Embed Size (px)

Citation preview

EmkayResearch

Piramal Life Sciences Ltd

Pure R&D Value Play

28th August, 2008

Paragon Center, H -13 -16, 1st Floor, Pandurang Budhkar Marg, Worli, Mumbai – 400 013. India

Init

iati

ng

Co

ve

rag

e

Manoj Garg

Research Analyst-Pharma

+91 22 6612 1257

Akshat Vyas

+91 22 6612 1491

BUY

Price TargetRs157 Rs270

Sensex - 14,048

Price Performance

(%) 1M 3M 6M 12M

Absolute (15) n.a. n.a. n.a.

Rel. to Sensex (17) n.a. n.a. n.a.

Source: Bloomberg

Stock Details

Sector Pharmaceuticals

Reuters PLSL.BO

Bloomberg PLSL@IN

Equity Capital (Rs mn) 255

Face Value (Rs) 10

No of shares o/s (mn) 25

52 Week H/L (Rs) 520/100

Market Cap (Rs bn/USD mn) 4/91

Daily Avg Vol (No of shares) 1110273

Daily Avg Turnover (US$ mn) 3.6

Shareholding Pattern (%)

30/6/2008

Promoters 58.8

FII/NRI 10.5

Institutions 13.2

Private Corp 7.0

Public 10.6

Source:Capitaline

Piramal Life Sciences Limited (PLSL), the demerged R&D entity of Piramal Healthcare

(PIHC) began operations a decade ago. PLSL today boasts of a world class drug discovery

facility, a strong pipeline of 15 molecules (half of them in Phase I and Phase II) and in-

licensing agreements with global innovator companies like Eli Lilly, Merck and Pierre

Fabre Laboratories. PLSL's innovation philosophy of finding a drug that is safe and

effective by focusing on well defined targets having strong commercial viability minimises

the risk associated with drug discovery research. Our risk adjusted DCF based NPV is

Rs270/share. From the infrastructure view, the company is a value play. The replacement

cost of its R&D facility is 50% of its current Enterprise Value (EV). PLSL trades at a

significant discount to its only comparable competitor, SPARC. Despite having a stronger

pipeline of 15 molecules as against 8 for SPARC, PLSL trades at a significant discount

(80%) to SPARC's market cap. We initiate coverage on the stock with a Buy rating and a

DCF based target price of Rs270.

Key Triggers

n Successful completion of Phase II trial for P276 by December ’08.

n Phase III trials on P276 are likely to be completed by mid to late 2009.

n Major milestone payment from Eli Lilly in 2010.

n Out-licensing deal for P1736 in 2011.

n Launch of P276 in US market by early 2011.

Impressive pipeline - significantly undervalued

PLSL has one of the most interesting innovation pipelines in the industry with 15 molecules in its kitty

out of which 7 molecules are in Phase I / II stages. By end FY09, the company expects one more

molecule to enter into human clinical trial. Our estimate for PLSL's NPV is Rs270/share. We believe

that the current price does not reflect the potential value of its R&D pipeline.

In-licensing revenues from FY09E, Out-licensing deal likely in FY11E

Besides the molecules invented in-house, PLSL is working on in-licensed molecules and targets. We

believe that In-licensed assets complement PLSL's own pipeline and enhance the probability of

success. PLSL already has in-licensing agreements with the three global innovator companies, a) Eli

Lilly b) Merck & c) Pierre Fabre Laboratories. We believe that from FY09E onwards, PLSL will start

generating revenues from its in-licensing deal (first installment of US$5mn from Eli Lilly). We also

believe that company will start monetising its impressive R&D pipeline over the next 18-24 months. We

believe that the out-licensing deal at an advanced stage will enhance the company’s credentials and

valuations as seen in Glenmark's case.

Robust business strategy of PLSL

PLSL works on known and unknown targets, but in order to minimise the high risk associated with

drug discovery, it ensures that it is one among the first five in that category. We believe that its

strategy of finding a drug that is safe and effective for unmet medical need by focusing on well

defined targets, where the chosen molecule is one among the first five in the category is an appropriate

strategy.

Valuations

Our risk adjusted DCF based NPV is Rs270/share. We believe that the current price does not reflect

the potential value of its R&D pipeline. On a replacement cost basis also, PLSL's valuations are

attractive. Despite having a stronger R&D pipeline of 15 molecules as against 8 molecules of SPARC,

it trades at a significant 80% discount to SPARC. Given its strong R&D pipeline (15 molecules, 7 in

Human clinical trials, NPV- Rs16473mn) and attractive valuations, we rate the stock a Buy with a

DCF based target price of Rs270. We expect significant value creation in the next 3-5 years.

Net Sales EBITDA PAT EPS ROE P/E EV/ P/BV

YE-Mar (Rs.mn) (Core) (Rs.mn) (Rs) (%) (x) EBITDA (x)

FY2008 0 -826 -917 -30.0 NA -5.2 0.0 4.3

FY2009 210 -864 -1,100 -36.0 NA -4.4 -1.5 -22.1

FY2010 1,050 -240 -439 -14.4 NA -10.9 -3.8 33.1

Financials

28 August, 2008 2Emkay Research

Piramal Life Sciences Initiating CoverageInnovative Pipeline

Innovative Pipeline

Well balanced innovative pipeline

PLSL has one of the most interesting innovation pipelines in the industry with 15 molecules

in its kitty, out of which 7 molecules are in Phase I / Phase II stages. By end FY09, the

company expects one more molecule, which has successfully completed toxicology studies

to enter into human clinical trials. The source of leads is not limited to the library of

synthetically developed chemical compounds. PLSL has a library of natural products,

comprising of 40,000 microbial strains and 5600 plants derived from the diverse habitat

of India. Out of 15 development programs, three are based on Phyto-pharmaceuticals

(which are derived from medicinal plants and herbs), as well as natural products generated

by microbial strains.

PLSL has one of the most interesting

innovation pipelines in the industry

with 15 molecules in its kitty, out of

which 7 molecules are in Phase I /

Phase II stages

PLSL's R&D snapshot

Source: Emkay Research

28 August, 2008 3Emkay Research

Piramal Life Sciences Initiating Coverage

Immediate Revenue stream - when and how?

In-licensing revenues from FY09E onwards, Out-licensing deal in FY11E

We believe that from FY09E onwards, PLSL will start generating revenues from its

in-licensing deals. We expect the first installment of US$5mn in FY09E (after successful

completion of Phase I of first target) and US$20mn in FY10E (after successful completion

of Phase II of first target and Phase I of first target) from Eli Lilly. We also believe that

company will start monetising its impressive R&D pipeline over the next 18-24 months,

leading to a re-rating of the company. Management has indicated that P-1736 (currently in

Phase-I, market potential ~US$4.5bn) and P276 in other indications (currently in Phase I/

II, market potential ~US$2.7bn) are the potential candidates for out-licensing. We believe

that the out-licensing deal, which is at an advanced stage (end of Phase II stage), will

enhance the credentials of the company and thus the value of the company. We have

witnessed a similar re-rating in Glenmark's case, where the intrinsic value of its R&D

pipeline increased multifold post out-licensing deals. Further, we believe that the value

creation will be higher in case of PLSL, as the out-licensing deal may be struck at a more

advanced stage of development. In order to enhance the intrinsic value of the company

significantly, the management plans to take few of its molecules in the oncology segment,

on their own in the US market. We also subscribe to a similar views as the pay-off is

potentially higher as seen in the case of Millenium Pharmaceuticals. Millenium

Pharmaceuticals, a US based oncology company, which has recently launched

Velcade for Multiple Myeloma (within two years, the drug has achieved US$800mn

sales) and has 4 other compounds in human clinical trial stages (oncology and

inflammation space) has recently been acquired by Takeda Pharmaceutical (Japan's

largest pharmaceutical company) for a total consideration of US$8.5bn.

