Embed Size (px)

Citation preview

Post-harvest losses in potato value chains in Kenya Analysis and recommendations for reduction strategies

Published by

2

Table of Contents

ABSTRACT 6EXECUTIVE SUMMARY 7 1 InTRodUCTIon 11 1.1 Study objective 11 1.2 Concept of food loss 11 1.2.1 The study approach 11 1.2.2 Definition of loss and critical loss points 12

2 METhodologY 14 2.1 Sampling of counties and value chain actors 14 2.2 Measurement 17 2.3 Load tracking 18

3 PoTATo VAlUE ChAIn In KEnYA – SURVEY RESUlTS 19 3.1 Background 19 3.2 Potato production 21 3.2.1 Ware potato growers 21 3.2.2 Comparison between contracted and non-contracted farmers 28 3.3 Potato marketing 30 3.3.1 Brokers at the farm level 30 3.3.2 Wholesale and retail trade 31 3.3.3 Supermarkets 35 3.3.4 Restaurants 35 3.4 Potato processing 36 4 AnAlYSIS oF Food loSSES And oPTIonS FoR Food loSS REdUCTIon 38 4.1 Assessment of quantitative and financial losses in the potato value chain 38 4.2 Challenges and options for food loss reduction 43 4.2.1 Seed improvements 43 4.2.2 Improved production and harvesting technologies 44 4.2.3 Improved post-harvest handling 45 4.2.4 Improved conditions for the processing industry 46 4.2.5 Capacity building and agricultural finance 47 4.3 List of important actors in the potato sub-sector 48 AnnEX 51 Annex 1: Surveys details and methodology 51 Annex 2: Further survey data 54

QUESTIonnAIRES 67

REFEREnCES 78

Table of CoNTeNTS

3Table of CoNTeNTS

list of tablesTable 1: Critical loss points along the potato value chain 13Table 2: Breakdown of farmer samples 16Table 3: Breakdown of samples of other value chain actors 16Table 4: Traditional potato measures 18Table 5: Traditional measures and their metric conversions 18Table 6: Main potato producing counties and the total area under potato production in Kenya 19Table 7: Land holdings and farming practices 22Table 8: Potato varieties grown 23Table 9: Farmers who experience losses during production and harvest 25Table 10: Sorting and grading practices 26Table 11: Potato storage practices 26Table 12: Losses in storage 27Table 13: Farmers’ transport and marketing practices 28Table 14: Contracted and non-contracted farmers in Bomet and Nyandarua Counties 29Table 15: Potato traders repacking bags 32Table 16: Results of bag tracking in kg 34Table 17: Results of opening bags at different markets 34Table 18: Characteristics of restaurants (multiple choice) 36Table 19: Market shares of different market channels in the potato value chain 36Table 20: Synopsis of reported damage/loss along the value chain 38Table 21: Production and loss/damage at the farm level 39Table 22: Weight and losses at the trader level in kg and % per bag 40Table 23: Average potato purchase prices in October/November 2013 41Table 24: Financial calculation of damage and loss occurring along the ware potato value chain 42Table 25: Relevant institutions and actors along the potato value chain 48Table 26: Surveys by county 51Table 27: Study methodology following the FAO’s five-stage approach 53Table 28: Characteristics of potato farmers 54Table 29: Farmers’ education levels by gender (%) 54Table 30: Characteristics of potato traders 54Table 31: Traders’ educational levels by gender (%) 55Table 32: Main challenges farmers face in potato production as a % (multiple choice) 55Table 33: Potato seed used by farmers 55Table 34: Seasons for potato planting and harvesting expressed – relevance as a % 57Table 35: Potato pre-harvesting practices 57Table 36: Potato harvesting practices - time and protection from sunlight 58Table 37: Potato harvesting practices - second gathering and handling of leftovers 58Table 38: Potato harvesting practices - tools and labour 59Table 39: Losses experienced on farms 60Table 40: Potato marketing practices 61

4 Table of CoNTeNTS

Table 41: Farm-gate potato prices 61Table 42: Main sourcing and sales markets of traders 63Table 43: Most common bag types bought by traders 63Table 44: Trader-perceived advantages and disadvantages of the main packaging materials 64Table 45: Traders’ preferences for potato varieties and reasons for these preferences (ranking) 64Table 46: Current lowest and highest purchase price 65Table 47: Causes of loss and suggested improvements (multiple choice) 65Table 48: Restauranteurs’ perceptions of the benefits of different potato varieties as a % 66 list of FiguresFigure 1: Synopsis of reported damage and loss occurring within different market channels of the potato value chain 8Figure 2: Map showing the four counties surveyed 15Figure 3: Ware potato value chain 21

list of graphsGraph 1: Causes of damages at retail level 33Graph 2: Use and quality of potatoes 41Graph 3: Types of seed used by farmers, as a % 56Graph 4: Number of seasons after which farmers renew seed, as a % 56Graph 5: Months with highest and lowest farm-gate prices – relevance of month in % 62

list of PhotographsPhotograph 1: The Shangi potato variety 23Photograph 2: Fork jembe 25Photograph 3: Seed potato storage – diffused light store 27Photograph 4: Brokers on site filling extended bags 30Photograph 5: Loading and handling of extended bags at Nairobi’s Wakulima Market 30Photograph 6: Conditions at Nairobi’s Wakulima wholesale market 31Photograph 7: Retailer selling out of an opened extended bag 32Photograph 8: Potato sample from load tracking 34

5Table of CoNTeNTS

AbbreviationsBMZ German Federal Ministry for Economic Cooperation and DevelopmentCIP International Potato CenterDLS Diffused light storeEUR EuroFAO Food and Agriculture OrganizationFPEAK Fresh Produce Exporters Association of Kenya FSP Food Security PortalGAP Good agricultural practicesGFP German Food PartnershipGIZ Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbHGIZ PSDA Private Sector Development in Agriculture ProgrammeHa HectareHCDA Horticultural Crops Development AuthorityILO International Labour OrganizationKARI Kenyan Agricultural Research InstituteKENFAP Kenyan National Federation of Agricultural ProducersKENOPOFA Kenya National Potato Farmers AssociationKEPHIS Kenya Plant Health Inspectorate ServiceKES Kenyan ShillingKIRDI Kenya Industrial Research and Development InstituteKFA Kenya Farmers AssociationKfW KfW Entwicklungsbankkg KilogramMoALF Ministry of Agriculture, Livestock and FisheriesNPCK National Potato Council of Kenya PHL Post-harvest loss SNRD Sector Network Rural Development

Currency exchange rate: eUR 1 = KeS 118

6 abSTRaCT

Abstract

Potato is the second most important food crop in Kenya after maize and is mostly cultivated by smallholders. The Kenyan Government has recognised the critical role potatoes play in alleviating food shortages given that potato provides higher yields compared to maize and is less affected by climate change. The issue of food loss is a highly important factor in securing the stable produc-tion required to combat hunger and raise incomes. food security is a priority area of German development policy. Therefore, the German federal Ministry for economic Cooperation and Development (bMZ) launched the special unit “one World – No Hunger” in order to inten-sify its dedication to alleviate hunger and malnutrition. This study, commissioned by Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) on behalf of bMZ, contributes to these efforts.

The survey on food loss in the potato sub-sector was completed by 247 potato farmers, more than 70 market-ers (brokers, traders, retailers and supermarkets), 3 processors and 10 restaurants. The farmers interviewed were based in the main production areas and thus were more commercially oriented, and, although these farmers’ yields come in above average, they are still low in comparison to yields projected by the Kenyan agricultural Research Institute. The survey showed that up to 95 per cent of recorded damage and loss occurs at the production level and is caused in particular by inappropriate harvesting tools and an insufficiently

trained workforce. With a market share of up to 80 per cent, the retail level is most affected by this, given that any resulting low-quality produce is then supplied to the markets. However, the absence of market signals stress-ing ‘better prices for better quality tubers’ contributes to the low performance in potato production.

The financial assessment of potato damage and loss along the value chain exposes the economic impact of this low performance in potato production. Per season, 19 per cent of produce is damaged or lost. extrapolating these losses to the national production level, we can assume that 815,000 tonnes are damaged or lost each year, representing a value of around KeS 12.9 billion (eUR 109 million).

This study on post-harvest losses of potato contributes to the efforts of the Kenyan Government and private sector to improve the development of the potato value chain. To strengthen market linkages in the potato value chain, it is necessary to stimulate and enhance coop-eration and coordination between the different actors. The intro duction of standardised bags along with per-weight payment and the expansion of contract farming present opportunities to support the market linkage of small-scale farmers. However, an important condition for cooperation is trust between the actors in the value chain.

public and private institutions in Kenya, and also with data from international sources. a verification workshop representing different actors and institutions in the sub-sector was held to discuss the results and elicit further thoughts regarding evaluation and reporting.

Potato is an important food crop in Kenya and is mostly cultivated by smallholders. Potatoes are mainly sold on the market as fresh produce and are then subsequently processed into different foodstuffs at the household or industrial level. Many factors contribute to the loss and damage of produce. at the production level, farmer prac-tices engender heavy losses. land preparation and soil management are poorly conducted, and pests and dis-eases are ineffectively controlled, leading to low yields. a recent survey showed that bacterial wilt was the most prevalent disease, affecting 77 per cent of potato farmers, followed by late blight (67 per cent) and viral diseases (12 per cent) (Kaguongo et al. 2014).

a shortage of clean seed is also contributing to this loss: available certified potato seed meets less than 5 per cent of the national demand for seed potato (Gildemacher et al. 2012). added to this, there is a shortage of high-yield-ing varieties. The farmers interviewed are based in the main production areas and are thus more commercially oriented, achieving yields of 13.5 tonnes per hectare per season. These yields are above average (7-10 tonnes/ha) but are still low when compared to the 25-tonne yields often realised by professional farmers using certified seed and sound agricultural practices. However, the absence of market signals stressing ‘better prices for better qual-ity tubers’ contributes to the low performance in potato production.

