Embed Size (px)

Citation preview

1 |

No dogmatic approach on inflation

Top macro theme(s):

No dogmatic approach to inflation (p. 2): The Monetary Policy Council remained unfazed by recent inflation shots underlining its exogenous and administrative nature. We stick to our baseline scenario for rates in Poland with a first hike in mid-2022 as the most recent comments from the NBP make start of policy normalization less likely.

What else caught our eye:

The registered unemployment rate in August was stable at 5.8%, on MinLab estimate. A 13-thousand decline in the number of unemployed was recorded in a month, the best August result in the last 4 years. Labour market conditions keep improving as economic expansion continues and the settlement of the Financial Shield’s subsidies have not triggered any massive restructuring. According to B.Marczuk from the Polish Development Fund (PFR), employment in companies that have benefited from the Shield stands at 95% of the pre-pandemic level.

The updated version of the Polish Deal showed that the increase in the healthcare contribution paid by one-man business activity will be lower than previously assumed (4.9% vs. 9%). The resulting decline of new revenues will be partially covered by the introduction of a minimum tax on large corporations, at 0.4% of their revenues. The new tax will apply to capital companies reporting income at or below 1% of revenues.

The government expects that the European Commission will approve the National Recovery Plan at the turn of September/October.

The week ahead:

Detailed CPI figures for August is the key local macro data release this week. The headline inflation rate is likely to be confirmed at the 20-year high of 5.4%, with core inflation up to 4.0%. Labour market data for August should show further gradual improvement of employment and wages.

Balance of payments for July should show roughly balanced current account, amid some weakening in trade volume growth on calendar effects.

Number of the week:

0.25% - NBP reference rate at the end of 2021 implied from FRA curve, compared to almost 0.50% implied from the curve 3 months ago.

10 September 2021

Chart of the week: CPI inflation accelerates in all CEE countries

Source: Macrobond, PKO Bank Polski.

-2

-1

0

1

2

3

4

5

6

7

8

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

Poland Czechia Hungary% y/y

Poland Macro Weekly

Macro Research

Chief Economist

Piotr Bujak [email protected] tel. +48 22 521 80 84

Macro Research Team

Marta Petka-Zagajewska Senior Economist [email protected] tel. +48 22 521 67 97

Marcin Czaplicki Economist [email protected] tel. +48 22 521 54 50

Urszula Krynska Economist [email protected] tel. +48 22 521 51 32

Kamil Pastor Economist [email protected] tel. +48 22 521 81 08

Michal Rot Economist [email protected] tel. +48 22 580 34 22

2020 2021†

Real GDP (%) -2.7 5.4

Industrial output (%) -1.0 16.0

Unemployment rate# (%) 6.2 5.4

CPI inflation** (%) 3.4 4.4

Core inflation** (%) 3.9 3.8

Money supply M3 (%) 16.4 9.0

C/A balance (% GDP) 3.5 2.0

Fiscal balance (% GDP)* -7.0 -1.7

Public debt (% GDP)* 57.5 56.2

NBP reference rate## (%) 0.10 0.10

EURPLN‡## 4.61 4.48

Source: GUS, NBP, MinFin, †PKO BP Macro Research team forecasts;,‡PKO BP

Market Strategy team forecasts; *ESA2010, **period averages; #registered

unemployment rate at year-end; ##at year-end.

2 |

Poland Macro Weekly 10 Sep 21

No dogmatic approach on inflation

The Monetary Policy Council remained unfazed by recent inflation shots underlining its exogenous and administrative nature. The after-meeting presser by Governor A.Glapinski confirmed our view that the majority of the MPC members has no dogmatic approach on inflation and will react only to demand-driven price pressure. All in all, we stick to our baseline scenario for rates in Poland with a first hike in mid-2022 and see interest rate hike this year less likely.

The MPC - as expected - did not introduce any changes to the monetary policy – both

interest rates (reference rate: 0.10%) and the QE program.

In the after-meeting statement, the Council noted the worsening of the pandemic

situation in the world. It also pointed at recent announcements of the main central banks

(Fed, ECB) to stick to accommodative monetary policy. Describing the domestic

economy, the MPC noticed a decline in the annual growth rate of retail sales as well as

industrial and construction output in July and assessed that it was only partially due to

base effects. It was also emphasized that the employment level remains below the pre-

pandemic one and that some employees are still covered by wage subsidies as a part of

anti-crisis shields.