Partnering with global leaders: pipeline expansion

Besides the molecules invented in-house, PLSL is working on in-licensed molecules

and targets. We believe that In-licensed assets complement PLSL's own pipeline and

enhance the probability of success. Moreover, it also provides a great learning opportunity

while working with world class innovator companies. Unlike most of the licensing deals,

where the in-licensor has to pay upfront milestone payment to acquire the development

and marketing rights of the drugs, PLSL works with innovators as a development partner.

Where PLSL does not pay any up-front fee in the in-licensing agreements, it bears the

pre-clinical and early stage (Phase I & II) development costs, while the partner is

responsible for late stage development (Phase III & IV), registration and launch in

developed markets. In-lieu of this, PLSL gets milestones on successful completion of

each stage and percentage royalty of global sales along with exclusive marketing rights

for India and / or additional South Asian Markets. We believe such deals provide higher

returns as the company (PLSL) is also sharing the development risks.

PLSL has already entered into in-licensing agreements with three partners, a) Eli Lilly b)

Merck & c) Pierre Fabre Laboratories

n Agreement with Eli Lilly - PLSL signed a drug development agreement to develop

and commercialize a select group of Lilly's pre-clinical drug candidates (two targets)

spanning multiple therapeutic areas. As per agreement, PLSL is responsible for

design and execution of the global clinical development program upto end of Phase

II and Eli Lilly will be responsible for Phase III, registration and launch worldwide

(excluding India and certain South Asian countries);

Revenue stream

PLSL believes that its strategy of

taking its oncology molecule on its

own to the market will enhance the

company’s intrinsic value significantly.

PLSL's In-licensing strategy

complements its own pipeline and

enhances the probability of success

28 August, 2008 4Emkay Research

Piramal Life Sciences Initiating Coverage

PLSL will receive the following:

n Milestone payments on successful completion of Phase I, II and III, aggregating

US$ 100 mn / each target

n Percentage royalty on global sales upon successful launch

n Exclusive marketing rights for India and certain neighboring countries

n R&D Agreement with Merck & Co - Merck & PLSL entered into a research and

development collaboration agreement to discover and develop new drugs for two

new oncology targets provided by Merck. PLSL will be responsible for carrying out an

integrated drug discovery program from hits to leads through pre-clinical candidate

selection, followed by investigational new drug (IND- involving non-clinical studies

and human clinical trials) demonstrating proof-of-concept, primarily for Oncology.

Merck will have an option to advance the most promising drug candidates into late

stage clinical trials and to commercialize these drug candidates. PLSL will receive

milestone payments on successful completion of Phase I, Phase II and III, aggregat-

ing US$175mn for each candidate plus percentage royalty on global sales upon

successful launch.

n R&D Agreement with Pierre Fabre Laboratories - In January 2008, PLSL entered

into a collaboration agreement with Pierre Fabre for research in oncology. The Pierre

Fabre Group will provide expertise in screening and research in oncology, while

PLSL will make available its natural products base, which will lead to the pharmaco-

logical characterisation of new molecules.

Key Triggers

n Successful completion of Phase II trial for P276 by December ’08.

n Phase III trials on P276 are likely to be completed by mid to late 2009.

n Major milestone payment from Eli Lilly in 2010.

n Out-licensing deal for P1736 in 2011.

n Launch of P276 in US market by early 2011.

Stake sale - benchmark for valuing the portfolio

We believe PLSL is likely to look for financing from strategic or financial investors, as its

cash balance is not enough to sustain the increasing R&D expenses because of its

growing pipeline. Its annual expenditure on R&D is likely to be in the range of Rs1200-

1400mn in the next 2-3 years.

The stake sale to these investors (strategic or financial) can form a benchmark for valuing

the portfolio. PLSL's management has indicated that it will not go for a large dilution in one

shot. The dilution is expected to be gradual and need based. Mr. Ajay Piramal has hinted

at a dilution of 10-15% of total equity. This ensures that the promoters retain control of the

research entity. With progress in clinical development, the portfolio value can increase

substantially over time. Management has indicated that because of current market

conditions, they may not go for immediate stake sale and till that time they can fund their

requirement through debts from the parent company.

Revenue stream

With progress in clinical development,

the portfolio value can increase

substantially over time

28 August, 2008 5Emkay Research

Piramal Life Sciences Initiating Coverage

Robust Business Strategy

From humble beginnings to best in class

PLSL commenced its drug discovery research journey 10 years ago, with the acquisition

of Hoechst R&D centre. Over the past five years, we have witnessed a substantial ramp-

up in its R&D efforts. We believe that these efforts have started yielding good results for

the company, as today, it boasts of one of the best innovation infrastructures in India. It has

built a world class drug discovery centre with its facility spread over 200,000 square

feet at Goregaon, Mumbai at an investment of over Rs1bn.The management has

indicated that a similar facility in Europe or US could cost anywhere between US$80-

90mn. Even in India, to build a similar facility at present, is likely to cost approximately

Rs2bn. At the CMP of Rs157, the enterprise value of the whole company is Rs4.0bn.

Currently, it has a competent team of over 309 scientists. So far, it has invested Rs4.2bn

on innovative R&D research.

Innovation Philosophy

PLSL works on known and unknown targets, but in order to reduce the high risk associated

with drug discovery, it ensures that it is one among the first five in that category. Working on

known targets not only reduces the overall drug development cost (as targets are already

defined) but also reduces the chances of failure and therefore, ensures "low risk and high

returns". Lipitor (Atorvastatin) is one of the best examples of known target, which was

developed by Pfizer and today, it is the world’s best selling drug with annual revenues of

over US$12.5bn. Besides expertise and understanding of target mechanism of action,

commercial viability is an important criterion for continuing development program at PLSL.

The company has made it a point that it should be among the first five in its class.

PLSL's key focus areas are based on the following criteria:

n Well defined and large unmet medical need

n An understanding of target mechanism of action and clinical pathway

n Leverage on strong In-house capabilities; and

n Commercial viability

PLSL's Innovation Philosophy

PLSL has built state of the art R&D

facility with an investment of

US$20mn. Similar facilty in US or

Europe will cost any where US$80-

100mn.

PLSL's innovation philosophy of

working on known targets is relatively

'low risk high returns' strategy

Source: Emkay Research

Robust Business Strategy

28 August, 2008 6Emkay Research

Piramal Life Sciences Initiating Coverage

PLSL is mainly focusing on four therapeutic areas- Oncology, Inflammation, Infectious

diseases and Diabetes.

Therapeutic focus area

Discovery and development strategy

We believe that its strategy of finding a drug that is safe and effective for unmet medical

needs is an appropriate strategy. PLSL focuses on relatively fast and well defined path,

having strong commercial viability. Its chosen molecule is generally one among the first

five in its category.

PLSL has stated that it will take new chemical entities (NCEs) from early discovery through

Phase II clinical trials in India and overseas and after that, pursue one of the following

pathways:

Develop to Proof-of-Concept: Then, Out-license

If a drug involves larger clinical trials like Anti-diabetic, Anti-inflammations, etc, PLSL will

out-license to global pharmaceutical companies after establishment of proof-of-concept

(up to Phase II). Management has indicated that by FY2011, they will out-license at least

one molecule (Depending upon the successful completion of upto proof of concept).

