Embed Size (px)

Citation preview

Master File No. 5:05-cv-3395 APPENDIX OF UNPUBLISHED AUTHORITIES IN SUPPORT OF LEAD PLAINTIFF’S OPPOSITION TO THE MOTION TO DISMISS OF PRICEWATERHOUSECOOPERS

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

PETER A. BINKOW #173848 ROBERT ZABB #114405 MARC L. GODINO#182689 ANDY SOHRN #241388 GLANCY BINKOW & GOLDBERG LLP 1801 Avenue of the Stars, Suite 311 Los Angeles, California 90067 Telephone: (310) 201-9150 Facsimile: (310) 201-9160 Email: [email protected] JOEL H. BERNSTEIN (admitted pro hac vice) LOUIS GOTTLIEB (admitted pro hac vice) CHRISTOPHER J. KELLER (admitted pro hac vice) ALLAN I. ELLMAN (admitted pro hac vice) LABATON SUCHAROW & RUDOFF LLP 100 Park Avenue New York, New York 10017 Telephone: (212) 907-0700 Facsimile: (212) 818-0477 Email: [email protected] Attorneys for the Mercury Pension Fund Group

UNITED STATES DISTRICT COURT

NORTHERN DISTRICT OF CALIFORNIA

SAN JOSE DIVISION

IN RE MERCURY INTERACTIVE CORP. SECURITIES LITIGATION This Document Relates To: All Actions

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )

Master File No.: 5:05-CV-3395 (Consolidated with 3:05-cv-3864; 3:05-cv-4031; and 3:05-cv-4036) APPENDIX OF UNPUBLISHED AUTHORITIES IN SUPPORT OF LEAD PLAINTIFF’S OPPOSITION TO THE MOTION TO DISMISS OF PRICEWATERHOUSECOOPERS Honorable Jeremy Fogel Hearing Date: March 30, 2007 Time: 9:00am Dept: Courtroom 3 Judge: Honorable Jeremy Fogel

Case 5:05-cv-03395-JF Document 197 Filed 01/08/2007 Page 1 of 2

Master File No. 5:05-cv-3395 APPENDIX OF UNPUBLISHED AUTHORITIES IN SUPPORT OF LEAD PLAINTIFF’S OPPOSITION TO THE MOTION TO DISMISS OF PRICEWATERHOUSECOOPERS

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

CASES

Tab In re First Merchants Acceptance Corp. Sec. Litig.,

No. 97 c 2715, 1998 U.S. Dist. LEXIS 17760 (N.D. Ill. Nov. 2, 1998)................................ 1 In re Fleming Cos. Sec. & Derivative Litig.,

No 5-03-MD-1530, 2004 U.S. Dist. LEXIS 26488 (E.D. Tex. June 10, 2004).................... 2 In re Nextcard, Inc. Sec. Litig., No. C 01-21029, 2006 WL 708663 (N.D. Cal. Mar. 20, 2006)............................................... 3

Case 5:05-cv-03395-JF Document 197 Filed 01/08/2007 Page 2 of 2

TAB 1

Page 1

LEXSEE 1998 US DIST LEXIS 1776 0

CautionAs of: Jan 08, 200 7

IN RE FIRST MERCHANTS ACCEPTANCE CORPORATION SECURITIESLITIGATION ; THIS DOCUMENT RELATES TO : ALL ACTIONS

Master File No. 97 C 2715

UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OFILLINOIS, EASTERN DIVISION

1998 U.S. Dist. LEXIS 17760

November 2, 1998, DecidedNovember 4, 1998, Docketed

DISPOSITION : [*I] Deloitte's motion to dismissCounts VI and VIII granted and its motion to dismissCounts I, II ; IV, and VII denied . Shockey, Weisgal andWyant's motion to dismiss Counts I-III denied .

JUDGES : David H . Coar, United States District Judge .

OPINION BY: David H. Coar

COUNSEL: For HARRY LAX, plaintiff: Marvin AlanMiller, Kenneth A . Wexler, Jennifer Winter Sprengel,Miller, Faucher, Cafferty and Wexler, L .L .P ., Chicago,IL .

For HARRY LAX, plaintiff: Mark C. Gardy, Stephen J .Fearon, Jr ., Abbey, Gardy & Squitieri , LLP, Robert P .Sugarman, Steven G Schulman, Samuel H Rudman,Aaron W. Tandy, Milberg , Weiss, Bershad, Hynes &Lerach LLP, New York, NY .

For MI'T'CHELL KAHN, defendant : Ronald DavidMenaker, James J . Moylan, David L . Strauss, Arnstein &Lehr, Chicago, IL.

For PAUL VAN E YL, defendant : Robert Montell Ste-phenson , Terence H. Campbell, Cotsirilos , Stephenson,Tighe & Streicker, Chicago, IL .

For STOWE W WYANT, MARCY H SHOCKEY,SOLOMON A WEISGAL, defendants : Jay A . Canel,Peter M. King, William H . Jones, Leslie Ford Notaro,Cane], Davis & King , Chicago, 11 .

For DELOITTE AND TOUCHE, L .L .P ., defendant : Wil-liam F . Lloyd, Sidley & Austin, Chicago, IL .

OPINION :

MEMORANDUM OPINION AND [*2]ORDE R

This is a consolidated securities action on behalf ofall purchasers of the publicly traded securities of FirstMerchants Acceptance Corporation ("First Merchants"),seeking remedies under the Securities Act of 1993 (the"Securities Act"), the Securities Exchange Act of 1934(the "Exchange Act") and Illinois state law . Before thiscourt are defendant Deloitte & Touche LLP's (" Deloitte)and defendants Marcy Shockey, Solomon Weisgal andStowe Wyant's (collectively , the "Audit Comm ittee De-fendants ") motions to dismiss the First Amended Con .-solidated Class Action Complaint ("first amended com-plaint" or "complaint ") . Deloitte seeks dismissal of allthe claims against it including alleged violations of Sec-tion 11 of the Securities Act . 15 U.S. C. § 77k (Counts Iand 1I) ; alleged violations of Section 10(b) of the Ex-change Act and Rule lOb-5 of the SEC (Count IV) ;common law fraud (Count VI) ; the Illinois ConsumerFraud and Deceptive Business Practices Act (Count VII) ;and negligent misrepresentation (Count VIII) . The AuditCommittee defendants seek to dismiss the claims againstthem under Section I I of the Securities Act (Counts Iand 11) and Section 15 of the Securities Act, [*3] 15U.S.C. § 77o (Count IIl) . For the reasons set forth be-

1998 U .S . Dist . LEXIS 17760, *

low, Deloitte's motion is GRANTED in part and

DENIED in part and the Audit Committee Defendants'motion is DENIED .

1 . Motion to Dismiss Standar d

A motion to dismiss pursuant to Rule 12(b)(6) of theFederal Rules of Civil Procedure does not test whetherthe plaintiff will prevail on the merits , but insteadwhether the plaintiff has properly stated a claim forwhich relief may be granted . Pickrel v. City of Spring-field, Ill., 45 F.3d 1115 (7th Cir. 1995) . A plaintiff failsto state a claim upon which relief may be granted only if"it appears beyond doubt that plaintiff can prove no setof facts in support of his claim which would entitle himto relief." Leahy v. Board of Trustees of Community Col-lege Dist. No. 508, 912 F.2d 917, 921 (7th Cir. 1990)(quoting Conley v. Gibson, 355 US. 41, 44-45, 78 S. Ct.99, 2 L. Ed. 2d 80 (1957)). For purposes of this motion,the court must take all of the well -pleaded factual allega-tions in the First Amended Complaint as true, and con-strue them in the light most favorable to the plaintiffs .Richmond v. Nationwide Cassel, L.P., 52 F. 3d 640, 644(7th Cir . 1995) . In accordance [*4] with this principle,the factual Background which follows assumes the fac-tual accuracy of the allegations in the First AmendedComplaint , without using qualifying terms such as "al-legedly," but should not be understood as representingfactual findings by this court . See Fugman v. Aprogenex,Inc., 961 F. Supp. 1190, 1191 ( .D. Ill. 1997) (Aspen,J .) .

Page 2

chants filed a bankruptcy petition revealing that .its networth had in fact been overstated . by approximately $ 90million . (P 7 .)

Deloitte was First Merchants' auditor and certifiedits financial statements throughout the class period . (P 5 .)Each of the Audit Committee defendants were directorsand members of the Audit Committee, and defendantWeisgal was the Chairperson of the Audit Committee .(PP 18-21 .) Plaintiffs allege that throughout the classperiod, First Merchants, through the individual defen-dants including the Audit Committee defendants, issuedfalse and misleading financial statements and press re-leases which grossly inflated First Merchants' incomeand assets by failing to recognize huge uncollectible loancosts as required by Generally Accepted Accounting [*6]Principles ("GAAP"), and by representing that First Mer-chants followed "conservative" accounting practices . (P3 .)

Plaintiffs allege several false and misleading state-ments made by the individual defendants, including theAudit Committee defendants, and certified by Deloitte .Specifically, plaintiffs allege that each 10-K form filedwith the SEC during the class period misrepresented thatthe financial statements had "been prepared in confor-mity with generally accepted. accounting principles andreporting practices," and misrepresented that Deloitte hadaudited First Merchants' annual financial statements "inaccordance with generally accepted auditing standards"("GAAS") . (PP 29, 30 .) n l

II . Backgroun d

First Merchants is a specialty finance company inthe business of buying and servicing sub-prime automo-bile loans . The finance contracts purchased by First Mer-chants were primarily in the credit market for high riskor "sub-prime" borrowers, This market includes borrow-ers trying to establish their credit, previously bankruptborrowers trying the re-establish their credit as well asborrowers who desire longer payment terms . (First Am,Cplt . P 2, hereinafter, "P " .) Plaintiffs include purchas-ers of First Merchants stock and subordinated reset notesin both public offerings and in the aftermarket from Sep-tember 23, 1994 through April 16, 1997 (the "class pe-riod") . (P 1, 12 .)

