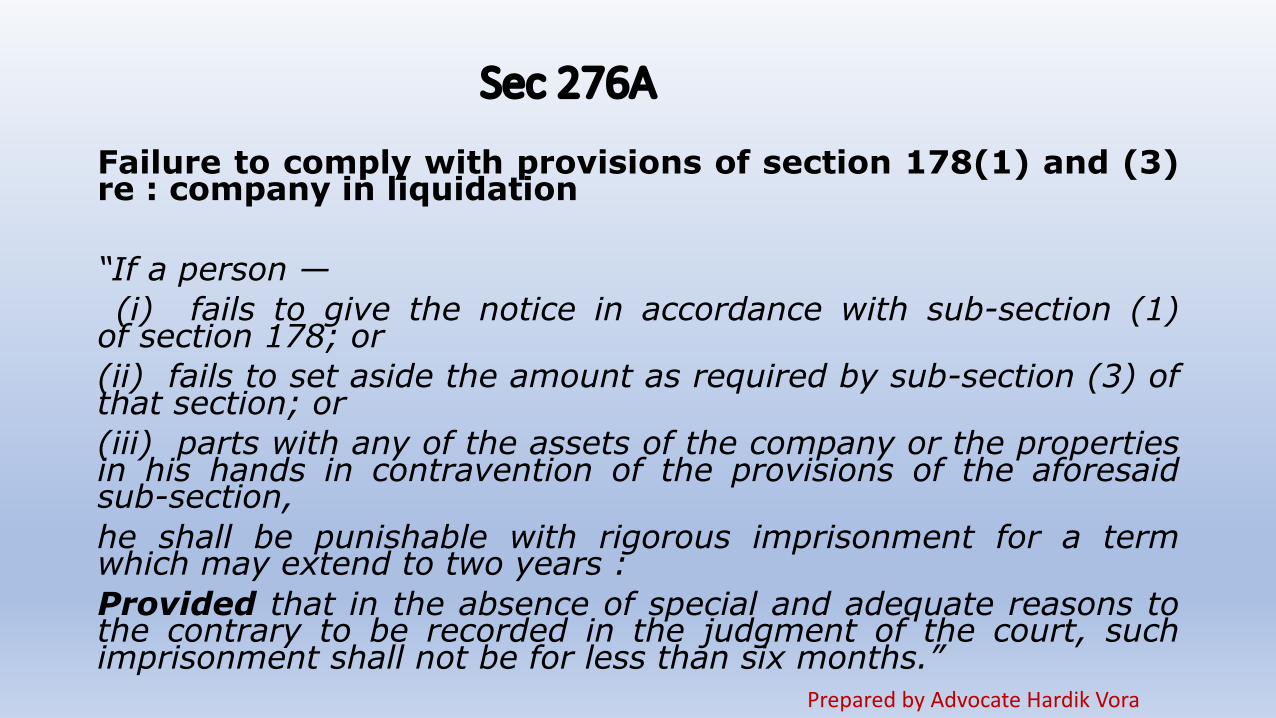

Sec276A

Failure to comply with provisions of section 178(1) and (3)re : company in liquidation

“If a person —(i) fails to give the notice in accordance with sub-section (1)

of section 178; or(ii) fails to set aside the amount as required by sub-section (3) ofthat section; or(iii) parts with any of the assets of the company or the propertiesin his hands in contravention of the provisions of the aforesaidsub-section,he shall be punishable with rigorous imprisonment for a termwhich may extend to two years :Provided that in the absence of special and adequate reasons tothe contrary to be recorded in the judgment of the court, suchimprisonment shall not be for less than six months.”

PreparedbyAdvocateHardikVora

• For liquidator to intimate liquidation and part money as per infoof AO.• 278AA for reasonable cause applicable

PreparedbyAdvocateHardikVora

Sec 276BFailure to pay to credit of Central Government (i) tax deducted atsource under Chapter XVII-B or (ii) tax payable u/s 115-O(2) or secondproviso to section 194B

“If a person fails to pay to the credit of the CentralGovernment,—(a) the tax deducted at source by him as required by orunder the provisions of Chapter XVII-B; or(b) the tax payable by him, as required by or under—(i) sub-section (2) of section 115-O; or(ii) the second proviso to section 194B,he shall be punishable with rigorous imprisonment for a termwhich shall not be less than three months but which mayextend to seven years and with fine.”276BB Failure to pay the tax collected under the provisions ofsection 206C PreparedbyAdvocateHardikVora

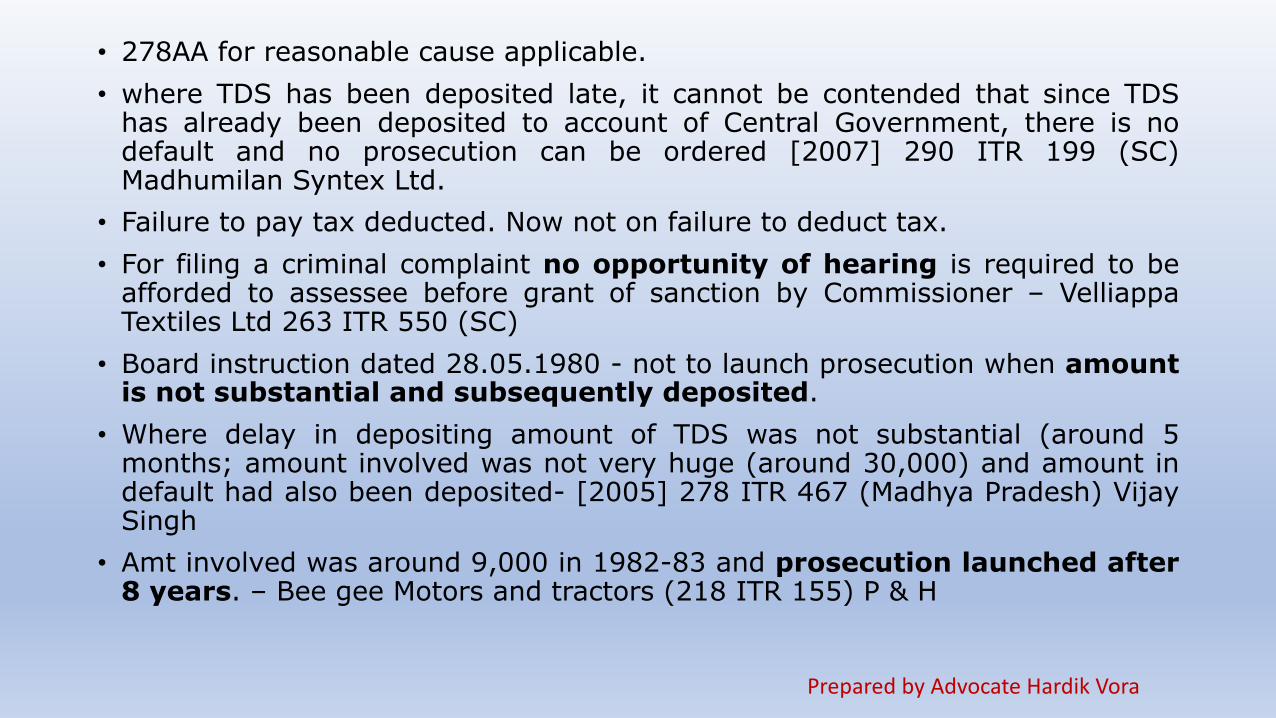

• 278AA for reasonable cause applicable.• where TDS has been deposited late, it cannot be contended that since TDS

has already been deposited to account of Central Government, there is nodefault and no prosecution can be ordered [2007] 290 ITR 199 (SC)Madhumilan Syntex Ltd.

• Failure to pay tax deducted. Now not on failure to deduct tax.• For filing a criminal complaint no opportunity of hearing is required to be

afforded to assessee before grant of sanction by Commissioner – VelliappaTextiles Ltd 263 ITR 550 (SC)

• Board instruction dated 28.05.1980 - not to launch prosecution when amountis not substantial and subsequently deposited.

• Where delay in depositing amount of TDS was not substantial (around 5months; amount involved was not very huge (around 30,000) and amount indefault had also been deposited- [2005] 278 ITR 467 (Madhya Pradesh) VijaySingh

• Amt involved was around 9,000 in 1982-83 and prosecution launched after8 years. – Bee gee Motors and tractors (218 ITR 155) P & H

PreparedbyAdvocateHardikVora

Sec 276CWilful attempt to evade tax, penalty or interest chargeableor imposable or under-reporting of Income

“If a person wilfully attempts in any manner whatsoever to evade anytax, penalty or interest chargeable or 63[imposable, or under reportshis income,] under this Act, he shall, without prejudice to any penaltythat may be imposable on him under any other provision of this Act, bepunishable,—

PreparedbyAdvocateHardikVora

• Sub section 1 Applicable even before assessment• Sub section (2) - Wilful attempt to evade payment of any tax,

penalty or interest (non-cognizable offence under section 279A)

PreparedbyAdvocateHardikVora

Explanation.—For the purposes of this section, a wilful attempt to evade any tax, penalty or interestchargeable or imposable under this Act or the payment thereof shall include a case where any person—(i) has in his possession or control any books of account or other documents (being books of account or otherdocuments relevant to any proceeding under this Act) containing a false entry or statement; or(ii) makes or causes to be made any false entry or statement in such books of account or other documents; or(iii) wilfully omits or causes to be omitted any relevant entry or statement in such books of account or otherdocuments; or(iv) causes any other circumstance to exist which will have the effect of enabling such person to evade anytax, penalty or interest chargeable or imposable under this Act or the payment thereof.