Despite the fact that inflation has risen by 1pp since the previous meeting of the MPC,

comments of the MPC regarding inflation have not been modified. Inflation (in the

opinion of the MPC) still results mainly from factors independent of monetary policy, in

the coming months CPI inflation will remain above the upper bound for deviations from

the NBP target and should decline next year. In total, the changes made in the statement

are, in our opinion, pretty dovish, and there are no signs that the MPC would be willing to

raise interest rates in the near future.

The result of the meeting is not surprising, especially in the context of Monday's

interview with A.Glapiński and the first live press conference of the NBP President since

March 2020. The presser confirmed that the MPC is strongly reluctant to start interest

rate increases this year. According to A.Glapiński, central bank should not react to

a negative supply shock, such as spike in energy and raw materials’ prices and supply

bottlenecks. In A.Glapiński’s view, changes in the reserve requirements proposed by

some MPC members are also inadvisable. The Governor underlined that half of the CPI

inflation (5.4% y/y in August) results from factors which stay beyond the control of the

MPC. He reiterated that all forecasts for 2022 indicate that inflation will decline. At the

same time, the Governor noted that the achievement of ambitious climate goals, which

would lead to an increase in energy prices, may be a permanent factor boosting

inflation. President A.Glapiński believes that currently there is no wage-inflation spiral,

labor productivity is growing rapidly, and unit labor costs are favorable. The situation on

the real estate market is not dangerous, and housing prices are rising in line with the

growth of the population's income. A.Glapiński pointed out that there is still a gap of

around 2 million apartments on the market. He also repeated his earlier assurances that

the MPC would not hesitate to raise interest rates if three conditions were

simultaneously met: (1) reduction of epidemic uncertainty, (2) high inflation driven by

demand factors amid a strong labor market and (3) inflation exceeding the upper bound

for deviations from the NBP target over the projection horizon.

The dovish outcome of the meeting and the presser reduces the likelihood of an

interest rate hike in November 2021. In our opinion, real considerations about an

interest rate increase will not take place until 2022 (and in practice, the issues indicated

by A.Glapiński can be assessed at the earliest in 2q22). Thus, we still assume that the

decision to raise interest rates will only be made by the new Monetary Policy Council,

which will be almost fully formed at the end of 1q22, and we expect a rate hike in mid-

2022.

CPI inflation – the highest in 20 years

Source: GUS, PKO Bank Polski.

CPI likely to be boosted by food prices

Source: GUS, PKO Bank Polski.

-3

0

3

6

9

12

Jan-00 Jan-04 Jan-08 Jan-12 Jan-16 Jan-20

%, y/y

-6

-4

-2

0

2

4

6

8

10

12

-30

-20

-10

0

10

20

30

40

Jan-08 Jan-11 Jan-14 Jan-17 Jan-20

FAO (PLN, 3mma, +9m, L)

CPI food&bev. (3mma, R)

% y/y % y/y

3 |

Poland Macro Weekly 10 Sep 21

Macro monitoring with alternative data

Electric energy consumption (total) Mobility*

Heavy truck traffic Economic activity status (acc. to CEiDG**)

Consumption based on PKO BP card payments Weekly consumer confidence survey

Source: PSE, Apple, Google, GDDKiA, CEIDG, Kantar, PKO Bank Polski, *weighted with market share of iOS and Android, no new google data available, 7DMA, **Central Registration and Information on Business.

-40

-30

-20

-10

0

10

20

30

40

50

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21

PolandFranceItalySpainGermany

% y/y, 7d MA

-100

-80

-60

-40

-20

0

20

40

Feb-20 May-20 Aug-20 Nov-20 Feb-21 May-21 Aug-21

Poland

United States

Germany

Italy

France

% change vs 15-29 Feb 2020 average

113

0

20

40

60

80

100

120

140

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Index: 2-8.03.2020 = 100

-30

-20

-10

0

10

20

3024

.02-1

.03

23

-29.0

3

20

-26.0

4

18

-24.0

5

15

-21.0

6

13

-19.0

7

10

-16.0

8

7-1

3.0

9

5-1

1.1

0

2-8

.11

30

.11-6

.12

28

.12-3

.01

25

-31.0

1

22

-28.0

2

22

-28.0

3

19

-25.0

4

17

-23.0

5

14

-20.0

6

12

-18.0

7

9-1

5.0

8

6-1

2.0

9

closed suspended

newly registered resumed

balance

ths.

