Embed Size (px)

Citation preview

August 3, 2007

PHILIPPINE STOCK EXCHANGE

4th

Floor, PSE Center

Tektite Towers, Exchange Road

Ortigas Center, Pasig City

Attention: ATTY. PETE M. MALABANAN

Head Disclosure Department

Dear Atty. Malabanan:

We are submitting an amended Quarterly Report (SEC Form 17-Q) to include additional

information on the 2Q results, as shown in page 9, Consolidated Statements of Income

and pages 32-33, Segment Revenues and Results for Business Segments. There is no

change in the net results reported, as the revisions simply highlighted our second quarter

performance.

Very truly yours,

AMADOR T. SENDIN

CIO/ Compliance Officer

VP – Planning and Business Devt

12/F, Allied Bank Center, 6754 Ayala Avenue, Makati City • Tel. No. (632) 840 2001 • Fax No. (632) 840 1892

COVER SHEET

4 0 5 2 4

SEC Registration Number

M A C R O A S I A C O R P O R A T I O N

A N D S U B S I D I A R I E S

(Company’s Full Name)

1 2 t h F l o o r , A l l i e d B a n k C e n t e r ,

6 7 5 4 A y a l a A v e n u e , M a k a t i C i t y

(Business Address: No. Street City/Town/Province)

Reynaldo O. Munsayac 840-2001 (Contact Person) (Company Telephone Number)

1 2 3 1 1 7 - Q

Month Day (Form Type) Month Day(Calendar Year) (Annual Meeting)

NA

(Secondary License Type, If Applicable)

Dept. Requiring this Doc. Amended Articles Number/Section

Total Amount of Borrowings

920 P25 M

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S

Remarks: Please use BLACK ink for scanning purposes.

TABLE OF CONTENTS

Page No.

PART I - FINANCIAL INFORMATION

Item 1 Consolidated Financial Statements 1

Item 2 Management’s Discussion and Analysis of Financial Condition and Results of Operations 1-5

PART II - OTHER INFORMATION 6

SIGNATURES 6

INDEX TO FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULE 7

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements.

The Consolidated Financial Statements listed in the accompanying Index to Financial Statements and Supplementary Schedules are filed as part of this Form 17-Q (pages 7 to 34)

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financial Conditions and Results of Operations

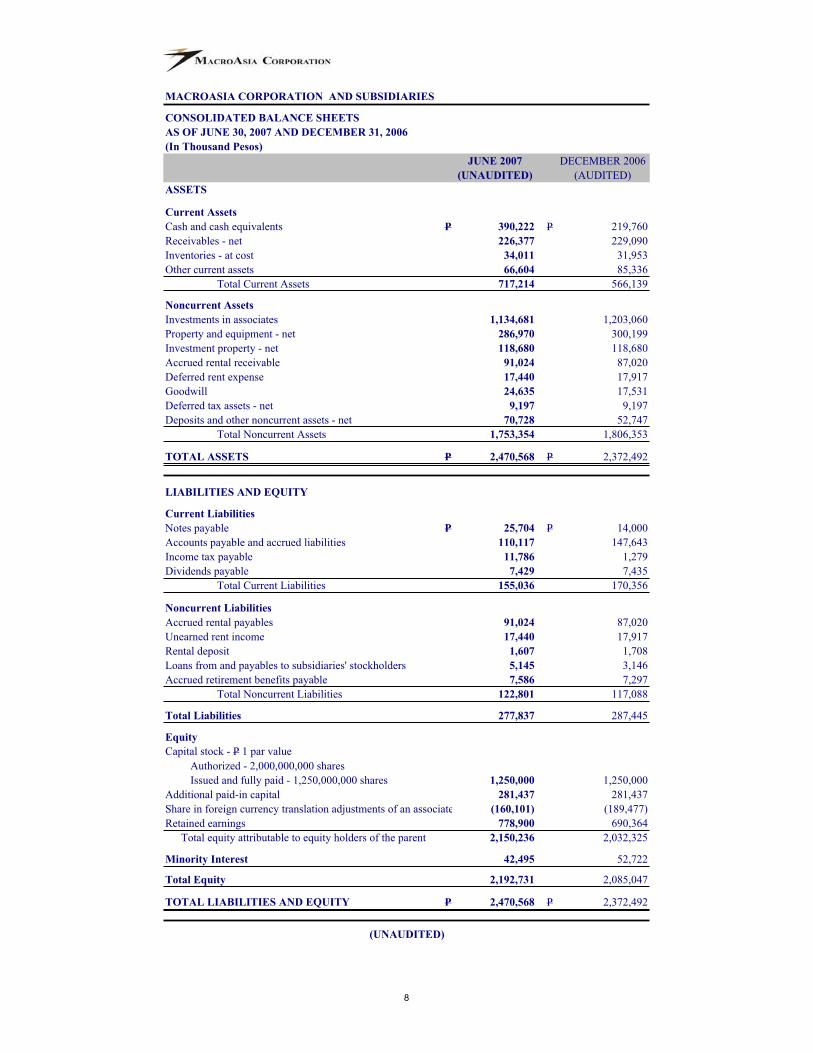

Total consolidated assets of P2.47 billion as of June 30, 2007 went up by 4% (or P98.08 million)

and 5% (or P112.74 million) compared to the December 31, 2006 and year-on-year balances due to the increases in cash and cash equivalents, receivables, deposits and other non-current assets.

Cash and cash equivalents were higher by P170.46 million (or 78%) compared to 2006 year end

balance and P155.36 million (or 66%) year-on-year mainly due to the aggressive collection of receivables and cash dividends received from associated companies.

Net receivables slightly decreased by P2.7 million (or 1%) compared to December 31, 2006

balance despite the big increase in meal volumes of airline clients mainly due to better collections of receivables and the additional provisions for doubtful accounts for the current year.

Inventories went up by 6% (or P2.1 million) against 2006 year end balance and 12% (or P3.7

million) year-on-year due essentially to the increase in raw materials requirements of the Company’s catering business, caused by the increased in meal uplift volumes of airline clients.

Other Current Assets include unused input taxes, office supplies, creditable withholding taxes

and prepaid insurance coverages for the building, equipment and staff. Total current assets decreased by 22% (or P18.73 million) against December 31, 2006 and 19% (or P15.55 million) year-on-year because of the utilization of tax credit certificates by the Company’s catering business.

The Company’s current ratio went up to 4.63:1 as of June 30, 2007 (from 3.32:1 as of December

31, 2006 and 4.10:1 as of June 30, 2006)

Investments in associates decreased by 6% (or P68.38 million) from its 2006 year end level of

P1.2 billion and 5% (or P61.94 million) year-on-year due to the associates’ issuance of P233 million cash dividends.

Property and Equipment of P286.97 million decreased by P13.23 million (or 4%) and P30.42

million (or 10%) compared to December 31 and June 30, 2006 balances, respectively, due to depreciation. On the other hand, accrued rental receivable and payable of P91.02 million increased by P8.00 million (or 10%) year-on-year due primarily to additional accrual of rental

1

income and expense in compliance with PAS 17, which requires the recognition of rentals on a straight-line basis (average) over the lease term.

Deposits and other non current assets rose by P17.98 million (or 34%) and P12.63 million (or

22%), when compared to the December 31 and June 30, 2006 levels, mostly because of additional deposits to suppliers for the expansion of the catering kitchen facilities to accommodate new airline clients.

Accounts payable and accrued liabilities decreased by P37.53 million (or 25%) when compared

to December 31 balance due to the sustained account settlements by the operating subsidiaries. Income tax payable on the other hand increased by P11.47 (or 3595%) year-on-year due to higher taxable income of operating units and less creditable withholding taxes available as of the end of the reporting quarter.

Notes payable of P25.70 million consist of unsecured short-term loans obtained from a local bank

by one of the operating subsidiaries to settle loans from a stockholder. These loans bear interest at an annual average rate of 8.78%.

Rental deposit (refundable to LTP) of P1.61 million decreased by P0.10 million (or 6%) compared

against its 2006 yearend balance due to straight-line amortization in accordance with PAS 39.

Accrued retirement benefits of P7.59 million went up by P0.95 million (or 14%) year-on-year due

to incremental accruals for the year based on the results of independent actuarial valuation.

Minority interest represents the 20% equity share of Singapore Airport Terminal Services in

MacroAsia Catering Services Inc. As of the April 15, 2007, the 30% equity share of Menzies Aviation Group in MacroAsia-Menzies was bought by MacroAsia. Changes in minority interest are dependent on the results of operations of the associate companies concerned.

Cumulative translation adjustments in the equity section of the balance sheets represents the

Group’s share in Lufthansa Technik’s foreign currency translation adjustments.

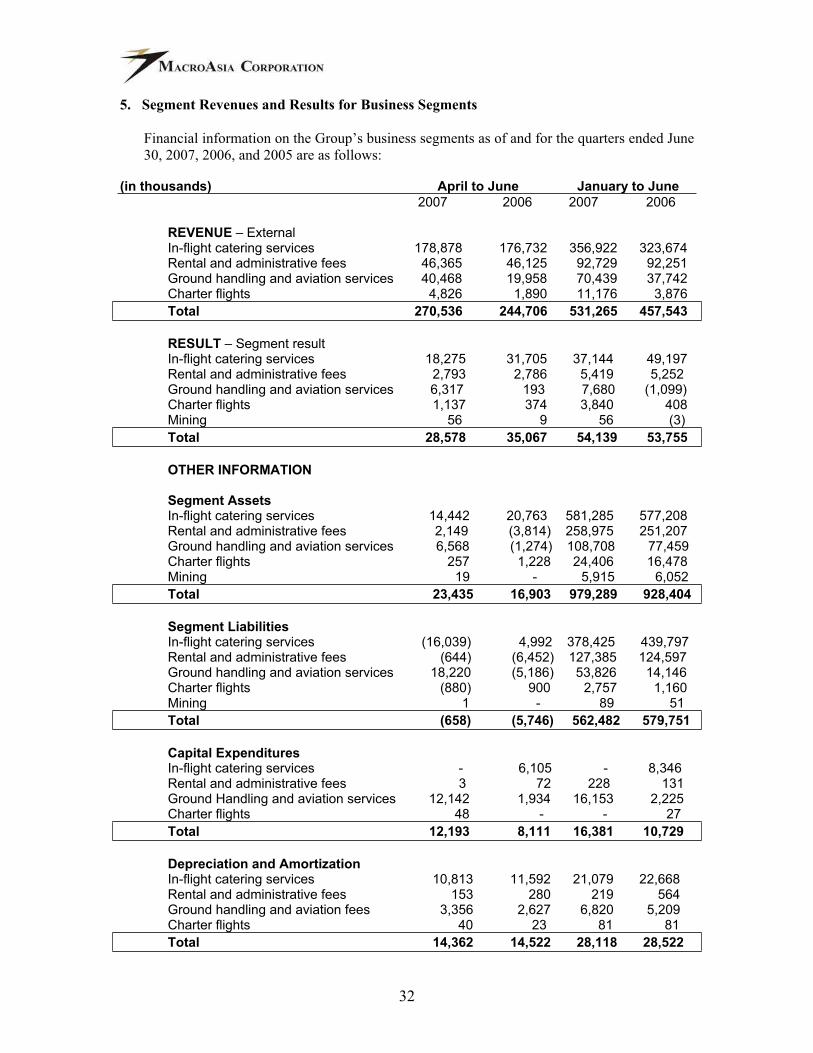

The Group’s total revenues were higher by P73.72 million (or 16%) compared to the P457.54

