Embed Size (px)

Citation preview

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Teaching Macroeconomics after the Crisis:

What have we learnt?

Peter Bofinger

Universität Würzburg

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Nothing

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Survey by Gärtner et al. (2011)

• Are these topics and models included in your

institution‘s mandatory macro courses?

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Finding the right trail head is important

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Axel Leijonhufvud (2011, p.1)

• “The IS-LM model which originated as an attempt to formalize the verbal economics of Keynes, led after years of debate to the seemingly inescapable conclusion that unemployment had to be due to the downward inflexibility of money wages. This old neoclassical synthesis thus casts Keynesian economics as a stable system with a “friction”, rather than a theory of an economy harboring dangerous instabilities.”

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

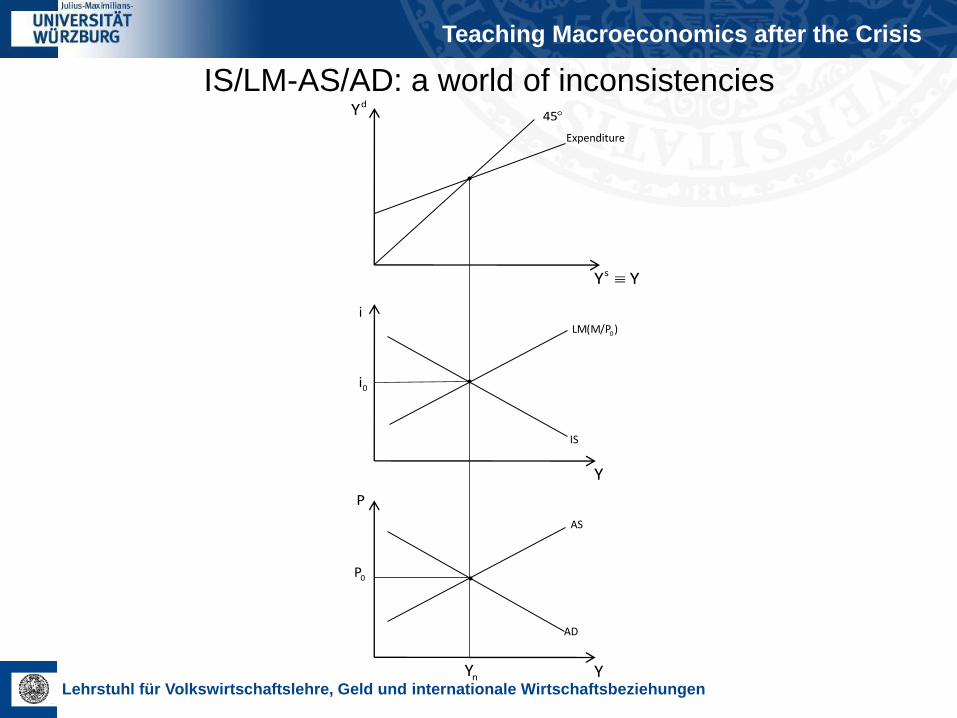

Flaws of the IS/LM-AS/AD model

• Logical inconsistencies: 2 supply curves (45°-lien, AS-

curve), 2 demand curves (aggregate demand in

income/expenditure model, AD-curve)

• No analytical explanation of involuntary

unemployment

• No analysis of fiscal and monetary policy on the basis

of loss functions

• No systematic analysis of shocks

• No zero-bound of interest rates: deflation is stabilizing

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

IS/LM-AS/AD: a world of inconsistencies

i

P

0P

0i

dY

YYs

Y

YnY

45

Expenditure

)LM(M/P0

AS

AD

IS

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Reinterpretation

• 45°-line (income/expenditure): Keynesian short-term supply curve

• Expenditure-line (income/expenditure): aggregate demand curve

• IS-Curve (IS): Demand equals supply curve

• LM-Curve (LM): Interest rate line for monetary targeting

• AD-Curve (AD): Monetary policy rule for monetary targeting

• AS-Curve (AS): Phillips-Curve for the price level

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

The re-interpreted model in comparison

Expenditure

i

P

0P

IS-LM / AS-AD

0i

dY

YYs

Y

YnY

45

)LM(M/P0

AS

AD

IS

AD

i

P

0P

Macro 2.0

0i

dY

YYs

Y

YnY

Phillips-curve for price level (PC)