Carry-to-Market

If a product involves orphan drug status, niche indications or accelerated clinical trials

such as oncology drugs, PLSL will develop the compound to launch. PLSL has decided

to launch P276 and NPS 31807 on its own. The Phase 1 trials of P276 are quite encouraging

which has not only established the safety of the compound but also found effective in two

terminally ill patients.

Drug discovery strategy

Source: Company, Emkay Research

Robust Business Strategy

Source: Company, Emkay Research

PLSL focuses on relatively fast and

well defined path, having strong

commercial viability

28 August, 2008 7Emkay Research

Piramal Life Sciences Initiating Coverage

Valuation

Valuation of R&D assets

We have used risk adjusted DCF based methodology for valuing PLSL's pipeline, where

we have captured the high failure risk by assigning the probability of success (from 5% to

20%), depending upon the stage in which the molecule is. We have valued the R&D

portfolio in three steps

n NPV of R&D assets ex-R&D cost

n R&D cost required to develop these assets

n Adjusting for external fund requirement, either through equity dilution or debt

NPV of R&D pipeline

We have valued 8 own R&D assets that are in various stages of development, adopting

risk adjusted DCF method. The key assumptions we have taken are peak sales, probability

of launch, year of launch and discount rate. We have also done a scenario analysis

assuming discount rate at 13%, 15% and 20%.

NPV of R&D assets

Valuation

We have captured the high failure risk

by assigning the probability of

success

Molecule Current Mkt. Launch Peak sales Prob NPV

Size (US $mn) est est (US$ mn) (%) (Rs mn)

P 276 2700 2011 800 20 8453

P1446 2700 2015 800 10 1179

NPB-001-056 1600 2011 500 20 2341

Pxxx 1000 2017 300 5 135

Onco Natural 1100 2013 200 5

P979 7500 2016 1000 5 615

NPS31807 300 2011 100 20 781

P1539 pro drug 1000 2016 300 5

P1736 4500 2015 1000 10 1345

PM 1811104 4500 2016 200 5 69

NPV of Eli Lilly deal 50 725

NPV of Merck deal 50 831

Total 16473

Source: Emkay Research

Key assumptions in our risk adjusted DCF model to arrive at fair value.

a) We have assumed peak sales, probability and year of launch for each of the mol-

ecules separately.

b) We have assumed that after launch of the product in the market, peak sales will be

attained in the seventh year.

c) After achieving peak sales, we expect sales to remain flat for another five years and

gradually to come down till the patent expiry. We have not taken any sales post patent

expiry.

d) Average PBT margin of 50% (for own launches) and mid-teen royalties for out-licens-

ing candidates.

e) We have done a scenario analysis at different discount rates (13%, 15% and 20%).

We have valued 8 R&D assets that

are in various stages of development,

adopting risk adjusted DCF method

28 August, 2008 8Emkay Research

Piramal Life Sciences Initiating Coverage

R&D expenses to develop portfolio

In order to arrive at a fair value we have deducted the R&D cost which PLSL is going to

incur to develop the R&D portfolio. We believe that the R&D cost is going to increase at a

CAGR of 20% over FY08-15E because of large numbers of molecules entering into

advanced clinical stages. Our development cost per molecule after adjusting for the

probability of success is Rs8209mn or US$198mn (our average R&D success rate is

11.5% and we have calculated the NPV of 8 molecules). We believe this a reasonable

assumption.

Impact of external funding in valuations

We believe that company will dilute a stake of 20% over the next 2 years, either in single or

multiple tranches. While valuing the R&D portfolio, we have considered the extended

equity of 30.5mn shares.

Valuation of R&D Assets (Rs mn)

NPV of R&D pipeline 16473

R&D spend (NPV) 8209

Net R&D value 8264

No. of shares (mn) 25.5

No. of shares - Post Dilution (mn)* 30.5

R&D value/per share if it dilute equity (Rs) 270

CMP (Rs) 157

Upside (%) 72%

*Assuming company will dilute 20% equity

Source: Emkay Research

We value PLSL at Rs270/share (at 15% Discount Rate). We believe that an out-licensing

deal for its R&D products will act as a catalyst, which would lead to higher valuations of the

company. Besides, the positive outcome of Phase II trials for P276 would lend credence

to the company's pipeline.

Scenario Analysis

Discount Rate 13% 15% 20%

NPV of R&D 19536 16473 11141

R&D expenses 8771 8209 7036

Net R&D Value 10764 8264 4106

NPV at current Equity 422 325 161

NPV per share post dilution 352 270 134

Source: Emkay Research

R&D pipeline - an attractive value proposition

We strongly believe that the current price does not reflect the potential value of PLSL's

R&D infrastructure. The company has invested almost Rs1bn to build a world class drug

discovery centre, spread over 200,000 square feet. Management has indicated that if one

build a similar facility in Europe or US, it will cost anywhere US$80-90mn. Even in India,

if today one want to build similar facility, it will cost approx. Rs2bn. At the CMP of Rs157, the

enterprise value of the whole company is Rs4.0bn. So practically the investors are getting

one of the best R&D infrastructures (15 molecules, 7 in Human clinical trial, NPV-

Rs16473mn) at Rs2.0bn, where company itself has pumped in Rs4.2bn in last 5 years for

the development of these assets. At CMP of Rs157, the stock is available at a significant

discount to its NPV and can provide an upside of 72% from the current price.