million earned in the same quarter last year due primarily to the P33.25 million (or 10%) increased in revenues from in-flight catering services and P32.70 million (or 87%) increase in ground handling and aviation. Revenues from catering services went up due to the increase in number of flights serviced and therefore higher number of meals served. Ground handling revenues on the other hand were up due to more clients serviced on behalf of PAL. Charter flight revenues tremendously increased by P7.3 million (or 188%) due to the recent midterm election.

Direct costs in relation to operating revenues went down by 5% compared to its level of 73% as

of the second quarter of 2006 due to lower direct overhead costs and achieved purchasing efficiencies. Operating expenses in relation to operating revenues, on the other hand, went up by 1% from 20%, as of June 30, 2006 due to increase in general and administrative expenses.

Equity in net income of associated companies was higher by P42.76 million (or 48%) due to the

considerable increase in the net income of LTP. Net foreign exchange loss of P3.61 million went down by P2.21 million (or 38%), year-on-year as a result of the lower Peso exchange rate against the US Dollar (i.e., payment of dollar denominated payables was settled at a lower peso conversion rate compared to the booking rate previously used). Interest income slightly went down by P0.21 million (or 8%) due mainly to lesser funds placed on temporary investments. Financing charges of P2.62 million was up by P1.31 million (or 99%) as a result of higher borrowings.

2

Equity in net income of associates represents MacroAsia Corporation’s (MAC) share in the net

income/ loss of its affiliated companies. Changes in shares from period to period are dependent upon the results of the operations of the affiliates/associated companies.

Provision for income tax increased by P11.02 million (or 97%) year-on-year due primarily to

higher taxable net income of subsidiaries.

Year-on-year, consolidated after tax net income of P159.25 million for the six months ended June

30, 2007 increased by P47.78 million (or 43%) due to increases in operating revenues particularly of the Company’s catering business and ground handling.

Material Events and/ or Uncertainties

NAIA Terminal 3 Contract with PIATCO

MacroAsia Corporation is presently engaged in aviation-support businesses at the Ninoy Aquino International Aiport (NAIA), Manila Domestic Airport and the General Aviation Areas. It provides in-flight catering services, ground handling services for passenger and cargo aircraft, helicopter charter flight services, and operates/develops economic zone. The Group is also pursuing other aviation related businesses and support services, such as the development of a modern aviation fuel tank farm, an aviation training center and cargo warehouse facility.

On January 21, 2004, the Supreme Court denied with finality the second motion for reconsideration of Philippine International Air Terminals Co. Inc. (PIATCO) over the Supreme courts decision nullifying PIATCO’s 1997 concession agreement to Build-Operate-Transfer arrangement (PIATCO contract) for the new international flight terminal – the NAIA Passenger Terminal 3 or “Terminal 3” – in Manila. Accordingly, the Supreme Court affirmed its May 5, 203 ruling, which voided the PIATCO contract and upheld the government’s decision to nullify all contracts with PIATCO for the construction of Terminal 3.

Under the said PIATCO contract, upon the completion of Terminal 3, all international flight operations would be moved from NAIA Passenger Terminal 1 (Terminal 1) and the Centennial Terminal (Terminal 2) to Terminal 3. PIATCO was to be the operator of Terminal 3 and would take over the functions of Manila International Airport-Ninoy Aquino International Airport (MIA-NAIA), including control over the amounts of fees and charges to be levied. Further, PIATCO ant its affiliate, Philippine Airport and Ground Services Inc., a NAIA service operator, were expected to have a total and exclusive control of Terminal 3 operations, which includes ground handling services (ramp and passenger) and in-flight catering among others. Accordingly, the operations of existing service operators that are providing such airport-related services to international carriers at Terminal 1 and 2 would have been affected upon transfer of their airline customers to Terminal 3.

Two of the Company’s subsidiaries, namely MacroAsia Catering Services Inc. (MACS, 80% owned) and MacroAsia-Menzies Airport Services Corporation (MASCORP, 100% owned) are providing in-flight catering and ground handling services, respectively, at Terminal 1.

With the above affirmed Supreme Court’s decision, the Management of MacroAsia Corporation believe that the issues emanating from the disputed provisions of the PIATCO contract have been resolved and the said Supreme Court’s decision has allowed the present service operators at NAIA, which includes MECS and MASCORP, to continue servicing their airline customers.

3

Other Matters

1. Passenger loads and flight frequencies of airlines are the two most important factors that affect the revenue levels of the Company’s operating units.

2. Management is not aware of any trends, demands, commitments, events or other uncertainties that may or will have a material negative impact on the company’s liquidity.

3. There are no unusual items or incidents affecting the issuer’s assets, liabilities, equity, net income or cash flows.

4. The Company has not issued, repurchased or repaid any debt or equity securities during the current interim reporting period.

5. During its special meeting last March 29, 2007, the Company declared cash dividends of P0.05 per share. Said cash dividends was payable on or before May 19, 2007 to stockholders of record as of April 24, 2007.

6. On March 28, 2006, the Company received its first Mineral Production Sharing Agreement (MPSA) from the Mines and Geosciences Bureau of DENR. The MPSA covers 1,114 hectares of land situated in Brooke’s Point, Palawan.

Under the MPSA, the Company shall have the exclusive right to conduct mining operations within, but not title over, the contracted area. Mining operations that are allowed include exploration, development and utilization for commercial purposes of nickel, chromite, iron and other associated mineral deposits that may be found in the area.

The MPSA runs for a term not exceeding twenty-five (25) years from the date of the grant of the MPSA and is renewable for another term not exceeding 25 years under the same terms and conditions, without prejudice to changes that will be mutually agreed upon by the Government and the Company.

MacroAsia Corporation has previously completed a high-profile exploration of the area covered by the mentioned MPSA. It is now still performing a more detailed exploration of the MPSA area.

7. On May 30, 2007, the Company received its second Mineral Production Sharing Agreement (MPSA) from the Mines and Geosciences Bureau of DENR covering 410 hectares of land in Brookes’ Point, Palawan.

As disclosed in SEC and PSE, portions of the said Contract Area are formerly covered by a Mining Lease Contract granted to Infanta Mineral and Mining Corporation (now MacroAisa Corporation).

The primary purpose of the MPSA is to provide for the rational exploration, development and commercial utilization of certain chromite, nickel and copper and associated mineral deposits existing within the Contract Area.

8. MacroAsia Corporation (MAC) signed on June 28, 2006, a sale and purchase agreement with Compass Group International B.V. (formerly Eurest International B.V) whereby MAC acquired the 13% shareholdings of the Compass Group in MacroAsia-Eurest Catering Services (MECS).

4

By mutual agreement of the three joint venture partners in MECS, the transaction effectively increases the shareholding of MacroAsia Corporation in MECS to 80%, and the balance of 20% stays with Singapore Air Terminal (SATS) as venture partner.

9. Effective April 15, 2007, MacroAsia Corporation had acquired the 30% shareholdings of Menzies Aviation Group in MacroAsia-Menzies Airport Services Corporation (MASCORP). This joint agreement has made MASCORP a wholly owned subsidiary of the MacroAsia.

10. No material events have occurred subsequent to the end of the current interim period that should be reflected in the financial statements for the interim period.

11. There have been no significant elements of income or loss that did not arise from the Company’s continuing normal operations.

12. The Company is not aware of any future event that will cause a material change in the relationship between cost and revenues.

13. The Company is not aware of any events that will trigger direct or contingent financial obligation that is material to the Company, including any default or acceleration of an obligation.

14. There are no material off-balance sheet transactions, arrangements, obligations (including contingent obligations), and other relationships of the company with unconsolidated entities or other persons created during the reporting period.

5

MACROASIA CORPORATION AND SUBSIDIARIES

INDEX TO FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES

FORM 17-Q, Item 1

Page No.