129

40

60

80

100

120

140

2-8

.03

30

.03

-5.0

4

27

.04

-3.0

5

25

-31.0

5

22

-28.0

6

20

-26.0

7

17

-23.0

8

14

-20.0

9

12

-18.1

0

9-1

5.1

1

7-1

3.1

2

3-1

0.0

1

1-7

.02

1-7

.03

29

.03

-4.0

4

26

.04

-2.0

5

24

-30.0

5

21

-27.0

6

19

-25.0

7

16

-22.0

8

Index: 2-8.03.2020 = 100

-60

-40

-20

0

20

15-Mar 15-Jun 15-Sep 15-Dec 15-Mar 15-Jun

Expected financial standing

Consumer confidence index

pts.

4 |

Poland Macro Weekly 10 Sep 21

Weekly economic calendar

Indicator Time (UK) Unit Previous Consensus* PKO BP Comment

Monday, 13 September

POL: Current account balance (Jul) 13:00 mn EUR 281 -270 1 The growth of trade volumes has likely slowed down in July, mainly on calendar effects. CA in July was roughly balanced in our view.

POL: Exports (Jul) 13:00 % y/y 23.9 16.0 18.0

POL: Imports (Jul) 13:00 % y/y 36.3 19.0 20.8

Tuesday, 14 September

USA: CPI inflation (Aug) 13:30 % y/y 5.4 5.3 -- --

USA: Core inflation (Aug) 13:30 % y/y 4.3 4.3 -- --

Wednesday, 15 September

POL: CPI inflation (Aug, final) 9:00 % y/y 5 5.4 5.4 CPI likely to be confirmed on the 20-year high.

EUR: Industrial production (Jul) 10:00 % y/y 9.7 -- -- --

USA: Industrial production (Aug) 14:15 % m/m 0.9 0.3 -- --

Thursday, 16 September

POL: Core inflation (Aug) 13:00 % y/y 3.7 3.9 4.0 Core inflation expected to rebound on the prices of services.

USA: Retail sales (Aug) 13:30 % m/m -1.1 -0.8 -- --

USA: Initial Jobless Claims 13:30 thous. 310 -- -- --

USA: Retail sales excl. autos (Aug) 13:30 % m/m -0.4 -0.2 -- --

Friday, 17 September

POL: Wages (Aug) 9:00 % y/y 8.7 8.7 8.7 Labour market continues to gradually improve. POL: Employment (Aug) 9:00 % y/y 1.8 1.1 1.1

EUR: HICP inflation (Aug, final) 10:00 % y/y 2.2 3.0 -- --

EUR: Core inflation (Aug, final) 10:00 % y/y 0.7 1.6 -- --

USA: University of Michigan sentiment (Sep, flash)

15:00 pts. 70.3 72 -- --

Source: GUS, NBP, Parkiet, PAP, Bloomberg, Reuters, PKO Bank Polski. Parkiet for Poland, Bloomberg, Reuters for others.