Monetary policy rule (MP) (monetary targeting)

Demand = Supply (DS)

Short-run aggregate supply (SRAS)

Interest rate rule (IR) (monetary targeting)

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

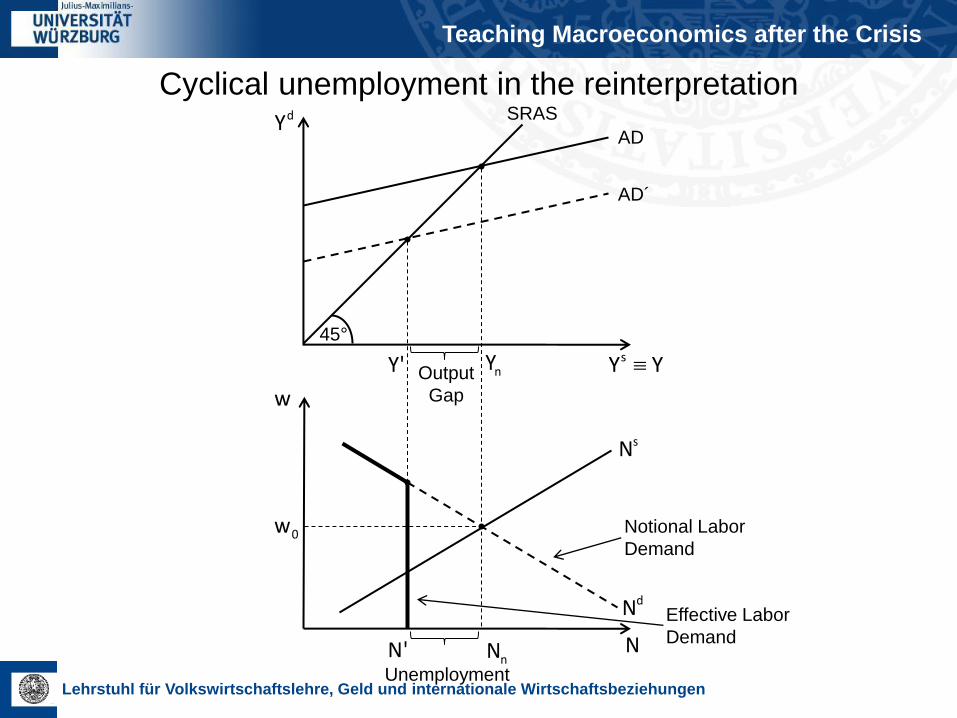

Cyclical unemployment in the reinterpretation

Unemployment

SRAS

AD

AD´

Notional Labor

Demand

Effective Labor

Demand

Output

Gap

YYs

dY

nYY'

sN

dN

nNN' N

0w

w

45°

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

The destabilizing effect of monetary policy in standard textbooks

0P

P

YnY

0AS

00 MAD

11 MAD

1P

1AS

• Expansionary monetary policy shifts AD-curve to the right

• This leads to higher inflation expectations (AS-curve shifts upwards)

• Monetary expansion has no permanent output effect only price level changes from

P0 to P1

Problem:

Monetary policy guided by a loss-function (e.g. L=(P-P0)2+𝜆(Y-Y0)

2) would have no

incentive to do such a monetary expansion!

