Embed Size (px)

Citation preview

Understanding Yu’E Bao: the implications of

Internet Finance development in China

BY

XIAO YAYUE STUDENT NO.14252961

A PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE DEGREE OF

BACHELOR OF SOCIAL SCIENCE (HONOURS) DEGREEN IN CHINA STUDIES

ECONOMICS CONCENTRATION

HONG KONG BAPTIST UNIVERSITY

APRIL 2018

2

HONG KONG BAPTIST UNIVERSITY

April 2018

We hereby recommend that the Project by Ms. Xiao Yayue entitled “Understanding

Yu’E Bao: the implications of Internet Finance development in China” be accepted in

partial fulfilment of the requirements for the Bachelor of Social Sciences (Honours)

Degree in China Studies in Economics.

_________________ _________________

Dr. Luk Sheung Kan Dr.

Project Supervisor Second Examiner

3

Acknowledgements

First and foremost, I would like to take this opportunity to express my deepest gratitude

to my supervisor Dr. Luk Sheung Kan, Paul for overseeing my progress and advising

me at every step through the entire project. It has been an honour and pleasure working

with him.

Moreover, thanks are also due to all the professors and lecturers in HKBU Department

of Economics for their constant guidance throughout the entire course of my

undergraduate study in Hong Kong. Their dedication and hard work make my college

years an unforgettable and valuable experience in my life.

Finally, I would like to thank my parents for their love and care. I am grateful for their

unconditional full support, financially and spiritually.

_______________

Student’s signature:

China Studies Degree Course

(Economics Concentration)

Hong Kong Baptist University

Date: _________________

4

Contents

Abstract ...................................................................................................................................... 5

1. Introduction and Background .................................................................................... 7

1.1. What is Internet Finance: Review on its development in China .....................10

1.2. What is Yu’E Bao: Review on money market fund ...............................................13

1.3. Historical data and policy change .............................................................................14

2. Literature Review ........................................................................................................ 20

2.1. Determinants of interest rate of Yu’E Bao ..............................................................20

2.2. Underlying risks of Yu’E Bao .......................................................................................22

2.3. Money market fund, traditional banking sector and interest rate liberalisation ...................................................................................................................................25

3. Data.................................................................................................................................. 28

4. Methodology and Empirical Results ...................................................................... 29

4.1. “Mean-Variance”, Capital Asset Pricing Model (CAPM) and Sharpe ratio ..29

4.1.1. Proxy selections and definitions of relevant terms ...............................................34

4.1.2. Empirical results and analysis ......................................................................................40

4.2. Third and fourth moment: shape of the distribution .........................................43

5. Economic Interpretations and Further Analysis ............................................... 46

6. Limitations..................................................................................................................... 54

7. Conclusions and Suggestions ................................................................................... 56

8. Appendix ......................................................................................................................... 58

9. References ...................................................................................................................... 62

5

Abstract

This paper is based on a case study of Yu’E Bao, a popular Internet Finance investment

product in China. We start with an introduction of China’s Internet Finance

development situation and four major forms of Internet Finance. Following this we

provided a detailed description on Yu’E Bao’s model, including its historical

performance, interest rates determinants, underlying risks, and its impacts on the

banking sector. Then, we move on to two research questions: 1) Has Yu’E Bao actually

outperformed other investment alternatives? If not, what are the major factors

contributing to its popularity? 2) Assuming Yu’E Bao is a representative of money

market funds and China’s Internet Finance product, what economic implications can we

draw from this development, especially regarding the Chinese financial system?

Based on Capital Asset Pricing Model (CAPM) and Sharpe ratios, we analysed daily

data on stock market performance and similar investment products, from 2013 to 2018.

We further divided the sample time period into shorter time frames to better see the

changes occurring overtime. Our research findings to the first question are as follows:

1) compared to the stock market, Yu’E Bao and other money market funds have a

higher risk-adjusted return. The advantage of less volatility in return is more obvious

during stock crash time; 2) compared to other money market funds, the Sharpe ratio of

Yu’E Bao is consistently higher than the average of money funds in different time

frames, providing a high and also stable risk-adjusted return; 3) high households’ saving

ratio, relatively poor performance of investment alternatives, and use of Internet and

technology together contribute to the popularity of money market funds in China.

6

Regarding the impacts of money market funds and Internet Finance on the Chinese

financial system, our analytical results are the following: 1) On one hand, the sheer size

of assets managed by money market funds will take away some portion of bank deposits

and thereby affect banks’ lending ability; 2) On the other hand, the large amount of

assets invested in cash equivalents extend the lending ability of banks through

negotiable deposits; 3) recent policy changes show that the development of money

market funds is still under control of the Chinese government and therefore, will not

cause fundamental change to China’s traditional banking sectors; 4) In general, Internet

Finance development has brought fiercer competition to the traditional banking sector

and accelerated the process of interest rate marketization.

Key Words: Yu’E Bao; Money Market Fund; Internet Finance; Sharpe Ratio; China

7

1. Introduction and Background

Yu’E Bao, an investment product based on the third-party payment platform Alipay and

managed by Tianhong Asset Management Co., has gained increasing popularity since it

first appeared on the market in May 2013. At the end of 2017, Yu’E Bao has reported

1.58 trillion yuan (US$ 251.2 billion)1 in asset value under management, surpassing

JPMorgan’s US government money market fund to become the largest money market

fund in the world. Yu’E Bao is also considered one of the most typical products of

Chinese Internet Finance (Jingu, 2014).

Even so, the concerns over the security and further development of the poduct exist.

Fitch, one of the world’s big three crediting rating agencies, consider Yu’E Bao much

riskier than JP Morgan’s US government money market fund. Their evaluation criteria

include credit quality, liquidity and market concentration.2 China’s implicit state-

guaranteed financial system3 and special economic environment also contribute to other

concerns about multiple regulators and regulatory arbitrage (Chan, 2017).4

The sheer size of Yu’E Bao’s asset under management and its broad investor base

mandates these risks merit our attention. This paper addresses two major questions: (1)

Has Yu’E Bao actually outperformed the market and other alternative investment? If

not, what major factors have inspired its popularity among Chinese investors? (2)

1 Data source: Tianhong Asset Management Co. (2017, Dec 31). Tianhong Yu’E Bao Money Market

Fund Q4 2017 Report 2 Fitch Ratings Inc. (2017, Dec 13). Comparing the World’s Two Largest Money Funds (More Risk for

World's Biggest, China's Yu'E Bao, than JPM USG MMF) Retrieved from

https://www.fitchratings.com/site/re/906997 3 Implicit state guarantee means that government will bail out a firm when the firm face default risk

through the implementation of public policies. 4 See Chan, H. (2017, May 10). Yu’E Bao: A Double-Edged Sword for Financial Innovation. Retrieved

from https://ippreview.com/index.php/Blog/single/id/434.html

8

Assuming Yu’E Bao is a representative of money market fund and China’s Internet

Finance development, what economic implications can we draw from this development?

What changes this development may put on Chinese financial system?

Year 2013, which is often referred to as “the year of Internet Finance in China”, is

widely considered a new era for Internet Finance development (Jingu, 2014). Most

research into Internet Finance has taken the form of qualitative analysis of the industry’s

emerging business models, underlying risks and governance and regulatory problems.

Pricing problems on P2P lending platforms has also been the subject of several

quantitative studies centred on Internet Finance centred.

Though some studies have been previously conducted, this paper still contains a number

of relevant contributions. Firstly, it provides an overview of Internet Finance

development in China and a detailed description on Yu’E Bao to readers who might not

be familiar with this product and the development situation in China. Secondly,

previous studies on Yu’E Bao only cover years up to 2015. We extend the studies to

2018. Such extension of study period is crucial because China’s stock market went

through dramatic fluctuations during the year 2015 and the year 2016. We consider the

stock market an investment alternative to money market funds in our study, so abnormal

fluctuation is an important consideration in evaluating product performance. Thirdly,

past studies focus on the single product, Yu’E Bao within a single period. We include

other money funds for comparison and also divide the whole of the time sample period

into shorter time period to better evaluate the performance as it changes over time.

9

The paper proceeds as follows: latter part of this section introduces basic information

and facts; Section 2 provides a related literature review; Section 3 and Section 4

describe data, methodology and empirical results; Section 5 discusses economic

interpretations and further analysis; Section 6 analyses the limitations of our study and

the last section concludes and suggests some directions for further research.

