Embed Size (px)

Citation preview

Topics

1

v PFM cycle; as per PFMR (2013-2018)

v PFM reforms in kenya – focus on accounting and IFMIS;

v Accounting Standards applicable in Kenya;

v IFMIS implementation in Kenya – successes and challenges

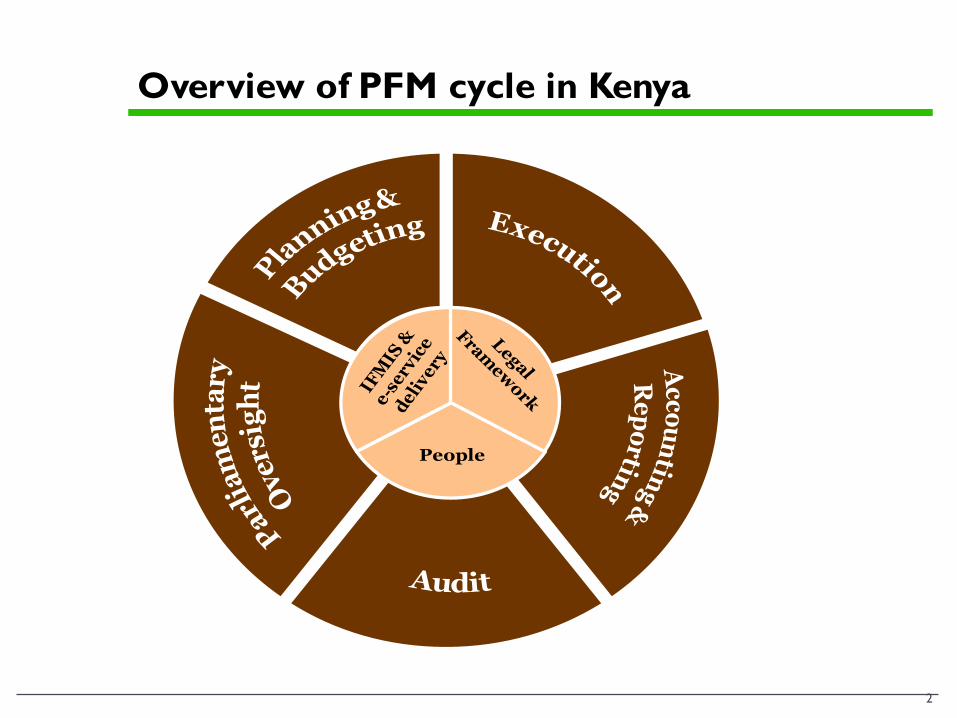

Overview of PFM cycle in Kenya

2

People

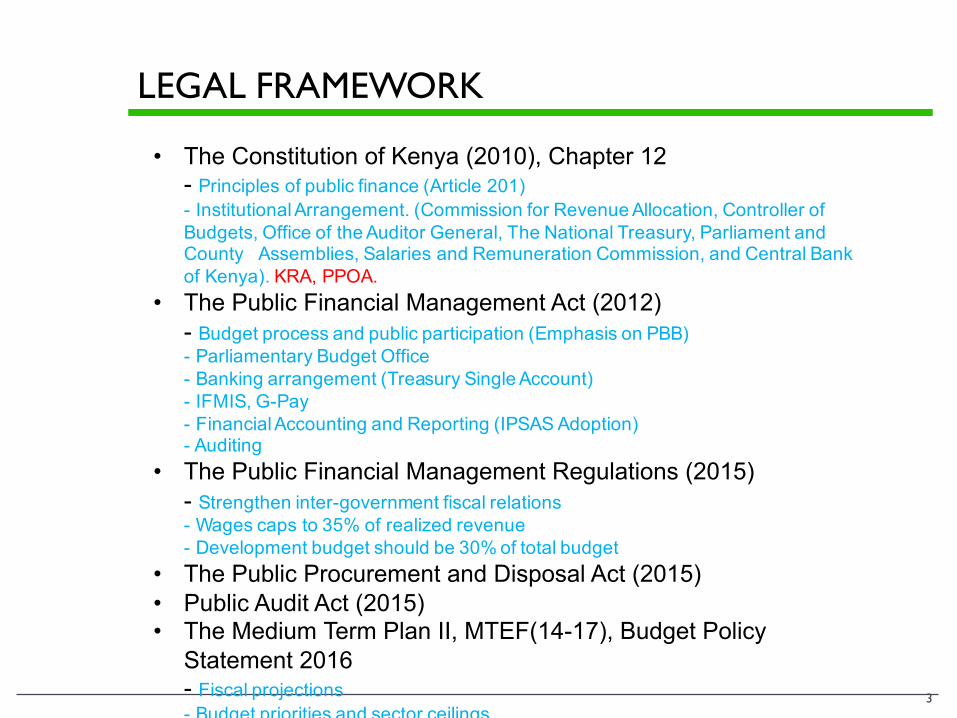

LEGAL FRAMEWORK

3

• The Constitution of Kenya (2010), Chapter 12- Principles of public finance (Article 201)- Institutional Arrangement. (Commission for Revenue Allocation, Controller of Budgets, Office of the Auditor General, The National Treasury, Parliament and County Assemblies, Salaries and Remuneration Commission, and Central Bank of Kenya). KRA, PPOA.

• The Public Financial Management Act (2012)- Budget process and public participation (Emphasis on PBB)- Parliamentary Budget Office- Banking arrangement (Treasury Single Account)- IFMIS, G-Pay- Financial Accounting and Reporting (IPSAS Adoption)- Auditing

