Embed Size (px)

Citation preview

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

1

The Implementation of the XIII Directive:

Germany

European Takeover Law: The State of the Art

Università Commerciale Luigi Bocconi

15 December 2008

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

2

I. IntroductionII. German takeover law: selected featuresIII. ControlIV. Mandatory bidV. Takeover bidVI. The default rule for target companies: limited passivityI. The opt-in/opt-out regime for (target) companiesVIII. The right of squeeze-outIX. Concluding remarks

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

3

I. Introduction– Takeover law

• Act on the Acquisition of Securities and on Takeovers(the “Act”) (2002)- major amendments- Act on the Implementation of the Takeover Directive

(2006)- Risk Limitation Act: extension of the acting in concert

(August 2008)• Regulation on the Contents of the Offer Document, the

Consideration in the Case of Takeover Bids and Mandatory Bids and the Exemption from the Obligation to Publish and Make a Bid (the “Bid Regulation“)

– Stock Corporation Act, Securities Trading Act, Commercial Code

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

4

– Act on the Acquisition of Securities and on Takeovers: Table of Contents

- General Provisions- Jurisdiction of the Federal Financial Authority (“BaFin”)- Offers for the Acquisition of Securities- Takeover Bids- Mandatory Offers- Squeeze-out, the Right of Sell-out- Procedures- Legal Remedies- Penalties- Jurisdiction of Courts, Transitional Arrangements

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

5

II. German takeover law: selected features– Three types of bids regulated

• mandatory bid

• takeover bid: bid aimed at acquiring control

• simple bid: bid not aimed at acquiring control

– Interrelation between takeover bids and mandatory bids • requirements for both bids are (nearly) identical, e.g.

– mandatory price rules for voluntary takeover bids

– no partial takeover bid allowed

• consequence: no mandatory bid required upon acquisition of control as a result of a takeover bid (Sect. 35(3) of the Act)

– Frustrating actions available to a target: severely limited– Squeeze-out: transfer of shares by court order

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

6

III. Control– Threshold for control: 30 % of the voting rights of the target

company at a minimum (Sect. 29(2) of the Act)– Attribution of voting rights: Sect. 30 of the Act

• identical to Sect. 22 of the Securities Trading Act?» transposition of Art. 10 of the Transparency Directive

– national level:» German legislator» but: different objectives

– European Securities Markets Expert Group

– Lateral attribution of voting rights to the offeror:if the offeror is able to control how the voting rights will be exercised in a shareholder meeting (Sect. 30(1) of the Act)

• chain principle applies in attributing votes

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

7

– Schaeffler KG acquisition of Continental AG- Facts

- direct holdings: 2,97% (+ 4,95 % qua financial instruments)- total return equity swaps with 9 banks: 28 %

- Merrill Lynch as coordinator- banks‘ holdings below 3 %-threshold - total return equity swap: cash settlement only- but: banks will sell to a bidder

- Problems- unilateral attribution of voting rights?

- “voting rights of a third party which are held by such third party for the account of the offeror“ (Sect. 30(1)(1) No. 2 of the Act = Sect. 22(1)(1) No. 2 of the Securities Trading Act)

- Schaeffler able to control bank‘ use of voting rights?- bid enforcement mechanisms available to BaFin?