10

1.1. What is Internet Finance: Review on its development in China

Internet Finance, also referred to as “digital finance” or “fintech”, has been grown

popular and inspired wide discussion in recent years. Definitions of Internet Finance

vary, covering different items. Chinese officials5 define Internet Finance as “the new

business model of utilizing the Internet information communication technologies to

accomplish a wide range of financial activities, such as third-party payment, online

lending, direct sales of funds, crowding, online insurance and banking” (Shen and

Huang, 2016). Broader definitions of Internet Finance also include Internet digital-

based currencies like Bitcoin, Q-coin and Amazon Coin. In this work, we have adapted

the narrower definition that defines Internet Finance as financial services and financial

intermediaries provided online.

Through technological advancement, individuals and corporations can enjoy traditional

financial services such as money deposits, withdrawals, online transfers, fundraising,

investment and wealth management. McKinsey (2014) estimates that by 2025, financial

services’ extensive use of Internet applications will contribute 1,200 billion CNY to

China’s annual GDP. In 2015, China’s Internet Finance user base has already expanded

to 500 million people, contributing to 20% of GDP, between 12 and15 trillion CNY.6

There are four major forms of Chinese Internet Finance: micro-financing services, peer-

to-peer lending (P2P), crowd funding and third-party payment. Micro-financing services

5 People's Bank of China, Ministry of Industry and Information Technology, Ministry of Public Security,

Ministry of Finance, State Administration for Industry and Commerce, State Council Legislative Affairs

Office, China Banking Regulatory Commission, China Securities Regulatory Commission, China

Insurance Regulatory Commission, and State Internet Information Office jointly issued the Guiding

Opinions on Promoting the Healthy Development of Internet Finance July 2015 Retrieved from

http://www.mof.gov.cn/zhengwuxinxi/zhengcefabu/201507/t20150720_1332370.htm 6 See Ngai, J. et al., ‘Disruption and Connection: Cracking the Myths of China Internet Finance

Innovation’, McKinsey Greater China FIG Practice July 2016.

11

primarily target customers without easy access to bank or cheap credit, including private

firms, small and medium enterprises (SMEs) and low-income individuals. Currently, E-

commerce and IT companies are primary providers of micro-financing services. Making

use of data technology, IT companies performed both quantitative and qualitative

analysis to determine users’ crediting ratings. The information7 used to build credit-

rating models includes but is not limited to the company business register information,

transaction history, payment of utility fees, personal profile and social connections.

From credit ratings, loan providers can determine financing details, including the

amount, interest rate, maturity date. After borrowers are lent fund, micro-financing

companies employ third-party payment platforms to monitor money use and detect

potential misuse. Mirco-financing companies can immediately terminate lending and

block relevant accounts on third-party platforms (Zhang and Zhou, 2015). As of March

2017, Ant Credit, an affiliate under Alibaba Group, has lent 5.2 million RMB unsecured

loans to small business in China.8 Internet-based Micro-financing in China is also

considered as progress in promoting financial inclusion and enhancing affordable access

to financial services for disadvantaged individuals and groups (Loubere, 2017).

The second type of Internet Finance, peer-to-peer (P2P) lending is a direct financing

method9 that enables borrowers to divide financing needs into small portions and

borrow from a large group of lenders. This process simultaneously allows lenders to

7 See Sesame Credit, a platform under Alipay and Alibaba for an example. Information is obtained from

https://www.xin.xin/#/detail/1-2 8 Data is obtained from official Website of Ant Financial. Unsecured loans refer to the loan issued and

supported by the borrowers’ credit ratings, instead of by any kinds of collaterals. 9 Direct financing refers to the way of financing that borrowers directly borrow from financial market

without the need to turn to a financial intermediary. While in the case of indirect financing, financial

intermediaries take money from the borrowers at an interest rate and lend the money to borrowers at a

higher rate, leading to high cost of borrowing.

12

reduce risk exposure by diversifying their portfolio and lending to many borrowers.

Currently, Lufax, an affiliate under Ping An Insurance (Group) Co., is one of China’s

largest P2P lending platforms. Unlike financial intermediaries, who profit from the

spread between lending and borrowing rates, P2P lending platforms primarily generate

profits from their service fee structures. These platforms’ services include financial and

wealth management products, investment consulting, debt assignment10

, credit rating

evaluation with credit data, and information disclosure (Zhang and Zhou, 2015).

The third category of Internet Finance is crowd funding, which raises capital for a

project and a venture via a huge Internet user base. Crowd funding can take the form of

a donation, loan, reward or equity. Popular Chinese crowed funding platforms include

Taobao and JD.

The fourth and equally indispensable subset of Internet Finance is China’s Internet

Finance is third-party payment platforms. Third-party payment was originally designed

in the United State, to resolve payment problems in Customer-to-Customer (C2C)

business. This payment method dates back to 1999, when E-commerce giant eBay

purchased and further developed Billpoint, a company providing individual-to-

individual money transfer services. PayPal, one of the most popular third-party

payment platforms worldwide, targets both customer-to-customer (C2C) and business-

to-business (B2B) services. At the end of 2017, its annual payment volume had reached

451.27 Billion USD11

, while mobile payment’s global total revenue, including third-

10

Debt assignment refers to the transfer of debt and all related rights and obligations from a creditor

(assignor) to a third-party (assignee). 11

Data is obtained from PayPal Annual Report 2017.

13

party payments and direct payments via bank-developed mobile apps, was reported at

780 Billion USD.12

China’s largest third-party payment platforms are Alipay, affiliated with Alibaba, and

TenPay, affiliated with Tencent. Respectively, these two platforms took up of 53.73%

and 39.35% of the market share in Q3 2017.13

Other platforms include Union Pay and

Baidu Wallet.

This study’s focus, Yu’E Bao, does not clearly belong within any of the four categories

presented above. Even so, Yu’E Bao’s development is closely tied to third-party

payment platforms. Yu’E Bao and its characteristics will be further discussed in the

following section

1.2. What is Yu’E Bao: Review on money market fund

Yu’E Bao, which translates to “leftover treasure” in Chinese, is a money market fund

that is typically espoused as open-end, low-risk, low-return, high-liquidity and cash-

equivalent. An open-ended fund issues an unlimited number of stock or bond shares and

allows investors to sell and buy these shares at any trading time. In contrast, close-

ended funds issue a fixed number of shares, and investors are only permitted to trade

these shares through a broker.

Compared to other fund types, money market funds typically accumulate lower returns

and exercise less risk. These funds typically invest in short-term, high quality debt

12

Data is obtained from TrendForce 13

Data is obtained from iResearch.

14

securities that include government treasury bonds, tax-exempt municipal securities, and

corporate and bank debt securities. In practice, many investors (perhaps incorrectly)

consider a money market fund to be as safe as a bank deposit and a useful alternative to

stock market investment.

Yu’E Bao’s investment process is simple and convenient. Investors can transfer money

into Yu’E Bao online or via mobile phone with Alipay from either an Alipay or bank

account. Once transferred, investors can remove money from Yu’E Bao at any time. At

its initial development stage (before mid-201714

), investors are able to do these

transactions at any time and in any amount without incurring transaction fee. Since May

2017, the fund management company implemented maximal purchase limits. Yu’E

Bao’s investor base now numbers around 3 billion.15

1.3. Historical data and policy change

This section provides historical data on Yu’E Bao’s return rate, asset value, asset value

growth rate, and asset allocation. This data is provided to allow readers a more

comprehensive and direct impression of this investment product. This section also

considers crucial historical policy changes in investment in Yu’E Bao. In China,

government intervention is quite common and heavily influences economic

development while regulatory directly affects market behaviour.

Figure 1.3.1 compares Yu’E Bao’ returns to the People’s Bank of China (PBoC

hereafter) 3-month benchmark deposits rate and demand deposit rate benchmark.

14

Changes will be covered in the Part 1.3 Historical data and policy change. 15

Data is obtained from Tianhong Asset Management Co.’s Website.

15

During our study period, which spanned from May 30, 2013 to Feb 12, 2018, Yu’ E

Bao’s average 7-day annualized return rate of Yu’E Bao is 3.86%, much higher than the

PBoC benchmark deposit rate.

Interest rate, which is closely related to the cost of borrowing and the price the capital,

has been rigidly controlled by Chinese government for a long time. A few measures for

exercising the control include bank reserve requirement, loan quota and deposit ceiling.