5 |

Poland Macro Weekly 10 Sep 21

Selected economic indicators and forecasts

Jun-21 Jul-21 Aug-21 1q21 2q21 3q21 4q21 2020 2021 2022

Economic activity

Real GDP (% y/y) x x x -0.9 11.1 5.7 5.9 -2.7 5.4 5.1

Domestic demand (% y/y) x x x 1.0 12.8 5.3 5.3 -3.7 6.0 5.1

Private consumption (% y/y) x x x 0.2 13.3 3.6 6.8 -3.0 6.0 4.7

Gross fixed capital formation (% y/y) x x x 1.3 5.0 3.0 5.0 -9.6 2.7 7.2

Inventories (pp) x x x 0.3 2.9 1.8 -0.1 -0.8 1.2 0.3

Net exports (pp) x x x -1.9 -0.7 0.7 1.0 0.8 -0.2 0.3

Industrial output (% y/y) 18.4 9.8 15.4 7.8 30.3 14.4 10.9 -1.0 16.0 7.5

Construction output (% y/y) 4.4 3.3 7.7 -12.5 2.8 6.6 3.0 -2.7 0.7 5.8

Retail sales (real, % y/y) 8.6 3.9 4.8 1.2 14.4 6.1 9.0 -2.7 7.0 5.0

Nominal GDP (PLN bn) x x x 585.2 618.0 635.6 713.3 2324 2552 2747

Labour market

Registered unemployment rate‡(%) 5.9 5.8 5.8 6.4 5.9 5.7 5.8 6.2 5.8 4.8

Employment in enterprises (% y/y) 2.8 1.8 1.1 -1.7 2.1 1.3 1.0 -1.2 0.7 1.3

Wages in enterprises (% y/y) 9.8 8.7 8.7 5.8 9.9 8.7 9.0 4.8 8.4 8.3

Prices^

CPI inflation (% y/y) 4.4 5.0 5.4 2.7 4.5 5.2 5.5 3.3 4.4 3.9

Core inflation (% y/y) 3.5 3.7 4.0 3.8 3.8 3.8 3.7 3.9 3.8 4.0

15% trimmed mean (% y/y) 3.1 3.6 x 2.6 3.2 x x 3.9 x x

PPI inflation (% y/y) 7.2 8.2 9.5 2.4 6.4 9.0 10.0 -0.5 6.9 5.0

Monetary aggregates‡

Money supply, M3 (PLN bn) 1876.0 1883.9 1889.1 1862.5 1876.0 1908.5 1986 1822.7 1985.8 2097.3

Money supply, M3 (% y/y) 7.4 8.2 9.1 14.4 7.4 8.3 9.0 16.4 9.0 5.6

Real money supply, M3 (% y/y) 2.9 3.1 3.6 11.3 2.8 3.0 3.3 12.7 4.3 1.7

Loans, total (PLN bn) 1349.2 1360.9 x 1344.0 1349.2 1373.3 1382.1 1333.8 1382.1 1468.6

Loans, total (% y/y) 0.6 2.3 x -1.7 0.6 2.7 3.6 0.8 3.6 6.3

Deposits, total (PLN bn) 1724.8 1754.3 x 1669.9 1724.8 1741.6 1727.0 1602.2 1727.0 1837.0

Deposits, total (% y/y) 6.6 8.9 x 12.5 6.6 7.0 7.8 13.9 7.8 6.4

Balance of payments

Current account balance (% GDP) 2.3 2.2 2.1 3.1 2.3 1.9 1.9 3.5 2.0 1.6

Trade balance (%GDP) 2.4 2.3 2.2 2.8 2.4 2.1 1.8 2.4 1.8 0.9

FDI (% GDP) 1.5 1.5 1.6 1.7 1.5 1.7 1.8 1.6 1.8 1.6

Fiscal policy

Fiscal balance (% GDP) x x x x x x x -7.0 -1.7 -1.3

Public debt (% GDP) x x x x x x x 57.5 56.2 53.6

Monetary policy‡

NBP reference rate (%) 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.50

NBP lombard rate (%) 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 1.00

NBP deposit rate (%) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

WIBOR 3Mx (%) 0.21 0.21 0.23 0.21 0.21 0.20 0.20 0.21 0.20 0.60

Real WIBOR 3Mx (%)# -4.15 -4.76 -5.13 -2.53 -4.26 -4.95 -5.25 -3.06 -4.25 -3.26

Exchange ratesx‡

EUR-PLN 4.52 4.57 4.50 4.66 4.52 4.50 4.48 4.61 4.48 4.44

USD-PLN 3.80 3.84 3.78 3.97 3.80 3.78 3.73 3.75 3.73 3.70

CHF-PLN 4.12 4.24 4.09 4.21 4.12 4.09 4.04 4.25 4.04 3.96

EUR-USD 1.19 1.19 1.19 1.17 1.19 1.19 1.20 1.23 1.20 1.20

Source: GUS, NBP, PKO Bank Polski. x PKO BP Market Strategy team forecasts, ^period averages for quarterly and yearly data, #deflated with current CPI inflation, ‡period end values,

6 |

Poland Macro Weekly 10 Sep 21

Monetary policy monitor

MPC Members Hawk-o-meter* Recent policy indicative comments^

E. Gatnar 4.8 “I propose to start this [PAP: tightening] cycle mildly, if we don't start it now we will have to raise rates sharply,

and that will be painful to borrowers.” (31.08.2021, Biznes24, PAP)

K. Zubelewicz 4.5 “A rate increase is necessary to stop inflation, though it’s probably here to stay for longer. (…) If asset

purchases or interest-rate cuts were emergency measures, they should all be abandoned by now.”