Consolidated Financial Statements

Consolidated Balance Sheets 8

Consolidated Statements of Income 9

Consolidated Statements of Changes in Equity 10

Consolidated Statement of Cash Flows 11

Supplementary Schedule

Summarized Income Statement Information for Unconsolidated Subsidiaries 12-14

Aging of Trade Accounts Receivable 15

Notes to Consolidated Financial Statements 16-34

7

e

MACROASIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

AS OF JUNE 30, 2007 AND DECEMBER 31, 2006

(In Thousand Pesos)

JUNE 2007 DECEMBER 2006

(UNAUDITED) (AUDITED)

ASSETS

Current Assets

Cash and cash equivalents P 390,222 P 219,760

Receivables - net 226,377 229,090

Inventories - at cost 34,011 31,953

Other current assets 66,604 85,336

Total Current Assets 717,214 566,139

Noncurrent Assets

Investments in associates 1,134,681 1,203,060

Property and equipment - net 286,970 300,199

Investment property - net 118,680 118,680

Accrued rental receivable 91,024 87,020

Deferred rent expense 17,440 17,917

Goodwill 24,635 17,531

Deferred tax assets - net 9,197 9,197

Deposits and other noncurrent assets - net 70,728 52,747

Total Noncurrent Assets 1,753,354 1,806,353

TOTAL ASSETS P 2,470,568 P 2,372,492

LIABILITIES AND EQUITY

Current Liabilities

Notes payable P 25,704 P 14,000

Accounts payable and accrued liabilities 110,117 147,643

Income tax payable 11,786 1,279

Dividends payable 7,429 7,435

Total Current Liabilities 155,036 170,356

Noncurrent Liabilities

Accrued rental payables 91,024 87,020

Unearned rent income 17,440 17,917

Rental deposit 1,607 1,708

Loans from and payables to subsidiaries' stockholders 5,145 3,146

Accrued retirement benefits payable 7,586 7,297

Total Noncurrent Liabilities 122,801 117,088

Total Liabilities 277,837 287,445

Equity

Capital stock - P 1 par value

Authorized - 2,000,000,000 shares

Issued and fully paid - 1,250,000,000 shares 1,250,000 1,250,000

Additional paid-in capital 281,437 281,437

Share in foreign currency translation adjustments of an associat (160,101) (189,477)

Retained earnings 778,900 690,364

Total equity attributable to equity holders of the parent 2,150,236 2,032,325

Minority Interest 42,495 52,722

Total Equity 2,192,731 2,085,047

TOTAL LIABILITIES AND EQUITY P 2,470,568 P 2,372,492

(UNAUDITED)

8

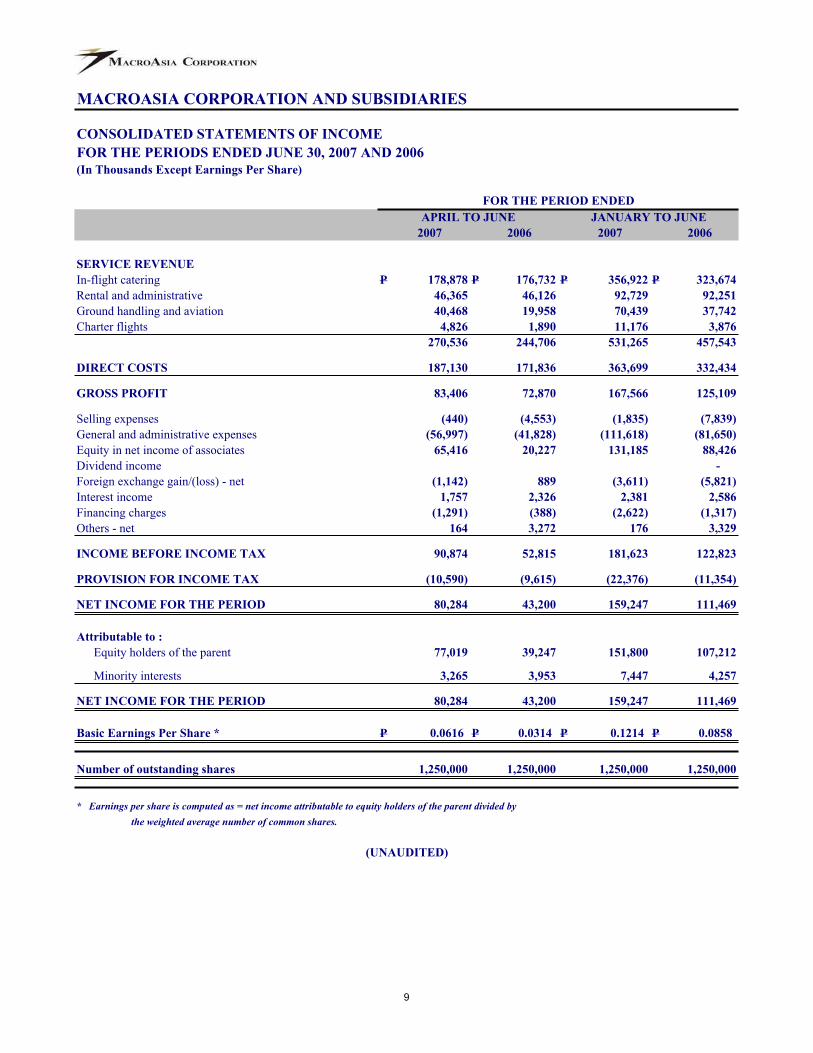

MACROASIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME

FOR THE PERIODS ENDED JUNE 30, 2007 AND 2006

(In Thousands Except Earnings Per Share)

2007 2006 2007 2006

SERVICE REVENUE

In-flight catering P 178,878 P 176,732 P 356,922 P 323,674

Rental and administrative 46,365 46,126 92,729 92,251

Ground handling and aviation 40,468 19,958 70,439 37,742

Charter flights 4,826 1,890 11,176 3,876

270,536 244,706 531,265 457,543

DIRECT COSTS 187,130 171,836 363,699 332,434

GROSS PROFIT 83,406 72,870 167,566 125,109

Selling expenses (440) (4,553) (1,835) (7,839)

General and administrative expenses (56,997) (41,828) (111,618) (81,650)

Equity in net income of associates 65,416 20,227 131,185 88,426

Dividend income -

Foreign exchange gain/(loss) - net (1,142) 889 (3,611) (5,821)

Interest income 1,757 2,326 2,381 2,586

Financing charges (1,291) (388) (2,622) (1,317)

Others - net 164 3,272 176 3,329

INCOME BEFORE INCOME TAX 90,874 52,815 181,623 122,823

PROVISION FOR INCOME TAX (10,590) (9,615) (22,376) (11,354)

NET INCOME FOR THE PERIOD 80,284 43,200 159,247 111,469

Attributable to :

Equity holders of the parent 77,019 39,247 151,800 107,212

Minority interests 3,265 3,953 7,447 4,257

NET INCOME FOR THE PERIOD 80,284 43,200 159,247 111,469

Basic Earnings Per Share * P 0.0616 P 0.0314 P 0.1214 P 0.0858

Number of outstanding shares 1,250,000 1,250,000 1,250,000 1,250,000

* Earnings per share is computed as = net income attributable to equity holders of the parent divided by

the weighted average number of common shares.

(UNAUDITED)

FOR THE PERIOD ENDED

APRIL TO JUNE JANUARY TO JUNE

9

MACROASIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

FOR THE PERIODS ENDED JUNE 30, 2007 AND 2006

(In Thousand Pesos)

Capital Stock

Additional

Paid-in

Capital

Warrants

Outstanding

Share in Foreign

Currency Translation

Adjustments of an

Associate

Retained

EarningsTotal

Minority

InterestTotal

BALANCES AT DECEMBER 31, 2005 P 1,250,000 P 281,437 P (30,860) P 471,504 P 1,972,081 P 62,698 P 2,034,778

Issuance of rights shares

Issuance of warrants

Effect of change of ownership in a subsidiary (13,251) (13,251) (23,242) (36,493)

Net foreign currency translation adjustments

for the period (8,598) (8,598) (8,598)

Net Profit 107,212 107,212 4,257 111,469

BALANCES AT JUNE 30, 2006 1,250,000 281,437 (39,458) 565,465 2,057,444 43,712 2,101,156

BALANCES AT DECEMBER 31, 2006 P 1,250,000 P 281,437 P (189,477) P 692,586 P 2,034,546 P 52,005 P 2,086,551

Issuance of rights shares

Issuance of warrants

Purchase of Minority Interest (16,957) (16,957)

Issuance of dividends (62,500) (62,500)

Adjustments to beginning balance of Retained Earnings (2,985) (2,985)

Net foreign currency translation adjustments

for the period 29,375 29,375

Net Profit 151,800 151,800 7,447 159,247

BALANCES AT JUNE 30, 2007 1,250,000 281,437 (160,101) 778,900 2,186,346 42,495 2,192,731

Attributable to the Equity Holders of the Parent

(UNAUDITED)

10

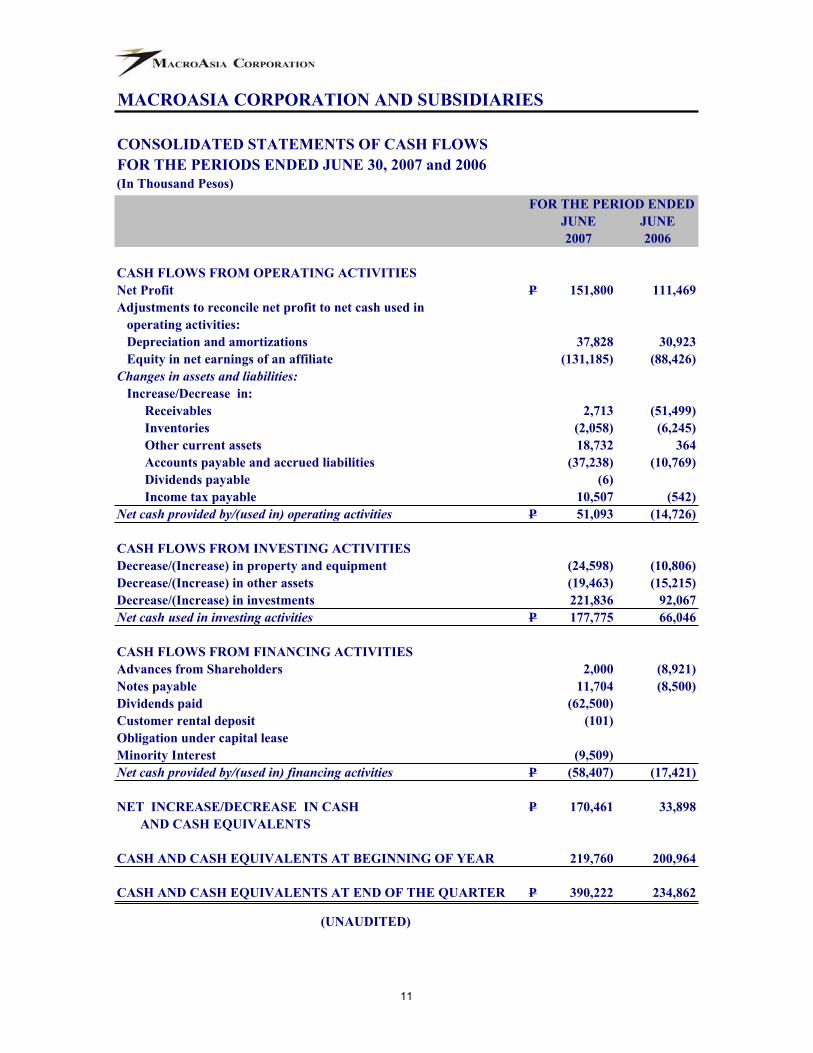

MACROASIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE PERIODS ENDED JUNE 30, 2007 and 2006