Before Nov 2015, as shown in the Table 1.3.1, PBoC implemented a deposit rate ceiling

on commercial banks based on the benchmark. A deposit ceiling is the upper limit that a

lending institution can charge for a loan and this directly limits interest earned from

bank deposits. The removal of interest rate ceilings in November 2015 is considered as

“the most decisive step” China made in interest rate liberalization and also accelerates

the process of financial reform (PBoC, 2015).

16

Table 1.3.1 RMB deposit rates

2004/10 Removed the floor of deposit rates

2012/06 Increased the ceilings of deposits rates to 1.1x of the benchmark deposit

rate

2014/11 Raised the ceilings of deposits rates from 1.1x to 1.2x of the benchmark

deposit rate

2015/03 Raised the ceilings of deposits rates from 1.2x to 1.3x of the benchmark

deposit rate

2015/05 Raised the ceilings of deposits rates from 1.3x to 1.5x of the benchmark

deposit rate

2015/08 Removed the ceilings of deposit rates with maturities > 1 year

2015/10 Removed the ceilings of deposit rates for commercial banks and rural

cooperative financial institutions

Sources: PBoC; CICC

17

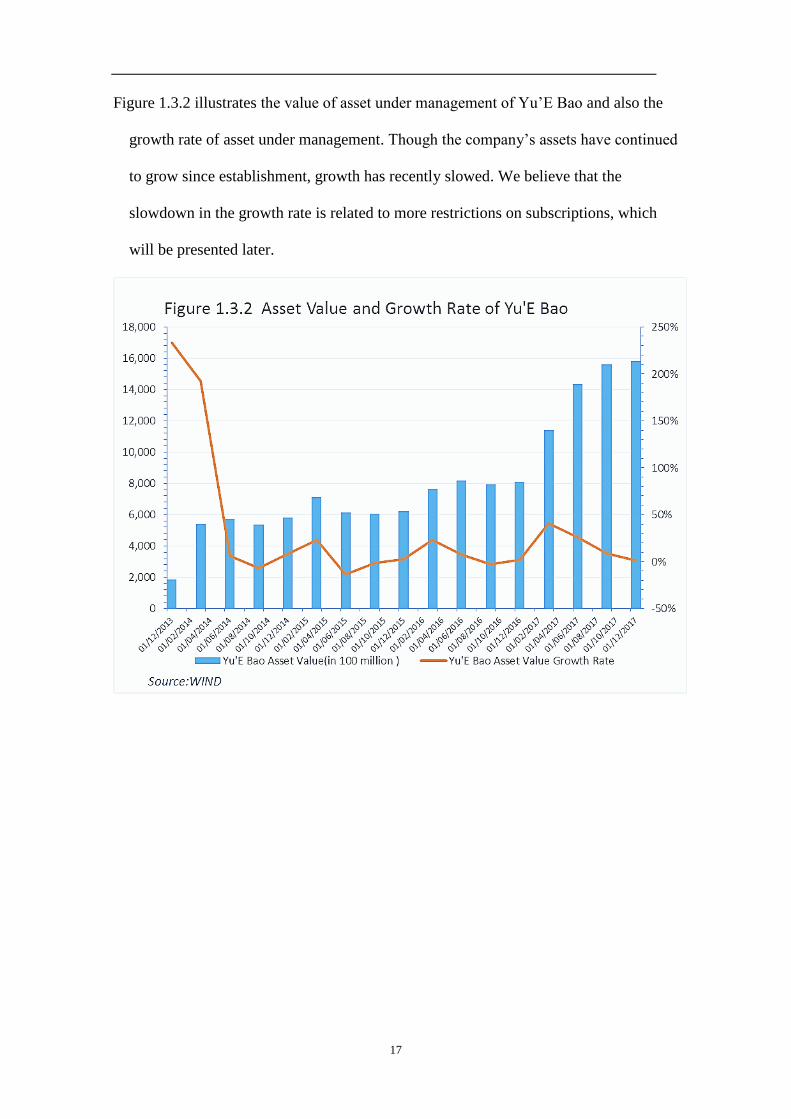

Figure 1.3.2 illustrates the value of asset under management of Yu’E Bao and also the

growth rate of asset under management. Though the company’s assets have continued

to grow since establishment, growth has recently slowed. We believe that the

slowdown in the growth rate is related to more restrictions on subscriptions, which

will be presented later.

18

Figure 1.3.3 illustrates Yu’E Bao’s asset allocation during the period considered by this

study. Cash and cash equivalents consistently occupied the largest proportion of the

company’s allocation, and these assets were primarily employed for negotiable bank

time deposits. Unfortunately, information regarding bank deposits counterparties and

Yu’E Bao’s investment securities is unavailable to the public.

19

Figure 1.3.4 outlines four major shifts in investment policies under Tianhong Asset

Management Co. These shifts include reduction in the maximum funds an individual

can deposit into Yu’E Bao, the maximum amount an investor can invest in a day, and

most recently, an aggregate daily subscription quota16

for all the investors. This

progression demonstrates the company and fund manager seek greater control over the

market, asset growth, and liquidity risk avoidance.

Figure 1.3.4 Investment Policy Change

16

Meaning that the total amount available to all the investors for subscription is limited.

May 30 2013 No limit on Subscription and redemption

May 27 2017 Individual Subscription Maximal: 250,000 Yuan

August 14 2017 Individual Subscription Maximal:

100,000 Yuan

December 8 2017 Daily Subscription Maximal: 20,000 Yuan

Feburary 1 2018 - March 15 2018 "Aggregate Daily Subscription Quota"

20

2. Literature Review

Despite Yu’E Bao’s rapid development, several past studies have addressed the

following three questions. First, what are the major determinants of Yu’E Bao’s interest

rate, and how can its relatively high return be explained? Second, what major risks

underlie Yu’E Bao and other money market fund returns? Third, since 2013, when

Yu’E Bao appeared on the market, whole money market funds market have reached a

valuation of 6.8 trillion yuan (as of November 2017),17

or about 60% of total mutual

funds(Chinadaily, 2018). This amount surpasses the 4.7 trillion total valuation of

individual bank account deposits with the Bank of China in 2017.18

This has attracted

attention to Yu’E Bao and other money market funds’ impacts on the traditional

banking industry and the interest rate liberalisation process.

2.1. Determinants of interest rate of Yu’E Bao

Previous interest rate related studies have attempted to identify the relationship between

Yu’E Bao’s returns and interbank rate and money supply factors such as exchange rates.

Some researchers have compared Yu’E Bao with the whole money fund market and

concluded Yu’E Bao exhibits the scale effect,19

which contributes to the firm’s

relatively high return and lower volatility (Cheng, Pang and Zhang, 2018).

In a study of Yu’E Bao’s costs and interest paid to investors, Liu (2014) applied a linear

regression model to analyse the relationship between the Yu’E Bao interest rate and the

17

Data is obtained from China Bank Association. 18

Data is obtained from Bank of China 2017 Annual Report. Retrieved from

http://www.bankofchina.com/en/investor/ 19

Scale effects means that when total output of a product increases, the average cost of production will

decrease.

21

Shanghai Inter-Bank Offered Rate (SHIBOR). She found no long-term relationship

between these two factors and argued that Yu’E Bao initially transferred some of profits

to investors as interest payments through bank deposit agreements.

Other research argued against this finding. Jiang (2015) reported a linear relationship

between Yu’E Bao’s return over period and the SHIBOR rate in the last historical

period and the return of Yu’E Bao in the period . Lu, Xue and Zhou (2015)

employed a multi-factor regression model to analyse the relationship between Yu’E Bao

and SHIBOR at different maturities. They identified significant relationships between

these two factors, but the directions of these impacts varied; while the 1-month and 3-

month SHIBOR rate were positively related to Yu’E Bao’s return, the 2-Week SHIBOR

was negatively related.

He and Bai (2015) constructed Ensemble Empirical Mode Decomposition Vector

Autoregression (EEMD-VAR) model and found that SHIBOR and money supply have

the highest degree of influence on Yu’E Bao’ s return and they thus concluded that the

tightness of domestic financing level and monetary policy are two most significant

determinants. Besides, they also suggested that exchange rate and bank loan ratio have a

negative correlation with the return.

