Embed Size (px)

Citation preview

EDITION 1.0

INTERNAL AUDIT COORDINATION BOARD

Performance Audit Manual for Public Internal Auditors

Case Studies

ANKARA | April 2016

INTERNAL AUDIT COORDINATION BOARD

Performance Audit Manual for Public Internal Auditors

Case Studies

ANKARA | April 2016

TABLE OF CONTENTS

1. CASE 1

PERFORMANCE AUDIT OF THE LIBRARY PROCESSES OF UNIVERSITY A ........................................ 7

A. LAUNCHING THE AUDIT ENGAGEMENT ................................................................................... 8

A1. ASSIGNMENT ................................................................................................................. 8

A2. PREPARATION OF THE IMPARTIALITY AND CONFIDENTIALITY DOCUMENT .................... 8

A3. NOTIFICATION TO THE AUDITEE ......................................................................................... 8

B. PRELIMINARY WORK ........................................................................................................... 11

B1. DEVELOPING THE AUDIT ENGAGEMENT TIME SCHEDULE ......................................... 10

B2. ASSESSMENT OF THE PERFORMANCE MANAGEMENT SYSTEM ................................. 13

B3. UNDERSTANDING THE LOGICAL FRAMEWORK ........................................................... 16

B4. IDENTIFICATION OF AUDIT COMPONENTS AND METHODS ....................................... 18

B5. KICK OFF MEETING ...................................................................................................... 18

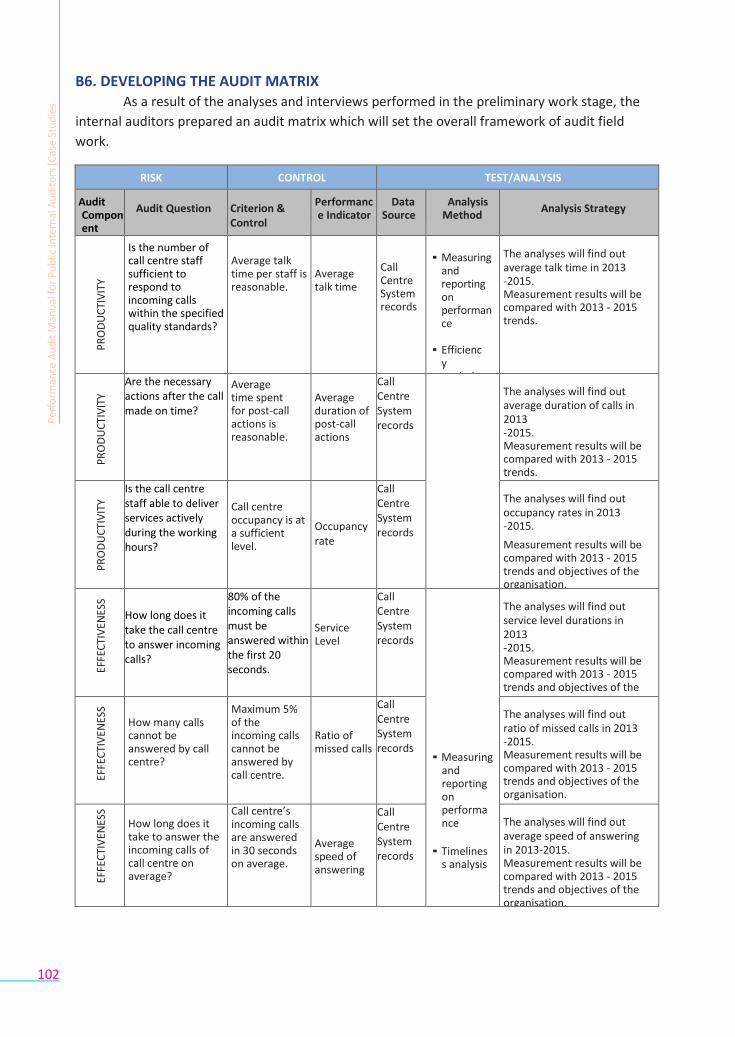

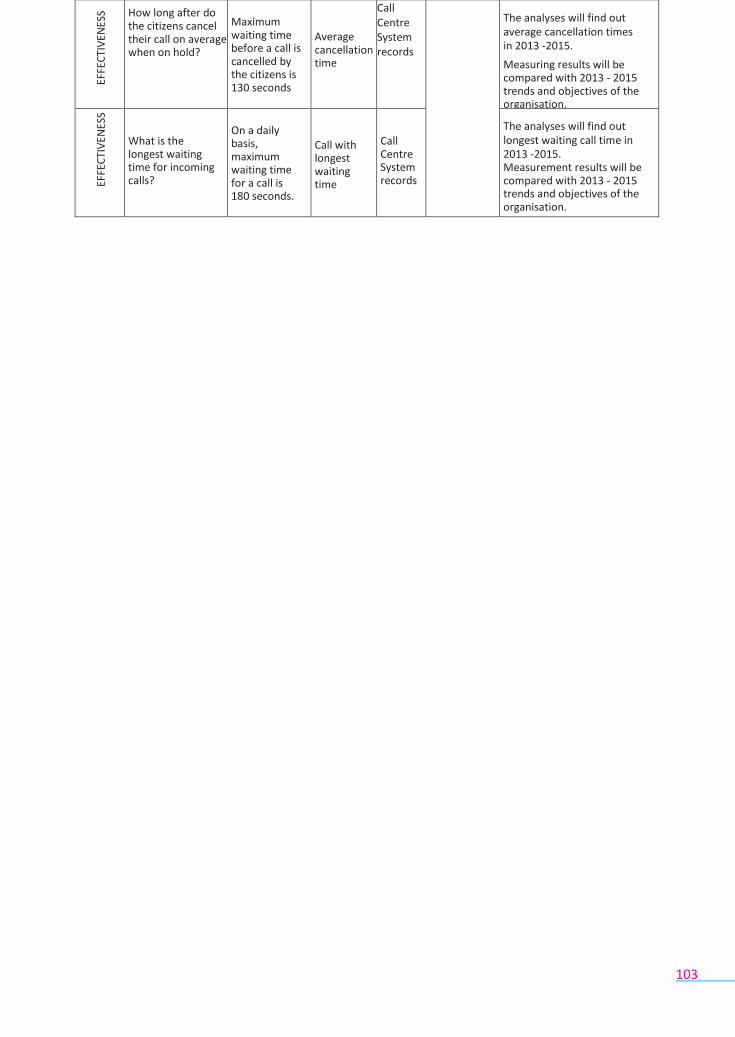

B6. DEVELOPING THE AUDIT MATRIX ............................................................................... 21

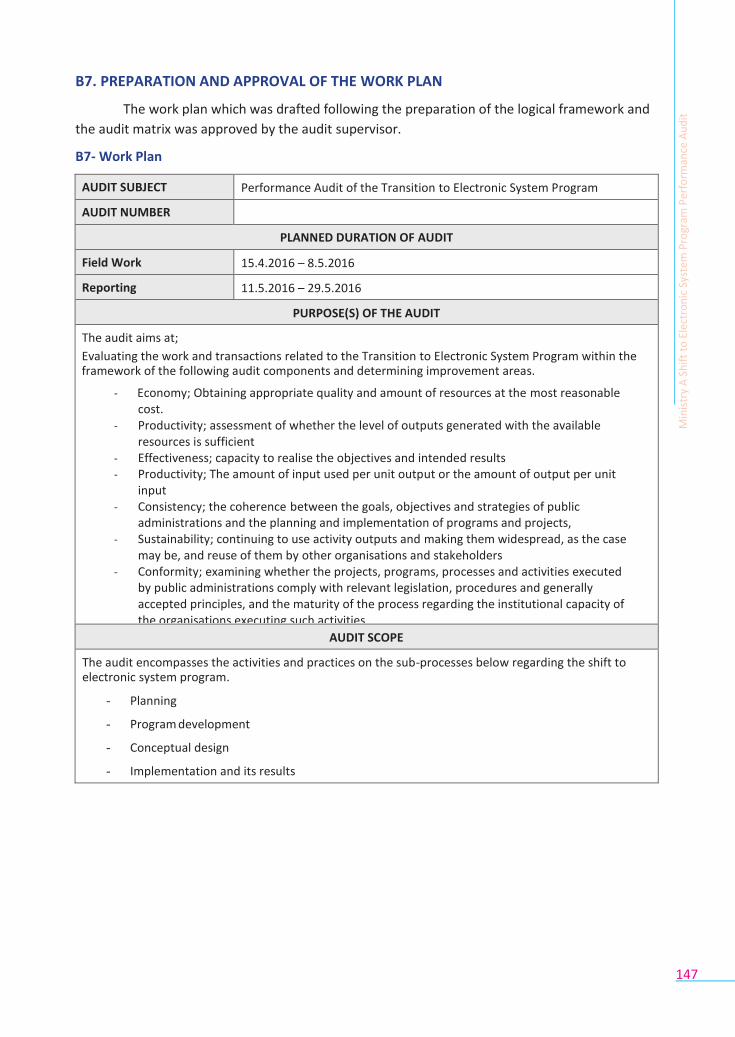

B7. PREPARATION AND APPROVAL OF THE WORK PLAN .................................................... 23

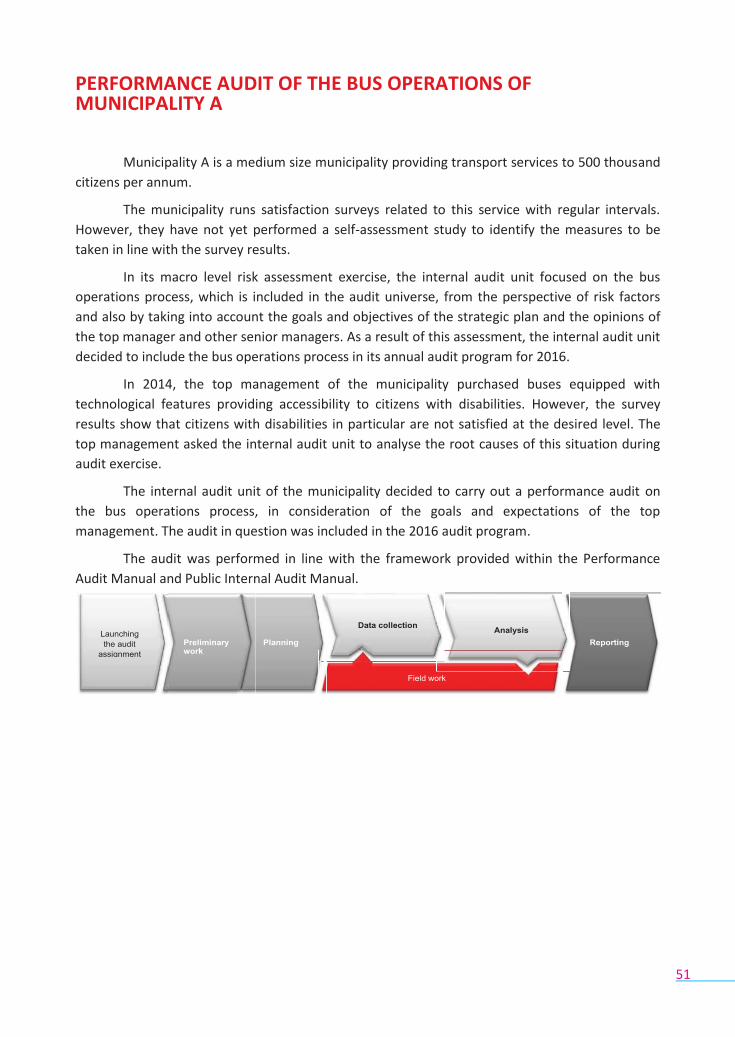

C.FIELD WORK......................................................................................................................... 25

C1. DATA COLLECTION ...................................................................................................... 25

C2. DATA ANALYSIS ........................................................................................................... 26

C3. IDENTIFICATION OF FINDINGS AND DEVELOPMENT OF RECOMMENDATIONS ......... 35

D.REPORTING ......................................................................................................................... 43

D1. OFFICIAL SHARING OF FINDINGS ........................................................................................ 43

D2. CLOSING MEETING ....................................................................................................... 48

2. CASE 2

PERFORMANCE AUDIT OF THE BUS OPERATIONS OF MUNICIPALITY A ..................................... 51

A. LAUNCHING THE AUDIT ENGAGEMENT ................................................................................. 52

A1. ASSIGNMENT ............................................................................................................... 52

A2. PREPARATION OF THE IMPARTIALITY AND CONFIDENTIALITY DOCUMENT .................. 52

A3. NOTIFICATION TO THE AUDITEE ................................................................................... 52

B. PRELIMINARY WORK ........................................................................................................... 55

B1. DEVELOPING THE AUDIT ENGAGEMENT TIME SCHEDULE.......................................... 55

B2. ASSESSMENT OF THE PERFORMANCE MANAGEMENT SYSTEM ................................. 56

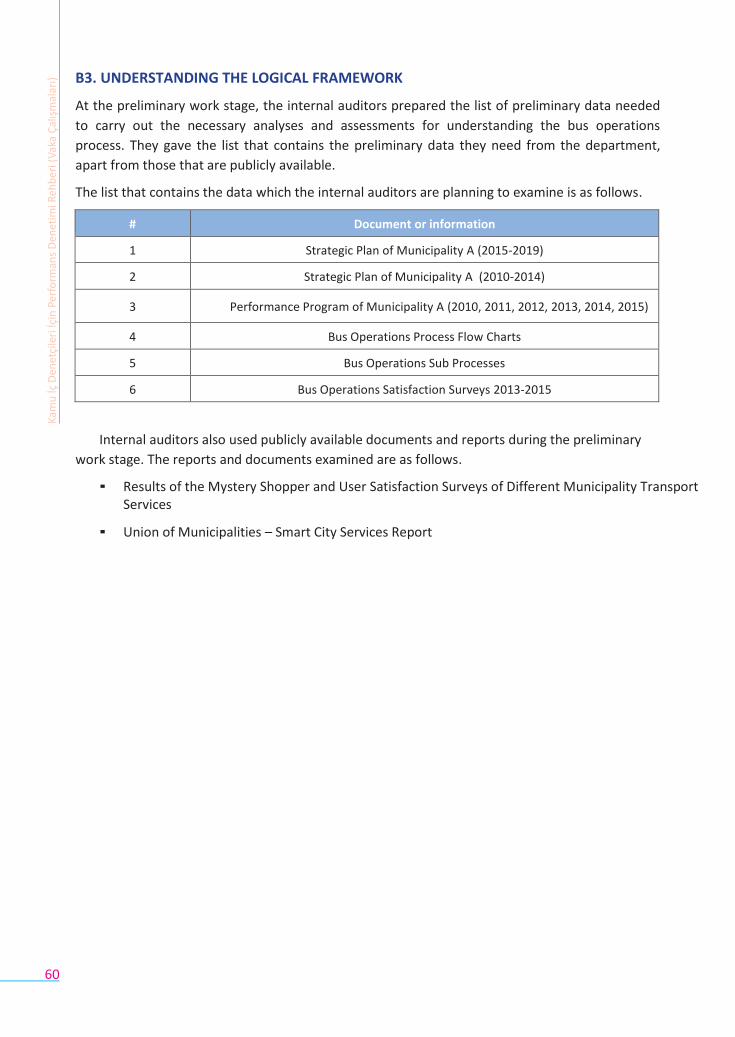

B3. UNDERSTANDING THE LOGICAL FRAMEWORK ........................................................... 60

B4. IDENTIFICATION OF AUDIT COMPONENTS AND METHODS ....................................... 62

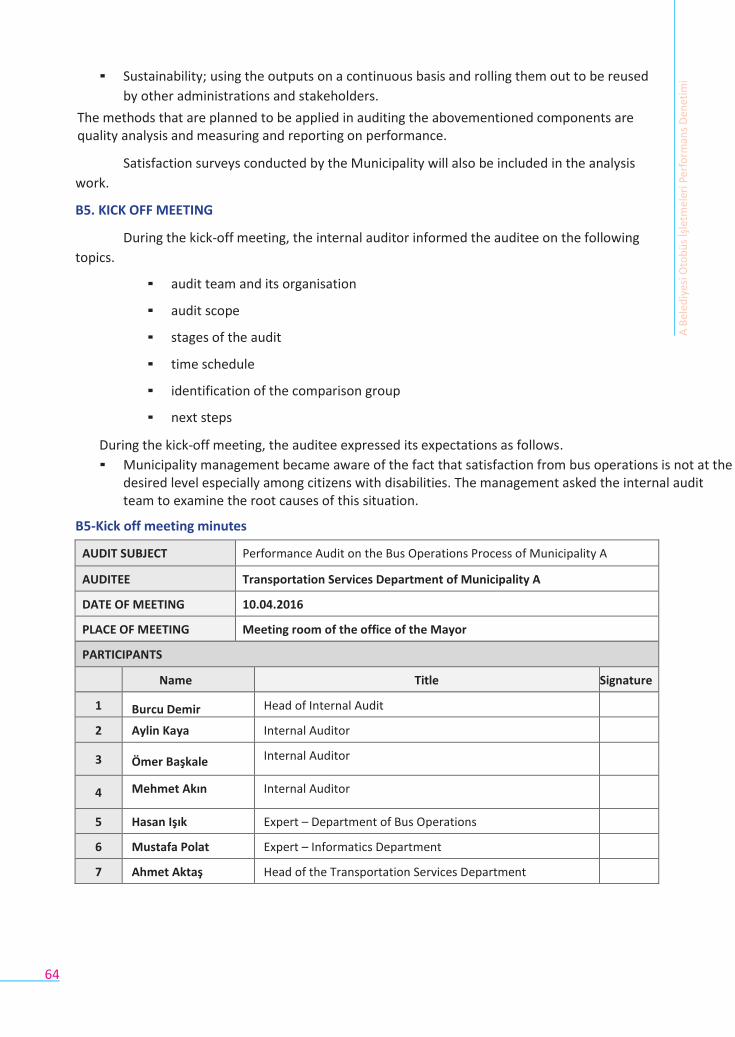

B5. KICK OFF MEETING ...................................................................................................... 63

B6. DEVELOPING THE AUDIT MATRIX ............................................................................... 64

B7. PREPARATION AND APPROVAL OF THE WORK PLAN .................................................... 68

C. FIELD WORK ........................................................................................................................ 70

C1. DATA COLLECTION....................................................................................................... 70

C2. DATA ANALYSIS ........................................................................................................... 72

D.R EPORTING.......................................................................................................................... 81

D1. OFFICIAL SHARING OF FINDINGS ........................................................................................ 81

D2. CLOSING MEETING ....................................................................................................... 85

3

4

3. CASE 3

PERFORMANCE AUDIT OF THE EMERGENCY CALL CENTRE OF PRESIDENCY A ........................... 89

A. DENETİM GÖREVİNİN BAŞLATILMASI ..................................................................................... 90

A1. GÖREVLENDİRME ........................................................................................................ 90

A2. PREPARATION OF THE IMPARTIALITY AND CONFIDENTIALITY DOCUMENT .................. 90

A3. NOTIFICATION TO THE AUDITEE ................................................................................... 90

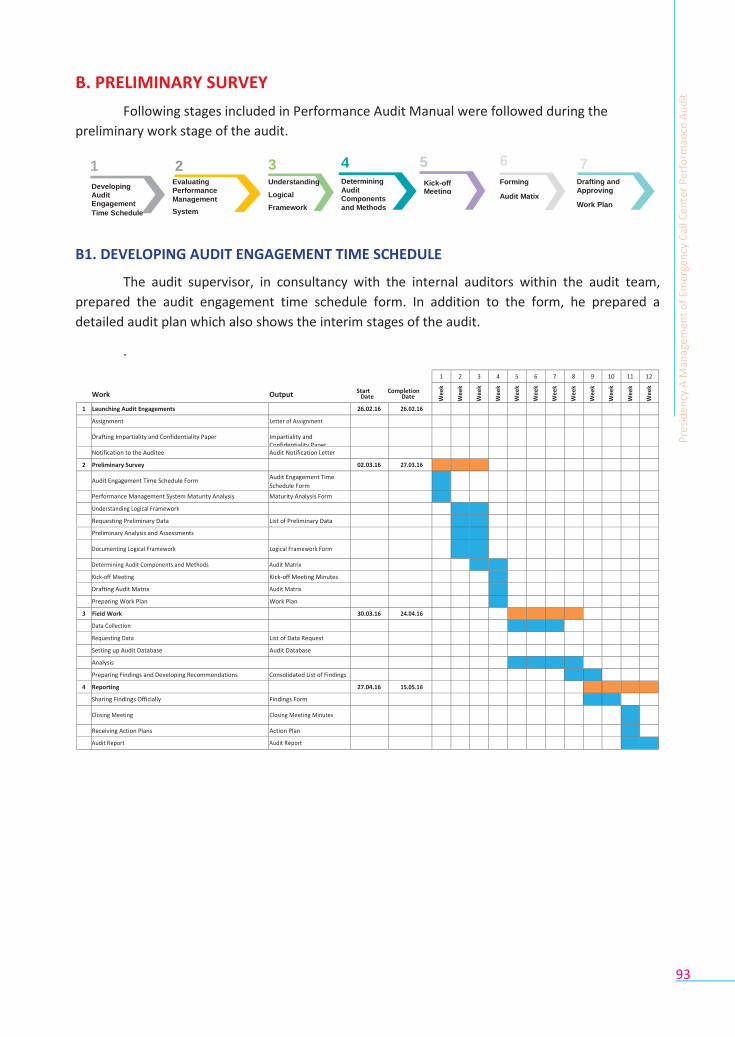

B. PRELIMINARY WORK ........................................................................................................... 93

B1. DEVELOPING THE AUDIT ENGAGEMENT TIME SCHEDULE ......................................... 93

B2. ASSESSMENT OF THE PERFORMANCE MANAGEMENT SYSTEM ................................. 94

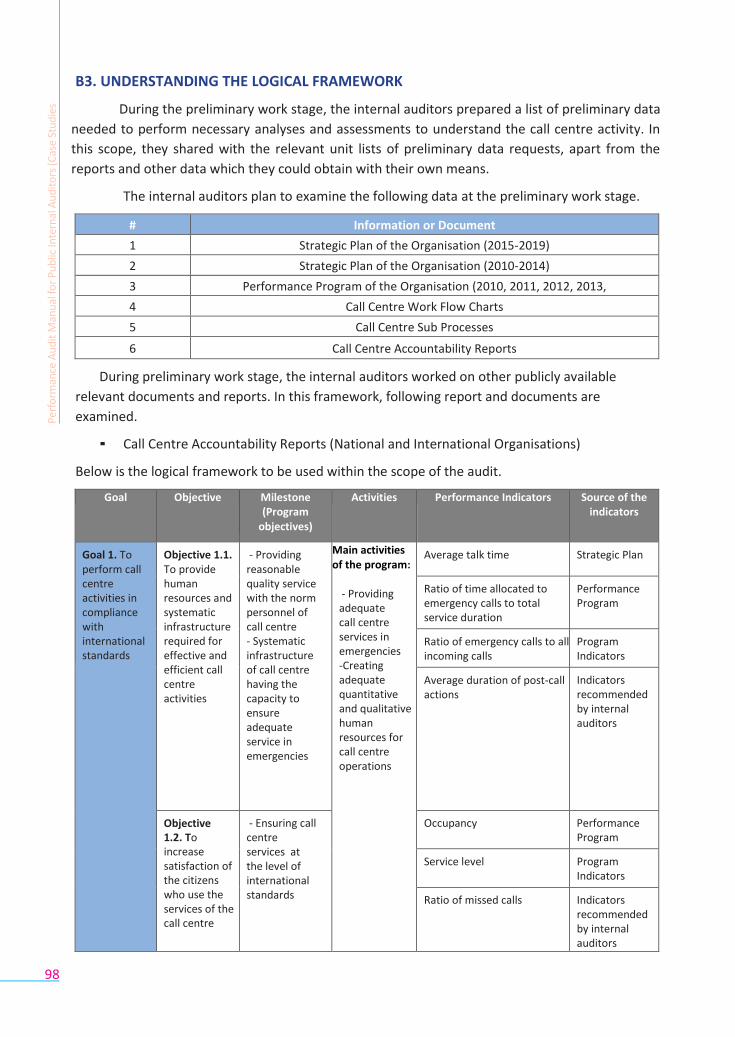

B3. UNDERSTANDING THE LOGICAL FRAMEWORK ........................................................... 98

B4. IDENTIFICATION OF AUDIT COMPONENTS AND METHODS ....................................... 99

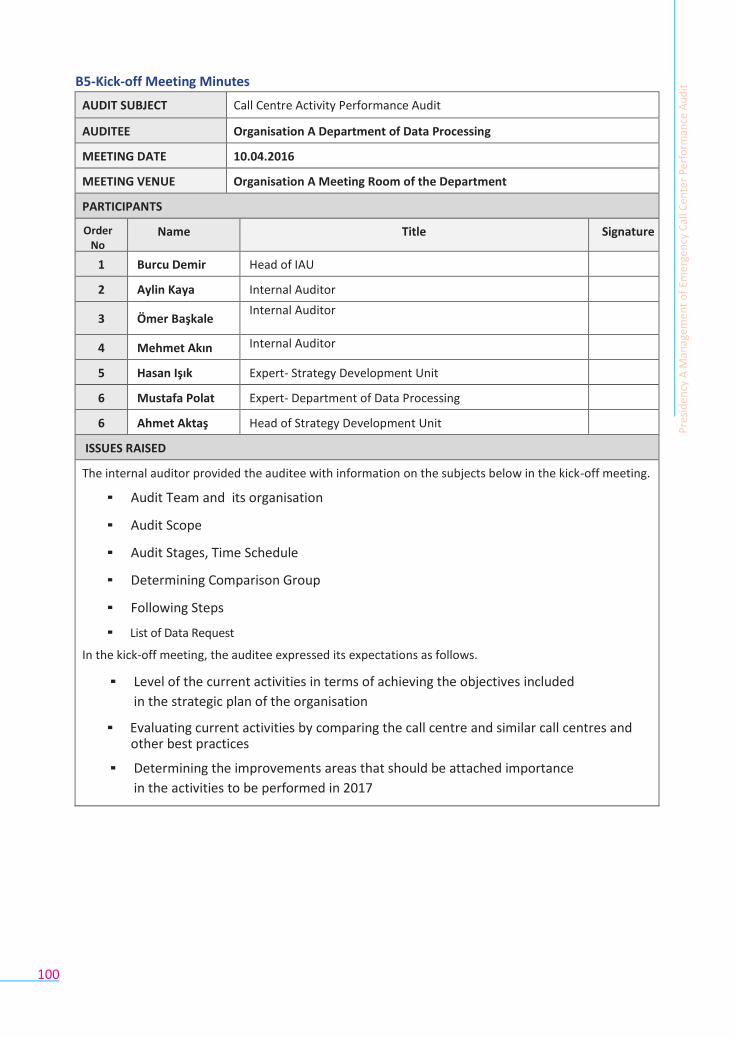

B5. KICK OFF MEETING ...................................................................................................... 99