(21.07.2021, Bloomberg)

L. Hardt 4.3 “The July inflation projection further strengthened my conviction such a change [an interest rate hike] is

necessary. (…) In the context of pandemic uncertainty and the accompanying increased inflation, one should

look at the entire macroeconomic policy of the country, and the expected continuation a relatively

expansionary fiscal policy gives another argument for a cautious monetary tightening.” (02.08.2021, PAP,

Bloomberg)

J. Kropiwnicki 2.8 “Taking into account vote distribution within the MPC, the earliest possible date for interest rate hikes is

November. (…) First of all, we need to be sure about resilience of inflation and of economic growth, so

economic indicators and forecasts available in autumn this year will be important (…) The changes should be

gradual and cautious, with the first step at 15 bps and further moves dependent on economic developments,

the rate setter argues. (…) The first hike should not exceed 15 bps. Further steps will depend on data coming in

from the economy (…) There's no need for rush. The point is not to shake the market. (…) Hiking interest rates

should be done gradually and cautiously" (09.08.2021, PAP).

J. Zyzynski 2.6 “Until the end of the year, there will rather be no interest rate changes in Poland (…) we have to see how the

fourth pandemic wave develops.” (31.08.2021, PAP)

R. Sura 2.5 “Monetary policy is on the right track. We are supporting the recovery after the pandemic recession, and we’re

making sure that the recovery is permanent (…) The most significant forecasting tool will November’s

projection of inflation and GDP. If this document shows that inflation in 2022 and 2023 will continuously

exceed 3.5% and will be caused by demand-side factors, which can be influenced by the MPC through interest

rates, then I will advocate tighter monetary policy.” (22.06.2020, PAP / Bloomberg).

G. Ancyparowicz 2.4 “Of course inflation is high, we see that and we are not happy, but it is caused by non-monetary factors and as

a result monetary policy instruments...will not solve anything.” (31.08.2021, Refinitiv)

C. Kochalski 2.0 "Regarding the eventual level of interest rates after the pandemic, for me the imperative of maintaining a stable

level of prices while simultaneously supporting the economic policy remains unchanged (…) And as regards the

sequence of monetary policy normalisation, ending the asset purchase [program] and then raising the rates is

the right normalisation" (17.06.2021, PAP).

A. Glapinski 1.7 “A central bank cannot react with interest rate hikes to negative supply shocks (…) If a risk appears of

lasting breech of the target as a result of lasting demand pressure then we will immediately tighten

monetary policy through interest rate hikes." (09.09.2021, PAP)

E. Lon 1.0 “Poland has made no final decisions in respect to the potential interest rate hike this November and could

end up keeping rates unchanged until end-year” (06.09.2021, wGospodarce.pl) *the higher the indicator the more hawkish views. Due to the fact that the new MPC has not voted yet on interest rates changes, the positioning has been made based positively on PAP survey conducted among economists at banks in Poland (scale 1-5). ^Quotes in bold have been modified in this issue of Poland Macro Weekly.

†WIBOR 3M from the last fixing, FRA transactions based on WIBOR 3M for subsequent periods, ‡in basis points, *PKO BP forecast of the NBP reference rate.

1M 2M 3M 4M 5M 6M 7M 8M 9M

Date 9-Sep 9-Oct 9-Nov 9-Dec 9-Jan 9-Feb 9-Mar 9-Apr 9-May 9-Jun

WIBOR 3M/FRA† 0.24 0.29 0.37 0.41 0.48 0.57 0.66 0.76 0.84 0.87

implied change (b. p.) 0.05 0.13 0.17 0.24 0.33 0.42 0.52 0.60 0.63

MPC Meeting 8-Sep 6-Oct 3-Nov 8-Dec - - - - - -

PKO BP forecast* 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10

market pricing* 0.15 0.23 0.27 0.34 0.43 0.52 0.62 0.70 0.73

Interest rates – PKO BP forecasts vs. market expectations

7 |

Poland Macro Weekly 10 Sep 21

Poland macro chartbook

NBP policy rate: PKO BP forecast vs. market expectations Short-term PLN interest rates

Slope of the swap curve (spread 10Y-2Y)* PLN asset swap spread

Global commodity prices (in PLN) Selected CEE exchange rates against the EUR

Source: Datastream, NBP, PKO Bank Polski. *for PLN, and EUR 6M, for USD 3M.

