Embed Size (px)

Citation preview

1

Potential of Distributed Generation (DG) in

Thailand and a Case Study of Very Small

Power Producer (VSPP) Cogeneration

POWERGEN ASIA 2015

Nicolas Leong, Business Development Manager, South East Asia,Power Plants, Wärtsilä Singapore Pte Ltd

Saara Kujala, Manager, Development & Financial Services, Asia & Australia, Power Plants, Wärtsilä Finland Oy

2

TableofContents1. Abstract................................................................................................................................................. 4

2. Introduction .......................................................................................................................................... 5

3. General Market Overview..................................................................................................................... 6

3.1 EGAT........................................................................................................................................................ 8

3.2 PEA and MEA........................................................................................................................................... 9

3.3 Power Development Plan (PDP) 2010 Rev 3........................................................................................... 9

3.4 VSPP Program .......................................................................................................................................10

4. Feasibility Study: Internal combustion engine (ICE) ...........................................................................11

4.1 Internal Combustion Engine (ICE) .........................................................................................................11

4.2 Wärtsilä 34SG Engine Technology ........................................................................................................13

4.3 Wärtsilä GasCube..................................................................................................................................15

4.4 Wärtsilä EPC capabilities....................................................................................................................... 17

4.5 Wärtsilä O&M capabilities .................................................................................................................... 17

4.6 Case Study – Wärtsilä GasCube (1 x 20V34SG)..................................................................................... 17

5. Conclusion...........................................................................................................................................21

3

Legal disclaimer

This document is provided for informational purposes only and may not be incorporated into any agreement. The

information and conclusions in this document are based upon calculations (including software built-in assumptions),

observations, assumptions, publicly available competitor information, and other information obtained by Wärtsilä or

provided to Wärtsilä by its customers, prospective customers or other third parties (the ”information”) and is not

intended to substitute independent evaluation. No representation or warranty of any kind is made in respect of any

such information. Wärtsilä expressly disclaims any responsibility for, and does not guarantee, the correctness or the

completeness of the information. The calculations and assumptions included in the information do not necessarily

take into account all the factors that could be relevant. Nothing in this document shall be construed as a guarantee or

warranty of the performance of any Wärtsilä equipment or installation or the savings or other benefits that could be

achieved by using Wärtsilä technology, equipment or installations instead of any or other technology.

4

1. Abstract

Distributed Generation in Thailand has been seriously developed through national energy polices

and government supporting schemes over the past decade and has good prospects also going forward.

Various measures have been initiated and applied to encourage the investors, such as “adder” or feed-in

tariff program, government funding program and energy efficiency funding. Distributed generation in

Thailand will continue to grow in line with the country power development plan and national

policy on increasing renewable energy target to reach 25% generation share in year 2021. The current

power development plan PDP Rev.3 (2013-2030) targets a further increase in distributed generation

(DG) through new SPP cogeneration (6,347 MW) and renewable energy (13,937 MW) that are planned

to be added in the system by year 2030. Small Power Producer (SPP) and Very Small Power

Producer (VSPP) programs are good examples of success stories under the distributed generation

schemes. Both SPP and VSPP programs are implemented for promoting of primary energy saving

and for encouraging the use of alternative energy in power generation sector. As of December 2013,

the government has released SPP licenses for 11,988 MW (129 projects) and VSPP licenses for 3,727

MW (888 projects). In addition, more than 3,250 MW are currently in the licensing process.

To focus on onsite generation, where the generation is next door to the electricity user, this paper will

study in detail the VSPP cogeneration scheme which is for power plant sizes <10MW that supply

electricity and heating or cooling directly to consumers. This paper contains a case of natural gas based

VSPP cogeneration plant with efficient internal combustion engine as prime movers. The study will

present a technology overview, and a feasibility study in order to guide investors on the best solution for

investment.

5

2. Introduction

Distributed generation is an approach where electricity is produced near to the end-users of power. In

other words, the generation source is as near as possible to the consumption point. Historically,

electricity generation and distribution model was dominated by centralized power generation. In that

model, power plants are located far away from the consumers and extensive transmission lines are

required for distribution. Such system has its drawbacks such as expensive transmission lines and power

and transmission losses over lengthy distance.

Nowadays, there is a trend for more and more countries to move towards decentralized power

generation and the benefits are reduced transmission and distribution losses, improved energy

efficiency, better reliability in terms of electricity supply and possibility of cogeneration (heat recovery).

Figure 1: Central Generation

6

Figure 2 Distributed Generation

Thailand is one of the countries that have adopted such distributed generation schemes. The Small

Power Producers (SPP) and Very Small Power Producers (SPP) programs implemented by the Thai

government have been success stories and such achievement can be measured by the number of SPP

and VSPP licenses issued in Thailand. The future of distributed generation in Thailand looks promising

and both schemes are expected to further grow with the upcoming release of the next Power

Development Plan.