The survey showed that up to 95 per cent of recorded damage and loss occurs at the production level and is caused in particular by inappropriate harvesting tools and an insufficiently trained workforce. all produce ear-marked for the fresh food market is packed in so-called extended bags, which farmers and brokers fill with un-selected harvested potatoes – i.e. they include green, cut, bruised or rotten produce. of the potatoes placed on the market, nearly a quarter are damaged or green. almost all of these potatoes are eventually sold, but the quality is-sues mean prices must sometimes be lowered.

every year, a significant proportion of food produced for human consumption is lost or wasted. annual losses have been estimated at about 1.3 billion tonnes by the UN food and agriculture organization (fao 2011). In light of rising food prices, widespread food insecurity and growing pressure on natural resources, avoidable food loss and waste is not acceptable. The world’s natural resources – such as its soil, water, fossil fuels and nutri-ents – are limited and must be used in a more efficient and responsible manner.

The term food wastage, as used by the fao, encompasses both food loss and food waste. Wastage occurs along the entire food value chain and varies in extent depending on the produce and the region. In developing countries, food loss occurs mostly in the post-harvest stages, during marketing and processing.

This study focuses on food loss in the harvesting, pro-cessing and marketing stages. Its main aim is to improve data availability on food loss in an important food value chain in Kenya and to identify options for German Development Cooperation to engage in food loss reduc-tion programmes.1

The scope of the study was to describe a typical value chain for potatoes (from harvest to retailer), providing quantitative and qualitative analysis of food loss, detect hot spots for loss, determining the causes of food loss, identifying important actors and partners in the private and public sectors and the research and donor commu-nities, and examining the role of these actors in reducing food loss along value chain. finally, it aimed to provide recommendations for reducing food loss at the opera-tional and policy level, and for the future engagement of the German federal Ministry for economic Cooperation and Development (bMZ).

The survey was completed by 247 potato farmers, more than 70 marketers (brokers, traders, retailers and super-markets), 3 processors and 22 restaurants. field data have been supplemented with information available from

1 See also the GIZ publication ‘food losses in Cassava and Maize Value Chains in Nigeria. analysis and Recommenda-tions for Reduction Strategies, 2013’.

7exeCUTIVe SUMMaRy

Executive Summary

8 exeCUTIVe SUMMaRy

most affected by the low quality of produce supplied to the markets. losses reported by the processing industry and supermarkets run from 12 per cent to 25 per cent within sector businesses. However, given that their mar-ket share remains small (but growing), this damage and loss only contributes around 5 per cent to the overall damage and loss occurring along the value chain.

The data on loss in the value chain shown in figure 1 below describes the damage and loss reported at each stage in the chain (farmers, processors, marketers). The percentages are based on different produce quantities and are therefore not part of an overall total percentage. However, they do expose significant hot spots and chal-lenges in terms of post-harvest losses. The retail level is

Figure 1: Synopsis of reported damage and loss occurring within different market channels of the potato value chain

Reported damage and loss occurring within different market channels

Farm level 12.8%

Harvesting12.0%

Handling/transport8.8%

Storage0.8%

Sorting 15.6%

open market 24.4%

Processing 12%

Varieties/sorting10%

Quality25%

Processing2%

Demandnot available

Supermarkets 25%

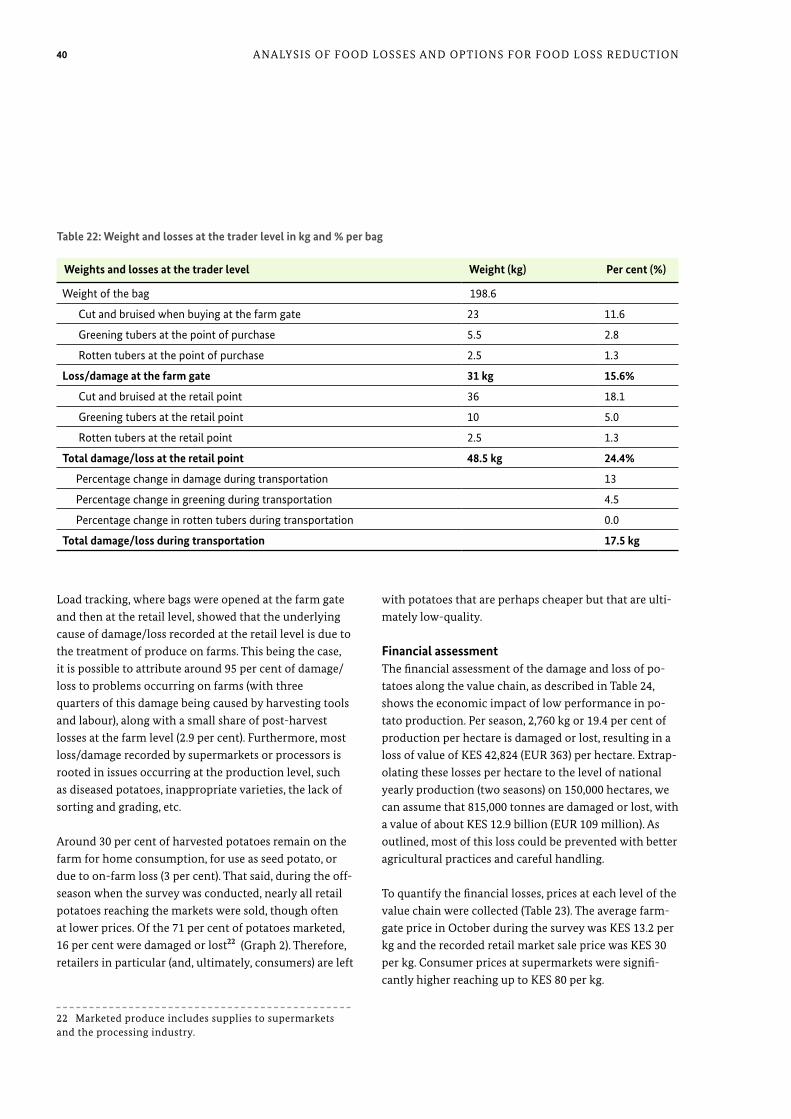

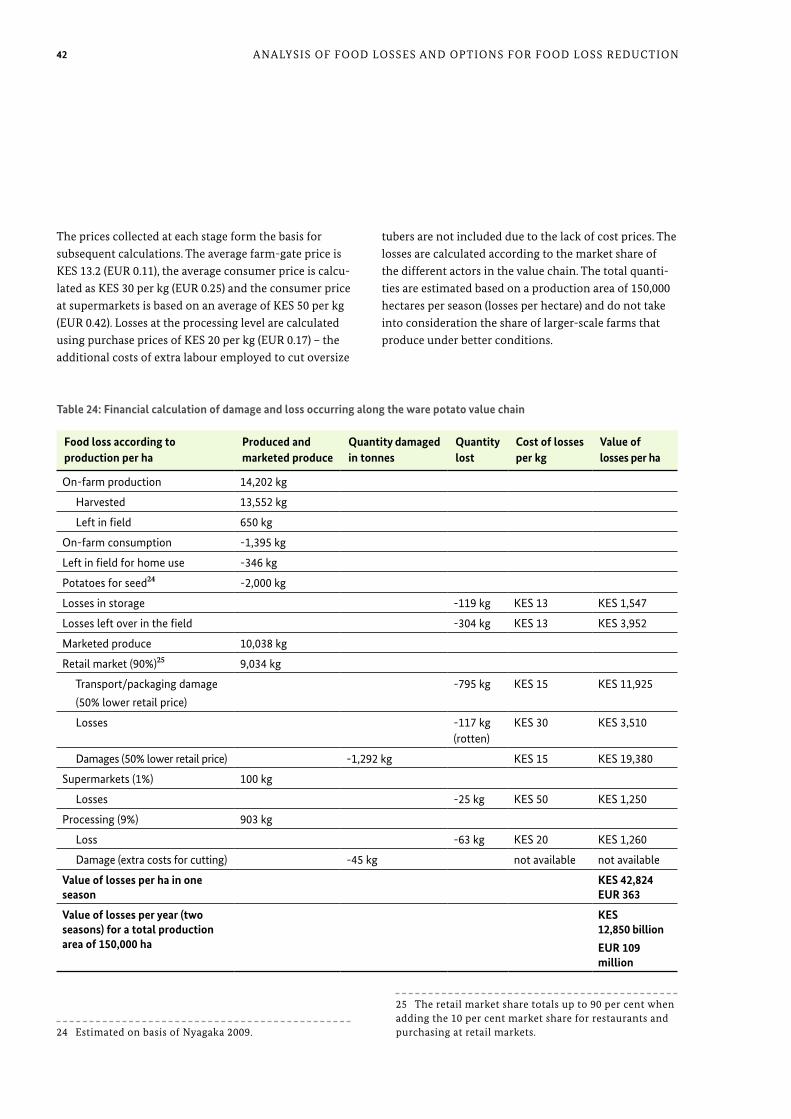

The financial assessment of potato damage and loss along the value chain exposes the economic impact of this low performance in potato production. In each harvest season, 2,715 kg or 19 per cent of per-hectare production is damaged or lost, representing a loss of KeS 42,824 (eUR 363) per hectare. extrapolating these per-hectare losses to the national production level, we can assume that 815,000 tonnes of produce are damaged or lost each year, representing a value of around KeS 12.9 billion (eUR 109 million).

The Kenyan Government has recognised potato’s criti-cal role in alleviating food shortages in the context of the decreasing production of maize and other staples (Mwaura 2009). The development of potato production could form part of the solution to overcome such short-ages given that potatoes have higher yields compared to

maize.2 This being the case, improvements in the potato sub-sector will also benefit food security in the country.