Sec276CCWilful failure to furnish returns

“If a person wilfully fails to furnish in due time the return offringe benefits which he is required to furnish under sub-section(1) of section 115WD or by notice given under sub-section (2)of the said section or section 115WH or the return of incomewhich he is required to furnish under sub-section (1)of section 139 or by notice given under clause (i) of sub-section (1) of section 142 or section 148 or section 153A,he shall be punishable,—(i) in a case where the amount of tax, which would have beenevaded if the failure had not been discovered, exceeds twenty-five hundred thousand rupees, with rigorous imprisonment for aterm which shall not be less than six months but which mayextend to seven years and with fine;(ii) in any other case, with imprisonment for a term which shallnot be less than three months but which may extend to twoyears and with fine:

PreparedbyAdvocateHardikVora

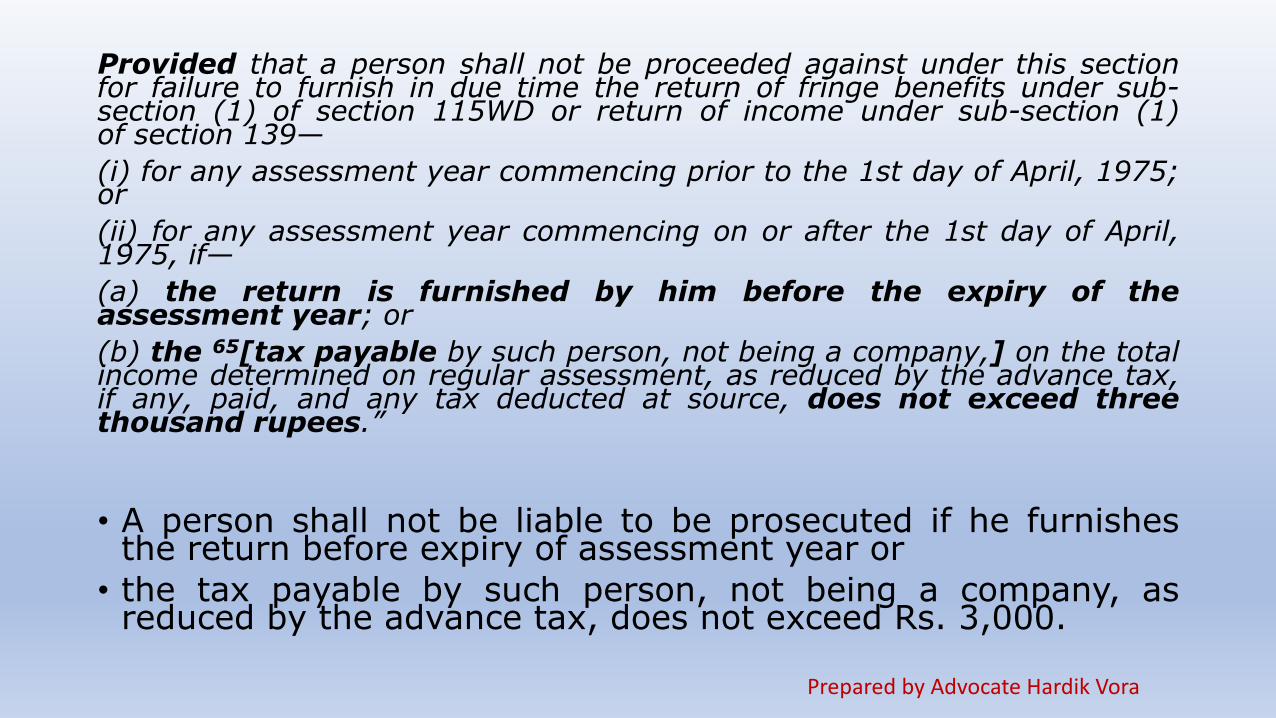

Provided that a person shall not be proceeded against under this sectionfor failure to furnish in due time the return of fringe benefits under sub-section (1) of section 115WD or return of income under sub-section (1)of section 139—(i) for any assessment year commencing prior to the 1st day of April, 1975;or(ii) for any assessment year commencing on or after the 1st day of April,1975, if—(a) the return is furnished by him before the expiry of theassessment year; or(b) the 65[tax payable by such person, not being a company,] on the totalincome determined on regular assessment, as reduced by the advance tax,if any, paid, and any tax deducted at source, does not exceed threethousand rupees.”

• A person shall not be liable to be prosecuted if he furnishesthe return before expiry of assessment year or• the tax payable by such person, not being a company, as

reduced by the advance tax, does not exceed Rs. 3,000.

PreparedbyAdvocateHardikVora

Sec276DWilful failure to produce accounts and documents

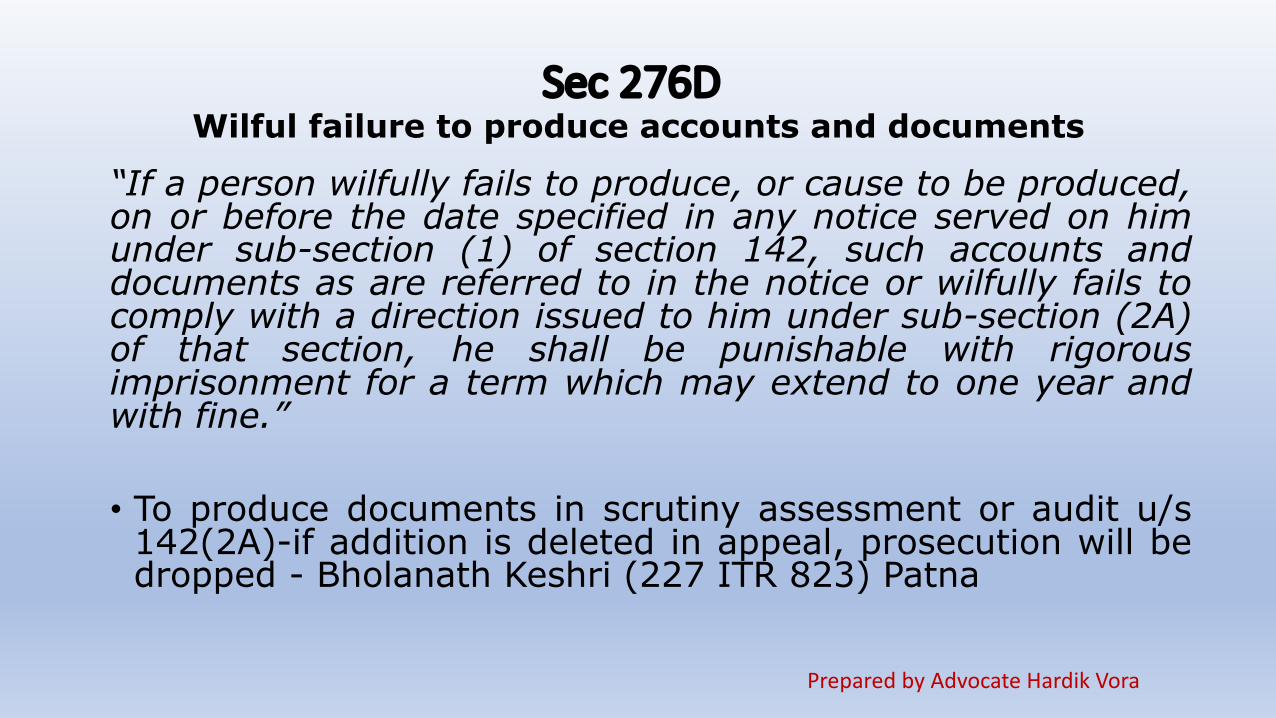

“If a person wilfully fails to produce, or cause to be produced,on or before the date specified in any notice served on himunder sub-section (1) of section 142, such accounts anddocuments as are referred to in the notice or wilfully fails tocomply with a direction issued to him under sub-section (2A)of that section, he shall be punishable with rigorousimprisonment for a term which may extend to one year andwith fine.”