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

Sep-20 Dec-20 Mar-21 Jun-21 Sep-21 Dec-21 Mar-22 Jun-22

market expectations (FRA)

PKO forecast

%

now

3 months ago0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

WIBOR 3M

FRA 6X9

FRA 9x12

%

-20

0

20

40

60

80

100

120

140

160

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

PLN

USD

EUR

pts

-80

-60

-40

-20

0

20

40

60

80

100

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

2Y 5Y 10Y

pts

-80

-60

-40

-20

0

20

40

60

80

100

120

140

160

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

GSCI agriculture

GSCI

GSCI oil

% y/y

96

98

100

102

104

106

108

110

112

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

PLN CZK

HUF RON

Index (1 Jan 2020=100)

8 |

Poland Macro Weekly 10 Sep 21

Economic sentiment indicators Poland ESI for industry and its components

Broad inflation measures CPI and core inflation measures

CPI inflation – NBP projections vs. actual Real GDP growth – NBP projections vs. actual

Source: Datastream, GUS, EC, NBP, PKO Bank Polski.

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

PMI

OECD CLI

Industry

Ifo (Germany)

Retail sales

st.dev.pts

-70

-60

-50

-40

-30

-20

-10

0

-50

-40

-30

-20

-10

0

10

20

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

ESI - industry (L)

Employment (L)

New orders (R)

pts, sa pts, sa

0

2

4

6

8

10

12

-4

-2

0

2

4

6

8

10

12

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

CPICorePPIWages ( R)

% y/y % y/y

-2

-1

0

1

2

3

4

5

6

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

Range of core inflation measures

CPI

% y/y

-2

-1

0

1

2

3

4

5

6

1q14 1q15 1q16 1q17 1q18 1q19 1q20 1q21 1q22 1q23

Actual

November 2020

March 2021

July 2021

%, y/y

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

1q14 1q15 1q16 1q17 1q18 1q19 1q20 1q21 1q22 1q23

Actual

November 2020

March 2021

July 2021

%, y/y

9 |

Poland Macro Weekly 10 Sep 21

Economic activity indicators Merchandise trade (in EUR terms)

Central government revenues and expenditures* General government balance (ESA2010)

Unemployment rate Employment and wages in the enterprise sector

Source: NBP, Eurostat, GUS, MinFin, PKO Bank Polski. *break in series in 2010 due to methodological changes.

-20

-15

-10

-5

0

5

10

15

20

25

30

-20

-15

-10

-5

0

5

10

15

20

25

30

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21Industry (L)

Retail sales (in real terms, L)

Construction ( R)

% y/y, 4mmed % y/y, 4mmed

-30

-20

-10

0

10

20

30

40

50

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

exports imports

% y/y, 4mmed

-20

-15

-10

-5

0

5

10

15

20

25

30

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

revenues

expenditures

% y/y, 4mmed

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

1q08 1q09 1q10 1q11 1q12 1q13 1q14 1q15 1q16 1q17 1q18 1q19 1q20

overall balance

primary balance

% GDP, 4quarter rolling

0

2

4

6

8

10

12

14

16

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

registered (NSA)

harmonized (SA)

NAIRU (harmonized)

%

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

real wage bill

wages (3MMA)