This study on post-harvest losses of potato and its find-ings also intend to contribute to the development of the sub-sector by, in particular, supporting the Kenyan Gov-ernment in its efforts to improve the development of the potato value chain. as such, Chapter 3 of this report sets out the challenges and options for delivering improve-ments along the ware potato value chain, summarised as follows:

2 fao (2009) established the cereal and maize equivalents based on the calorie content of selected foods, which indicate that five units of potato can replace one unit of maize.

9exeCUTIVe SUMMaRy

holders should also group together to share equipment and thereby generate economies of scale.

Improved post-harvest handlingThe currently dominant potato variety is Shangi,3 which has a short dormancy and begins sprouting after only five to six weeks. as such, it is not suitable for longer-term storage, neither as seed nor as ware potato. Improving seed and ware potato quality requires new varieties, which, in turn, requires improved on- and off-farm storage and storage technology. Diffused light stores (DlS) and im-proved traditional stores (with charcoal-coated walls) have proved to be useful low-cost storage alternatives, particu-larly for storing seed potatoes. However, to date, neither of these storage technologies is widely used in Kenya.

The Dutch study ‘Value Chain of Seed and Ware Potatoes in Kenya’ (Janssens et al. 2013) calculated that modern cooled storage facilities should have a minimum capacity of 100 tonnes to make investment worthwhile. Small- capacity storage facilities are relatively expensive and substantially raise investment and running cost per kg of seed potatoes. Consequently, professional modern stor-age is more attractive for the farmers, farmer groups or processors who store big quantities.

Improved packagingThe Kenyan Government and private sector sought to improve packaging by means of legal Notice No 44 of 2005 and No 113 of 2008, which specify that potato must be marketed in standard bags of 110 kg. besides the weight, the standard also defined the packaging mate-rial suitable for potatoes. The implementation of this law did not result in a real change, as it was not properly enforced. Recently the Government, National Potato Council of Kenya (NPCK) and county governments have started a new initiative to introduce maximum 50 kg bags in line with the requirements of the International labour organization (Ilo).

as the survey results show, extended bags have severe impacts on the quality of potatoes marketed. This is because produce is paid for per bag rather than per kilo-gram and bag sizes vary, even within the same categories.

3 Shangi has also been called ‘Zangi’ or ‘Cangi’ in different publications.

Seed improvements – new varieties and rapid multiplicationThe limited availability and use of quality seed potato is a key barrier to increasing productivity in Kenya’s potato sector. To improve certified seed potato supply, research institutes and the private sector have begun introducing an aeroponics technique in which mini-tubers are grown from in vitro plants in protected greenhouses. further-more, after a long period during which Kenya barred seed imports, the Kenyan Ministry of agriculture, live-stock and fisheries (Moalf) has begun cooperating with the Dutch Government and private companies on a fast-track system for rapidly multiplying certified seed.

a further challenge for seed potato production is the ab-sence of a distribution system for certified seeds. farm-ers seeking seed potatoes sometimes must travel more than 200 km to reach quality seed providers. Improving the seed potato distribution network is therefore of the utmost importance for reaching more farmers with cer-tified seed.

Improved production and harvesting technologiesSoil fertility is one of the major problems in potato farm-ing in Kenya. fertiliser use in Kenya is low compared to the recommended rates of application and this results in the rapid decline of soil fertility. The biggest complaint farmers make is about increasing input costs and this factor results in the limited use of agro-inputs. about 38 per cent of farmers in Kenya stated that the costs of fertiliser, fungicide and employee wages have been ris-ing and that this affects their incomes. Consequently, the lack of funds to buy inputs was reported as an important problem affecting potato production in Kenya (Kaguongo et al. 2008). This being the case, small-scale as well as larger-scale farmers should be supported in applying good agricultural practices to improve soil fertility, seed quality, fertilising and spraying.

on smallholdings, most work is performed manually, resulting in significant potato damage and loss. as the survey shows, damage caused by casual labour and har-vesting tools represents 7.4 per cent of on-farm losses. an ongoing challenge for reducing damage is the presence of farms that are too small for mechanisation. as such, the size of potato production and harvesting machinery in Kenya should be geared towards local needs. Small-

10 exeCUTIVe SUMMaRy

a further market signal could come from contract farm-ing, which helps farmers to exit the vicious circle of insecure markets and exploitation through extended bags. Contract farming is a well-known arrangement for supplying the processing industry, but processors in Kenya face problems in their cooperations with farmers. as such, processors and farmers should be supported in developing stable business relationships to ensure the provision of suitable varieties, appropriate sorting and constant supply.

human capacity developmentThere is a need to expand farmers’ training on improved agronomic and management practices, with the support of extension services. Priority should be given to inno-vative approaches that enhance extension and farmer training, such as (i) the use of group approaches, (ii) farm-er-led extension that involves, for example, farmer field schools operating demonstration plots, on-farm trials, etc., and (iii) the provision of communications technol-ogy (ICT) to support agricultural production (Nyagaka et al. 2009).

besides farmers, those involved in trading stock also need comprehensive training to improve their post-harvest handling, storage, processing and marketing. Relevant training should be provided to operators in the wholesale and retail markets to improve their handling and storage of produce with a view to maintaining qual-ity and reducing physical losses.

as such, traders prefer to buy extended bags, as they are more profitable. This encourages farmers and brokers to pack all their potato stock regardless of its quality. In addition, the greater difficulty in handling the large bags and the material used to make them cause further damage.

Market signals rewarding quality are required to encour-age farmers to deliver better production results. There-fore, implementing regulations on marketing standards would be a first step towards better quality and the fair payment of farmers. firstly, having better bag material and a lower bag weight decreases spoilage and damage. furthermore, a fixed bag weight would reduce the ex-ploitation of farmers. also, the content of a smaller bag can be better controlled, which helps improve the quality of produce supplied. To ensure the law is enforced, the process to improve packaging should involve brokers, local traders, wholesalers, retailers and the county au-thorities in order to reach an agreement supported by all actors along the value chain. overall, standards and infrastructure should be established for and awareness raised about marketing potatoes by weight.

Improved conditions for the processing industryKenya has an expanding food processing industry, driven by its growing urban population, changing population structure, new eating habits and increasing tourism. The industry requires potato varieties with better processing qualities to replace the traditional varieties that are assusceptible to bacterial and viral diseases. Processors are calling for the production of suitable varieties to meet their needs for better-quality raw material for pro-cessing.

11IntroductIon

The study will inform Kenyan partners, GIZ and the German food Partnership on how to design appropriate measures and investments to reduce losses in the potato value chain and, in general, how to improve efficiency in value chains.

1.2 Concept of food loss

1.2.1 The study approach although ware potato is the focus of this study on post-harvest losses of potato (PHl study), aspects relating to seed potato use and production at the farm level were also taken into consideration.

This study looks at losses occurring at the pre-harvest, harvest, post-harvest and processing stages, as these are the most relevant in developing countries. following the approach taken in the fao study ‘Global food losses and food Waste (Gustavsson et al. 2011) five system boundaries are distinguished in the food supply chains of vegetable commodities. food loss/waste should be estimated for each of these segments in the chains:

• Pre-harvest: practices affecting the quality of har-vested potatoes.

• Harvest: losses due to mechanical damage during harvesting, as well as crops left in the field due to poor harvesting technologies.

• Post-harvest handling and storage, which includes losses during post-harvest crop sorting and losses during handling, storage and transportation between farms and distribution points including losses caused by packaging (extended bags).

• Processing, which includes losses due to spillage and degradation during industrial processing, such as: when crops being sorted are identified as unsuitable for processing; during washing, peeling, slicing and boiling; during process interruptions; or as a result of accidental spillage.

1.1 Study objective

Potato4 (commonly referred to as Irish potato) is the second most important food crop in Kenya after maize. Potato production in Kenya is expected to grow and could even take the number one spot as food crops like maize become affected by climate change, e.g. due to insufficient rainfall. faced with droughts, farmers are being encouraged by the government to diversify their production. The Ministry of agriculture reported that many farmers are opting to grow potato because it is fast-maturing compared to maize and can be used to bridge the gap during shortages of the staple grain. The number of farmers abandoning maize is not known but, according to the Ministry, the number of potato farmers has grown from 500,000 farmers in 2003 to 800,000 in 2011 ( Thompson Reuters foundation 2011).

In spite of this popularity, several studies have reported major constraints in potato production, such as diseases and pests mainly spread by diseased seed and the lack of crop rotation. other problems are the climate (drought, heavy rains), the costs of inputs for smallholders, seed quality, soil quality and (post-)harvest losses.

The issue of food loss is a highly important factor in ef-forts to combat hunger and raise incomes. However, food loss also represents wasted production resources such as land, water, energy and inputs. These additional envi-ronmental impacts of food loss were not included in this study but were evaluated as part of the GIZ study on ‘The ecological footprint of Cassava and Maize Post-Harvest losses in Nigeria’ (2013),5 which showed that food loss has a significant impact on the environment.

The aim of this study is to improve the availability of data on food loss in the potato value chain in Kenya in order to identify options for the public and private sectors to engage in food loss reduction programmes.

4 The relevance of potatoes (Solanum tuberosum) as a food crop is significant compared to sweet potatoes (Ipomoea batatas), which make up only around 20 per cent of potato production. In 2011, sweet potato cultivation occupied 33,000 hectares and provided a yield of 300,267 tonnes, valued at KeS 3.6 billion (provisional data, HCDa 2012).5 See also GIZ 2013b.

1 Introduction

12 IntroductIon

at the end of the food chain (retail and final consump-tion) is called ‘food waste’ and is the result of retailer and consumer behaviour.

Losses include:

• physical losses – products that are not marketable/consumable, e.g. spoiled, rotten, damaged, green potatoes

• financial losses – lower prices paid due to insufficient quality or loss of value due to bad storage facilities

Critical loss points can occur all along the value chain (Table 1). Given that at certain points not all damaged produce is lost, specifications have been drawn up to distinguish between losses and other uses.