- Future

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

8

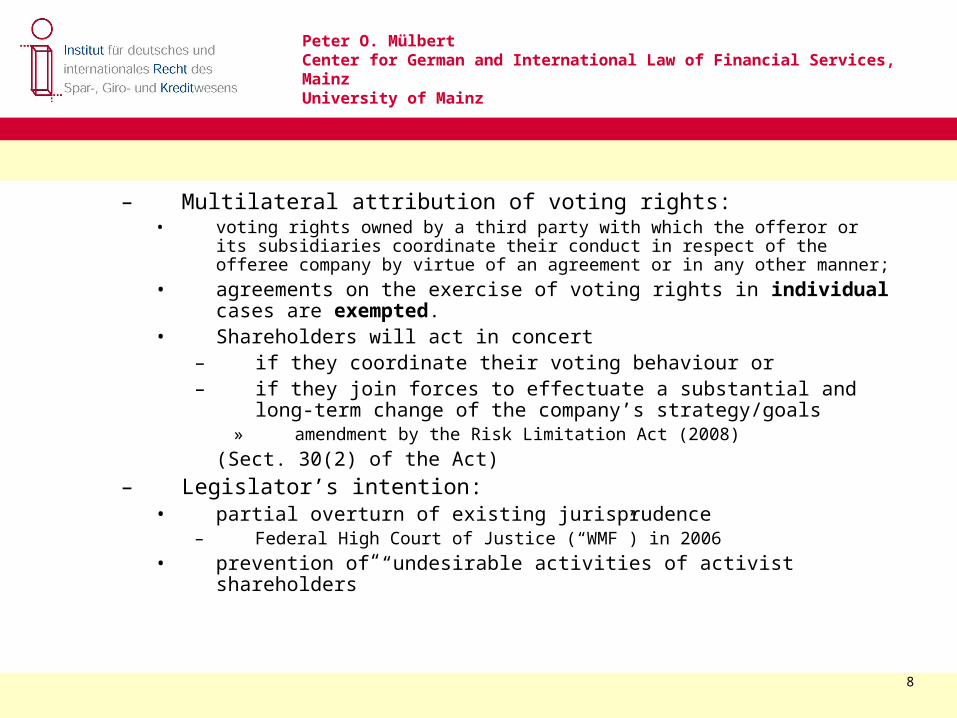

– Multilateral attribution of voting rights:• voting rights owned by a third party with which the offeror or its subsidiaries

coordinate their conduct in respect of the offeree company by virtue of an agreement or in any other manner;

• agreements on the exercise of voting rights in individual cases are exempted.

• Shareholders will act in concert – if they coordinate their voting behaviour or– if they join forces to effectuate a substantial and long-term

change of the company’s strategy/goals» amendment by the Risk Limitation Act (2008)

(Sect. 30(2) of the Act)

– Legislator’s intention:• partial overturn of existing jurisprudence

– Federal High Court of Justice (“WMF”) in 2006

• prevention of “undesirable activities of activist shareholders”

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

9

- But: limited impact of revision- co-ordinated exercise of votes

– election of supervisory board members (still) exempt– co-ordinated rejection of board-sponsored voting

proposals (authorized capital) admissible- co-ordinated exercise of influence by other means

- means» co-ordination on the level of the supervisory board?

– substantial and long-term change of business» business model alteration, sale of a major subsidiary

– exemption for one-time changes available?» election of the chairman of the supervisory board

(„WMF“)» change of business

-

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

10

- Parallel acquisition of shares as a concerted action?– legislator´s stated intention v. legislative intention

» Schaeffler/Conti case– required by Art. 2(1)(d) of the Directive?

- Acting in concert (Art. 2(1)(d) of the Directive): “persons who cooperate with the offeror … on the basisof an agreement … aimed at acquiring control”

– “acquiring control”:» “pure” acquisition principle?» acquisition as a minimum requirement?» co-ordinating the exercise of votes sufficient?

– minimum or maximum harmonisation?

-

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

11

IV. Mandatory bids (Sect. 35 to 39 of the Act)– Persons required to make a bid:

anyone who directly or indirectly gains control (Sect. 35)• indirectly controlled company

– subsidiary as sole target– subsidiary of a target company

» BaFin may grant an exception for small subsidiaries• bidders in the case of an attribution of voting rights

– unilateral attribution: subsidiaries etc. required to join bid?– multilateral attribution: all persons acting in concert?

» compatible with Art. 5(1) of the Directive– exemptions available?

» no statutory exemptions/exceptions granted by BaFin» delimiting Sect. 35 despite Art. 5(3) of the Directive?

• possible exceptions granted by BaFin– Intra-group changes; acquisition of control in a work-out

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

12

– Bid price requirement: dual minimum price threshold• Threshold 1: consideration offered must correspond at least to

the highest consideration “granted” or “agreed” for the acquisition of shares of the target company … during the six months prior to the publication of the offer

– But see Art. 5(4) of the Directive: “paid”, “gezahlt worden”

and

• Threshold 2: Weighted average stock market price during the three months prior to the publication of the offer

– in line with the Directive because of Art. 3(2)(b) of the Directive?

• not available: price adjustment by the BaFin (but see Art. 5(4) of the Directive)

– Price discrimination between common and preferred non-voting stock admissible (“Wella/P&G”)