employment

% y/y

10 |

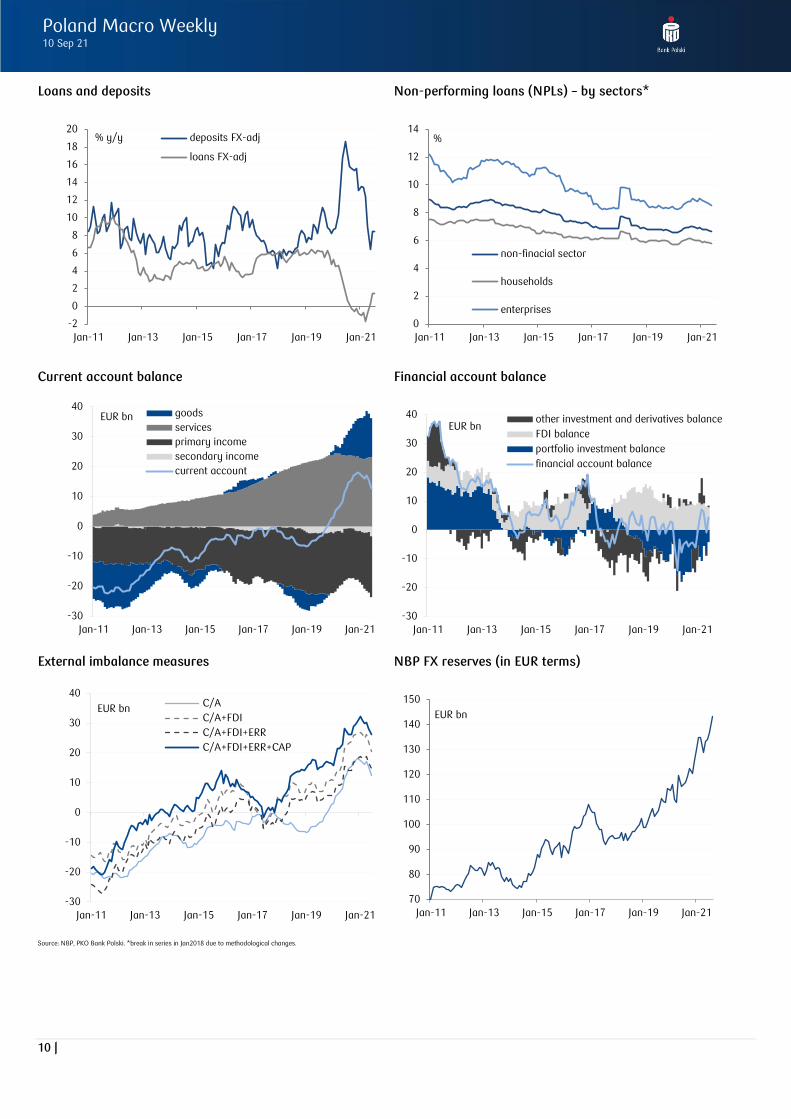

Poland Macro Weekly 10 Sep 21

Loans and deposits Non-performing loans (NPLs) – by sectors*

Current account balance Financial account balance

External imbalance measures NBP FX reserves (in EUR terms)

Source: NBP, PKO Bank Polski. *break in series in Jan2018 due to methodological changes.

-2

0

2

4

6

8

10

12

14

16

18

20

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

deposits FX-adj

loans FX-adj

% y/y

0

2

4

6

8

10

12

14

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

non-finacial sector

households

enterprises

%

-30

-20

-10

0

10

20

30

40

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

goods

services

primary income

secondary income

current account

EUR bn

-30

-20

-10

0

10

20

30

40

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

other investment and derivatives balance

FDI balance

portfolio investment balance

financial account balance

EUR bn

-30

-20

-10

0

10

20

30

40

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

C/A

C/A+FDI

C/A+FDI+ERR

C/A+FDI+ERR+CAP

EUR bn

70

80

90

100

110

120

130

140

150

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

Tysi

ące

EUR bn

11 |

Poland Macro Weekly 10 Sep 21

Previous issues of PKO Macro Weekly:

Consumption-based recovery (Sep 3, 2021)

Budget surplus ahead? (Aug 27, 2021)

Maturing recovery (Aug 20, 2021)

Double digit expansion (Aug 13, 2021)

Economy on holidays (Aug 6, 2021)

American style inflation, American style monetary policy (Jul 30, 2021)

A double-digit rebound (Jul 23, 2021)

Is the CPI inflation really on hold? (Jul 16, 2021)

MPC on hold until late autumn (Jul 9, 2021)

House price growth accelerates after pandemic slowdown (Jul 2, 2021)

Straight to the hot summer (Jun 25, 2021)

Back to pre-pandemic trends (Jun 18, 2021)

MPC waits and doesn’t see (Jun 11, 2021)

Economy roars out of lockdown (May 28, 2021)

The New (Polish) Deal (May 21, 2021)

Fasten your seatbelts, please (May 14, 2021)

Lift-off (May 7, 2021)

To the moon! (Apr 30, 2021)

What's the score? (Apr 23, 2021)

Inflation rears its head yet again (Apr 16, 2021)

Inside the NBP’s comfort zone (Apr 9, 2021)

Locked-down Easter (Mar 26, 2021)

The third wave hits the economy (Mar 19, 2021)

Choke points in focus (Mar 12, 2021)

Blueprint for Recovery (Mar 5, 2021)

This time is (really) different (Feb 26, 2021)