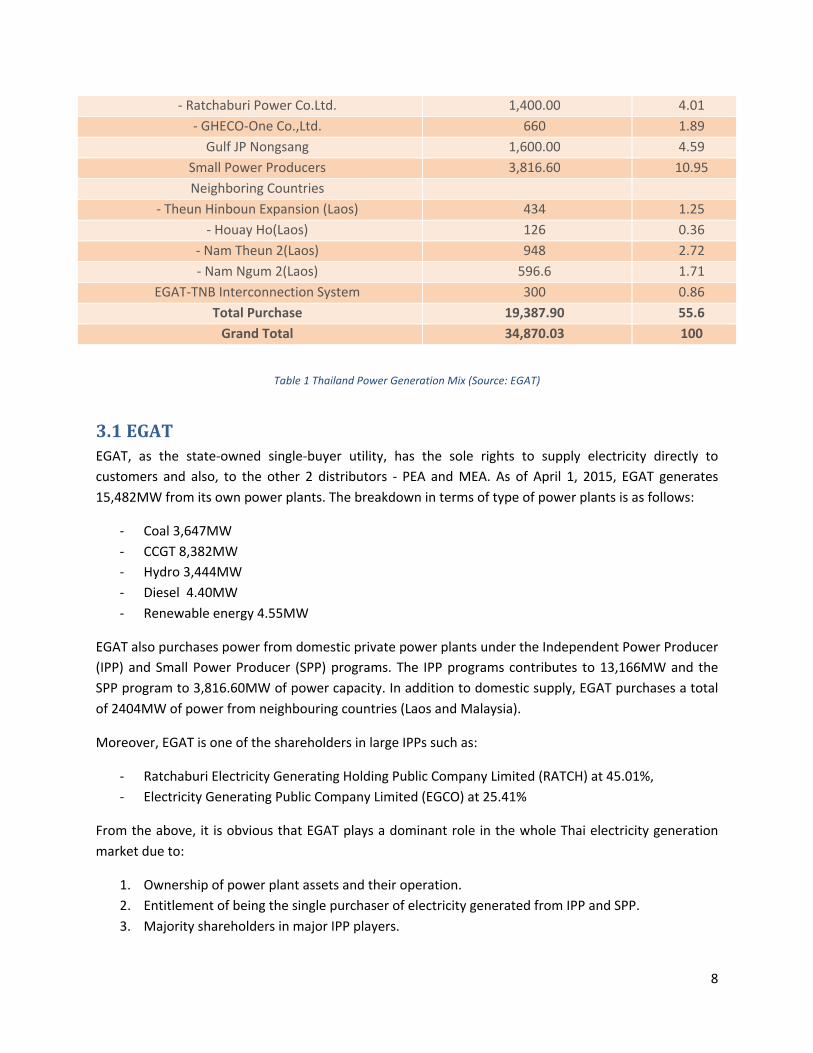

3. GeneralMarket Overview

Thai electricity market operates under a single-buyer system and consists of three main state-owned

players, as illustrated in Figure 3 below. Electricity Generating Authority of Thailand (EGAT) acts as the

single buyer and controls a sizeable part of generation capacity and the transmission system. Two

utilities the Provincial Electricity Authority (PEA) and the Metropolitan Electricity Authority of Thailand

(MEA) are responsible for electricity distribution to end-users. As of April 2015, Thailand’s Power System

has total generation capacity of 34.87GW as shown in Table 1.

7

Figure 3 Thailand Electricity Market (Source: www.pugnatorius.com)

Type of Power Plant Apr-15

MW %

EGAT’s Power Plants

- Thermal 3,647.00 10.46

- Combined cycle 8,382.00 24.04

- Hydropower 3,444.18 9.88

- Diesel 4.4 0.01

- Renewable energy 4.55 0.01

Total 15,482.13 44.4

Purchase from

Domestic Private Power Plants

Independent Power Producers

- Electricity Generating Public Co.,Ltd 748.2 2.15

- Ratchaburi Electricity Generating Co.,Ltd. 3,481.00 9.98

- Global Power Synergy Co.,Ltd. 700 2.01

- Tri Energy Co.,Ltd. 700 2.01

- Glow IPP Co.,Ltd. 713 2.04

- Eastern Power & Electric Co.,Ltd. 350 1

- BLCP Power Limited 1,346.50 3.86

- Gulf Power Generation Co.,Ltd. 1,468.00 4.21

8

- Ratchaburi Power Co.Ltd. 1,400.00 4.01

- GHECO-One Co.,Ltd. 660 1.89

Gulf JP Nongsang 1,600.00 4.59

Small Power Producers 3,816.60 10.95

Neighboring Countries

- Theun Hinboun Expansion (Laos) 434 1.25

- Houay Ho(Laos) 126 0.36

- Nam Theun 2(Laos) 948 2.72

- Nam Ngum 2(Laos) 596.6 1.71

EGAT-TNB Interconnection System 300 0.86

Total Purchase 19,387.90 55.6

Grand Total 34,870.03 100

Table 1 Thailand Power Generation Mix (Source: EGAT)

3.1EGAT

EGAT, as the state-owned single-buyer utility, has the sole rights to supply electricity directly to

customers and also, to the other 2 distributors - PEA and MEA. As of April 1, 2015, EGAT generates

15,482MW from its own power plants. The breakdown in terms of type of power plants is as follows:

- Coal 3,647MW

- CCGT 8,382MW

- Hydro 3,444MW

- Diesel 4.40MW

- Renewable energy 4.55MW

EGAT also purchases power from domestic private power plants under the Independent Power Producer

(IPP) and Small Power Producer (SPP) programs. The IPP programs contributes to 13,166MW and the

SPP program to 3,816.60MW of power capacity. In addition to domestic supply, EGAT purchases a total

of 2404MW of power from neighbouring countries (Laos and Malaysia).