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

13

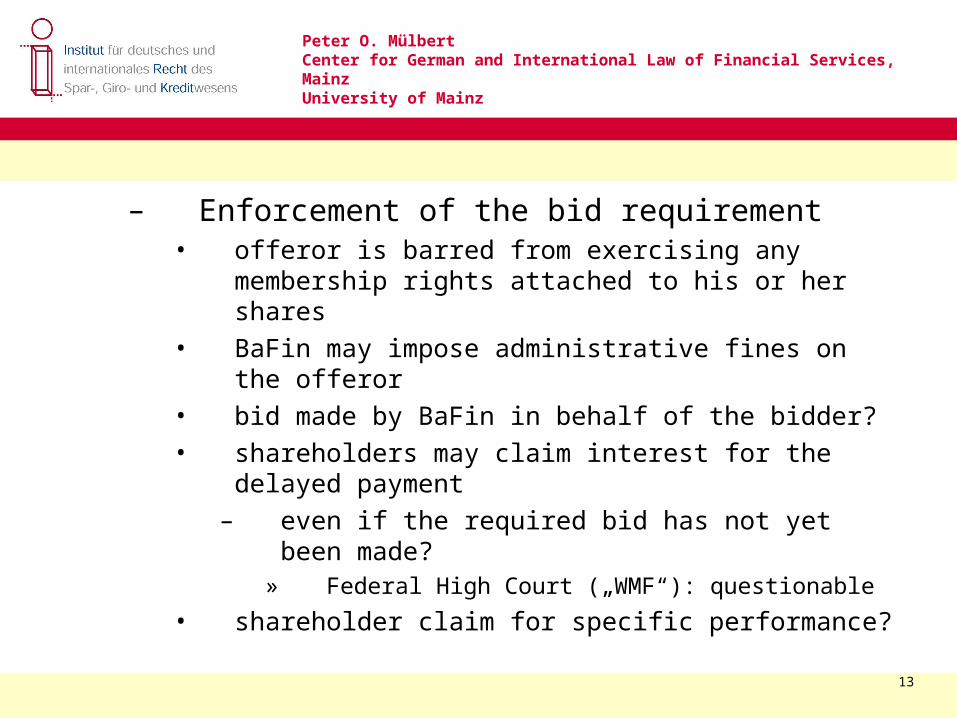

– Enforcement of the bid requirement• offeror is barred from exercising any membership rights

attached to his or her shares• BaFin may impose administrative fines on the offeror• bid made by BaFin in behalf of the bidder?• shareholders may claim interest for the delayed

payment– even if the required bid has not yet been made?

» Federal High Court („WMF“): questionable

• shareholder claim for specific performance?

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

14

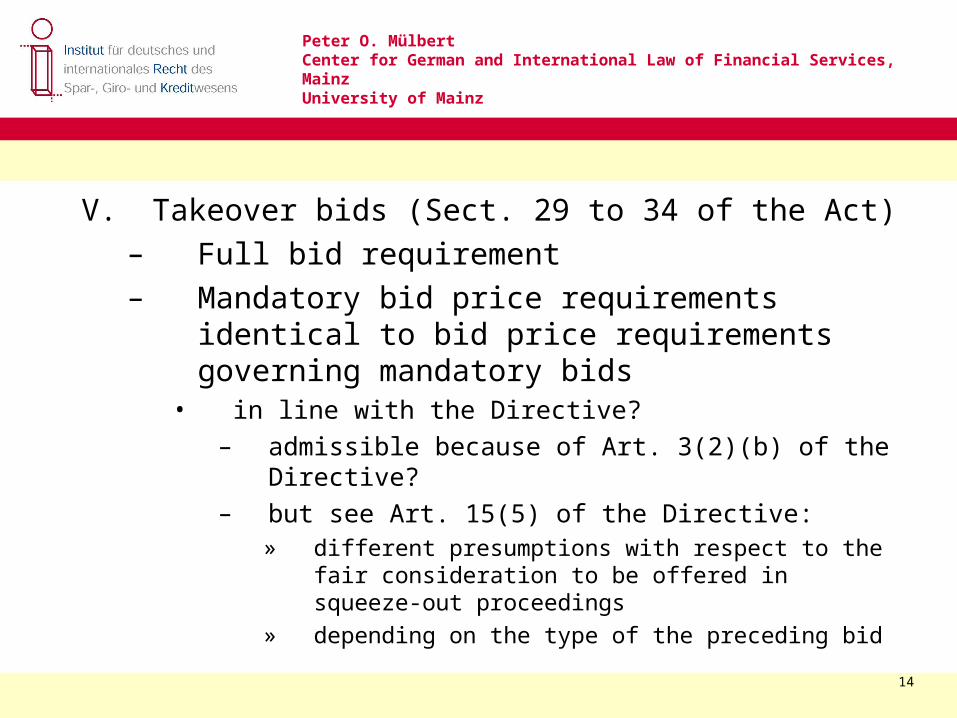

V. Takeover bids (Sect. 29 to 34 of the Act)– Full bid requirement– Mandatory bid price requirements identical to bid

price requirements governing mandatory bids• in line with the Directive?