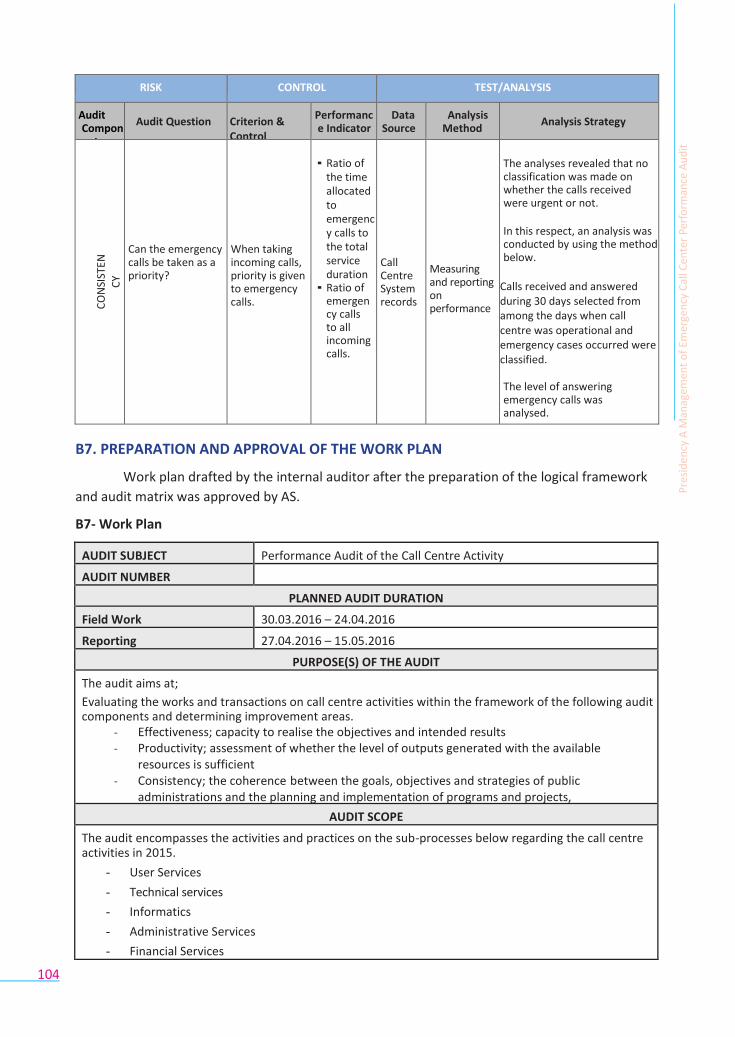

B6. DEVELOPING THE AUDIT MATRIX ............................................................................. 102

B7. PREPARATION AND APPROVAL OF THE WORK PLAN .................................................. 103

C. FIELD WORK ...................................................................................................................... 105

C1. DATA COLLECTION..................................................................................................... 105

C2. DATA ANALYSIS ......................................................................................................... 106

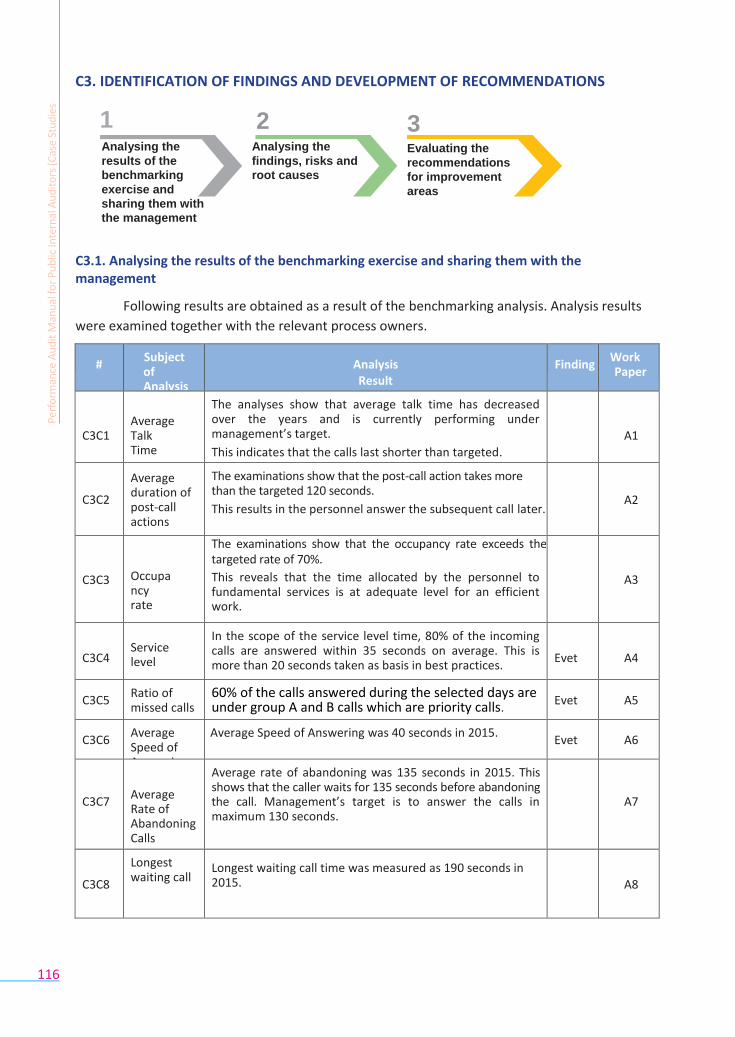

C3. IDENTIFICATION OF FINDINGS AND DEVELOPMENT OF RECOMMENDATIONS ....... 116

D.REPORTING ....................................................................................................................... 118

D1. OFFICIAL SHARING OF FINDINGS ...................................................................................... 118

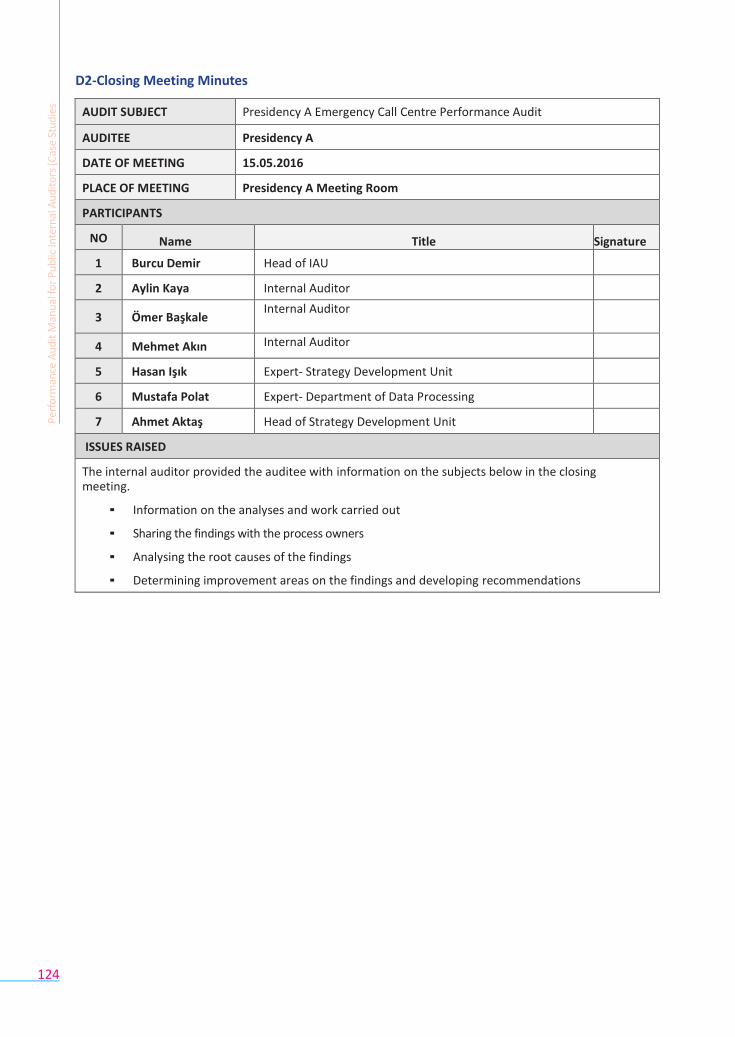

D2. CLOSING MEETING ..................................................................................................... 123

4. VAKA

PERFORMANCE AUDIT OF THE TRANSITION TO ELECTRONIC SYSTEM PROGRAM ................... 129

A. LAUNCHING THE AUDIT ENGAGEMENT .............................................................................. 130

A1. ASSIGNMENT ............................................................................................................. 130

A2. PREPARATION OF THE IMPARTIALITY AND CONFIDENTIALITY DOCUMENT ................ 130

A3. NOTIFICATION TO THE AUDITEE ................................................................................. 130

B. PRELIMINARY WORK ......................................................................................................... 133

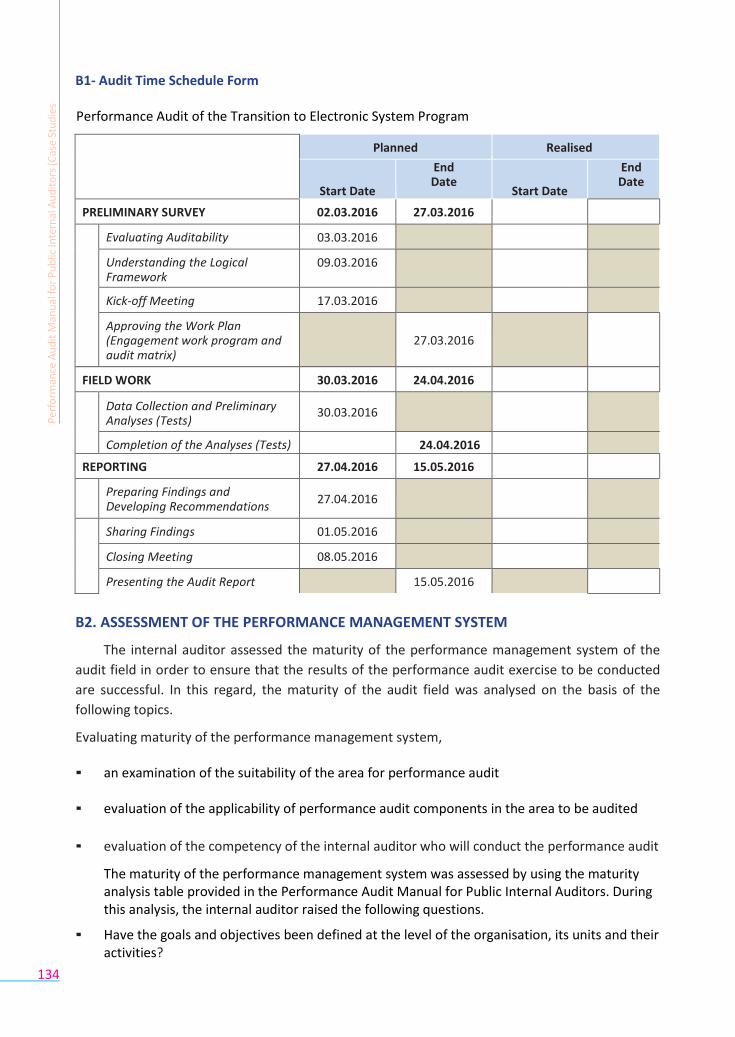

B1. DEVELOPING THE AUDIT ENGAGEMENT TIME SCHEDULE........................................ 133

B2. ASSESSMENT OF THE PERFORMANCE MANAGEMENT SYSTEM ............................... 134

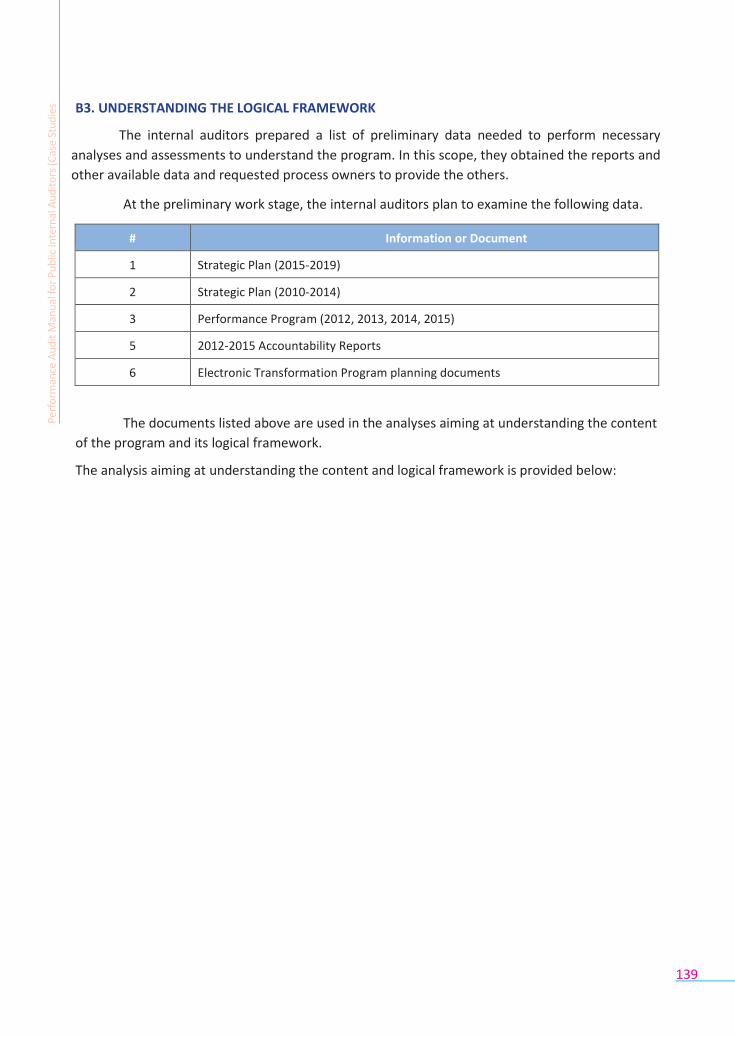

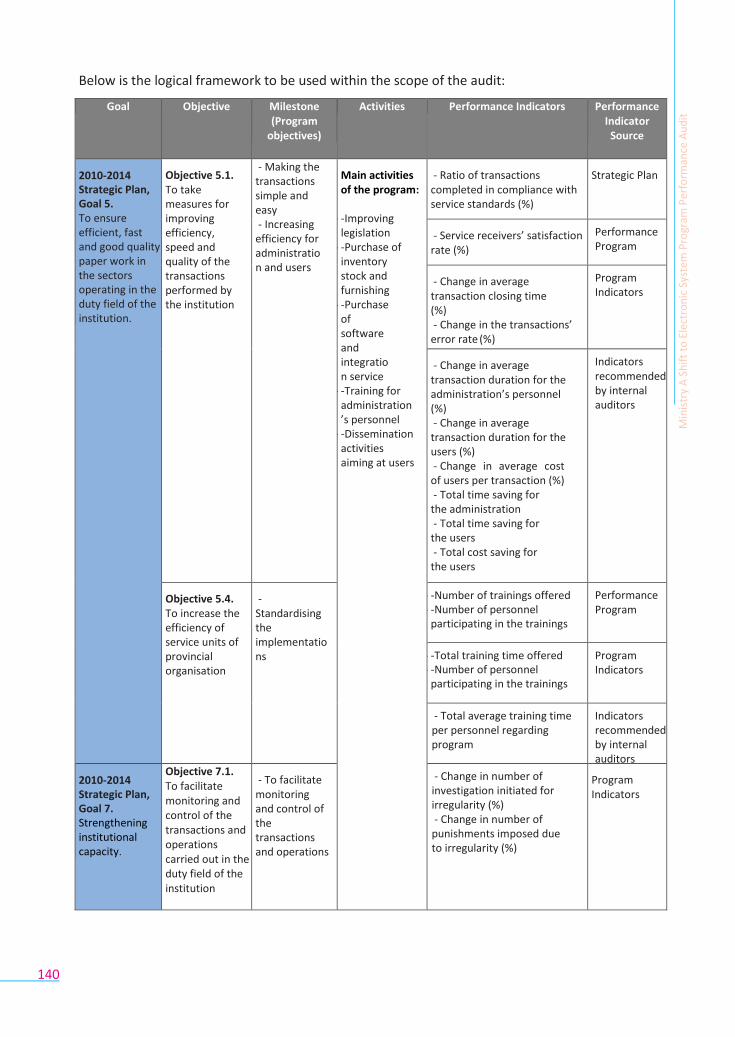

B3. UNDERSTANDING THE LOGICAL FRAMEWORK ......................................................... 138

B4. IDENTIFICATION OF AUDIT COMPONENTS AND METHODS ..................................... 140

B5. KICK OFF MEETING .................................................................................................... 140

B6. DEVELOPING THE AUDIT MATRIX ............................................................................. 142

B7. PREPARATION AND APPROVAL OF THE WORK PLAN .................................................. 147

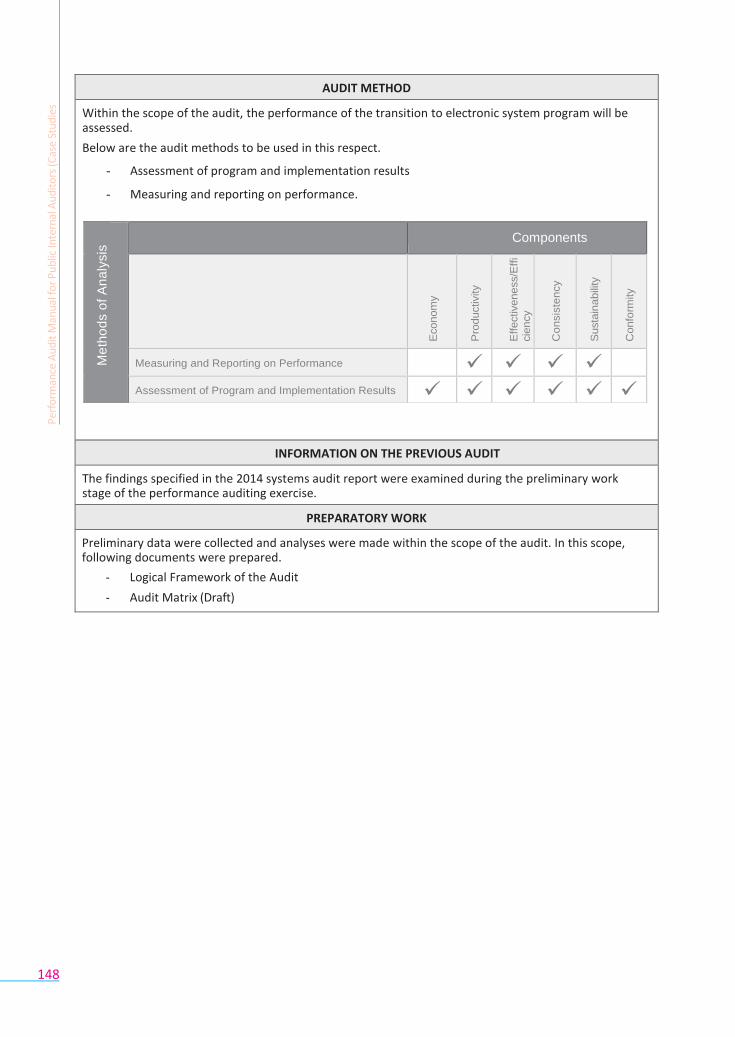

C. FIELD WORK ...................................................................................................................... 149

C1. DATA COLLECTION ..................................................................................................... 149