Moreover, EGAT is one of the shareholders in large IPPs such as:

- Ratchaburi Electricity Generating Holding Public Company Limited (RATCH) at 45.01%,

- Electricity Generating Public Company Limited (EGCO) at 25.41%

From the above, it is obvious that EGAT plays a dominant role in the whole Thai electricity generation

market due to:

1. Ownership of power plant assets and their operation.

2. Entitlement of being the single purchaser of electricity generated from IPP and SPP.

3. Majority shareholders in major IPP players.

9

3.2PEA andMEA

The distribution market is controlled and geographically separated by the PEA and MEA.

PEA is a stated-owned enterprise in the utility sector attached to the Interior Ministry. Its primary

responsibilities include procurement, distribution and sale of electricity to the public, business and

industrial sectors in 74 provinces, over a nationwide area of 510,000 square kilometers or 99.4% of

Thailand, with the exception of Bangkok, Nonthaburi and Samut Prakarn provinces.

MEA is a stated-owned enterprise and is responsible on supplying electric power to distribution areas

for three provinces: Bangkok Metropolis, Samut Prakan and Nonthaburi with a coverage service area of

3,192 square kilometres. As per its Annual Report 2013, MEA energy sales was 47,617 GWh and MEA

had 3,281,574 customers.

3.3PowerDevelopmentPlan(PDP) 2010 Rev3

Power Development Plan (“PDP”) is an official study and projection of the electricity supply and demand

in Thailand over 20 year period, endorsed by the National Energy Policy Council and the Cabinet. PDP

2010 Revision 3, of which a summary was published in June 2012, indicates that the total added capacity

during the period of 2012 – 2030 would be 55,130 MW according to the following power plant types:

1. Renewable energy power plants 14,580 MW

a. Power purchase from domestic 9,481 MW

b. Power purchase from neighboring countries 5,099 MW

2. Cogeneration 6,476 MW

3. Combined cycle power plants 25,451 MW

4. Thermal power plants 8,623 MW

a. Coal-fired power plants 4,400 MW

b. Nuclear power plants 2,000 MW

c. Gas turbine power plants 750 MW

d. Power purchase from neighboring countries 1,473 MW

Total 55,130 MW

From the above, 6,476MW is expected to come from Cogeneration plants under SPP and VSPP schemes.

All information related to VSPP Cogeneration have been extracted from Appendix 4 of PDP 2010

Revision 3, and the results are compiled below in Table 2.