• Distribution, which includes losses and waste in the marketing system – for example, at wholesale markets, supermarkets, retailers and local markets.

• Unlike the fao study, waste occurring during the final consumption stage was not factored into this GIZ PHl study.

1.2.2 definition of loss and critical loss points according to fao, food loss refers to a decrease in edible food mass throughout the part of the supply chain that specifically provides edible food for human consump-tion. Therefore, food destined for human consumption that falls out of the human food chain is considered as food loss or waste. This approach distinguishes between ‘planned’ non-food uses and ‘unplanned’ non-food uses, with the latter being counted as loss. food loss occurring

Financial losses due to low quality of potatoes is a challenge to retailers

13IntroductIon

Stages Critical loss points Specifications of loss according to the Phl study

Production Energy Audit Subsidy Small potatoes are losses if they are not for used for home consumption or for seed.

Capital Cost Subsidy

Harvest Planting and harvesting techniques that leave remnants on the fields (volunteer crops)

Volunteer crops (those left on the field and harvested early the following year) are lost if not used for home consumption.

Harvesting tools cause damage Damaged/cut potatoes: partly for home consumption, with the rest being losses.

Harvest timing – premature harvesting (green potatoes) or harvesting in wet weather

Green potatoes are losses if they are not used for seed.

Packing Quantity and quality of produce packed into extended bags

Size of extended bags

Material of extended bags

Transpor-tation and handling

Weight of extended bags does not allow careful handling

Extended bags become heated (affecting sugar content)

Several stages of loading and unloading prior to reaching the end customer

Losses due to a lack of access roads or poor road conditions

Inadequate means of transport

Storage Lack of storage facilities or simple stores

Unsuitable varieties for storage

Stored products are immature, not disease-free

Market conditions

Wet markets (dirt, contamination, weather) Lower prices due to market oversupply/fluctuations are not losses.

Losses caused by lack of sales are incorporated.

Green potatoes due to sunlight and inadequate packaging material (nylon)

Reduction of prices due to low quality (green/cut potatoes) cause financial losses.

Processing Wrong varieties for processing

Sorting and grading losses Additional labour required to sort/cut potatoes causes financial losses.

Forced to process by-products Potato peel is not a loss.

Table 1: Critical loss points along the potato value chain

14 Methodology

Bomet County was selected to gain an understanding of contract farming from farmers producing potatoes for processors. The production, marketing and handling practices of contract farmers are influenced by contrac-tual arrangements. They plant varieties preferred by processors, allow the crop to fully mature before harvest and, in the main, pack potatoes in standard 110 kg bags.

Meru County farmers have secured a niche market, sup-plying potatoes to most of the markets in the drylands of northern Kenya, such as Marsabit. They also supply markets in Meru and embu Counties. In Meru County, farmers grow potatoes off-season and use irrigation. both irrigating and non-irrigating farmers allow the crop to fully mature before harvesting.

Nakuru County farmers mainly sell in large extended bags. farmers are known not to wait until their crops are fully mature – traders ask farmers to harvest as soon as the crop flowers and farmers also like to harvest early when the prices are high.

Nyandarua County farmers grow potatoes in all sub-counties as their main crop. Contract farming was in-troduced in 2013 but is not progressing well. Nyandarua farmers also tend to harvest potatoes before they are fully mature to take advantage of high prices. Nyandarua and Nakuru Counties are two of the major sources of potatoes marketed in Nakuru, Nairobi and Mombasa. Ware potato growers/farmers all the major potato growing sub-counties in each of the four selected counties were included in the survey. Two sub-counties were selected in bomet (bomet Central and bomet east), three in Nakuru (Molo, Kuresoi, Njoro), four in Nyandarua (Kinangop, Mirangine, Nyandarua North and ol Kalou) and two in Meru (buuri and Meru Central).

The sample size was calculated according to potato producing households and using information from the Seed Potato Sub-sector Master Plan for Kenya 2009-2014 (Kaguongo et al. 2010).

The chosen methodology was based on a five-step approach (details in Table 27, annex 1) following that of the fao (van otterdijk 2012).

1. Screening of food losses including rapid appraisal.2. Survey on food loss assessment. 3. Sampling including load-tracking assessment.4. Data analysis, verification workshop and reporting.5. Synthesis: recommendations and solution finding.

General data for the study were collected from published sources and through key informants, and specific data through questionnaires and group discussions.6 Con-ducting a rapid appraisal to determine specific issues during the preparatory stage proved to be crucial for get-ting a better understanding of the context and for better preparing the survey.

Data was collected during the survey from the major participants along the value chain and on the major sources, causes and also quantities of loss and waste. a randomised survey was used so that statistically reliable quantitative data could be obtained on losses at the defined critical points. Multi-stage sampling was employed so that different regions and types of farmer, broker and trader were included in the survey. The survey results were discussed in a verification workshop, which provided further input to the reporting.

2.1 Sampling of counties and value chain actors

The farmer survey was conducted in four main potato-growing counties in Kenya, namely bomet and Nakuru Counties in the Rift Valley area, Nyandarua County in Central Kenya and Meru County in eastern Kenya (fig-ure 2). These four were purposively selected to provide a representative overview of potato production, post-harvest handling and marketing practices in the country. In bomet and Nyandarua counties contract farming is already underway.

6 The questionnaires are attached in annex 3.

2 Methodology

15Methodology

ed according to the number of potato producing house-holds in the four counties. In bomet, 52 farms (39 individual farmers and 13 contracted farmers) were included; in Nakuru, 69 farms; in Nyandarua, 73 farms (60 individual potato farmers and 13 contracted farmers); and, in Meru, 53 farms were surveyed. The results in the tables and graphs summarised under ‘all’ show the weighted average of the counties.

and in each sub-location administrative units were listed and a sample selected. from each unit, villages were listed and a sample selected, and then the farmers who grow and sell potatoes in each village were listed and a sample selected. on average, a sample of four farmers per village were interviewed. farmers with contract farming arrange-ments were indicated in the questionnaires using the relevant respondent code.

0 100 200 300 km

0 50 100 150 miles

N

©GIZ/Ira Olaleye

1

2

3

5

7

6

8

4

10

9

11

4212

13

14

1516

17

2246

23

47

26

2524

28

2930

3132

33

36

4039

38

3743

3534

41

44

45

27

21

20

1918

1 Turkana 2 Marsabit 3 Samburu 4 Laikipia 5 Isiolo 6 Mandera 7 Mandera 8 Garissa 9 Tana River 10 Lamu 11 Kilifi 12 Kwale 13 Taita-Taveta 14 Kitui 15 Makueni 16 Kajiado 17 Machakos 18 Nairobi 19 Kiambu 20 Murang’a 21 Nyeri 22 Embu 23 Meru 24 Nyandarua

25 Nakuru 26 Narok 27 Bomet 28 Migori 29 Kisii 30 Nyamira 31 Kericho 32 Homa Bay 33 Kisumu 34 Siaya 35 Vihiga 36 Nandi 37 Kakamega 38 Uasin Gishu 39 Elgeyo-Marakwet 40 Baringo 41 West Pokot 42 Mombasa 43 Busia 44 Trans Nzoia 45 Bungoma 46 Kirinyaga 47 Tharaka-Nithi

Counties

Ethiopia

Somalia

South Sudan

Tanzania

Uganda

NAIROBI

Lake Victoria

To collect data from farmers, specific questionnaires were developed (annex 3). The questionnaires were used as an interview guide for the trained enumerators tasked with collecting information from farmers. Using enumerators was important as some of the farmers were not able to read and therefore could not complete the questionnaires without assistance. a sample of 247 randomly selected farmers was interviewed.7 The sample size was calculat-

7 a multi-stage sampling technique was adopted to select the farmers. In each of the counties, all the sub-counties that grow potatoes were listed and then a sample was selected at random. once the sample of sub-counties was obtained, the wards in each sub-county were listed and a sample of these was then selected. from here, locations in the chosen wards were listed and a sample selected. In each location, the sub-locations were listed and a sample selected

Figure 2: Map showing the four counties surveyed

16 Methodology

challenges. on this basis, broker selection was purposive and, as they work in groups, it was decided to organise group discussions. Groups from the sub-counties with the highest potato production and marketing activities were selected (Table 3).

Brokers brokers’ characteristics are the same in each county in terms of how they operate, link up with traders and farmers, get paid for the work they do, and grade and package potatoes, and also in that they face the same

County Brokers group Wholesalers Retailers Supermarkets Restaurants Processors

BOMET 1 4 3 1

MERU 1 4 3 1

NAKURU 1 4 3 1 1

NYANDARUA 1 4 3 1 1

MOMBASA 4 3 3

NAIROBI 16 12 2 3 2

4 63 3 10 3

Table 3: Breakdown of samples of other value chain actors

County Sub-county Villages surveyed number of farmers County sample size

BOMET Bomet Central 9 36 52

Bomet East 4 16

MERU Meru Central 4 17 53

Buuri 9 36

NAKURU Kuresoi 7 28 69

Njoro 5 17

Molo 6 24

NYANDARUA Kinangop 6 24 73

Mirangine 6 24

Nyandarua North 3 12

Ol Kalou 1 13

60 247 247

Table 2: Breakdown of farmer samples 8

8

8 See also Table 26 in annex 1.

17Methodology

2.2 Measurement

With regard to farm size and potato fields, the interview discussions with farmers were based on quarter acres (1,000 m2) but that was later changed to one hectare (10,000 m2). Since farmers use several plots on their farm for potatoes, they were asked to quantify according to the output of their largest potato plot under production. This approach meant farmers could provide more concrete answers but also carried the risk that they would overes-timate output when converting the information to the farm scale. all data were finally converted into quantities per hectare.