When investigated Yu’E Bao’s asset allocation and profit statements, Chen and Bai

(2017) found over 70% of the company’s assets are held in bank deposits and reserves,

and 99% of interest came from bank deposit agreements. Based on a Bayesian Quantile

Regression Model, they also identified a significant positive relationship between the

Yu’E Bao’s return and SHIBOR, a 1-year bank investment product return, and the

22

Chinese government’s 1-year bond yield. Their study also demonstrated a negative

correlation between money supply (M2) and Yu’E Bao’s return. They concluded

macroeconomic development negatively relates to Yu’E Bao’s return.

The most recent literature, published by Chen et al (2018), focuses on Yu’E Bao’s

volatility and externality compensative return. The study employed a time-variant

capital asset pricing model (CAPM). The WIND Index and CSI money fund index acted

as market proxies and compared to Yu’E Bao’s performance. Their results demonstrate

that Yu’E Bao’s returns were less volatile than the overall market, and only a relatively

insignificant correlation exists between Yu’E Bao and the market, leading to smaller

beta than traditional financial products. Chen et al (2018) posited that Yu’E Bao’s

relatively high return and low volatility resulted from the scale effect – as Yu’E Bao

gathered investors’ income at its large scale, each individual’s money contributed

positive externality20

to others’ return. The three present the term “externality rate of

return” to refer to this advantage wielded by Yu’E Bao and other Internet Financial

products.

2.2. Underlying risks of Yu’E Bao

Yu’E Bao and other similar money market fund products are associated with five types

of risk: credit, liquidity, interest rate, policy and operation (Chen, 2014; Wang et al,

2014; Lin, 2015; Li, 2015).

Credit risk refers encompasses the outcome wherein borrowers default and prove unable

to service debt payment. In this situation, investors may be unable to reacquire their

20

Externality refers to the benefit or cost to society or another person of a private action.

23

principal funds, let alone interest. In the case of Yu’E Bao, this category of risk may

arise due to asset mismanagement. According to Lin (2015), over 90% of Yu’E Bao’s

assets are currently allocated in interbank deposits. As a result, credit risk takes the form

of bank default.

Liquidity risk is dictated by Yu’E Bao’s buying and redemption rules. As an open-

ended fund, Yu’E Bao can be bought and redeemed by investors at any time. The “T+0”

transaction cycle requires same-trading-day payment settlement, and in practice,

investors can typically withdraw money from Yu’E Bao to their Alipay accounts

immediately. Compared to China stock market, where a “T+1” 21

settlement cycle is

employed, Yu’E Bao has proved an attractive investment option for investors who value

near-instant liquidity.

But Yu’E Bao’s “T+0” transaction settlement rule also facilitates some risk. If a large

volume of shares are simultaneously redeemed, the company may have insufficient cash

to fulfil short-term financial demands. Such sudden widespread redemption is not

unprecedented in China. On Nov 11, 2013, China’s largest online shopping day (similar

to Black Friday in the US), 16.79 million online shopping transactions were paid with

investor funds withdrawn from Yu’E Bao. In total, these transactions were valued at

61.25 billion yuan and set a record for single-day fund redemption value worldwide

(Lin, 2015). Notably, on September 30, 2013, the total value of Yu’E Bao’s assets

under management was 556.53 billion yuan. Even accounting for asset growth between

September 30 and November 11, the 61.25 billion yuan withdrawn constitute a sizable

portion of Yu’E Bao’s assets.

21

“T+1” transaction cycle allows one more day to settle the payment.

24

Interest rate risk emerges from fluctuations in the market interest rate. Investment

product value is altered based on the spread between the market interest rate and the

return rate from Yu’E Bao. Increased market interest rates will, for example, result in a

decrease in investment value and affect investors’ real purchasing power. Chen (2014)

argues that monetary policy, macroeconomic development and inflation all contribute to

this type of risk.

Policy risk results from uncertainty in the adoption and implementation of policy

changes. Still new and immature, China’s Internet Finance industries and products have

not yet received sufficient regulatory attention and guidance. More broadly, China’s

financial market is also not well-established. Potential policy changes or stricter future

regulations may damage investor interests and positions (Wang, 2014).

Finally, operation risk is primarily the result of imperfections in Yu’E Bao’s transaction

system, lack of management experience and concerns over cyber security (Chen, 2014).

Chen (2014) applied the Value-at-Risk (VAR) method to measure Yu’E Bao’s risk. His

analysis demonstrates the firm’s risk now is controllable, but he argues the public

should closely monitor potential default, increasingly strict supervision from external

regulators and cyber security problems.

In conclusion, Yu’E Bao’s associated risk can generally be classified into two

categories. The first type of risk closely relates to this investment product’s

development environment and includes risks arising from immature operation systems

and cyber security. In addition, China’s financial system, sometimes characterised as

25

“dominated by large banking sectors with inefficiency and non-performing loan”,22 also

contributes to credit and liquidity risk. The remaining type of risk includes all general

risks faced by money market funds, including interest rate risk, liquidity risk and so on.

2.3. Money market fund, traditional banking sector and interest rate liberalisation

The following section considers the influence of Yu’E Bao and other money market

funds’ actual effects on the interest rate liberalisation process. In addition, the overall

effect of Internet Finance development on traditional banking industries is first

presented.

In studying Internet Finance’s overall effects on traditional banking sectors, Guo and

Shen (2016) stated the Internet Finance development’s major influences include

upgraded technology, improved work efficiency, increased capital cost and reduced

management costs and risk-taking. They also demonstrated a “U” shaped trend in the

impacts of Internet Finance on commercial banking sectors; in Internet Finance’s early

phase, commercial banks benefited from reduced management costs and risk-taking.

Later, however, Internet Finance development facilitated increased capital cost and risk-

taking. In addition, Guo and Shen (2016) noted heterogeneity in the sensitivity of banks’

responses to these changes: small and medium banks proved more sensitive, while large

commercial banks were generally slower to respond.

Hassanali, Bernard and Marc (1995) cited evidence of U.S. money market fund

development to explain the relationship between money funds and interest rate

22

Non-performing loan(NPL) refers to the loan that the borrower does not make the interest payment or

repay the principal. For details, see Allen, F., Qian, J., Zhang, C., & Zhao, M. (2012). China's financial

system: opportunities and challenges (No. w17828). National Bureau of Economic Research.

26

liberalisation. They argued interest rate liberalisation is a crucial factor in money market

fund growth, and the development of money market funds also accelerates the interest

rate liberalisation process. According to Shaw (1973), interest rate liberalisation, which

allows the interest rate to be determined by market supply and demand, is a critical step

in financing deepening23

and removing excessive government interventions.

When considering the relationship between money market funds and traditional banking

sectors, Xiao (2016) was the first to employ quantitative analysis to determine the

impacts of money market funds on bank deposits, liquidity and interest rate

liberalisation in China. Xiao (2016) employed data collected from 16 publicly listed

Chinese banks between 2008 and 2014 and found that money market fund growth

significantly impacted bank deposit volume. For every 1% increase in money market

fund valuation, bank deposits fell around 0.08%. In addition, money market fund

development reduced banks’ liquidity ratios by altering their demand deposit ratio. She

found that China’s deposit rate constrains prevented banks’ deposit volumes from

illustrating interest rate sensitivity. However, a positive correlation does exist between

the yields of bank-guaranteed financial products and money market funds. When money

market fund yields increase by 1%, bank-guaranteed yields increase by 0.643%. As a

result, Xiao (2016) concluded money market fund development positively impacts

China’s interest rate liberalisation and also affects the traditional banking industry.

Zhao and Ji (2017) adopted “Structure-Conduct-Performance” (SCP) theory and

analysed both bank and Yu’E Bao financial products. Based on data gathered between

23

Financial deepening means the increased provision of financial services. Financial deepening includes

providing a wider range of services and providing different socioeconomic groups better access to

financial services.

27

2012 and 2015, the two researchers posited the emergence of Yu’E Bao improved bank

financial product yields. In addition, Yu’E Bao’s presence and expansion fosters more

intense competition within the traditional banking industry and helps improve the

service quality.

Previous literature closely relates to this study’s scope. Analysis of interest rate and risk

factors enables better understanding of investors’ choices to invest in money market

funds and how investors weight risk types in China’s unique financial and economic

system. However, past research has primarily focused on Yu’E Bao, which is a single

product. Less attention has been dedicated to investment alternatives, such as stock

investments and other money market funds. In this study, we seek to determine if Yu’E

Bao provides a higher return to risk ratio than other investment choices. In addition, we

analyse Yu’ E Bao’s performance across different development time periods framed by

key changes.

28

3. Data

The data employed in this study was exported from Bloomberg Terminal and WIND.

