Embed Size (px)

Citation preview

Perspectives 2016

Adolfo Fontes – October 2015

Pork Global Market

Pork Global Market Perspectives

Pork market overview

Latin American Potential

Brazilian Pork industry

Challenges

Conclusions

Rabobank is a premier bank to the leading companies across the food, beverage and agribusiness industry

Leading Global Bank

Relationship-Focused

Financial solutions to more than 10 million clients in 46 countries

• Rabobank International global presence

• Rabobank Netherlands

• Rabobank International

Over 100 years of banking history rooted in the Food & Agri sector

Safest privately-owned bank, more than USD1 trillion in Assets

Wholesale Banking

F&A Research

Corporate Banking Global Financial Markets

Mergers & Acquisitions

Focus on Food & Agribusiness

International Retail Banking

Professional Products/ AF

Asset management

Mortgage

Leasing

Commercial Real Estate Insurance

Corporates

All industries

Corporate and Retail banking

Rabobank global research team

Page 4

World population

Source: US Department of Commerce, 2014

Bil

hõ

es

2014 7.2 More food will be needed

in the first half of this

century, than it was

consumed in the last

7,000 years

Globally, poultry is the fastest growing meat and should replace pork as the most consumed animal protein by 2022

• Global consumption of meat [ MM tons]

• Note 1: Compound annual growth rate • Source: Rabobank, OECD, FAO

+1,4%

CAGR¹

2013-2022

+1,3%

+1,9%

+1,5%

Pork

Poultry

Sheep

Beef

2022p

+1,6%

+2,6%

346

76 (22,0%)

16 (4,6%)

128 (37,0%)

126 (36,4%)

2013

301

14 (4,7%)

108 (35,9%)

112 (37,2%)

67 (22,3%)

2005

254

12 (4,7%)

83 (32,7%)

98 (38,6%)

61 (24,0%)

1995

189

9 (4,8%)

46 (24,3%)

78 (41,3%)

56 (29,6%)

FAO Projection (2023) for Latin America*

Page 7 Source: OECD, FAO, 2015

(1,000 t.)

Latin America and Caribbean Production

24.03627.113

29.880

7.384

8.060

8.833

19.760

20.479

18.025

59.192

54.933

2019 2024 2014

49.445

Pigmeat Beef Poultry CARG 2014-24

1,3%

1,8%

2,2%

*and Caribbean

Meat per capita consumption per region per year

28 3219

15

49

28 36

2237

34

13

33 1428

1612216 126 7

World

41

10

Oceania

84

Europe

68

Asia

31

10 5

South America

81

Central America and Caribbean

53

North America

110

Africa

15

Pork

Poultry

Beef

3920

34 28

20

1745

38

51

31

10

13

39 60

35

16

15140 9

13

Argentina

107

Brazil

98

South Korea

64

Japan

50

India

4

2 1

China

57 5

Mexico

62

USA

114

Fonte: USDA, FAO, Rabobank

• Per capita consumption (kg/year) – 2013

Per capita consumption (kg/year)