Since different measures are used for business transac-tions across the surveyed counties, quantities and prices were difficult to standardise. Various measures for the so-called extended bags are currently in use, and all transactions are calculated in buckets/bags rather than by weight. The weight and content of extended bags are assessed according to the number of buckets required to fill a bag. an average bucket contains 17 kg of potatoes.

There are two key measurement terms associated with extended bags: Kamba determines the size of the bag’s netting top section and Kata determines the additional pieces of cut bags used to extend a standard bag (Table 4). Traders also use different names for different sizes of bag – for example, Gatabuko corresponds with Kata 2 Kamba 4, or Wa kaguku or Bomb correspond with Kata 2 Kamba 5. Mukurinu describes the closed-bag packing method used, with bags ranging in size from 160 to 200 kg.

The observed weight per bag type varied by 7 to 10 kg (Table 5). The bag size keeps on changing from one season to another and from one locality to another depending on the buyer. bags tend to be biggest at peak harvesting seasons and smallest when potatoes are in short supply. It should be noted that, because the survey was taken in the off-season period, the range of packaging types used in the market was fairly limited in many areas.

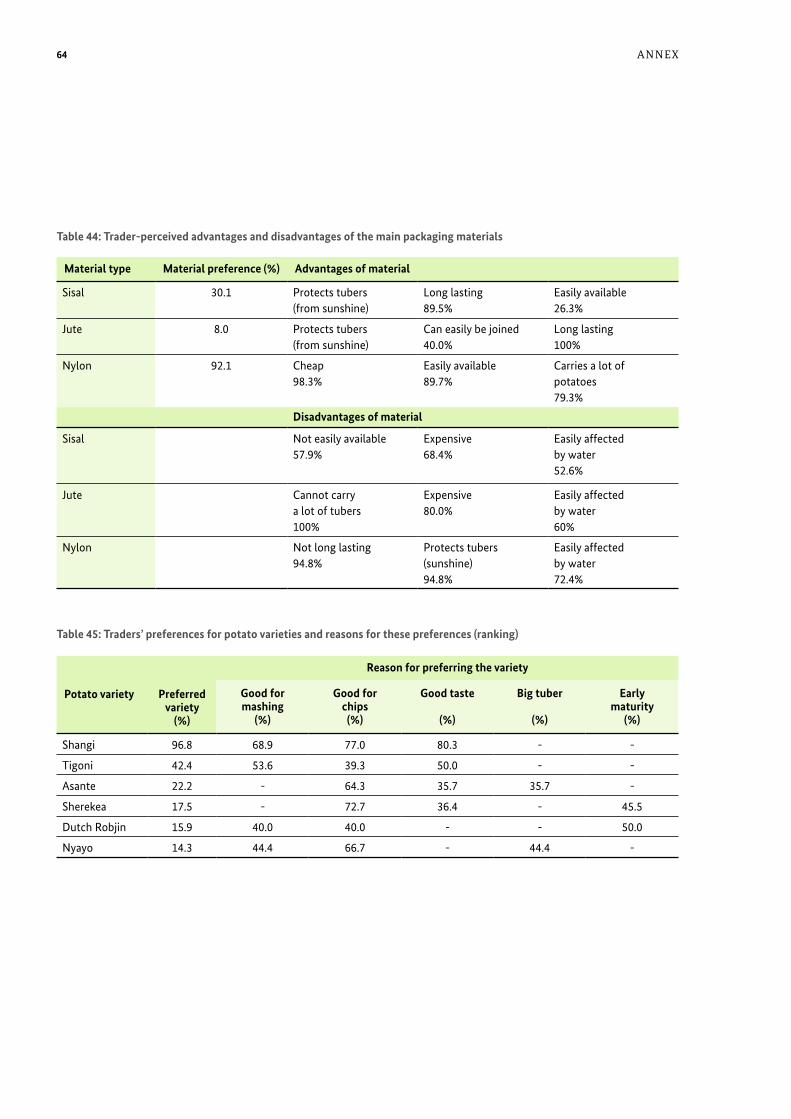

Three types of bag materials are used to pack and market potato, namely jute, sisal and nylon. Potatoes kept for longer than a week in nylon bags spoil.

Wholesalers and retailers Trader samples were selected at random. The potato traders present in each market were listed and three wholesalers and four retailers were randomly selected and interviewed. In Nairobi, four different market places were included: Wakulima, Gikomba, Kangemi and Githurai. a total of 63 traders were interviewed: 27 wholesalers, 27 retailers, and 9 traders who conducted both wholesale and retail operations.

SupermarketsSupermarkets are mainly located in the major urban cen-tres. In many supermarkets, purchasing is centralised and branches receive weekly goods deliveries. The pattern of purchasing agricultural produce is similar for most of the supermarkets, with produce being supplied centrally by a contracted supplier on a weekly basis. Purposive sampling was used to select the three major supermarket chains – Nakumatt, Uchumi and Tuskeys – for interviews with branch supervisors. Data were collected from one branch in Nairobi and one in Nakuru town.

ProcessorsPotato processors who make crisps and chips are few in Kenya. The main processors are the Nairobi-based com-panies Deepa Industries, Norda, Pioneer and Propack, and also Midlands, located in Nyandarua county. Pur-posive sampling was used to select three processors for interview.

Restaurants Restaurants were sampled randomly from the high streets of selected towns.9 one restaurant was inter-viewed in each main town of the four study counties; in Nairobi and Mombasa, the biggest potato markets in Kenya, three restaurants were selected in each city.

9 Sample selection involved picking one restaurant located in one of the three main streets of the principal towns of each of the four study counties. In Nairobi and Mombasa three restaurants were selected for each city.

18 Methodology

2.3 load tracking

bag size, weight and material are expected to have a significant impact on produce quality and losses. To measure the impact of extended bags on the quality of the potatoes and, thus, on losses, three bags were traced along the supply chain.

Starting on a farm in Kanjuiri village in ol Kalou Sub-County, Nyandarua County, the packing of bags was observed. following this, packed bags were opened to analyse their content. The sorting was performed on the basis of selecting and weighing green, damaged/cut and rotten potatoes. bucket-size samples were taken on the farm to determine the levels of quality and loss accord-ing to the above-mentioned definition.

Table 4: Traditional potato measures

Packaging types

Non-extended bag Bucket Kamba 6 Kata 210 Mukurinu

name of packaging Size Average weight

Bucket 1 bucket 17 kg

Non-extended bag 7 buckets 119 kg

Kata 2 Kamba 4 11 buckets 180-187 kg

Kata 2 Kamba 5 12 buckets 195-204 kg

Mukurinu Different sizes 160-200 kg

Table 5: Traditional measures and their metric conversions

The identified bags (of Kata 2 Kamba 5 size) were traced from their place of origin to their destination market in Nairobi. at the retail market level (the produce’s final destination and location where bags are opened and re-packed), each of the bags were weighed and then opened and the various categories of potato in each bag were separated out and weighed. To get a broader understand-ing on the losses caused by the bags, interviews with re-tailers included questions related to seasonal effects. 10

10 Kamba 6 is the size of the netting top section the bag. Kata 2 indicates the number of additional cut bag pieces used for the bag extension panels; in this case, it means two pieces of cut nylon bag are used with half a nylon bag for the top section.

19POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

smallholders dedicating 0.2 to 0.4 hectares to potato production, while approximately 17 per cent of potato plots belong to larger-scale farmers dedicating 2 to 10 hectares to the crop (Janssens et al. 2013). average production in Kenya is estimated at 7 to 10 tonnes per hectare (Muthoni et al. 2011), compared to a global average yield of 17 tonnes per hectare (faoSTaT 2011). Kenyan farmers achieve up to two harvests per year.

The total production area has increased in recent years and is estimated to have reached 150,000 to 160,000 hectares to date (Table 6).

3.1 Background

Potato is the second most important staple food in Kenya after maize. The most favourable climatic conditions for potato cultivation in Kenya are found in areas at altitudes between 1,500 and 3,000 metres above sea level, where the country’s main staple food, maize, has no compara-tive advantage. at this altitude, potatoes grow faster than maize and produce more energy and protein per hectare per day. Potato production areas are found mainly in the highlands of the Central, eastern and Rift Valley regions and on the slopes of Mount Kenya. also, other regions like Mount elgon (bungoma County) in Western Kenya are prominent production areas (see figure 2).

Potatoes are grown by up to 800,000 farmers, who are mainly smallholders.11 It is estimated that 83 per cent of the land under potato cultivation belongs to

11 The exact number is not known. ‘The National Root and Tuber Crops Policy’ published by the Ministry of agriculture in 2010 estimates the number of farmers to be 790,000. In 2011, the Ministry reported 800,000 farmers.

3 Potato value chain in Kenya – survey results

County Area in ha 2010 2011 2012

Meru 17,463 12,500 18,092

Nyandarua 28,688 30,577 27,520

Nakuru 16,053 16,804 22,566

Bomet 2,900 3,680 2,987

Elgeyo Marakwet 8,311 15,097 20,992

Narok 6,836 7,808 6,292

Kiambu 11,271 10,092 18,769

Nyeri 8,067 6,404 7,821

Bungoma 5,113 6,051 5,321

Estimated total area under potato production 150,000-160,000 haSource: HCDa 2012, Kaguongo et al. 2013, and author’s own estimations.

Table 6: Main potato producing counties and the total area under potato production in Kenya

20 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

over KeS 40 billion or eUR 339 million (1 per cent) to the national economy (Kasina & Nderitu 2010). It therefore follows that potato is an important economic crop.

In addition to there being up to 800,000 potato farmers, another 2.5 million people work in the potato value chain (Kaguongo et al. 2013). Potato is ideal as a food security crop as it has a short season and provides food within just 2.5 to 3 months, especially when planting fast-maturing varieties. at the same time, farmers are assured of a harvest as the crop is drought resistant and will provide some produce, even with little rain.