• To produce documents in scrutiny assessment or audit u/s142(2A)-if addition is deleted in appeal, prosecution will bedropped - Bholanath Keshri (227 ITR 823) Patna

PreparedbyAdvocateHardikVora

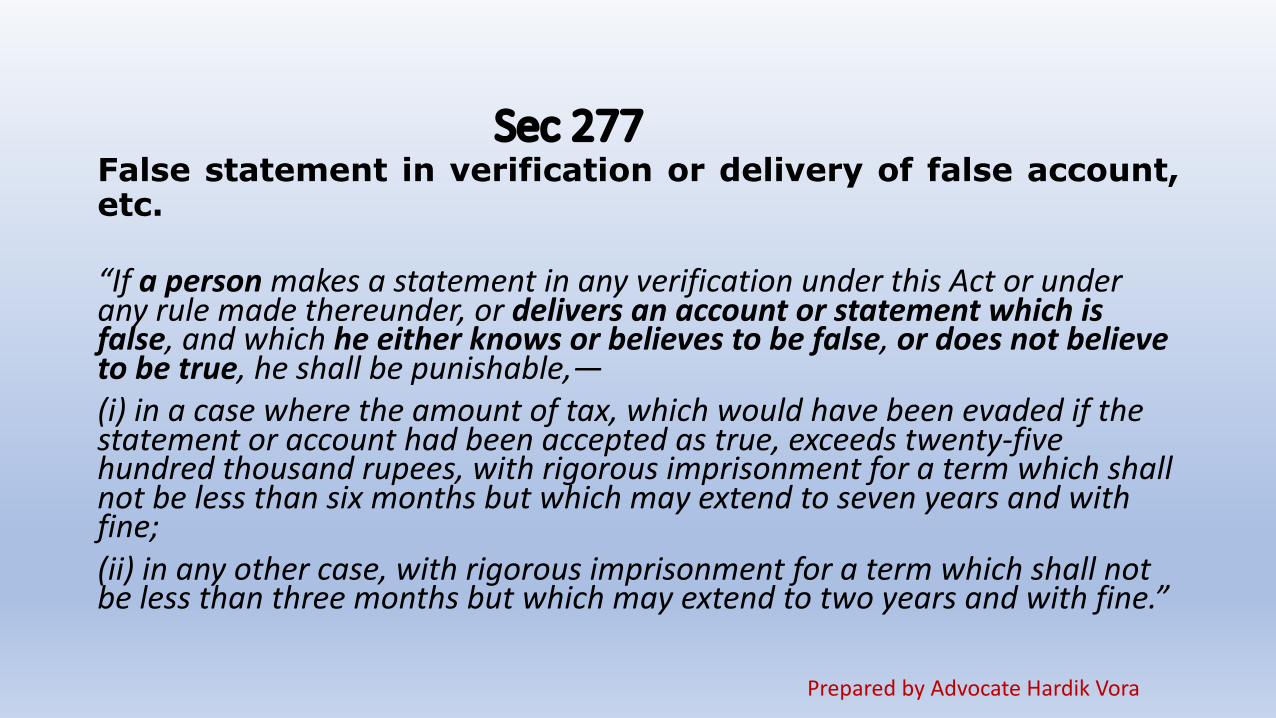

Sec 277False statement in verification or delivery of false account,etc.

“IfapersonmakesastatementinanyverificationunderthisActorunderanyrulemadethereunder,ordeliversanaccountorstatementwhichisfalse,andwhichheeitherknowsorbelievestobefalse,ordoesnotbelievetobetrue,heshallbepunishable,—(i)inacasewheretheamountoftax,whichwouldhavebeenevadedifthestatementoraccounthadbeenacceptedastrue,exceedstwenty-fivehundredthousandrupees,withrigorousimprisonmentforatermwhichshallnotbelessthansixmonthsbutwhichmayextendtosevenyearsandwithfine;(ii)inanyothercase,withrigorousimprisonmentforatermwhichshallnotbelessthanthreemonthsbutwhichmayextendtotwoyearsandwithfine.”

PreparedbyAdvocateHardikVora

• By any person in any verification under this act• This section has no bearing with assessment• Applicable to any person including tax practitioner (N K Mohnot)

195 ITR 72 (Mad)• With knowledge of belief that it is false or not true – mens rea

required to prove – Sawan Mal (147 ITR 123) (P&H)

PreparedbyAdvocateHardikVora

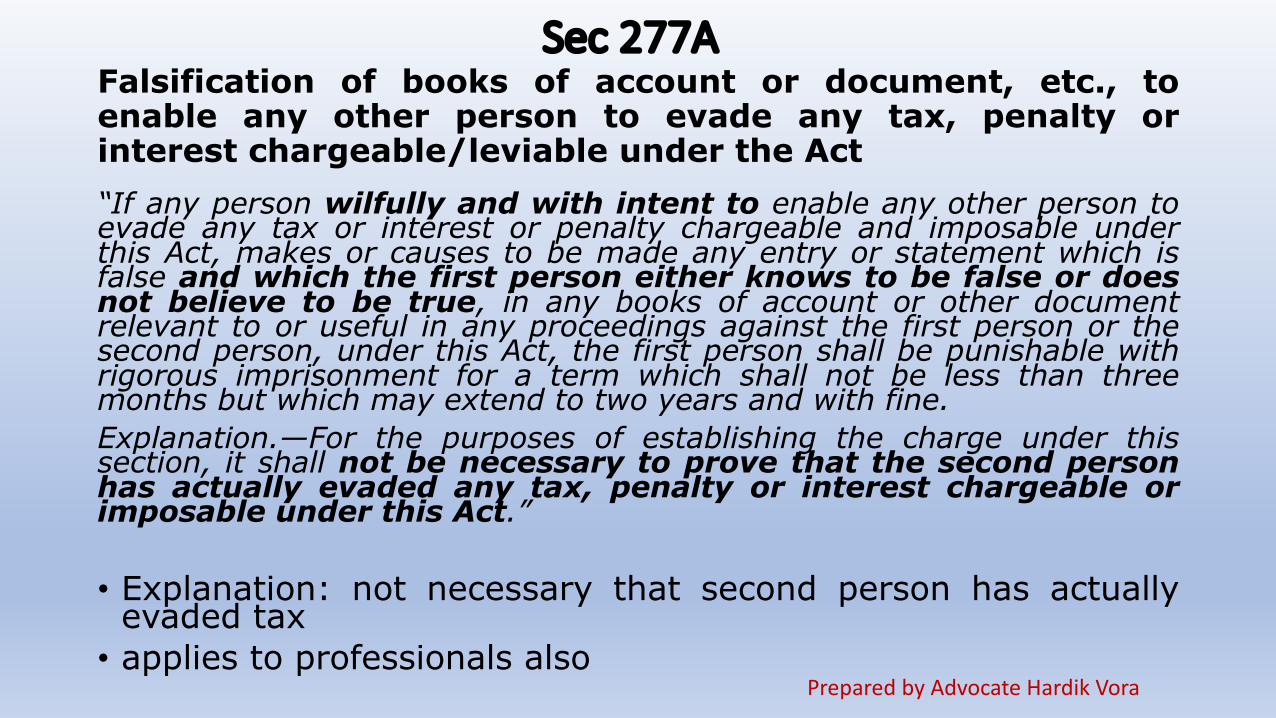

Sec 277AFalsification of books of account or document, etc., toenable any other person to evade any tax, penalty orinterest chargeable/leviable under the Act“If any person wilfully and with intent to enable any other person toevade any tax or interest or penalty chargeable and imposable underthis Act, makes or causes to be made any entry or statement which isfalse and which the first person either knows to be false or doesnot believe to be true, in any books of account or other documentrelevant to or useful in any proceedings against the first person or thesecond person, under this Act, the first person shall be punishable withrigorous imprisonment for a term which shall not be less than threemonths but which may extend to two years and with fine.Explanation.—For the purposes of establishing the charge under thissection, it shall not be necessary to prove that the second personhas actually evaded any tax, penalty or interest chargeable orimposable under this Act.”

• Explanation: not necessary that second person has actuallyevaded tax• applies to professionals also

PreparedbyAdvocateHardikVora

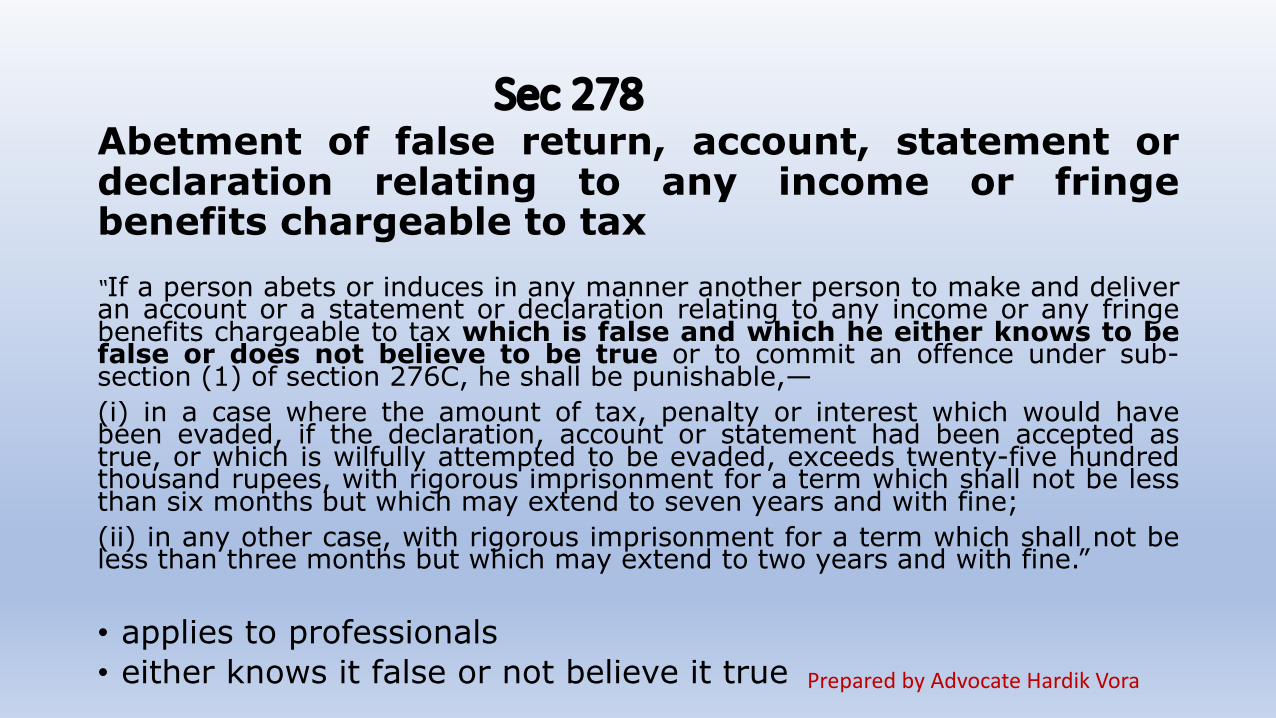

Sec 278Abetment of false return, account, statement ordeclaration relating to any income or fringebenefits chargeable to tax“If a person abets or induces in any manner another person to make and deliveran account or a statement or declaration relating to any income or any fringebenefits chargeable to tax which is false and which he either knows to befalse or does not believe to be true or to commit an offence under sub-section (1) of section 276C, he shall be punishable,—(i) in a case where the amount of tax, penalty or interest which would havebeen evaded, if the declaration, account or statement had been accepted astrue, or which is wilfully attempted to be evaded, exceeds twenty-five hundredthousand rupees, with rigorous imprisonment for a term which shall not be lessthan six months but which may extend to seven years and with fine;(ii) in any other case, with rigorous imprisonment for a term which shall not beless than three months but which may extend to two years and with fine.”