(In Thousand Pesos)

JUNE JUNE

2007 2006

CASH FLOWS FROM OPERATING ACTIVITIES

Net Profit P 151,800 111,469

Adjustments to reconcile net profit to net cash used in

operating activities:

Depreciation and amortizations 37,828 30,923

Equity in net earnings of an affiliate (131,185) (88,426)

Changes in assets and liabilities:

Increase/Decrease in:

Receivables 2,713 (51,499)

Inventories (2,058) (6,245)

Other current assets 18,732 364

Accounts payable and accrued liabilities (37,238) (10,769)

Dividends payable (6)

Income tax payable 10,507 (542)

Net cash provided by/(used in) operating activities P 51,093 (14,726)

CASH FLOWS FROM INVESTING ACTIVITIES

Decrease/(Increase) in property and equipment (24,598) (10,806)

Decrease/(Increase) in other assets (19,463) (15,215)

Decrease/(Increase) in investments 221,836 92,067

Net cash used in investing activities P 177,775 66,046

CASH FLOWS FROM FINANCING ACTIVITIES

Advances from Shareholders 2,000 (8,921)

Notes payable 11,704 (8,500)

Dividends paid (62,500)

Customer rental deposit (101)

Obligation under capital lease

Minority Interest (9,509)

Net cash provided by/(used in) financing activities P (58,407) (17,421)

NET INCREASE/DECREASE IN CASH P 170,461 33,898

AND CASH EQUIVALENTS

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 219,760 200,964

CASH AND CASH EQUIVALENTS AT END OF THE QUARTER P 390,222 234,862

FOR THE PERIOD ENDED

(UNAUDITED)

11

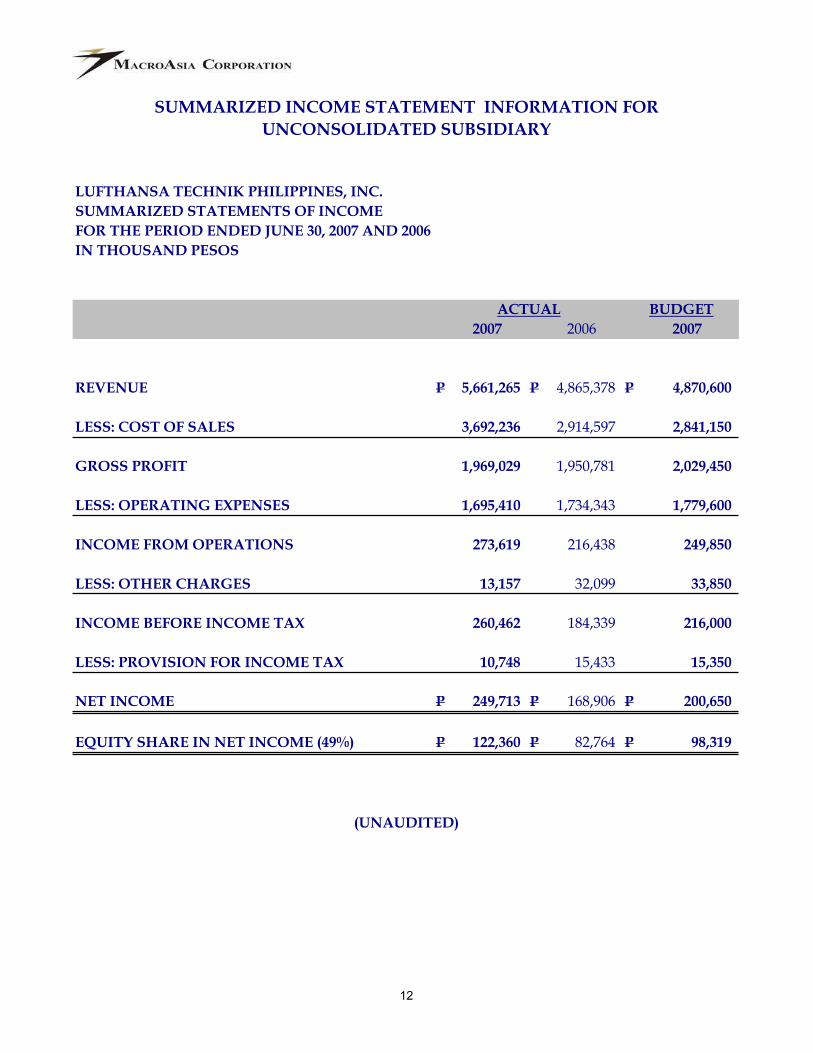

LUFTHANSA TECHNIK PHILIPPINES, INC.

SUMMARIZED STATEMENTS OF INCOME

FOR THE PERIOD ENDED JUNE 30, 2007 AND 2006

IN THOUSAND PESOS

2007 2006 2007

REVENUE P 5,661,265 P 4,865,378 P 4,870,600

LESS: COST OF SALES 3,692,236 2,914,597 2,841,150

GROSS PROFIT 1,969,029 1,950,781 2,029,450

LESS: OPERATING EXPENSES 1,695,410 1,734,343 1,779,600

INCOME FROM OPERATIONS 273,619 216,438 249,850

LESS: OTHER CHARGES 13,157 32,099 33,850

INCOME BEFORE INCOME TAX 260,462 184,339 216,000

LESS: PROVISION FOR INCOME TAX 10,748 15,433 15,350

NET INCOME P 249,713 P 168,906 P 200,650

EQUITY SHARE IN NET INCOME (49%) P 122,360 P 82,764 P 98,319

(UNAUDITED)

SUMMARIZED INCOME STATEMENT INFORMATION FOR

UNCONSOLIDATED SUBSIDIARY

ACTUAL BUDGET

12

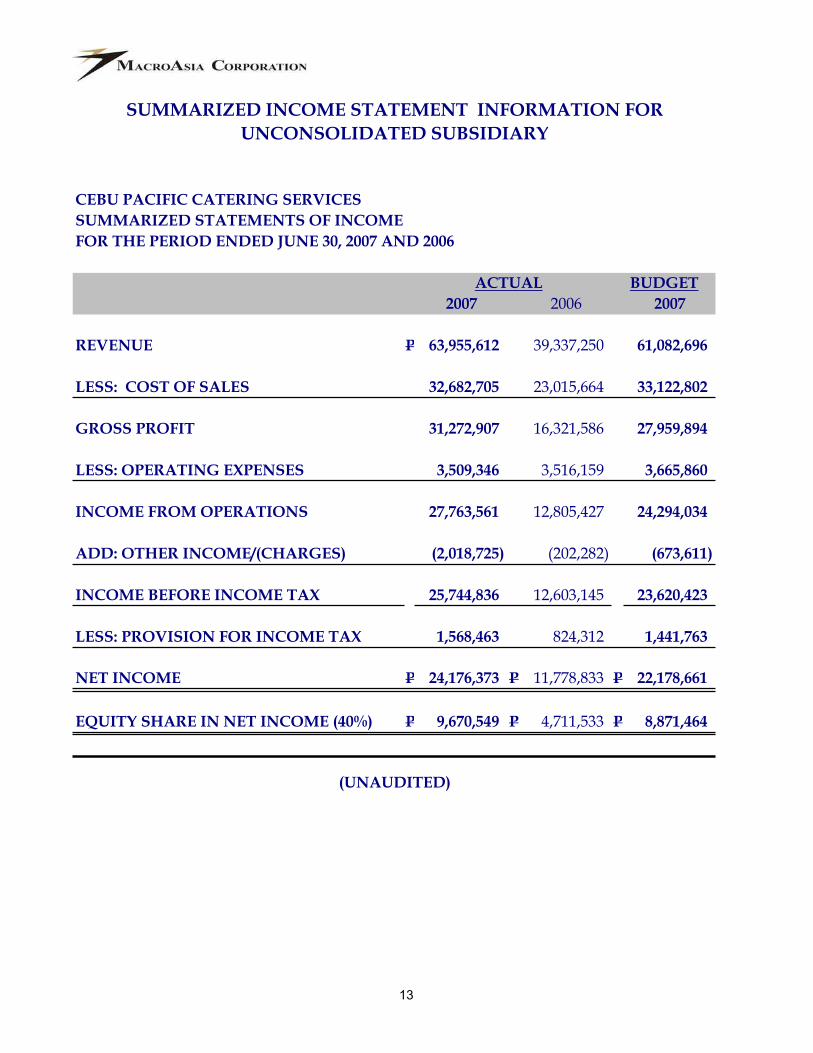

CEBU PACIFIC CATERING SERVICES

SUMMARIZED STATEMENTS OF INCOME

FOR THE PERIOD ENDED JUNE 30, 2007 AND 2006

2007 2006 2007

REVENUE P 63,955,612 39,337,250 61,082,696

LESS: COST OF SALES 32,682,705 23,015,664 33,122,802

GROSS PROFIT 31,272,907 16,321,586 27,959,894

LESS: OPERATING EXPENSES 3,509,346 3,516,159 3,665,860

INCOME FROM OPERATIONS 27,763,561 12,805,427 24,294,034

ADD: OTHER INCOME/(CHARGES) (2,018,725) (202,282) (673,611)

INCOME BEFORE INCOME TAX 25,744,836 12,603,145 23,620,423

LESS: PROVISION FOR INCOME TAX 1,568,463 824,312 1,441,763

NET INCOME P 24,176,373 P 11,778,833 P 22,178,661

EQUITY SHARE IN NET INCOME (40%) P 9,670,549 P 4,711,533 P 8,871,464

(UNAUDITED)