Valuation

Our development cost per molecule

after adjusting for the probability of

success is Rs8209mn or US$198mn

R&D pipeline- With its R&D

infrastructure replacement cost of

Rs2bn, PLSL available with a Mcap

of Rs4.0bn

28 August, 2008 9Emkay Research

Piramal Life Sciences Initiating CoverageValuation

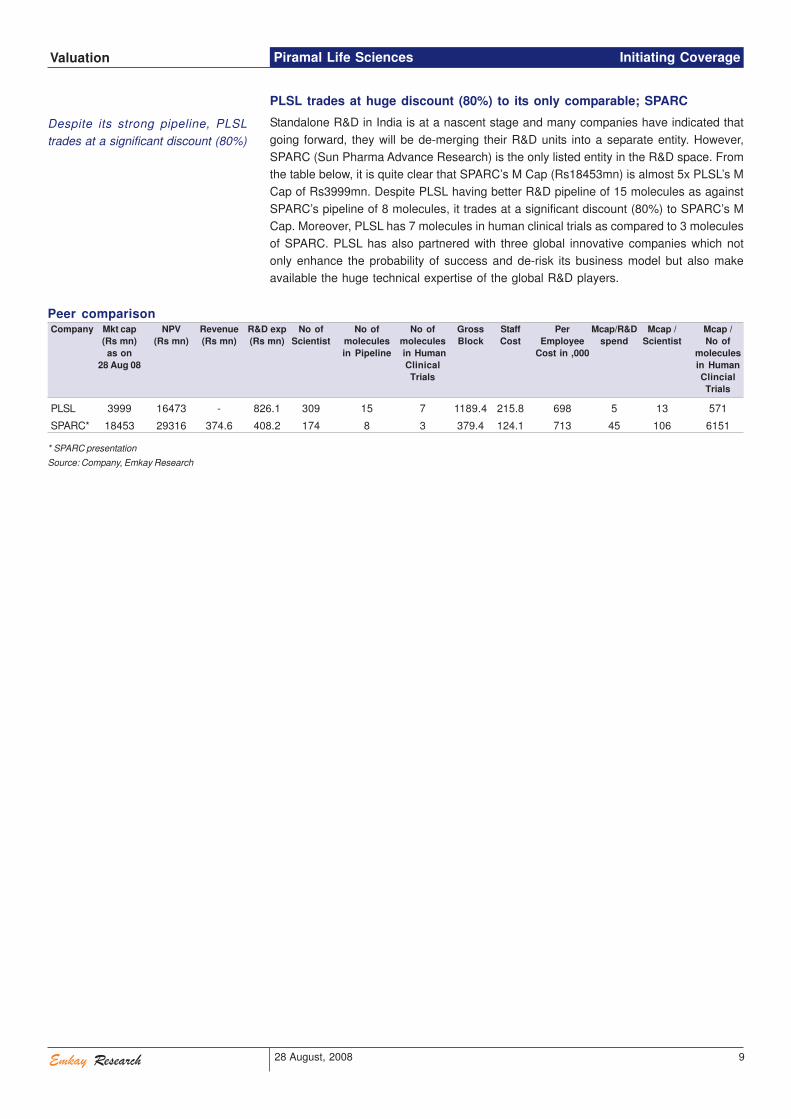

PLSL trades at huge discount (80%) to its only comparable; SPARC

Standalone R&D in India is at a nascent stage and many companies have indicated that

going forward, they will be de-merging their R&D units into a separate entity. However,

SPARC (Sun Pharma Advance Research) is the only listed entity in the R&D space. From

the table below, it is quite clear that SPARC’s M Cap (Rs18453mn) is almost 5x PLSL’s M

Cap of Rs3999mn. Despite PLSL having better R&D pipeline of 15 molecules as against

SPARC’s pipeline of 8 molecules, it trades at a significant discount (80%) to SPARC’s M

Cap. Moreover, PLSL has 7 molecules in human clinical trials as compared to 3 molecules

of SPARC. PLSL has also partnered with three global innovative companies which not

only enhance the probability of success and de-risk its business model but also make

available the huge technical expertise of the global R&D players.

Peer comparisonCompany Mkt cap NPV Revenue R&D exp No of No of No of Gross Staff Per Mcap/R&D Mcap / Mcap /

(Rs mn) (Rs mn) (Rs mn) (Rs mn) Scientist molecules molecules Block Cost Employee spend Scientist No of

as on in Pipeline in Human Cost in ,000 molecules

28 Aug 08 Clinical in Human

Trials Clincial

Trials

PLSL 3999 16473 - 826.1 309 15 7 1189.4 215.8 698 5 13 571

SPARC* 18453 29316 374.6 408.2 174 8 3 379.4 124.1 713 45 106 6151

* SPARC presentation

Source: Company, Emkay Research

Despite its strong pipeline, PLSL

trades at a significant discount (80%)

28 August, 2008 10Emkay Research

Piramal Life Sciences Initiating Coverage

Key Risks

Drug discovery is a high risk high return business

Drug-discovery research involves substantial risk due to high failure rates and

uncertainties surrounding discovery and development of newer and better medicines.

Thereby, it becomes difficult to predict the outcome of each compound and plot future

projections. Besides, drug discovery is a long process, which usually takes 8-10 (or

more) years for introducing a compound in the market, provided things proceed within

plan, which is rare. A company would need to maintain a healthy balance between risk

and return for long-term success. We believe that PLSL's innovation strategy of focusing

on relatively fast and well defined targets is likely to ensure success.

Investing in drug discovery - Needs huge risk appetite

Investing in a drug discovery company needs huge risk appetite, given its unique, high-

risk high-return nature. Besides, the complex nature of the business proves difficult for

investors to understand the dynamics of science and commerce involved. We consider

quality of pipeline and evaluation of underlying risks coupled with experienced scientific

team to be most critical for a profitable investment.

Retention of scientists

Human assets play a very critical part towards the success or failure of any company and

it holds true for PLSL also. PLSL today has 309 scientists in its team out of which 10% of

them have worked with global innovator companies. The average experience of senior

scientists team is around 10 years. The retention of highly skilled scientists is a big

challenge for the company. However, in the last three years, PLSL has been able to retain

most of its senior scientists. The overall attrition rate in PLSL is 18% because few of the

people have left to pursue higher studies. Adjusting this the attrition rate is just 8% (people

left to join other companies)

Key Risks

28 August, 2008 11Emkay Research

Piramal Life Sciences Initiating CoverageFinancials tables

Income Statement

Y/E,Mar (Rs. mn) FY08 FY09E FY10E

Net Sales 0 210 1050

Growth (%) 400

Expenses (826) (1074) (1290)

Growth (%) 30 20

Other Operating Expense 826 1074 1290

EBIDTA (826) (864) (240)

Growth (%) 5 (72)

Other income 1 0 0

Interest (2) 127 87

Depreciation 91 107 111

PBT (915) (1098) (437)

Total Tax 2 2 2

Effective tax rate (%) 0 0 0

PAT (917) (1100) (439)

Source: Emkay research Source: Emkay research

Cash Flow Statement

Y/E, Mar (Rs. mn) FY08 FY09E FY10E

Pre-tax profit (915) (1098) (437)

Depreciation 91 107 111

Chg in working cap 1020 0 0

Tax paid (2) (2) (2)

Operating cash Inflow 193 (993) (329)

Capital expenditure (198) (86) (43)

Free Cash Flow (4) (1079) (372)

Investments 0 0 0

Equity Capital Raised 0 0 765

Loans Taken / (Repaid) 0 1270 (400)

Dividend (incl tax) (1) 0 0

Others 7 0 0

Increase in Msc Exp 0 0 0

Net chg in cash 2 191 (7)

Opening cash position 0 2 193

Closing cash position 2 193 186

Ratios

Y/E, Mar FY08 FY09E FY10E

Profitability (%)

EBIDTA margin NA NA NA

PAT margin NA NA NA

ROCE NA NA NA

ROE NA NA NA

Per share data (Rs.)

FDEPS (30) (36) (14)

CEPS (32) (26) (7)

BVPS 36.1 (7) 6

DPS (Rs) 0.0 0.0 0.0

Valuations

P/E (5) (4) (11)

Cash PE (4) (6) (22)

P/BV 4.3 (22) 33

EV / Net Sales 6.2 0.9

EV / EBITDA 0.0 (2) (4)

Dividend Yield (%) 0.0 0.0 0.0

Turnover (x) Days

Debtors T/O 0.0 0.0 0.0

Inventory T/O 0.0 0.0 0.0

Gearing Ratio

Total Debt/Equity (x) 0.0 (7) 6

Source: Emkay research

Balance Sheet

Y/E, Mar (Rs. mn) FY08 FY09E FY10E

Equity share capital 255 255 305

Reserves & Surplus 1582 1582 2296

Networth 1837 1837 2601

Deferred tax liability 67 67 67

Diventure/pref. Share 0 0 0

Loan Funds 0 1270 870

Total Liabilities 1904 3174 3538

Gross Block 1189 1479 1522

Less: Depreciation 288 395 506

Net block 902 1084 1016

Capital work in progress 204 0 0

Current Assets 23 214 207

Inventories 8 8 8

Sundry debtors 0 0 0

Cash & bank balance 2 193 186

Loans & advances 14 14 14

Other assets 0 0 0

Current liabilities 142 142 142

Current liabilities 127 127 127

Provisions 15 15 15

Net current assets (119) 72 65

Profit loss (Debit balance ) 917 2017 2456

Total Assets 1904 3174 3538

Source: Emkay research

28 August, 2008 12Emkay Research

Piramal Life Sciences Initiating Coverage

Annexure-I

Industry snapshot

The Indian pharmaceutical industry has evolved substantially and transformed itself from

a reverse engineering led industry, focused on the domestic markets- to a research

driven, export oriented industry with a global presence.