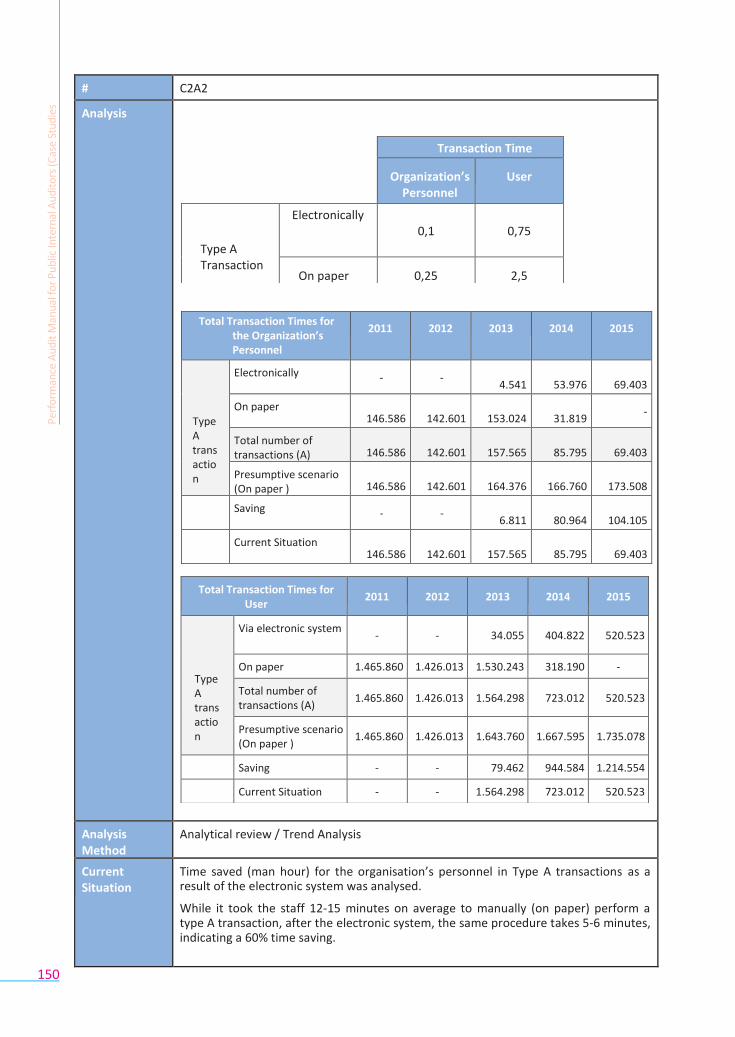

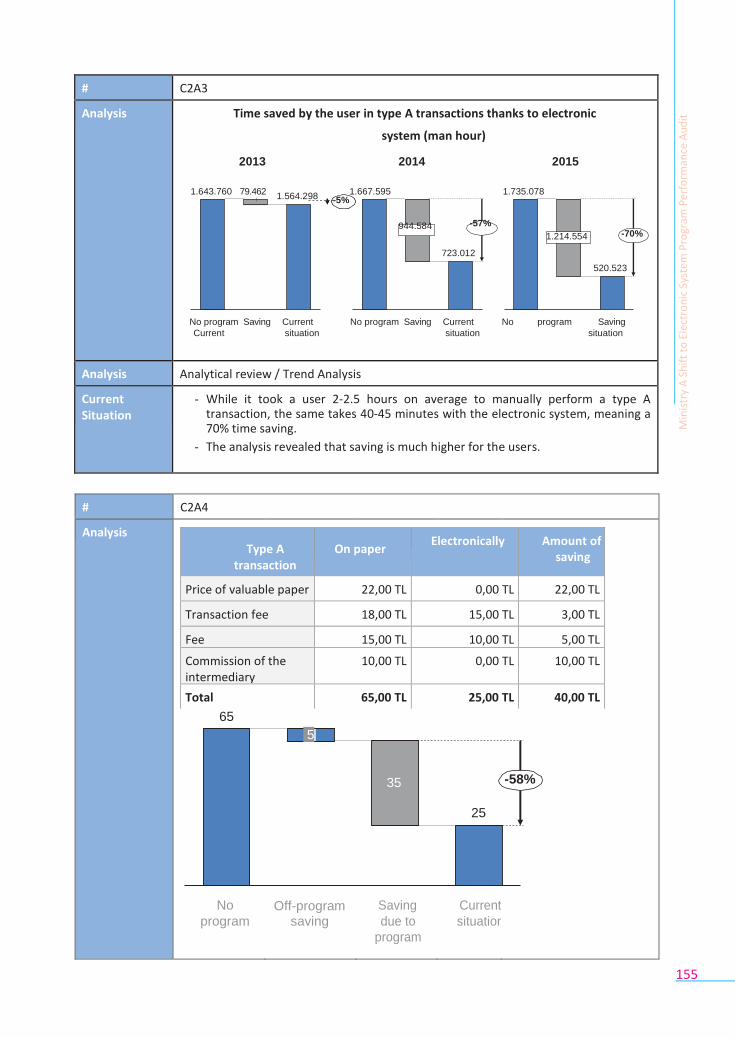

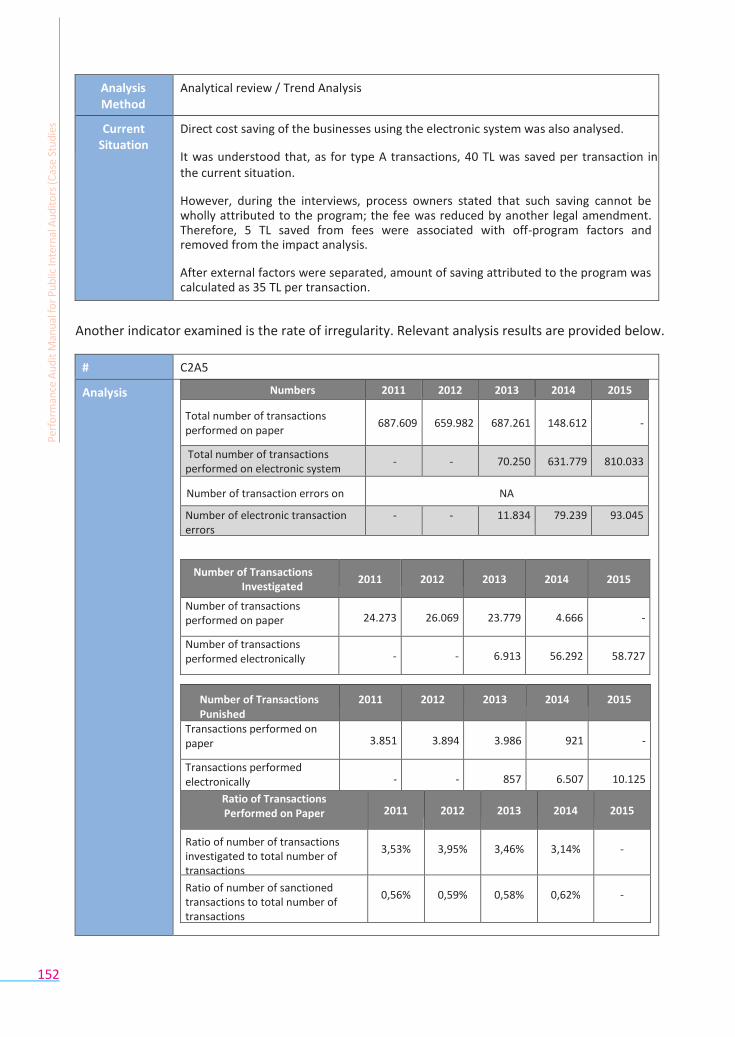

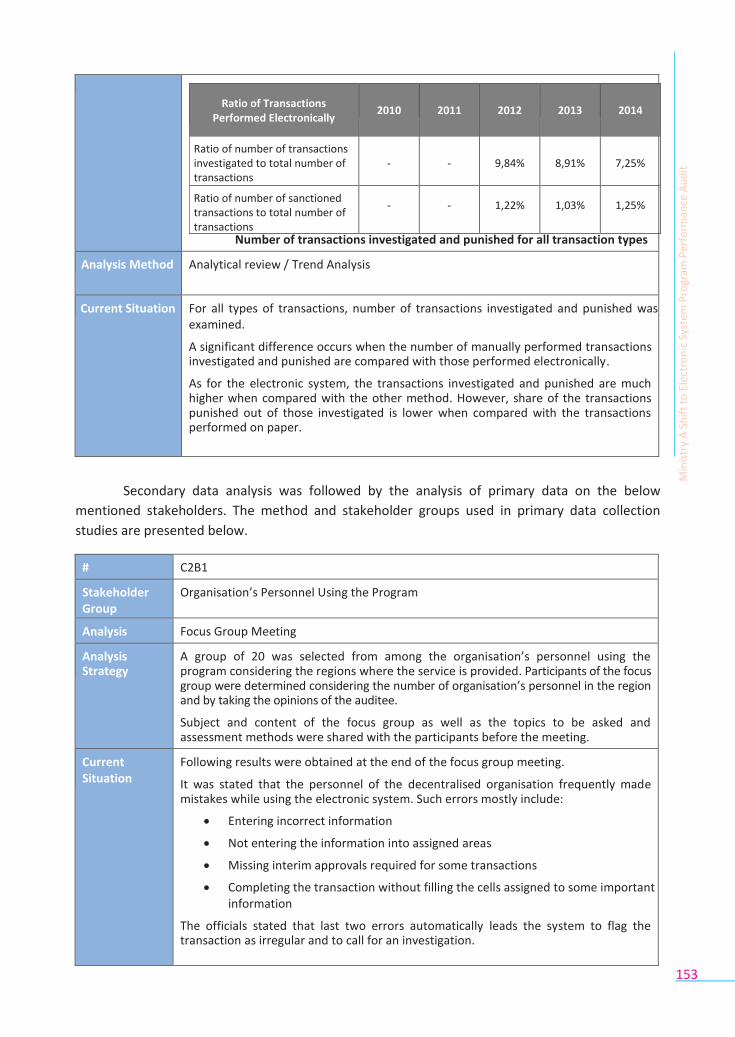

C2. DATA ANALYSIS ......................................................................................................... 149

C3. IDENTIFICATION OF FINDINGS AND DEVELOPMENT OF RECOMMENDATIONS ....... 154

D.REPORTING ....................................................................................................................... 156

D1. OFFICIAL SHARING OF FINDINGS ...................................................................................... 156

D2. CLOSING MEETING ..................................................................................................... 159

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

Performance Audit of the Library Processes of University A

The content of the case study is not related to any organisation, practice or person. The content developed is completely fictional.

7

PERFORMANCE AUDIT OF THE LIBRARY PROCESSES OF UNIVERSITY A

University A is a well-established university with faculties of social sciences, engineering

and fine arts, where the language of instruction is English. According to leading indices, the

university ranks among the ten most successful universities nationwide.

University management declared 2017 as the library year. In this regard, a new objective

was set to enrich the university library, which has been in service since the establishment of the

university and is considered to be among the best of its kind in the country, and to increase the

number of users which was in a decline from 2011 to 2015.

Within the scope of the macro level risk assessment exercise conducted by the internal audit

unit, the library processes, which form part of the audit universe, were assessed against the risk factors

and in consideration of the goals and objectives of the strategic plan and the opinions of the top

manager and other senior managers. At the end of the assessment, it was decided to include the library

process in the audit program for 2016.

The university management is planning to use the audit results to take necessary actions for

the restructuring of the library in 2017.

The main expectations of the top management from the audit to be carried out are:

Assessment of the extent to which the existing library processes are sufficient to reach

the objectives set forth in the strategic plan of the university,

Assessment of the existing activities in comparison with the other city universities similar

to University A and with other good practices,

Identification of areas of development that need to be taken into account while

developing activities within the scope of 2017 library year.

In line with the objectives and expectations of the management, the internal audit unit

of the university decided to carry out a performance audit on the library processes. The audit has

been included in the audit program for 2016.

The audit is performed in line with the framework provided in the Performance Audit

Manual for Public Internal Auditors and Public Internal Audit Manual.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

8

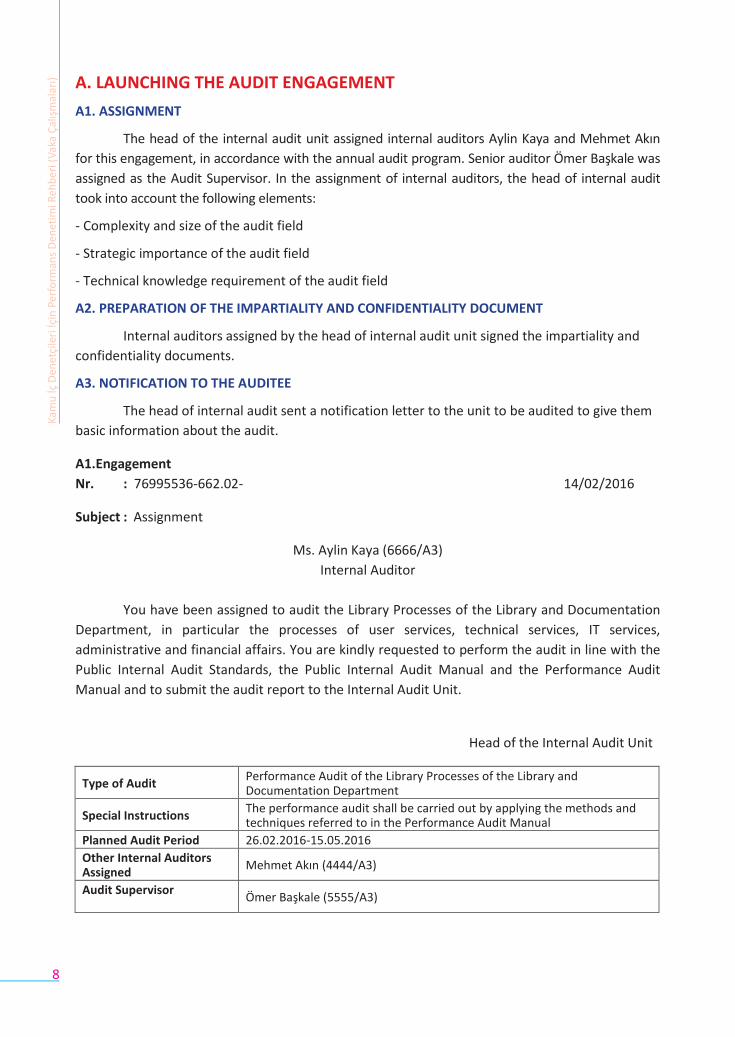

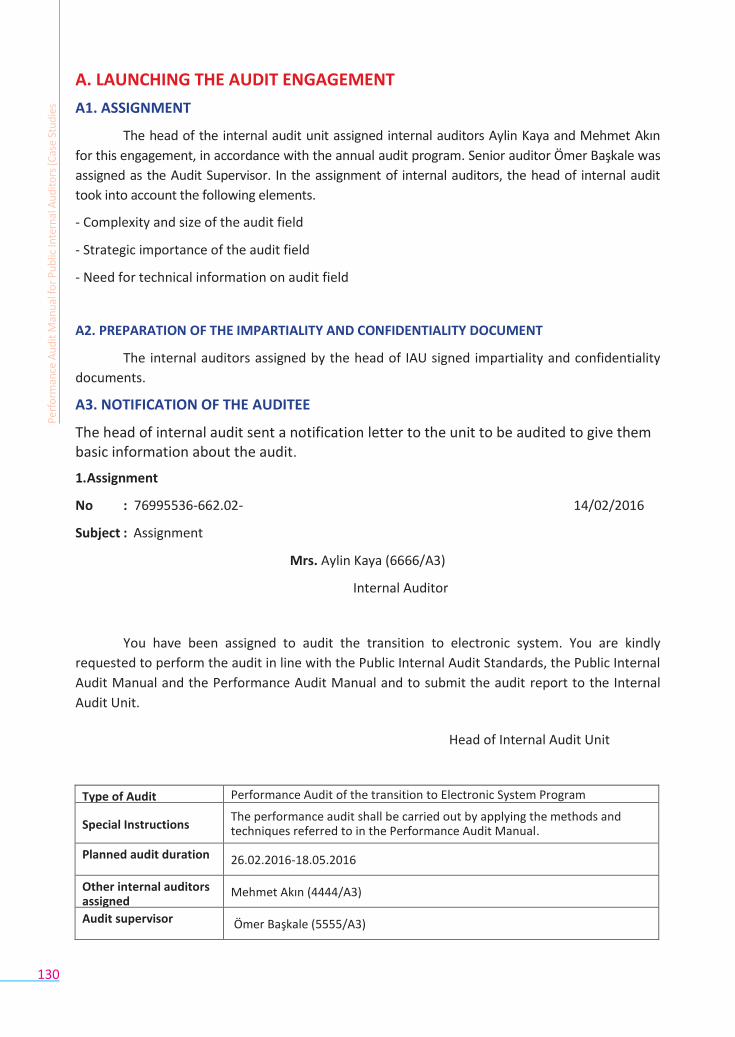

A. LAUNCHING THE AUDIT ENGAGEMENT

A1. ASSIGNMENT

The head of the internal audit unit assigned internal auditors Aylin Kaya and Mehmet Akın

for this engagement, in accordance with the annual audit program. Senior auditor Ömer Başkale was

assigned as the Audit Supervisor. In the assignment of internal auditors, the head of internal audit

took into account the following elements:

- Complexity and size of the audit field

- Strategic importance of the audit field

- Technical knowledge requirement of the audit field

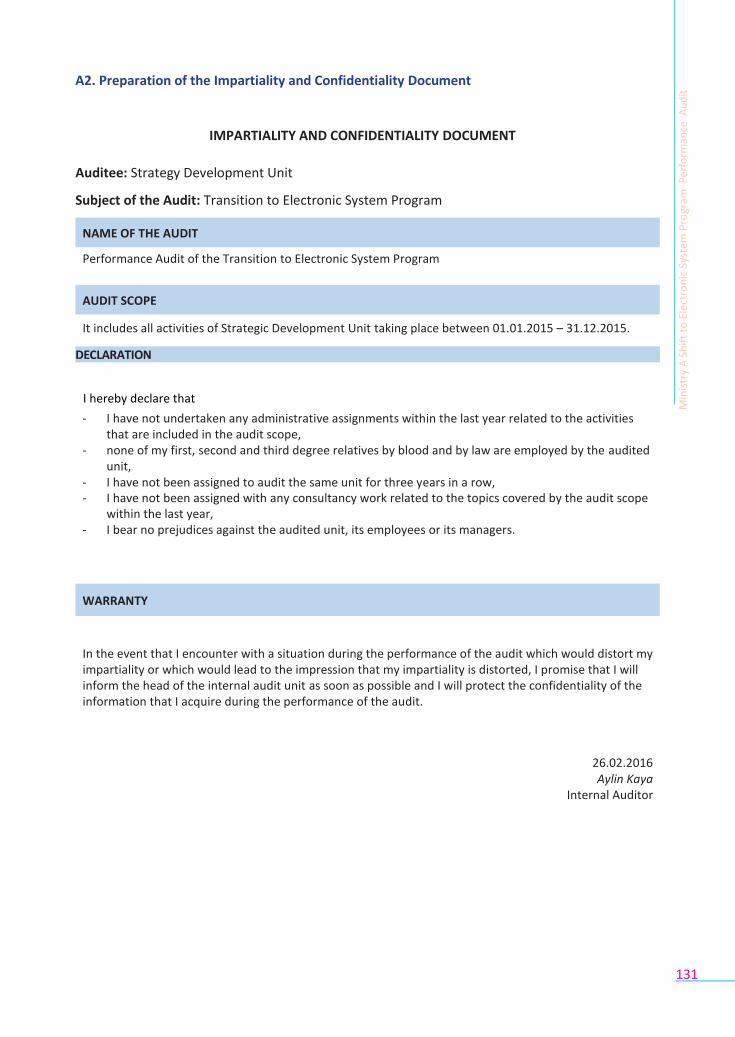

A2. PREPARATION OF THE IMPARTIALITY AND CONFIDENTIALITY DOCUMENT

Internal auditors assigned by the head of internal audit unit signed the impartiality and

confidentiality documents.

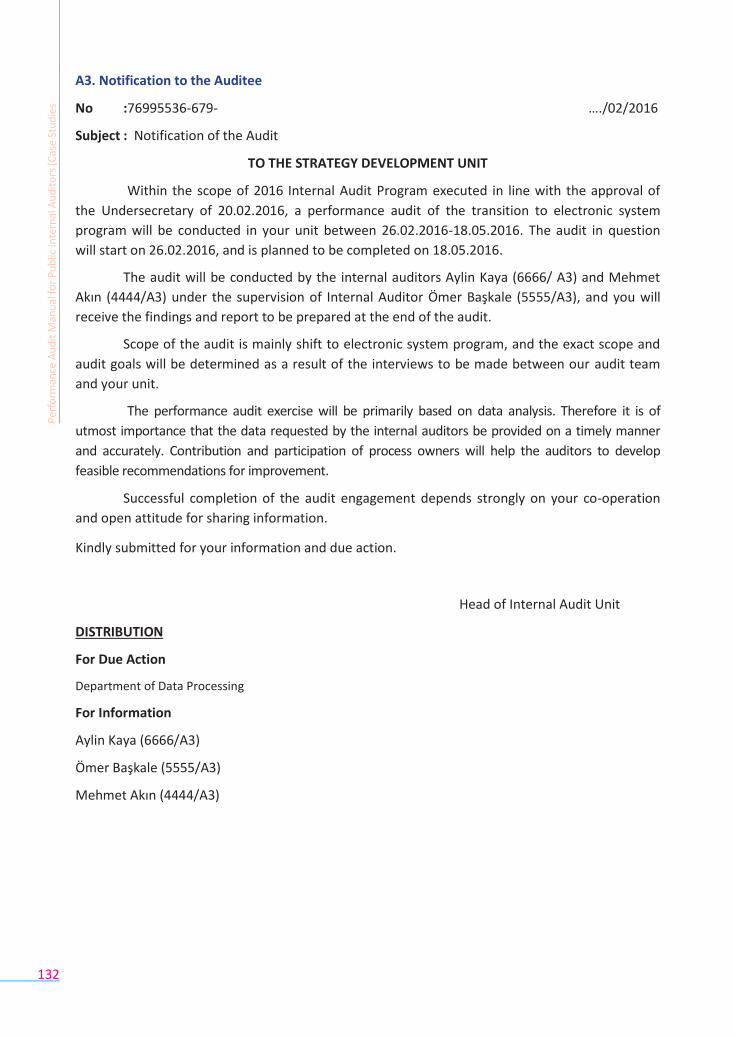

A3. NOTIFICATION TO THE AUDITEE

The head of internal audit sent a notification letter to the unit to be audited to give them

basic information about the audit.

A1.Engagement

Nr. : 76995536-662.02- 14/02/2016

Subject : Assignment

Ms. Aylin Kaya (6666/A3)

Internal Auditor

You have been assigned to audit the Library Processes of the Library and Documentation

Department, in particular the processes of user services, technical services, IT services,

administrative and financial affairs. You are kindly requested to perform the audit in line with the

Public Internal Audit Standards, the Public Internal Audit Manual and the Performance Audit

Manual and to submit the audit report to the Internal Audit Unit.

Head of the Internal Audit Unit

Type of Audit Performance Audit of the Library Processes of the Library and Documentation Department

Special Instructions The performance audit shall be carried out by applying the methods and techniques referred to in the Performance Audit Manual

Planned Audit Period 26.02.2016-15.05.2016

Other Internal Auditors Assigned

Mehmet Akın (4444/A3)

Audit Supervisor Ömer Başkale (5555/A3)

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

9

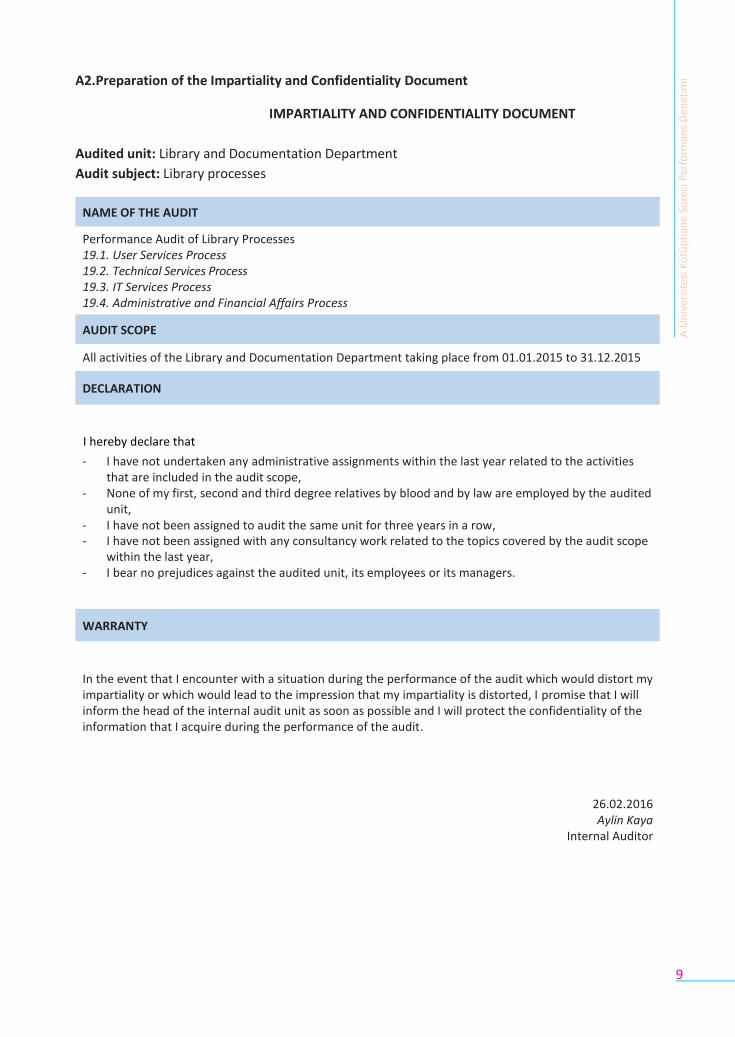

A2.Preparation of the Impartiality and Confidentiality Document

IMPARTIALITY AND CONFIDENTIALITY DOCUMENT

Audited unit: Library and Documentation Department

Audit subject: Library processes

Performance Audit of Library Processes 19.1. User Services Process 19.2. Technical Services Process 19.3. IT Services Process 19.4. Administrative and Financial Affairs Process

All activities of the Library and Documentation Department taking place from 01.01.2015 to 31.12.2015

I hereby declare that

- I have not undertaken any administrative assignments within the last year related to the activities that are included in the audit scope,

- None of my first, second and third degree relatives by blood and by law are employed by the audited unit,

- I have not been assigned to audit the same unit for three years in a row, - I have not been assigned with any consultancy work related to the topics covered by the audit scope

within the last year, - I bear no prejudices against the audited unit, its employees or its managers.

In the event that I encounter with a situation during the performance of the audit which would distort my impartiality or which would lead to the impression that my impartiality is distorted, I promise that I will inform the head of the internal audit unit as soon as possible and I will protect the confidentiality of the information that I acquire during the performance of the audit.

26.02.2016 Aylin Kaya

Internal Auditor

DECLARATION

NAME OF THE AUDIT

AUDIT SCOPE

WARRANTY

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

11

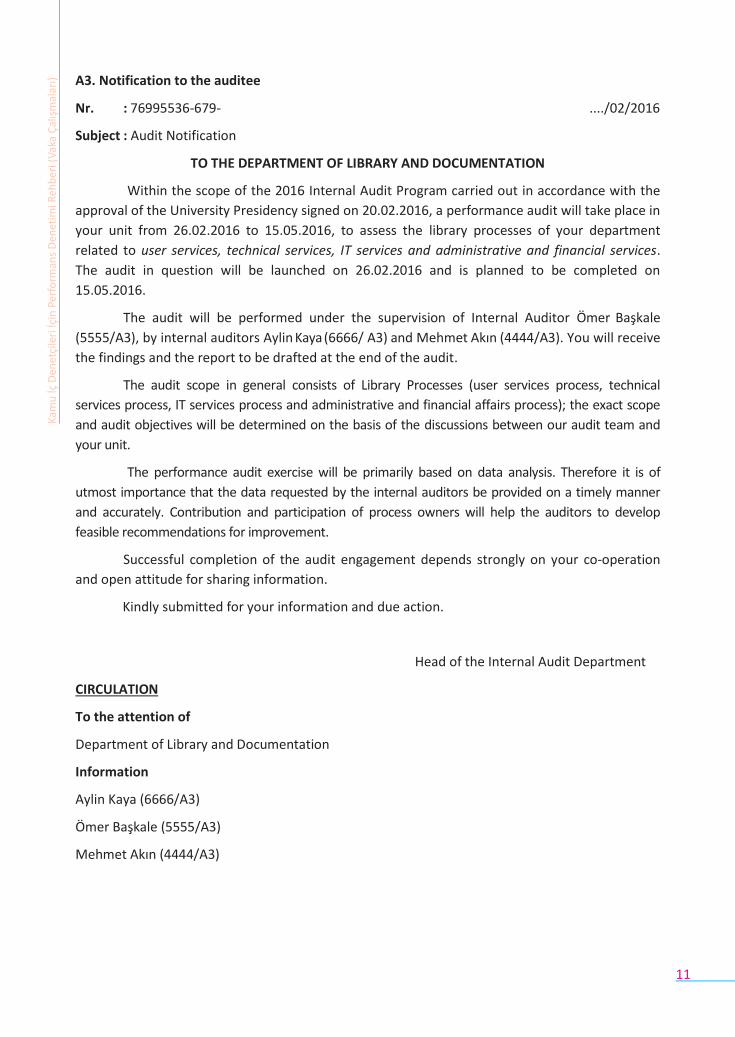

A3. Notification to the auditee

Nr. : 76995536-679- ..../02/2016

Subject : Audit Notification

TO THE DEPARTMENT OF LIBRARY AND DOCUMENTATION

Within the scope of the 2016 Internal Audit Program carried out in accordance with the

approval of the University Presidency signed on 20.02.2016, a performance audit will take place in

your unit from 26.02.2016 to 15.05.2016, to assess the library processes of your department

related to user services, technical services, IT services and administrative and financial services.

The audit in question will be launched on 26.02.2016 and is planned to be completed on

15.05.2016.

The audit will be performed under the supervision of Internal Auditor Ömer Başkale

(5555/A3), by internal auditors Aylin Kaya (6666/ A3) and Mehmet Akın (4444/A3). You will receive

the findings and the report to be drafted at the end of the audit.

The audit scope in general consists of Library Processes (user services process, technical

services process, IT services process and administrative and financial affairs process); the exact scope

and audit objectives will be determined on the basis of the discussions between our audit team and

your unit.