During the class period, First Merchants followed anaggressive growth policy, taking on longer term, higherrisk contracts, without [* 5] a corresponding increase inits allowance for credit losses . (E.g . PP 43, 61, 64, 67 .)On April 16 and 17, 1997, First Merchants announcedthat reported net income in its financial statements wasoverstated by approximately $ 28 million . (P 6.) As aresult of the Company's announcement, the market priceof First Merchants' common stock and reset notes de-clined significantly. (Id .) On July 11, 1997, First Mer-

nI While plaintiffs have alleged a number ofadditional misrepresentations contained in pressreleases, 10-Q Forms and Annual Reports, thisstatement of facts refers only to alleged misrepre-sentations by Deloitte or the Audit Committee de-fendants .

The 1994 Registration Statemen t

On September 23, 1994, First Merchants [*7] fileda stock registration statement with the SEC for an initialpublic offering of 1,460,000 shares of common stock .The 1994 Stock Registration Statement was signed byAudit Committee defendants Shockey and Wyant,among others . (P 32.) The 1994 Stock RegistrationStatement and prospectus contained First Merchants'financial statements certified by Deloitte for the yearsending May 31, 1992, 1993 and 1994 . (P33 .) The 1994Stock Registration Statement and the prospectus falselyrepresented First Merchants' procedure regarding repos-session of collateral, causing inflation of reported earn-

1998 U . S. Dist . LEX1S 17760, *

ings . (P 35.) In addition, the 1994 Registration Statementand the financial statements incorporated therein falselyunderstated the allowance for bad debts by disregardingthe fact that higher risk loans were being purchased lead-ing to increased rates of defaults , and by violating theCompany's charge -off policy through extensions of timefor payment for delinquent accounts . (P 36.) The 1994Registration Statement and financial statements alsofalsely stated that the financial statements were preparedin accordance with GAAP and that Deloi tt e's audit wasprepared in accordance with GAAS . (P [*8] . )

The 1995 Note Registration Statement , 1995 10-K and1995 Secondary Offering Registration Statemen t

On February 7, 1995, First Merchants fi led anamended Registration Statement for the sale of subordi-nated reset notes (the "1995 Note Registration State-ment" ) . The 1995 Note Registration Statement wassigned by Audit Committee defendants Shockey, Weis-gal and Wyant, among others . (P 40.) Attached to the1995 Note Registration Statement were the same falseand misleading financial statements as attached to the1994 Registration Statement. (P 41 . )

On August 29, 1995, First Merchants filed with theSEC a Form 10-K for the year ending May 31, 1995 .Audit Committee defendants Shockey, Weisgal and Wy-ant signed the 1995 10-K. (P 47.) The 1995 10-K con-tained an Auditors' Report signed by Deloitte stating thatit had audited the Company's financial statements as ofMay 31, 1994 and 1995 . (P 51 .) The 1995 10-K and at-tached financial statements falsely overstated net earn-ings and understated the loan loss allowance and failed tofollow First Merchants' procedures for establishing loanlosses and repossessing collateral . The financial state-ments and Auditors' Report also falsely [*9] stated thatthe financial statements were prepared in accordancewith GAAP and the audit conducted in accordance withGARS . (PP 50-51 .)

On October 2, 1995, First Merchants filed with theSEC an amended Registration Statement for a secondaryoffering of common stock ("Secondary Offering Regis-tration Statement") . (P 54 .) The Secondary Offering Reg-istration Statement was signed by all of the Audit Com-mittee defendants, among others . (Id .) The audited finan-cial statements contained in the Secondary Offering Reg-istration Statement and prospectus for the period endedMay 31, 1995, were the same false and misleading finan-cial statements filed with the 1995 10-K. (P 55,) The1995 stock prospectus also contained the false and mis-leading auditor's report filed with the 1995 10-K . (P 59 .)

The Second 1995 10-K, 1996 Note RegistrationStatement and 1996 10-K

Page 3

On April 1, 1996, First Merchants filed a Form 10-Kfor the fiscal year ended December 31, 1995 (the "Sec-ond 1995 10-K") . n2 The Second 1995.10-K and thefinancial statements attached thereto misrepresented FirstMerchants' true earnings by understating the allowancefor loan losses and by failing to follow published proce-dures [*10] for repossession of collateral and to makeappropriate adjustments to the allowance for creditlosses. (P 64.) The Second 1995 10-K also contained anAuditors' Report signed by Deloitte falsely stating thatthe financial statements were prepared in accordancewith GAAP and that its audit was conducted in accor-dance with GAAS . (P 65 . )

n2 In December 1995, the Company an-nounced that it was changing from a May 31year-end to a December 31 year-end, which. iswhy it filed two Form 10-Ks for 1995 . (P 60 .)

On October 29, 1996, First Merchants filed with theSEC a Registration Statement for a sale of 9 .5% subordi-nated reset notes ("1996 Note Registration Statement"),signed by the Audit Committee defendants, among oth-ers . (P 75.) The 1996 Note Registration Statement andprospectus contained financial statements audited byDeloitte for the two-year period ended December 3 1,1995 (May 31, 1994, May 31, 1995 and December 31,1995), and an auditors' report falsely stating that the fi-nancial statements were prepared in accordance [*IIIwith GAAP and that its audit was conducted in accor-dance with GAAS . (P 76, 78 .) The financial statementscontained the same false and misleading statements asthose filed with the two 1995 10-Ks . (Id .) The 1996 NoteRegistration Statement was further false and misleadingbecause, at the time of the 1996 Note Offering, FirstMerchants was technically insolvent -- the cash availableto operate its business was less than S 2 million and theCompany's finance receivables and its principal assetswere under-reserved and overvalued by approximately $28 million . (P 79 .)

On February 4, 1997, Deloitte furnished a letter tothe Audit Committee reflecting "reportable conditions" atFirst Merchants " relating to significant deficiencies inthe design or operation of the internal control structurethat . . . could adversely affect the Company's ability torecord, process, summarize and report financial data con-sistent with the asse rt ions of management in the financialstatements ." (P 82.) Despite this recognition and itswarning to the Company, Deloitte nonetheless ce rt i fi edthe 1996 financial statements and Form 10-K filed withthe SEC on March 28 , 1997 (the "1996 10-K") . The 199610-K also ['12] contained an auditor 's report signed byDeloitte falsely stating that the financial statements were

1998 U .S . Dist . LEXIS 17760 ,

prepared in accordance with GAAP and the audit wasconducted in accordance with GAAS . (P 86.) In fact, lessthan a month after the 1996 10-K was filed, the Com-pany's newly hired Chief Financial Officer, NormanSmagley ("Srnagley"), began to raise questions about theveracity of the financial statements certified by Deloitte,forcing a public announcement that the 1996 financialstatements overstated income by at least $ 3 .5 million . (P6.) A few months later, it was revealed that First Mer-chants' net worth was in fact overstated by approximately$ 90 million . (P 7 . )

GAA1 and GAAS Violation s

Plaintiffs allege that First Merchants' accountingpractices violated several accounting principles and pro-visions of GAAP, including :

(a) The principle that "[a] finance com-pany should maintain a reasonable allow-ance for credit losses applicable to allcategories of receivables through periodiccharges to operating expenses " (AmericanInstitute of Certi fied Public Accountants("AICPA") Audit and Accounting Guide,Audits of Finance Comp anies P 2,04) ;

(b) The principle [* 13] that all "estimatedloss[es] from a loss contingency . . . shallbe accrued by a charge to income" (Fi-nancial Accounting Standards Board("FASB") Statement of Standards, Ac-counting for Contingencies, Statement ofFinancial Accounting Standards No . 5, P8) ;

(c) The principle that financial reportingshould provide information that is usefulto present to [sic] potential investors andcreditors and other users in making ra-tional investment , credit and similar deci-sions (FASB Statement of Concepts No.1, P 34) ;

(d) The principle that financial reportingshould provide information about the eco-nomic resources of an enterprise, theclaims to those resources, and the effectsof transactions, events and circumstancesthat change resources and claims to thoseresources (FASB Statement of ConceptsNo. 1, P 40) ;

(e) The principle that financial reportingshould provide information about an en-

terprise's financial performance during aperiod . Investors and creditors often usehistorical financial information to help inassessing the prospects of an enterprise .Thus, although investment and credit de-cisions reflect investors ' expectationsabout future enterprise performance,[*14] those expectations are commonlybased at least part ly on evaluations of pastenterprise performance (FASB Statementof Concepts No. 1, P 42) ;

(f) The principle that financial reportingshould be reliable in that it representswhat it purports to represent (FASBStatement of Concepts No . 2, PP 58-59) ;

(g) The principle of completeness, whichmeans that nothing is left out of the in-formation that may be necessary to ensurethat it validly represents underlying eventsand conditions (FASB Statement of Con-cepts No . 2, P 79); and

(h) The principle that conservatism beused as a prudent reaction to uncertaintyto try to ensure that uncertainties and risksinherent in business situations are ade-quately considered (FASB Statement ofConcepts No . 2, PP 95, 97) .

(P 94 .)