After transforming the global generic industry, the Indian pharma industry is poised to play

a decisive role in redefining the global drug discovery paradigms. We believe that with its

high quality and low cost scientific skills, India has the potential to become a key R&D

player in the global pharma value chain. Availability of high quality research scientists at 1/

5th of the comparable cost in the US makes India an attractive destination for R&D.

Product patent implementation from 2005 coupled with government incentives for R&D,

has also provided impetus to discovery R&D.

Research is steadily becoming an integral part of the strategy of Indian pharma companies,

who want to build a sustainable long term advantage. Over the last couple of years, the

discovery R&D segment has gained significant momentum and discovery R&D pipelines

of several players have expanded substantially. At present, as many as 11-12 companies

have molecules under various stages of development. R&D spending by Indian companies

as a percentage of sales has increased significantly in the past five years, from 2% to 8%.

R&D spends of major companies have grown at a CAGR of 38% over 2001-2006. With

robust activities on the R&D front, the Associated Chambers of Commerce and Industry of

India (ASSOCHAM) has indicated that the R&D spending of the Indian pharmaceutical

industry will reach about 9-10% of revenues by the year 2010.

Three main changes have taken place over the years for the Indian pharmaceutical industry:

a) Change in IP (intellectual property) regime- from process to product based

b) Co-options- Focus on alliances (be it licensing, contract research and manufactur-

ing, co-development, co-marketing, etc.) as a means to grow and sustain business

c) Indian companies going global- Adoption of inorganic avenue of growth

India's competitive advantage in offering strong chemistry innovation skills at significantly

lower costs has lured many multinational innovator pharma companies to make India a

major component of their global drug delivery value chain.

Declining R&D productivity, drying R&D pipeline, patent expirations of block buster drugs

coupled with pressure on margins has forced global pharmaceutical companies to revisit

their business strategies.

Global discovery and clinical research outsourcing is expected to increase from US$18bn

in 2006 to $33bn by 2010 (CAGR 16%). As per Kolorama information, the outsourcing

proportion for US pharmaceuticals had increased substantially from 10% in 1997 to 33%

in 2005. This proportion is expected to further rise to 41% by 2009, implying a CAGR of

16.5% in R&D outsourcing.

Annexures

28 August, 2008 13Emkay Research

Piramal Life Sciences Initiating Coverage

Annexure-II

R&D snapshot

Sourc

e: E

mkay R

esearc

h

Annexures

28 August, 2008 14Emkay Research

Piramal Life Sciences Initiating Coverage

Annexure-III

PLSL product pipeline

CDK Inhibitors

Cyclin dependent kinase (CDK) inhibitors are a new class of drugs that are being developed

for the treatment of cancers. Cancer continues to be a killer disease throughout the world

and is the second leading cause of death after cardiovascular diseases. All multiplying

cells have to go through a process called as 'cell cycle'. The CDK complexes play an

important role in regulation of cell cycle progression. Slowing down the Cyclins/CDKs

therefore offers a potential mechanism for treatment of cancer.

Market size: The potential market for the CDK4 inhibitor is around US$2700mn. At present,

Piramal Lifescience is developing 2 CDK inhibitors, belonging to the Oncology segment

(P276 & P1446).

P276

The P276 inhibitor is in Phase II clinical trials. The P276 is an injectable. P276 is a flavone

that inhibits CDK’s and has been identified as a novel antineoplastic agent. P276 is a

novel potent small molecule flavone derived selective CDK 4-D1, CDK1-B and CDK9-T

inhibitor, with potent cytotoxic effects against tumor cell lines.

PLSL has also initiated a phase I/II study in Multiple Myeloma (cancer of a specific type of

white blood cells) across 5 centres in India, in addition to a phase I study in multiple

myeloma to be conducted across three centers in USA. The Phase 1 trials of P276 are

quite encouraging which has not only established the safety of the compound but also

found effective in two terminally ill patients.

Multiple Myeloma (MM), a cancer of bone marrow, is generally considered incurable and

complete remission is possible only in 5% of the patients. The drugs present blockbuster

potential. For instance, Lenalidomide, a derivative of Thalidomid, the latest MM drug

approved in the US, is expected to reach peak sales of US$2,500 mn in the US in 2013.

Given the criticality of the drugs, fast track approval can be obtained for these drugs from

the USFDA. For instance, Velcade (Bortezomib) was approved in less than four months by

the US FDA.

PLSL management expects Phase II results for P276 by late 2008 and Phase III by mid-

2009 in Multiple Myeloma. Management expects to obtain an orphan drug status (orphan

drug is one which meets significant unmet medical needs and is useful to treat rare

disease) and a fast track approval for the same. The Phase III trials shall be limited to

250-300 patients. The overall cost shall be limited to less than US$15mn. We expect

Piramal to launch this molecule by 2011. Company is planning to launch this molecule on

its own in Multiple Myoloma and has indicated that launch cost in US would be around

US$20-30mn.

Management has indicated that they will be shortly conducting Phase II trials for other

indications such as Head & Neck cancer, Mantle cell Lymphoma and Malignant Melanoma.

They (management) has also indicated that they may go for out-licensing of P276 in other

indications once it will be through to Phase II stage.

The company also plans initiating studies of P276 in combination with gemcitabine

(which is already approved for the treatment of pancreatic cancer) and in combination with

radiation.

Annexures

28 August, 2008 15Emkay Research

Piramal Life Sciences Initiating Coverage

P1446

P1446 has just entered into Phase I clinical trials. P1446, the oral drug, is estimated to

enter the market 18-24 months after the launch of P276. P1446 is a novel, selective and

potent inhibitor of CDK4 D1, CDK1 B and CDK9 T. This molecule would serve as a back-

up molecule for P276. P1446 effectively slows down the proliferation of and induces

cytotoxicity on both sensitive and resistant cells without any significant cytotoxicity to normal

human cells. Additional phase I study to explore a continuous dosing schedule is also

being planned to be initiated in North America. Management has indicated that they may

launch this molecule on there own as a natural follow-up of the follow-up of P276.

Competing products are as follows

CDK Inhibitor Sales Expected Peak Exp Peak

Drug 2007 ($ mn) sales ($ mn) Sales year

Thalomid (Thalidomid) 447 433 2006

Revlimid (Lenalidomide) 774 2500 2013

Velcade (Bortezomib) 800 2000 2014

Gleevec resistant drug (NPB-001-05)

CML (chronic myelogenous leukemia) is a malignant cancer of bone marrow resulting in

abnormal growth in white blood cells. CML is a slowly progressing disease, in which too

many white blood cells (not lymphocytes) are made in the bone marrow. CML accounts for

almost 15% of all leukemias with 4000-5000 new cases being diagnosed every year in

the US alone.

The current medical therapy of CML includes tyrosine kinase inhibitors such as Gleevec

(Imatinib mesylate), Sprycel (Dasatinib), Tasigna (Nilotinib), Interferon-alpha and

cytoreductive agents such as Hydroxyurea, Busulfan, Cytarabine and their combinations.

Gleevec has emerged as a standard therapy of CML with significant improvement in

remission and survival rate. The survival rate has gone up from 35% in 2001 (prior to

Gleevec approval) to about 90% in 2006 (after the Gleevec approval). Although effective

and durable, the emergence of resistance and intolerability to tyrosine kinase inhibitors is

the biggest drawback of continued therapy with them.