• applies to professionals• either knows it false or not believe it true PreparedbyAdvocateHardikVora

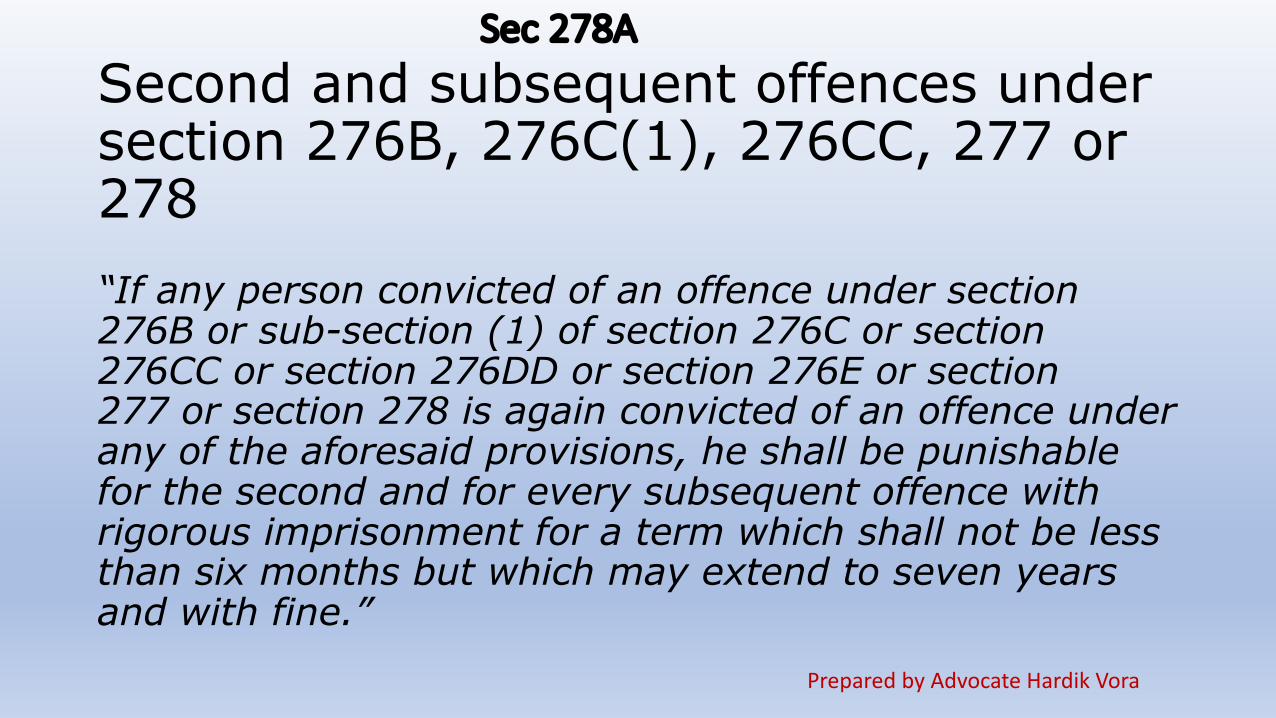

Sec278ASecond and subsequent offences under section 276B, 276C(1), 276CC, 277 or 278“If any person convicted of an offence under section 276B or sub-section (1) of section 276C or section 276CC or section 276DD or section 276E or section 277 or section 278 is again convicted of an offence under any of the aforesaid provisions, he shall be punishable for the second and for every subsequent offence with rigorous imprisonment for a term which shall not be less than six months but which may extend to seven years and with fine.”

PreparedbyAdvocateHardikVora

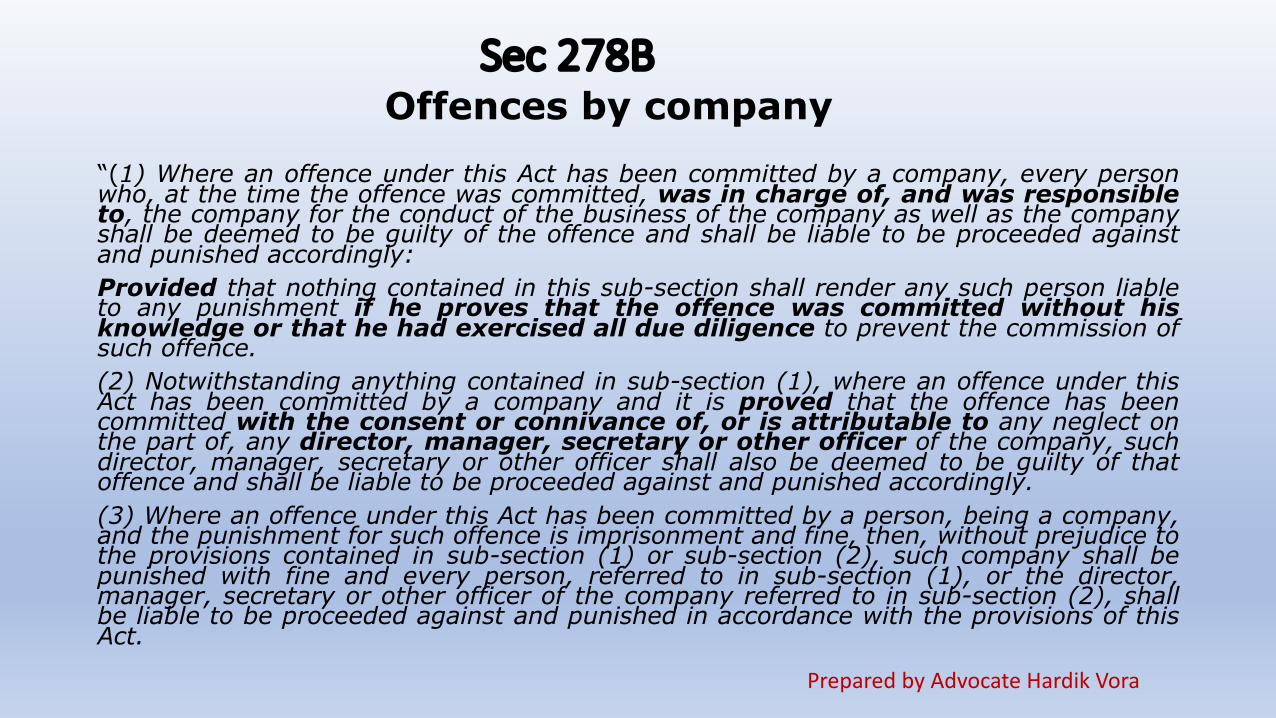

Sec278BOffences by company

“(1) Where an offence under this Act has been committed by a company, every personwho, at the time the offence was committed, was in charge of, and was responsibleto, the company for the conduct of the business of the company as well as the companyshall be deemed to be guilty of the offence and shall be liable to be proceeded againstand punished accordingly:Provided that nothing contained in this sub-section shall render any such person liableto any punishment if he proves that the offence was committed without hisknowledge or that he had exercised all due diligence to prevent the commission ofsuch offence.(2) Notwithstanding anything contained in sub-section (1), where an offence under thisAct has been committed by a company and it is proved that the offence has beencommitted with the consent or connivance of, or is attributable to any neglect onthe part of, any director, manager, secretary or other officer of the company, suchdirector, manager, secretary or other officer shall also be deemed to be guilty of thatoffence and shall be liable to be proceeded against and punished accordingly.(3) Where an offence under this Act has been committed by a person, being a company,and the punishment for such offence is imprisonment and fine, then, without prejudice tothe provisions contained in sub-section (1) or sub-section (2), such company shall bepunished with fine and every person, referred to in sub-section (1), or the director,manager, secretary or other officer of the company referred to in sub-section (2), shallbe liable to be proceeded against and punished in accordance with the provisions of thisAct.