SUMMARIZED INCOME STATEMENT INFORMATION FOR

UNCONSOLIDATED SUBSIDIARY

ACTUAL BUDGET

13

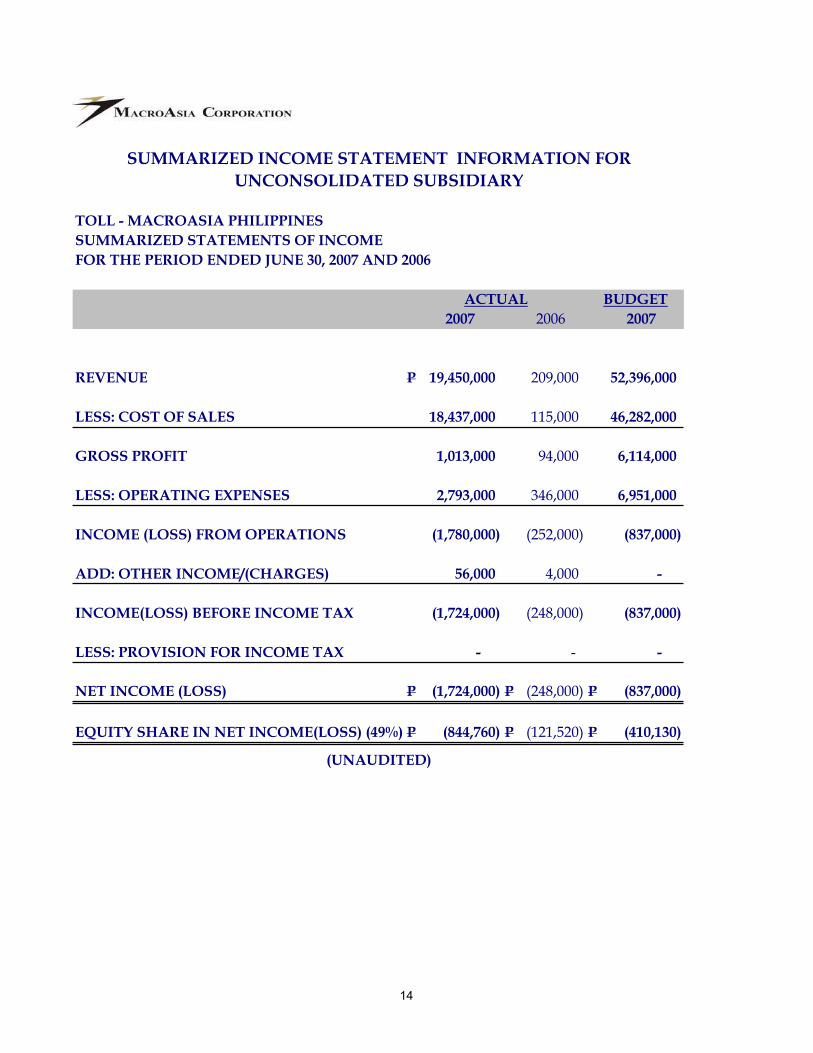

TOLL - MACROASIA PHILIPPINES

SUMMARIZED STATEMENTS OF INCOME

FOR THE PERIOD ENDED JUNE 30, 2007 AND 2006

2007 2006 2007

REVENUE P 19,450,000 209,000 52,396,000

LESS: COST OF SALES 18,437,000 115,000 46,282,000

GROSS PROFIT 1,013,000 94,000 6,114,000

LESS: OPERATING EXPENSES 2,793,000 346,000 6,951,000

INCOME (LOSS) FROM OPERATIONS (1,780,000) (252,000) (837,000)

ADD: OTHER INCOME/(CHARGES) 56,000 4,000 -

INCOME(LOSS) BEFORE INCOME TAX (1,724,000) (248,000) (837,000)

LESS: PROVISION FOR INCOME TAX - - -

NET INCOME (LOSS) P (1,724,000) P (248,000) P (837,000)

EQUITY SHARE IN NET INCOME(LOSS) (49%) P (844,760) P (121,520) P (410,130)

(UNAUDITED)

SUMMARIZED INCOME STATEMENT INFORMATION FOR

UNCONSOLIDATED SUBSIDIARY

ACTUAL BUDGET

14

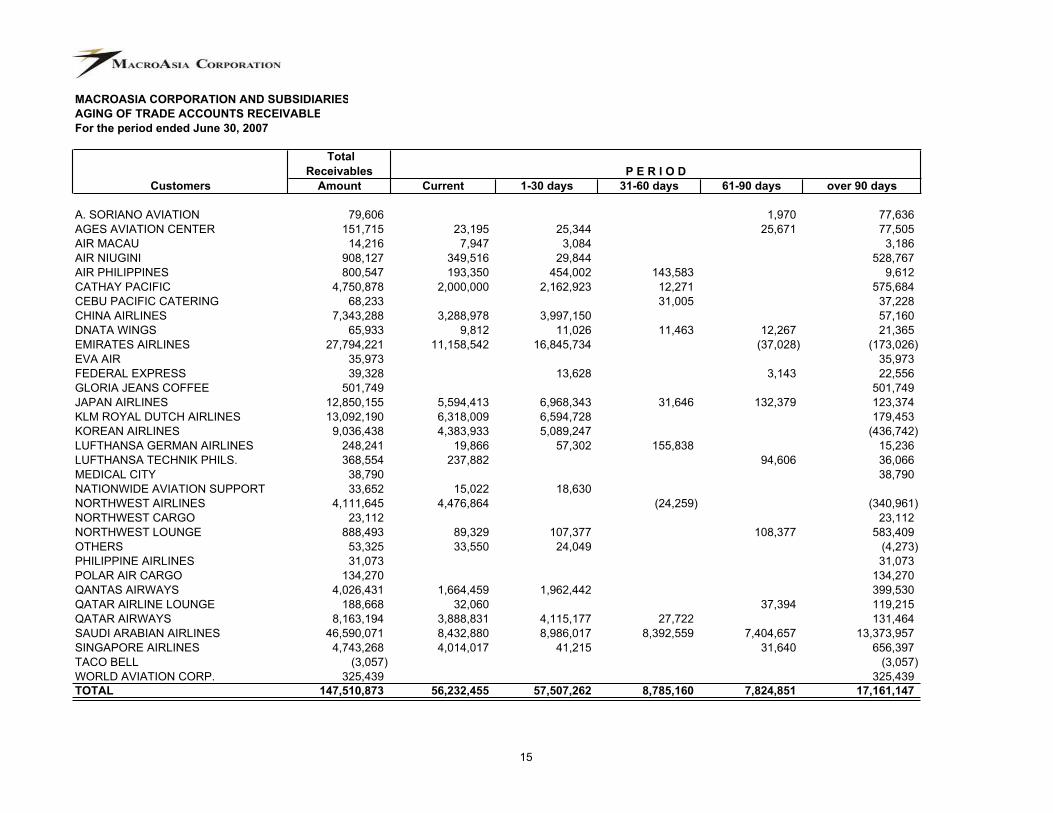

MACROASIA CORPORATION AND SUBSIDIARIES

AGING OF TRADE ACCOUNTS RECEIVABLE

For the period ended June 30, 2007

Total

Receivables

Amount Current 1-30 days 31-60 days 61-90 days over 90 days

A. SORIANO AVIATION 79,606 1,970 77,636

AGES AVIATION CENTER 151,715 23,195 25,344 25,671 77,505

AIR MACAU 14,216 7,947 3,084 3,186

AIR NIUGINI 908,127 349,516 29,844 528,767

AIR PHILIPPINES 800,547 193,350 454,002 143,583 9,612

CATHAY PACIFIC 4,750,878 2,000,000 2,162,923 12,271 575,684

CEBU PACIFIC CATERING 68,233 31,005 37,228

CHINA AIRLINES 7,343,288 3,288,978 3,997,150 57,160

DNATA WINGS 65,933 9,812 11,026 11,463 12,267 21,365

EMIRATES AIRLINES 27,794,221 11,158,542 16,845,734 (37,028) (173,026)

EVA AIR 35,973 35,973

FEDERAL EXPRESS 39,328 13,628 3,143 22,556

GLORIA JEANS COFFEE 501,749 501,749

JAPAN AIRLINES 12,850,155 5,594,413 6,968,343 31,646 132,379 123,374

KLM ROYAL DUTCH AIRLINES 13,092,190 6,318,009 6,594,728 179,453

KOREAN AIRLINES 9,036,438 4,383,933 5,089,247 (436,742)

LUFTHANSA GERMAN AIRLINES 248,241 19,866 57,302 155,838 15,236

LUFTHANSA TECHNIK PHILS. 368,554 237,882 94,606 36,066

MEDICAL CITY 38,790 38,790

NATIONWIDE AVIATION SUPPORT 33,652 15,022 18,630

NORTHWEST AIRLINES 4,111,645 4,476,864 (24,259) (340,961)

NORTHWEST CARGO 23,112 23,112

NORTHWEST LOUNGE 888,493 89,329 107,377 108,377 583,409

OTHERS 53,325 33,550 24,049 (4,273)

PHILIPPINE AIRLINES 31,073 31,073

POLAR AIR CARGO 134,270 134,270

QANTAS AIRWAYS 4,026,431 1,664,459 1,962,442 399,530

QATAR AIRLINE LOUNGE 188,668 32,060 37,394 119,215

QATAR AIRWAYS 8,163,194 3,888,831 4,115,177 27,722 131,464

SAUDI ARABIAN AIRLINES 46,590,071 8,432,880 8,986,017 8,392,559 7,404,657 13,373,957

SINGAPORE AIRLINES 4,743,268 4,014,017 41,215 31,640 656,397

TACO BELL (3,057) (3,057)

WORLD AVIATION CORP. 325,439 325,439

TOTAL 147,510,873 56,232,455 57,507,262 8,785,160 7,824,851 17,161,147

Customers

P E R I O D

15

MACROASIA CORPORATION AND SUBSIDIARIES/ AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

1. Significant Accounting Judgments and Estimates

The preparation of the accompanying consolidated financial statements in accordance with

PFRS requires the Group to exercise judgments, make estimates and use assumptions that

affect the reported amounts of assets, liabilities, income and expenses and related

disclosures. Future events may occur which will cause the assumptions used in arriving at

the estimates to change. The effects of any change in estimates are reflected in the

consolidated financial statements as they become reasonably determinable.

Judgments and estimates are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

Determination of the Group’s functional currency Judgment is exercised in assessing various factors in determining the functional currency of

each entity within the Group, including prices of goods and services, competition, cost and expenses, and other factors including the currency in which financing is primarily undertaken. Additional factors are considered in determining the functional currency of a foreign operation, including whether its activities are carried as an extension of that of the Company rather than being carried out with significant autonomy.

The Group, based on the relevant economic substance of the underlying circumstances, has determined its functional currency to be Philippine peso. It is the currency of the primary economic environment in which its subsidiaries and two of its associates operate. The functional currency of LTP, one of the Company’s associated companies, has been determined to be United States (US) dollar.