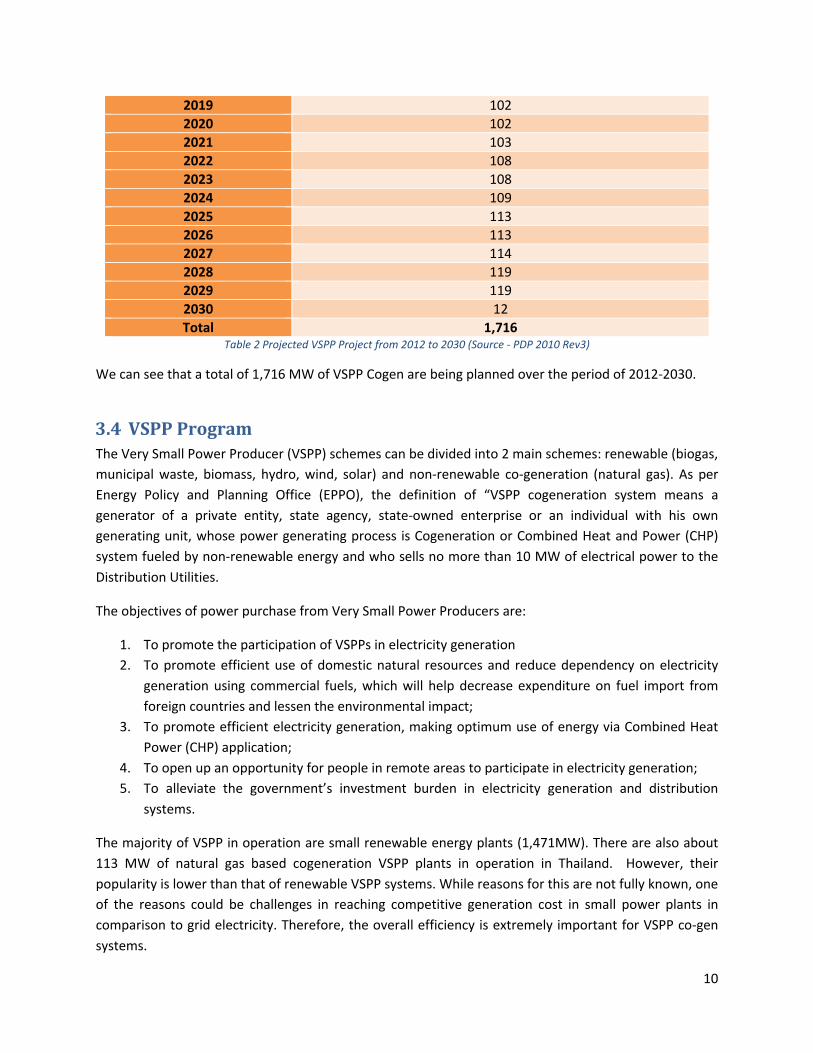

Year Projected VSPP Projects (MW)

2012 27

2013 43

2014 59

2015 76

2016 96

2017 96

2018 97

10

2019 102

2020 102

2021 103

2022 108

2023 108

2024 109

2025 113

2026 113

2027 114

2028 119

2029 119

2030 12

Total 1,716Table 2 Projected VSPP Project from 2012 to 2030 (Source - PDP 2010 Rev3)

We can see that a total of 1,716 MW of VSPP Cogen are being planned over the period of 2012-2030.

3.4 VSPPProgram

The Very Small Power Producer (VSPP) schemes can be divided into 2 main schemes: renewable (biogas,

municipal waste, biomass, hydro, wind, solar) and non-renewable co-generation (natural gas). As per

Energy Policy and Planning Office (EPPO), the definition of “VSPP cogeneration system means a

generator of a private entity, state agency, state-owned enterprise or an individual with his own

generating unit, whose power generating process is Cogeneration or Combined Heat and Power (CHP)

system fueled by non-renewable energy and who sells no more than 10 MW of electrical power to the

Distribution Utilities.

The objectives of power purchase from Very Small Power Producers are:

1. To promote the participation of VSPPs in electricity generation

2. To promote efficient use of domestic natural resources and reduce dependency on electricity

generation using commercial fuels, which will help decrease expenditure on fuel import from

foreign countries and lessen the environmental impact;

3. To promote efficient electricity generation, making optimum use of energy via Combined Heat

Power (CHP) application;

4. To open up an opportunity for people in remote areas to participate in electricity generation;

5. To alleviate the government’s investment burden in electricity generation and distribution

systems.

The majority of VSPP in operation are small renewable energy plants (1,471MW). There are also about

113 MW of natural gas based cogeneration VSPP plants in operation in Thailand. However, their

popularity is lower than that of renewable VSPP systems. While reasons for this are not fully known, one

of the reasons could be challenges in reaching competitive generation cost in small power plants in

comparison to grid electricity. Therefore, the overall efficiency is extremely important for VSPP co-gen

systems.

11

The total amount of VSPP in operation is now 1,585 MW (476 projects). In addition, 412 projects (2,142

MW) are under implementation and construction. In total, 888 VSPP licenses for 3,727 MWs have been

released. In addition, around 1,244 MW of capacity (313 projects) currently under PPA signing process

will also be added to the system. Therefore, the total amount of VSPPs in operation, construction, and

PPA process is 4,971 MW (1,201 projects). The majority of these are solar power plants with a total

capacity of 2,465MW (572 projects). A complete list of VSPP projects is listed below in Table 3.

Status In Operation Under Implementation / Construction

Under Process of Power Purchasing

Agreement

VSPP Number of Projects

Generating Capacity (MW)

Number of Projects

Generating Capacity (MW)

Number of Projects

Generating Capacity (MW)

Biogas 95 158 60 107 36 54

Municipal Waste 18 43 16 111 4 20

Biomass 104 642 141 990 83 160

Hydro 2 1 11 14 3 0

Wind 8 9 22 69 3 16

Solar 226 619 162 850 184 996

Natural Gas 23 113 0 0 0 0

Total Renewable (1) 453 1471 412 2142 313 1244

Non-Renewable (2) 23 113 0 0 0 0

Total (1) + (2) 476 1585 412 2142 313 1244

Table 3 VSPP Status (February 2014 (Source: http://www.erc.or.th/ERCSPP/MainPage.aspx)

4. FeasibilityStudy:Internalcombustionengine(ICE)

In this section, we evaluate the feasibility of internal combustion engine technology for the Thailand

VSPP market. From this study, we would know whether it makes sense both technically and

economically to have a VSPP cogeneration using Internal Combustion Engine (ICE) with natural gas as

fuel.

4.1 InternalCombustionEngine(ICE)Today’s modern internal combustion engines are excellently suited for various stationary power

generation applications. They cover a wide capacity range, and have the highest simple cycle efficiency

in the industry. At the lower end of the range, the power plant can consist of only one generating set,

while larger plants can consist of tens of units and have a total output of several hundred MW.

12

On 29 April 2015, the inauguration of IPP3, the world’s largest internal combustion engine (ICE) power

plant, took place at the plant site near Amman, Jordan. The plant is powered by 38 Wärtsilä 50DF multi-

fuel engines with a combined capacity of 573 MW. In recognition of its world record size, the plant has

been accepted into the Guinness book of records.