PreparedbyAdvocateHardikVora

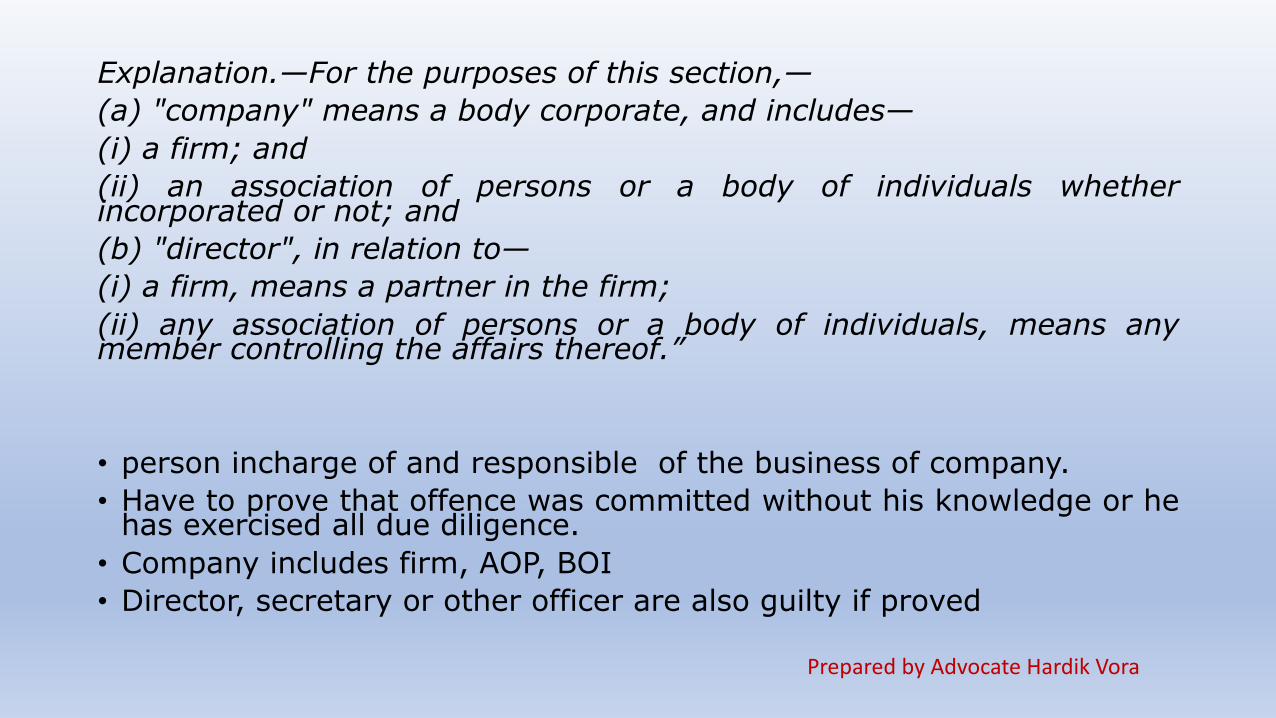

Explanation.—For the purposes of this section,—(a) "company" means a body corporate, and includes—(i) a firm; and(ii) an association of persons or a body of individuals whetherincorporated or not; and(b) "director", in relation to—(i) a firm, means a partner in the firm;(ii) any association of persons or a body of individuals, means anymember controlling the affairs thereof.”

• person incharge of and responsible of the business of company.• Have to prove that offence was committed without his knowledge or he

has exercised all due diligence.• Company includes firm, AOP, BOI• Director, secretary or other officer are also guilty if proved

PreparedbyAdvocateHardikVora

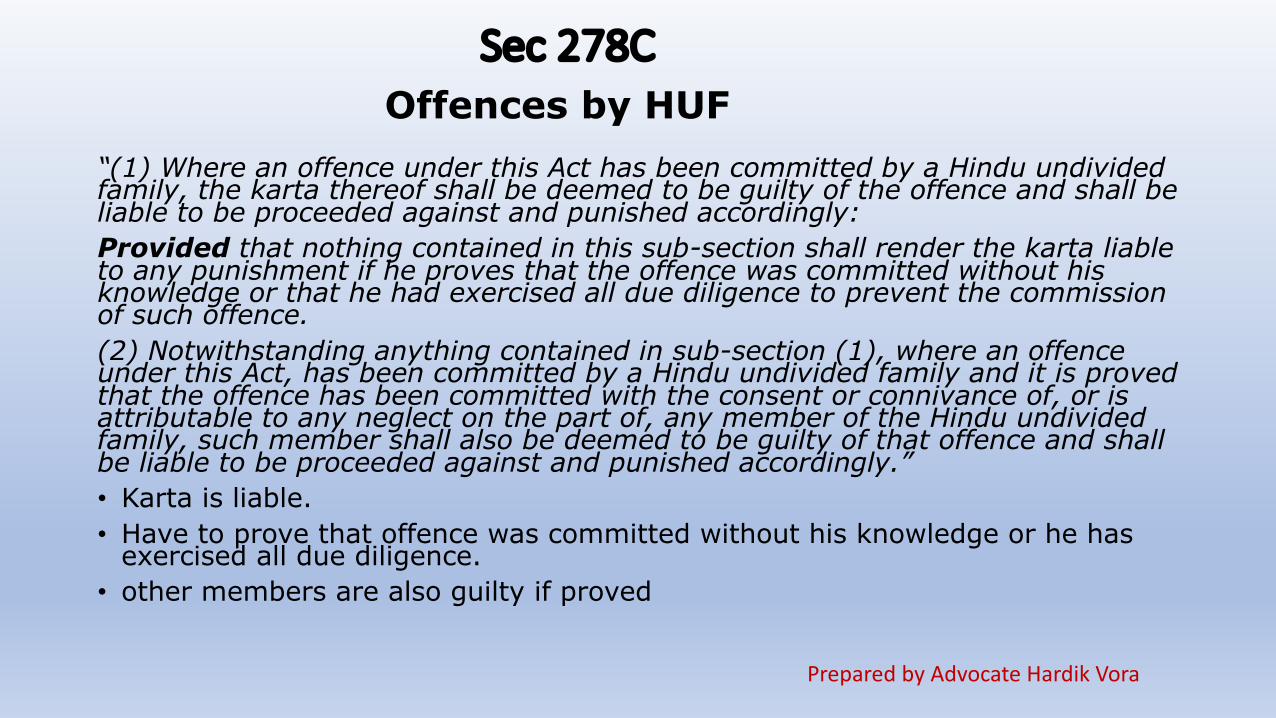

Sec278COffences by HUF

“(1) Where an offence under this Act has been committed by a Hindu undivided family, the karta thereof shall be deemed to be guilty of the offence and shall be liable to be proceeded against and punished accordingly:Provided that nothing contained in this sub-section shall render the karta liable to any punishment if he proves that the offence was committed without his knowledge or that he had exercised all due diligence to prevent the commission of such offence.(2) Notwithstanding anything contained in sub-section (1), where an offence under this Act, has been committed by a Hindu undivided family and it is proved that the offence has been committed with the consent or connivance of, or is attributable to any neglect on the part of, any member of the Hindu undivided family, such member shall also be deemed to be guilty of that offence and shall be liable to be proceeded against and punished accordingly.”• Karta is liable. • Have to prove that offence was committed without his knowledge or he has

exercised all due diligence.• other members are also guilty if proved

PreparedbyAdvocateHardikVora

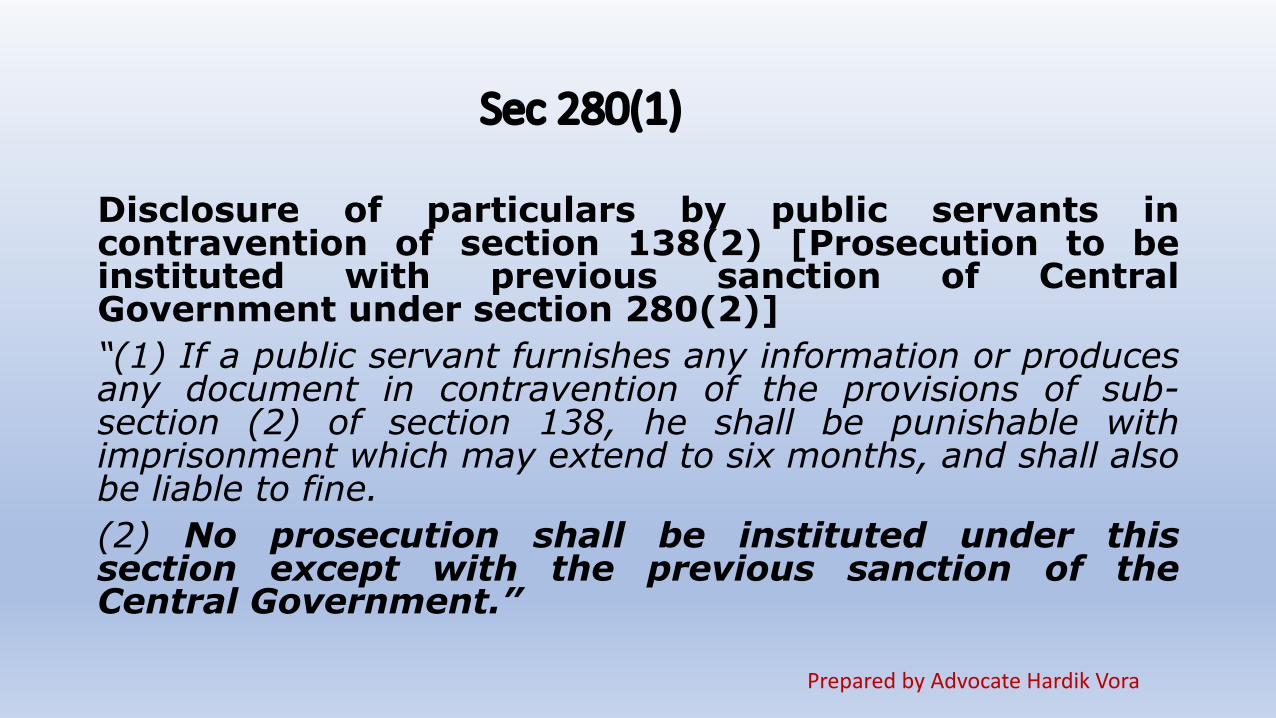

Sec280(1)

Disclosure of particulars by public servants incontravention of section 138(2) [Prosecution to beinstituted with previous sanction of CentralGovernment under section 280(2)]“(1) If a public servant furnishes any information or producesany document in contravention of the provisions of sub-section (2) of section 138, he shall be punishable withimprisonment which may extend to six months, and shall alsobe liable to fine.(2) No prosecution shall be instituted under thissection except with the previous sanction of theCentral Government.”