The ware potato value chain is structured rather simply (figure 3) given that most of the potatoes marketed are bought and consumed as fresh produce by end-consumers. farmers sell their produce mostly via brokers to local traders. local traders take the produce to the wholesale markets where, again, brokers organise sales on behalf of the traders. only farmers engaged in contract farming for the processing industry sell directly to their custom-ers. Processing accounts for only around 9 per cent of marketed produce,12 although a trend towards increasing demand for processed products has been observed. average per capita consumption is estimated at 30 kg and is expected to rise due to increases in potato consumption by urban populations (fao 2013) and rapid population growth. Present estimates indicate that around 1 to 1.5 million tonnes of potatoes are marketed in Kenya per season.13 Currently, potatoes contribute

12 according to NPCK estimates.13 In 2012, Kenya had a population of 41 million and this is expected to rise to 50 million by 2020 (Zulu et al. 2012).

The common packing of potatoes in heavy bags causes damages

21POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

The education levels of ware potato growers correspond with their age (Table 28 in annex 2). bomet County, where potato production often involves contract farming for processors, there are more young farmers. farmers in this County also had the highest levels of literacy, with 73.1 per cent having completed secondary education and college. Compare this with Nakuru County, for example, where farmers had a low literacy level and only 49.3 per cent had completed secondary and college education. a comparison of male and female respondents showed higher illiteracy among women (10.3 per cent to 2.4 per cent of men) and consequently a lower education level (Table 29 in annex 2).

age and education is known to have an impact on openness to change and innovation and on the com-mercialisation of agricultural production. farmers with higher levels of education tend to be more efficient in production. better performance by more educated farm-ers may be attributed to the fact that education gives the farmers the ability to perceive, interpret and respond to

3.2 Potato production

3.2.1 Ware potato growersThe characteristics of the potato farmer sample (Table 28 in annex 2) indicate the dominance of elder male farm-ers heading a family of five to six persons (68 per cent of the respondents were men, 32 per cent women). That said, the sub-sector is known for being gender-balanced. GIZ’s PSDa14 programme conducted labour studies in selected agriculture sub-sectors and the study on the potato sub-sector showed that women (49 per cent) and men (51 per cent) are nearly equally involved in the op-erations.15 Some operations are heavy-duty in nature, meaning they are more likely to be performed by men (e.g., the handling of extended bags); conversely, women dominate the retail business.

14 http://www.gtzpsda.co.ke/index.php?option=com_content&view=article&id=18&Itemid=5515 This runs in contrast to sweet potato production where, according to the GIZ PSDa study, women perform 75 per cent of the production activities.

Figure 3: Ware Potato Value Chain

StageConsump-

tion

Operators

End- users

House-holds

Farmers

Brokers Brokers Retailers

Contract farmers

Local traders

Industrial processors

Whole- salers

Restaurants

Super- market

on-farm production

Packaging/transport

Processing Wholesale/retail trade

22 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

new information and improved technology such as ferti-lisers, pesticides and planting materials much faster than their counterpartss (Nyagaka et al. 2009).

land holdings and production methodsSmallholders with farm sizes averaging less than 2 hec-tares dominate the potato sub-sector in Kenya. land ownership is predominantly freehold. The average farm size of surveyed potato farmers was 1.6 hectares (Table 7), while the average area of land given over to potato growing was 0.6 hectares, or 35.4 per cent of their overall farmland. Nyandarua County had the largest average land holding (1.9 hectares), with 0.7 hectares being dedi-cated to potato growing. Conversely, bomet County had the smallest average land holding (1.4 hectares) and also the smallest area dedicated to potato growing (0.3 hectares).

Putting together a serious estimate of harvested and marketed potato in Kenya is difficult as data on produc-tion areas and yields are not systematically collected. also, bag sizes used by traders vary from one area to an-other. Moalf and the Horticultural Crops Development authority (HCDa) publish annual production data and, in 2012, HCDa calculated a production of 2.53 million tonnes on a 143,000-hectare area. The Kenyan agricul-tural Research Institute (KaRI) estimates smallholder yields to be in the region of 7 to 10 tonnes per hectare,

equivalent to 1 to 1.5 million tonnes per season. The farmers interviewed for the study looking at main pro-duction areas harvest on average 13.5 tonnes per hectare per season, which is higher than the national average.

Most farmers produce two potato crops a year because of the bimodal rainfall in most potato growing areas. The long rainy season lasts from March/april to June/July, while the short rainy season lasts from october to December (Table 34 in annex 2). among the surveyed counties, only farmers from Meru (79.2 per cent) practise substantial off-season farming using irrigation, and these off-season crops secure higher prices (Table 7).

The majority of surveyed potato farmers (95.5 per cent) indicate that they practise crop rotation. However, the effectiveness of this crop rotation could not be deter-mined as farmers did not report their rotation schedule. It is known that farmers rotate crops with, for example, maize, beans or cabbages; however, such rotations are not designed for the control of pests and diseases. CIP reported that 21 per cent of farmers grow potatoes continuously on the same plot and only one out of two farmers practises some form of rotation (Kaguongo et al. 2008).

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Potato yield (kg/ha) 13,243.8 11,888.6 14,950.3 13,629.4 13,551.6

Quantities eaten per farmer family (kg/ha) 1,295.6 2,032.7 1,326.8 1,041.8 1,394.9

Land holding in ha

Total farm size 1.4 1.5 1.6 1.9 1.6

Land for potato production 0.3 0.4 0.7 0.7 0.6

Farming practices (%)

Potato production irrigated 0.0 79.2 8.7 2.7 20.2

Farmer practising crop rotation 100 100 92.8 91.7 95.5

Table 7: land holdings and farming practices

23POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

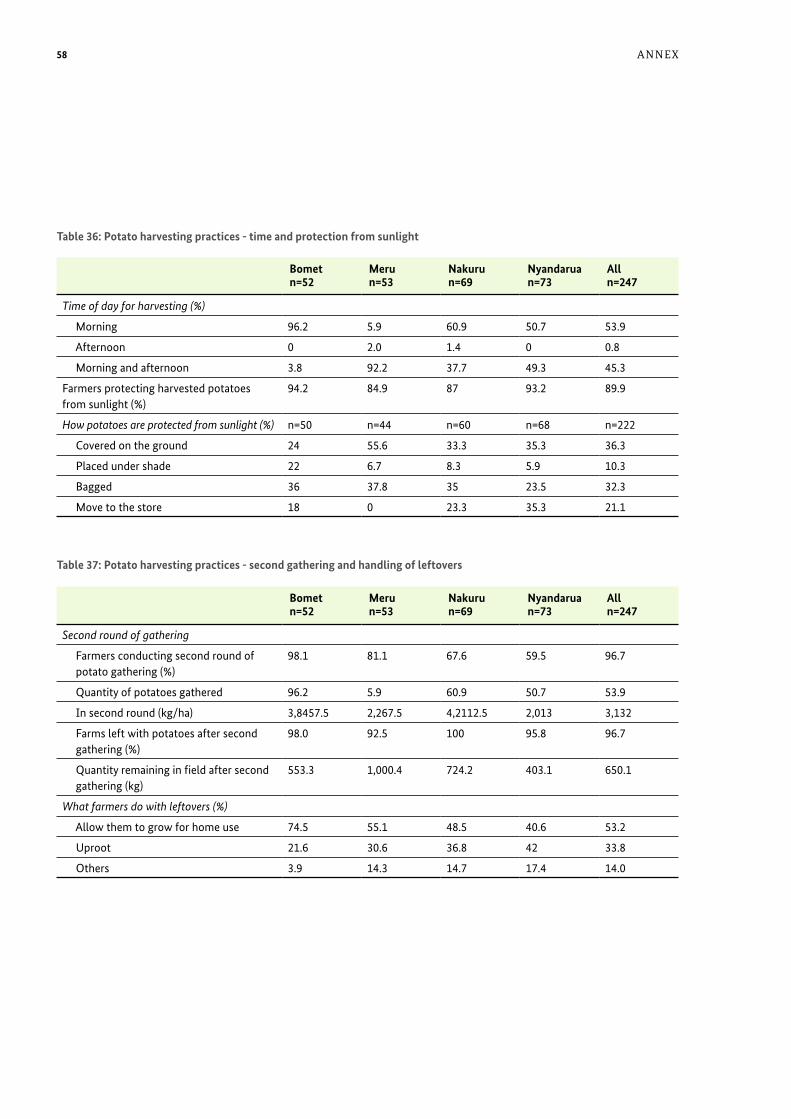

Kenya’s soil-borne diseases,16 limited pest management and low soil fertility mean current production practices are not sustainable. This situation is further aggravated by the remnants left in the field after harvest that pro-duce so-called volunteer plants in the next season. even though crops are rotated, the volunteer plants will carry diseases from one season into the next. The PHl survey showed that 97 per cent of interviewed farmers report leaving volunteer plants in the field, using them mostly for home consumption. The average quantities remain-ing in the field are estimated at 0.65 tonnes per hectare, Given surveyed farmers report an average yield of 13.5 tonnes per hectare, we can deduce that at least 5 per cent of the potato crop is left in the ground. a total of 53.2 per cent of farmers allow the volunteer plants to grow for home use, while others uproot the remnants (Table 37 in annex 2).

16 a recent survey showed that bacterial wilt was the most prevalent disease, affecting 77 per cent of potato farms, followed by late blight affecting 67 per cent and viral diseases affecting 12 per cent (Kaguongo et al. 2014). See also Janssens et al. 2013.

Farmers’ seed systemMore than 60 potato varieties are grown in Kenya, but relatively few are widely distributed. The dominance of certain varieties shifts over time. Today, Shangi17 (a farmers’ variety, shown in Photograph 1) and Tigoni (an officially released variety) are the main varieties be-cause of market preferences (Table 45 in annex 2). Shangi has a very short cooking time, saving energy and cutting costs, and so is preferred by low-income households. al-though most varieties in Kenya have white skin, there is preference in some regions for red skin varieties.