Bloomberg is a digital platform specializing in the provision of data and financial

analysis. Practitioners and investors can also use the platform to monitor real-time

market fluctuations and trade.

WIND is China’s Bloomberg equivalent. It provides analysis focused on the Chinese

market and is widely employed by Chinese individuals and institutions. We downloaded

any data unavailable on Bloomberg from WIND.

This study considers a period spanning from 30 May 2013 to 13 Feb 2018 (inclusive).

This period starts with Yu’E Bao’s establishment. A wider coverage of data will enable

us to better observe interest rate changes and improve comparison accuracy.

All collected data is daily data normalized on a weekly-rolling basis. A detailed

description of this normalization and calculation process for each data category is

provided in this study’s empirical analysis section. Proxy selection criteria will also be

discussed in the empirical analysis section. In the appendix, Table 8.1 describes each

data source.

29

4. Methodology and Empirical Studies

4.1. “Mean-Variance”, Capital Asset Pricing Model (CAPM) and Sharpe ratio

Capital Asset Pricing Model (CAPM), a classical modern finance model, was first

introduced by William Sharpe (1964) and John Lintner (1965) and has been widely

discussed ever since. In addition to its use as the base of many academic studies, CAPM

is also widely applied in industry analysis. Practitioners and investors employ risk

indexes derived from CAPM, such as the Sharpe Ratio and Beta, to evaluate portfolio

performance. These indexes are crucial in considering investment decisions. In 1990,

CAPM’s importance and widespread impact earned Markowitz and Sharpe the Nobel

Prize in Economic Science.

This study’s empirical analysis is based on CAPM. We interpret the performance of

Yu’E Bao using empirical results. However, since CAPM was developed based on

Modern Portfolio Theory (MPT), MPT first warrants further explanation.

Modern Portfolio Theory and “Mean-Variance Analysis”

Modern Portfolio Theory development was founded by Markowitz’s work Portfolio

Selection in 1952. He argues there are two major steps in forming a portfolio. First,

through observations and analysis of investment products’ past performance, potential

investors form expectations about future performance. Second, investors then select

portfolios based on these future performance beliefs. Markowitz’s theory primarily

emphasises this second phase. He presented the “Mean-Variance Analysis” technique to

facilitate more efficient investment decisions.

30

In Markowitz’s model,

∑

∑

∑ ∑

where

denotes the percentage of asset i to be invest in portfolio j.

denotes the return of assets i.

, and all the weights are non-negative given that short-sale is not

permitted.

is the standard deviation of the asset i during the sample period.

is the coefficient correlation between asset i and asset j during the sample period.

is also the covariance between asset i and asset j during the sample period.

One of Modern Portfolio Theory’s key insights is that an asset or portfolio’s return and

risk should not be viewed or assessed independently. Instead, investors should consider

how each investment contributes to the overall portfolio’s return and risk. If we assume

all investors are rational and risk-averse, then investors analyse a portfolio’s variance

and mean and attempt to optimize portfolios by either maximizing expected returns

within a specific level of variance or minimizing variance at a specific level of return.

One major limitation of Modern Portfolio Theory is its more normative theory on

portfolio optimization (Sharifzadeh, 2005); the model is also unsuitable for application

31

by individual investors. The model also fails to explain how investors initially construct

their return expectations for single individual assets.

Second, Markowitz’s model requires the estimation and calculation of the variance-

covariance matrix (Sharifzadeh, 2005). This process can prove troublesome, as it

requires the estimation of n variances and

convariance. For a CSI 300 Index stock,

for example, 45,150 calculations of variances and covariance are required. Previous

theories did not provide a market equilibrium price for assets under risk and did not

explain the relationship between “the price of individual asset price” and “various

components of its risks” (Sharpe, 1964, pp 425-427). Soon after MPT’s introduction,

CAPM was developed based on “Mean-Variance” trade-off and the “Risk-Return”

concept.

Capital Asset Pricing Model

CAPM began with Markowitz’s “Mean-Variance Efficient Portfolio Optimizer” model

and additional assumptions of capital market structure and investor behaviour. These

major assumptions include (1) investors are risk-averse, rational individuals who try to

maximize the utility of their wealth; (2) investors can borrow and lend unlimited

volumes of risk-free assets at a risk-free rate; (3) investment quantities are fixed and

limited to all marketable assets (this assumption excludes all privately traded or

nontraded assets or investments); (4) markets are frictionless: costless information is

simultaneously available to all investors, and individual investor actions have no effect

on market price; finally, (5) there are no market imperfections, such as transaction costs

or tax liabilities. This assumption ensures only two factors affect how investors form

32

their portfolios: expected return and return variance (Copeland et al. 2005; Sharifzadeh,

2005).

In essence, CAPM addresses the relationship between an individual asset’s expected

rate of return and risk. CAPM measures the sensitivity of a single asset to the entire

market and calculates whether the expected excess return of any portfolio, ( ) , has a

linear relationship with the portfolio’s sensitivity to the market, , and expected excess

market return, ( ) . The model is expressed as follows:

( ) ( ) Where

( ) denotes the expected return on an investment.

denotes the theoretical risk-free rate of return.

( ) denotes the average expected market rate of return.

( )

( ) denotes the sensitivity of the individual asset’s

rate of return to the overall market’s rate of return.

The difference between the actual return rate and expected equilibrium rate return rate is

denoted by alpha, or Jensen’s index:

( ) ( ) ( )

Where

( ) denotes the expected return on an asset or portfolio.

denotes the theoretical risk-free rate of return.

( ) denotes the average expected market rate of return.

( )

( )

33

The alpha ratio compares the actual realized performance of a portfolio and its required

rate of return by measuring whether an investment outperforms or underperforms the

market. Alpha is also referred to as the “overall excess return” or “abnormal return”. A

positive alpha ratio of 1%, for example, indicates the return on investment outperformed

the market benchmark by 1% in the same period. Thus, investors attempt to identify

investments with higher alpha ratios.

Risk-Reward Analysis: Sharpe Ratio

Like alpha, beta, standard deviation and R-squared, the Sharpe Ratio, a statistical risk-

adjusted return, is a crucial indicator of performance.

Arthur D Roy (1952) was the first to suggest the use of a risk-reward ratio for portfolio

selection and risk management. Roy’s safety-first criterion (1952) stated that investors

should minimize the probability an asset’s return will fall below the minimal acceptable

return, denoted by ( ) where is the actual return of the asset, i, and is

the minimal acceptable return rate. Later, in 1966, William Sharpe developed this

criterion into a “reward-to-variability” ratio now known as the Sharpe Ratio. The ratio

is expressed as follows:

( )

√ ( )

Where

( )

√ ( )

34

The Sharpe Ratio measures excess return, referred to as risk premium, by undertaking

one more unit of risk. This ratio is useful because it labels an investment as suitable

only if higher returns do not facilitate additional risk. Thus, a higher Sharpe Ratio

implies better risk-adjusted performance.

In next section, we apply CAPM and “Risk-Reward Analysis” to calculate the value of

Sharpe Ratios. Comparisons between Yu’E Bao and other investment choices are

included to address our first research question: Has Yu’E Bao outperformed the market

and other similar investment products? In addition, we repeated this calculation process

across different time frames to identify any changes in Sharpe ratios and locate

rationales behind these changes. First, we must outline the criteria and reasons behind

proxy selections. Then, we display our results. Economic interpretations of these results

are discussed in a later section.

4.1.1. Proxy selections and definitions of relevant terms

The choice of market rate: CSI300 Index

The Shanghai-Shenzhen China Stock Market 300 Index (CSI 300 Index) was selected

as a market performance proxy. The CSI 300 Index replicates the performance of the

top 300 stocks traded in the Shanghai and Shenzhen Stock Exchanges. The CSI 300

Index is a market-value-weighted index, and each stock component is weighted

according to the total market value of its outstanding shares.24

24

Market-value weighted index is also known as capitalization-weighted index. The changes in individual

stock price have different impacts on the stock index according to their market capitalization (the share

price times the number of shares outstanding). In contrast, in a price-weighted index, price of each stock

is the only factor for determining the stock index.

35

We selected the CSI 300 Index for two reasons. First, the index possesses wide

coverage of stock market performance. The CSI 300 Index is comprised of 300 stocks

with the highest market values in many sectors, including finance, utilities,

construction, and IT. This distribution more effectively represents overall market

performance than similar indexes with less coverage, such as the CSI 100 Index or

indexes focusing on a specific industry, such as the CSI 300 Capital Markets Index.