PreparedbyAdvocateHardikVora

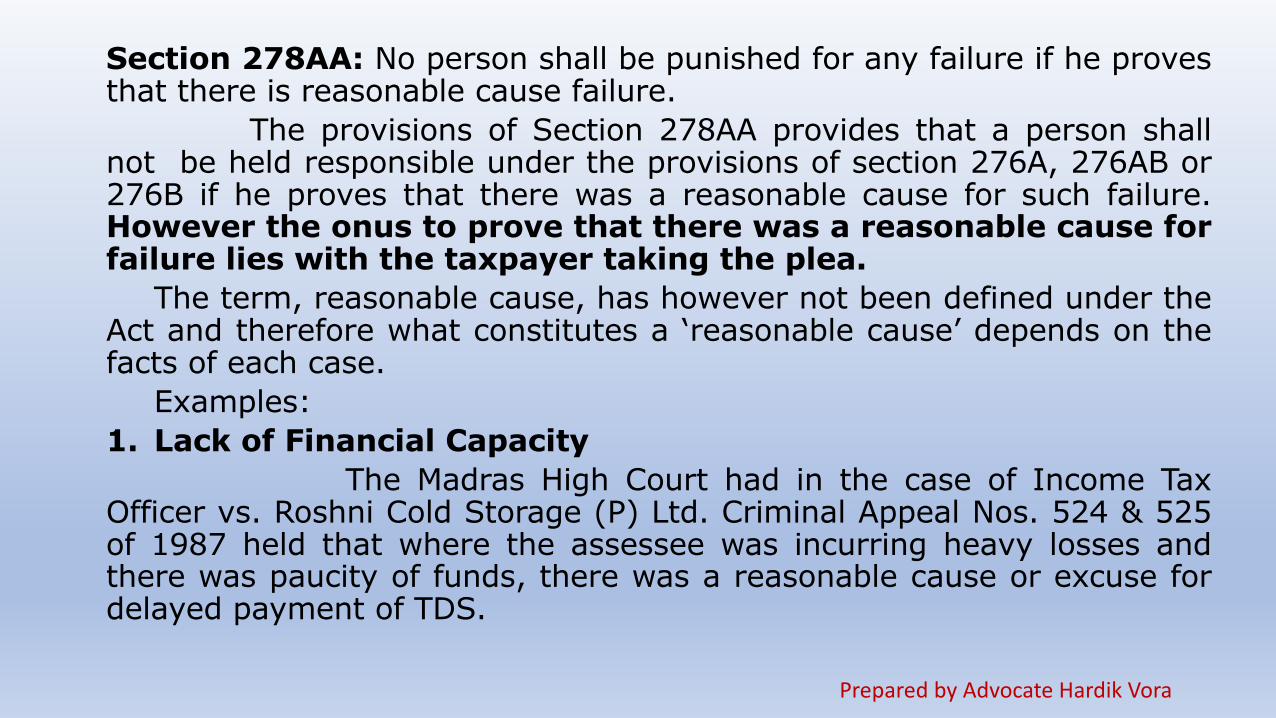

Section 278AA: No person shall be punished for any failure if he provesthat there is reasonable cause failure.

The provisions of Section 278AA provides that a person shallnot be held responsible under the provisions of section 276A, 276AB or276B if he proves that there was a reasonable cause for such failure.However the onus to prove that there was a reasonable cause forfailure lies with the taxpayer taking the plea.

The term, reasonable cause, has however not been defined under theAct and therefore what constitutes a ‘reasonable cause’ depends on thefacts of each case.

Examples:1. Lack of Financial Capacity

The Madras High Court had in the case of Income TaxOfficer vs. Roshni Cold Storage (P) Ltd. Criminal Appeal Nos. 524 & 525of 1987 held that where the assessee was incurring heavy losses andthere was paucity of funds, there was a reasonable cause or excuse fordelayed payment of TDS.

PreparedbyAdvocateHardikVora

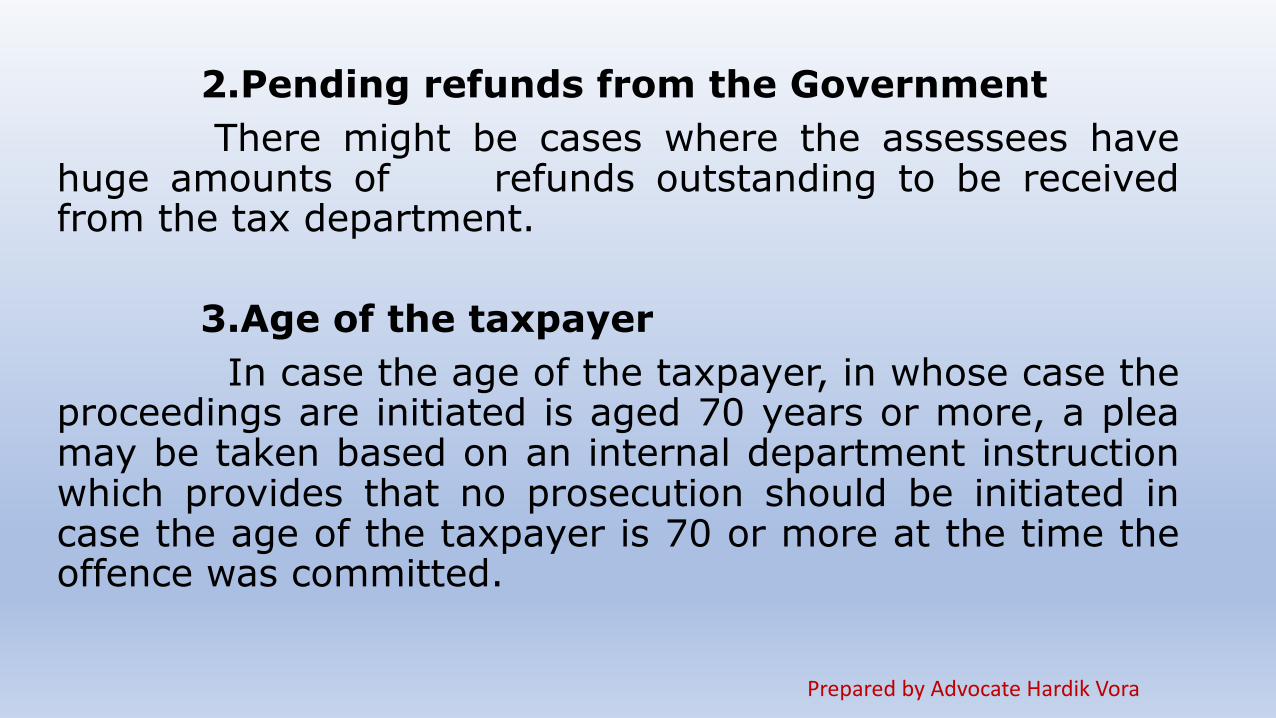

2.Pending refunds from the GovernmentThere might be cases where the assessees have

huge amounts of refunds outstanding to be receivedfrom the tax department.

3.Age of the taxpayerIn case the age of the taxpayer, in whose case the

proceedings are initiated is aged 70 years or more, a pleamay be taken based on an internal department instructionwhich provides that no prosecution should be initiated incase the age of the taxpayer is 70 or more at the time theoffence was committed.

PreparedbyAdvocateHardikVora

REMEDIESINCASEOFPROSECUTIONUNDERCHAPTERXXIIOFTHEI.T.ACT

PreparedbyAdvocateHardikVora

In case, a prosecution has been launched, the accusedmay defend the case:• In a Warrant-case, by demonstrating at the state offraming of the charge by the court, that no case can bemade out on the basis of the facts and documentsavailable on record;• By discharging the onus of proof of absence ofMens rea for commission of the crime alleged;• By pleading not guilty and facing trial;• By filing a petition under Sec. 482 of the Cr.P.C. forquashing of the prosecution, provided merits of thecase support such petition or• By compounding

PreparedbyAdvocateHardikVora

QUASHINGPETITIONUNDERSEC.482OFTHECR.P.C.