Though Gleevec has been a successful drug, cases of Gleevec resistance are reported

in patients with advanced stage disease. Mutation of the target is the major cause of

resistance, which impacts drug binding. The most troublesome mutant is believed to be

T315I, which is found in almost 20% of the cases. The other therapies which were recently

approved against Gleevec resistant cases for CML are Sprycel (Dasatinib) and Tasigna

(Nilotinib). Though these drugs inhibit the Bcr-Abl mutants that Gleevec fails to bind to

because of mutation, however, even these molecules fail to inhibit the mutant T3151.

PLSL's drug NPB-001-05 has shown effectiveness in T3151 xenograft. The drug is being

developed as an oral formulation.

Market size: The potential market for the Bcr-Abl is around US$1600mn.

NPB001-05, a Phytopharmaceutical Gleevec resistant drug, is an oral liquid and has

demonstrated tyrosine inhibitor properties. The Phase II data shall throw more light on

efficacy of the drug. PLSL's management expects more information on NPB-001-05 to be

available in September 2008.

Annexures

28 August, 2008 16Emkay Research

Piramal Life Sciences Initiating Coverage

PLSL's product (NPB-001-05) is a phytopharmaceutical (plant-based product). The

regulatory hurdle shall be to establish consistency and repeatability of the manufacturing

process. PLSL remains confident that it can overcome the hurdle to obtain the USFDA

approval. PLSL plans to launch this molecule first in India by 2010 and a year later in US

(2011).

Competing products are as follows

Bcr-Abl

Sales Expected Peak Exp Peak

Drug 2007 ($ mn) sales ($ mn) Sales year

Sprycel (Dasatinib) 158 700 2015

Tasigna (Nilotinib)* 29 750 2016

Gleevec 3100

Source: Company, Emkay Research *Sale of H1CY08

Inflammation (NPS31807)

TNF Alpha is a protein manufactured by white blood cells to stimulate and activate the

immune system in response to infection or cancer. Overproduction of this compound can

lead to disease, where the immune systems act against healthy tissues, such as arthritis

or psoriasis. Some treatments for these diseases utilize drugs that bind and inactivate

TNF alpha, thereby reducing unhealthy inflammation. Rheumatoid arthritis (RA) is a chronic,

systemic, inflammatory disease affecting 1% of general population and leads to significant

disability and a consequent reduction in the quality of life. TNF-alpha is one of the major

mediators and has a potential role in the establishment of inflammation in the joints and

its eventual destruction. The novel drugs useful in Rheumatoid Arthritis are targeted

against TNF-alpha.

Successful biologic drugs have been developed to treat rheumatoid arthritis (RA) that

inhibit TNF alpha. These include Enbrel (2007 sales: US$3200 mn), Remicade (2007

sales: US$3327 mn) and Humira (2007 sales: US$3000 mn), which have all reached

blockbuster status. These drugs are reckoned as significant achievement in the treatment

of RA. These three drugs account for 98% of the RA treatment market in the US in value

terms. Biologics are difficult to manufacture and administer, and there are issues with

accessibility and compliance. Moreover biologics drugs are not only very costly but also

lead to reactivation of Tuberculosis.

A small molecule TNF alpha inhibitor can address many of these issues. However, the

advantages with biologics are its quick action and longer stay in the body. The small

molecules may have toxicity issues.

Small molecules are being developed by various companies in an attempt to overcome

the drawback of biologics. Please note that the small molecules are not necessarily TNF

alpha inhibitor only.

P979

PLSL is developing a small TNF alpha molecule P979 for various inflammatory

conditions - RA, psoriasis, and ankylosing spondylitis. The molecule is known to inhibit

TNF alpha and IL 6. The molecule has successfully completed toxicology study and is

likely to enter Phase I by year end (2008). It has been found effective in animal models of

RA. PLSL also has a number of back-up molecules in this category. Management has

Annexures

28 August, 2008 17Emkay Research

Piramal Life Sciences Initiating Coverage

indicated that this could be a potential target for outlicensing in FY2012. The potential

market for P979 is US$7.5bn.

NPS31807

PLSL is developing a phytopharmaceutical drug (NPS31807), which is an oral monoherbal

extract formulated in capsules. NPS31807 has shown better efficacy than Enbrel, a high-

priced bio-therapeutic. PLSL has completed one pilot Phase II study in Rheumatoid

Arthritis and other study in Rheumatoid Arthritis is nearing completion. Also the Phase II

study in Psoriasis is ongoing. Following are the competing products in the same category

Competing products are as follows

Drugs for RA- Biologics Sales

2007 ($ mn)

Enbrel (Etanercept) 3200

Remicade (Infliximab) 3327

Humira (Adalimumab) 3000

Source: Company, Emkay Research

Metabolic Disorder

Metabolic Disorder means disorders caused by problems with chemical processes in

the body. Similarly, Obesity is a condition with chronic nutritional imbalance. It is emerging

as a global outbreak of concern due to its high association with metabolic co-morbidities.

In the US alone, the prevalence of obesity has increased from 15% (1976-1980 NHANES

survey) to more than 32% (2003-2004 NHANES survey) in the adult population.

The current treatment recommendations for obesity include lifestyle changes in terms of

diet and physical activity for the mildly obese. The only two drugs approved for long-term

use in obesity are Sibutramine and Orlistat. These drugs are known to affect a weight loss

of only 5-10% on chronic administration.

P1201-07

P1201-07 is an orally active compound with selective actions against specific receptors

in the brain. It has been found to reduce food intake in the rodent model on short term as

well as long term administration. A drug being developed against this target has shown

efficacy in large phase II studies and is currently undergoing phase III trials in the US. After

completing the necessary studies to evaluate the toxicity in animals, Piramal Lifescience

has completed the first phase I study with P1201-07 in healthy overweight or obese

subjects in Europe to determine the safety, tolerability, pharmacokinetics and

pharmacodynamics of this drug. A phase II clinical study involving 3 months administration

of P1201-07 would later be conducted after ascertaining the safety and tolerability in

multiple dose study.

Type 2 Diabetes Mellitus

Diabetes is a life-long disease, marked by high levels of sugar in the blood. There are 3

types of diabetes i.e. Type1 Diabetes, Type 2 Diabetes and Gestational Diabetes. Type1

diabetes is usually diagnosed in childhood.

Annexures

28 August, 2008 18Emkay Research

Piramal Life Sciences Initiating Coverage

Type 2 diabetes is far more common than Type1 and makes up most of all cases of

diabetes. It usually occurs in adulthood. The pancreas does not make enough insulin to

keep blood glucose levels normal, often because the body does not respond well to the

insulin. Many people with Type 2 diabetes do not know they have it, although it is a serious

condition. Type 2 diabetes is becoming more common due to the growing number of

older Americans, increasing obesity and failure to exercise. About 20 mn Americans have

Type 2 diabetes and an additional 54 million have pre-diabetes. According to a 2007 study

by the U.S. Centers for Disease Control, the prevalence of Type 2 diabetes has been

increasing by 5% each year since 1990.

India is the world capital of Type 2 diabetes and this can be justified with the number of

diabetics estimated at 40 million in India in 2007 and this number is predicted to rise to

almost 70 million people by 2025. It is estimated that every fifth person with diabetes will

be an Indian and one of the factor could be the rising rates of obesity. WHO estimates that

mortality from diabetes, heart disease and stroke cost about $210 billion in India in the

year 2005. Current drugs such as Thiazolidinediones (TZDs) are associated with adverse

events such as weight gain, fluid retention, hepatotoxicity and possibly myocardial

infarction. Some of the adverse effects of TZD drugs are attributed to the peroxisome

proliferator activated receptor (PPAR gamma) activation by these agents. Therefore, a

safer agent that reverses insulin resistance by other (non-PPAR gamma activity)

mechanisms may be preferred as anti-diabetic therapeutics.