Figure 4 The tri-fuel power plant IPP3 is the world’s largest internal combustion engine power plant. It comprises 38 Wärtsilä 50DF engines with a combined capacity of 573 MW.

Combustion engine power plant solutions have many unique features compared to power plants based

on other technologies.

Below are the key features of internal combustion engines:

a) Flexible plant sizes

Investments in combustion engine power plants can easily be made in several steps. Due to

several sizes of engine generating sets, the right number of units can be chosen to match the

required power demand. This breaks the concept of “one size fits all” for power plants. For

example, a power plant can initial operate on open cycle application. Later, due to increased

power demand or funds availability, additional units can be added or Heat Recovery Steam

Generators (HRSG) and a steam turbine can be installed to close the cycle for combined cycle

operation. This modular concept also enables easy and repeatable installation work.

b) Multiple independent units

13

Since power plants typically consist of several generating sets, the excellent fuel efficiency can

be maintained across a wide load range also at part load operation. The plant can be operated

at all loads with almost the same high efficiency.

c) Start-up, synchronisation and loading

Fast start-up, synchronisation, and quick loading are valuable benefits for power plant owners.

Quick synchronization (30 seconds) is especially valuable for the grid operator, as these plants

are the first to synchronise when an imbalance between supply and demand begins to occur.

System operators benefit from the possibility to support and stabilize the grid in many

situations, such as peaking power, reserve power, load following, ancillary services including

regulation, spinning and non-spinning reserve, frequency and voltage control, and black-start

capability.

d) Fast track EPC project delivery

Internal Combustion engine power plant construction projects can be executed with fast

delivery schedules. EPC (engineering, procurement, construction) power plant construction

projects can take as little as 10 months from the notice to proceed to final handing over. As an

example, a 102 MW Dohazari power plant in Asia was delivered in only 10 months.

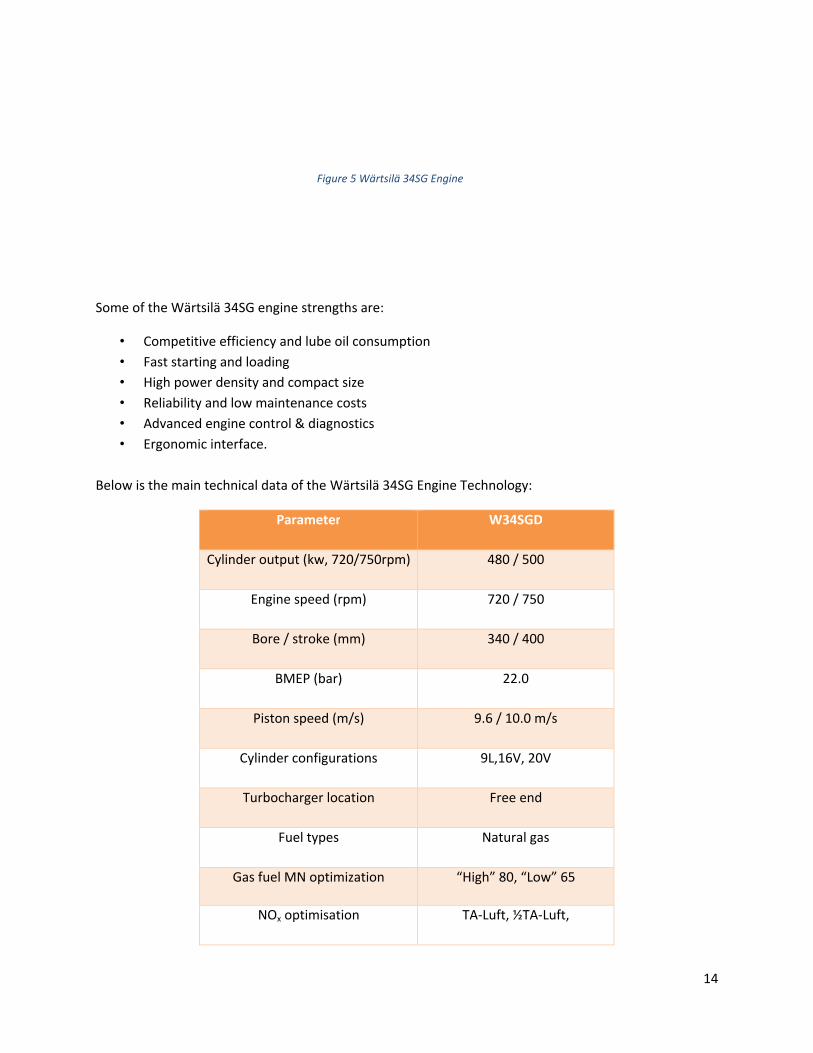

4.2Wärtsilä34SGEngineTechnologyThe Wärtsilä 34SG is a four-stroke, spark-ignited gas engine that works according to the Otto process

and the lean-burn principle. The engine has ported gas admission and a pre chamber with a spark plug

for ignition. The engine runs at 720 or 750 rpm for 60 or 50 Hz applications and produces 9,340 and

9,730 kW of power, respectively. The efficiency of the Wärtsilä 34SG is among the highest of any spark-

ignited gas engines today. The natural gas fuelled, lean-burn, medium-speed engine is a reliable, high-

efficiency and low-pollution power source for baseload, intermediate, peaking and cogeneration plants.