• The Public Financial Management Regulations (2015)- Strengthen inter-government fiscal relations- Wages caps to 35% of realized revenue- Development budget should be 30% of total budget

• The Public Procurement and Disposal Act (2015)• Public Audit Act (2015)• The Medium Term Plan II, MTEF(14-17), Budget Policy

Statement 2016- Fiscal projections - Budget priorities and sector ceilings

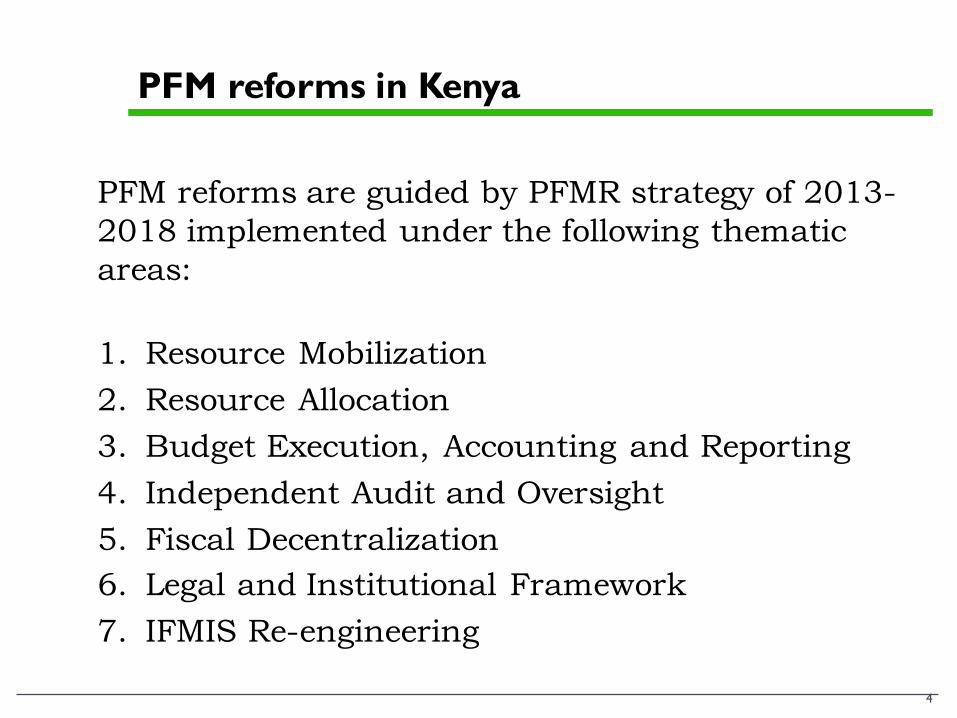

PFM reforms in Kenya

4

PFM reforms are guided by PFMR strategy of 2013-2018 implemented under the following thematic areas:

1. Resource Mobilization2. Resource Allocation 3. Budget Execution, Accounting and Reporting 4. Independent Audit and Oversight 5. Fiscal Decentralization 6. Legal and Institutional Framework 7. IFMIS Re-engineering