Page 4

Deloitte certified that First Merchants' financialstatements were prepared in accordance with the stan-dards set forth above . In doing so, Plaintiffs allege thatDeloitte violated several principles of GAAS . The fol-lowing allegations pertain to the GAAS principles alleg-edly violated :

. GAAS requires that an audit report statewhether a company's financial statementsare presented in conformity [*151 withGAAP,AU§ 110 .01 .(P97 . )

. GAAS requires that an auditor is re-quired to qualify its opinion if there is anydoubt about a company 's ability to pro-ceed as a going concern . AU § § 341 .02,341 .03 . (P 99. )

. GAAS provides that an inabili ty to ob-tain sufficient competent evidential ma tterconstitutes a restriction on the scope of

1998 U.S . Dist . LEXIS 17760, *

the audit which requires and auditor toqualify or disclaim an opinion. AU §508.17 . (P 100 .) (a) The bad debt write-offs for First Mer -

chants' loans rose from $ 7 .6 million in"GAAS requires that an audit be ade- 1995 to $ 26 .6 million in 1996, a 220 per-

quately planned and assistants be properly cent increase. But First Merchants' badsupervised . AU § 150.02 . Audit planning debt reserves increased by only 20 percent

involves developing an overall strategy between 1995 and 1996 .for the conduct and scope of the audit . AU§ 311 .03 . In planning an audit, the audi- (b) Dramatic increases in the rate of de-tor is required to obtain a knowledge of linquencies approaching the 90 day write -the entity's business, its organization and off limit should also have served as a re doperating characteristics (AU § 311 .07) flag to Deloitte . For example, the numberso that the auditor can identify areas that of loans which were unpaid for more tha nneed special attention . AU § 311 .06, The 61 days in 1996 was more that [sic] 50 0auditor must design the audit to provide percent greater than in 1995 . But again ,reasonable assurance of detecting errors the 1996 bad debt reserves were increase dand irregularities (intentional misstate- by only 20 percent .ments) that are material to the financia lstatements . AU § 316 .05 ." (PP 103, 105 .) (c) Similarly, the dollar value of loan s

more than 61 days overdue increased b y"GAAS requires that the efforts of assis- 39 times for year end May 31, 1995 over

tarts be directed and supervised to assure the comparable period in 1994 . Yet thethat [*16] the objectives of the audit are 1995 loan loss reserves were increased b yaccomplished . AU § 311 .10 . GAAS re- only three time over the same period i nquires that the work performed by each the prior year.assistant be reviewed and evaluated to de -termine whether the audit results are con- (d) The dollar value of loans more than 6 1sistent with the conclusions expressed in days overdue increased by 21 time for th ethe auditor's reports . AU § 311 .13 ." (P six months ended November 30, 199 4104 .) over the comparable period in 1993 . Ye t

the November 30, 1994 loan loss reserve s"The auditor must perform procedures to were only 2 .75 times greater than what

obtain a sufficient understanding of three they had been a year earlier .elements of an entity's internal contro lstructure : the control environment, the ac- (e) [* 18] Between May 31 and Decem-counting system, and control procedures . ber 31, 1995, the number of accounts 6 1AU § 319 .02 . The auditor must document days or more overdue rose by over 20 0his understanding of the entity's internal contracts to 257 and between Decembercontrol structure elements in order to plan 31, 1995 and June 30, 1996 the numberthe audit . § 319.26 ." (PP 105-06 .) almost doubled to 494 ; however, this wa s

not reflected by an increase in the re-serves .

Red Flag Allegations

Within a few weeks after his arrival in mid-March (f) During the class period there were sig-1997, Smagley noted errors in the financial statements nificant increases in the term of the notescertified by Deloitte, leading to the Company's April 16 First Merchants was buying . For example

and 17, 1997, disclosures . (P 6.) Plaintiffs allege that the average length of the notes went from

Deloitte, like Smagley, should have seen the "writing on 48 months during 1994 to 55 months as ofthe wall" with respect to First Merchants' improper ac- December 31, 1996 reflecting borrowerscounting practices, and that Deloitte knowingly or reek- less able to repay their loans

. This in-

lessly disregarded its auditing obligations in certifying crease should have been reflected by in-First Merchants' financial statements . (P 96, 102

.) Plain- creases in the loan loss reserves but etas

tiffs [*17] point to several "red flags" Deloitte ignored not.

or recklessly disregarded :

Page 5

1998 U .S . Dist . LEXIS 17760, *

(g) The dollar value of loans more than 61days overdue increased enormously dur-ing certain periods without correspondingincreases in the loans over 91 days over-due which had to be charged off. Whilethe delinquencies between 61 and 90 dayswas 21 times greater in the six monthsended November 31 [sic], 1994 than inthe comparable period of 1993, the dollarvalue of loans which the Companycharged off increased less than threetimes. While the dollar value of loansmore than 61 days overdue increased by39 times for year end May 31, 1995 over[*19] the comparable period in 1994, thedollar value of loans which the Companycharged off increased less than nine times .These anomalies should have served asred flags for the Deloitte to carefully re-view First Merchants records to see ifthese numbers were being manipulated tohide loans which actually became morethan 91 days delinquent or, more im-probably, whether there was simply asurge of payments as delinquent loans ap-proached their 91st day of non-payment .

(P 102 . )

111. Analysis

A. Pleading Requirements Under Rule 9(b) andthe Private Securities Litigation Reform Act of 1995(PSLRA).

"Rule 9(b) requires that 'the circumstances constitut-ing fraud . . . be stated with particularity .'' In re Health-care Compare Corp. Securities Litigation, 75 F. 3d 276,281 (7th Cir. 1996) . Thus, a securities fraud plaintiffmust plead "in detail" the facts surrounding fraud, i .e .,"the who, what, when, where, and how : the first para-graph of any newspaper story." Dileo v . Ernst & Young,901 F2d 624, 627 (7th Cir .), cert. denied, 498 U.S. 941,III S. Ct. 347, 112 L. Ed. 2d 312 (1990). "This require-ment has three main purposes : to protect defendants'reputations, to prevent [*20] fishing expeditions, and toprovide adequate notice to defendants of the claimsagainst them ." Fugman v. Aprogenex, Inc., 961 F. Supp .1190, 1195 (ND. Ill. 1997) .

The PSLRA amends the 1934 Act to raise pleadingstandards in securities fraud cases to a more rigorouslevel, such that the complaint must "state with particular-ity facts giving rise to a strong inference that the defen-dant acted with the required . state of mind ." 15 U.S. C. §78u-4(b)(2) . While the PSLRA does not contain a spe-

Page 6

cific scienter requirement for § 10(b) fraud claims, it isgenerally recognized that the appropriate standard foralleging scienter under the PSLRA is the Second Circuitstandard which requires a plaintiff "to allege facts thatgive rise to a strong inference of fraudulent intent ."Shields v. Citytrust Bancorp, Inc., 25 F.3d 1124, 1128(2d Cir . 1994) .

Defendants argue, however , that the PSLRA createda pleading standard even more stringent than that enun-ciated by the Second Circuit and that mere allegations ofrecklessness no longer suffice to plead scienter under §10(b) . Cou rts in this District have uniformly rejected thisargument, holding that recklessness is still su fficient un-der § [*21] 10(b). See Miller v. Material Sciences Cor-poration, 9 F. Supp. 2d 925, 927 (N.D. 111. 1998) (Get-tleman , J .); Fugman v . Aprogenex, Inc., 961 F Supp. at1195; Rehm v . Eagle Finance Corp., 954 F. Supp. 1246,1252 (N.D. Ill. 1997) (Moran, J .) ; see also In re HealthManagement Securities Litigation , 970 F. Supp. 192, 200(E.D.N.Y. 1997) ( finding argument that recklessness nolonger suffices to plead scienter unpersuasive ) . While theSeventh Circuit has yet to address the question ofwhether the PSLRA completely displaced case law re-garding pleading standards in private securities law, thiscourt agrees with the other courts in this District whohave held that the "§ 78u-4(b)(2) adopts the Second Cir-cuit standard but declines to bind cou rts to the SecondCircuit's interpretation of its standard ." Rehm, 954 F.Supp. at 1252 (Moran, J .) ; Fugman, 961 F. Supp. at 1195(citing Rehm) .

B. Section 10(b) and Rule lOb-5 Allegations .

Count IV of the First Amended Complaint allegesthat Deloitte violated § 10(b) of the 1934 Act and Rule10b-5 . "SEC Rule lOb-5, promulgated under Section10(b) of the Securities Exchange Act of 1934, prohibitsthe making of any untrue [*22] statement of materialfact or the omission of a material fact that would renderstatements made misleading in connection with the pur-chase or sale of any security ." 17 C.F.R. § 240.10b-5 .To state a valid Rule lob-5 claim, a plaintiff must allegethat the defendant (1) made a misstatement or omission,(2) of material fact, (3) with scienter, (4) in connectionwith the purchase or sale of securities, (5) upon whichthe plaintiff relied, and (6) that reliance proximatelycaused plaintiffs injuries ." In re Healthcare CompareCorp., 75 F.3d at 280 (citing Stranslcy v . Cummins En-gine Co ., 51 F. 3d 1329 (7th Cir. 1995)) . In this motion todismiss, Deloitte challenges the sufficiency of plaintiffs'misrepresentation and scienter allegations . n 3

n3 Deloitte also argues that because the firstamended complaint is pled on information andbelief, it fails in its entirety or at least fails to al-

1998 U.S. Dist . LEXIS 17760, *

lege fraud with particularity . The court rejectsthis argument . The complaint sets forth detailedallegations of fraud and alleges substantiallymore than " rumor or hunch ." See Bankers TrustCo. v . Old Republic Ins. Co., 959 F.2d 677, 683-84 (7th Cir. 1992) . The fact that Plaintiffs do nothave all of the specific documents to support theirclaims at this time is not fatal to their complaint .STI Classic Fund v. Bollinger Indus ., Inc., 1996U.S. Dist. LEXIS 21553, 1996 WL 885802 at *2(N.D. Tex . 1996) ("the actual contents of thebooks and records and the [defendant' s] knowl-edge thereof are peculiarly within the Movants'knowledge and control , thereby warranting somerelaxation in the application of Rule 9(b)") .

[*231

1 . Misrepresentation s

In challenging the specificity of Plaintiffs' misrepre-sentation allegations, Deloitte primarily contends that the"what," "why" and "how" of the allegations are lacking .Deloitte's challenges are directed at the sufficiency of theGAAP and GAAS allegations . Plaintiffs allege thatDeloitte falsely stated that the financial statements wereprepared in accordance with GAAP and audited in ac-cordance with GAAS . Deloitte asserts that the complaintfails to allege with particularity why its audit reportswere misleading ; what was materially misstated in thefinancial statements ; and how the financial statementsand Deloitte's audit of those statements violated GAAPand GAAS. The court finds that the allegations in thecomplaint contain sufficient detail to satisfy each ofthese elements .