Second, the CSI 300 Index more comprehensively reflects stock market fluctuations.

Because the CSI 300 Index is a cross-market index with stocks in both the Shanghai

Stock Exchange and Shenzhen Stock Exchange, it is more representative than a single-

market index, such as the Shanghai Stock Exchange 150 Index (SSE 150 Index).

The Risk-Free Rate Option: China Demand Deposit Rate

A risk-free rate refers to the rate investors can acquire from risk-free investments.

Damodaran (2009) outlines two major criteria for risk-free investments: no risk of cash

flow associated default, and no reinvestment risk.25

In reality, almost all investments

have some risk. Governments also can collapse and default on sovereign debt. The most

recent example of such default occurred in Greece in 2015 and led to repayment failure

of 1.7 Billion USD in government debt to the International Monetary Fund (CNN,

2015).

Considering the political, economic power and Government Bond, the U.S. is unlikely

to collapse soon. In addition, the short maturity of U.S. Treasury bills26

further reduces

25

Reinvestment risk refers to the risk that the coupon received from the investment has the potential to be

reinvested at a lower interest rate. 26

Usually issued with maturity dates of 28 days, 91 days, 182 days and 364 days, all less than one year.

36

interest rate risk. In practice, so called T-bills commonly act as a reliable proxy for the

risk-free return rate for academics and practitioners. In contrast, China’s government

bond liquidity 27

is relatively low. This makes its use as a proxy inappropriate when

compared to money market funds. Past studies have employed China’s Shanghai

Interbank Offered Rate (SHIBOR) as a risk-free rate proxy, but this rate is also

unsuitable for comparison to Yu’E Bao’s high liquidity product.

Like Chen et al. (2018), we selected and applied the demand deposit rate as a proxy for

the risk-free rate. The demand deposit is the money individuals can withdraw from their

bank deposit accounts at any time without notifying their banks in advance. This high

liquid characteristic resembles Yu’E Bao’ near-instant liquidity. During our study

period, demand deposit rates differed between banks. However, the five largest state

banks28

maintained the same demand deposit rate. This rate was used for our study.

The choices of other money market funds for comparisons

We selected and compared the performance of six funds to Yu’E Bao’s performance.

Funds were selected based on several major criteria. First, all funds were money market

funds. We limited our comparisons to this category to limit potential biases in result

interpretation. We excluded bond, equity, and index, fund investment through qualified

domestic institutional investors (QDII) schemes and other non-money market funds.

Second, selected funds were established before Yu’E Bao was introduced to the market,

May 30, 2013. This criterion ensures compared data sets share time frames and similar

sample sizes. As discussed in the above literature review, Yu’E Bao’s interest rate

27

Usually issued with maturity of 3 or 5 years, longer than 1 year. 28

Refers to Bank of China; Industrial and Commercial Bank of China; Agriculture Bank of China; China

Construction Bank; Bank of Communications.

37

closely relates to several economic factors, including SHIBOR, the exchange rate and

money supply. The comparison of performance ratios between funds is not objective

across differing time periods and macroeconomic environments. Third, the minimal

purchase amounts for selected funds range from 0.01 CNY to 100 CNY with an upper

maximal purchase amount limit. In China, two classes/categories can exist within the

same money market fund: category A and category B. The biggest difference between

these categories is the purchase threshold. Category A targets individual investors and

assigns a maximal holding amount, while in contrast, category B targets institutional

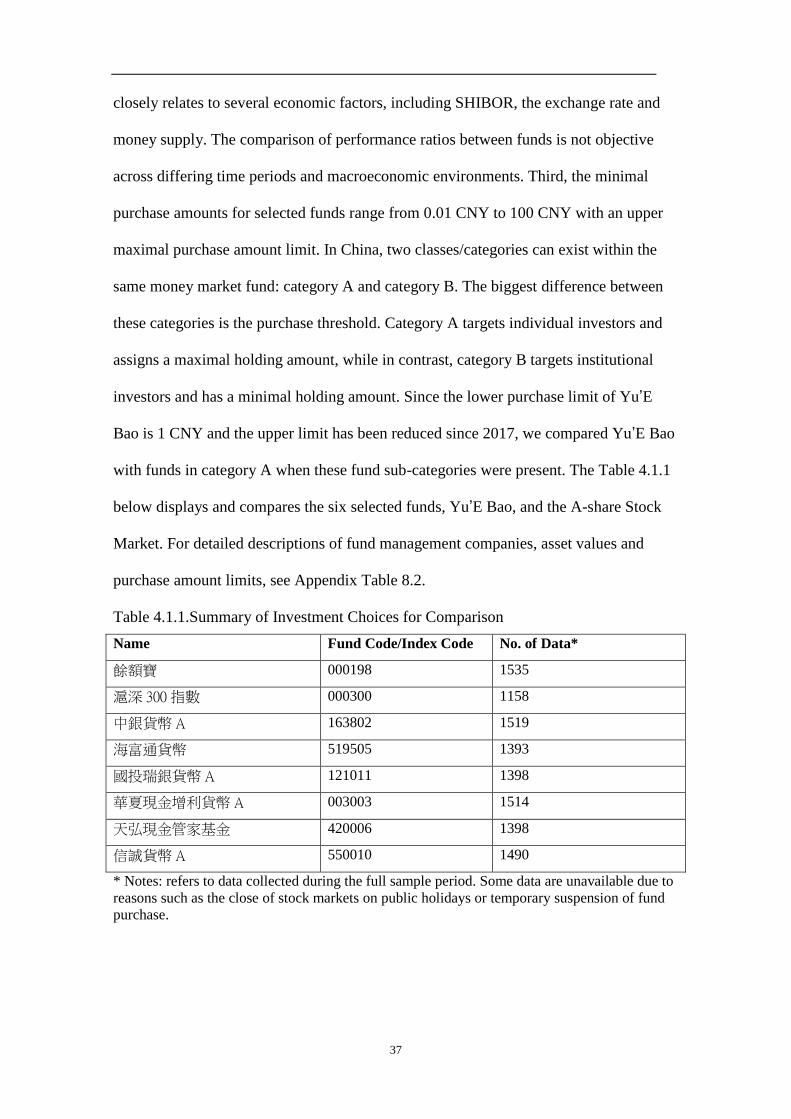

investors and has a minimal holding amount. Since the lower purchase limit of Yu’E

Bao is 1 CNY and the upper limit has been reduced since 2017, we compared Yu’E Bao

with funds in category A when these fund sub-categories were present. The Table 4.1.1

below displays and compares the six selected funds, Yu’E Bao, and the A-share Stock

Market. For detailed descriptions of fund management companies, asset values and

purchase amount limits, see Appendix Table 8.2.

Table 4.1.1.Summary of Investment Choices for Comparison

Name Fund Code/Index Code No. of Data*

餘額寶 000198 1535

滬深 300 指數 000300 1158

中銀貨幣 A 163802 1519

海富通貨幣 519505 1393

國投瑞銀貨幣 A 121011 1398

華夏現金增利貨幣 A 003003 1514

天弘現金管家基金 420006 1398

信誠貨幣 A 550010 1490

* Notes: refers to data collected during the full sample period. Some data are unavailable due to

reasons such as the close of stock markets on public holidays or temporary suspension of fund

purchase.

38

The Choice of Sub-Time Frames

As discussed in the Data session, our full sample study period is from May 30 2013 to

Feb 13 2018. To see how Yu’E Bao and other money market fund performed during the

time when abnormal fluctuations and volatility occurred in stock market, we further

divided the study time periods into four shorter timeframes:

- First period: May 30, 2013 - May 29, 2015

- Second period: May 30, 2015 - Feb 13, 2018

- Stock Crash Time: May 29 2015 - Feb 29 2016

- Post-Crisis Time: March 01 2016 - Feb 13 2018

The cut-off point is the China Stock Crash in 2015. During the June 2015 to Feb 2016,

China stock market fluctuated dramatically. On the single “Black Monday” August 24

2015, Shanghai Stock market fell by 8.48% and Shenzhen main index fell 7%, leading

to a largest plunge since 2007(The New York Times, 2015). A few government

responses include suspension of scheduled Initial Public Offering (IPO),

implementation of circuit breaker29

in January 2016, interest rate cut and etc.