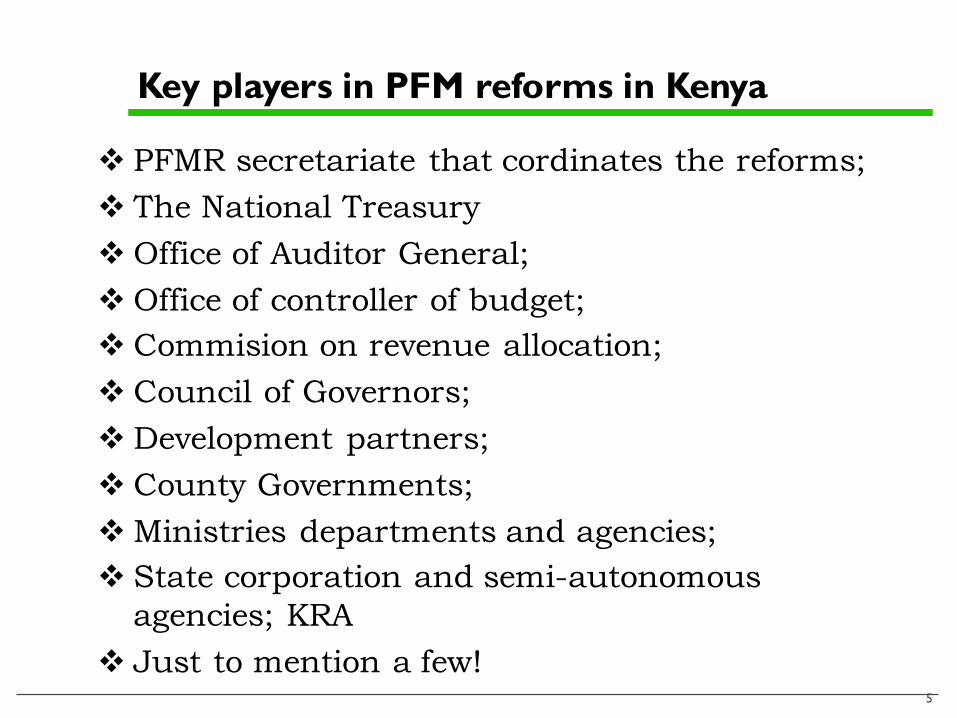

Key players in PFM reforms in Kenya

5

v PFMR secretariate that cordinates the reforms;v The National Treasuryv Office of Auditor General;v Office of controller of budget;v Commision on revenue allocation;v Council of Governors;v Development partners;v County Governments;v Ministries departments and agencies;v State corporation and semi-autonomous

agencies; KRAv Just to mention a few!

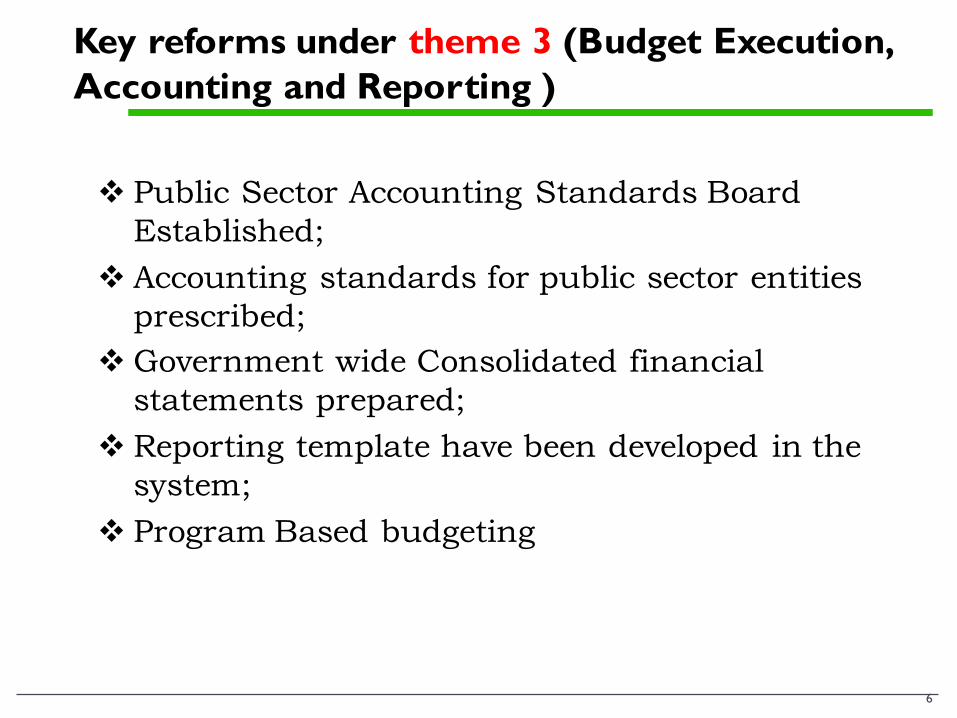

Key reforms under theme 3 (Budget Execution, Accounting and Reporting )