Deloi tte's contention that plaintiffs fail to suffi-ciently allege why each of the audit reports was mislead-ing is unpersuas ive . The complaint expressly alleges thateach of Deloi tt e ' s audit reports filed in conjunction withthe 10-K Forms and Registration Statements was mis-leading because Deloitte 's opinion that the financialstatements were prepared in accordance [*24] withGAAP and audited in accordance with GAAS was false.An outside auditor can be liable for stating its opinion ona company ' s financial statements if that opinion is falseand misleading . Cashman v. Coopers & Lybrand, 877 F.Supp. 425, 431 (N.D. Ill. 1995) (Castillo, J .) (an account-ant "may be held primarily liable for ce rtifying or issuingrepo rts on . . . financial statements if those repo rts con-tain materially misleading statements or omissions" re-lied upon and incorporated into a prospectus ) (citingDiLeo, 901 F .2d at 627) . Further, the complaint suffi-ciently states why the financial statements containedmaterially misleading statements : " the financial state-ments . . . misrepresented First Merchants ' true earn ingsby understating the allowance for loan losses and by fail-

Page 7

ing to follow published procedures for repossession ofcollateral and to make appropriate adjustments to theallowance for credit losses . " (See e .g , P 33, 47, 63, 64 . )

Similarly , the allegations detail what was materiallymisstated in the financial statements -- the Company'strue earnings and net wo rth. Deloitte complains that thefirst amended complaint fails to state the precise amountof [*25] the overstatement of earnings in each of theaudited financial statements ; which loans were not prop-erly wri tten off, and which collateral was not repossessedaccording to proper procedures , etc . The court agreesthat this information is noticeably absent from the com-

plaint and that, in order to prove its allegations , plaintiffswill be required to fill in these details . However, giventhat most of this information is in the hands of defen-dants, the court finds that plaintiffs have satisfied theirburden at this stage of the litigation . See DiVittorio v.Equidyne Extractive Industries, Inc., 822 F.2d 1242,1247 (2nd Cir . 1987) (requirements of Rule 9 (b) are tobe relaxed where the facts are "peculiarly within the ad-verse parties' knowledge") . Indeed, the true amounts ofFirst Merchant' s reserves, income and net worth cannotbe determined without a re-audit of the Company's fi-nancial records -- records in the hands of defendants andobtainable through discovery .

Moreover, several courts have held that a complaintneed not describe each single specific transaction in de-tail nor allege the precise amount of overstatement on aperiod by period basis . See Cooper v . Pickett, 137 [*26]F.3d 616, 627 (9th Cir. 1997) ("it is not fatal to the com-plaint that it does not describe in detail a single specifictransaction ") ; SEC v. Feminella, 947 F. Supp. 722, 733(S.D.N.Y 1996) (" Rule 9 (b) does not require nor makelegitimate the pleading of detailed evidentiary matter")(quotations omi tted); Klein v. King, 1990 U.S. Dist.LEXIS 5392, 1990 WL 61950 at *I I (N .D. Cal . 1990)(holding that plaintiff was not required to plead the pre-cise dollar amount of the overstatement of earnings inorder to state a claim under Rule lOb -5) . In Feminella,the court rejected the defendant ' s argument that the com-plaint failed to satisfy Rule 9 (b) because the SEC had notalleged the dates or amounts of payments, the manner ofpayments or the total value of payments , finding that "theComplaint provides defendant with fair notice of theSEC's claims , enabling him to prepare a reasonable de-fense ." 947 F. Supp. at 733 . The court agrees that Rule9(b) does not require that plaintiffs state the precise dol-lar amount that earnings and net wo rth were overstatedfor each of the financial statements audited and ce rt ifiedby Deloitte . The complaint sufficiently alleges whichportions of the financial statements were [*27] over-stated (net worth and earn ings) and which port ions un-derstated ( loss reserves), such that Deloitte can prepare areasonable defense to the allegations .

1998 U . S . Dist . LEXIS 17760, *

Deloitte finally argues that the misrepresentation al-legations fail to state how the financial statements andaudit reports violated GAAP and GAAS . The GAAP andGAAS allegations are set forth in substantial detail in thecomplaint and in the background portion of the court'sopinion. Deloitte argues that several of the principlescited in the complaint are not GAAP principles . Thisgoes not to the specificity of the allegations, but towhether Plaintiffs can prove a violation of GAAP orGAAS sufficient to satisfy the scienter requirement. Atthis stage, the court finds the specificity of the account-ing principle violations more than sufficient to satisfyRule 9(b) -- the allegations cite the specific principleviolated and how they were violated ,

Finally, the court finds that the policy considerationsbehind requiring specificity for fraud allegations are met-- the complaint plainly contains enough detail to satisfythe court that this is not a fishing expedition and to pro-vide Deloitte with copious notice of the allegations [*28]against it . Moreover, the allegations in the complaint arenot akin to a "smear campaign" damaging Deloitte'sreputation without sufficient facts to back up the allega-tions . The court accordingly finds sufficient detail in theallegations to conclude that Plaintiffs have pled misrep-resentation with particularity .

2 . Scienter

"Only persons who act with an intent to deceive ormanipulate Rule 10b -5" may be found liable under RulelOb-5 . Securities and Exchange Commission v. Jaku-bowski, 150 F.3d 675, 681 (7th Cir. 1998) . "Recklessdisregard of the truth counts as intent for this purpose ."Id . Under the PSLRA!Second Circuit pleading require-ment, a plaintiff may demonstrate a "strong inference" offraud "either (a) by alleging facts to show that defendantshad both motive and opportunity to commit fraud, or (b)by alleging facts that constitute strong circumstantialevidence of conscious misbehavior or recklessness ."Shields, 25 F.3d at 1128 . While the court finds thatPlaintiff has failed to establish a sufficient motive todemonstrate " motive and opportunity ," n4 plaintiffs havealleged "strong circumstantial evidence of consciousmisbehavior or recklessness . "

n4 The only allegations related to motivepertain to Deloitte's alleged acceptance of a feetoo low to justify a careful audit in order to obtainmore business in the sub-prime auto lending in-dustrv . This Circuit has repeatedly rejected suchallegations, recognizing that an accounting firm's"greatest asset is its reputation for honesty, fol-lowed closely by its reputation for careful work ."Robin v . Arthur Young & Company, 915 F .2d1120, 1127 (7th Cir. 1990) (quoting DiLeo, 901

Page 8

F.2d at 629) . Because Plaintiffs' sole allegation ofmotive is insufficient under the law and is basedon economic irrationality, Plaintiffs fail to meetthe 2nd Circuit motive and opportunity test .

*29

Recklessness in a securities fraud action against anaccountant is de fined as "highly unreasonable conduct,involving not merely simple , or even inexcusable negli-gence , but an extreme departure from the standards ofordinary care, and which presents a danger of misleadingbuyers or sellers that is either known to the defendant oris so obvious that the actor must have been aware of it ."SEC v . Price Waterhouse , 797 F. Supp. 1217, 1240(S.D.N.Y. 1992) (citations and quotation omitted) . Anallegation of recklessness against outside auditors "re-quires more than a misapplication of accounting princi-ples," a plaintiff must allege that " the accounting prac-tices amounted to no audit at all, or an egregious refusalto see the obvious , or to investigate the doubtful , or thatthe accounting judgments which were made were suchthat no reasonable accountant would have made the samedecisions if confronted with the same facts ." Id, (quota-tions and citations omitted ) : Rehm, 954 F. Supp. at 1255.

Moreover, Deloitte correctly points out that , while a"company's overstatement of revenues in violation ofGAAP can constitute a false or misleading statement ofmaterial fact necessary to [*30] establish securities fraudunder Section 10 ( b) and Rule lob -5 violation ," Clark v.TRO Learning, Inc., 1998 U.S. Dist. LEXIS 7989, 1998WL 292382, *2 (N.D. Ill . 1998), a plaintiff cannot showscienter merely by stating that a defendant violatedGAAP . See, e .g., Lovelace v. Software Spectrum Inc ., 78F.3d 1015, 1020-21 (5th Cir. 1996); In re SoftwareToolworks, 50 F.3d 615, 627-28 (9th Cir. 1994), cert .denied , 516 U.S. 907, 116 S. Ct. 274 (1995) ; In reWorlds of Wonder Securities Litigation, 35 F.3d 1407,1426 (9th Cir . 1994), ce rt . denied, 516 U.S. 868, 116 S.Ct. 185 (1995) and cert . denied, 516 U.S. 909, 116 S. Ct.277 (1995) ; Malone v. Microdyne Corp ., 26 F.3d 471,479 (4th Cir. 1994); Health Management, 970 F. Supp.at 203; Rehm, 954 F. Supp . at 1256; Duncan v. Pencer,1996 U.S. Dist. LEXIS 401, 1996 WL 19043 at *10(S .D.N.Y. 1996 ) . However , " although it is true that aviolation ofGAAP will generally will not be su fficient toestablish fraud, when combined with other circumstancessuggesting fraudulent intent, allegations of improperaccounting may support a strong inference of scienter ."Marksman Partners, L.P., 927 F. Supp . 1297, 1313 (C. D .Cal . 1996) .

"Other circumstances suggesting [*31] fraudulentintent" can include the presence of "red flags" or warningsigns that the financial reports are fraudulent, as well as

1998 U .S . Dist , LEXIS 17760, *

the magnitude of the fraud alleged, Miller, 9 F. Supp. 2d

at 928 ("deliberately ignoring "red flags" such as thosealleged here can constitute the sort of recklessness neces-sary to support § 10(b) liability") ; Rehm, 954 F. Supp. at

1256 ("the more serious the error, the less believable aredefendants' protests that they were completely unawareof [the Company's] true financial status and the strongerthe inference that defendants must have known about thediscrepancy"); In re Health Management, 970 F. Supp.at 203 (finding that allegations of accounting firm's igno-rance of red flags presented evidence of fraudulent in-tent); In re Leslie Fay Companies, 835 F. Supp. 167, 175("in cases where small accounting errors only ripplethrough the corporate books, a court may conclude . . .that an accountant's failure to discover his client's fraudwas not sufficiently reckless to sustain a lOb-5 claim . Onthe other hand, when tidal waves of accounting fraud arealleged, it may determine that the accountant's failure todiscover his client's fraud ['321 raises an inference ofscienter on the face of the pleading") .

With these principles in mind, the court finds thatPlaintiffs have offered sufficient facts to survive a mo-tion to dismiss on the issue of scienter, Although plain-tiffs' allegations may be difficult to prove at trial, at thisstage, plaintiffs have alleged specific facts which giverise to a strong inference that Deloitte deliberately ig-nored various warning signs, constituting the reckless-ness necessary to support § 10(b) liability . See Miller, 9F. Supp. 2d at 928.