Source: Rabobank

0

2,000

4,000

6,000

8,000

10,000

12,000

Chicken Beef Pork

x 1,000 tonnes

Growing importance of trade, but volatile global market conditions

Global trade in meat 2000-2015

Source: Rabobank, USDA, 2015

Pork: CAGR: +5.4% , 6% of global supply

Poultry: CAGR: +5.5% , 12% of global supply

Beef: CAGR: +3.7%, 17% of global supply

Page 11

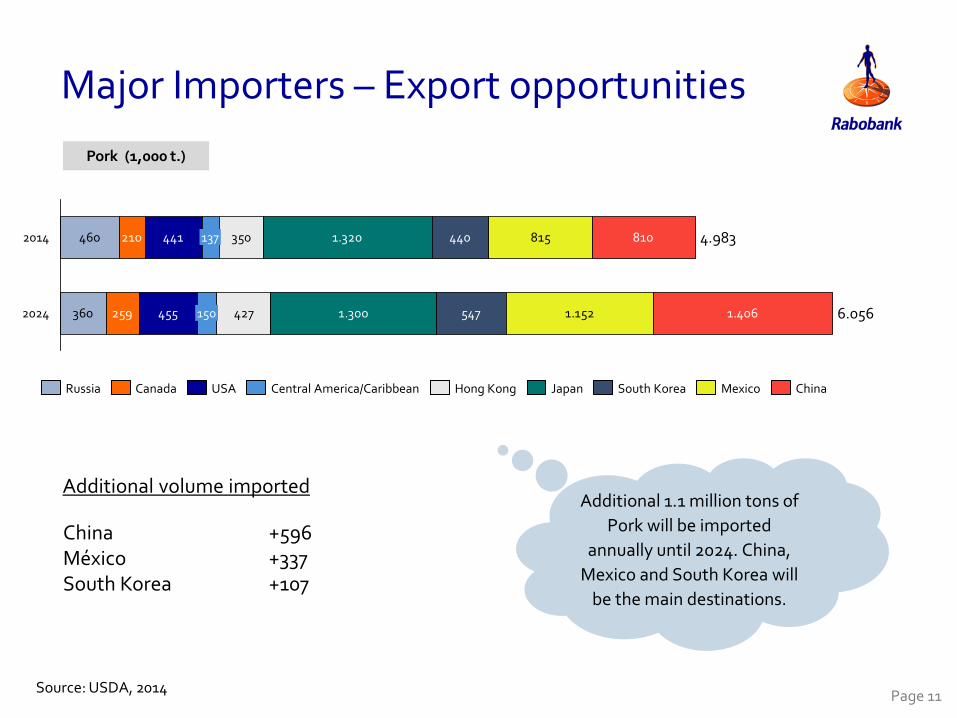

460

360

210

259

441

455

350

427

1.320

1.300

440

547

815

1.152

810

1.4062024 6.056 150

2014 4.983 137

Canada Russia China Mexico South Korea Japan Hong Kong Central America/Caribbean USA

+596 +337 +107

Additional 1.1 million tons of

Pork will be imported

annually until 2024. China,

Mexico and South Korea will

be the main destinations.

Additional volume imported

China México South Korea

Major Importers – Export opportunities

Pork (1,000 t.)

Source: USDA, 2014

Asia’s growing impact on global meat markets

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1990 1995 2000 2005 2010

Beef Pork Broiler

1,000 tonnes

43%

46%

48%

Asian imports of meat 1990-2014

Source: Rabobank/USDA, 2015

Rising.....

Population

Urbanization

And per capita income

Page 13

Self-sufficiency in animal protein and GDP per capita (1980-2014)

Source: USDA, FAO

As China grows economically, it will not only import grain but also meat

40%

50%

60%

70%

80%

90%

100%

$0 $10.000 $20.000 $30.000 $40.000 $50.000

Pe

rce

nt

self

-su

ffic

ien

t in

an

ima

l pro

tein

GDP per capita (current prices, US$)

Japan

Korea

China (including Hong Kong)

Page 14

Fonte: Rabobank, 2015

China’s Self-Sufficiency Has Big Implications for Global Pork

Page 15

Today, China (including Hong Kong) imports only 2% of its annual pork demand.

This 1,150k tons of imports accounts for about 19% of the global pork trade.

BUT, if China’s self-sufficiency fell by 5% (from 98% to 93%) then its share of the pork trade would rise to 40% .

AND, pork production in the US would have to rise by 28% to meet this demand.

More changes are coming...

15%

85%

34%

66%

68%

32%

Packaged Pork

Fresh Pork

Page 16

Global view: Pork 2015/2016

Fonte: Rabobank, 2014

Strong recovery after PEDv

Pork production increased more than

70% in the last 5 years

Embargo against the US, Australia and

the EU

Production has decreased in 2015 while

imports are increasing

Pork exports will increase almost

10% in 2015

Page 18

Brazil has been benefited from the

Russia embargo against other exporters

Largest

importer

Latin America Pork Production

Pork production in 2015 (million tons) Latin America production in 2015

China

EU

Latin America

Russia

5,7

10,8 2,3

54,7

USA

22,5 Others

13,0

Total 109 million tons

0,50,6

1,3

3,4

Argentina Brazil Chile Mexico

The fourth largest producer

Page 19 Source: USDA, 2015

USDA Pork estimations

+5%

-1%

+8%

+6%

+7%

+8%

+5%

USDA Pork estimations

-5%

+12%

+11%

+25%

+10%

-42% -33%

+8%

+3%

Brazilian exports 2015

Source: MDIC

-29%

-3% -19%

+37%

Uruguai

15,3 15,7

Singapura

20,9 25,8

Angola

27,3 38,7

Hong Kong

84,8 82,6

Russia

176,8

129,5 +3%

Jan/Sep15 Jan/Sep14

(1.000 tons)