Wärtsilä has delivered more than 1000 34SG engines (8.7 GW) to 40 countries worldwide and

accumulated more than 14 million running hours.

14

Figure 5 Wärtsilä 34SG Engine

Some of the Wärtsilä 34SG engine strengths are:

• Competitive efficiency and lube oil consumption

• Fast starting and loading

• High power density and compact size

• Reliability and low maintenance costs

• Advanced engine control & diagnostics

• Ergonomic interface.

Below is the main technical data of the Wärtsilä 34SG Engine Technology:

Parameter W34SGD

Cylinder output (kw, 720/750rpm) 480 / 500

Engine speed (rpm) 720 / 750

Bore / stroke (mm) 340 / 400

BMEP (bar) 22.0

Piston speed (m/s) 9.6 / 10.0 m/s

Cylinder configurations 9L,16V, 20V

Turbocharger location Free end

Fuel types Natural gas

Gas fuel MN optimization “High” 80, “Low” 65

NOx optimisation TA-Luft, ½TA-Luft,

15

IED2010 (0.4xTA-Luft)

Table 4 Technical data for Wärtsilä 34SG Engine Technology

Below is the engine range in the Wärtsilä 34SG Engine Technology:

Figure 6 Engine range in the Wärtsilä 34SG Engine Technology

4.3WärtsiläGasCube

The Wärtsilä GasCube is a modular, pre-engineered single-engine power plant produced within a cost

framework that justifies turnkey deliveries for small plants while still complying with the needs of

different clients and applications. With this solution, the same benefits as customers for large turnkey

power plants can be enjoyed such as proven technical and logistical solutions and reliable delivery

schedules guaranteed by a single supplier. Gas cube concept can be cost efficiently employed also for 2

and 3 engine power plant installations.

16

Figure 7 Wärtsilä GasCube

Figure 8 GasCube Bontang, Indonesia (2 x Wärtsilä 16V34SG)

Some of the advantages of the Cube Design are listed below:

Validated and reliable technical solutions

High electrical efficiency through minimization of the plant’s own consumption

17

Compact design and a minimized annex system

Fluent and cost-efficient project execution from planning to start-up

Optimized lifetime support and reduced warranty costs

Future expansion flexibility.

4.4WärtsiläEPCcapabilitiesIn addition of being the leading supplier of Internal Combustion Engines for global power generation

markets, Wärtsilä has proven capabilities to execute power plant projects on EPC/ full turnkey basis.

Once awarded the contract, Wärtsilä takes care of all engineering, logistics, construction, installation

and commissioning. The customer has a single point of contact and in the end, receives a complete

Power Plant solution which is fully ready to start operating.

Wärtsilä Global EPC experience is a total of 456 plants with 1,657 engines producing 15,873 MW in 103

countries over the last 35 years.

4.5WärtsiläO&McapabilitiesWärtsilä has provided operation and maintenance (“O&M”) services to customers owning Wärtsilä

equipped power plants for over 20 years. Wärtsilä currently operates 151 power plants worldwide with

a total of 6600 MW under O&M contracts.

4.6 CaseStudy– WärtsiläGasCube (1x20V34SG)In this case study, we evaluate the feasibility of a VSPP cogen system for an industrial user. W e have

chosen Wärtsilä GasCube with 1 unit of 20V34SG as prime mover for a VSPP engine-based cogeneration

power plant. We calculate the payback period for the VSPP cogeneration system where half of the

electric output is used to replace grid electricity purchases and the other half is sold to a distribution

utility under the VSPP tariff scheme. Thermal output of the cogenerat ion plant is assumed to partially

replace industrial natural gas use for steam generation.