6

v Public Sector Accounting Standards Board Established;

v Accounting standards for public sector entities prescribed;

v Government wide Consolidated financial statements prepared;

v Reporting template have been developed in the system;

v Program Based budgeting

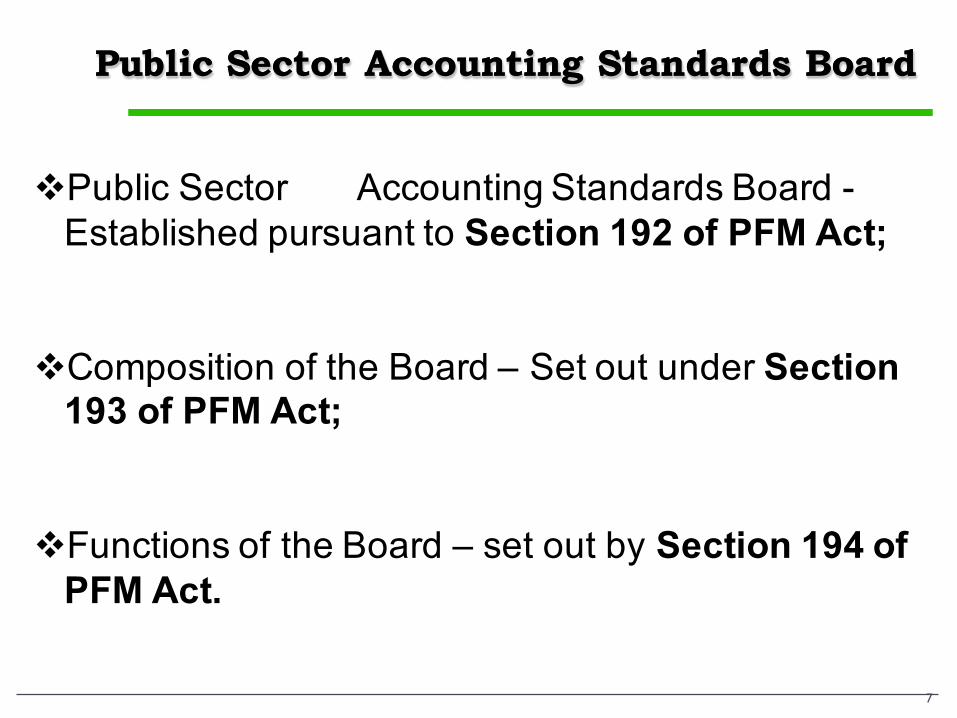

Public Sector Accounting Standards BoardPublic Sector Accounting Standards Board

7

vPublic Sector Accounting Standards Board -Established pursuant to Section 192 of PFM Act;

vComposition of the Board – Set out under Section 193 of PFM Act;

vFunctions of the Board – set out by Section 194 of PFM Act.