The performance audit exercise will be primarily based on data analysis. Therefore it is of

utmost importance that the data requested by the internal auditors be provided on a timely manner

and accurately. Contribution and participation of process owners will help the auditors to develop

feasible recommendations for improvement.

Successful completion of the audit engagement depends strongly on your co-operation

and open attitude for sharing information.

Kindly submitted for your information and due action.

Head of the Internal Audit Department

CIRCULATION

To the attention of

Department of Library and Documentation

Information

Aylin Kaya (6666/A3)

Ömer Başkale (5555/A3)

Mehmet Akın (4444/A3)

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

10

Identification of Audit Components and Methods

Kick off meeting

Understanding

the Logical

Framework

Audit Matrix Preparation and

approval of the Work

Plan

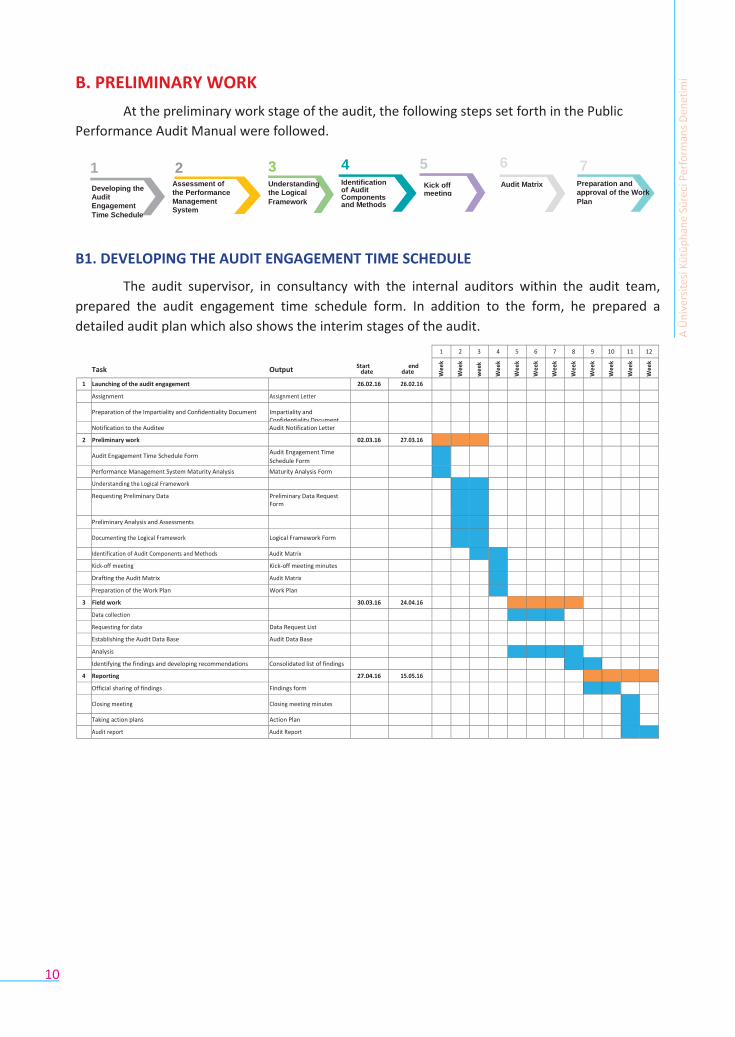

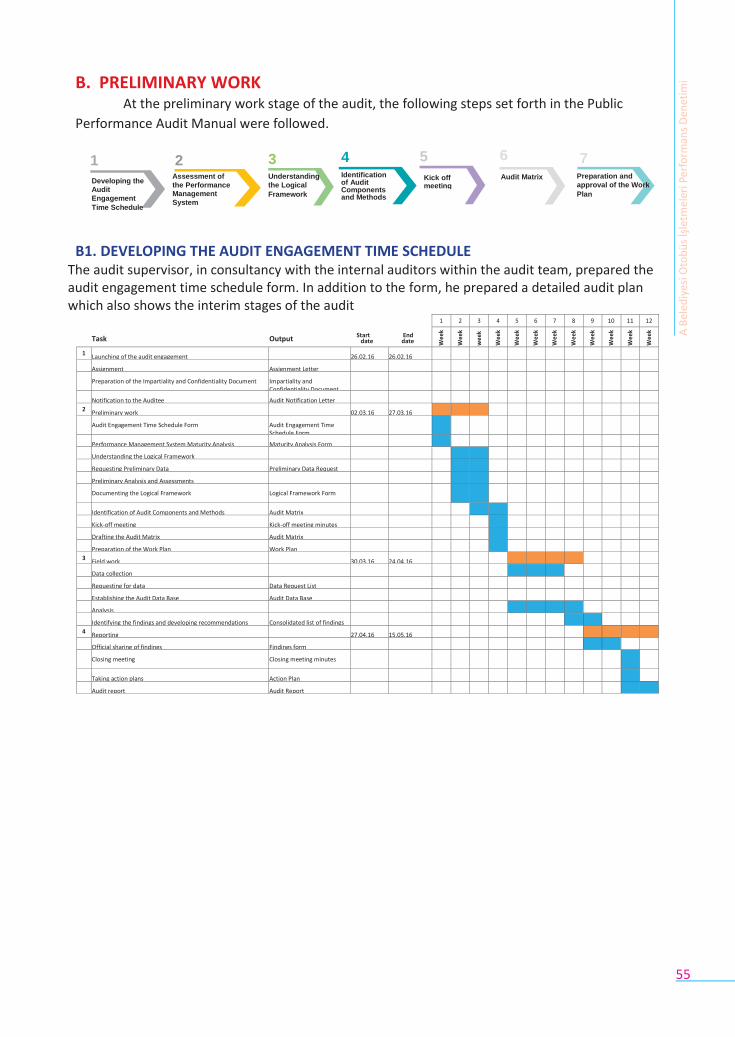

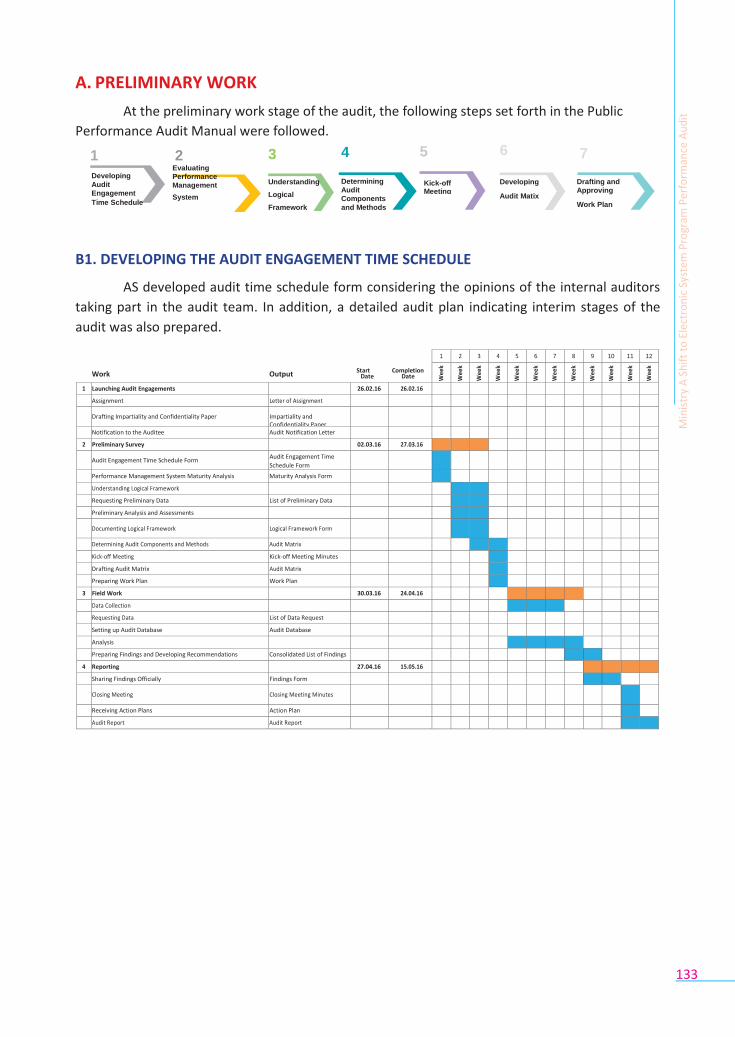

B. PRELIMINARY WORK

At the preliminary work stage of the audit, the following steps set forth in the Public

Performance Audit Manual were followed.

1 2 3 4 5 6 7 Assessment of

the Performance

Management

System

B1. DEVELOPING THE AUDIT ENGAGEMENT TIME SCHEDULE

The audit supervisor, in consultancy with the internal auditors within the audit team,

prepared the audit engagement time schedule form. In addition to the form, he prepared a

detailed audit plan which also shows the interim stages of the audit.

Task Output Start end date date

1 2 3 4 5 6 7 8 9 10 11 12

Wee

k

Wee

k

wee

k

Wee

k

Wee

k

Wee

k

Wee

k

Wee

k

Wee

k

Wee

k

Wee

k

Wee

k

1 Launching of the audit engagement 26.02.16 26.02.16 Assignment Assignment Letter Preparation of the Impartiality and Confidentiality Document Impartiality and

Confidentiality Document

Notification to the Auditee Audit Notification Letter 2 Preliminary work 02.03.16 27.03.16

Audit Engagement Time Schedule Form Audit Engagement Time

Schedule Form

Performance Management System Maturity Analysis Maturity Analysis Form Understanding the Logical Framework Requesting Preliminary Data Preliminary Data Request

Form

Preliminary Analysis and Assessments Documenting the Logical Framework Logical Framework Form

Identification of Audit Components and Methods Audit Matrix Kick-off meeting Kick-off meeting minutes Drafting the Audit Matrix Audit Matrix Preparation of the Work Plan Work Plan

3 Field work 30.03.16 24.04.16 Data collection Requesting for data Data Request List Establishing the Audit Data Base Audit Data Base Analysis Identifying the findings and developing recommendations Consolidated list of findings

4 Reporting 27.04.16 15.05.16 Official sharing of findings Findings form Closing meeting Closing meeting minutes

Taking action plans Action Plan Audit report Audit Report

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

Developing the

Audit

Engagement

Time Schedule

12

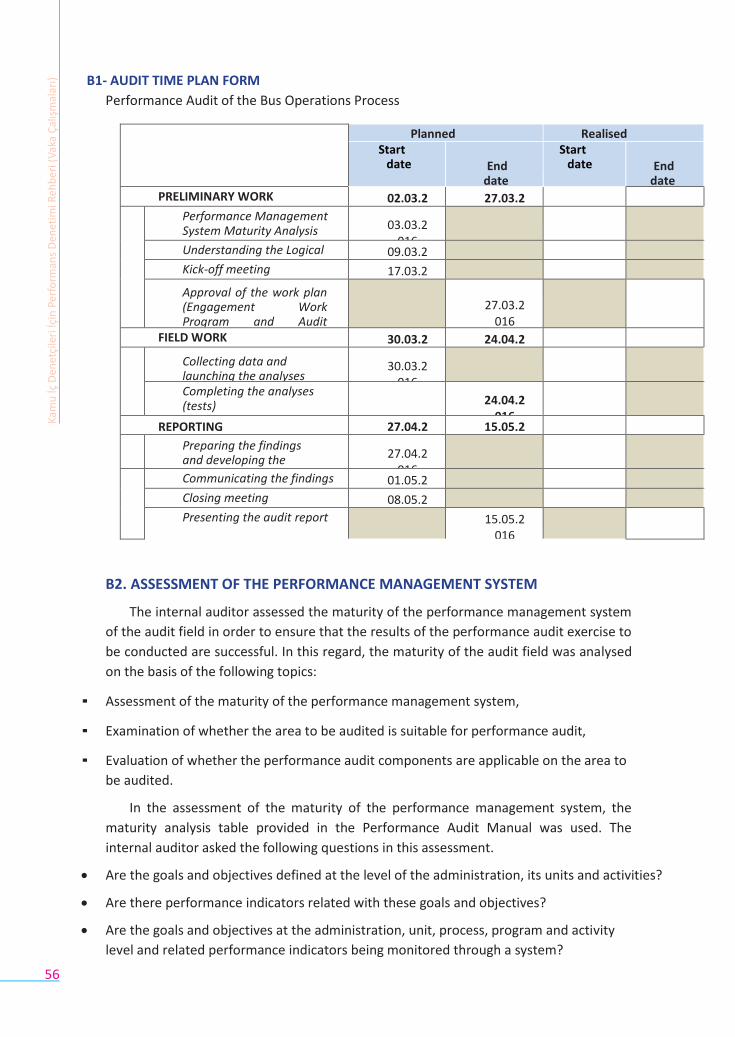

B1. AUDIT TIME PLAN FORM

Performance Audit of the Library Process

Planned Realised

Start date

End

date

Start

date

End date

PRELIMINARY WORK 02.03.2016 27.03.2016

Performance Management System Maturity Analysis

03.03.2016

Understanding the Logical Framework

09.03.2016

Kick-off meeting 17.03.2016

Approval of the work plan (Engagement Work Program and Audit Matrix)

27.03.2016

FIELD WORK 30.03.2016 24.04.2016

Collecting data and launching the analyses (tests)

30.03.2016

Completing the analyses (tests) 24.04.2016

REPORTING 27.04.2016 15.05.2016

Preparing the findings and developing the recommendation

27.04.2016

Communicating the findings 01.05.2016

Closing meeting 08.05.2016

Presenting the audit report 15.05.2016

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

13

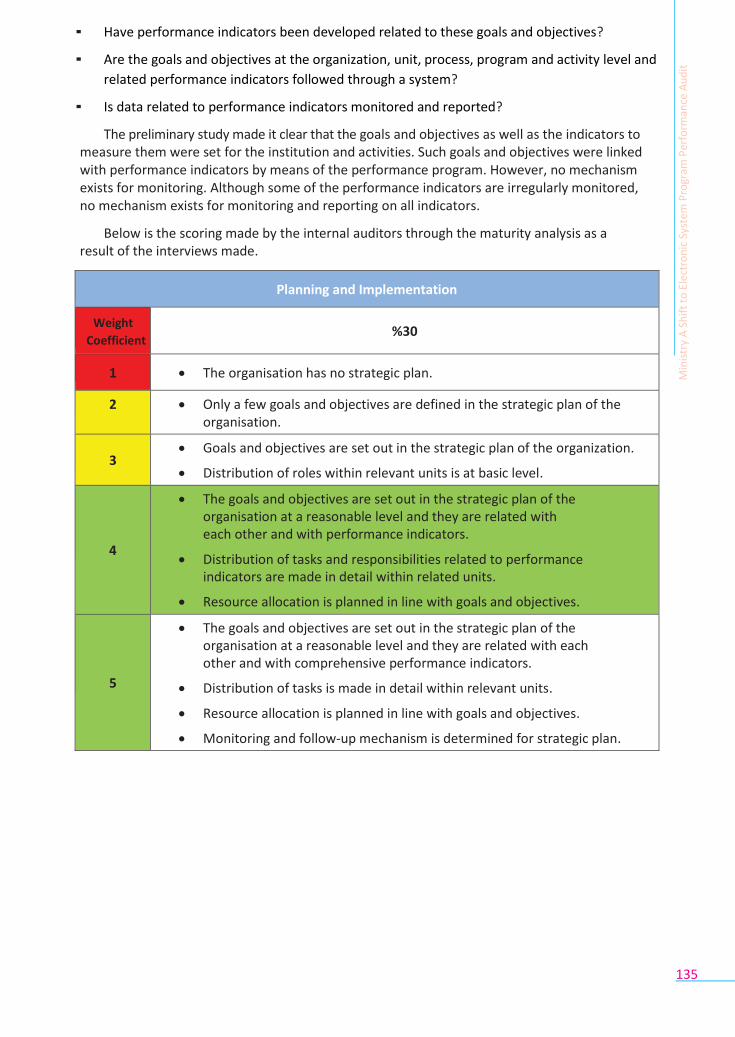

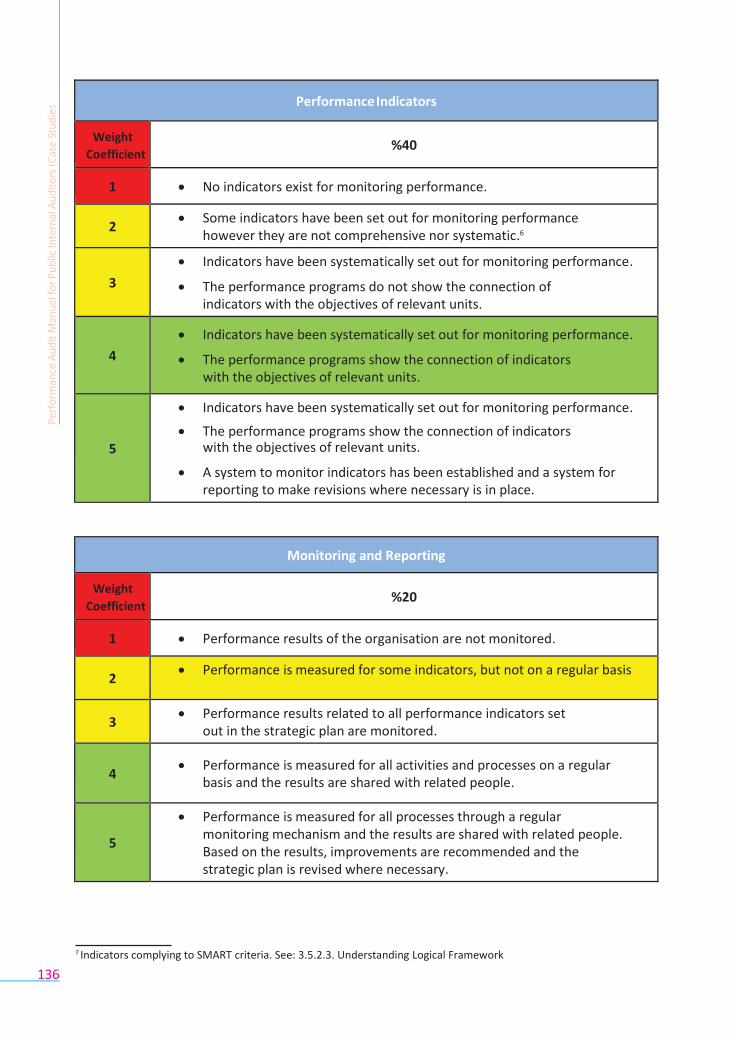

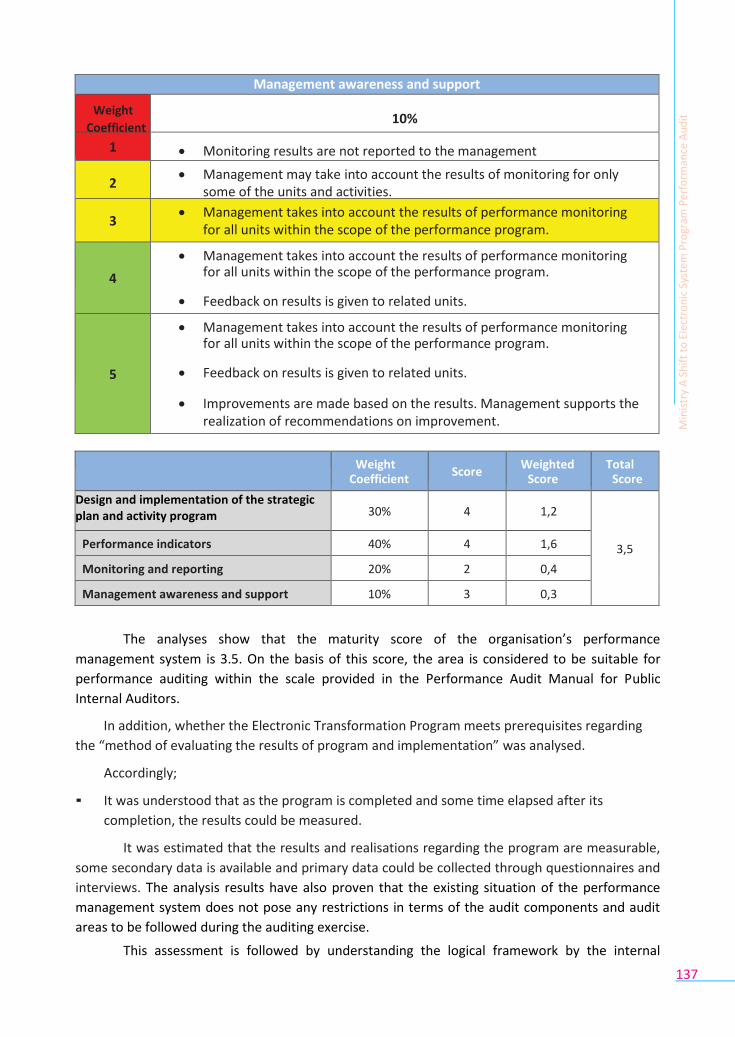

B2. ASSESSMENT OF THE PERFORMANCE MANAGEMENT SYSTEM

The internal auditor assessed the maturity of the performance management system of the

audit field in order to ensure that the results of the performance audit exercise to be conducted

are successful. In this regard, the maturity of the audit field was analysed on the basis of the

following topics:

▪ Assessment of the maturity of the performance management system,

▪ Examination of whether the area to be audited is suitable for performance audit,

▪ Evaluation of whether the performance audit components are applicable on the area to

be audited.

In the assessment of the maturity of the performance management system, the maturity

analysis table provided in the Performance Audit Manual was used. The internal auditor asked the

following questions in this assessment.

Have the goals and objectives been defined at the level of the administration, its units and activities?

Have performance indicators been developed related to these goals and objectives?

Are the goals and objectives at the administration, unit, process, program and activity

level and related performance indicators followed through a system?

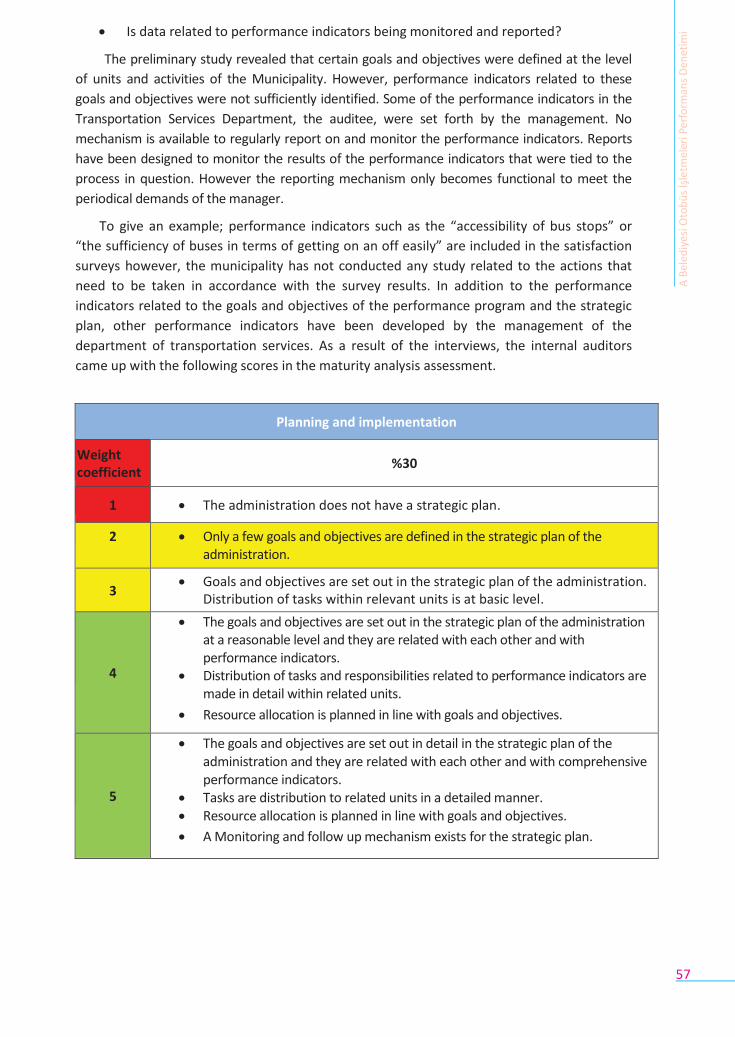

Is data related to performance indicators monitored and reported?