• One of the most resorted to and sought after remedy inprosecutions under Chapter XXII of the I.T. Act, is filingof a quashing petition under Sec. 482 of the Cr.P.C.However, one has to understand that for each andevery case, quashing petition under Sec.482 of theCr.C.P.C., may not be an effective remedy. The generaland consistent law is that the inherent power of theHigh Court under Sec. 482 of Cr.P.C. for quashing hasto be exercised sparingly with circumspection andin the rarest of rare cases.

PreparedbyAdvocateHardikVora

COMPOUNDINGOFOFFENCE• In absence of the existence of a reasonable cause and when the

taxpayer admits his guilt, he can have an option of filing anapplication for compounding the said offence.• Section 279(2) of the Act empowers the CCIT or DG to

compound the offences under Chapter 22 of the Act.• Compounding application can be filed at any time i.e. either

before or during or after the initiation of the prosecutionproceedings.• Compounding of an offence is not a right vested in the

assessees. Therefore, it is not necessary that all the offencesunder the Act would be compounded and is therefore incumbentupon the discretion of the compounding authority as to whethera case would be compounded or not.• LATEST GUIDELINES F.No. 285/35/2013 IT(Inv.V)/108 applicable

wef 01.01.2015 PreparedbyAdvocateHardikVora

• Only the prosecutions launched under the Act can be compounded.Offences committed under any other Act cannot be compounded.

• Conditions for compounding an offenceBefore making any application for compounding, it should beensured that the following conditions have been satisfied:1. The application must be made in the format prescribed tothe CCIT/DGIT having jurisdiction over the assessee.2. The applicant has paid the outstanding tax, interest andpenalty or any other sum due relating to the offence forwhich the compounding is sought.3. The applicant undertakes to pay the compoundingcharges including the compounding fee, the prosecutionestablishment expenses and litigation expenses includingcounsel’s fee, if any, determined and communicated byCGIT/DGIT concerned.4. The applicant undertakes to withdraw any appeals filed byhim if the appeal filed has a bearing on the offence sought to becompounded. PreparedbyAdvocateHardikVora

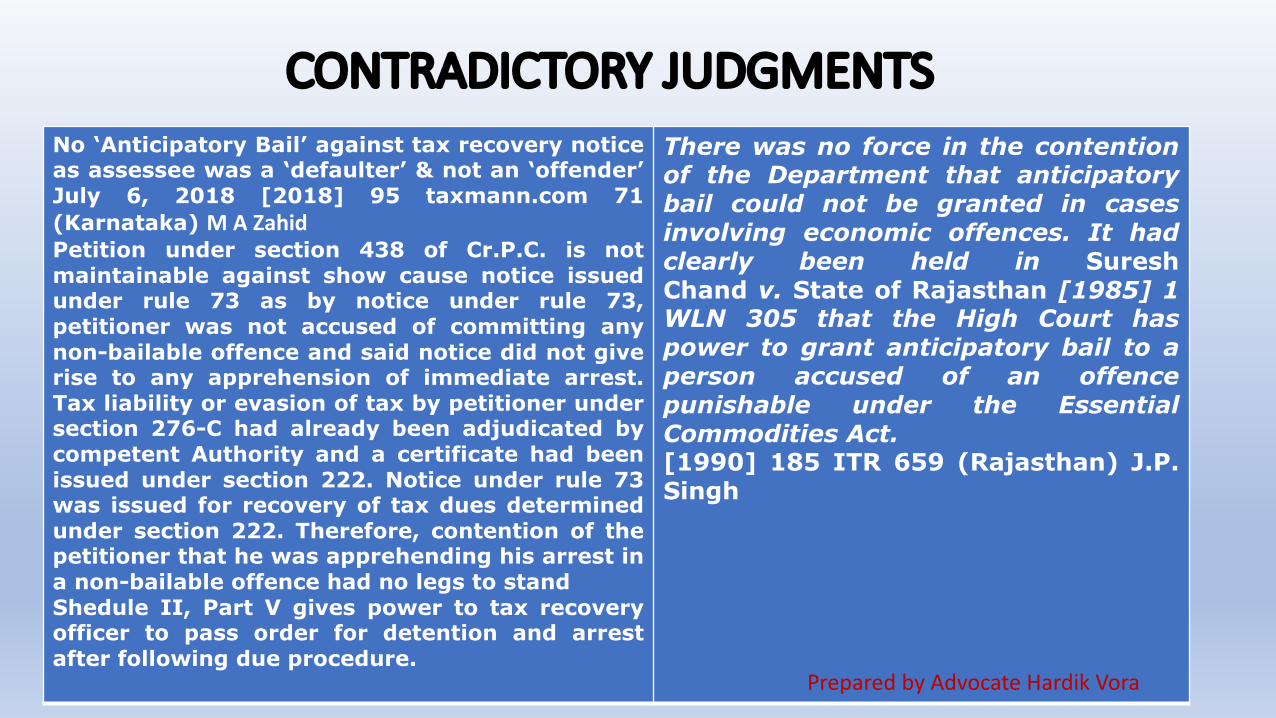

CONTRADICTORYJUDGMENTSNo ‘Anticipatory Bail’ against tax recovery noticeas assessee was a ‘defaulter’ & not an ‘offender’July 6, 2018 [2018] 95 taxmann.com 71(Karnataka) M A ZahidPetition under section 438 of Cr.P.C. is notmaintainable against show cause notice issuedunder rule 73 as by notice under rule 73,petitioner was not accused of committing anynon-bailable offence and said notice did not giverise to any apprehension of immediate arrest.Tax liability or evasion of tax by petitioner undersection 276-C had already been adjudicated bycompetent Authority and a certificate had beenissued under section 222. Notice under rule 73was issued for recovery of tax dues determinedunder section 222. Therefore, contention of thepetitioner that he was apprehending his arrest ina non-bailable offence had no legs to standShedule II, Part V gives power to tax recoveryofficer to pass order for detention and arrestafter following due procedure.

There was no force in the contentionof the Department that anticipatorybail could not be granted in casesinvolving economic offences. It hadclearly been held in SureshChand v. State of Rajasthan [1985] 1WLN 305 that the High Court haspower to grant anticipatory bail to aperson accused of an offencepunishable under the EssentialCommodities Act.[1990] 185 ITR 659 (Rajasthan) J.P.Singh

PreparedbyAdvocateHardikVora

Differencebetweendetentionandarrest

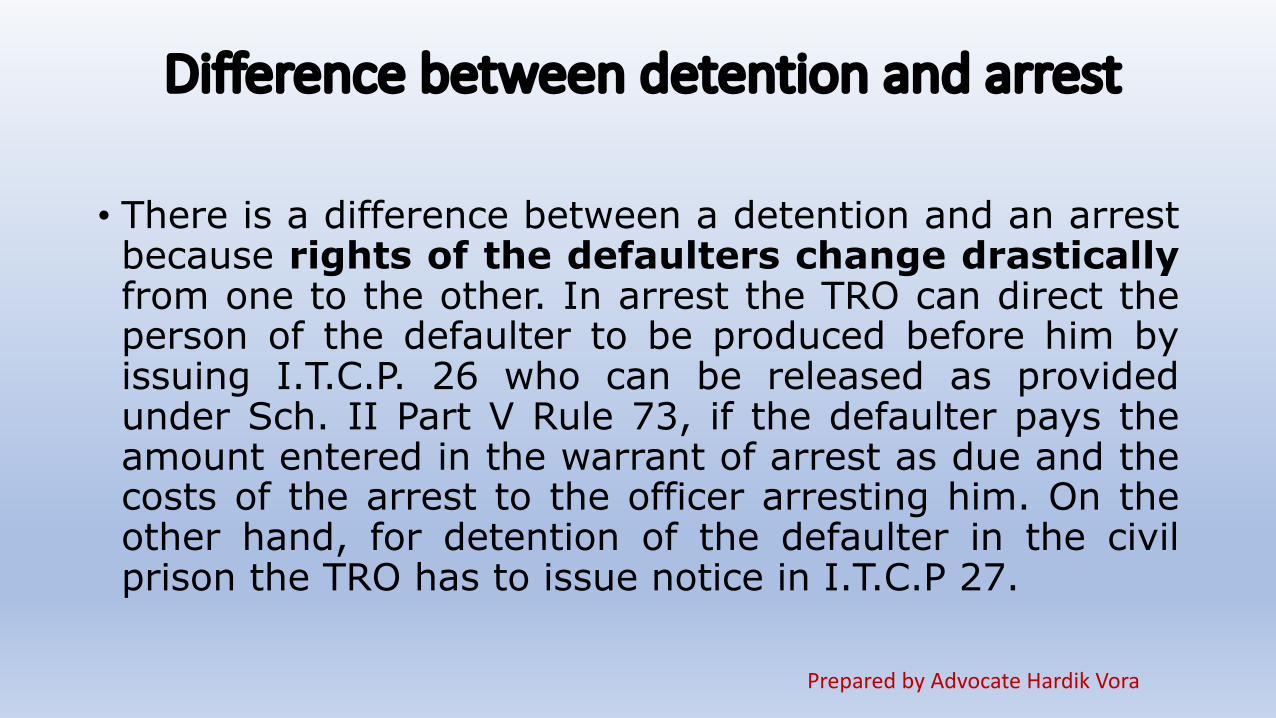

• There is a difference between a detention and an arrestbecause rights of the defaulters change drasticallyfrom one to the other. In arrest the TRO can direct theperson of the defaulter to be produced before him byissuing I.T.C.P. 26 who can be released as providedunder Sch. II Part V Rule 73, if the defaulter pays theamount entered in the warrant of arrest as due and thecosts of the arrest to the officer arresting him. On theother hand, for detention of the defaulter in the civilprison the TRO has to issue notice in I.T.C.P 27.