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

The stabilising effect of monetary policy after a demand shock P

YnY

0AS

11 MAD

00 MAD

1P

0P

1Y

• Negative demand shock moves AD-curve to the left

• For a central bank (characterized through a loss-function) P1/Y1 implies a loss

Implications for monetary policy:

Central bank perfectly compensates the demand shock by increasing the money

supply from M0 to M1 (P1/Y1 is reached)

Demand shock causes no trade-off for the monetary authority

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Deflation as a self-stabilizing mechanism

• “Even without action by policy makers, the

recession will remedy itself over a period of time.

(…) Even though the wave of pessimism has

reduced aggregate demand, the price level has

fallen sufficiently (…) to offset the shift in

aggregate demand.” (Mankiw and Taylor, 2010,

p.714).

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Deflation in the standard model

• Negative demand shock moves AD-curve to the left

• Downward adjustment of price expectations shifts AS-curve to the right

Implications in the standard model:

The deflationary tendency is a desirable phenomenon which helps to stabilize the

output level (Y1 to Yn) following a negative demand shock without policy intervention

P

YnY

0AS

1AD

0AD

1P

0P

1Y

1AS

2P

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen 15

Severe demand shock and the zero lower bound

LM0

IS

IS‘

AS

AS‘

AD

AD‘

i0

iZLB

P0

P1

i

P

LM*

-iFE

Yn Y* Y

Y

P2

Y1

i1

• Strong negative demand shock shifts

IS&AD-curve sharply to the left

• Output level with full employment Yn would

require a negative nominal interest rate –iFE

• Maximum output level Y* is fully restricted

by the binding zero lower bound

• AD-curve is kinked

• Deflation (downward shift of AS-curve) only

has an impact on the price level (P1 to P2)

but does not influence the output level which

remains at Y*

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

More flaws

• IS-LM/AS-AD: Central bank targets the price

level with the instrument of the money stock

• Reality: Central bank targets the inflation rate

with the instrument of the interest rate

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

An alternative approach: The BMW-model

• Only 3 simple equations needed:

IS-Curve

(New Keynesian) Phillips-Curve

Loss-function (Central bank)

1y a br

0 2dy

2 2

0L y

y

r

PC

0

yny

ryd

0r IR

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

y

r

PC

0 2

y2yyn

ryd

0

0r

ryd

1

1

1r

0IR

1IR

1y

BMW-Model: Demand Shock

• Negative demand shock shifts

IS-curve to the left

• If the central bank does not

react (r0 stays constant) the

shock causes a negative output-

gap (y1) and a lower inflation

rate ( )

• If the central bank reacts with

lowering the interest rate

then the old equilibrium can

be reached again

1

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Useful applications

• Taylor rule

• Time inconsisteny problem

• Open economy macroeconomics

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Other areas for new macroeconomc

teaching

• Loanable funds theory: Banks as intermediaries

of a given stock of savings

• Reality: Banks create loans and thereby create

deposits and savings

• The process of money supply by the central

bank (price-theoretic money supply model,

Bofinger, 2001)

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Implications of the flawed introductory

approach for advanced models (DSGE)

• No involuntary unemplyoment

• No co-ordination problem between saving and

investment plans

• No role for banks

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Summary

• Basic macroeconomic models create the illusion

of a self-stabilzing mechanism

• Last decade: Belief in „great moderation“

• Today: Underestimation of negative demand

effects of fiscal consolidation

Teaching Macroeconomics after the Crisis

Lehrstuhl für Volkswirtschaftslehre, Geld und internationale Wirtschaftsbeziehungen

Literature

• Peter Bofinger, Eric Mayer and Timo Wollmershäuser,

"The BMW Model: A New Framework for Teaching

Monetary Economics", The Journal of Economic

Education, vol. 37, no. 1, pp. 98-117, 2006.

• Peter Bofinger, "Teaching Macroeconomis after the

crisis", Würzburg Economic Papers, Dezember 2011.

• Peter Bofinger, „Monetary policy: Goals, institutions,

strategies, and instruments”, Oxford University Press

2001.