Plaintiffs allege not only violations of GAAP andGAAS, but that Deloitte deliberately ignored several redflags in the financial statements which would have ex-posed the fraud. n5 Moreover, the complaint containsallegations that the final Form 10-K filed with the SECoverstated First Merchants' net worth by approximately $90 million dollars . The magnitude of the fraud combinedwith the allegation that First Merchants' new Chief Fi-nancial Officer almost immediately discovered the dis-crepancies in the financial statements, suggests a deliber-ate ignorance on the part of Deloitte . Thus, the allega-tions in the complaint, including the magnitude of themisstatements, [*33] the specific GAAP and GAASviolations and the "red flags" together support an infer-ence that Deloitte's audit "amounted to no audit at all oran egregious refusal to see the obvious or investigate thedoubtful ." Accordingly, Deloitte's motion to dismissCount TV is denied .

n5 Deloitte argues that the fact that it ful-filled its duty to report weaknesses in the finan-cial statement absolves it of liability . The ques-tion before the court, however, is whether thecomplaint sufficiently alleges that Deloitte made

Page 9

misrepresentations of material fact by stating thatthe financial statements were prepared in accor-dance with GAAP and whether those representa-tions were made with scienter . The fact thatDeloitte reported weaknesses in the fi nancialstatements yet certified those same financialstatements less than two months later support s,rather than detracts from the allegations of reck-lessness . In the same vein , Deloitte contends thatthe complaint fails to state how it ignored the al-leged red flags or that it did not consider thosered flags in its audits . In other words , Deloitte ar-gues that the complaint should be dismissed be-cause Deloitte might have properly consideredthe warning signs in its audit of the financialstatements . The speci fics of Deloi tte's audit are,however, precisely the type of facts which areparticularly within defendants' knowledge andtherefore, need not be included in the complaint ."In re Leslie Fay, 835 F. Stipp. at 174 .

[*34]

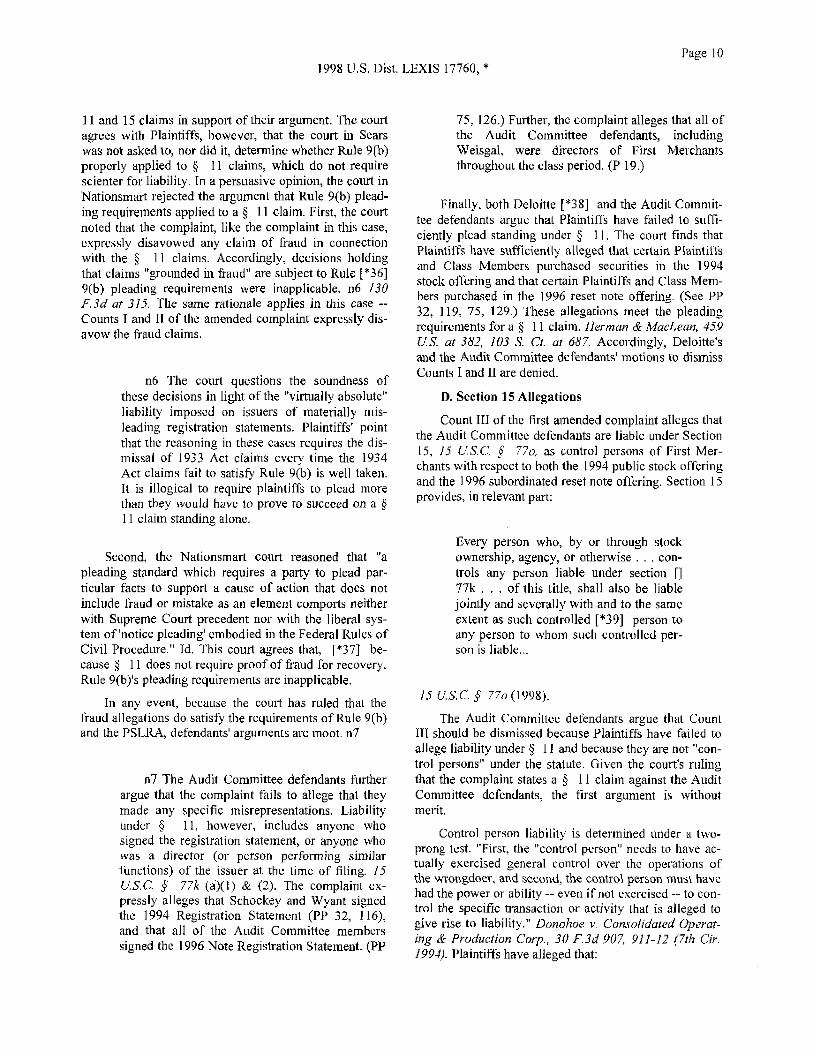

C. Section It Allegations

Both Deloitte and the Audit Committee membersseek a dismissal of the Section I 1 claims (Counts I andI1) . Section 11 imposes civil liability on persons prepar-ing and signing materially misleading registration state-ments . 15 U.S.C. ,7 77k(a) (1998) . A registration state-ment is materially misleading if it contains an untruestatement of material fact or if it omits a material factnecessary to prevent the statement from being mislead-ing. Id , Any person who purchases a registered securityis entitled to sue under this section . Id . "Section I1 im-poses 'a stringent standard of liability on the pa rt ies whoplay a direct role in a registered offering ."' NationsmartCorp. v. Thaman, 130 F.3d 309, 314-15 (8th Cir. 1997)( quoting Herman & MacLean v. Huddleston, 459 U.S.375, 381-82, 103 S. Ct. 683, 74 L. Ed. 2d 548 (1983)),"To establish a prima facie § 11 claim, a plaintiff needshow only that he bought the security and that there wasa material misstatement or omission . Scienter is not re-quired for establishing liability under this section ." Id .Indeed , " the liability of the issuer of a materially mis-leading registration statement is 'vi rtually [*35] abso-lute, even for innocent misstatements ."' Id . (quotingHerman & MacLean, 459 U.S. at 382, 103 S. Ct. at 687).

Deloitte and the Audit Committee defendants posetwo challenges to Plaintiffs ' § 11 claims . First, they con-tend that the allegations fail to plead a material mis-statement with sufficient particularity . Plaintiffs counterthat Rule 9 (b) particularity is not required for § IIclaims , citing authority from other circuit and districtcourts . Defendants cite Sears v. Likens, 912 F.2d 889,892-93 (7th Cir. 1990), which applied Rule 9(b) to a § §

1998 U .S . Dist . LEXIS 17760, *

11 and 15 claims in support of their argument . The courtagrees with Plaintiffs, however, that the court in Searswas not asked to, nor did it , determine whether Rule 9(b)properly applied to § I 1 claims , which do not requirescienter for liability . In a persuasive opinion, the court inNationsmart rejected the argument that Rule 9(b) plead-ing requirements applied to a § 1 l claim. First , the courtnoted that the complaint, like the complaint in this case,expressly disavowed any claim of fraud in connectionwith the § 11 claims . Accordingly, decisions holdingthat claims "grounded in fraud" are subject to Rule [*36]9(b) pleading requirements were inapplicable . n6 130F.3d at 315. The same rationale applies in this case --Counts I and 11 of the amended complaint expressly dis-avow the fraud claims .

n6 The court questions the soundness ofthese decisions in light of the "virtually absolute"liability imposed on issuers of materially mis-leading registration statements . Plaintiffs' pointthat the reasoning in these cases requires the dis-missal of 1933 Act claims every time the 1934Act claims fail to satisfy Rule 9(b) is well taken .It is illogical to require plaintiffs to plead morethan they would have to prove to succeed on a §11 claim standing alone .

Second, the Nationsmart court reasoned that "apleading standard which requires a party to plead par-ticular facts to support a cause of action that does notinclude fraud or mistake as an element comports neitherwith Supreme Court precedent nor with the liberal sys-tem of 'notice pleading' embodied in the Federal Rules ofCivil Procedure ." Id, This court agrees that, [*37] be-cause § 11 does not require proof of fraud for recovery,Rule 9 (b)'s pleading requirements are inapplicable .

In any event, because the court has ruled that thefraud allegations do satisfy the requirements of Rule 9(b)and the PSLRA, defendants' arguments are moot . n 7

n7 The Audit Committee defendants fu rtherargue that the complaint fails to allege that theymade any specific misrepresentations . Liabilityunder § 11, however , includes anyone whosigned the registration statement , or anyone whowas a director (or person performing similarfunctions) of the issuer at the time of filing . 15U.S.C. § 77k (a)( l) & (2) . The complaint ex-pressly alleges that Schockey and Wyant signedthe 1994 Registration Statement (PP 32, 116),and that all of the Audit Commi ttee memberssigned the 1996 Note Registration Statement. (PP

Page 1 0

75, 126.) Further, the complaint alleges that all ofthe Audit Committee defendants , includingWeisgal, were directors of First Merchantsthroughout the class period. (P 19 . )

Finally, both Deloitte [*38] and the Audit Commit-tee defendants argue that Plaintiffs have failed to suffi-ciently plead standing under § 11 . The court finds thatPlaintiffs have sufficiently alleged that certain Plaintiffsand Class Members purchased securities in the 1994stock offering and that certain Plaintiffs and Class Mem-bers purchased in the 1996 reset note offering . (See PP32, 119, 75, 129 .) These allegations meet the pleadingrequirements for a § 11 claim . Herman & MacLean, 459U.S. at 382, 103 S. Ct. at 687. Accordingly, Deloitte'sand the Audit Committee defendants' motions to dismissCounts I and II are denied.

D. Section 15 Allegation s

Count I II of the first amended complaint alleges thatthe Audit Committee defendants are liable under Section15, 15 US.C. § 770, as control persons of First Mer-chants with respect to both the 1994 public stock offeringand the 1996 subordinated reset note offering . Section 15provides, in relevant part:

Every person who, by or through stockownership, agency, or otherwise . . . con-trols any person liable under section []77k . . . of this title, shall also be liablejointly and severally with and to the sameextent as such controlled [*39] person toany person to whom such controlled per-son is liable . . .