Classification of financial instrumentsThe Group classifies a financial instrument, or its components, on initial recognition as a financial liability, a financial asset or an equity instrument in accordance with the substance of the contractual arrangement and the definitions of a financial liability, a financial asset or an equity instrument. The substance of a financial instrument, rather than its legal form, governs its classification in the Group’s consolidated balance sheet.

The Group determines the classification at initial recognition and re-evaluates this classification at every reporting date.

Estimation of allowance for doubtful accountsAllowance for doubtful accounts is provided for accounts that are specifically identified to be doubtful of collection. The level of allowance is evaluated by management on the basis of factors that affect the collectibility of the accounts.

In addition to specific allowance against individually significant receivables primarily from airline customers, the Group also assesses at least on an annual basis a collective impairment allowance against credit exposures which, although not specifically identified as requiring a specific allowance, have a greater risk of default than when the receivables were originally granted to customers. This collective allowance is based on various factors such as historical performance of the customers within the collective group, deterioration in the markets in which the customers operate, various country risks, overall performance of the airline industry, and technological obsolescence which affects the confidence of the air transport market, as well as identified structural weaknesses or deterioration in the cash flows of customers.

16

The carrying value of the Group’s receivables amounted to P226.4 million and P229.1million as of June 30, 2007 and December 31, 2006, respectively. Related allowance for doubtful accounts amounted to P10.2 million and P2.0 million as of June 30, 2007 and December 31, 2006 respectively.

Recognition of deferred tax assetsThe Group reviews the carrying amounts of deferred tax assets at each balance sheet date and adjusts the balance of deferred tax assets to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax assets to be utilized.

Deferred tax assets recognized amounted to P9.2 million as of June 30, 2007 and December 31, 2006.

Estimation of useful lives and residual values of property and equipment The Group estimates the useful lives and residual values of property and equipment based

on the internal technical evaluation and experience with similar assets. Estimated lives of property and equipment are reviewed periodically and updated if expectations differ from previous estimates due to physical wear and tear, technical and commercial obsolescence and other limits on the use of the assets.

The carrying value of property and equipment as of June 30, 2007 and December 31, 2006 amounted to P287.0 million and P300.2 million, respectively.

Impairment of non-financial assetsThe Group assesses at each reporting date whether there is any indication that property and equipment, investment property and goodwill may be impaired. If such indication exists, the entity shall estimate the recoverable amount of the asset, which is the higher of an asset’s fair value less costs to sell and its value in use. Estimating the value in use requires the Group to make an estimate of the expected future cash flows from the cash generating unit and also to choose the approximate pre-tax discount rate to calculate the present value of those cash flows.

As of June 30, 2007and December 31, 2006, the carrying value of the Group’s property and equipment, investment property and goodwill amounted to P430.3 million and P436.4 million, respectively, on which an impairment loss on investment properties of P25.2 million has been recognized as of both balance sheet dates.

Estimation of retirement benefits cost The Group’s retirement benefits cost is actuarially computed. This entails using estimation of

the present value of the Group’s obligation using certain assumptions like annual salary increases, rate of return on plan assets and discount rates. Total accrued retirement benefits payable amounted to P7.6 million and P7.3 million as of March 31, 2007 and December 31, 2006, respectively.

ProvisionsThe Group provides for present obligations (legal or constructive) when it is probable that there will be an outflow of resources embodying economic benefits that will be required to settle said obligations. An estimate of the provision is based on known information at the balance sheet date, net of any estimated amount that may be reimbursed to the Group. If the effect of the time value of money is material, provisions are discounted using a current pre-tax rate that reflects the risks specific to the liability. The amount of provision is reassessed at least on an annual basis to consider new relevant information.

The Group has not recognized any provision in 2006 and 2005.

17

2. Summary of Significant Accounting Policies and Financial Reporting Practices

Basis of Financial Statements Preparation and Presentation The accompanying consolidated financial statements have been prepared on a historical cost

basis, and are presented in Philippine pesos, the Company’s functional currency.

Statement of Compliance The consolidated financial statements have been prepared in compliance with Philippine

Financial Reporting Standards (PFRS).

Changes in Accounting Policies The accounting policies adopted in 2007 and 2006 are consistent with those of the previous

financial years, except as follows:

The Group has adopted the following new and amended PFRSs in 2006. The adoption of these new and amended standards did not have any effect on the consolidated financial statements of the Group except for the additional disclosures required. These additional disclosures have been included in the accompanying consolidated financial statements.

Amendments to Philippine Accounting Standard (PAS) 19, Employee Benefits, provides additional disclosures about trends in the assets and liabilities in the define benefit plans and the assumptions underlying the components of the defined benefit cost. This change did not have recognition or measurement impact as the Group chose not to apply the new option offered to recognize actuarial gains and losses outside of the consolidated statement of income.

Amendments to PAS 21, The Effects of Changes in Foreign Exchange Rates, provides that all exchange differences arising from a monetary item that forms part of the Group’s net investment in a foreign operation are recognized in a separate component of equity in the consolidated financial statements regardless of the currency in which the monetary item is denominated.

Amendments to PAS 39, Financial Instruments: Recognition and Measurement:

Amendment for financial guarantee contracts requires financial guarantee contracts that are not considered to be insurance contracts to be recognized initially at fair value and to be remeasured at the higher of the amount determined in accordance with PAS 37, Provisions, Contingent Liabilities and Contingent Assets and the amount initially recognized less, when appropriate, cumulative amortization recognized in accordance with PAS 18, Revenue.

Amendment for hedges of forecast intragroup transactions permits the foreign currency risk of a highly probable intragroup forecast transaction to qualify as the hedged item in a cash flow hedge, provided that the transaction is denominated in a currency other than the functional currency of the entity entering into that transaction and that the foreign currency risk will affect the consolidated statement of income.

Amendment for the fair value option restricts the use of the option to designate any financial asset or any financial liability to be measured at fair value through the consolidated statement of income.

PFRS 6, Exploration for and Evaluation of Mineral Resources, permits an entity to develop an accounting policy for exploration and evaluation assets without specifically considering the requirements of PAS 8, Accounting Policies, Changes in Accounting Estimates and Errors. Thus, under PFRS 6, an entity may continue to use the accounting

18

policies applied immediately before adopting PFRS 6. This includes continuing to use recognition and measurement practices that are part of those accounting policies. It also requires entities recognizing exploration and evaluation assets to perform and impairment test on those assets when facts and circumstances suggest that the carrying amount of the assets may exceed their recoverable amount. It varies in recognition of impairment from that in PAS 36, Impairment of Assets, but measures the impairment in accordance with that standard once the impairment is identified.

Basis of Consolidation The accompanying consolidated financial statements comprise the financial statements of the

Company and the following subsidiaries:

Percentage of ownership

Direct Indirect

MacroAsia Air Taxi Services, Inc. (MAATS) 100 –MAPDC 100 –MacroAsia-Menzies Airport Services Corporation (MASCORP)*

100 –

Airport Specialists’ Services Corporation (ASSC)** 100 –MacroAsia Catering Services, Inc. (MACS)*** 80 –MacroAsia Mining Corporation (MMC)**** 67 –

* Effective April 15, 2007, the Company bought the 30% minority interest of Menzies

Aviation Group in MASCORP

** A wholly-owned subsidiary of the Company; prior to 2006, ASSC is a wholly-owned subsidiary of MASCORP; has ceased commercial operations effective May 1, 2001.

*** In 2006, the Company bought the 13% minority interest of Compass Group International B.V. (Compass) in MACS.

**** Incorporated on September 25, 2000; has not started commercial operations.

The consolidated financial statements comprise the financial statements of the Company and the above subsidiaries as of June 30, 2007 and December 31, 2006. The financial statements of the subsidiaries are prepared using accounting policies, consistent with those of the Company. All significant intra-group balances, transactions, income and expenses, profits and losses resulting from intra-group transactions are eliminated in full in the consolidation.

Subsidiaries are all entities over which the Group has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity.

Subsidiaries are fully consolidated from the date on which control is transferred to the Group. Control is achieved where the Group has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. Consolidation of subsidiaries ceases when control is transferred out of the Group. The results of subsidiaries acquired or disposed of during the year are included in the consolidated statement of income from the date of acquisition or up to the date of disposal, as appropriate.

19

Minority Interests Minority interest represents the portion of the net assets of consolidated subsidiaries not held

by the Group, and are presented separately in the consolidated statements of income and within the equity section of the consolidated balance sheets, separate from parent’s equity.

The losses applicable to the minority in a consolidated subsidiary may exceed the minority interest’s equity in the subsidiary. The excess, and any further losses applicable to the minority, are charged against the majority interest except to the extent that the minority has a binding obligation to and is able to make good the losses. If the subsidiary subsequently reports profits, the majority interest is allocated all such profits until the minority’s share of losses previously absorbed by the majority is recovered.

The acquisition of minority interests is not considered a business combination under PFRS 3, Business Combinations, and therefore, the re-measurement of the net assets acquired to their fair values, as not permissible, is not performed. Acquisitions of minority interests are accounted for using the parent entity extension concept method, wherein the difference between the consideration and the book value of the net assets acquired is recognized as goodwill.

Future changes in minority interests

The Company is not aware of any other future changes that might affect minority interest.

Investments in AssociatesAssociates are all entities over which the Group has significant influence but not control, generally accompanying a shareholding of between 20% and 50% of the voting rights. Investments in associates are accounted for under the equity method of accounting in the consolidated financial statements. Under this method, the investments in associates are carried in the consolidated balance sheets at cost plus post-acquisition changes in the Company’s share in the net assets of the associate, less any impairment in value. Dividends are considered return of capital and are deducted from the investment account.

The consolidated statements of income reflect the Company’s share in the results of operations of the associates. Unrealized gains or losses arising from transactions with associates are eliminated to the extent of the Company’s interests in those associates, against the investments in those associates. Unrealized losses are eliminated similarly but only to the extent that there is no evidence of impairment of the asset transferred.

The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the Group’s share in the losses of an associate equals or exceeds its interest in the associate, including any other unsecured receivables, the Group does not recognize further losses, unless it has incurred obligations or made payments on behalf of the associate.