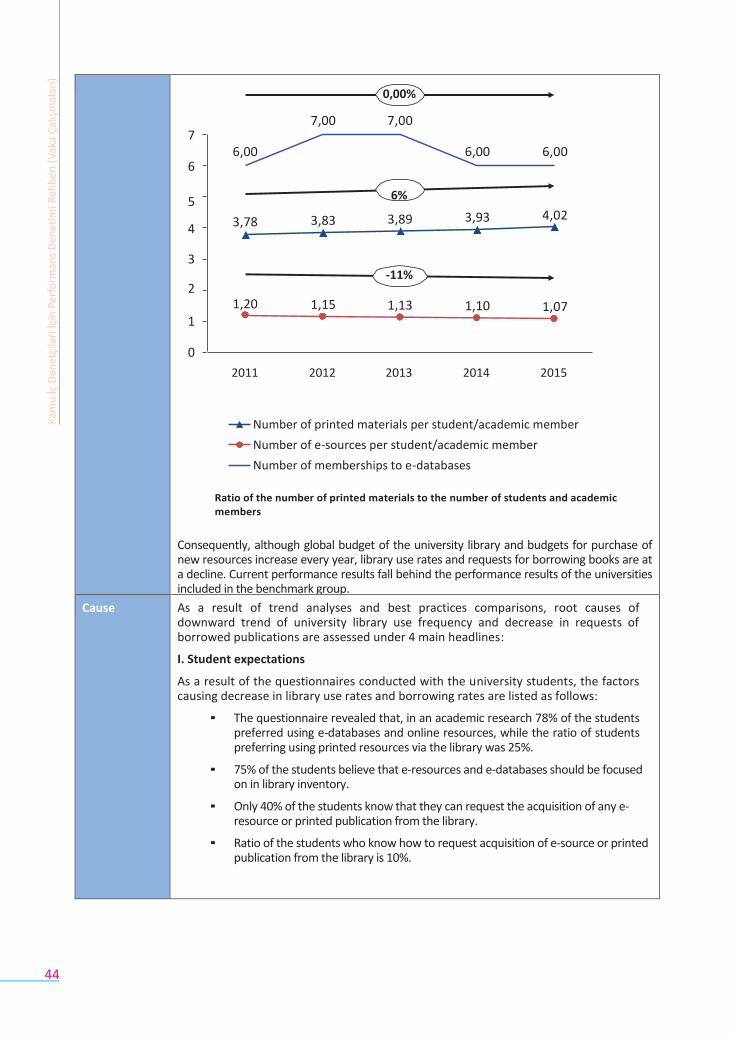

The preliminary study revealed that goals and objectives were defined at the level of units and activities of the University. Also, the goals and objectives of the library unit were described in the performance program. These goals and objectives were related with performance indicators. To monitor the performance indicators in a systematic manner, a software called “performance management system” is used. Some of the performance indicators are monitored through this program, which, however, lacks the necessary capacity to report on all performance indicators. The management attaches importance to this program and plans to make necessary investments for its further improvement.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

14

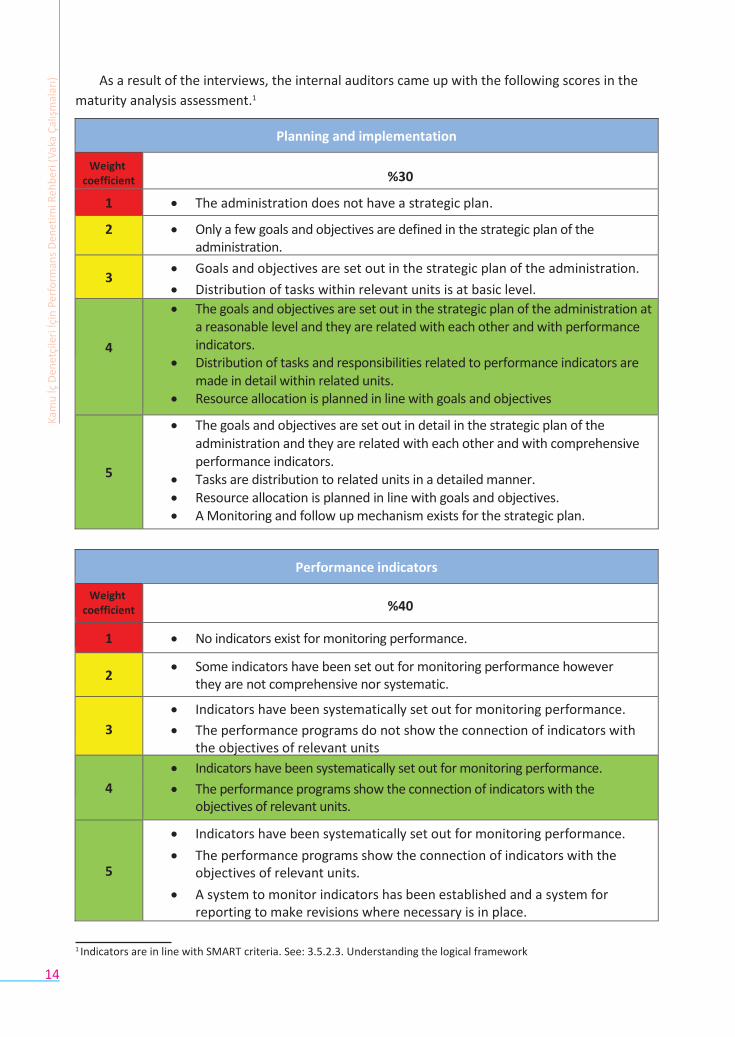

As a result of the interviews, the internal auditors came up with the following scores in the

maturity analysis assessment.1

Planning and implementation

Weight coefficient

%30

1 The administration does not have a strategic plan.

2 Only a few goals and objectives are defined in the strategic plan of the administration.

3 Goals and objectives are set out in the strategic plan of the administration.

Distribution of tasks within relevant units is at basic level.

4

The goals and objectives are set out in the strategic plan of the administration at a reasonable level and they are related with each other and with performance indicators.

Distribution of tasks and responsibilities related to performance indicators are made in detail within related units.

Resource allocation is planned in line with goals and objectives

5

The goals and objectives are set out in detail in the strategic plan of the administration and they are related with each other and with comprehensive performance indicators.

Tasks are distribution to related units in a detailed manner. Resource allocation is planned in line with goals and objectives. A Monitoring and follow up mechanism exists for the strategic plan.

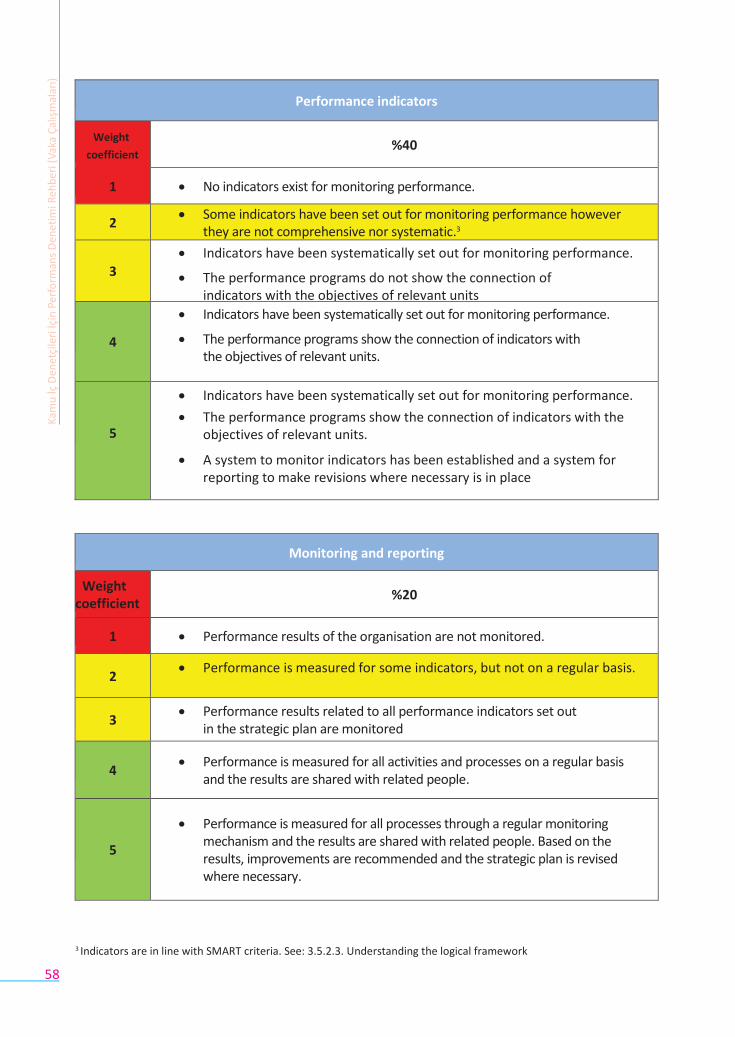

Performance indicators

Weight coefficient %40

1 No indicators exist for monitoring performance.

2 Some indicators have been set out for monitoring performance however

they are not comprehensive nor systematic.

3

Indicators have been systematically set out for monitoring performance.

The performance programs do not show the connection of indicators with the objectives of relevant units

4

Indicators have been systematically set out for monitoring performance.

The performance programs show the connection of indicators with the objectives of relevant units.

5

Indicators have been systematically set out for monitoring performance.

The performance programs show the connection of indicators with the objectives of relevant units.

A system to monitor indicators has been established and a system for reporting to make revisions where necessary is in place.

1 Indicators are in line with SMART criteria. See: 3.5.2.3. Understanding the logical framework

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

15

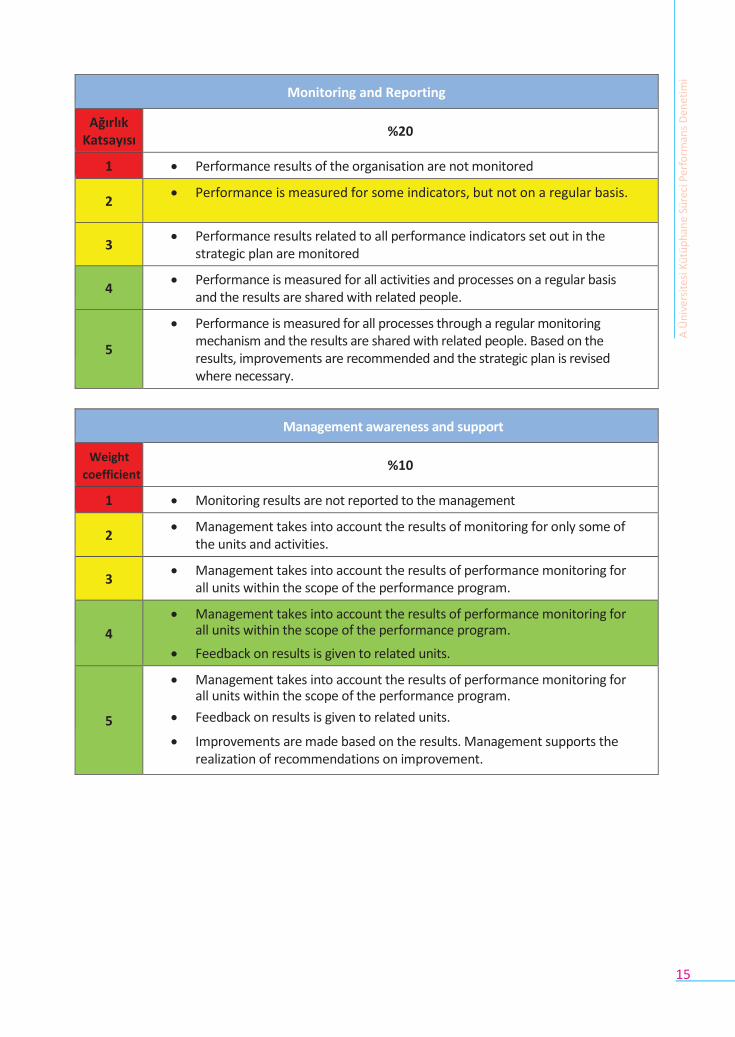

Monitoring and Reporting

Ağırlık Katsayısı

%20

1 Performance results of the organisation are not monitored

2 Performance is measured for some indicators, but not on a regular basis.

3 Performance results related to all performance indicators set out in the

strategic plan are monitored

4 Performance is measured for all activities and processes on a regular basis

and the results are shared with related people.

5

Performance is measured for all processes through a regular monitoring mechanism and the results are shared with related people. Based on the results, improvements are recommended and the strategic plan is revised where necessary.

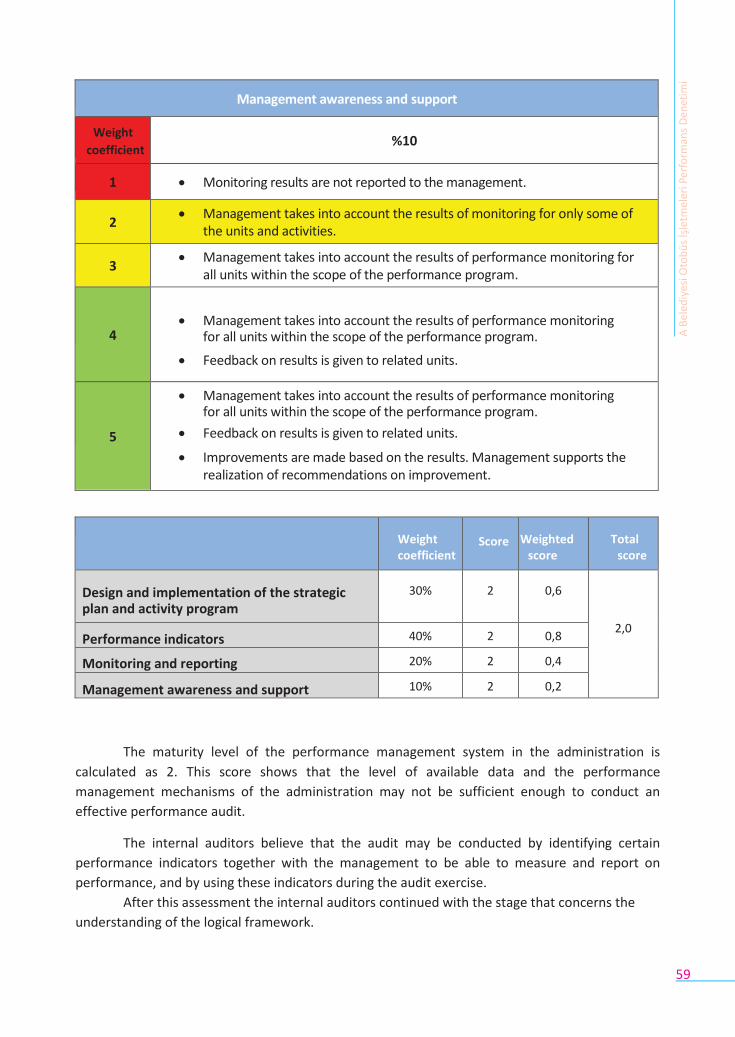

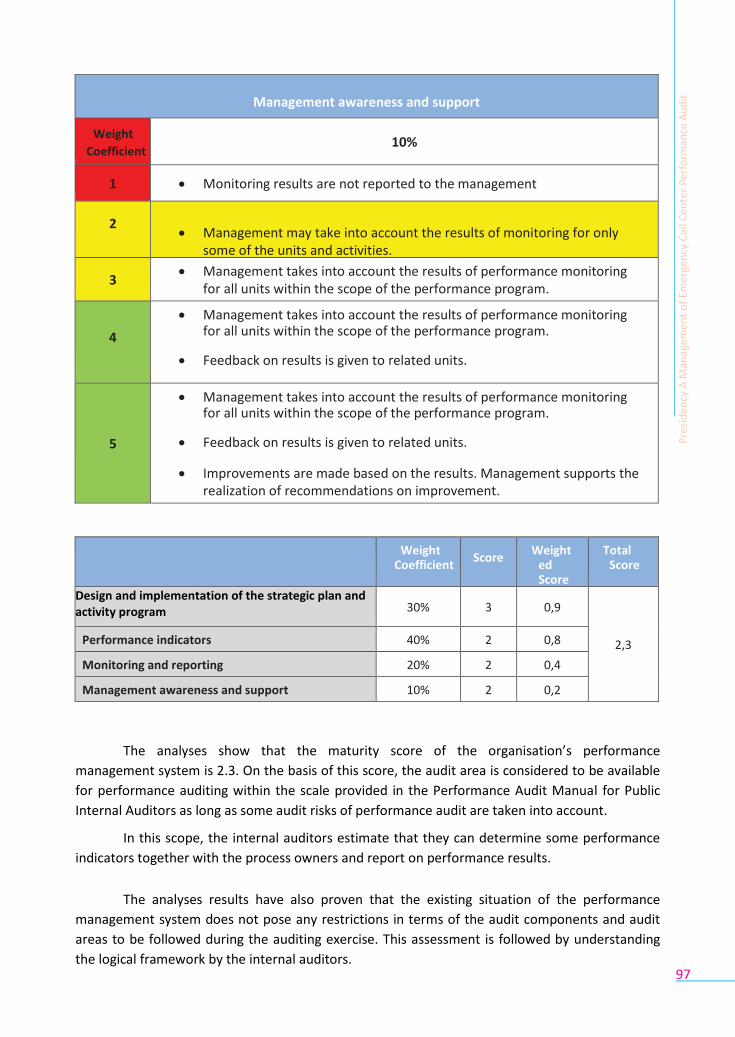

Management awareness and support

Weight

coefficient %10

1 Monitoring results are not reported to the management

2 Management takes into account the results of monitoring for only some of

the units and activities.

3 Management takes into account the results of performance monitoring for

all units within the scope of the performance program.

4

Management takes into account the results of performance monitoring for all units within the scope of the performance program.

Feedback on results is given to related units.

5

Management takes into account the results of performance monitoring for all units within the scope of the performance program.

Feedback on results is given to related units.

Improvements are made based on the results. Management supports the realization of recommendations on improvement.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

16

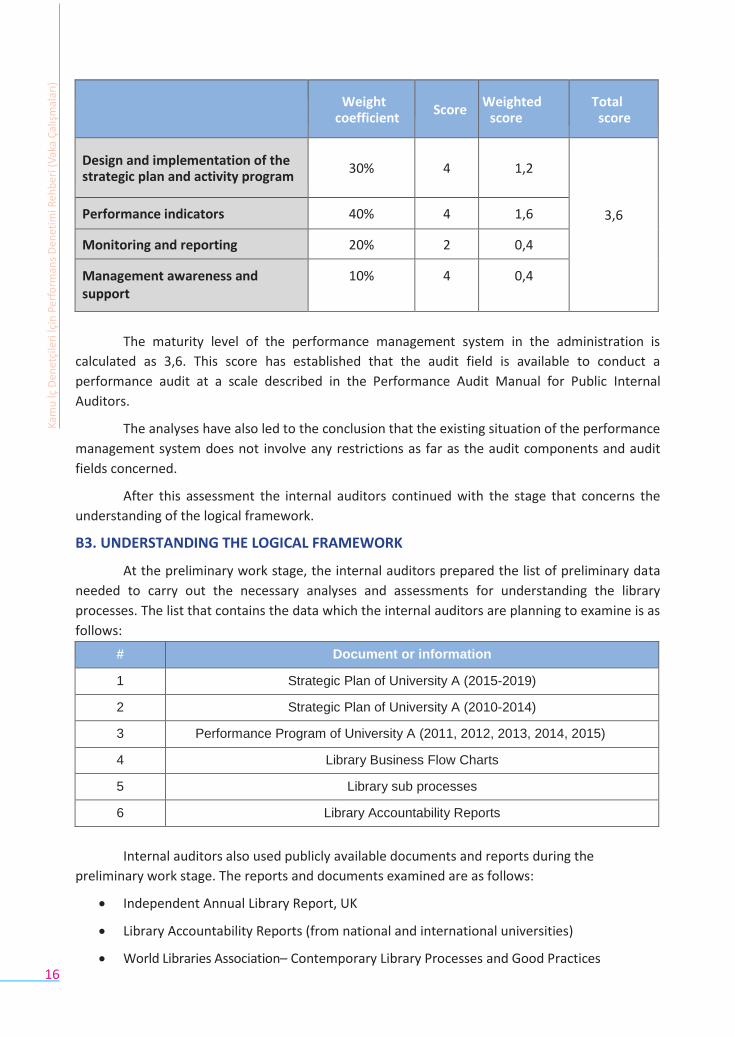

Weight

coefficient

Score

Weighted score

Total score

Design and implementation of the strategic plan and activity program

30%

4

1,2

3,6 Performance indicators 40% 4 1,6

Monitoring and reporting 20% 2 0,4

Management awareness and support

10% 4 0,4

The maturity level of the performance management system in the administration is

calculated as 3,6. This score has established that the audit field is available to conduct a

performance audit at a scale described in the Performance Audit Manual for Public Internal

Auditors.

The analyses have also led to the conclusion that the existing situation of the performance

management system does not involve any restrictions as far as the audit components and audit

fields concerned.

After this assessment the internal auditors continued with the stage that concerns the

understanding of the logical framework.

B3. UNDERSTANDING THE LOGICAL FRAMEWORK

At the preliminary work stage, the internal auditors prepared the list of preliminary data

needed to carry out the necessary analyses and assessments for understanding the library

processes. The list that contains the data which the internal auditors are planning to examine is as

follows:

# Document or information

1 Strategic Plan of University A (2015-2019)

2 Strategic Plan of University A (2010-2014)

3 Performance Program of University A (2011, 2012, 2013, 2014, 2015)

4 Library Business Flow Charts

5 Library sub processes

6 Library Accountability Reports

Internal auditors also used publicly available documents and reports during the

preliminary work stage. The reports and documents examined are as follows:

Independent Annual Library Report, UK

Library Accountability Reports (from national and international universities)

World Libraries Association– Contemporary Library Processes and Good Practices

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

17

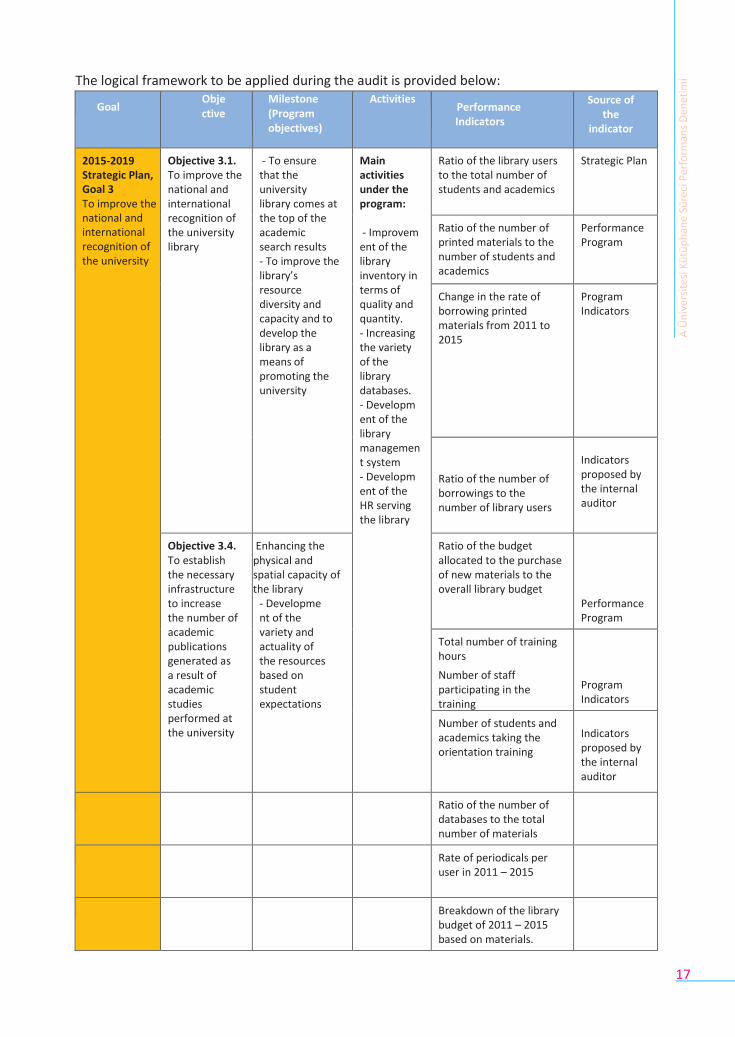

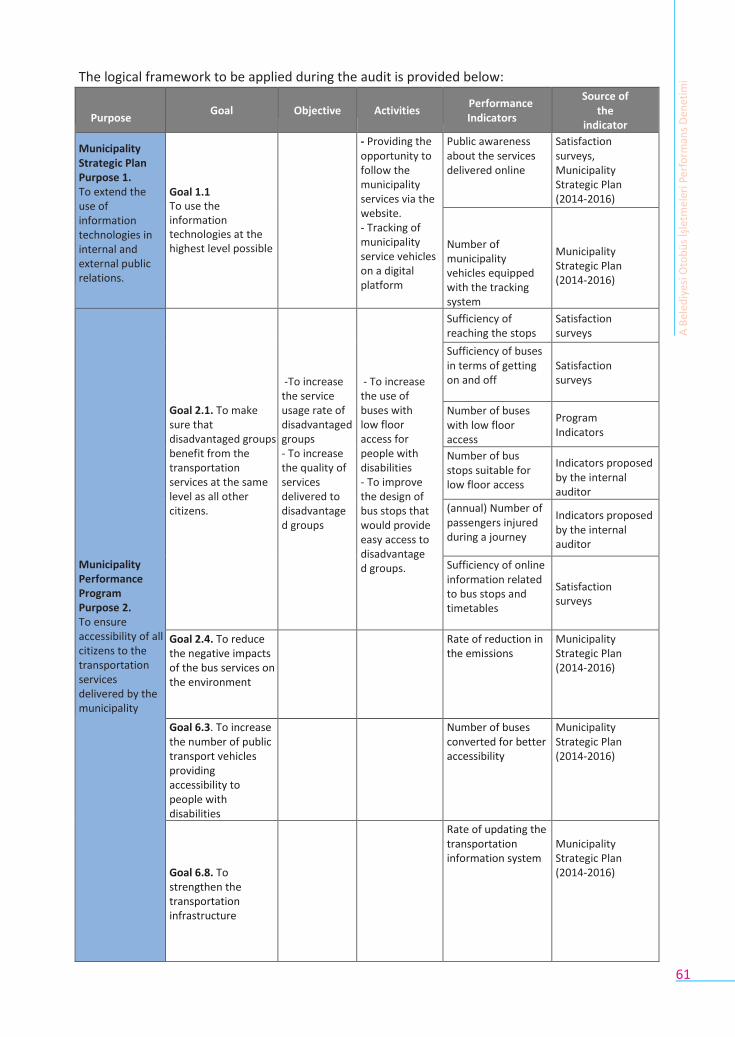

The logical framework to be applied during the audit is provided below:

Goal Objective

Milestone (Program objectives)

Activities Performance Indicators

Source of the

indicator

2015-2019 Strategic Plan, Goal 3 To improve the national and international recognition of the university

Objective 3.1. To improve the national and international recognition of the university library

- To ensure that the university library comes at the top of the academic search results - To improve the library’s resource diversity and capacity and to develop the library as a means of promoting the university

Main activities under the program:

- Improvement of the library inventory in terms of quality and quantity. - Increasing the variety of the library databases. - Development of the library management system - Development of the HR serving the library

Ratio of the library users to the total number of students and academics

Strategic Plan

Ratio of the number of printed materials to the number of students and academics

Performance Program

Change in the rate of borrowing printed materials from 2011 to 2015

Program Indicators

Ratio of the number of borrowings to the number of library users

Indicators proposed by the internal auditor

Objective 3.4. To establish the necessary infrastructure to increase the number of academic publications generated as a result of academic studies performed at the university

Enhancing the physical and spatial capacity of the library

- Development of the variety and actuality of the resources based on student expectations

Ratio of the budget allocated to the purchase of new materials to the overall library budget

Performance Program

Total number of training hours

Number of staff participating in the training

Program Indicators

Number of students and academics taking the orientation training

Indicators proposed by the internal auditor

Ratio of the number of databases to the total number of materials

Rate of periodicals per user in 2011 – 2015

Breakdown of the library budget of 2011 – 2015 based on materials.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

18

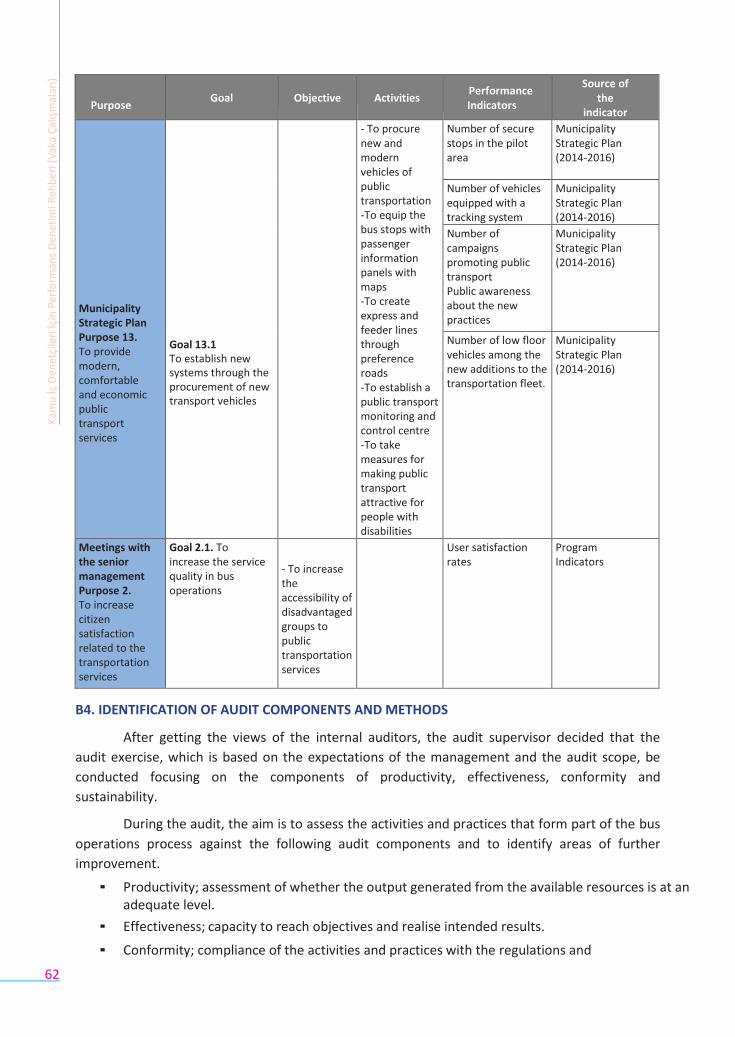

B4. IDENTIFICATION OF AUDIT COMPONENTS AND METHODS

After getting the views of the internal auditors, the audit supervisor decided that the

audit exercise, which is based on the expectations of the management and the audit scope, be

conducted focusing on the components of productivity, effectiveness, consistency and

conformity.