18

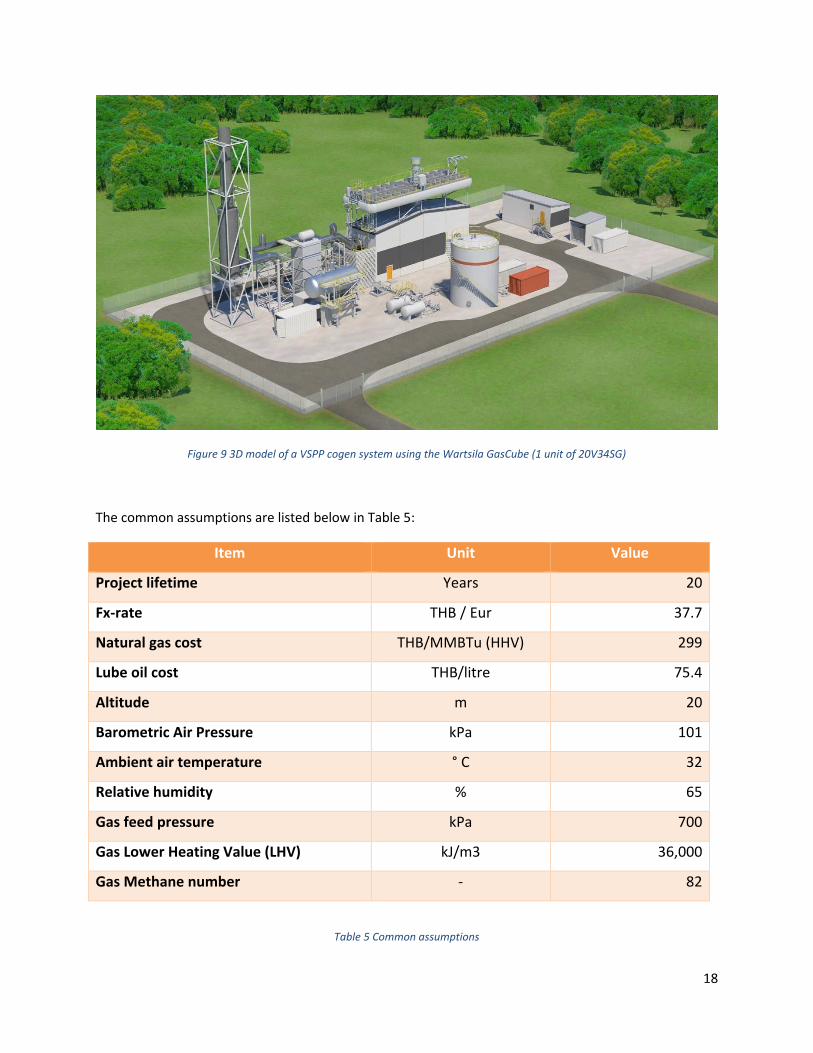

Figure 9 3D model of a VSPP cogen system using the Wartsila GasCube (1 unit of 20V34SG)

The common assumptions are listed below in Table 5:

Item Unit Value

Project lifetime Years 20

Fx-rate THB / Eur 37.7

Natural gas cost THB/MMBTu (HHV) 299

Lube oil cost THB/litre 75.4

Altitude m 20

Barometric Air Pressure kPa 101

Ambient air temperature ° C 32

Relative humidity % 65

Gas feed pressure kPa 700

Gas Lower Heating Value (LHV) kJ/m3 36,000

Gas Methane number - 82

Table 5 Common assumptions

19

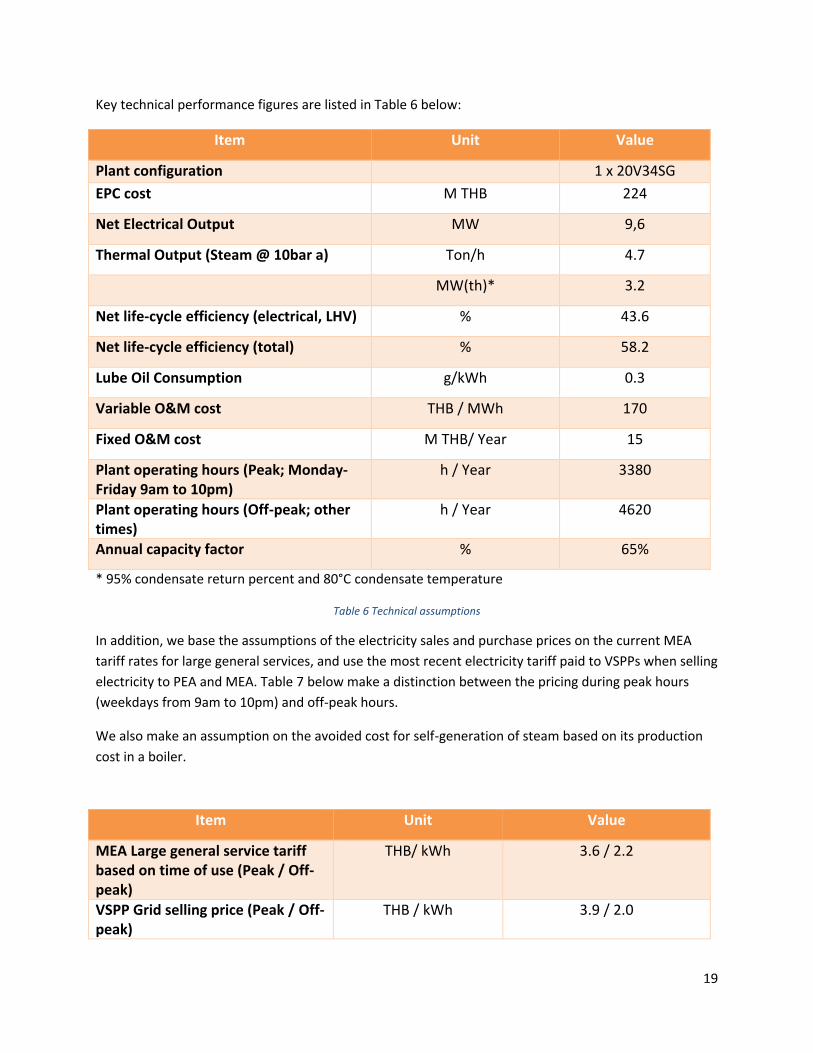

Key technical performance figures are listed in Table 6 below:

Item Unit Value

Plant configuration 1 x 20V34SG

EPC cost M THB 224

Net Electrical Output MW 9,6

Thermal Output (Steam @ 10bar a) Ton/h 4.7

MW(th)* 3.2

Net life-cycle efficiency (electrical, LHV) % 43.6

Net life-cycle efficiency (total) % 58.2

Lube Oil Consumption g/kWh 0.3

Variable O&M cost THB / MWh 170

Fixed O&M cost M THB/ Year 15

Plant operating hours (Peak; Monday-Friday 9am to 10pm)

h / Year 3380

Plant operating hours (Off-peak; other times)

h / Year 4620

Annual capacity factor % 65%

* 95% condensate return percent and 80°C condensate temperature

Table 6 Technical assumptions

In addition, we base the assumptions of the electricity sales and purchase prices on the current MEA

tariff rates for large general services, and use the most recent electricity tariff paid to VSPPs when selling

electricity to PEA and MEA. Table 7 below make a distinction between the pricing during peak hours

(weekdays from 9am to 10pm) and off-peak hours.

We also make an assumption on the avoided cost for self-generation of steam based on its production

cost in a boiler.

Item Unit Value

MEA Large general service tariff based on time of use (Peak / Off-peak)

THB/ kWh 3.6 / 2.2

VSPP Grid selling price (Peak / Off-peak)

THB / kWh 3.9 / 2.0

20

Ft rate THB / kWh 0.3

Electricity demand for industrial use (Peak / Off-peak)

MW 4.8 / 4.8

Electricity sold to distribution utility (Peak / Off-peak)

MW 4.8 / 0

Steam use Tons / hour 4.7

Steam production cost in a boiler MWh (th) 1.3

Table 7 Tariff assumptions

Based on the assumptions listed above in Tables 5, 6 and 7, we can calculate the average electricity cost

of production, as summarized in Table 8 below.

Variable costs THB/kWh M THB/year

Variable expenses 0.2 10.5

Fuel expenses 2.7 149.1

Total Variable Costs 2.9 160.0

Fixed costs

Fixed expenses 0.3 15.0

Cost of own capital (5%) 0.2 11.2

Cost of Production 3.4 185.9

Table 8 Cost of production for 1 x 20V34SG cogeneration system

Cost of production for electricity with the co-generation system doesn’t give a complete picture of the

project feasibility. In addition, we need to consider the savings from replacing steam generation by

cogeneration system. We assume that in absence of VSPP co-generation system, the steam would be

generated using natural gas in an industrial boiler. Finally, the project can generate additional revenue

by selling 50% of power output to the distribution utility under VSPP rates during peak times. The results

of the overall project costs and revenues are illustrated below in Table 9 and Figure 10.

Item Unit Value

Annual production (electricity) MWh 54 453

Annual production (steam) MWh 25 688

Project Savings 20 year average

+ Avoided cost (Grid Purchase for industrial use)

M THB /year 117.8

+ Avoided cost (Steam production) M THB /year 34.6

+ Revenue from electricity sold under VSPP scheme

M THB /year 67.4

21

- Fuel cost M THB /year - 149.1

- Variable operating cost M THB /year -10.5

- Annual fixed operating cost M THB /year -15.1

Total savings M THB /year 43.5

Payback Years 5.1

Table 9 VSPP project savings and payback time

Figure 10 Cumulative savings for a VSPP cogeneration project

The results illustrate that for an industry with some steam and electricity demand, the cogen VSPP

scheme is a good fit. The project can take advantage of time of use tariffs and sell surplus output to the

grid during times when grid sales price is high. Due to the high total efficiency of over 58%, the project

can reach significant savings with about 5 years’ payback period.

5. ConclusionTo summarize, Thailand has invested heavily in promoting energy efficiency, distributed generation, and

renewable energy through SPP and VSPP schemes. In particular, VSPP projects based on renewable and

cogeneration systems will continue to benefit from government’s policies and subsidies programme

implemented during last few years. We firmly believe that the next Power Deve lopment Plan (PDP)

- 300,000

- 200,000

- 100,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

0 2 4 6 8 10 12 14 16 18 20

Years

Cumulative savings

22

which is expected to be officially released in the near future, will provide further incentives for both

foreign and local investors to move towards Distributed Generation. Hence, it is clear that Distributed

Generation will keep on growing over the next few decades and represent the way forward in Thailand

This paper gives an overview of the Power Development Plan (PDP), focuses on VSPP scheme, and also,

introduces Wärtsilä V34SG gas engine model, which is an ideal choice for VSPP cogene ration systems.

For a typical VSPP system with both industrial use and electricity sales to grid, a VSPP project with 1 unit

of Wärtsilä 20V34SG can yield payback time of 5 years and total efficiency of over 58%. With such value

proposition, Wärtsilä is offering an alternative solution to VSPP owners and investors. This will

contribute in the long term to the ever-growing success of VSPP cogeneration power plants in Thailand.