Investments in associates pertain to the Company’s investments in the shares of stock of Cebu Pacific Catering Services Inc. (CPCS), 40%-owned; and LTP and Toll-MacroAsia Philippines, Inc. (TMP), 49%-owned. Since the Company has no joint control but instead has significant influence over these associates, the Company accounts for its investments in compliance with the provisions of PAS 28, Investments in Associates.

Functional Currency and Foreign Currency Translation Each entity in the Group determines its own functional currency and the items included in the

financial statements of each entity are measured using that functional currency. Transactions in foreign currencies are initially recorded in the functional currency rate at the date of the

20

transaction. Outstanding monetary assets and liabilities denominated in foreign currencies are retranslated at the functional currency rate of exchange at balance sheet date. All differences are taken to profit or loss. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates as at the dates of the transactions. Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

Various factors are considered in determining the functional currency of each entity within the Group, including prices of goods and services, competition, cost and expenses, and other factors including the currency in which financing deals are primarily undertaken. Additional factors are considered in determining the functional currency of a foreign operation, including whether its activities are carried as an extension of the Company rather than being carried out with significant autonomy.

The financial position and results of operations of an associate whose functional currency is not the currency of a hyperinflationary economy is translated into the Group’s presentation currency using the following procedures:

a. Assets and liabilities for each consolidated balance sheet presented are translated at the closing rate at the balance sheet date.

b. Income and expenses for each consolidated income statement are translated using the average rate.

c. All resulting exchange differences are recognized as a separate component of equity.

Cash and Cash Equivalents Cash consists of cash on hand and in banks. Cash equivalents are short-term, highly liquid

investments that are readily convertible to known amounts of cash with original maturities of three months or less from dates of acquisition and are subject to an insignificant risk of changes in value.

Financial Assets and Financial Liabilities Financial assets and financial liabilities are recognized initially at fair value. Transaction

costs are included in the initial measurement of all financial assets and liabilities, except for financial instruments measured at fair value through profit and loss. Fair value is determined by reference to the transaction price or other market prices. If such market prices are not readily determinable, the fair value of the consideration is estimated as the sum of all future cash payments or receipts, discounted using the prevailing market rates of interest for similar instruments with similar maturities.

The Group recognizes a financial asset or a financial liability in the consolidated balance sheet when it becomes a party to the contractual provisions of the instrument.

Financial assets are classified into the following categories: a. Financial asset at fair value through profit or loss b. Loan and receivable c. Held-to-maturity investment d. Available-for-sale financial asset

Financial liabilities, on the other hand, are classified into the following categories: a. Financial liability at fair value through profit or loss b. Other liability

21

The Group determines the classification at initial recognition and, where allowed and appropriate, re-evaluates this classification at every reporting date.

a. Financial assets or financial liabilities at fair value through profit or loss

Financial assets or financial liabilities classified in this category are designated by management on initial recognition when the following criteria are met:

The designation eliminates or significantly reduces the inconsistent treatment that would otherwise arise from measuring the assets or recognizing gains or losses on them on a different basis, or

The assets and liabilities are part of a group of financial assets and financial liabilities, respectively, or both financial assets and financial liabilities, which are managed and their performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, or

The financial instrument contains an embedded derivative, unless the embedded derivative does not significantly modify the cash flows or it is clear, with little or no analysis, that it would not be separately recorded.

Financial assets and financial liabilities at fair value through profit or loss are recorded in the consolidated balance sheet at fair value. Changes in fair value are recorded in trading gain - net on financial assets and financial liabilities designated at fair value through profit or loss. Interest earned is recorded in interest income, while dividend income is recorded in other income according to the terms of the contract, or when the right of the payment has been established. Interest incurred is recorded in interest expense.

The Company has not designated any financial asset or financial liability as at fair value through profit or loss.

b. Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise when the Group provides money, goods or services directly to a debtor with no intention of trading the receivables. Loans and receivables are carried at cost or amortized cost in the consolidated balance sheet. Amortization is determined using the effective interest rate method. Loans and receivables are included in current assets if maturity is within twelve months from the balance sheet date. Otherwise, these are classified as noncurrent assets.

Classified as loans and receivables are the Group’s trade receivables, and advances to officers and employees.

c. Held-to-maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities wherein the Group has the positive intention and ability to hold to maturity. Held-to-maturity investments are carried at cost or amortized cost in the consolidated balance sheet. Amortization is determined using the effective interest rate method. Assets under this category are classified as current assets if maturity is within 12 months from the balance sheet date and noncurrent assets if maturity is more than a year.

22

The Group has not designated any financial asset as held-to-maturity.

d. Available-for-sale financial assets

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. Available-for-sale financial assets are carried at fair value in the consolidated balance sheet. Changes in the fair value of investments classified as available-for-sale financial assets are recognized in equity, except for the foreign exchange fluctuations on available-for-sale debt securities and the related effective interest which are taken directly to the consolidated statement of income. These changes in fair values are recognized in equity until the investment is sold, collected or otherwise disposed of, or until the investment is determined to be impaired, at which time the cumulative gain or loss previously reported in equity is included in the consolidated statement of income.

The Group has not designated any financial asset as available-for-sale.

e. Other financial liabilities

This category pertains to financial liabilities that are not held for trading or not designated as fair value through profit or loss upon the inception of the liability. These include liabilities arising from operations (e.g., payables, accruals).

The liabilities are recognized initially at fair value and are subsequently carried at amortized cost, taking into account the impact of applying the effective interest method of amortization (or accretion) for any related premium, discount and any directly attributable transaction costs.

Derecognition of Financial Assets and Financial LiabilitiesFinancial assets

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognized when:

a. the rights to receive cash flows from the asset have expired;

b. the Group retains the right to receive cash flows from the asset, but has assumed an obligation to pay them in full without material delay to a third party under a ‘pass-through’ arrangement; or

c. the Group has transferred its rights to receive cash flows from the asset and either (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Where the Group has transferred its rights to receive cash flows from an asset and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the asset is recognized to the extent of the Group’s continuing involvement in the asset.

Financial liabilities A financial liability is derecognized when the obligation under the liability is discharged or

cancelled or expires.

Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the

23

recognition of a new liability, and the difference in the respective carrying amounts is recognized in profit or loss.

Impairment of Financial AssetsThe Group assesses at each balance sheet date whether a financial asset or a group of financial assets is impaired.

a. Assets carried at amortized cost

If there is objective evidence that an impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rates (i.e., the effective interest rate computed at initial recognition). The carrying amount of the asset shall be reduced either directly or through the use of an allowance account. The amount of loss, if any, is recognized in the consolidated statement of income.

The Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and collectively for financial assets that are not individually significant. If it is determined that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, the asset is included in the group of financial assets with similar credit risk and characteristics and that group of financial assets is collectively assessed for impairment. Assets that are individually assessed for impairment and for which an impairment loss is recognized are not included in a collective assessment of impairment.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed. Any subsequent reversal of an impairment loss is recognized in the consolidated statement of income, to the extent that the carrying value of the asset does not exceed its amortized cost at the reversal date.

b. Assets carried at cost

If there is an objective evidence that an impairment loss of an unquoted equity instrument that is not carried at fair value because its fair value cannot be reliably measured, or a derivative asset that is link to and must be settled by delivery of such an unquoted equity instrument has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the current market rate of return for a similar financial asset.

c. Available-for-sale financial assets

If an available-for-sale financial asset is impaired, the amount comprising the difference

between its cost (net of any principal payment and amortization) and its current fair value,

less any impairment loss previously recognized in the consolidated statement of income,

is transferred from equity to the consolidated statement of income. Reversals in respect

of equity instruments classified as available-for-sale are not recognized in the

consolidated statement of income. Reversals of impairment losses on debt instruments

are reversed through the consolidated statement of income, if the increase in fair value of

the instrument can be objectively related to an event occurring after the impairment loss

was recognized in the consolidated statement of income.

24

Offsetting Financial Instruments Financial assets and financial liabilities are offset and the net amount reported in the

consolidated balance sheet if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. This is not generally the case with master netting agreements, and the related assets and liabilities are presented gross in the consolidated balance sheet.

Inventories Inventories are stated at the lower of cost and net realizable value (NRV). Costs incurred in

bringing the product to its present location and condition are accounted for at purchase cost, determined primarily on the basis of the moving average method.

NRV of food and beverage is the estimated selling price in the ordinary course of business less the estimated costs of completion and estimated costs necessary to make the sale. In the case of materials and supplies, NRV is the recoverable value of the inventories when disposed of at their current conditions.

Property and Equipment Property and equipment are stated at cost, less accumulated depreciation and amortization

and any impairment in value.

The initial cost of property and equipment comprises of its purchase price, including import duties, taxes, borrowing costs and any directly attributable costs of bringing the asset to its working condition and location for its intended use. Expenditures incurred after the property and equipment have been put into operation, such as repairs and maintenance and overhaul

costs, are normally charged to operations in the period when the costs are incurred. Insituations where it can be clearly demonstrated that the expenditures have resulted in an increase in the future economic benefits expected to be obtained from the use of an item of property and equipment beyond its originally assessed standard of performance, the expenditures are capitalized as an additional cost of property and equipment.

Construction in progress, included in property and equipment, is stated at cost. This includes cost of construction, equipment and other direct costs. Borrowing costs that are directly attributable to the construction of equipment are capitalized during the construction period. Construction in progress is not depreciated until such time as the relevant assets are completed and become available for use.

Each part of an item of property and equipment with a cost that is significant in relation to the total cost of the item is depreciated separately.

Except for a helicopter unit, which is depreciated based on flying hours, depreciation is computed using the straight-line method over the estimated useful lives of the assets as follows:

No. of years

Building 25Kitchen and other operations equipment 3 to 10Office furniture, fixtures and equipment 3 to 7Transportation equipment 5Helicopter spare parts 3 to 5 Aviation equipment 5

Building and leasehold improvements are amortized over the terms of the leases or the lives of the assets (which range from two to five years), whichever is shorter.

25

Depreciation and amortization of an item of property and equipment begins when it becomes available for use, i.e., when it is in the location and condition necessary for it to be capable of operating in the manner intended by management. Depreciation and amortization ceases at the earlier of the date that the item is classified as held for sale (or included in a disposal group that is classified as held for sale) in accordance with PFRS 5, Noncurrent Assets Held for Sale and Discontinued Operations, and the date the asset is derecognized.

The residual values, useful lives and depreciation and amortization methods are reviewed periodically to ensure that the residual values, periods and methods of depreciation and amortization are consistent with the expected pattern of economic benefits from items of property and equipment.