During the audit, the aim is to assess the activities and practices that form part of the library

processes against the following audit components and to identify areas of further improvement:

Productivity; assessment of whether the output generated from the available resources is

at an adequate level.

Effectiveness; capacity to reach objectives and realise intended results

Consistency; coherence between the defined goals, objectives and strategies of public

administrations and the planning and design of their programs and projects

Conformity; compliance of the activities and practices with the regulations and

procedures in force and adequacy of the institutional capacity for implementation

The methods that are planned to be applied in auditing the abovementioned components are

benchmarking and measuring and reporting on performance.

The benchmarking analysis will focus on:

the performance trends of the library from 2011 to 2015

performance of the library as compared to the libraries of national and international university libraries.

B5. KICK OFF MEETING

During the kick-off meeting, the internal auditor informed the auditee on the following topics:

audit team and its organisation

audit scope

stages of the audit

time schedule

identification of the comparison group

next steps

During the kick-off meeting, the auditee expressed its expectations as follows:

international university libraries are also used as a benchmark as part of the analysis on

the library activities

universities without a faculty of medicine are included in the comparison group

human resources and physical/spatial conditions of the library are taken into account

during the assessment.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

19

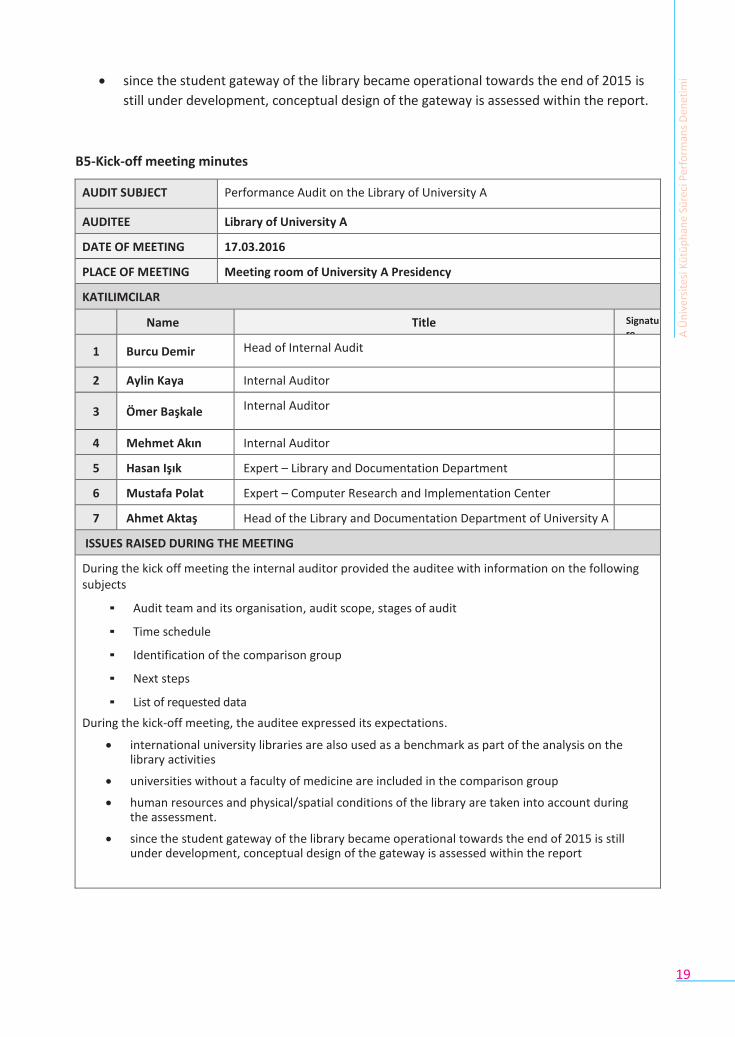

since the student gateway of the library became operational towards the end of 2015 is

still under development, conceptual design of the gateway is assessed within the report.

B5-Kick-off meeting minutes

AUDIT SUBJECT Performance Audit on the Library of University A

AUDITEE Library of University A

DATE OF MEETING 17.03.2016

PLACE OF MEETING Meeting room of University A Presidency

KATILIMCILAR

Name Title Signature

1 Burcu Demir Head of Internal Audit

2 Aylin Kaya Internal Auditor

3 Ömer Başkale Internal Auditor

4 Mehmet Akın Internal Auditor

5 Hasan Işık Expert – Library and Documentation Department

6 Mustafa Polat Expert – Computer Research and Implementation Center

7 Ahmet Aktaş Head of the Library and Documentation Department of University A

ISSUES RAISED DURING THE MEETING

During the kick off meeting the internal auditor provided the auditee with information on the following subjects

▪ Audit team and its organisation, audit scope, stages of audit

▪ Time schedule

▪ Identification of the comparison group

▪ Next steps

▪ List of requested data

During the kick-off meeting, the auditee expressed its expectations.

international university libraries are also used as a benchmark as part of the analysis on the library activities

universities without a faculty of medicine are included in the comparison group

human resources and physical/spatial conditions of the library are taken into account during the assessment.

since the student gateway of the library became operational towards the end of 2015 is still under development, conceptual design of the gateway is assessed within the report

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

21

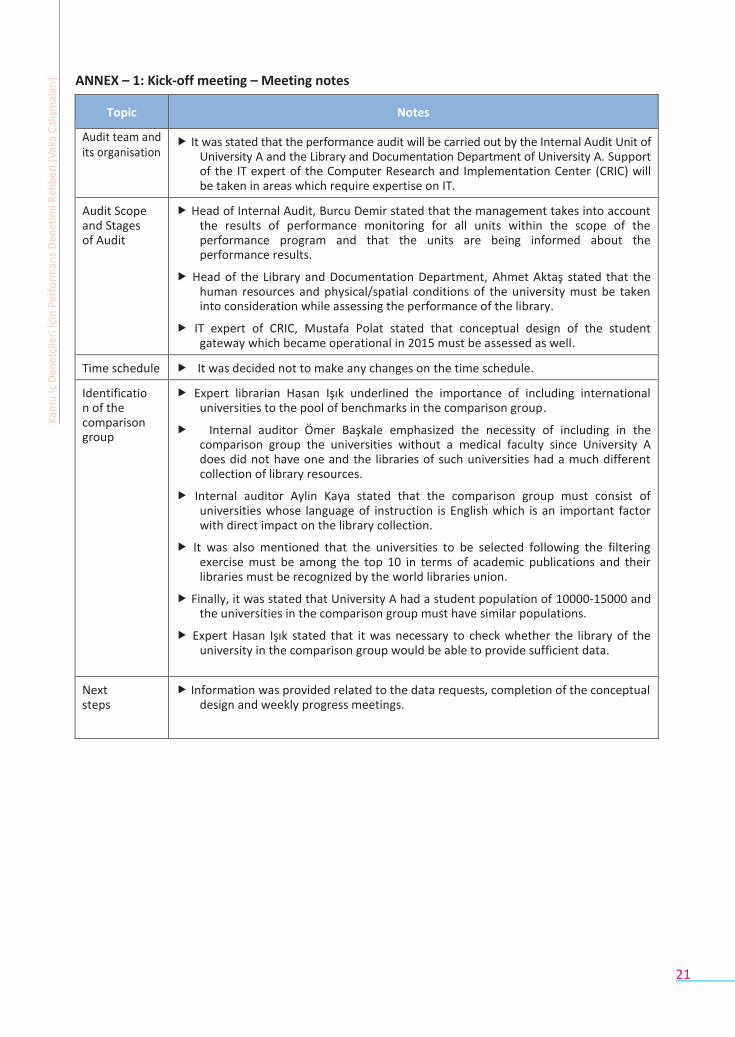

ANNEX – 1: Kick-off meeting – Meeting notes

Topic Notes

Audit team and its organisation

It was stated that the performance audit will be carried out by the Internal Audit Unit of University A and the Library and Documentation Department of University A. Support of the IT expert of the Computer Research and Implementation Center (CRIC) will be taken in areas which require expertise on IT.

Audit Scope and Stages of Audit

Head of Internal Audit, Burcu Demir stated that the management takes into account the results of performance monitoring for all units within the scope of the performance program and that the units are being informed about the performance results.

Head of the Library and Documentation Department, Ahmet Aktaş stated that the human resources and physical/spatial conditions of the university must be taken into consideration while assessing the performance of the library.

IT expert of CRIC, Mustafa Polat stated that conceptual design of the student gateway which became operational in 2015 must be assessed as well.

Time schedule It was decided not to make any changes on the time schedule.

Identification of the comparison group

Expert librarian Hasan Işık underlined the importance of including international universities to the pool of benchmarks in the comparison group.

Internal auditor Ömer Başkale emphasized the necessity of including in the comparison group the universities without a medical faculty since University A does did not have one and the libraries of such universities had a much different collection of library resources.

Internal auditor Aylin Kaya stated that the comparison group must consist of universities whose language of instruction is English which is an important factor with direct impact on the library collection.

It was also mentioned that the universities to be selected following the filtering exercise must be among the top 10 in terms of academic publications and their libraries must be recognized by the world libraries union.

Finally, it was stated that University A had a student population of 10000-15000 and the universities in the comparison group must have similar populations.

Expert Hasan Işık stated that it was necessary to check whether the library of the university in the comparison group would be able to provide sufficient data.

Next steps

Information was provided related to the data requests, completion of the conceptual design and weekly progress meetings.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