15 US. C, § 77o (1998) .

The Audit Committee defendants argue that CountIII should be dismissed because Plaintiffs have failed toallege liability under § 1 I and because they are not "con-trol persons" under the statute . Given the court's rulingthat the complaint states a § 11 claim against the AuditCommittee defendants, the first argument is withoutmerit .

Control person liability is determined under a two-prong test. "First, the "control person" needs to have ac-tually exercised general control over the operations ofthe wrongdoer , and second, the control person must havehad the power or ability -- even if not exercised -- to con-trol the specific transaction or activity that is alleged togive rise to liability ." Donohoe v, Consolidated Operat-ing & Production Corp., 30 Fad 907, 911-12 (7th Cir.1994). Plaintiffs have alleged that :

1998 U .S . Dist . LEX1S 17760, *

Each of these Defendants was a controlperson of the Company with respect to theOfferings referred to in Counts I and 11above by virtue of, among other things,his or her stock ownership and/or positionas a senior executive officer and/or direc-tor of the Company [*40] and had thepower and influence, and exercised thesame, to control the contents of the Com-pany's Registrations Statements, Prospec-tuses . . . Each of these Defendants wasprovided with copies of the Company'sfilings, reports, press releases and otherpublic statements alleged herein to befalse and misleading, prior to or shortlyafter their issuance, and had the abilityand opportunity to prevent their issuanceor cause them to be corrected . Moreover,each of these Defendants was a partici-pant in the Section 11 violations allegedin Counts I and II above, based on theirhaving signed the Registration Statementsor having otherwise participated in theprocess which allowed the Offerings to besuccessfully completed.

(P 135.) Thus, Plaintiffs have alleged both that the AuditCommittee defendants exercised general control over thecontents of the Company's public representations and hadthe ability to control the specific misrepresentations inthe Registration Statements, prospectuses and financialstatements . The court finds these allegations sufficient tomeet the general pleading requirements under Rule 8(a)(2) of the Federal Rules of Civil Procedure . See Na-tionsmart, [*41] 130 F.3d at 315; Goldsmith v. Tech-nolo~y Solutions Company, 1993 U.S Dist. LEIS 6136,1993 WL 150035 (N.D. Ill. 1993) (noting that liability ofthe defendants under Section 15 is wholly dependent ontheir alleged liability under Section 11) , n8 Defendants'motion to dismiss Count III is denied .

n8 The Audit Committee defendants citeBomarko, Inc. v. Hemodynamics, 848 F. Supp.1335 (W.D. Mich. 1993), for the contention thatoutside directors who are also members of theaudit committee are not necessarily controllingpersons . The decision in Bomarko , was renderedpursuant to a motion for summary judgment,however, not a motion to dismiss . Indeed, thecourt relied on the deposition testimony of the de-fendants in concluding that they were not control-ling persons . 848 F, Supp, at 1340 . On summary

Page 1 1

judgment, plaintiffs may very well be unable toprovide sufficient evidence to support its allega-tion that the Audit Committee defendants werecontrolling persons. At this time, however, Plain-tiffs' allegations suffice to withstand a motion todismiss .

[*42]

E. State Law Claim s

Finally, Deloitte seeks dismissal of the various statelaw claims against it including common law fraud, viola-tion of the Illinois Consumer Fraud Act and negligentmisrepresentation (Counts VI-VIII) . The court will ad-dress each of these claims in turn .

1 . Common Law Fraud and Negligent Misrepre-sentation

Claims for common law fraud and negligent misrep-resentation require a showing of actual reliance . Board ofEducation v. A, C, & S, Inc., 131 Ill. 2d 428, 546 N.E.2d580, 137111. Dec. 635 (1989); City of Chicago v . Michi-gan Beach Housing Cooperative, 297 Ill . App. 3d 317,323, 696 N.E.2d 804, 809, 231 111. Dec. 508 (Ist Dist,1998) (the torts of negligent and fraudulent misrepresen-tation differ only in the mental state element -- both re-quire action taken in justifiable reliance on the truth ofthe statement) ; Morse v. Abbott Laboratories, 756 F.Supp. 1108, 1112 (N. D . Ill. 1991) .

Plaintiffs argue that they need not allege direct reli-ance in order to sustain their common law fraud claim,but should be able to assert fraud on the market . Thecourt disagrees . "Plaintiffs' contention that they shouldbe able to proceed on the common law fraud [*43] claimbased on a 'fr aud -on-the-market ' theory, without proof ofindividual reliance, is . . . without merit." In re SoybeanFutures Litigation, 892 F. Supp. 1025, 1030 (N.D . 111.1995) . Plaintiff has not cited , nor has the court found,"any Illinois precedent indicating that Illinois commonlaw recognizes a claim for fraud or negligent misrepre-sentation that does not plead actual direct reliance." Gil-Jbrd Partners v . Sensormatic Electronics Corp., 1997U.S. Dist. LEXIS 19032, 1997 WL 757495 at *12 (N.D .Ill . 1997) (Manning , J .) ; Morse, 756 F. Supp . at 1112 . n 9

n9 Plaintiffs cite Hartmann v . Prudential In-surance Co. of America, 9 Fad 1207 (7th Cir .1993) to support their contention that actual reli-ance need not be pled, However, "Ha rt mannshould be limited to its unusual facts and reason-ing : plaintiffs, who would have been beneficiariesto their deceased father's life insurance policywere it not for the misrepresentations made to thefather by his insurance agent, need not have re-

1998 U .S . Dist . LEXIS 17760, *

lied on the misrepresentations ; their father reliedon the misrepresentations and they were conse-quently harmed . (Citation omitted) Moreover, theforegoing is merely dictum, because the court didnot allow plaintiffs to recover under their fraudtheory ." Caplan v. International Fidelity Insur-ance Co ., 902 F. Supp. 170, 174 (N. D. Ill. 1995).

[*44]

Because Plaintiffs have failed to plead direct, indi-vidual reliance on the alleged misrepresentations, theirfraud and negligent misrepresentation claims cannotstand . See Ventre v . Datronic Rental Corp., 1996 U.S.Dist. LEXIS 17501, 1996 WL 681279 (N.D. 111. 1996)(Coax, J .) ("in cases such as this one where a class actionhas not been ce rt i fied, each individual plaintiff mustplead that he or she relied upon the misrepresentation") .Accordingly , Counts VI and VIII are dismissed .

2 . The Illinois Consumer Fraud and DeceptiveBusiness Practices Act

Deloitte argues for the dismissal of the ConsumerFraud Act claims on two grounds . First, Deloitte arguesthat accountants should be exempt from the ConsumerFraud Act, and second, that Plaintiffs have failed to al-lege fraud with particularity. Deloitte's second argumentis easily dispensed with in light the court's finding thatthe fraud allegations in the complaint satisfy Rule 9(b)'spleading requirements .

Nor does Deloitte's first argument find any supportin the case law. The parties do not dispute that securitiestransactions are subject to the Consumer Fraud Act . SeeLyne v. Arthur Andersen & Co., 772 F. Supp . 1064, 1068(N.D. Ill. 1991) . Deloitte [*45] argues, however, thatlike lawyers and doctors, accountants should not be sub-

Page 1 2

ject to liability under the Act. Deloitte cites a number ofcases exempting doctors and lawyers from the Act andreasons that all "regulated professions" including ac-counting, should be exempt.

The court finds no authority to support Deloitte's po-sition . Indeed, the only direct authority cited rejects theargument that the Consumer Fraud Act does not apply toaccountants who perform accounting services in connec-tion with securities offerings . Lyne, 772 F. Supp. 1064,1068 (N.D. lll . 1991). While noting, in dicta, the strin-gent policing of the legal and medical professions, thecourt found no "indication that Illinois courts would con-sider accountants to be immune from the provisions ofthe Consumer Fraud Act ." Id . Likewise, Deloitte has notprovided, and the court has not found, any additionalevidence indicating a willingness on the part of Illinoiscourts to exempt accountants from the Act. The courttherefore declines Deloitte's invitation to extend exemp-tions under the Illinois Consumer Fraud Act . Accord-ingly, Deloitte's motion to dismiss Count VII is denied .

IV. Conclusion

For the foregoing [*46] reasons, Deloitte's motionto dismiss Counts VI and VIII is granted and its motionto dismiss Counts 1, II, IV, and VII is denied . Shockey,Weisgal and Wyant's motion to dismiss Counts 1-111 isdenied .

Enter :

David H. Coar

United States District Judge

Dated : November 2, 1998

TAB 2

Page I

LEXSEE 2004 US DIST LEXIS 26488

CautionAs of: Jan 08, 2007

IN RE : FLEMING COMPANIES INC . SECURITIES & DERIVATIVELITIGATION, THIS DOCUMENT RELATES TO ALL CASE S

CIVIL ACTION NO. 5-03-MD-1530 (TJW), MDL-153 0

UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OFTEXAS

2004 U.S. Dis t. LEXIS 26488

June 10, 2004 , Decided

SUBSEQUENT HISTORY : Transferred by In re Flem- lett, New York, NY ; Peter E Kazanoff, Simpson Thachering Cos . Inc. Secs. & Derivative Litig., 2005 U.S. Dist . & Bartlett, New York, NY ; Nicholas Even, Haynes andLEXIS 10674 (J.P,M.L ., Apr . 20, 2005) Boone , Dallas, TX .

PRIOR HISTORY: In re Fleming Cos . Sees. & Deriva-tive Litig., 269 F. Supp. 2d 1374, 2003 U.S Dist. LEXIS11029 (J.P.ML., 2003)

DISPOSITION : [*1] Defendants' Motions to Dismissgranted in part and denied in part .

For Wachovia Securities , Inc ., Defend ant : Kenneth RDavid, Simpson Thacher & Bartlett, New York, NY ;Michael J Chepiga, Simpson Thacher & Bartle tt, NewYork, NY; Peter E Kazanoff , Simpson Thacher & Bart-lett, New York, NY ; Nicholas [*2] Even, Haynes andBoone , Dallas, TX .

COUNSEL : For In re : Fleming Companies, Inc ., Securi-ties & Derivative Litigation, Plaintiff : Samuel FranklinBaxter, Attorney at Law, Marshall, TX .