Jan to Sep 2015: +6%

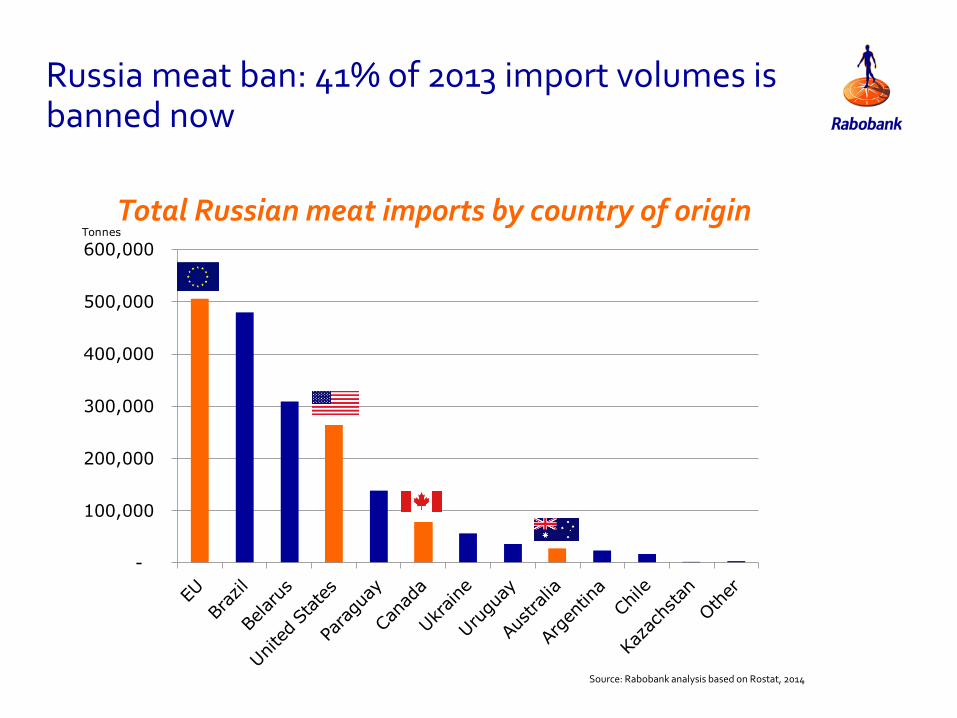

Russia ban has had particularly impact on global pork and beef market

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0

500

1,000

1,500

2,000

2,500

3,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Global beef imports in 2013

Global pork imports in 2013

Global chicken imports in 2013

14% 13%

6%

1,000 tonnes 1,000 tonnes 1,000 tonnes

10% of global meat trade was sold to Russia Source: Rabobank analysis based on USDA, Rostat, 2014

Russia meat ban: 41% of 2013 import volumes is banned now

Total Russian meat imports by country of origin

-

100,000

200,000

300,000

400,000

500,000

600,000 Tonnes

Source: Rabobank analysis based on Rostat, 2014

Exchange rate in Brazil

26 Source: Bloomberg, 2015

0,80

1,20

1,60

2,00

2,40

2,80

3,20

3,60

4,00

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

BRL/USD

Jul/10 Sep/15 0,57 USD/BRL 0,26 USD/BRL Devaluation

~55%

...From the Brazilian point of view...

27

28

...From the American point of view...

29

...From the Russian point of view...

Russian supermarket H2 2014

Page 30

International meat prices

Source: Bloomberg, 2015 Page 32

Live Cattle (LC1) and Lean Hog (LH1)

0

50

100

150

Jul-15 Apr-11 Oct-11 Apr-12 Oct-12 Jul-13 Apr-13 Jan-11 Jul-11 Jul-14 Jan-15 Jan-14 Oct-10 Oct-15 Apr-15 Oct-14 Apr-14 Oct-13 Jan-13 Jul-12 Jan-12

-42%

-16%

-14%

Usd/cwt

-60%

Live Cattle

Lean Hog

Source: World Bank, 2010

World: new land available for rain-fed agriculture

South America.: new land availability estimated by crop

LA has considerable scope to expand food and feed production

[million hectares]

[million hectares]

95

94

44

25

107

29

28

3

3

0

11

7

ME/N Africa

S & E Asia

E Europe/C Asia

Latam/Caribbean

Sub-Saharan Africa

RoW

Bad logistics

Good logistics

10 10

1122

9

46 47

Wheat

10

2

Sugarcane

15

1

Soybeans

1

36

Corn

26 Other S America

Argentina

Brazil

Global demand for agricultural commodities is rising

as a result of increasing population and rising real

incomes

Although part of the need for greater output can be

achieved by raising productivity, new land will

nevertheless be required for agriculture in the future

The distribution of such resources is hard to

evaluate, but it is certainly uneven around the world.