20

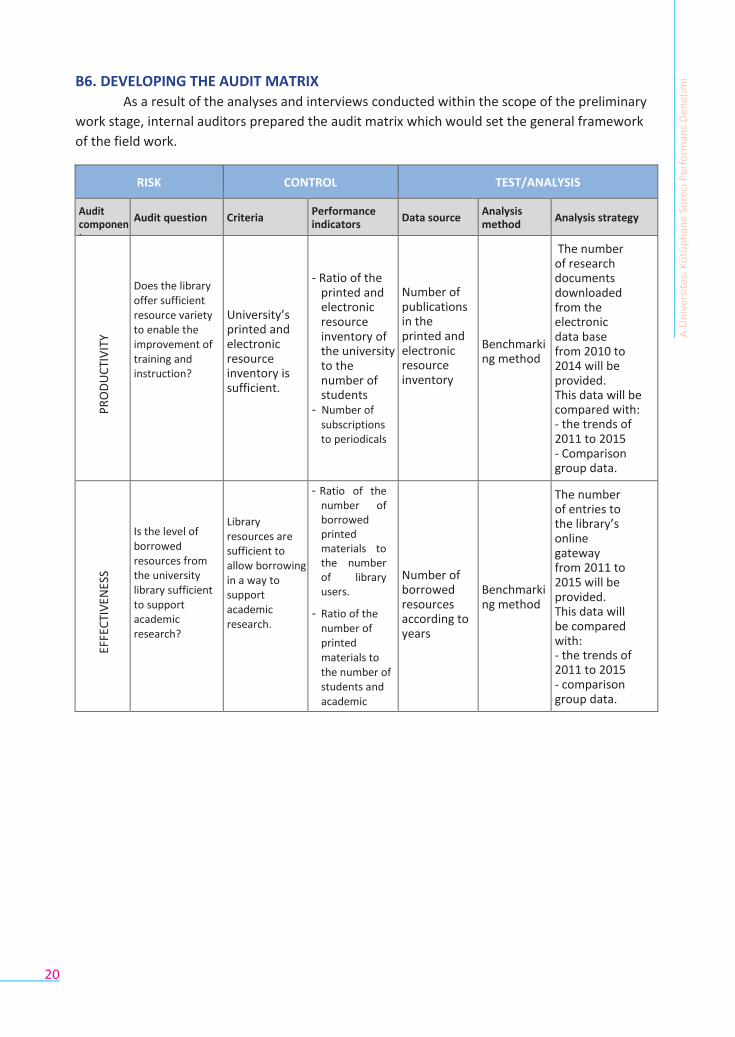

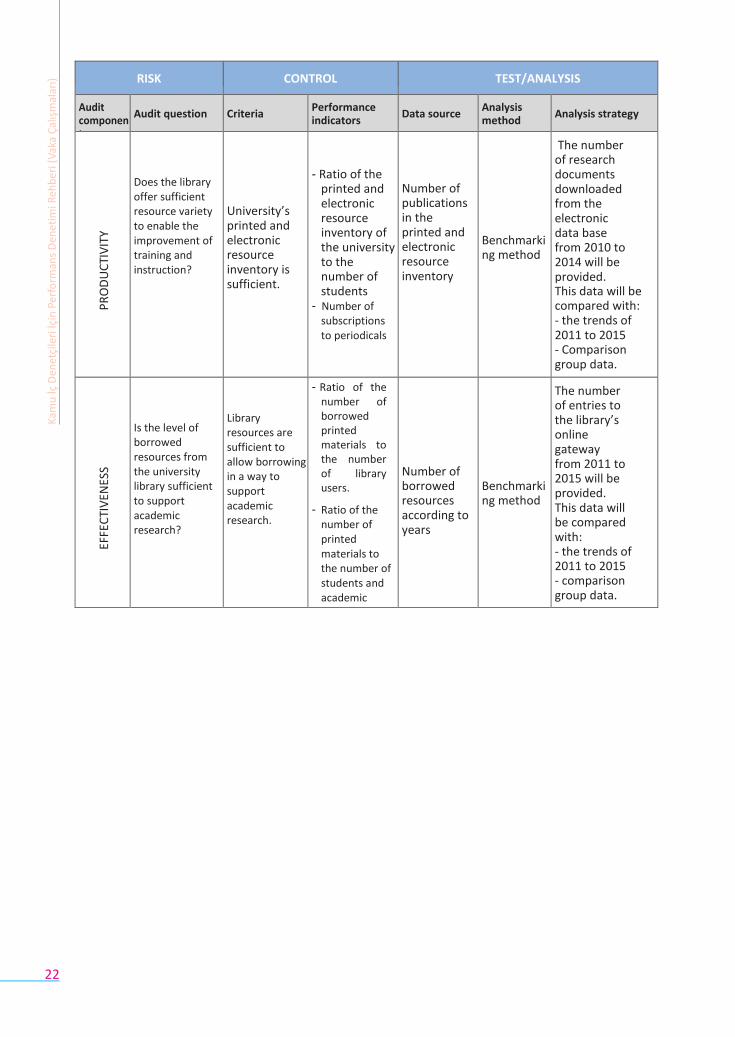

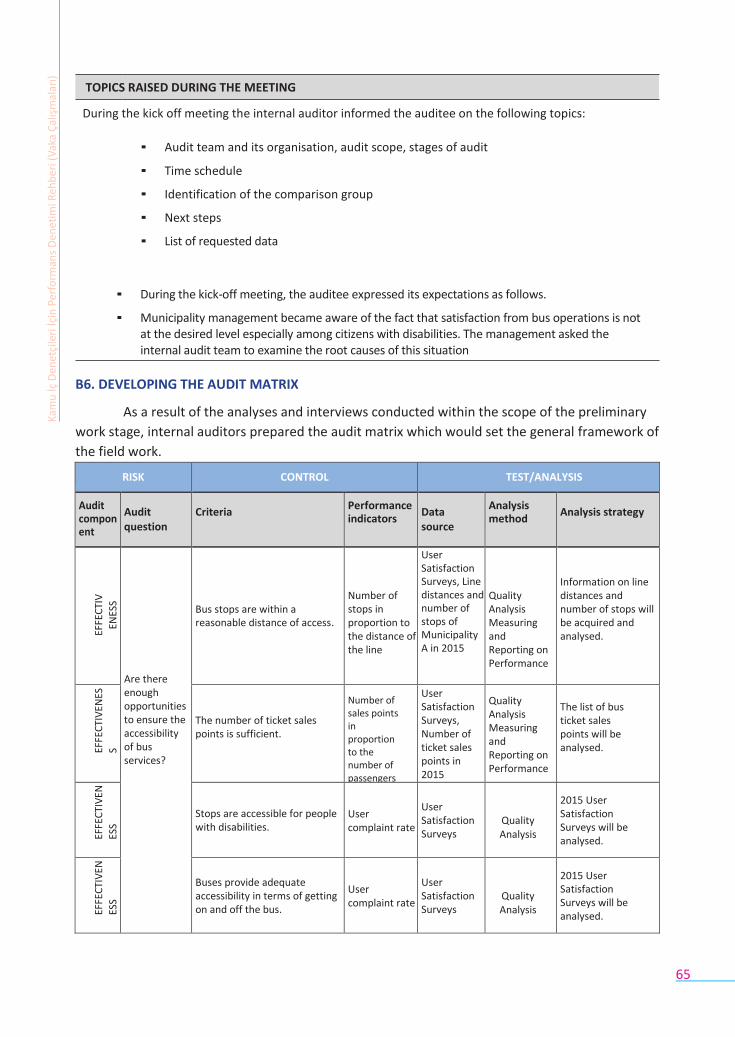

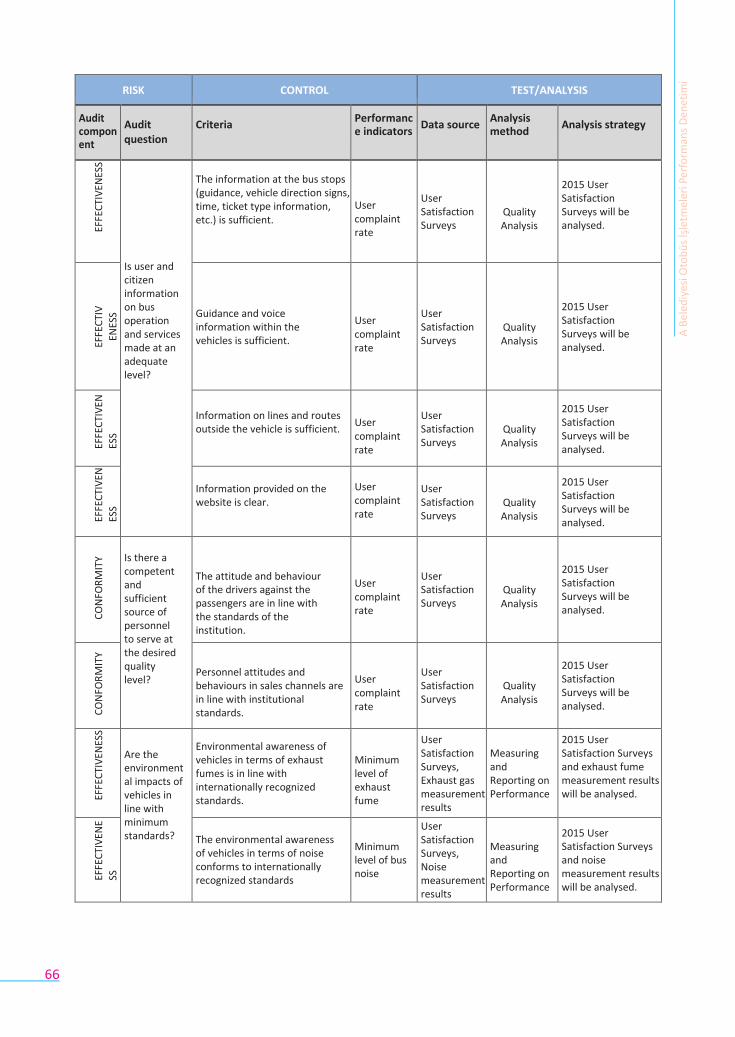

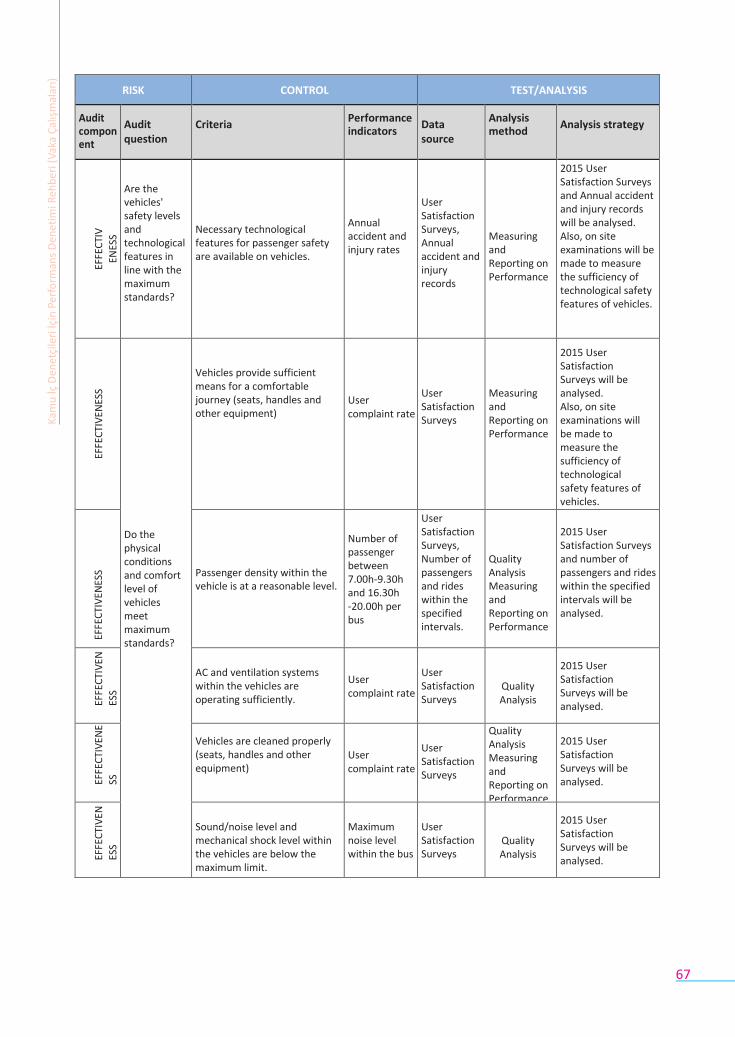

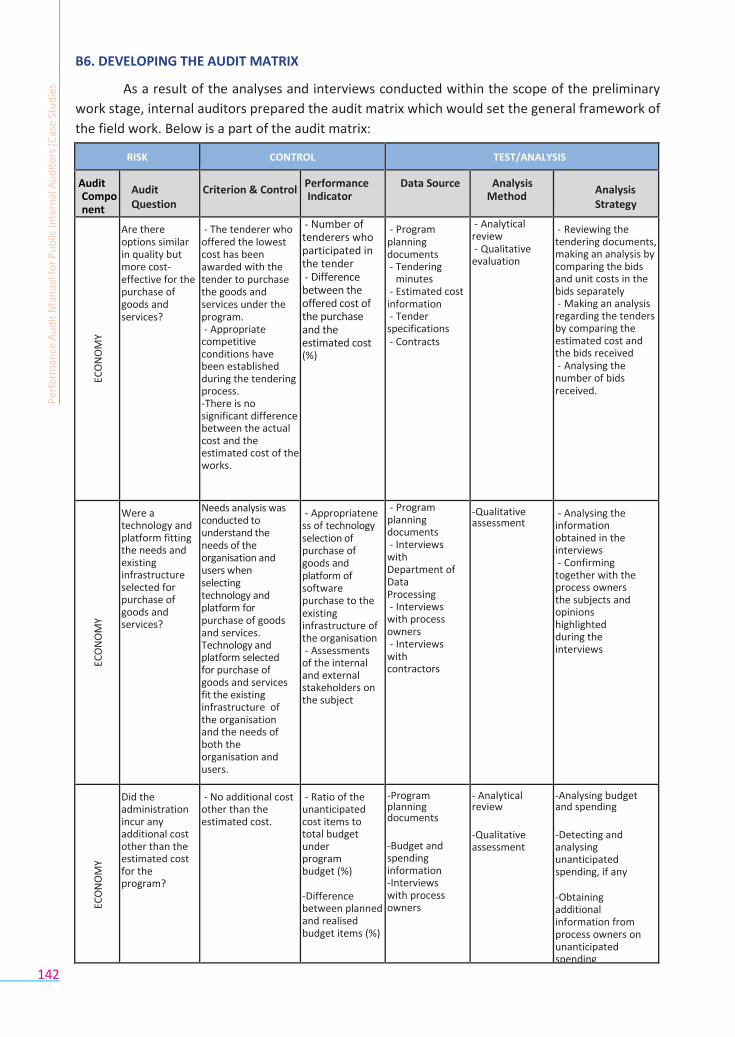

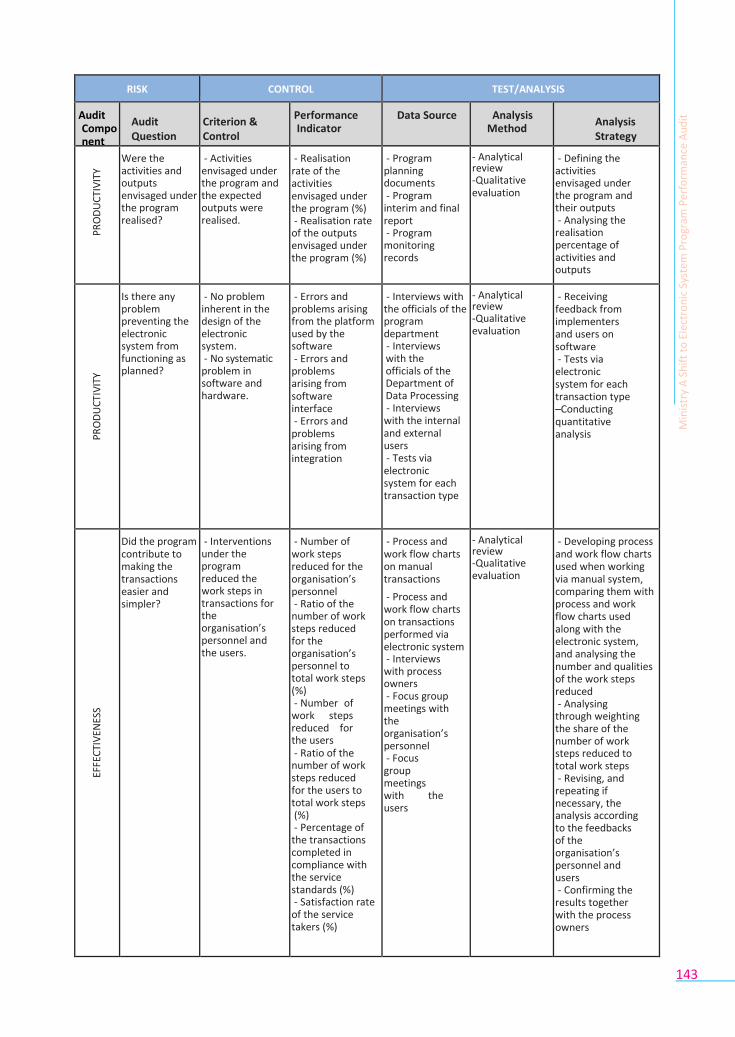

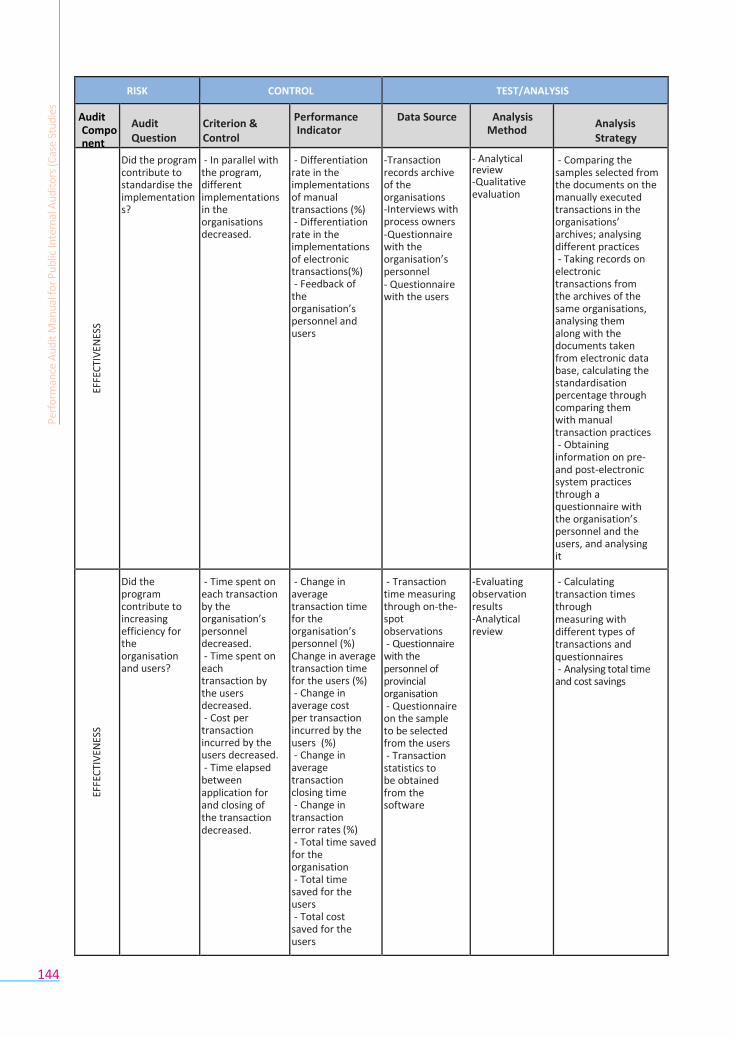

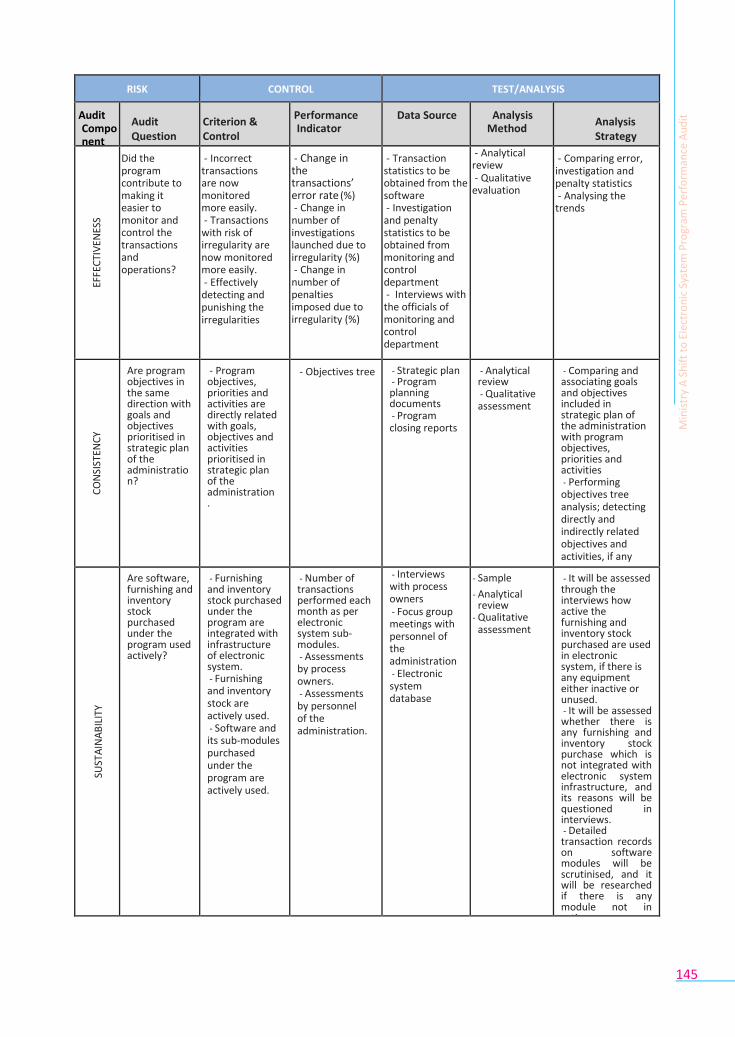

B6. DEVELOPING THE AUDIT MATRIX As a result of the analyses and interviews conducted within the scope of the preliminary

work stage, internal auditors prepared the audit matrix which would set the general framework

of the field work.

RISK CONTROL TEST/ANALYSIS

Audit component

Audit question

Criteria Performance indicators

Data source Analysis method

Analysis strategy

PR

OD

UC

TIV

ITY

Does the library offer sufficient resource variety to enable the improvement of training and instruction?

University’s printed and electronic resource inventory is sufficient.

- Ratio of the

printed and electronic resource inventory of the university to the number of students

- Number of subscriptions to periodicals

Number of publications in the printed and electronic resource inventory

Benchmarking method

The number of research documents downloaded from the electronic data base from 2010 to 2014 will be provided. This data will be compared with: - the trends of 2011 to 2015 - Comparison group data.

E

FFEC

TIV

ENES

S

Is the level of borrowed resources from the university library sufficient to support academic research?

Library resources are sufficient to allow borrowing in a way to support academic research.

- Ratio of the number of borrowed printed materials to the number of library users.

- Ratio of the number of printed materials to the number of students and academic staff.

Number of borrowed resources according to years

Benchmarking method

The number of entries to the library’s online gateway from 2011 to 2015 will be provided. This data will be compared with: - the trends of 2011 to 2015 - comparison group data.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

22

RISK CONTROL TEST/ANALYSIS

Audit component

Audit question

Criteria Performance indicators

Data source Analysis method

Analysis strategy

PR

OD

UC

TIV

ITY

Does the library offer sufficient resource variety to enable the improvement of training and instruction?

University’s printed and electronic resource inventory is sufficient.

- Ratio of the

printed and electronic resource inventory of the university to the number of students

- Number of subscriptions to periodicals

Number of publications in the printed and electronic resource inventory

Benchmarking method

The number of research documents downloaded from the electronic data base from 2010 to 2014 will be provided. This data will be compared with: - the trends of 2011 to 2015 - Comparison group data.

E

FFEC

TIV

ENES

S

Is the level of borrowed resources from the university library sufficient to support academic research?

Library resources are sufficient to allow borrowing in a way to support academic research.

- Ratio of the number of borrowed printed materials to the number of library users.

- Ratio of the number of printed materials to the number of students and academic staff.

Number of borrowed resources according to years

Benchmarking method

The number of entries to the library’s online gateway from 2011 to 2015 will be provided. This data will be compared with: - the trends of 2011 to 2015 - comparison group data.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

23

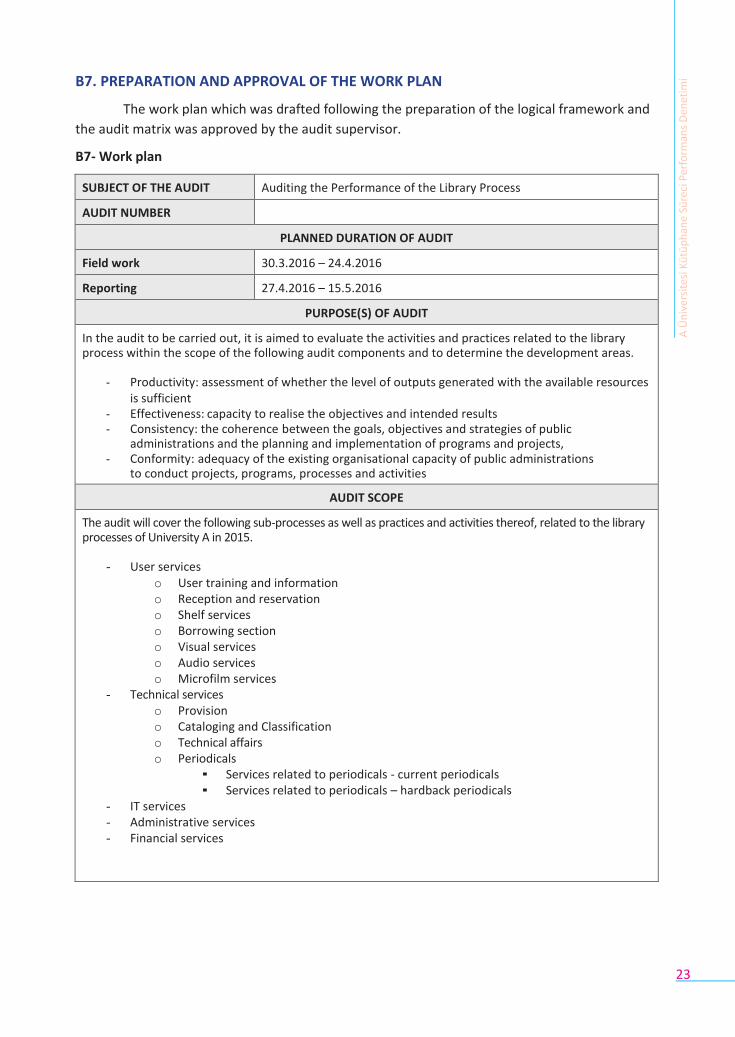

B7. PREPARATION AND APPROVAL OF THE WORK PLAN

The work plan which was drafted following the preparation of the logical framework and

the audit matrix was approved by the audit supervisor.

B7- Work plan

SUBJECT OF THE AUDIT Auditing the Performance of the Library Process

AUDIT NUMBER

PLANNED DURATION OF AUDIT

Field work 30.3.2016 – 24.4.2016

Reporting 27.4.2016 – 15.5.2016

PURPOSE(S) OF AUDIT

In the audit to be carried out, it is aimed to evaluate the activities and practices related to the library process within the scope of the following audit components and to determine the development areas.

- Productivity: assessment of whether the level of outputs generated with the available resources is sufficient

- Effectiveness: capacity to realise the objectives and intended results - Consistency: the coherence between the goals, objectives and strategies of public

administrations and the planning and implementation of programs and projects, - Conformity: adequacy of the existing organisational capacity of public administrations

to conduct projects, programs, processes and activities

AUDIT SCOPE

The audit will cover the following sub-processes as well as practices and activities thereof, related to the library processes of University A in 2015.

- User services o User training and information o Reception and reservation o Shelf services o Borrowing section o Visual services o Audio services o Microfilm services

- Technical services o Provision o Cataloging and Classification o Technical affairs o Periodicals

▪ Services related to periodicals - current periodicals ▪ Services related to periodicals – hardback periodicals

- IT services - Administrative services - Financial services

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

24

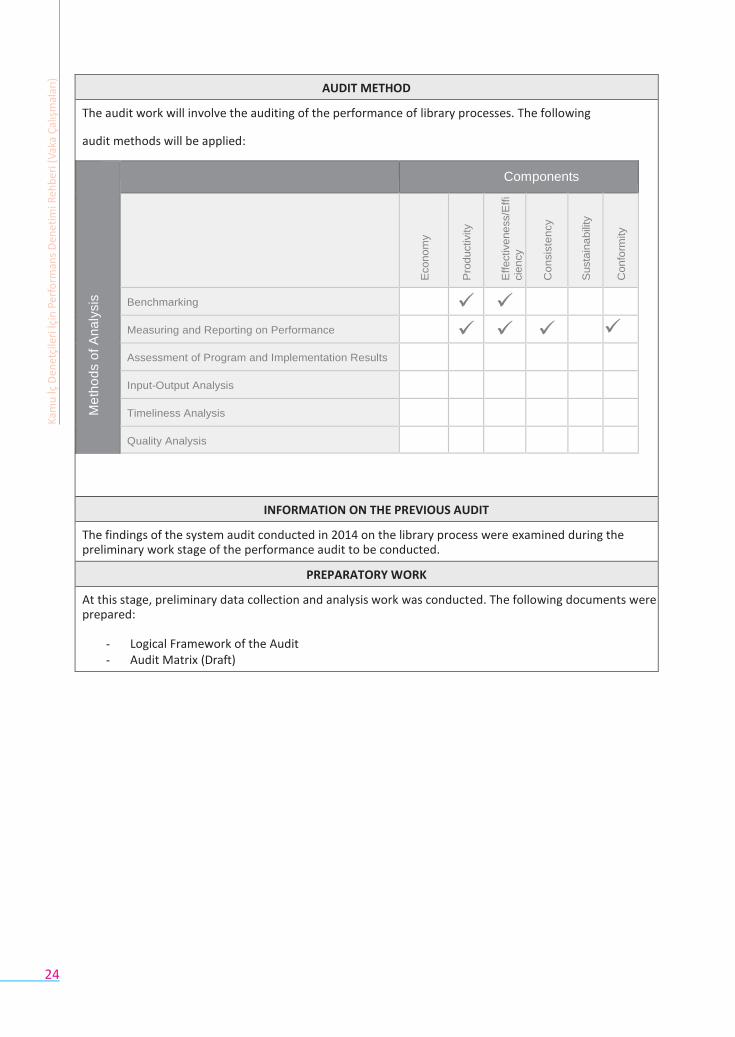

AUDIT METHOD

The audit work will involve the auditing of the performance of library processes. The following

audit methods will be applied:

Me

tho

ds o

f A

na

lysis

Components

Econom

y

Pro

ductivity

E

ffectivene

ss/E

ffi

cie

ncy

C

on

sis

ten

cy

Susta

ina

bili

ty

Confo

rmity

Benchmarking

Measuring and Reporting on Performance

Assessment of Program and Implementation Results

Input-Output Analysis

Timeliness Analysis

Quality Analysis

INFORMATION ON THE PREVIOUS AUDIT

The findings of the system audit conducted in 2014 on the library process were examined during the preliminary work stage of the performance audit to be conducted.

PREPARATORY WORK

At this stage, preliminary data collection and analysis work was conducted. The following documents were prepared:

- Logical Framework of the Audit - Audit Matrix (Draft)

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

25

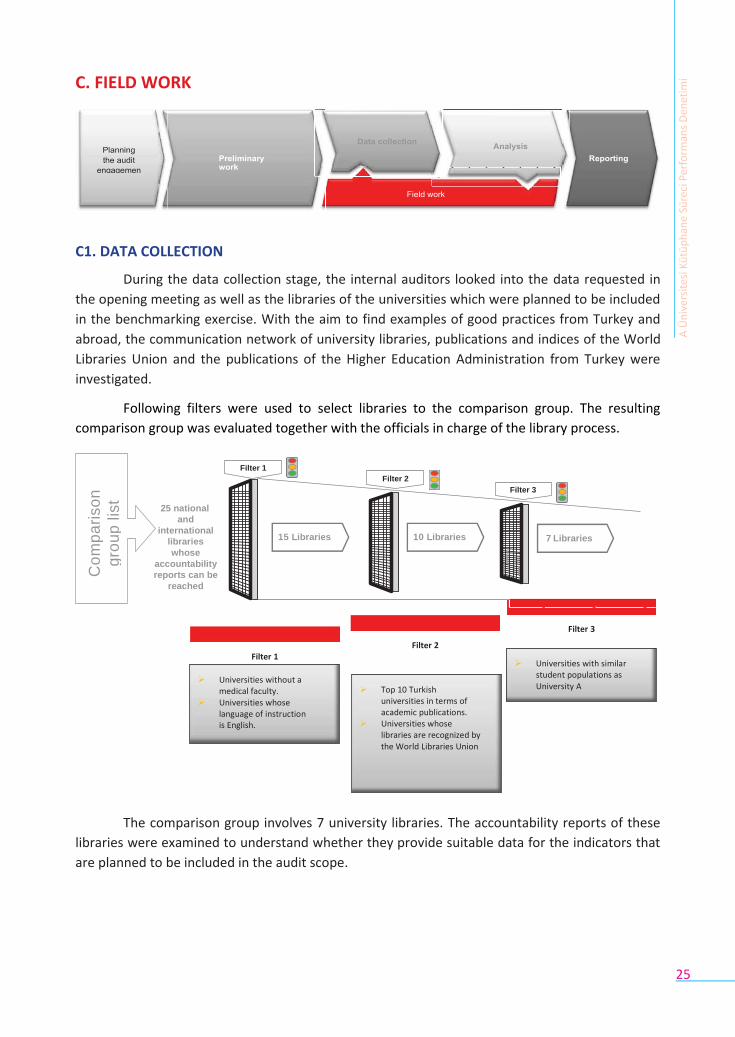

C. FIELD WORK

C1. DATA COLLECTION

During the data collection stage, the internal auditors looked into the data requested in

the opening meeting as well as the libraries of the universities which were planned to be included

in the benchmarking exercise. With the aim to find examples of good practices from Turkey and

abroad, the communication network of university libraries, publications and indices of the World

Libraries Union and the publications of the Higher Education Administration from Turkey were

investigated.

Following filters were used to select libraries to the comparison group. The resulting

comparison group was evaluated together with the officials in charge of the library process.

Filter 1

Filter 2

Filter 3

25 national

and

international

libraries

whose

accountability

reports can be

reached

15 Libraries 10 Libraries 7 Libraries

Filter 1

Filter 2

Filter 3

The comparison group involves 7 university libraries. The accountability reports of these

libraries were examined to understand whether they provide suitable data for the indicators that

are planned to be included in the audit scope.

Universities without a medical faculty. Universities whose language of instruction is English.

Top 10 Turkish universities in terms of academic publications. Universities whose libraries are recognized by the World Libraries Union

Universities with similar student populations as University A

Co

mp

ari

so

n

gro

up

lis

t

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

26

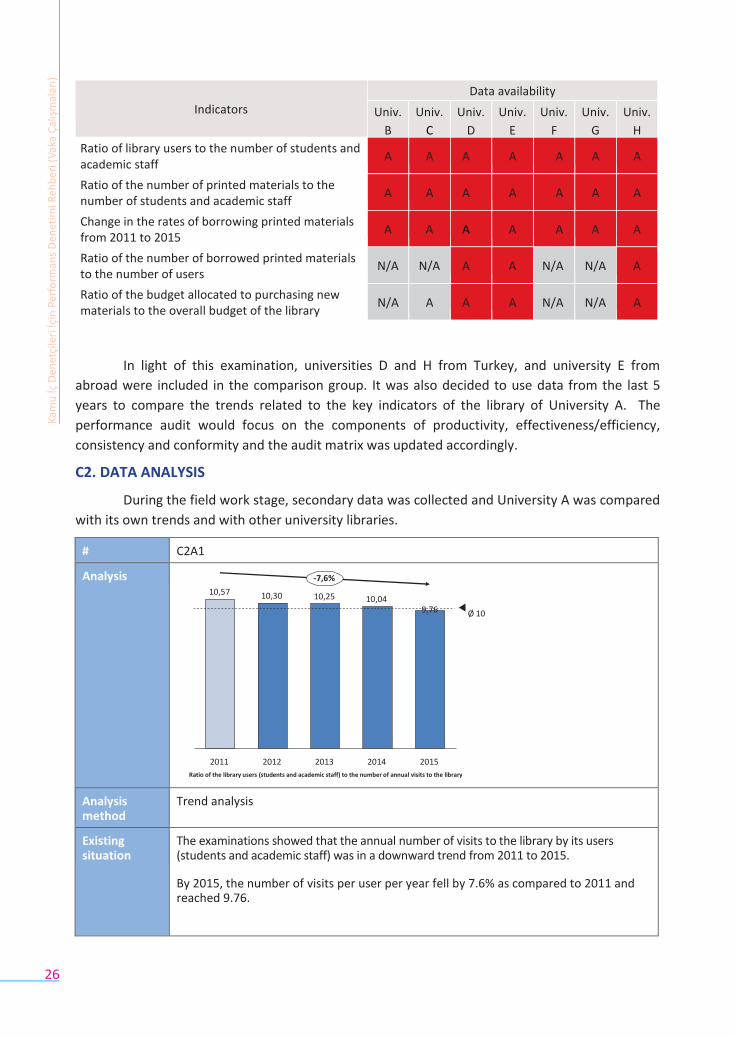

Indicators

Data availability

Univ.

B

Univ.

C

Univ.

D

Univ.

E

Univ.

F

Univ.

G

Univ.