When property and equipment are sold or retired, their cost and related accumulated depreciation and amortization and any impairment in value are removed from the accounts, and any gain or loss resulting from their disposal is included in the consolidated statement of income.

Investment PropertyInvestment property pertains to land held for appreciation in value that is measured at cost less any impairment in value.

Investment property is derecognized when it has either been disposed of or when the investment property is permanently withdrawn from use and no future benefit is expected from its disposal. Any gains or losses resulting from the derecognition of an investment property is recognized in the consolidated statement of income in the year of derecognition.

Impairment of Non-financial Assets The Group assesses at each reporting date whether there is an indication that property and

equipment, investment property and goodwill may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the Group makes an estimate of the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. Where the carrying amount of an asset exceeds its recoverable value, the asset is considered impaired and is written down to its recoverable amount. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of time value of money and the risks specific to the asset. Impairment losses of continuing operations are recognized in the consolidated statement of income in those expense categories with the function of the impaired asset.

An assessment is made at each reporting date as to whether there is any indication that previously recognized impairment losses may no longer exist or may have decreased. If such indication exists, the recoverable amount is estimated. A previously recognized impairment loss is reversed only if there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognized. If that is the case, the carrying amount of the asset is increased to its recoverable amount. That increased amount cannot exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognized for the asset in prior years. Such reversal is recognized in profit or loss unless the asset is carried at revalued amount, in which case the reversal is treated as a revaluation increase. After such a reversal, the depreciation charge is adjusted in future periods to allocate the asset’s revised carrying amount, less any residual value, on a systematic basis over its remaining useful life.

26

Deferred Mine Exploration Costs Expenditures for mine exploration works on mining properties are deferred as incurred and

included under the “Deposits and other noncurrent assets” in the consolidated balance sheet. When, as a result of the exploration work, recoverable reserves are determined to be present in quantities that can be commercially produced, exploration expenditures and subsequent development costs are capitalized as mine and mining properties and classified as part of property and equipment.

A valuation allowance is provided for estimated unrecoverable costs based on the technical assessment by the Group of the future prospects of each mining property. When a project is abandoned, the related deferred mine exploration costs are written-off.

Revenue Revenue is recognized to the extent that it is probable that the economic benefits associated with the transactions will flow to the Group and the revenue can be reliably measured.

Sale of goods Catering revenue is recognized upon delivery of goods to and acceptance by airline clients

and other customers.

Rendering of services Revenue from ground handling and aviation and administrative services, and charter flights is

recognized when the related services are rendered.

Rental income Rental income is accounted for on a straight-line basis over the lease term.

Interest income Interest income is recognized as the interest accrues using, where applicable, the effective interest method, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial assets to the net carrying amount of the financial asset.

Retirement Benefits Costs Retirement benefits costs are actuarially determined using the projected unit credit method.

Actuarial gains and losses are recognized as income or expense when the net cumulative unrecognized actuarial gains and losses for the plan at the end of the previous reporting year exceeded 10% of the higher of the defined benefit obligation and the fair value of plan assets at that date. These gains or losses are recognized over the expected average remaining working lives of the employees participating in the plan.

Past service cost is recognized as an expense on a straight-line basis over the average period until the benefits become vested. If the benefits are already vested immediately following the introduction of, or changes to, a retirement plan, past service cost is recognized immediately.

The defined benefit liability is the aggregate of the present value of the defined benefit obligation and actuarial gains and losses not recognized, reduced by past service cost not yet recognized, and the fair value of plan assets out of which the obligations are to be settled or the aggregate of cumulative unrecognized net actuarial losses and past service cost and the present value of any economic benefits available in the form of refunds from the plan or reductions in the future contributions to the plan.

If the asset is measured at the aggregate of cumulative unrecognized net actuarial losses and past service cost and the present value of any economic benefits available in the form of refunds from the plan or reductions in the future contributions to the plan, net actuarial losses

27

of the current period and past service cost of the current period are recognized immediately to the extent that they exceed any reduction in the present value of those economic benefits. If there is no change or an increase in the present value of economic benefits, the entire net actuarial losses of the current period and past service cost of the current period are recognized immediately to the extent that they exceed any reduction in the present value of those economic benefits. Similarly, net actuarial gains of the current period after the deduction of past service cost of the current period exceeding any increase in the present value of the economic benefits stated above are recognized immediately if the asset is measured at the aggregate of cumulative unrecognized net actuarial losses and past service cost and the present value of any economic benefits available in the form of refunds from the plan. If there is no change or a decrease in the present value of the economic benefits, the entire net actuarial gains of the current period after the deduction of past service cost of the current period are recognized immediately.

Borrowing CostsBorrowing costs are generally expensed as incurred. Borrowing costs are capitalized if they are directly attributable to the acquisition or construction of a qualifying asset. Capitalization of borrowing costs commences when the activities to prepare the asset are in progress and expenditures and borrowing costs are being incurred. Borrowing costs are capitalized until the assets are substantially ready for their intended use.

Operating Leases Lease expense (income) under an operating lease agreement is recognized in the

consolidated statement of income as expense (income) on a straight-line basis over the lease term.

Provisions and Contingencies Provisions are recognized when the Group has a present obligation (legal or constructive) as

a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation. If the effect of the time value of money is material, provisions are determined by discounting the effective future cash flows at a pretax rate that reflects current market assessment of the time value of money and where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provisions due to the passage of time is recognized as an interest expense.

Contingent liabilities are not recognized in the consolidated financial statements. These are disclosed unless the possibility of an outflow of resources embodying economic benefits is remote. A contingent asset is not recognized in the consolidated balance sheet but disclosed when an inflow of economic benefits is probable.

Income TaxCurrent tax

Current tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted at the balance sheet date.

Deferred tax Deferred tax assets and liabilities are provided, using the balance sheet liability method, on

all temporary differences at the balance sheet date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred tax liabilities are recognized for all taxable temporary differences. Deferred tax assets are recognized for all deductible temporary differences, carryforward benefits of excess minimum corporate income tax (MCIT) over the regular corporate income tax (RCIT),

28

and net operating loss carryover (NOLCO), to the extent that it is probable that taxable profit will be available against which the deductible temporary differences and the carryforward benefits of excess MCIT and unused NOLCO can be utilized. Deferred income tax, however, is not recognized when it arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit.

Deferred tax liabilities are not provided on non-taxable temporary differences associated with investments in domestic subsidiaries, associates and interest in joint ventures. With respect to investments in other subsidiaries, associates and interests in joint ventures, deferred tax liabilities are recognized except where the timing of the reversal of the temporary difference can be controlled and it is probable that the temporary difference will not reverse in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at each balance sheet date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax assets to be utilized. Unrecognized deferred tax assets are reassessed at each balance sheet date and are recognized to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the balance sheet date.

Deferred tax assets and deferred tax liabilities are offset if a legally enforceable right exists to set off the deferred tax assets against the deferred tax liabilities and the deferred taxes relate to the same taxable entity and the same taxation authority.

Income tax relating to items recognized directly in equity is recognized in equity and not in the consolidated statements of income.

Events After the Balance Sheet DatePost-year-end events that provide additional information about the Group’s position at the balance sheet date (adjusting events), if any, are reflected in the consolidated financial statements.

Post-year-end events that are not adjusting events are disclosed in the notes to consolidated financial statements when material.

Earnings Per Share Basic earnings per share is computed by dividing net income for the year attributable to

ordinary equity holders of the parent by the weighted average number of shares outstanding during the year.

Diluted earnings per share amounts are calculated by dividing the net profit by the weighted average number of ordinary shares outstanding during the year plus the weighted average number of ordinary shares that would be issued upon conversion of all dilutive potential ordinary shares. Currently, the Group has no potential dilutive shares.

Future Changes in Accounting Policies

The following are the new accounting standards and Philippine Interpretation International

Financial Reporting Interpretations Committee (IFRIC) interpretations that will become

effective subsequent to 2006:

PFRS 7, Financial Instruments: Disclosures, and the complementary amendment to PAS

1, Presentation of Financial Statements: Capital Disclosures (effective for annual periods

29

beginning on or after January 1, 2007), introduces new disclosures to improve the

information about financial instruments. It requires the disclosure of qualitative and

quantitative information about exposure to risks arising from financial instruments,

including specified minimum disclosures about credit risk, liquidity risk and market risk, as

well as sensitivity analysis to market risk. It replaces PAS 30, Disclosures in the

Financial Statements of Banks and Similar Financial Institutions, and the disclosure

requirements of PAS 32, Financial Instruments: Disclosure and Presentation. It is

applicable to all entities that report under PFRS. The amendment to PAS 1 introduces

disclosures about the level of an entity’s capital and how it manages capital.

PFRS 8, Operating Segments (effective for annual periods beginning on or after January

1, 2009), requires a management approach to reporting segment information. PFRS 8

will replace PAS 14, Segment Reporting, and is required to be adopted only by entities

whose debt or equity instruments are publicly traded, or are in the process of filing with

the Philippine SEC for purposes of issuing any class of instruments in a public market.

Philippine Interpretation IFRIC 7, Applying the Restatement Approach under PAS 29,

Financial Reporting in Hyperinflationary Economies (effective for annual periods

beginning on or after March 1, 2006), provides guidance on how to apply PAS 29 when

an economy first becomes hyperinflationary, in particular the accounting for deferred tax.

Philippine Interpretation IFRIC 8, Scope of PFRS 2 (effective for annual periods

beginning on or after May 1, 2006), requires PFRS 2 to be applied to any arrangements

where equity instruments are issued for consideration which appears to be less than fair

value.

Philippine Interpretation IFRIC 9, Reassessment of Embedded Derivatives (effective for

annual periods beginning on or after June 1, 2006), establishes that the date to assess

the existence of an embedded derivative is the date an entity first becomes a party to the

contract, with reassessment only if there is a change to the contract that significantly

modifies the cash flows.

Philippine Interpretation IFRIC 10, Interim Financial Reporting and Impairment (effective

for annual periods beginning on or after November 1, 2006), prohibits the reversal of

impairment losses on goodwill and available for sale equity investments recognized in the

interim financial reports even if impairment is no longer present at the annual balance

sheet date.

Philippine Interpretation IFRIC 11, PFRS 2 - Group and Treasury Share Transactions,