Nevertheless, it is clear that Latin America, and

specifically Brazil, holds a substantial part of the world’s

unused agricultural land

Page 34

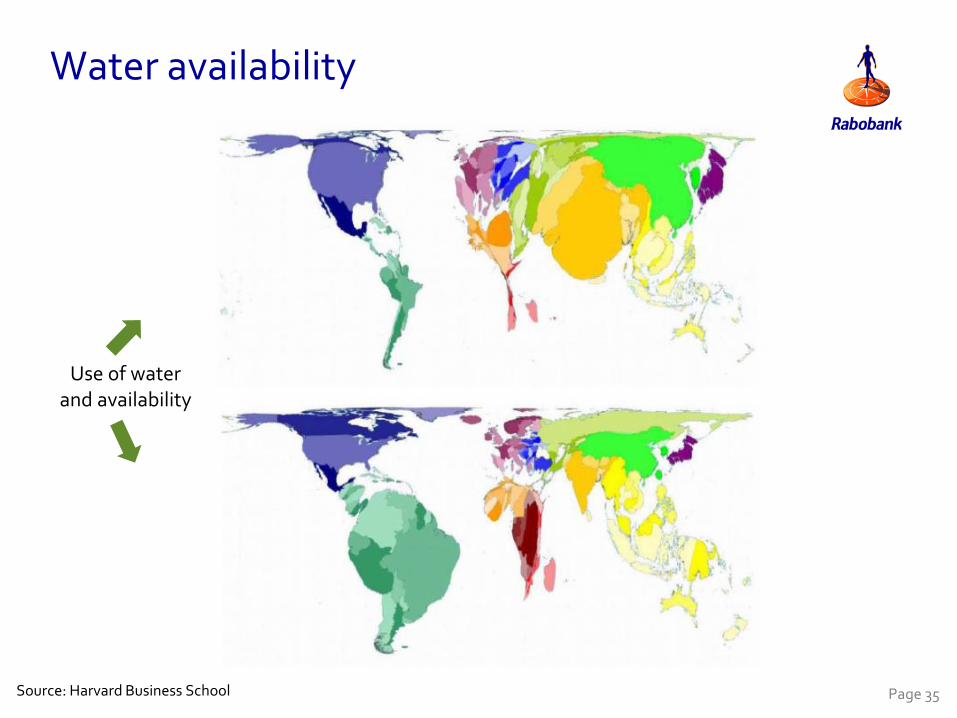

Water availability

Source: Harvard Business School

and availability Use of water

Page 35

Pork cost price comparison selected countries (EUR kg cwe)