P1736-05

P1736, developed by PLSL, is an oral non-PPAR gamma insulin sensitizer. Currently, the

molecule is in Phase I. Management expects to finish Phase II studies by April 2009.The

potential market size is around $4.5bn and following are the competing products.

Competing products are as follows

Type 2 Diabetes Mellitus

Sales

Drug 2007 ($ mn)

Avandia (Rosiglitazone) 377

Actos (Pioglitazone) 2786

Source: Company, Emkay Research

Dermatophytes

Dermatophytes are a group of fungi that under most conditions, have the ability to infect

and survive only on dead keratin, found on the top layer of the skin, the hair, and the nails.

It cannot survive on moist skin found inside the mouth or the vagina. It is also responsible

for the majority of skin, hair, and nail fungal infections. Dermatophytes of the genera

Trichophyton and Microsporum are the most common causative agents.

NPH30907

PLSL is developing a molecule (NPH30907), a good anti-dermatophyte activity against a

panel of microorganisms. The company has completed clinical study to prove the efficacy

of 5% NPH30907 cream, as an anti-dermatophyte formulation in patients with localized

tinea lesions and is exploring options to commercialize the same. Tinea, also known as

Ringworm, is a common contagious fungal infection of the skin. The potential market is

around US$100mn and the competing product is Ketaconazole class compounds (Nizoral).

Annexures

28 August, 2008 19Emkay Research

Piramal Life Sciences Initiating Coverage

Anti-infective portfolio (PM-181104)

Antibiotic resistance is a common phenomenon and the pharmaceutical industry has

overcome this challenge by developing a new class of compounds. Stephalococus Aureus

is one of the more resistant pathogens. It was the first bacteria in which penicillin resistance

was found. Methicillin and later oxacillin were then introduced but they also developed

resistance in certain cases. Now methicillin-resistant Stephalococus Aureus (MRSA) is

quite common. It is now believed that almost half the Stephalococus Aureus infections are

resistant to penicillin, methicillin, tetracycline and erythromycin. This led to the development

of vancomycin. But soon, vancomycin-resistant strains of Stephalococus Aureus (VRE)

were found. Thereafter, new class of antibiotics called oxazolidones was developed in

1990. Linezolid was the first commercialized oxazolidones and resistance to the same

was reported in 2003.

PM181104

PM-181104 is a first-in-class compound and has a totally new structure, according to the

management. It has completed the toxicology studies and is expected to enter clinical

trials by Q3 2008 This would be followed by a 14 day phase II study in patients with MRSA

infections. The potential market is around US$500 mn. It is highly potent and effective

against all tested strains of S. aureus, including MRSA and MSSA strains.

Annexures

28 August, 2008 20Emkay Research

Piramal Life Sciences Initiating Coverage

Annexure-IV

Out-licensing Deals in early drug development phase

Company Molecule Therapeutic Stage at Potential Partner Upfront Additonal

Segment which it was deal size Payment payment

outlicensed

Glenmark GRC 6211 Pain Management Phase II $350mn Eli Lilly $45mn $305mn

Glenmark GRC 8200 Diabetes Phase II $280mn Merck $28mn $252mn

Isis Pharma ISIS 325568 Diabetes Drug Pre-Clincial $275mn Ortho-McNeil, $45mn $230mn

and ISIS studies J&J co.

377131

Glenmark GRC 3886 Asthmna / COPD Phase I $190mn Forest labs $10mn $190mn

$53mn Tejin $6mn $47mn

KAI Pharma KAI-9803 Cardiovascular Phase I/II $217mn BMS $25mn $192mn

Disease

Roche KOS-862 Oncology Phase I $210 Kosan $30mn $180mn

(R1492)

Vertex Pharma VX-680 Oncology Phase II $350mn Merck $101mn $249mn

VX-689 Oncology Preclincial

Astex Oral cell cycle Oncology Pre-Clincial $520mn Novartis $25mn $495mn

Therapeutics inhibitor studies

Vertex Pharma Telaprevir Investigational Clinical studies $380mn Janseen $210 mn $170mn

oral inhibitor of Pharmaceuticals

hepatitis C virus

protease

Source: Emkay Research

Annexures

28 August, 2008 21Emkay Research

Piramal Life Sciences Initiating Coverage

Annexure-V

Profiles and valuations of international R&D Companies

We have highlighted some of the small and mid-sized companies, who have scored big

with a single or couple of new molecules

Vertex Pharmaceuticals is a company with drug development programmes, focusing on

hepatitis C, HIV infection, oncology and cystic fibrosis. Vertex has 10 molecules in various

clinical stages, out of which Fosamprenavir calcium, an HIV protease inhibitor, is being

marketed through collaboration with GlaxoSmithKline, under the trade name Lexiva in the

United States and under the trade name Telzir in the European Union. It has eight molecules

in human clinical trial stages (1 in Phase III III ~ HCV infection, 3 in Phase II ~ 1 in cancer,

1 in cystic fibrosis, 1 in RA & 2 in Phase I) and 4 are in Phase I. Vertex has granted the

marketing rights of its lead candidate Telaprevir to Jansen Pharmaceuticals for ROW

markets, excluding North America & Far East, for a total consideration of $380mn, including

an upfront payment of $165mn plus $45mn research fund. Similarly, for the Far East

market, Vertex has tied up with Mitsubishi Tanabe Pharma Corporation for a total

consideration of $33mn milestone payment, while for the NA market, it has kept the

marketing rights with itself. For cancer molecules (VX-680 ~ currently in Phase II & VX-689

~ Preclinical candidate)), Vertex has granted the marketing rights to Merck for a total

consideration of US$350mn, including an upfront payment of $85mn plus $15.8mn

research fund. For another oncology molecule ~ VX-944 ~ Phase II candidate ~ Vertex has

tied up with Avalon Pharmaceuticals and has received $5mn upfront payment so far.

Vertex Pharmaceuticals was founded in 1989 and is headquartered in Cambridge,

Massachusetts.

Vertex

(US $M) 2005 2006 2007

Revenue 160.9 216.4 199

R&D spend 248.0 371.7 513.1

Net profit (loss) (203.4) (206.9) (391.3)

EPS (US$) (2.3) (1.8) (3.0)

M Capitalisation 2742 4699 3073

No. of drug candidates in pipeline 12

Cash & cash equivalent 361 704 460.7

M cap / R&D expense 11.1 12.6 6.0

M cap / Cash 7.6 6.7 6.7

M cap/ Sales 17.0 21.7 15.4

Source: Company, Emkay Research

Rigel Pharmaceuticals engages in the discovery and development of novel, small-

molecule drugs for the treatment of inflammatory/autoimmune diseases, cancer, viral

and metabolic diseases. Rigel has 4 molecules in clinical stages, out of which R788 is in

Phase 2 clinical trial for the treatment of rheumatoid arthritis (RA) and immune

thrombocytopenia purpura (ITP). Another molecule, R348 is in Phase 1 clinical trial for the

treatment of immune indications, such as psoriasis, RA, transplant rejection, and graft vs.

host disease. Its products also include R763, which is in Phase 1 clinical trial in the area

of oncology; and R343, a Phase 1 clinical trial product for asthma. Rigel Pharmaceuticals

has collaboration agreement with Merck Serono for R763, for which it has received $18.5mn

as upfront and milestone payment. Similarly it has collaboration agreement with Pfizer for