Definitions of relevant terms

Closing Price (for CSI 300 Index): the final price of a security at which it is traded on a

given trading day. Closing price thus represents the latest valuation of a security until

trading begins on the next trading day.

29

Circuit breaker, also called trading curb or “collars”, refers to the mechanism that transactions will be

halt temporarily if the prices hit pre-defined threshold. 5% and 7% are two thresholds applied in China

stock market.

39

7-Day Annualized Return Rate (for all money market funds): the average return level of

the money market fund over the past 7 days. The data obtained after the annualization

and is a reflection of the fund's profitability.

Since the data exported are on daily basis and we adjusted it as follows:

For the return of CSI 300, the weekly return is calculated by:

Where

is the weekly return of CSI300 Index at the time t,

is the closing price at the time t

Considering that market may close due to public holidays or other reasons, calculation

is on the trading days’ basis instead of calendar days to avoid ambiguity.

For the return of Yu’E Bao and other money market funds, the weekly turn is calculated

by:

( )( )

Where

is the 7-day annualized return for money market funds

is the weekly return for these products

40

4.1.2. Empirical results and analysis

Sharpe Ratios

Table 4.2.2 and Figure 4.2.2 display the results of Share ratios. There are three major

findings in terms of Sharpe ratios. Firstly, using China demand deposit rate as the risk-

free rate, stock market generally has a lower value of Sharpe ratios, or even negative

ones during the crisis time, than the money market funds. This implies that for every

unit of extra risk taken, investors may not receive a higher return but even suffer loss.

While in the case of money market funds, the positive values represent less downside

risk, which is the possibility that the actual return being lower than the expected one and

investors suffer from loss when the market condition is not good. We consider

difference in Sharpe ratios is related to different investment natures between equity and

mutual funds. For the stock market investment, it is commonly characterized “high risk,

high return”. In contrast, mutual funds usually can diversify risks through asset

allocations and it offers professional management to the investors, which make money

market funds more attractive for investors who cannot bear much risks and lack of

professional knowledge in stock market.

Secondly, for the comparison among different money funds, we find that Yu’E Bao is

not always the “Best performer” among all the seven money funds in terms of Sharpe

ratios. However, for all six time periods, Yu’E Bao outperformed at least half of rest

funds, ranking top 3 among six funds constantly. This implies that during our study

periods, the return from investing in Yu'E Bao and bearing risks is relatively stable and

higher.

41

Thirdly, regarding the performance of a single fund, we find that the Sharpe ratios

fluctuated a lot in different market conditions. In the first two years' of development,

Yu’E Bao carried a Sharpe ratio of 5.63 while in the most recent two and a half years,

Sharpe ratio decreased to around 4.40. In addition, this ratio is even higher when the

stock market was experiencing a decline, reaching 7.14 during 2015 China stock crash.

This means that during the crisis, investors even received higher return for the same unit

of risk they undertook.

Similar unexpected higher Sharpe ratios during crisis time also exist in other six money

funds. Based on the calculation formula,

( )

√ ( )

We found that the higher Sharpe ratios result from relatively smaller value in

dominator, which is the standard deviation of the return √ ( ), instead of a larger

value of numerator, expected excess return ( ). This led us to think that during

stock crisis time, even though people generally held a lower expectation of return from

investment, Sharpe ratio might be even higher due to less volatility in return. Detailed

calculation results for each investment product will be provided in Appendix Table 8.3.

42

Table 4.1.2 Summary of Sharpe Ratios Time

CSI 300 Index Yu'E Bao 中銀貨幣 A 海富通貨幣 國投瑞銀貨幣 A 華夏現金增利 A 天弘現金管家 信誠基金

Full sample period 0.0745 3.5040 3.3375 3.5176 3.2052 2.8811 2.9467 2.6003

13/05/30 -15/05/29 0.2302 5.6351 5.0493 4.9440 4.9531 4.8451 4.3647 3.1981

15/05/30 -18/02/13 -0.0335 4.3677 4.4998 4.0157 3.3995 3.3754 3.2373 3.9296

Stock Crash -0.2188 7.1422 9.5188 4.6793 3.6196 10.7038 3.9319 6.1009

Post-Crisis Time 0.1771 4.0926 4.1020 3.8506 3.4597 2.9277 3.3847 3.6842

43

4.2. Third and fourth moment: shape of the distribution

Previous analysis based on CAPM is subject to the two crucial conditions. First, the

return rate of each investment product is normally distributed. Second, investors are

only concerned with the first two central moments of the probability distribution of the

return: the average return rate and the variance of return. In these settings, the best

option to maximize their utility lies on in “mean-variance frontier”. However, in reality,

these conditions might not always be met. Literatures related to fund performance

assessment have found that the return of portfolio is not always normally distributed

(Cambell and Hentschel, 1992) and Leptokurtic problems30

exist in return distribution

(Hsu, Ou and Ou, 2012).

For this reason, we included the third and fourth moments in the empirical studies and

with the aid of Excel, we drew the distribution curve to visually compare the

distributions of return.

Third moment: Skewness

The third moment, skewness, is the measure of the degree of asymmetry of the

distribution around the mean. Skewness is calculated by:

∑ ( )

Where is the mean value, is the cubed standard deviation, and is the number of

data points. Normal distribution has a skewness value of 0. A negative value of

skewness indicates that there is a long tail in the negative direction and data distribution

30

A Leptokurtic problem means that the distribution tends to be more peaked and fatter tailed than

normal distribution.

44

is skewed to the right. In contrast, a positive value of skewness indicates that there is a

long tail in the right direction and data distribution is skewed to the left.

Fourth moment: Kurtosis

The fourth moment, kurtosis, is a measure of the peakedness of a distribution, whether it

is more or less peaked than normal distribution. Kurtosis is calculated by:

∑ ( )

A normal distribution has a kurtosis has value of 3. A kurtosis value less than 3

indicates a “light tailed distribution”, producing a relatively flat distribution and is said

to be “platyurtic”. A kurtosis value greater than 3 indicates a “heavy tailed distribution”,

producing a relatively peaked distribution and is said to be “leptokurtic”.

To better equip our analysis of money fund performance, we further investigated

previous studies on the relationship between third and fourth moments of investment

products’ performance and investors’ preference. We found that the discussion on

skewness has already been hotly debated for a few decades and the results and opinions

greatly vary. Francis (1975) is the first to question whether it is important to include

skewness parameters in investors’ decision-making process. Based on empirical

evidence, Francis (1975) claimed investors actually do not consider skewness in stock

market investment. On the other hand, it has been suggested by many other scholars that

risk-averse investors should prefer investments displaying positive skewness (Arditti,

1967; Jean, 1971). Recent research on hedge fund skewness and subsequent investment

flows into and out of hedge funds found that investors do include skewness in the

evaluation of historical performance of hedge funds and this contributes to better ex-

ante fund selections. Additionally, the returns for inflows into hedge funds with positive

45

skewness grow by 11.5% more annually than hedge funds with negative skewness

(Heuson, Hutchinson and Kumar, 2012).

In contrast, investors’ preference for positive kurtosis can be more intuitively

interpreted. Darlington (1970) stated that, at a given variance, kurtosis can be used to

describe the dispersion of the observations from the average. Thus, it measures the

possibility of extreme outcomes, or the extent to which investors may garner either

extreme loss or gains. Later studies provided evidence to risk-adverse investors’

preference for positive kurtosis (Dittmar, 2002; Agarwal, Bakshi Huij, 2008).

Unfortunately, most existing theories and studies about skewness and kurtosis problems

center on equity and hedge fund investment and little are related to the focus of our

study: money market funds. Considering that some features of money funds and hedge

funds greatly differ31

, we did not directly employ these theories to interpret and

compare the third and fourth moment performance of money market funds.

In addition, considering that our primary research interest lies in Internet Finance

development and the implications on the Chinese financial system, we left the problems

related to parameter selections and possible data transformation processes in Sharpe

ratio model for future research. Instead, we provide graph illustrations of the

distributions and statistical results as shown in the Appendix Figure 8.4. More

suggestions for future research are mentioned in Part Seven: Conclusions and

recommendations for future research.

31

Hedge funds sometimes can be aggressively managed and are only open to a few “accredited”

investors. In addition, the management fee for hedge funds is much higher than that for money market

funds. The primary goal of investing in hedge fund is to outperform the market.