0,00

0,50

1,00

1,50

2,00

Feed Other variable costs Labour Other fixed costs

EU high quality processed pork products

EU meat consumption per specie Processed meat consumption

By category and country (1,000 tonnes pw) Beef 15%

Pork 61%

Poultry 21%

Other 3%

-

5.000

10.000

15.000

20.000

25.000

Canned meat Frozen ConvenienceCured meat Bacon & hamChilled convenience

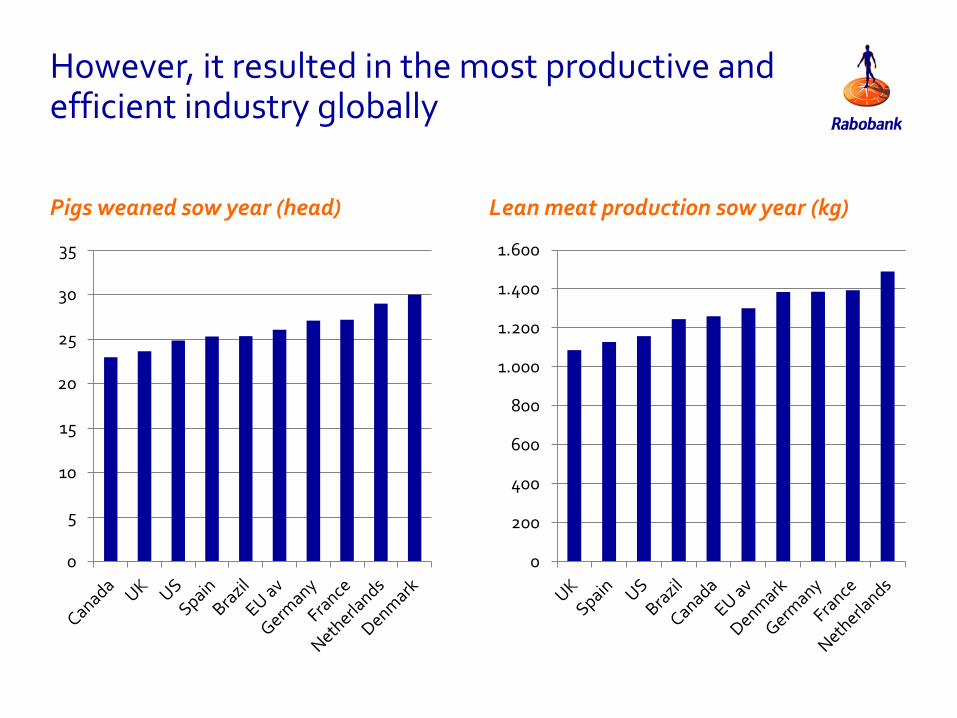

However, it resulted in the most productive and efficient industry globally

Pigs weaned sow year (head) Lean meat production sow year (kg)

0

5

10

15

20

25

30

35

0

200

400

600

800

1.000

1.200

1.400

1.600

EU pork industry dominated by Germany and Spain

EU pork production 2000-2025 (1,000 tonnes cwe)

0

1.000

2.000

3.000

4.000

5.000

6.000

2000 2005 2010 2014 2025F

In the US, High-Flying Pork Producers Margins Have Returned to Earth

• Source: Iowa State

($60)

($40)

($20)

$0

$20

$40

$60

$80

$100

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

2012 Drought

RFS and Great Recession

PEDv Outbreak

Hog Production Margin per Head

Page 41

Corn prices

Source: Bloomberg, Rabobank, 2015

Source: Bloomberg, Rabobank, 2015

Page 42

Soybean prices

Potential in Argentine meat production

Page 43 Source: OECD, Rabobank estimates, 2014

(1,000 t.)

Beef

Poultry Pork

0

500

1.000

1.500

2.000

2.500

3.000

3.500

2023F 2022F 2021F 2020F 2019F 2018F 2017F 2016F 2015F 2014 2013 2012 2011 2010 2009 2008 2007 2006 2024F

+2,2%

2005 2004 2003 2002 2001 2000

OECD outlook

Beef Production

0

500

1.000

1.500

2.000

2.500

3.000

20

01

20

00

20

23F

20

22

F

20

21F

20

20

F

20

19F

20

18F

20

17F

20

16F

20

15F

20

14

20

13

20

12

20

11

20

10

20

09

20

08

20

07

20

06

20

05

20

04

20

03

20

02

20

24

F

+2,5%

OECD outlook

Poultry Production

0

100

200

300

400

500

600

700

20

23F

20

22

F

20

21F

20

20

F

20

19F

20

18F

20

17F

20

16F

20

15F

20

14F

20

13

20

12

20

11

20

10

20

09

20

08

20

07

20

06

20

05

20

04

20

03

20

02

20

01

20

00

20

24

F

+2,9%

OECD outlook

Pork Production

Rabobank estimates on the Brazilian meat market

Source: USDA, Rabobank estimates, 2015

Growth Potential within 10 years

Beef Poultry Pork

+1,078 +2,585

+750

+1,111 +1,367 +140

Consumption Trade Status Meat

8.826

3.4824.849

7.875

8.953

1.849

2.961

3.4462.696

2013

8.535

725

2023

5.916

585

+2,1%

19.397

2013 2023

11.411

23.810

+3,7%

Poultry

Pork

Beef

Domestic Consumption

Trade Status

World export of AP and Brazilian Share (2013-2023)

(1,000 t.)

18,7% 24,8%

28,8%

30,3%

8,2% 8,5%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

2013 Beef 2023 Beef 2013Poultry

2023Poultry

2013 Pork 2023 Pork

Others Brazil Brazil Share

Challenges

Page 45

Infrastructure

Political and economic crisis

Conclusions

Source: Rabobank, 2014

Logistics

Will logistics capacity grow at the same rate as production & export availability?

Increased demand

Asian Protein demand

Domestic Middle Class

Health & security

Animal Heath status

Food safety & quality

Economic framework

Credit crunch, crisis

Exchange rates

Economics

Grain costs

Large (600 mn) domestic market with rising real incomes

Environment

Climate change & emissions

Animal welfare

Potential

Room to growth in productivity

Land and water availability

Page 46

S

O

W

T

Volatile business environment

Exchange rate, commodity prices, interest rates

47

Rabobank International…

“The financial link in the global food chain”™