17 Shangi is also called ‘Zangi’ or ‘Cangi’ in other publications.

Potato varieties grown in each county (% within the county)

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Shangi 30.8 49.1 98.5 100 74.0

Asante 0.0 79.2 5.9 6.8 20.7

Dutch Robjin 96.2 0.0 2.9 0.0 21.1

Tigoni 3.8 0.0 17.6 38.4 17.1

Sherekea 0.0 50.9 5.9 8.2 15.0

Kenya Karibu 7.7 0.0 14.7 23.3 12.6

Tigoni Red 0.0 52.8 0.0 0.0 11.4

Désirée 23.1 3.8 4.4 11 10.2

Table 8: Potato varieties grown

Photograph 1: The Shangi potato variety

24 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

The farmer seed system currently dominates the sub-sector. Due to limited seed production, the lack of attrac-tive varieties and an insufficient distribution network, certified seed18 – including clean seed and positive select-ed seed – only meets around 5 per cent of the national demand for seed potato, according to NPCK. The limited availability and use of quality (and certified) seed potato is a key barrier to increasing productivity in Kenya’s potato sector. Given farmers tend to practise short crop rotations, seed potato quality is an important factor in improving the sustainability of production. Clean seeds have the greatest impact on yields followed by irrigation, fungicides and fertilisers. However, clean seeds have the lowest adoption rate (Wang’ombe & van Dijk 2013). of the farmers interviewed, most (77.7 per cent) used farm-ers’ seed, with the main sources being their own harvest or seed from neighbouring farms (Table 33 in annex 2). only 6.9 per cent of farmers use certified seed purchased from certified seed suppliers (Graph 3 in the annex 2).

only 42 per cent of farmers renewed seed regularly (Graph 4 in annex 2). The seed renewal rate was higher in bomet and Meru where more than 60 per cent of farmers renewed seed after one to three seasons. Conversely, over 50 per cent of farmers in Nyandarua and Nakuru Coun-ties never renewed their seed. farmers from Meru and bomet showed the highest rate of certified seed applica-tion (30 per cent). Note that in bomet farmers are much more likely to be involved in producing for the process-

18 Clean seed: Multiplied at farm level, clean seed originates from certified or basic seed and its production follows guidelines laid down in farmer training programmes delivered by organisations like Moalf, KaRI or GIZ. Most production guidelines used in the production of certified seed are also used to produce clean seed – the only differ-ence is that the sample testing and supervision by KePHIS is lacking. Negative selection is used to remove diseased and weak plants.Positively selected seeds: Positively selected seeds are produced from ordinary or farmer-saved seeds through a process of selection undertaken by farmers who know how to select and manage good seed. However, Kenyan law stipulates that certified seed developed in accordance with strict production guidelines and inspected by the Kenya Plant Health Inspectorate Service (KePHIS) are the only seeds that can be traded. all other seeds – including positively selected seeds, clean seeds and farmers’ own seeds – are considered to be non-tradable by law (Kaguongo, W. et al. 2014).

ing industry and industrial clients generally provide the required seed material.

on-farm seed multiplication is further supported by varieties like Shangi; however, the variety is not certi-fied and clean Shangi seed is not available. So, despite its advantages of higher yields and fast growth, the variety is easily affected by disease. Shangi germinates rapidly after harvest, meaning seed tubers can be planted out within just a few weeks. This short dormancy means the seed from one season can be planted in the next growing sea-son. as ware potato, the variety is immediately sold after harvest, given it is not suitable for storage.

harvesting practicesa total of 64 per cent of the farmers reported that they do not harvest potatoes when it is raining. However, those who do harvest during the rains experience damage and loss of up to 1,469 kg/ha, mostly caused by the potatoes rotting. When converted to the average of surveyed farmers, these losses stand at 344.2 kg/ha (Table 9). farm-ers tend to harvest during the rains in order to reach the market early and fetch higher prices. also, traders force farmers to harvest early. a comparison of farmers from bomet and Nyandarua engaged in contract farming (Table 13) clearly indicates the impact of market forces on harvesting during the rains – e.g. contracted farmers from bomet report 90 per cent less rain-induced damage than non-contracted farmers in the county. Still, weath-er conditions also play a role, such as when unexpected rains occur during a harvest. annual rainfall patterns are becoming less easy to predict, with both drought and unseasonable rainfalls affecting production.

25POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

Meru County was the only location where sticks were reported to be used (by 41.5 per cent); and, in Nyandarua, 97.2 per cent of farmers use a fork jembe.

The fork jembe is the main harvesting tool for farmers although most farmers (87.0 per cent) consider that the tool damages (cuts and bruises) potatoes during harvest. The damage caused by using fork jembes was estimated at 679 kg/ha. That said, other tools such as the hoe or stick damage crops even more.

Most farmers (85.4 per cent) used casual labour for harvesting potatoes and only 12.1 per cent also employ family members as part of their workforce (Table 38 in annex 2). an important reason for this relates to how work is paid for: work provided by family members is usually not paid for and this makes them less willing to work on the family farm. Most farmers (80.8 per cent) considered harvesting operations to be the main cause of potato damage during harvest. The amount of damage caused by this type of labour was estimated at 488.2 kg/ha. However, as shown in Table 9, farmers experience most of their losses during production, e.g. through disease and other issues that are not reflected in this study.

Most small-scale farmers cannot afford motorised mech-anisation (no cash to invest, farm acreage and plots are too small) and do most of their work manually (planting, fertilising, harvesting). The most commonly used tool for harvesting potatoes is the fork jembe (52.8 per cent), followed by oxen (23.2 per cent). However, the tools used varied from one county to another (Table 38 in annex 2): in bomet County, the majority (92.3 per cent) use oxen;

Photograph 2: Fork jembe

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Potato yield (kg/ha) 13,243.8 11,888.6 14,950.3 13,629.4 13,551.6

Farmers experiencing losses (%) 94.2 100.0 97.1 100.0 98.0

Stages at which losses occur (%)

Production 77.6 81.1 74.6 55.6 71.0

Harvesting 53.1 56.6 44.8 45.8 49.4

Sales 28.6 39.6 26.9 36.1 32.8

Storage 8.2 15.1 10.4 15.3 12.4

Damage caused during harvest

Harvesting in rain (kg/ha) 179.9 185.1 633.6 261.5 344.2

Harvesting tools (kg/ha) 430.3 525.1 759.2 528.7 568.2

Harvesting labour (kg/ha) 213.1 537.5 631.0 514.7 488.2

Table 9: Farmers who experience losses during production and harvest

26 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

Post-harvesting practicesMost farmers reported sorting and grading potatoes at harvest. The majority of farmers (60.0 per cent) graded by size, with 85 per cent of their crop being either medium- or large-size potatoes (Table 10). Sorting and grading mainly involved separating out small potatoes for seed. after deducting potatoes for home use, medium and large tubers end up being bagged for sale along with cut, bruised and green tubers.

as there are usually only a few months between harvests, it is not common practice to store ware potatoes in Kenya, although smaller quantities may be stored on farms. Those operating modern storage facilities are the larger processors or larger producers of seed potato. The major-ity of the surveyed farmers (92.2 per cent) stored some potatoes after harvest, but most farmers (60.4 per cent) stored potato for seed (Table 11).

26

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Farmers sorting and grading potatoes (%) 94.1 100 98.5 100 98.4

Stage of sorting and grading (%)

During harvesting 85.4 94.3 86.4 90.1 89.1

Just before storing 10.4 5.7 10.6 4.2 7.6

When selling 4.2 0 3 5.6 3.4

Sorting and grading potatoes of each category obtained from a hectare (%)

Small 11.0 8.4 9.5 6.2 8.4

Medium and large 85.1 84.3 81.5 86.3 84.9

Cut and bruised 3.7 5.3 7.5 4.9 5.2

Greening tubers 0.2 1.6 1.0 2.0 1.1

Off-type variety 0 0.4 0.5 0.6 0.4

Table 10: Sorting and grading practices

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Farmers who store potatoes (%) 94.1 96.2 91.0 88.9 92.2

Where the farmer stores potatoes (%) n=51 n=48 n=61 n=64 n=224

Dark store 27.1 64.7 22.0 7.9 29.0

Store allowing light 47.9 15.7 22.8 49.2 35.7

Store with a wooden floor 18.8 2.0 15.3 20.6 14.5

Others 6.2 17.6 33.9 22.3 20.8

Why the farmer stores potatoes (%)

To wait for better prices 9.1 55.1 1.7 10.9 18.0

Home consumption 2.3 30.6 16.7 32.8 21.7

For seed 88.6 14.3 81.7 56.2 60.4

Table 11: Potato storage practices

27POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

a survey carried out as part of the Seed Potato Sub- sector Masterplan (Kaguongo et al. 2010) showed that although more than 90 per cent of interviewed farmers store seeds, only 4 per cent had been trained in seed storage and suitable technologies such as diffused light stores (DlS).19

only 18 per cent of the farmers surveyed stored potatoes in order to wait for better market prices, although the majority of farmers (55.1 per cent) in Meru County stored stocks for reasons of price (Table 11). farmers in Meru in particular set aside potatoes from rain-fed production to wait for better prices. off-season production produced under irrigation secures high prices so, in the main,

19 In diffused light stores (DlS), seed tubers are stored on trays or racks and the stores are shaded and aerated. This type of store provides excellent conditions for seed tubers, but it is not widely used (Photograph 3).

farmers sell directly after harvest. Meru farmers who stored potatoes reported, however, that this year’s prices were not significantly higher – the difference being just KeS 1.3 per kg. It is possible that, in other years, storing ware potatoes will prove more financially rewarding.