For Named Plaintiffs , Plaintiff: Steven W Pepich, LerachCoughlin Stoia Geller Rudman & Robbins, San Diego,CA .

For In re : Fleming Companies , Inc ., Securities & Deriva-tive Litigation Defendants, Defendant : Diane Marie Su-moski, Carrington Coleman Sloman & Blumenthal LLP,Dallas, TX; Randall Mark Foret, Secore & Waller, Dal-las, TX ; Stephen Cass Weiland , Patton Boggs , Dallas,TX.

For Thomas . Dahlen, Defendant : David Alan Stephan,McManemin & Smith, Dallas, TX .

For Deutsche Bank Securities Inc ., Defendant : KennethR David, Simpson Thacher & Bartlett, New York, NY ;Michael J Chepiga, Simpson Thacher & Bartlett, NewYork, NY; Peter F Kazanoff, Simpson Thacker & Bart-lett, New York, NY ; Nicholas Even, Haynes and Boone,Dallas, TX .

For Lehman Brothers Inc ., Defendant: Kenneth R David,Simpson Thacher & Bartlett, New York, NY ; Michael JChepiga, Simpson Thacher & Bartlett, New York, NY ;Peter E Kazanoff, Simpson Thacher & Bartlett, NewYork, NY; Nicholas Even, Haynes and Boone, Dallas,TX .

For Mark D Shapiro, Defendant : Terence J Hart, MunschHardt Kopf & Harr, Dallas, TX .

For Deloitte & Touche, Defendant : Keefe Michael Bern-stein, Akin Gump etal, Dallas, TX.

For Morgan Stanley & Co . Incorporated, Defendant :Kenneth R David, Simpson Thacher & Bartlett, NewYork, NY; Michael J Chepiga, Simpson Thacher & Bart-

2004 U.S . Dist. LEXIS 26488, *

For Alice M Peterson, Defendant : Diane Marie Sumoski,Carrington Coleman Sloman & Blumenthal LLP, Dallas,TX .

For Carlos M Hernandez, Defendant : Diane Marie Su-moski, Carrington Coleman Sloman & Blumenthal LLP,Dallas, TX .

For Robert S Ramada, Defendant : Diane Marie Sumoski,Carrington Coleman Sloman & Blumenthal LLP, Dallas,TX .

For Carol B Hallett, Defendant : Diane Marie Sumoski,Carrington Coleman Sloman & Blumenthal [*3] LLP,Dallas, TX .

For Archie R Dykes, Defendant : Diane Marie Sumoski,Carrington Coleman Sloman & Blumenthal LLP, Dallas,TX .

For Kenneth M Duberstein, Defendant: Diane MarieSumoski, Carrington Coleman Sloman & BlumenthalLLP, Dallas, TX.

For Herbert M Baum, Defendant : Diane Marie Sumoski,Carrington Coleman Sloman & Blumenthal LLP, Dallas,TX .

For Stephen . Davis, Defendant : Jim L Flegle, Loewin-sohn & Flegle, Dallas, TX .

For Terry Slater , Defendant: S Gene Cauley , CauleyBowman Carney & Williams, Little Rock , Ar; T BrentWalker, Cauley Bowman Carney & Williams , LittleRock, Ar; J Allen Carney, Cauley Bowman Carney &Williams, Li tt le Rock, Ar ; Marcus Bozem an , CauleyBowman Carney & Williams, Little Rock, Ar; Tiffany MWyatt , Cauley Bowman Carney & Williams , Li ttle Rock,Ar ,

For Neal J Rider, Defendant : Stephen Cass Weiland,Patton Boggs , Dallas, TX .

For Anthony Colarich, Movant : S Gene Cauley, CauleyBowman Carney & Williams, Little Rock, Ar ; Tiffany MWyatt, Cauley Bowman Carney & Williams, Little Rock,Ar.

For Raheela Zaman, Movant : S Gene Cauley, CauleyBowman Carney & Williams, Little Rock, Ar ; Tiffany MWyatt, Cauley Bowman Carney & Williams, [*4] LittleRock, Ar .

JUDGES: T. JOHN WARD, UNITED STATESDISTRICT JUDGE .

OPINION BY: T . JOHN WAR D

OPINION :

Page 2

MEMORANDUM OPINION AND ORDE R

1. INTRODUCTIO N

This private securities class action case relates toFleming Companies, Inc . ("Fleming") . Fleming, at onetime the second largest food distributor in the UnitedStates, first foreshadowed problems on July 30, 2002.The problems continued, culminating in a formal SECinvestigation into Fleming's accounting practices, A se-ries of class actions followed, which were consolidated .In April 2003, the company declared bankruptcy andannounced its need to make a massive restatement of itsearnings for 2001 and 2002 . The company has yet tomake any restatements of its earnings . An MDL proceed-ing ensued, and the cases were all transferred to thiscourt for pre-trial handling . The court has appointed alead plaintiff and set a briefing schedule . The plaintiffsfiled their Third Amended Consolidated Class ActionComplaint ("TAC°), The defendants have moved to dis-miss the TAC on various grounds . The court held an oralhearing on the matter and, after considering the motions,responses, the [*5] arguments, and the applicable law, isof the opinion that the following order should issue .

it. FACTUAL BACKGROUND ANDPROCEDURAL POSTURE

The facts are stated in . the light most favorable to theplaintiffs as alleged in the TAC. Baker v. Putnal, 75 F. 3d190, 196 (5th Cir. 1996) . Fleming is a wholesale dis-tributor of groceries . A wholesaler like Fleming pur-chases groceries from vendors and sells them to super-markets and grocery stores . During the 1990s, Flemingstruggled, due in part to its sharp business practices withits customers . Fleming's earnings steadily declined from1995 through 1998, culminating in the termination ofCEO Robert Smith in July, 1998 .

In November 30, 1998, Fleming appointed MarkHansen as CEO and Chairman of the Board . A weeklater, Fleming announced a "Strategic Plan to ImprovePerformance ." One part of the plan was to improve theperformance of Fleming's retail segment . AlthoughFleming had historically been a grocery wholesaler, thecompany identified a retail segment of price impact su-permarkets as a potential growth opportunity . A priceimpact supermarket is a sort of "no frills" approach toselling groceries . Price impact [*6] supermarkets typi-cally cost less to build and operate, lack amenities suchas delis, and, ultimately, pass the savings along to cus-tomers in the form of lower prices . Hansen told share-

2004 U.S . Dist . LEXIS 26488 ,

holders at an annual meeting that Fleming would make astronger and more focused push on retailing than everbefore .

Throughout 1999, 2000, and 2001, Fleming madevarious statements concerning its strategic plan to ana-lysts and investors . Fleming stated in a January 2000,press release that it attributed revenue growth to its em-phasis on Food4Less price impact stores and expectedfuture retail growth on a "same store" basis . To illustrate,Fleming expected that sales in retail stores 1, 2, and 3would increase over the numbers realized by those storesin the preceding year . The court notes that same storesales comparison is important because it allows analystsand investors to evaluate the actual internal growth of thecompany, unclouded by acquisitions or divestitures .

Throughout 2000, Fleming indicated that its focuswould be on price impact stores, at the expense of con-ventional stores. Fleming began to divest its conven-tional stores and, by May, 2001, represented that it hadsold all of its conventional [*7] stores . During that sametime period, Fleming reported earnings growth, attrib-uted in part to the success of its retail strategy . Also dur-ing this time period, Fleming and certain officers madepublic statements touting the success of its retail strategy .One Fleming press release stated, for instance, that Flem-ing's reported 36% net earning increase for the fourthquarter of 2001 "validated our strategic initiatives" relat-ing to price impact supermarkets . (TAC, P 82) . Fleming's10K for 2000 also promoted this retail strategy .

Throughout the first half of 2001, analysts reactedfavorably to Fleming's strategy . Bear, Steams & Co .,Deutsche Banc Alex . Brown, and UBS Warburg all is-sued reports commenting favorably on Fleming's retailoperations focus . (TAC, P 86-88) . Additional analystsresponded favorably throughout the balance of 2001 andinto the first half of 2002 . (TAC, PP 89-92).

All was not well inside Fleming, however . Theplaintiffs allege that Fleming used accounting manipula-tions to inflate its earnings numbers for 2001 and 2002 .The details of this scheme are discussed in more detailbelow; however, for present purposes, it is sufficient tonote that the plaintiffs allege [*81 first that Fleming ex-ecutives instituted a practice wherein Fleming's retail andwholesale divisions would arbitrarily and improperlydeduct amounts payable from vendors' invoices, withoutcause and with no expectation that the vendors wouldapprove the deduction . At the same time, although Flem-ing would reserve for a portion of those deductions, thereserves were often woefully inadequate to cover theamount of deductions . This practice had the effect ofinflating the quarterly and yearly earnings reported bythe company in press releases, SEC quarterly and annual

Page 3

reports, and Registration Statements filed in March andJune 2002, for public offerings of securities .

The second significant area of numbers manipula-tions that the plaintiffs attack is the company's reportingof same store sales growth. The plaintiffs allege that cer-tain Fleming executives instituted a practice whereby thereported same store sales figures were inflated, Theseinflated numbers led the investing public to assume thatFleming's retail strategic plan was growing . The plain-tiffs allege that the true same store sales figures, had theybeen revealed, would have shown that Fleming's retailsegment was suffering [*9] and that its price impactformat was not successful .

In July 2002, despite the company ' s statements con-cerning the success of its business strategy , Fleming be-gan to foreshadow problems in its retail segment . OnJuly 30, 2002 , Fleming issued a press release which indi-cated it was evaluating strategic alternatives to its retailsegment, and in particular , its price impact retail stores .The company stated that comparable store sales declined4 .7 percent . At the same time, according to the plaintiffs,Fleming overstated its wholesale earnings and maskedthe extent of retail losses to cushion any decline in stockvalue . Although Fleming reiterated its prior ea rn ingsforecasts, analysts began to doubt the validity of thosenumbers . J.P . Morgan analyst Stephen Chick, for in-stance , cut Fleming from "market perform" to "marketunderperform ." An article in Supermarket News ob-served that Fleming's announcement concerning alterna-tives to its retail segment "appears to have caught mostanalysts by surprise ." (TAC, P 272) .