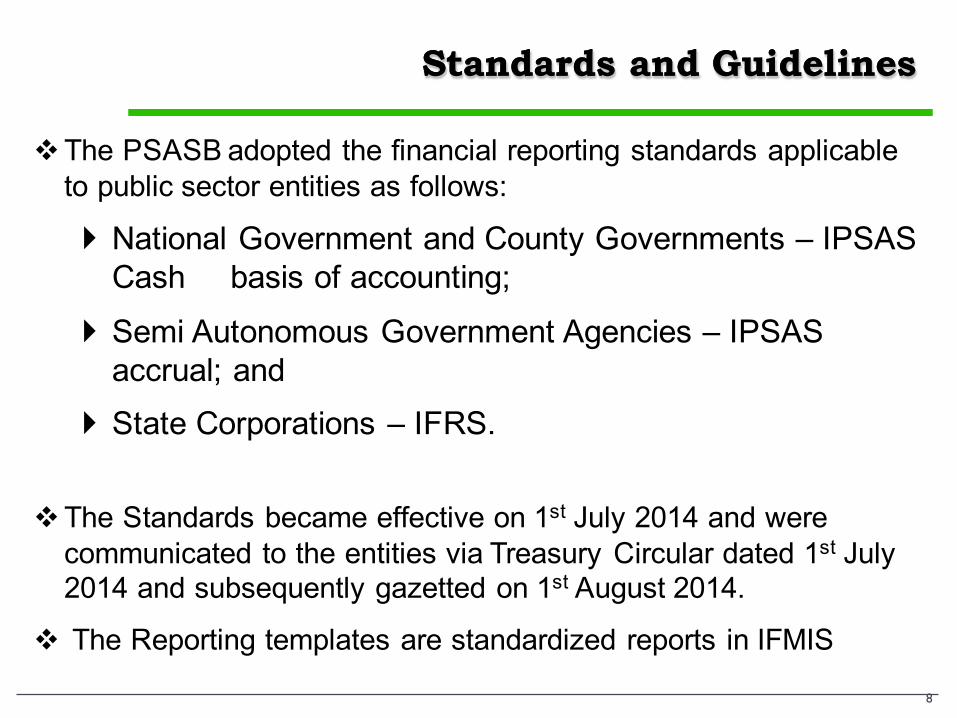

Standards and GuidelinesStandards and Guidelines

8

vThe PSASB adopted the financial reporting standards applicable to public sector entities as follows:

} National Government and County Governments – IPSAS Cash basis of accounting;

} Semi Autonomous Government Agencies – IPSAS accrual; and

} State Corporations – IFRS.

vThe Standards became effective on 1st July 2014 and were communicated to the entities via Treasury Circular dated 1st July 2014 and subsequently gazetted on 1st August 2014.

v The Reporting templates are standardized reports in IFMIS

Implementation of standardsImplementation of standards

9

v All entities are required to prepare their Financial Statements based on the issued standards and guidelines;

vTraining has been carried out and has covered finance officers of all public sector entities;

vTechnical Assistance procured from EY, Deloitte and PwC in capacity building, quality reviews and preparation of financial statements;

vThe Standards enabled The National Treasury prepare Consolidated Financial Statements for public entities as per PFM Act (Section 80); Important audited statistics on actual revenue, expenditure and public debt that can guide future planning.

vConvergence with GFS being explored.

vCapacity building targeting internal and external auditors carried out to ensure all are reading from same page.

Consolidation of FS for the Gov. of KenyaConsolidation of FS for the Gov. of Kenya

10

v First ever consolidated financial statements were prepared by Accountant General department relating to FY 2013/14.

vSecond consolidated financial statements prepared relating to FY 2014/15;

vConsolidation done in two parts i.e National Govt. MDAs (Using cash based IPSAS) and State Corporations and SAGAs (Using IPSAS Accrual and IFRS).

vConsolidations done within statutory deadline of 30th

October.

PROGRAMME BASED BUDGETING

11

u A requirement by the PFM Act 2012 that budget be prepared on both line basis and programme basis from 2013/14. Programme priorities will be determined by MTP II, respective MTEF and BPS.

u Important for the PFM that the budget is credible.u Important for County government budgeting where

functions were devolved as programmes. Important to link inputs with outputs/outcomes. Case of free primary education.

u Kenya still uses line expenditure votes in budget execution but plans to move to programme based budgets in 2016/17 as per BPS 2016. Budget will be keyed in IFMIS on a programme basis.

u KPI will be done bottom up and moderated by the NT.

Key ChallengesKey Challenges

12

Key ChallengesKey Challenges

13

IPSAS Adoption

•As expected, entities had difficulties in complying with international standards adopted by the PSASB during the 1st and 2nd year of implementation. Levels of disclosures are higher

•Human resource capacity constraints– comprehensive change management, training and capacity building programme required.

•Financial statements for National Government entities exclude liabilities and physical assets. These are progressively being added to the financial statements as capacity is built.

Key ChallengesKey Challenges

14

IPSAS Adoption

• Suspense accounts, automated bank reconciliation, inter-entity transfers and unsupported balances in the FS are a key challenge but these are being eliminated as entities build capacity.

• Consolidation of close to 650 public entities and 410 projects eliminating minority interest is a challenge. Only entities that the government control is above 50% is consolidated.

• How to consolidate entities where the Auditor General has issued a disclaimer.

• How to account for and consolidate the approximately 27,000 primary and 9000 secondary schools.

• Quarterly financial reports as per PFM Act

Key ChallengesKey Challenges

15

Budget Execution

-Designing a credible budget: Reducing Supplementary and budget revisions. Improving fiscal forecasting. -Together with the CoB, enforce budgetary principles: 30:60 ratios between recurrent and development, not more than 35% of revenues to go to wages.-All revenues be deposited in CRF accounts with CBK-National and County governments adhere to E-procurement module in IFMIS-Borrowings be used only for purposes for development projects -Implementing Programme based budgeting to link inputs and outcomes and devolve budget decisions to MDA’s.- Cash management and prioritization. Implementing the TSA at both National and County levels. - Eliminate wastage and duplication between the two levels of government: Roads and Health services

Next Steps!Next Steps!