PreparedbyAdvocateHardikVora

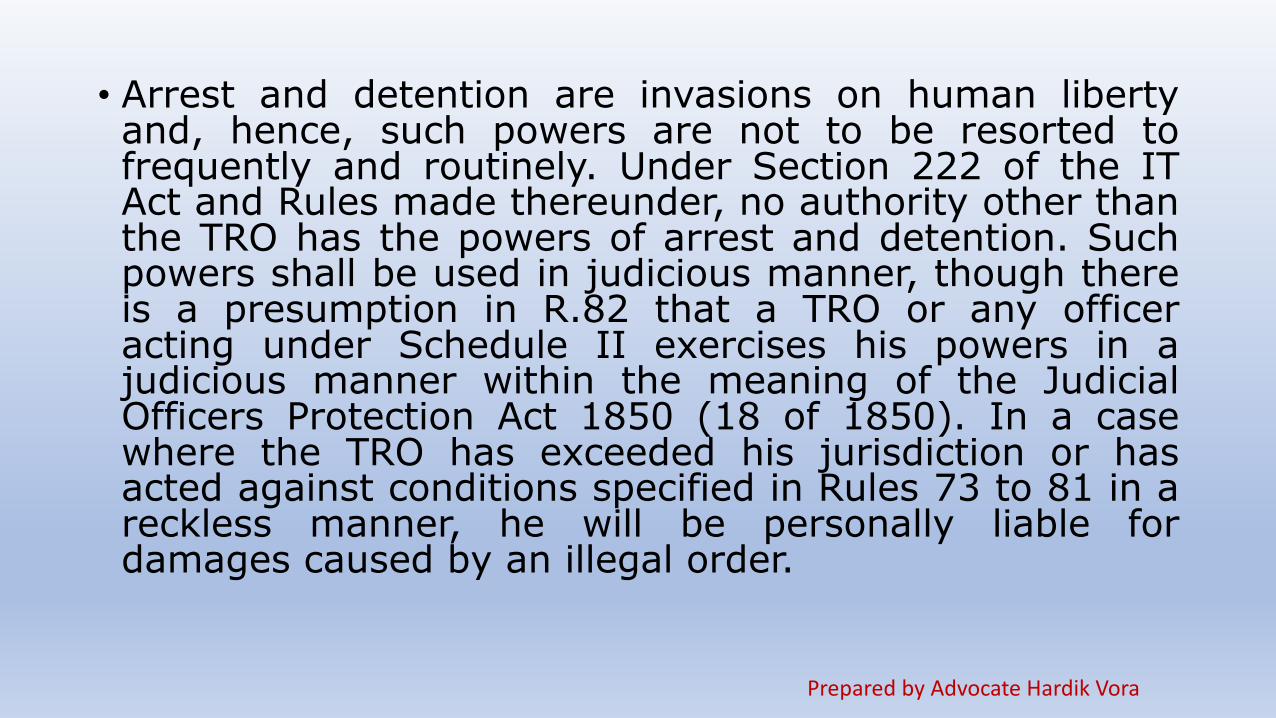

• Arrest and detention are invasions on human libertyand, hence, such powers are not to be resorted tofrequently and routinely. Under Section 222 of the ITAct and Rules made thereunder, no authority other thanthe TRO has the powers of arrest and detention. Suchpowers shall be used in judicious manner, though thereis a presumption in R.82 that a TRO or any officeracting under Schedule II exercises his powers in ajudicious manner within the meaning of the JudicialOfficers Protection Act 1850 (18 of 1850). In a casewhere the TRO has exceeded his jurisdiction or hasacted against conditions specified in Rules 73 to 81 in areckless manner, he will be personally liable fordamages caused by an illegal order.

PreparedbyAdvocateHardikVora

Latestcaselaws

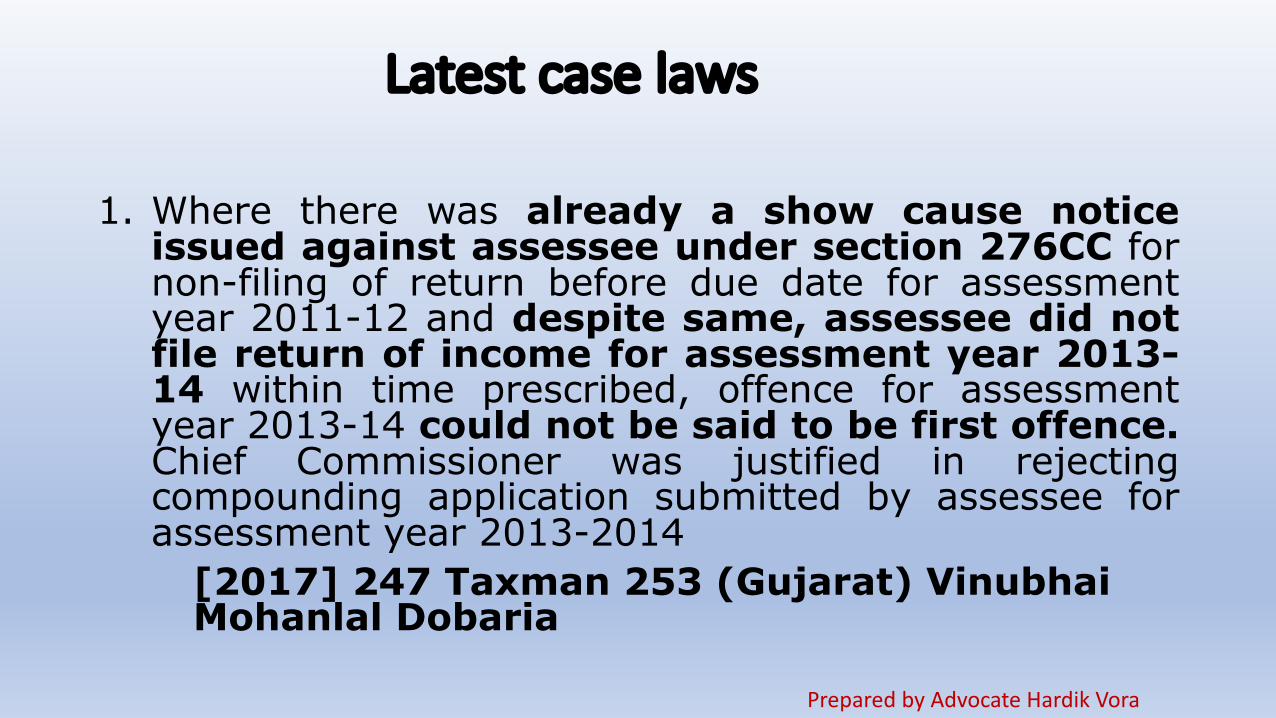

1. Where there was already a show cause noticeissued against assessee under section 276CC fornon-filing of return before due date for assessmentyear 2011-12 and despite same, assessee did notfile return of income for assessment year 2013-14 within time prescribed, offence for assessmentyear 2013-14 could not be said to be first offence.Chief Commissioner was justified in rejectingcompounding application submitted by assessee forassessment year 2013-2014

[2017] 247 Taxman 253 (Gujarat) VinubhaiMohanlal Dobaria

PreparedbyAdvocateHardikVora

Latestcaselaws2 Assessee had properly deducted tax at source forrelevant year but failed to deposit same with CentralGovernment within specified time limit. Said amount wasdeposited along with interest subsequently whenmistake was noticed by its StatutoryAuditors. Prosecution proceedings was launched againstassessee after three years of default. It was found thatimpugned tax could not be deposited within time dueto oversight on part of assessee’s accountant.Whether this could be presumed to be a reasonablecause for not depositing tax by assessee within time and,thus, initiation of proceedings after three yearswould be in contravention of CBDT instruction dated 28-5-1980 and, therefore, deserved to be quashed[2017] 396 ITR 636 (Patna) Sonali Auto PVT LTD

PreparedbyAdvocateHardikVora

Latestcaselaws3. CBDT cannot arrogate to itself, on strength of section 279 or Explanation

thereunder, power to insist on a 'pre-deposit' of compounding fee evenwithout considering application for compoundingThe circular dated 23-12-2014 does not stipulate a limitation periodfor filing the application for compounding. What the said circular setsout are 'Offences generally not to be compounded'. In this, one of thecategories which is mentioned in sub- clause (vii) is: 'Offencescommitted by a person for which complaint was filed with thecompetent court 12 months prior to receipt of the application forcompounding’The above clause is not one prescribing a period of limitation for filing anapplication for compounding. It gives a discretion to the competent authorityto reject an application for compounding on certain grounds. Again, it does notmean that every application, which involves an offence committed by aperson, for which the complaint was filed to the competent court 12 monthsprior to the receipt of the application for compounding, will without anythingfurther, be rejected. In other words, resort cannot be had to the circular toprescribe a period of limitation for filing an application for compounding.[2017] 394 ITR 746 (Delhi) Vikram Singh

PreparedbyAdvocateHardikVora

THANKYOU

ContactDetails:208,AbhinavArcade,Nr.KothawalaFlats,Ellisbridge,

Ahmedabad-380006(M):9998966233(O):079-26574033

E-mail:[email protected]