On September 4, 2002, the Dow Jones Newswire re-leased an article on Fleming which disclosed customerdissatisfaction with certain of Fleming's price impactretail stores, [*101 inventory problems in those stores,and Fleming's practice of taking large vendor deductionsto increase the company's cash flow . Although the articlenoted that the company was not alone in this practice,some of Fleming's unidentified customers said they hadstopped shipping to Fleming because of the practice andone such customer, referring to Fleming, noted that"when it comes to deductions, they're off the scale com-pared to other customers," On September 5 , 2002, theWall Street Journal published the expose' released by theNewswire the day before .

Fleming responded to the September 5, 2002 articleby holding a conference call that day with analysts . Thecompany's CFO, Neal Rider, stated on the conferencecall that Fleming's vendor deductions were "appropri-ately reserved for" and Fleming's CEO stated that "wehave absolutely no issues with how we treated deduc-tions, we reserve against deductions, and we certainlydon't assume 100% collection ." (TAC, P 282). In the

2004 U.S . Dist . LEXIS 26488, *

same conference call, the officers stated that Fleming'sfinancial condition was solid and that the deductionswere an ordinary part of the business , and were an indus-try-accepted practice . Indeed, according to Rider, [*l1]"less than one-tenth of one percent of all the vendors wedeal with, and even a smaller amount of that in terms ofdollars , have a dispute that's risen to the level that we areat an impasse today." (TAC, P 289) . The plaintiffs con-tend that these statements were false .

The stock market reacted adversely to the September4 and 5 articles . On September 3, 2002, Fleming stockwas trading at $ 9 .31 per share . By September 5, thestock closed at S 6 .92 per share, a decline of 26%. Ac-cording to the plaintiffs, even though the stock price de-clined significantly , the statements by Fleming's execu-tives cushioned the fall of the stock because those state-ments represented that the deductions that might reach"impasse" were minimal and that the deductions in anyevent were an industry standard practice and were prop-erly accounted for . (TAC, PP 295-296).

On September 24, 2002, Fleming announced the di-vestiture of its price impact stores . Thereafter, on Octo-ber 23, 2002, Fleming announced its third quarter earn-ings, confirmed its decision to divest its price impactstores, and suggested that its relationship with its largestcustomer, Kmart, might be in jeopardy because ofKmart's bankruptcy [* 12] proceedings and reorganiza-tion .

On November 13, 2002, Fleming announced that theSEC had commenced an informal investigation intoFleming's accounting practices . In particular, the SEC'sinvestigation focused on Fleming's vendor trade practicesand the company's calculation of comparable store salesin its discontinued retail operations . Following Fleming'sJanuary 23, 2003, announcement of a $ 190 million lossin retail operations for 2002, and its announcement of theloss of the Kmart contract in February 2003, Fleming'sCFO insisted that the notion that Fleming would seekbankruptcy protection was "ludicrous ." On February 25,2003, the SEC reclassified its investigation as a formalone.

In February and March, 2003, Fleming's credit rat-ings were downgraded . On March 3, 2003, Fleming an-nounced the resignation of its CEO . Contrary to the pre-vious representations of Fleming's CFO and unable tosecure alternate sources of financing, Fleming announcedon April 1, 2003, that it had filed a voluntary petition forreorganization under Chapter 11 of the BankruptcyCode .

On April 17, 2003, Fleming announced that it wouldrestate its 2001 annual and qua rterly financial statementsand 2002 [* 13] qua rterly financial statements previouslyfiled with the Securities and Exchange Commission and

Page 4

that it would revise its previously announced 2002 fourthquarter and annual financial results . The Fleming pressrelease stated in part that "the Company expects that therelated restatements of the results for the full-year 2001and the first three quarters of 2002 will reduce the pre-tax financial results from continuing operations for suchperiods by an aggregate amount of not more than $ 85million ." According to the press release, the restatements"mainly correct the timing of when ce rtain vendor tran s-actions are recognized and the balance of certain reserveaccounts ." (TAC, P 322) . Finally, the press release statedthat Fleming's "fourth quarter 2002 pre-tax loss fromcontinuing operations will be increased by expenses to-taling not more than $ 80 million as a result of a numberof factors , including increased vendor payback rates, theKma rt contract cancellation and corrections identified asa result of the Audit and Compliance Commi ttee's inde-pendent investigation ." (TAC, P 322) . Fleming subse-quently announced it would restate its 2000 annual fi-nancial statements . To date, Fleming [* 14] has not actu-ally made its restatements ,

These securities fraud cases raise the same issues in-volved in the SEC investigation and the announced re-statements. The claims in this case may be divided intotwo categories: those brought under the 1934 Act andthose brought under the 1933 Act . As will be seen, dif-ferent standards apply to each .

In their 1934 Act claims , brought under section 10and Rule IOb(5) promulgated thereunder, the plaintiffscomplain of the conduct of five individual defendants .These defendants are referred to in this opinion either byindividual name or collectively as the 1934 Act Individ-ual Defendants . The 1934 Act Individual Defendantsinclude the following past or present company officers :Mark Hansen, Fleming 's Chief Executive Officer("CEO"), Neal J . Rider , Fleming's Chief Financial Offi-cer ("CFO"), Mark D. Shapiro , Fleming's Chief Account-ing Officer ("CAO"), Thomas Dahlen, a Fleming Execu-tive Vice -President and head of Fleming's Retail Divi-sion , and E . Stephen Davis , a Fleming Executive Vice-President and head of Fleming's Wholesale Division . Theplaintiffs have also asserted securities fraud claims underthe 1934 Act against Deloitte and Touche ("D&T"),[*15] Fleming's outside auditor . The basis for the plain-tiffs' fraud claims against D&T is that D&T conducted itsaudits while ignoring several "red flags" that D&Tshould have investigated and, by failing to do so, actedwith severe recklessness suf ficient to warr ant liabilityunder section 10 .

In their 1933 Act claims, brought under sections 1Iand 12(u)(2) of that act, the plaintiffs complain of theconduct of several additional individuals, namely theoutside directors and any other executive who signed theCompany's Registration Statements filed with the SEC in

2004 U . S . Dist . LEXIS 26488, *

March 2002 and June 2002 . These individuals are re-ferred to in this opinion as the 1933 Act Individual De-fendants . The 1993 Act Individual Defendants includethe following chief officers , directors and general coun-

sel : Mark Hansen, Neal J . Rider, Mark D. Shapiro, Her-bert M. Baum , Kenneth M . Duberstein, Archie R . Dukes,Carol B . Hallett , Robert S . Hamada, Alice M. Peterson,Edward C. Joulian, III , Guy A . Osbo rn and Carlos M .Hernandez . Also, the plaintiffs join as defendants to their1933 Act claims the various underwriters involved in theJune 2002 offering . These defendants are referred toherein as the Underwriter Defendants . f * l6] D&T isalso joined as a defendant to the 1933 Act claims . Thecou rt will sometimes refer to the defendants to the 1933Act claims collectively as the 1933 Act Defendants . Thecou rt now turns to a discussion of the applicable legalstandards , followed by a discussion of securities law,and, finally, to the analysis of the myriad issues raised bythe motions to dismiss .

III. STANDARDS FOR MOTIONS TO DISMISS INSECURITIES LITIGATIO N

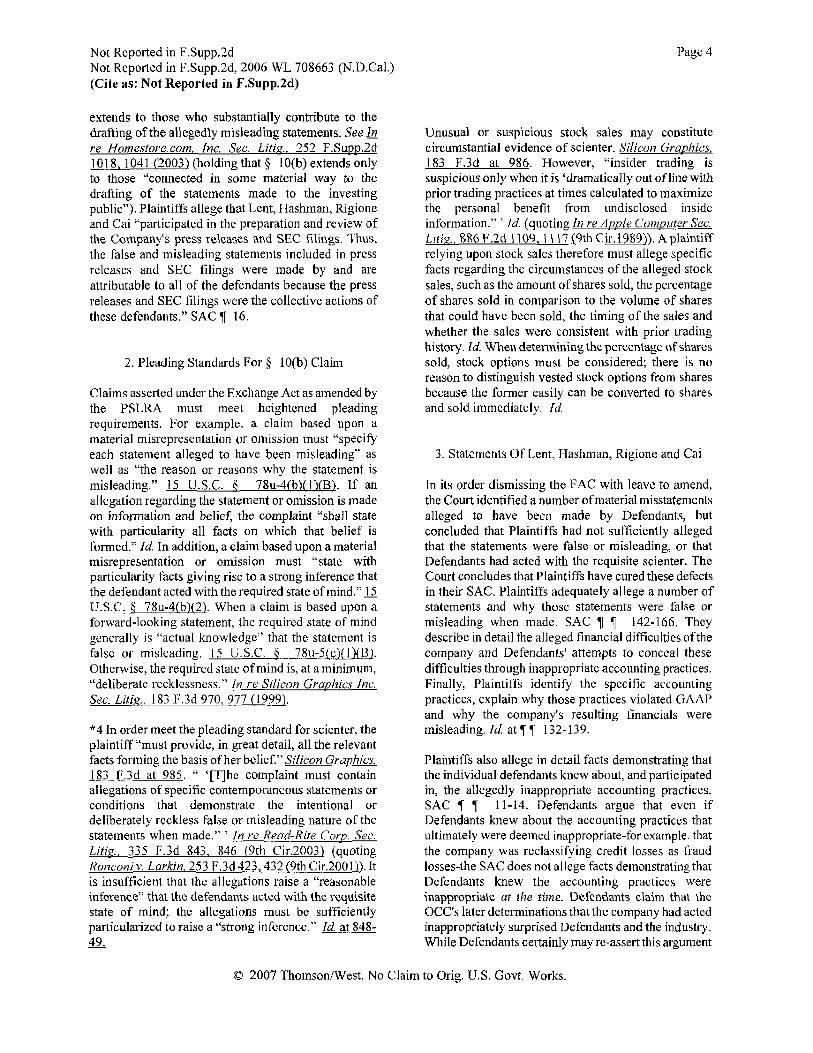

A. Rule 12(b)(6)