Bottlenecks, winter and lockdowns (Feb 19, 2021)

Green fiscal island (Feb 12, 2021)

Spotlight: fiscal stance (Feb 5, 2021)

2020 better than feared, bounce back ahead (Jan 29, 2021)

Labour waves goodbye to difficult year (Jan 22, 2021)

Housing frenzy exposes some perils of ultralow rates (Jan 15, 2021)

New Year’s sale at the NBP (Jan 08, 2021)

Surplus economy (Dec 18, 2020)

Deal done (Dec 11, 2020)

Bumpy road to recovery (Dec 4, 2020)

A tipping point (Nov 27, 2020)

12 |

Poland Macro Weekly 10 Sep 21

Poland’s macro in a nutshell

2020 2021 Comment

Real economy We stick to our 2021 GDP growth forecast to 5.4% and expect it to remain above 5% in 2022, without taking into account the potential effects of the Polish New Deal (we estimate the impact of tax changes alone at ca. 1.0% of GDP). Strong economic growth will be driven by three engines – (1) consumption (pent-up demand, “forced savings”, high wage growth), (2) investments (National Recovery Plan, high liquidity in enterprises), (3) export (upgrades in global value chains, FDI).

- real GDP (%) -2.7 5.4

Prices Elevated inflation is the price of the rapid recovery. In 2h21 inflation will remain around the level of 5.0%, and we think it will be only slightly lower in 2022. Importantly, we still see the risk balance for this scenario tilted clearly upwards. Food will be the main factor keeping inflation elevated in the coming months, due to both a low base (pork), a weaker harvest (fruits), and rising production costs. Finally, it appears that core inflation is not about to let up. High nominal wage growth also means services price inflation.

- CPI inflation (%) 3.4 4.4

Monetary aggregates With the rebound of the economic growth, we expect credit demand to increase slowly, fueling a moderate bank lending expansion. Smaller scale of asset purchases will result in a deceleration of money supply growth.

- M3 money supply (%) 16.4 9.0

External balance Exports remains the bright star of the Polish economy. The continuation of the strong trend at the beginning of this year indicates that structural rather than transitory factors are behind the Polish export expansion. Trade and overall current account surpluses, combined with EU inflows and strong nominal GDP growth, will lower the foreign debt-to-GDP ratio, which we see as an important factor supporting an upward revision of Poland's rating in the medium term.

- current account balance (% GDP) 3.5 2.0

Fiscal policy Rapid recovery, high inflation, and payment of the NBP profit make the situation of the state budget comfortable, and the scale of the surprise in the execution of this year's budget (vs. the 2021 plan) would be huge. Our current state budget deficit estimate (PLN 19.7 bn) is close to the recent MinFin announcement targeting the 2021 state budget deficit at PLN 13 bn.

- fiscal balance (% GDP) -7.0 -1.7

Monetary policy Market expectations promise a revolution in domestic monetary policy, but the central bank clearly prefers evolution. The NBP remains in crisis mode and is cautious about normalizing monetary policy. However, the first step in this direction has been taken - the MPC is no longer ruling out rate hikes, and all that remains to be decided is "when" interest rates in Poland will start to rise. The Fed and the ECB are giving ambiguous hints to the NBP. In our opinion, the MPC will delay rate hikes until next year.

- NBP reference rate (%) 0.10 0.10

Source: GUS, NBP, Eurostat, PKO Bank Polski.

The above information has been prepared for informational purposes only and is provided to PKO BP SA Group clients. It is not an offer (as understood under the Civil Law of 23rd April 1964) to buy or sell or

the solicitation of an offer to buy or sell any financial instrument and does not constitute the provision of investment, legal or tax advice. It is also not intended to provide a sufficient basis on which to make an

investment decision. The above information has been obtained from or based upon sources believed to be reliable, but PKO BP SA Group does not warrant its completeness or accuracy. PKO Bank Polski Group

strongly recommends that clients independently evaluate particular investments and accepts no liability for the financial effect of its clients’ investment decisions.

The above information is prepared and/or communicated by Powszechna Kasa Oszczedności Bank Polski S.A., registered in the District Court for the Capital City of Warsaw, 13th Commercial Division of the

National Court Register under KRS number 0000026438, Tax Identification Number (NIP): 525-000-77-38, REGON: 016298263, share capital 1,250,000,000 PLN.