16

• Improvements to the reporting templates – currently on-going.

• Intensified trainings to enhance compliance standards

• Emphasis is on comprehensive disclosures in readiness for adoption of IPSAS accrual

• Quarterly government consolidation as per requirement of the PFM Act is being pursued.

• Implementing programme based budgeting and ensuring National budgets are self financing

• Streamlining County level PFM especially in revenue collection

IFMISTransformation of Doing Business in

Government

Integrated Financial Management Information System (IFMIS) in Kenya

18

} PFM Act (12e). National Treasury to design and prescribe an efficient financial management system as contemplated in Article 226 of the Constitution.

} An automated system that is used for public financial management that interlinks planning, budgeting, expenditure management , control, accounting, audit and reporting.

} Oracle platform - Web based;} IFMIS launched in 2003;} IFMIS Re-engineering commenced in 2011.

IFMIS Components

19

IFMIS Vision“An excellently secure, reliable,

efficient, effective and fully integrated financial management

system”

Plan to Budget Revenue to Cash Procure to Pay Record to

Report

PFM Vision“A PFM system that is efficient, effective and equitable for transparency,

accountability and improved service delivery”

Re-Engineering for Improved Business Results

ICT to Support

Communicate to Change

Integrated Financial Management Information System (IFMIS) in Kenya

20

} Re-engineering for Business Results: The objective of this component is to re-engineer business processes for improved financial management.

} Plan to Budget: The objective of this component is to develop a fully integrated process and system that links planning, policy objectives and budget allocation.

} Procure to Pay: This component aimed at having an automated procurement process from requisition, tendering, evaluation, contract award and payment.

Integrated Financial Management Information System (IFMIS) in Kenya

21

} Revenue to Cash and Record to Report: These two components are aimed at capturing financial data in a uniform and consistent manner, and timely reconciliation of bank accounts to facilitate generation of the necessary management and statutory reports.

} ICT to support: The aim of this component was to develop a dedicated IFMIS support function for software, hardware and infrastructure.

} Communicate to Change: The component aimed at facilitating a process of change management through communication and capacity building.

Scope and status of roll out

22

} Rolled out to all National Government Ministries, Departments and Agencies;

} Rolled out to all the 47 County Governments;

} The roll out has been done on all IFMIS modules.

Key reforms under theme 7 (IFMIS)

23

v Full roll out of IFMIS to MDA - 98% achieved;v Full roll out to County Governments – 100%

achieved;v Roll out of Eprocurement - has taken root;v Statutory reporting through IFMIS - templates

have been developed in the system;v Cash management practices are being automated

in the IFMIS system;v Asset management module in IFMIS being

worked on.

Achievements attributed to IFMIS

24

} Efficiency procurement: - eprocurement platform rolled out in fy 2014/15 has resulted in transparency and value for money in procurements.

} Budget control: - overspending has been contained through budget controls inbuilt in the system.

} Reporting: - timely report noting that all statutory reports have been automated.

} Payment process: – enhanced internal control in the payment process.

} Operational efficiency: - manual process have been automated.

Critical success factors

25

} Training and capacity building: - Establishment of the IFMIS academy played a role in building a critical mass of trained users.

} Leadership support: - support from top leadership and funding has played a key role in success of system.

} Management of dependancies: - require understanding of different user requirements & integrations requirements for other systems.

} Legislative backing: - more needs to be done in terms of enacting enabling legislations for e-business.

Areas of further improvement

26

} Asset management module: - roll out of asset management module is still at it nascent stage.

} Cash/treasury management: - automation of cash release process from national treasury is ongoing.

} Integration with KRA: - the process of integration is ongoing.

} Key in budget from a programme perspective} Connectivity issues especially for far flung Counties} Help desk management: - improvements are being

made to support the users more effectively.

27

Thank you

![P Murphy, IFMIS Nairobi November 2004 1 Perspectives on IFMIS Implementation in selected Sub-Saharan African Countries [P. Murphy]](https://img.dokumen.tips/doc/110x75/551b5026550346ae7a8b5228/p-murphy-ifmis-nairobi-november-2004-1-perspectives-on-ifmis-implementation-in-selected-sub-saharan-african-countries-p-murphy.jpg)