R343 and has already received $10mn as upfront and milestone payment so far. It has

Annexures

28 August, 2008 22Emkay Research

Piramal Life Sciences Initiating CoverageAnnexures

also tied up with other pharmaceutical companies like Johnson & Johnson, Novartis

Pharma and Daiichi Pharmaceuticals. The company was founded in 1996 and is based

in South San Francisco, California

Rigel

(US $M) 2005 2006 2007

Revenue 16.5 33.5 12.6

R&D spend 52.0 57.0 70.4

Net profit (loss) (45.3) (37.6) (74.3)

EPS (US$) (2.1) (1.5) (2.6)

M Capitalisation 202 298 788

No. of drug candidates in pipeline 4

Cash & cash equivalent 138.2 104.5 108.3

M cap / R&D expense 3.9 5.2 11.2

M cap / Cash 1.5 2.9 7.3

M cap/ Sales 12.2 8.9 62.6

Source: Company, Emkay Research

Cardiome is a company with drug development programmes focusing on the

cardiovascular segment. It has one antiarrhythmic drug, Vernakalant (iv) ~RSD 1235, with

an intravenous formulation in Phase III, and the oral version in Phase II. In October 2003,

the company granted the North American right for the intravenous formulations to Astellas

for a total consideration of US$68mn, including an upfront payment of $10mn. In Q406,

Astellas has submitted a NDA application for Vernakalant (iv) to US FDA. Cardiome also

has a Phase 1 program for GED-aPC, an engineered analog of recombinant human

activated Protein C (aPC) and a pre-clinical program directed at improving cardiovascular

function.

Cardiome

(US $M) 2005 2006 2007

Revenue 13.3 18.2 4.5

R&D spend 34.2 38.3 52.9

Net profit (loss) (44.1) (31.9) (79.6)

EPS (US$) (0.9) (0.6) (1.3)

M Capitalisation 513.7 597.7 568.4

No. of drug candidates in pipeline

Cash & cash equivalent 63.6 47.7 68.7

M cap / R&D expense 15.0 15.6 10.8

M cap / Cash 8.1 12.5 8.3

M cap/ sales 38.6 32.8 125.2

Source: Company, Emkay Research

28 August, 2008 23Emkay Research

Piramal Life Sciences Initiating CoverageThe team

www.emkayshare.com

BUY Expected total return (%) of stock price appreciation and dividend yield) of over 25% within the next 12-18 months.

ACCUMULATE Expected total return (%) of stock price appreciation and dividend yield) of over 10% within the next 12-18 months.

REDUCE Expected total return (%) of stock price appreciation and dividend yield) of below 10% within the next 12-18 months.

SELL The stock is believed to under perform the broad market indices or its related universe within the next 12-18 months.

NEUTRAL Analyst has no investment opinion on the stock under review.

DISCLAIMER: This document is not for public distribution and has been furnished to you solely for your information and may not be reproduced or redistributed to any other person. The manner of circulation and

distribution of this document may be restricted by law or regulation in certain countries, including the United States. Persons into whose possession this document may come are required to inform themselves of,

and to observe, such restrictions. This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or

the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. No person associated with Emkay Global Financial Services Ltd. is obligated to call or initiate

contact with you for the purposes of elaborating or following up on the information contained in this document. The material is based upon information that we consider reliable, but we do not represent that it is accurate

or complete, and it should not be relied upon. Neither Emkay Global Financial Services Ltd., nor any person connected with it, accepts any liability arising from the use of this document. The recipient of this material

should rely on their own investigations and take their own professional advice. Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable

basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements

are not predictions and may be subject to change without notice. We and our affiliates, officers, directors, and employees world wide, including persons involved in the preparation or issuance of this material may;

(a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage

or other compensation or act as a market maker in the financial instruments of the company (ies) discussed herein or may perform or seek to perform investment banking services for such company(ies)or act as advisor

or lender / borrower to such company(ies) or have other potential conflict of interest with respect to any recommendation and related information and opinions. The same persons may have acted upon the information

contained here. No part of this material may be duplicated in any form and/or redistributed without Emkay Global Financial Services Ltd.’sprior written consent. No part of this document may be distributed in Canada

or used by private customers in the United Kingdom. In so far as this report includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

Institutional Equities Team

Anish Damania Business Head [email protected] 91-22-66121203

Research Team

Ajay Parmar Head Research [email protected] 91-22-66121258Ajit Motwani Cement & Capital Goods [email protected] 91-22-66121255Amit Adesara Logistics, Engines,Real Estate [email protected] 91-22-66121241Chirag Shah Auto, Auto Ancillaries [email protected] 91-22-66121252Kashyap Jhaveri Banks [email protected] 91-22-66121249Manik Taneja IT [email protected] 91-22-66121253Manoj Garg Pharma [email protected] 91-22-66121257Naveen Jain Construction, Real Estate [email protected] 91-22-66121289Pritesh Chheda, CFA FMCG, Engineering, Mid -Caps [email protected] 91-22-66121273Rohan Gupta Paper, Fertilisers, Real Estate [email protected] 91-22-66121248Sumit Modi Telecom [email protected] 91-22-66121288Vishal Chandak Metals [email protected] 91-22-66121251Amit Golchha Midcaps [email protected] 91-22-66121408Chirag Dhaifule Research Associate [email protected] 91-22-66121238Chirag Khasgiwala Research Associate [email protected] 91-22-66121254Pradeep Agrawal Research Associate [email protected] 91-22-66121340Prerna Jhavar Research Associate [email protected] 91-22-66121337Vani Chandna Research Associate [email protected] 91-22-66121272Vikas Jhabakh Research Associate [email protected] 91-22-66121383Akshat Vyas Research Associate [email protected] 91-22-66121491Sachin Bobade Research Associate [email protected] 91-22-66121409Meenal Bhagwat Database Analyst [email protected] 91-22-66121322Mohan Billava Production Analyst [email protected] 91-22-66121271

Sales Team

Meenakshi Pai India / UK Sales Desk [email protected] 91-22-66121235Rajesh Chougule India Sales Desk [email protected] 91-22-66121295Falguni Doshi Institutional Equity Sales [email protected] 91-22-66121236Palak Shah Institutional Equity Sales [email protected] 91-22-66121277Ashok Agarwal Associate Inst.Equity Sales [email protected] 91-22-66121262Roshan Nagpal Associate Inst.Equity Sales [email protected] 91-22-66121234

Dealing Team

Kalpesh Parekh Senior Dealer [email protected] 91-22-66121230Ajit Nerkar Dealer [email protected] 91-22-66121237Dharmesh Mehta Dealer [email protected] 91-22-66121299Ketan Mehta Dealer [email protected] 91-22-66121233

Derivatives Sales Team

Sandeep Singal Co Head Institutions - Derivatives [email protected] 91-22-66121355

Nupur Barve Institutional Trader Derivatives [email protected] 91-22-66121222Manish Somani Sales Trader [email protected] 91-22-66121221Manjiri Muzumdar Sales Trader [email protected] 91-22-66121224Ankur Agarwala Sales Trader [email protected] 91-22-66121213Babita Sharma Sales Trader [email protected] 91-22-66121333

Technicals Research Team

Manas Jaiswal Technical Analyst [email protected] 91-22-66121274Suruchi Kapoor Jr.Technical Analyst [email protected] 91-22-66121275

Derivatives Research Team

Sameer Shetye Associate Analyst [email protected] 91-22-66121276

Emkay Rating Distribution