The majority of farmers (83.9 per cent) reported expe-riencing losses during potato storage, mainly caused by rotten potatoes (82.5 per cent) affected by disease or damage (Table 12). on average, 119 kg/ha (0.8 per cent of the production) were lost in storage. The highest such losses were reported in Meru where larger quantities of ware potatoes are stored.

27

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Farmers experiencing losses (%) 80.4 84.3 84.2 85.7 83.9

Causes of damage during storage

Pests and diseases (%) 40.5 10.5 10.4 9.3 16.4

Rotting (%) 59.5 84.2 89.6 90.7 82.5

Others (frost, rodents, etc.) (%) 32.7 5.7 24.6 50.0 29.7

Losses during storage (kg/ha) 122.8 414.0 105.6 62.6 119.0

Table 12: losses in storage

Photograph 3: Seed potato storage - diffused light store

28 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

Bomet n=52

Meru n=53

nakuru n=69

nyandarua n=73

All n=247

Packers of bags for selling (%)

Broker 49.0 88.7 76.8 91.8 78.0

Trader 27.5 7.5 11.6 0.0 10.6

Farmer 19.6 3.8 8.7 4.1 8.5

Workers 3.9 0.0 2.9 4.1 2.8

Consumer 3.8 0.0 1.4 0.0 1.2

To whom the farmer sells potatoes (%)

Local trader 63.5 96.2 56.5 60.3 67.6

Wholesaler 3.8 15.4 40.6 37.0 26.3

Processor 17.8 0.0 0.0 0.0

Table 13: Farmers’ transport and marketing practices

When selling potatoes, bags were mainly packed by brokers (78 per cent) as the majority of farmers (67.6 per cent) sold their potatoes via brokers to local traders (Ta-ble 13). farmers from bomet selling their potatoes to pro-cessors (17.8 per cent) also take on the packing of their produce (19.6 per cent). In the 2013 season, bomet farm-

ers remained the only group in the survey cohort selling to the processing industry. farmers from Nyandarua were contracted to produce for the processing industry but this arrangement did not work out and the produce was eventually sold to traders (see chapter 3.2.2).

3.2.2 Comparison between contracted and non- contracted farmersa comparison of ware potato growers operating as con-tract farmers in bomet and Nyandarua County is set out in Table 14. as the results show, improved conditions under contract farming end up delivering better produc-tion performance, in particular when supported with the provision of inputs like fertiliser or seed. However, challenges are arising in the cooperations between farm-ers and processors, especially regarding fulfilment of the contract. The costs of the inputs provided are based on market prices but, sometimes, the pricing and quality of these inputs is questioned: farmers accuse processors of calculating higher than market prices or the quality of seed is called into question. In return, processors com-plain about farmers breaching their contracts despite the fact that they have provided them with inputs. also, unmet quality standards are an issue needing discussion, given that farmers generally do not receive any training on improved agricultural practices.

farmers from bomet work closely with potato crisp manufacturers, hence the prevalence of the Dutch Robjin variety, which is preferred by the processing industry and grown by both contracted and non-contracted farmers in bomet County. Non-contracted farmers in bomet sell Dutch Robjin to the fresh produce markets as there is also demand for the variety in retail markets. a notable difference between the two kinds of farmer is that con-tracted farmers use certified seed more (23.1 per cent) than non-contracted farmers (10.3 per cent).

The quantities harvested per hectare were 14,945.9 kg for contracted farmers and 12,572.6 kg for non-contracted farmers, or 16 per cent less. The high yield for contracted farmers may be attributed to the use of high quality seed and improved production practices. The quantity of damaged potatoes per hectare for contracted farmers was 383 kg, whereas non-contracted farmers reported damages of 842 kg. Nevertheless, bomet farmers’ losses come in nearly 50 per cent lower than all other surveyed

29POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

Bomet contracted n=13

Bomet non-contracted n=39

nyandarua contracted n=13

nyandarua non-contracted n=60

Main varieties grown (%)

Shangi 15.4 35.9 100.0 100.0

Tigoni 0.0 5.1 100.0 26.2

Dutch Robjin 100.0 94.9 - -

Kenya Karibu - - 75.0 13.1

Désirée 15.4 25.6 50.0 3.3

Type of seed used (%)

Farmers' seed 61.5 71.4 88.3 91.8

Positively selected seed 15.4 17.9 0.0 3.3

‘Clean’ seed 0.0 0.0 8.3 4.9

Certified seed 23.1 10.3 8.3 0.0

Harvest

Quantity harvested (kg/ha) 14,945.9 12,572.6 16,877.6 12,356.4

Quantity damaged (kg/ha) 383.1 842.3 1,618.8 1,202.4

by harvesting tool (kg/ha) 306.0 416.4 791.1 443.3

by harvesting in rain (kg/ha) 25.8 265.4 142.1 297.3

by harvest workforce (kg/ha) 51.3 160.5 685.6 461.8

Percentage of damaged harvested potatoes 1.9 6.7 9.6 9.7

Table 14: Contracted and non-contracted farmers in Bomet and nyandarua Counties

farmers. The difference can be explained by the varieties selected (mainly Dutch Robjin) as well as the handling of produce. In all the categories of harvest-related damage, the quantities reported in bomet were significantly lower than those of other counties (Table 9).

In Nyandarua, the quantity harvested per hectare was 16,877.6 kg for contracted farmers and 12,356.4 kg for non-contracted farmers. The high yield for contracted farmers may be attributed to better crop husbandry. However, different to the situation in bomet, contracted farmers in Nyandarua had high quantities of damaged

potatoes per hectare (1,618.8 kg/ha) in comparison to non-contracted farmers (1,202.4 kg/ha). It has been reported that the losses were the result of the contrac-tor’s strict sorting requirements. farmers here are new to contract farming and do not have enough experience in reducing damage or unwanted potatoes. as such, they produced more waste compared to non-contracted farmers. The introduction of unfamiliar standards led to a high proportion of rejects by the contracting processor and so the farmers ended up selling the bulk of the har-vest to traders.

30 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

During the wet season, brokers organise tractors to transport potatoes from the field to the road. at other times, potatoes are transported using donkey or ox carts or loaded onto donkeys. lorries/trucks or pickups are also used (Table 40 in annex 2). brokers normally load potatoes onto the truck. Depending on its size, a single bag is carried by three to six people or is loaded on the shoulders of one broker who subsequently throws the bag into a wheelbarrow.

Photograph 4: Brokers on site filling extended bags

Photograph 5: loading and handling of extended bags at nairobi’s Wakulima Market

3.3 Potato marketing

3.3.1 Brokers at the farm levelbrokers act as intermediaries between farmers and local traders and keep in close contact with farmers to stay abreast of the quantities and varieties they have available. brokers work in groups and each group can deal with 30 to 70 farmers. brokers get a fixed fee per bag from local traders.

brokers tend always to be male as the work involves lots of heavy lifting. brokers, contrary to the perception that they exploit farmers, work under very difficult condi-tions. They reported that lifting the heavy bags damages their health and that some have been injured when load-ing and offloading extended bags. It was observed that many of them appeared in poor health.

one of the challenges brokers come up against is the failure to implement standards in potato marketing. as intermediaries between farmers and traders, they have to convince farmers to accept extended bags for sale. Imple-mentation of standard bags would facilitate their busi-ness operations. When brokers pack, they try to avoid including bad quality potatoes in the bags; however, they do not grade or buy potatoes by grade.

31POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

from here, the produce is usually then distributed to other towns or markets or even to neighbouring coun-tries. There is no storage at the wholesale level and the produce is distributed and sold within a short period. Traders selling at Wakulima in Nairobi cooperate with brokers based at the wholesale markets. The brokers wait for the trucks to arrive at the market and inform their customers about the expected load. all transactions are in the hands of the wholesale market brokers and, when a transaction is agreed, the trader is provided with a receipt of the purchased produce, quantities and price. brokers at Wakulima Market earn commission of around KeS 40-50 (eUR 0.35-0.40) on each bag.

Currently, the main wholesale market in Nairobi (photo-graphs taken in December 2013) is highly congested and spills over into the surrounding areas, where conditions are very unhygienic. The same is true for other markets around the country, yet, in recent years, only a few mar-ket places have benefited from refurbishment.

In rural areas, road infrastructure is very poor and bro-kers have difficulty transporting potatoes from farms. The poor roads cause delays in collecting purchased stocks, which can result in the potatoes going bad. This kind of loss is transferred to the brokers, as the trader may not take the spoilt stock. brokers consider that the main dam-age to potatoes is caused by extended bag sizes but also acknowledge that delayed collection leads to damaged stock. brokers estimate that in each 110 kg standard bag an average of 5 kg of stock will be damaged/lost.

3.3.2 Wholesale and retail tradeDistances from farms to sales points range from 15 km (i.e., a market local to producing areas) to up to 500 km (i.e., where Mombasa or Kampala is the furthest point). Traders buying in the surveyed counties come from Wakulima Market in Nairobi, Kongowea Market in Mombasa or Northern Tanzania. Wakulima Market in Nairobi is the largest terminal market and is estimated to handle over 50 per cent of all potatoes traded in Kenya.

Photograph 6: Conditions at nairobi‘s Wakulima wholesale market

32 POTATO VALUE CHAIN IN KENYA – SURVEY RESULTS

because most of the markets have sections catering to both sectors. Wakulima Market in Nairobi also includes a retail section located in the old covered-market building (Table 42 in annex 2).

The packaging bought also depends on the season and availability of produce. a total of 25 per cent of whole-salers bought standard bags with a Mukurinu closure. These are normally cheaper because the bag is totally closed up, meaning the content is not visible (Table 43 in annex 2). Nylon bags are most commonly purchased and their average weight totals 173 kg. Nylon bags are cheap and strong enough to carry larger quantities compared to jute bags (Table 44 in annex 2).