– admissible because of Art. 3(2)(b) of the Directive?– but see Art. 15(5) of the Directive:

» different presumptions with respect to the fair consideration to be offered in squeeze-out proceedings

» depending on the type of the preceding bid

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

15

VI. The default rule for target companies: limited passivity

– Interplay between Sect. 33 of the Act and Sect. 93(1) of the Stock Corporation Act

– Starting point: after the publication of the decision to make a bid the management board of the target company may not take any actions that may frustrate the success of the bid (first sentence of Sect. 33(1))

• applicability to the supervisory board doubtful• not applicable to the shareholder meeting

– General exemptions (sentence 2 of Sect. 33(1)): • actions taken by a prudent and diligent manager

in the absence of a bid• search for a white knight

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

16

– Exemptions depending on a prior approval by the supervisory board (sentence 2 of Sect. 33(1) of the Act)

• duty of care/duty of loyality• BJR (sentence 2 of Sect. 93(1) of the Stock Corporation

Act): not applicable because of a potential conflict of interest (possible job loss)

• standards for approval:– action must be in the target company's interest

» independence as such being a company's interest?

– the company's interest must clearly outweigh the shareholders' interest in selling their shares

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

17

– Exceptions depending on a shareholder meeting’s authorization obtained during the offer period

• limited relevance for several reasons:– minimum period for calling a shareholder meeting– offeror will challenge a resolution by filing an action to set

aside said resolution

– Exceptions depending on a shareholder meeting’s authorization obtained before the publication of the decision to launch a bid (Sect. 33(2) of the Act)

• authorization must be expressly granted for the purpose of frustrating a hostile bid

• but: shareholders may only authorize such actions that fully comply with the general requirements of the Stock Corporation Act

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

18

– e.g., in case of authorized capital shareholders may empower the board to exclude pre-emptive rights in order to frustrate a hostile bid, but are barred from authorizing the board to issue the new shares below their intrinsic value

– e.g., a sale of substantive assets may be authorized but not at a below-market price

– A final note: the importance of pre-bid defenses• cases:

– Freenet v. United Internet/Drillisch (2008)– MLP v. AWD/Swiss Life (2008)

• lessons: the pivotal role of authorized capital

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

19

VII. The opt-in/opt-out regime for (target) companies – A regime without any subjects– Opt-in in the articles of association

• opt-in with respect to– board passivity (Art. 9 of the Directive)

or/and– break-through rule (Art. 11 of the Directive)

• opt-out with respect to a bidder if the bidder or a controlling “enterprise” does not face comparable restrictions other than those chosen by the bidder

– bidders or controlling “enterprises” (“Unternehmen”)» broader than Art. 12(3) of the Directive (“companies”)

since “Unternehmen” do not have to be organized in a corporate form

– shareholder resolution

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

20

VIII. The right of squeeze-out– (mostly) uniform rules regardless of the type of preceding

bid– Two squeeze-out mechanisms in the form of exclusive

alternatives available subsequent to a successful bid:• Sect. 39a et seq. of the Act (only subsequent to a bid)

andSect. 327a et seq. of the Stock Corporation Act (general)

• differing preconditions and procedures

– Fair Consideration• offer price to be presumed fair where, through acceptance of

the bid, the offeror has acquired at least 90% of the voting rights comprised in the bid

– extension of the 90% threshold to mandatory bids in line with Art. 15(5) of the Directive?

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

21

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

22

– Squeeze-out by a decision of a Frankfurt civil court: procedural aspects

• bidder has to file a motion before the Frankfurt civil court of first instance

– problem: several bidders (acting in concert!)

• bidder must hold 95% of the voting rights in the target company (Art. 15(2)(a) of the Directive)

– non-implementation of Art. 15(2)(b) of the Directive despite less strict preconditions for exercising the squeeze-out right?

• 95% requirement must only be fulfilled at the time of the final oral hearing before the court, not at the time of filing the motion

– bidder can file a motion for a squeeze-out even in the case of a conditional offer (e.g., pending approval by cartel authorities)

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

23

Peter O. MülbertCenter for German and International Law of Financial Services, MainzUniversity of Mainz

24

X. Concluding remarks– German takeover law, in the main, complies with the

Takeover Directive; (possible) deviations often reflect well-founded uncertainty regarding the content of the Directive

– German takeover law, in implementing the Directive, did not create new barriers for (cross-border) takeovers

• recent takeover of 2 DAX 30-companies– VW; Continental

• Schaeffler/Conti: public relations as sole defense

– Increased transparency obligations as the new barrier to takeovers and shareholder activism

![Tel. Bibliographischer Informationsdienst - kant.uni-mainz… · Johannes Gutenberg-Universität Mainz (JGU) D 55099 Mainz ... [The History of Continental Philosophy 1; Hardback 2010.]](https://img.dokumen.tips/doc/110x75/5b7ef6417f8b9ad4778b7974/tel-bibliographischer-informationsdienst-kantuni-johannes-gutenberg-universitaet.jpg)