46

5. Economic Interpretations and Further Analysis

In this section, we first interpret the empirical results and address our first research

question: Has Yu’E Bao actually outperformed the market and other alternative

investments? If not, what major factors have inspired its popularity among Chinese

investors? Then, we use Yu’E Bao as a representative of money market funds and

China’s Internet Finance development to further extend our discussion to the second

research question: What implications can we draw from this development and what

changes may Internet Finance bring to China’s traditional financial system?

Based on a single-criteria “Risk-to-Reward” analysis, we find that during our study

period, Yu’E Bao had a higher Sharpe ratio than stock market investment. Compared to

the other six selected money funds, the performance of Yu’E Bao is more stable in the

sense that its Sharpe ratios are higher than at least half of six similar money funds, all in

the same time period. This finding drives us to characterize the performance of Yu’E

Bao as “more stable”. In addition, we find that during the crisis, money funds show

even higher Sharpe ratios even though stock market investors might suffer great loss.

However, we do not hold the direct interpretation that “it is a higher Sharpe ratio alone

that leads to the popularity of Yu’E Bao among investors,” because investors may have

different investment preferences, and other indicators also affect the evaluation of its

performance. In fact, we have identified other crucial factors contributing to the

popularity of Yu’E Bao and the rapid development of money market fund products in

general.

47

First and foremost, China’s household saving rate has been quite high for a long time,

providing the basis for the most direct source of money for money market fund

investment. As shown in the Figure 5.1, around half of GDP is saved in China (Red

solid line in Figure 5.1), both among individual households and at firms. Regarding

households, national rural-urban adjusted data from National Bureau of Statistics of

China reveals that households saved more than 40% of earnings (Song and Xiong,

2017).

Figure 5.1 Saving and Investment figure

Source: Data source: China Statistical Yearbook

Many studies have been conducted to analyse the underlying reasons for such a higher

saving ratio.32

Some explanations include, the changes in population policies and

32

A few classical models applied include Keynesian absolute-income hypothesis, Modigliani-Brumberg’s

life-cycle theory, and Friedman’s permanent-income hypothesis. For details, see Qian (1988) and Yang

(2012).

48

subsequent structural change in demography, imbalanced sex ratio, the on-going and

incomplete transition from public-provided housing, education, and healthcare to

private provision, and so on. One recent study on household finances in China

compared with U.S household finances development situation33

finds that the higher

wealth-to-income ratio in China is driven by investor preference parameters and

institutional parameters. That is, Chinese investors tend to be more patient than those in

the U.S. and this characteristic is believed to be related to the long agriculture

development traditions in China. Additionally, China’s labour market is riskier with a

higher level of uncertainty. More variable income changes34

and a low consumption

floor35

motivate China’s households to maintain more in precautionary savings (Cooper

and Zhu, 2018). Thus, we think that the popularity of Yu’E Bao and large volume of

assets under management of the money market fund is closely related to investors’ high

saving ratios and disposable income. When a “cash-equivalent” investment product,

with near-intense liquidity but bringing a much higher interest than bank deposits,

comes into the market, it provides a channel for Chinese investors to spend their large

amount of accumulated savings.

Second, the popularity of Yu’E Bao is closely related to the less desirable performance

of other investment alternatives. In this study, we consider stock market investment as

the major alternative choice. China’s stock market is frequently described as “a casino

driven by speculations rather than end-investment” (Elliott and Yan, 2013). The term

“speculation” refers to the investors’ behaviour in purchasing a certain group of stocks

33

See Cooper and Zhu(2018) Household Finance in China, NBER Working Paper No. 23741 34

Variable income refers to uncertainty in the future revenue and it is often related to unpredictability and

instability of changes. 35

Consumption floor refers to the expected level of lowest consumption and it is an indicator of a

country’s social safety net.

49

which they believe will soon increase, spurring other investors to pay a higher price for

it. With little regard to the underlying value of the firms, the primary aim of speculation

is to make quick money rather than profit from long-term investment (Song and Xiong,

2017). Thus, the turnover rate36

is a direct reflection of speculative behaviours in the

market. Figure 5.2 illustrates the volatility of China’s A-share market and high turnover

rate.

Figure 5.2 Shanghai Stock Exchange Composite Index and Monthly Market Turnover Rate

Note: The Shanghai Stock Exchange Composite Index uses the right y-axis, while the

monthly market turnover rate uses the left y-axis.

Source: Song and Xiong (2017)

Regarding the Sharpe ratios, the major measurement of investment performance used in

our study, previous studies on China’s stock market return show a high mean return and

a high standard deviation37

. Recent research by Cooper and Zhu (2018) compares stock

market performances between China and the U.S. and report a 10.07% average return

with a standard deviation of 0.47 in China, while the U.S. experiences a 6.33% average

36

Turnover rate is calculated by dividing the total amount of shares traded in one period by the average

amount of shares outstanding. It measures the trading volume and liquidity of stock markets. 37

Fang, Gu, Xiong and Zhou (2015) reported a 7.3% average stock market return and a standard

deviation of 0.0515 during the year 2003-2013. For details, see “Demystifying the Chinese Housing

Boom," Working Paper 21112, National Bureau of Economic Research.

50

return with a standard deviation of 0.155. The authors argued that a lower risk-adjusted

return together with stock adjustment, high cost of stock market participation, and a

high variability in returns, shows that China’s stock market is still underdeveloped.

In short, we believe that the popularity of Yu’E Bao and other money funds is not only

attributable to the attractiveness of this single group of products itself but is also closely

related to the performance of the market alternatives and the availability of investment

products in the current market. We might expect a change if China’s stock market were

to make fundamental and significantly improvements, if Chinese investors were to

become more knowledgeable of the stock market or if other new, breakthrough

investment products were to appear in the market.

Relevant technological developments also contribute to Yu’E Bao’s superior popularity.

One major advantage Yu’E Bao holds over other money funds is that it is based on

Alipay, a leading digital payment platform developed by Chinese Internet giant,

Alibaba. Investors can freely access their Yu’E Bao’s account balance and use it as cash

in daily life through Alipay, which seems impossible for money funds provided by

traditional banks or those that can currently only be redeemed online. We also have

observed the rapid development of other money funds based on another Internet giant,

Tencent and their WeChat digital payment platform.38

Here, we draw the conclusion for our first research question regarding the popularity of

Yu’E Bao and other money funds: First, high saving ratios provide sufficient money for

Chinese investors to put in Yu’E Bao accounts and it is the basis of the large volume of

38

South China Morning Post (Jan 4 2015)“Tencent gets a licence to sell mutual funds to WeChat’s 1

billion users in China” Available at http://www.scmp.com/business/companies/article/2126876/tencent-

granted-licence-sell-mutual-funds

51

assets managed by China’s money fund markets. Second, the relatively underdeveloped

stock market with high volatility and a lower ratio risk-adjusted return leads to a lower

participation from Chinese investors. Therefore, Yu’E Bao and other money funds

become a more attractive investment choice. Thirdly, the combination of Internet

technology and a digital payment platform further boosts the popularity of Yu’E Bao.

Before moving on to the second research question regarding the impacts of money

market funds on financial system, we intend to provide some background information

on China’s financial system to facilitate our interpretation. For a long time, in contrast

to the U.S. and U.K., China’s financial system has been described as a “bank-based”

system instead of “market based” (Chan, Fung and Thapa, 200639

). In China, bond

financing and equity financing make up only one-fifth of the total credit for non-

financial institutions. Meanwhile, state-owned banks contribute more than 40% of total

bank deposits (Song and Xiong, 2017). In addition, the Chinese government has been

playing an active role in the country’s economic development and financial system

reform (Elliott and Yan, 2013). In this setting, we believe Yu’E Bao, or other Internet

Finance products, influences China’s financial system in four major ways.

First, the sheer size of assets managed under money market funds may take away some

bank deposits and therefore, have an impact on bank profitability and operation.

Additionally, the major business of China’s commercial banks is absorbing deposits and

offering loans; as a result, the primary source of profit is the spread between the deposit

39

In a bank-based financial system, as the case in Germany, banks play a crucial role in capital allocation,

saving mobilization, and risk management. In contrast, in a market-based financial system, such as the

financial system in the U.S., securities markets play a leading role in firms financing, corporate

governance, and risk management. The comparison between these two systems has been debated for a

long time under two disciplines, development economics and corporate finance. For details, See

Demirgüç-Kunt, Levine (1999)

52

rate and lending rate. If a substantial amount of money is moved from bank deposits to

money market funds, or other Internet Finance products such as P2P lending, the