H Ratio of library users to the number of students and

academic staff

Ratio of the number of printed materials to the number of students and academic staff

Change in the rates of borrowing printed materials from 2011 to 2015

Ratio of the number of borrowed printed materials to the number of users

Ratio of the budget allocated to purchasing new materials to the overall budget of the library

A A A A A A A

A A A A A A A

A A A A A A A

N/A N/A A A N/A N/A A

N/A A A A N/A N/A A

In light of this examination, universities D and H from Turkey, and university E from

abroad were included in the comparison group. It was also decided to use data from the last 5

years to compare the trends related to the key indicators of the library of University A. The

performance audit would focus on the components of productivity, effectiveness/efficiency,

consistency and conformity and the audit matrix was updated accordingly.

C2. DATA ANALYSIS

During the field work stage, secondary data was collected and University A was compared

with its own trends and with other university libraries.

# C2A1

Analysis

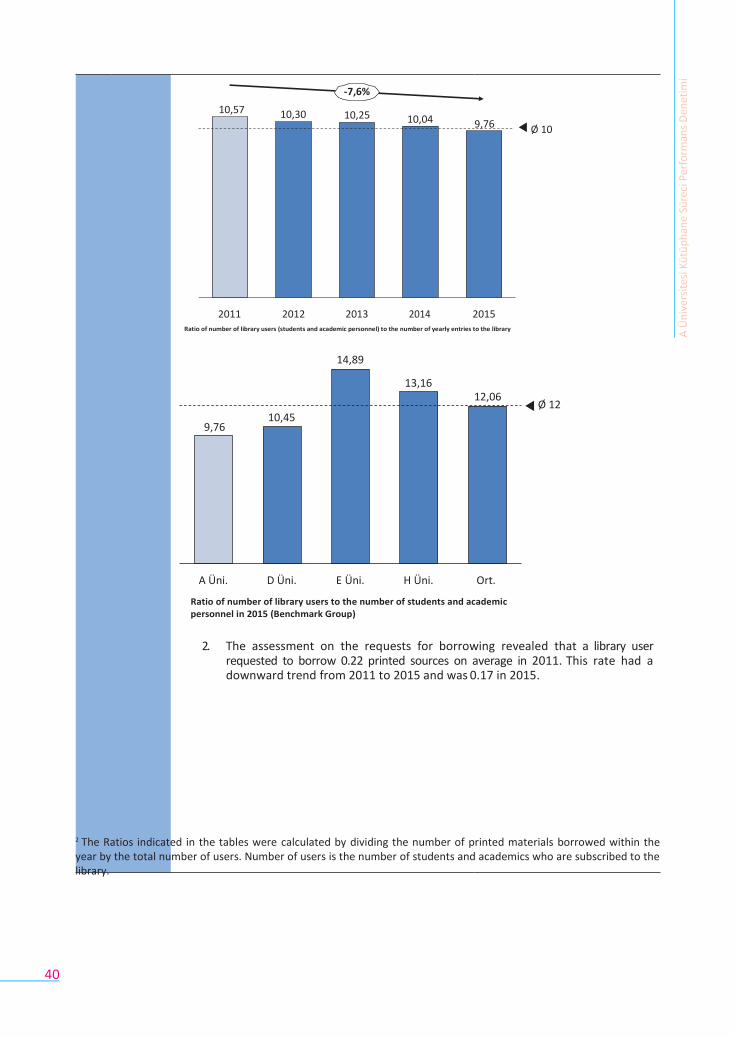

-7,6%

10,57 10,30 10,25 10,04

9,76 Ø 10

2011 2012 2013 2014 2015

Ratio of the library users (students and academic staff) to the number of annual visits to the library

Analysis method

Trend analysis

Existing situation

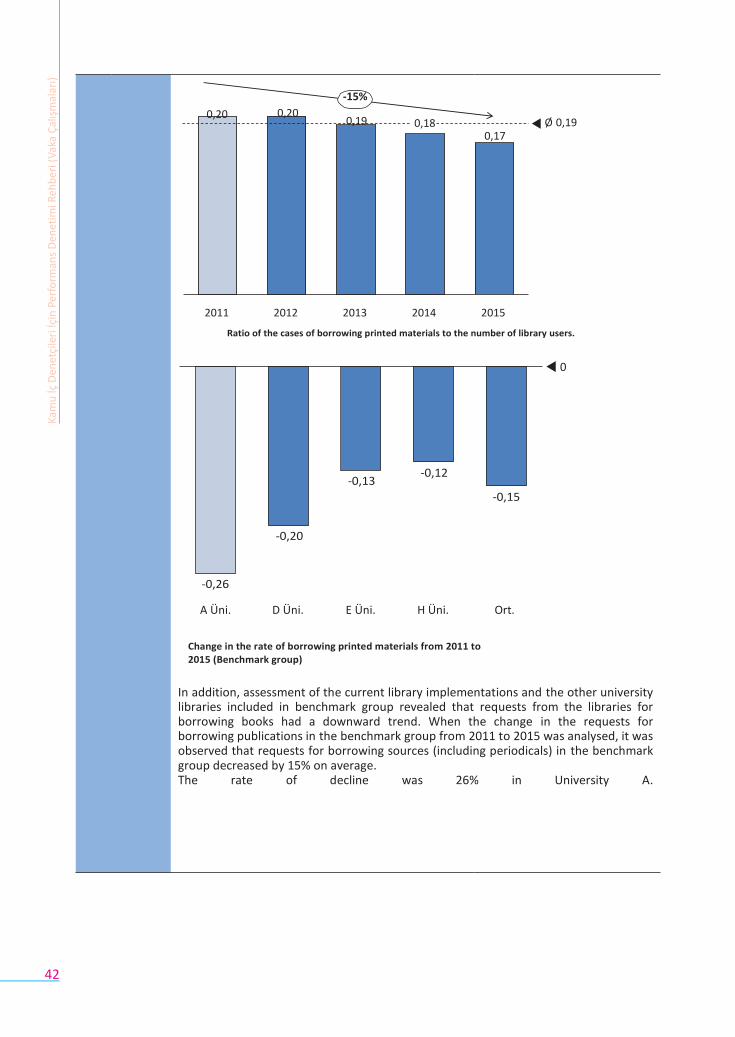

The examinations showed that the annual number of visits to the library by its users (students and academic staff) was in a downward trend from 2011 to 2015.

By 2015, the number of visits per user per year fell by 7.6% as compared to 2011 and reached 9.76.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

27

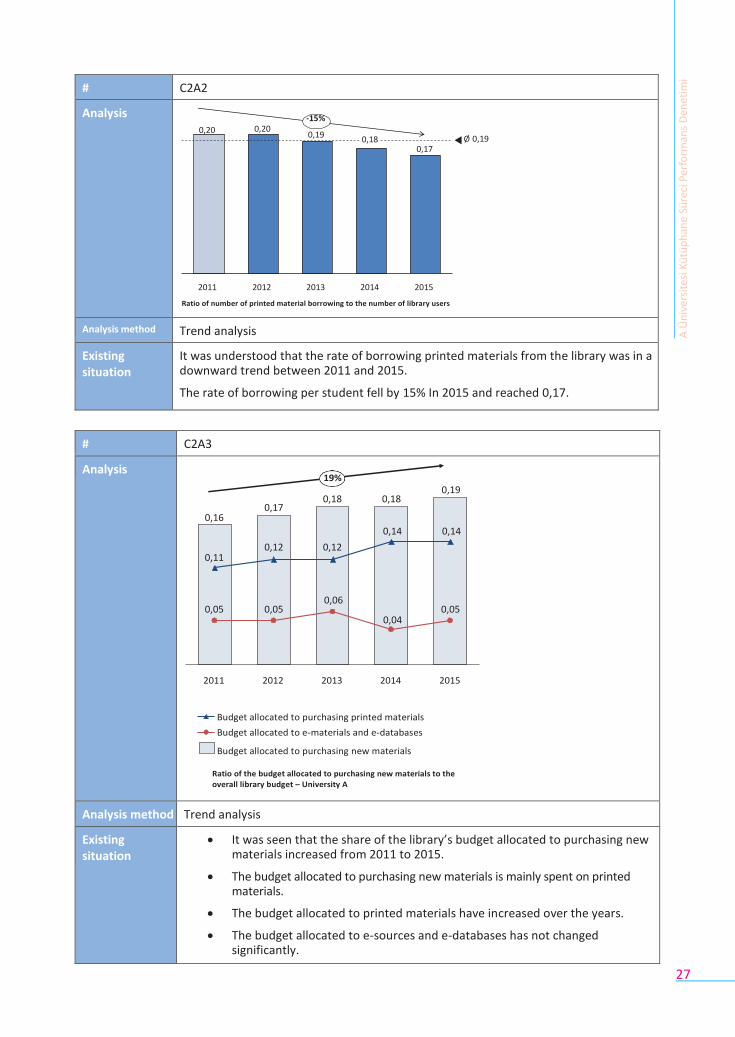

# C2A2

Analysis -15%

0,20 0,20 0,19

0,18 Ø 0,19

0,17

2011 2012 2013 2014 2015

Ratio of number of printed material borrowing to the number of library users

Analysis method Trend analysis

Existing situation

It was understood that the rate of borrowing printed materials from the library was in a downward trend between 2011 and 2015.

The rate of borrowing per student fell by 15% In 2015 and reached 0,17.

# C2A3

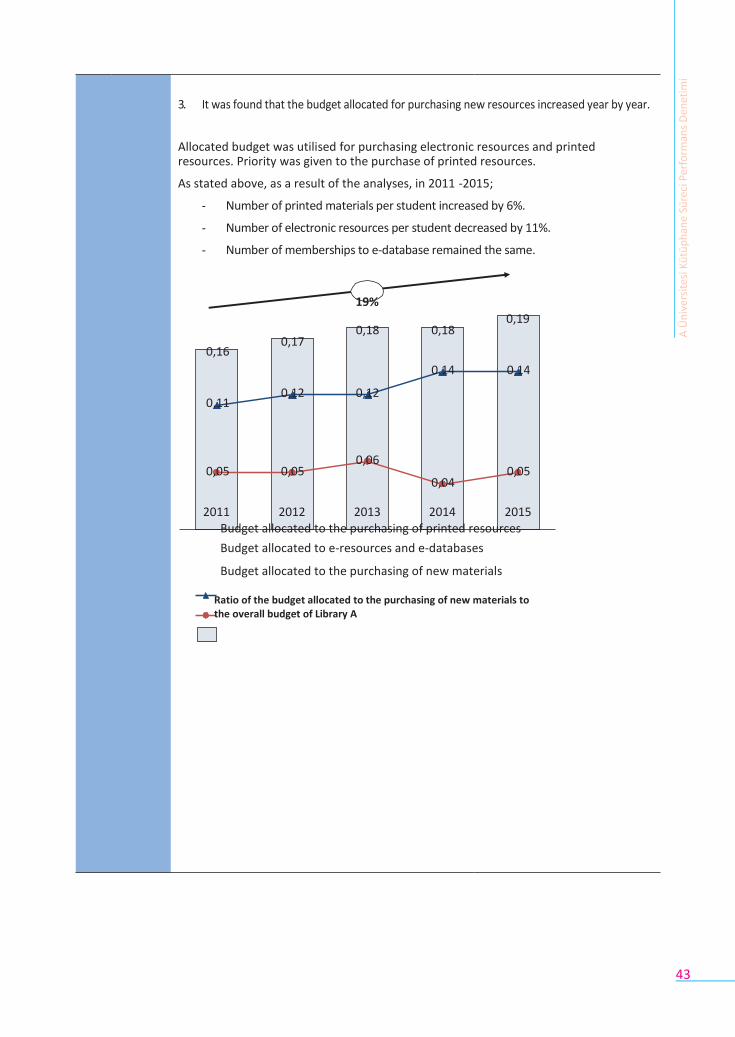

Analysis 19%

0,19 0,18 0,18

0,17 0,16

0,14 0,14

0,12 0,12 0,11

0,06 0,05 0,05 0,05

0,04

2011 2012 2013 2014 2015

Budget allocated to purchasing printed materials

Budget allocated to e-materials and e-databases

Budget allocated to purchasing new materials

Ratio of the budget allocated to purchasing new materials to the overall library budget – University A

Analysis method Trend analysis

Existing situation

It was seen that the share of the library’s budget allocated to purchasing new materials increased from 2011 to 2015.

The budget allocated to purchasing new materials is mainly spent on printed materials.

The budget allocated to printed materials have increased over the years.

The budget allocated to e-sources and e-databases has not changed significantly.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

28

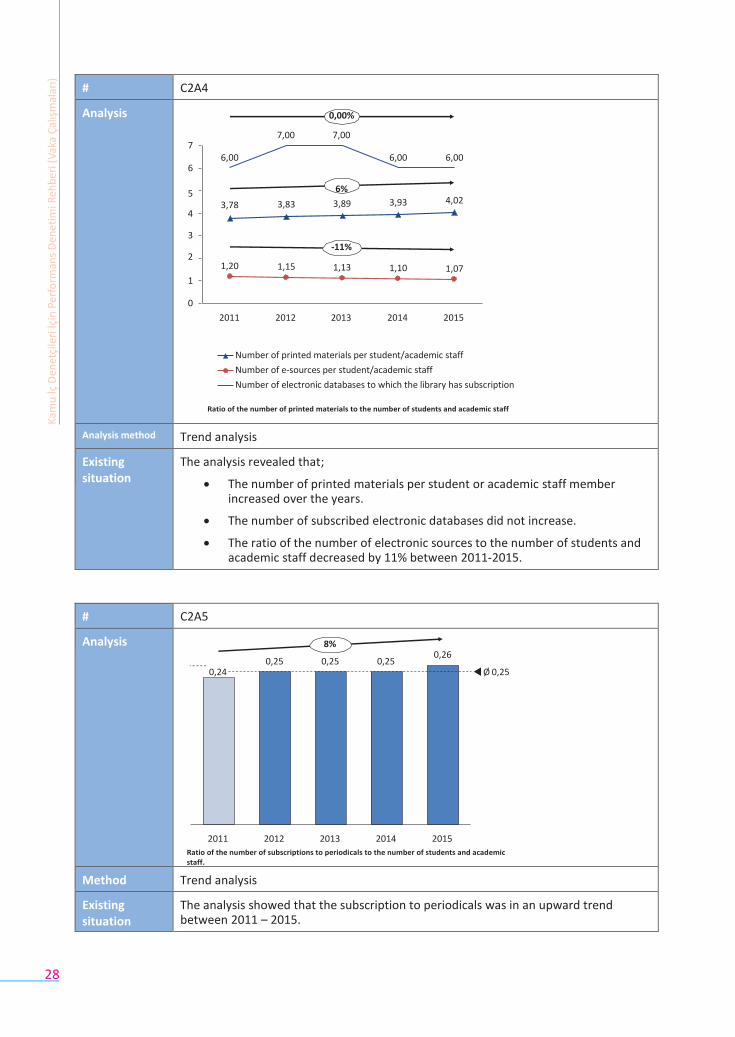

# C2A4

Analysis

0,00%

7,00 7,00 7

6,00 6,00 6,00 6

5 6%

3,78 3,83 3,89 3,93 4,02 4

3 -11%

2 1,20 1,15 1,13 1,10 1,07

1

0

2011 2012 2013 2014 2015

Number of printed materials per student/academic staff

Number of e-sources per student/academic staff

Number of electronic databases to which the library has subscription

Ratio of the number of printed materials to the number of students and academic staff

Analysis method Trend analysis

Existing situation

The analysis revealed that;

The number of printed materials per student or academic staff member increased over the years.

The number of subscribed electronic databases did not increase.

The ratio of the number of electronic sources to the number of students and academic staff decreased by 11% between 2011-2015.

# C2A5

Analysis

8%

0,25 0,25 0,25 0,26

0,24 Ø 0,25

2011 2012 2013 2014 2015

Ratio of the number of subscriptions to periodicals to the number of students and academic staff.

Method Trend analysis

Existing situation

The analysis showed that the subscription to periodicals was in an upward trend between 2011 – 2015.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

29

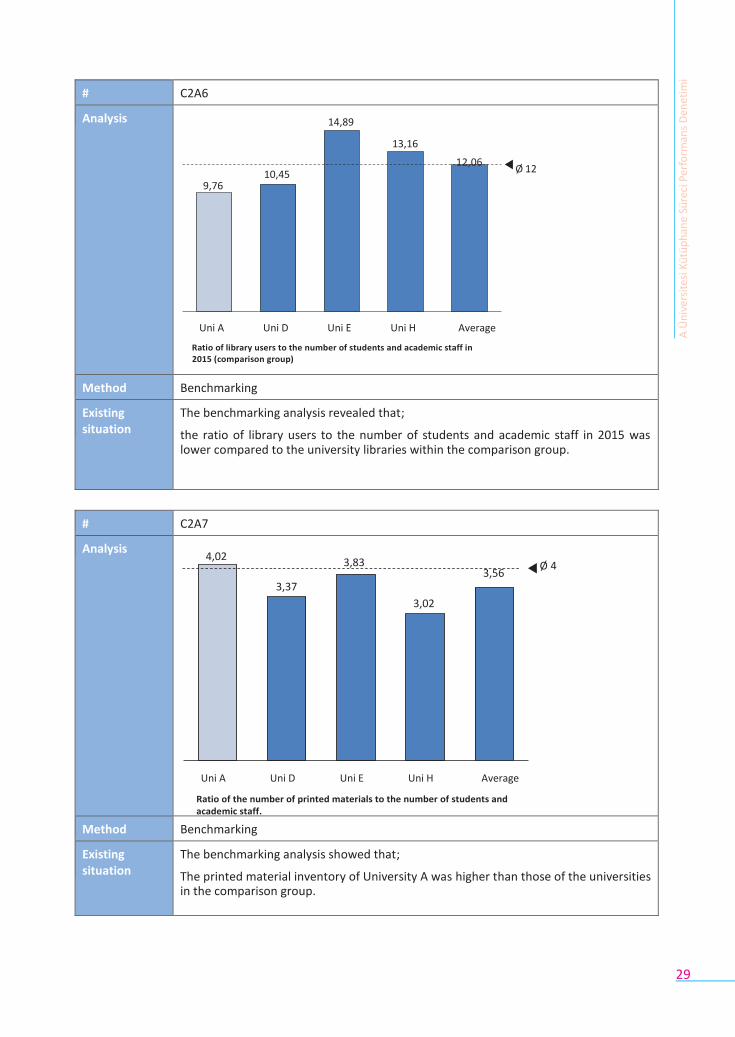

# C2A6

Analysis

14,89

13,16

12,06 Ø 12

10,45

9,76

Uni A Uni D Uni E Uni H Average

Ratio of library users to the number of students and academic staff in 2015 (comparison group)

Method Benchmarking

Existing situation

The benchmarking analysis revealed that;

the ratio of library users to the number of students and academic staff in 2015 was lower compared to the university libraries within the comparison group.

# C2A7

Analysis 4,02

3,83

3,56 Ø 4

3,37

3,02

Uni A Uni D Uni E Uni H Average

Ratio of the number of printed materials to the number of students and academic staff.

Method Benchmarking

Existing situation

The benchmarking analysis showed that;

The printed material inventory of University A was higher than those of the universities in the comparison group.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

37

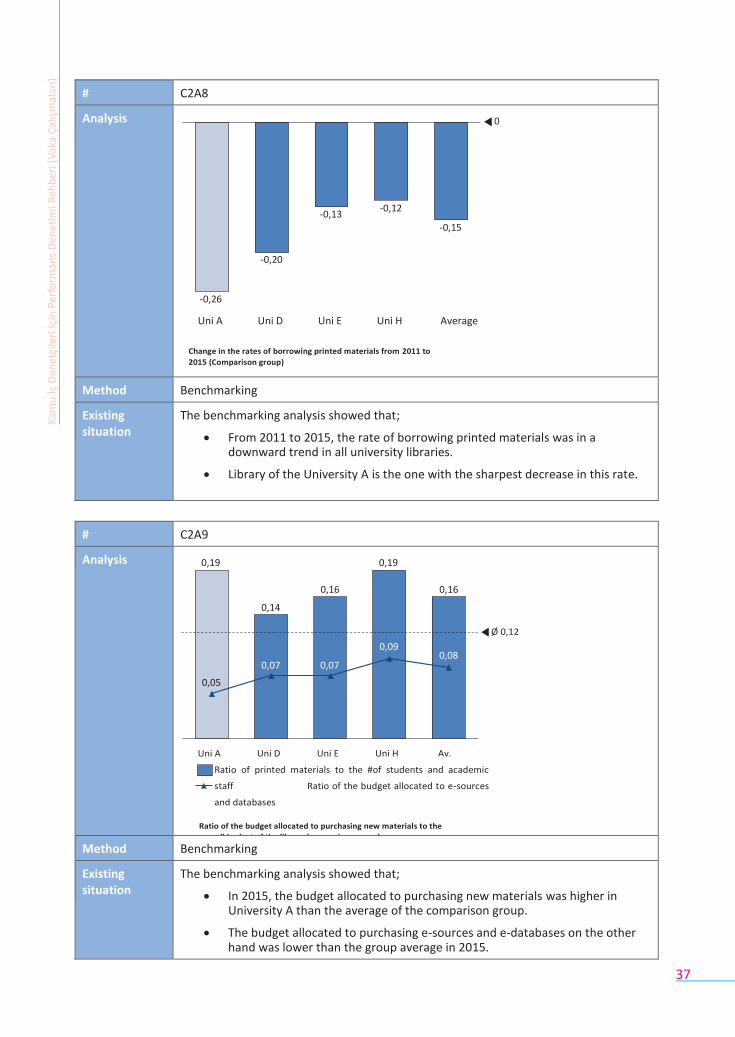

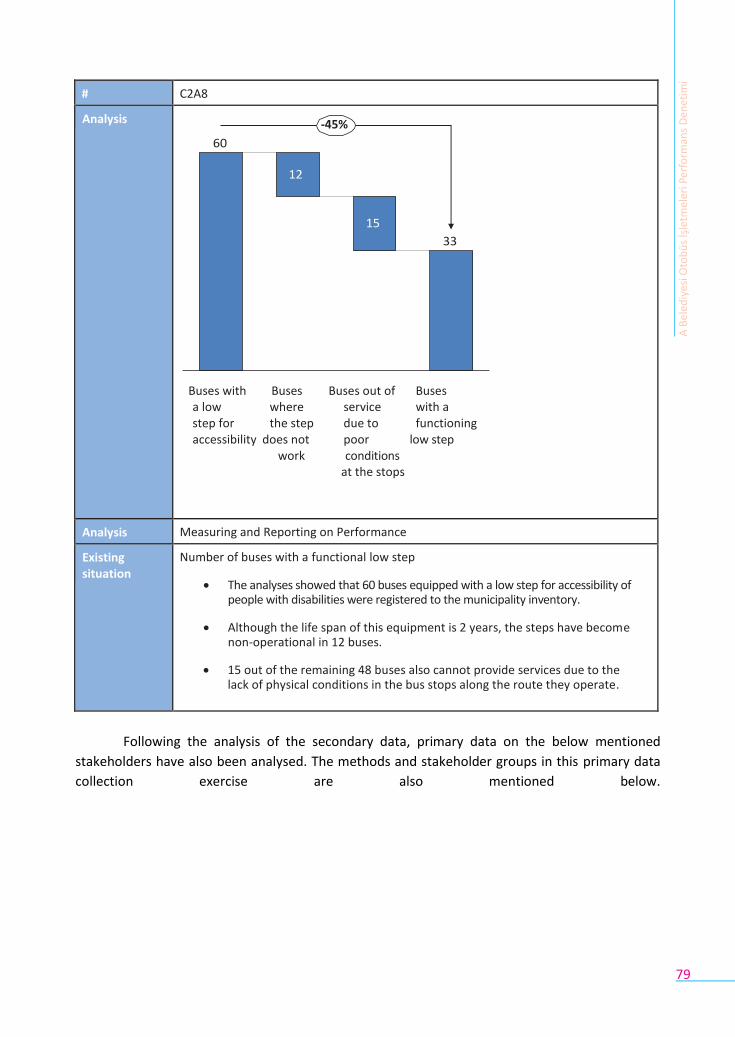

# C2A8

Analysis 0

-0,13 -0,12

-0,15

-0,20

-0,26

Uni A Uni D Uni E Uni H Average

Change in the rates of borrowing printed materials from 2011 to

2015 (Comparison group)

Method Benchmarking

Existing situation

The benchmarking analysis showed that;

From 2011 to 2015, the rate of borrowing printed materials was in a downward trend in all university libraries.

Library of the University A is the one with the sharpest decrease in this rate.

# C2A9

Analysis 0,19 0,19

0,16 0,16

0,14

Ø 0,12

0,09 0,08

0,07 0,07

0,05

Uni A Uni D Uni E Uni H Av.

Ratio of printed materials to the #of students and academic

staff Ratio of the budget allocated to e-sources

and databases

Ratio of the budget allocated to purchasing new materials to the

overall budget of the library (comparison group)

Method Benchmarking

Existing situation

The benchmarking analysis showed that;

In 2015, the budget allocated to purchasing new materials was higher in University A than the average of the comparison group.

The budget allocated to purchasing e-sources and e-databases on the other hand was lower than the group average in 2015.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

30

The analysis of the secondary data was followed by an analysis of the primary data related

to the below-mentioned stakeholders. The method of collecting primary data and the stakeholder

groups are stated below.

# C2B1

Stakeholder Academic staff

Analysis method Focus group meeting

Analysis strategy

Participants were chosen from all faculties of the university, for a focus group meeting on library processes.

It was requested that the participants would be identified by the faculty management.

The number of academic members representing each faculty was proportional to the overall number of academic members in that faculty.

The subject of the focus group meeting, its content, general topics to be discussed and the assessment method to be applied were communicated to the participants beforehand.

Existing situation

As a result of the focus group meeting, following conclusions were made:

Majority of the academic staff have subscriptions to e-databases outside the university library.

The main reasons for this are stated below:

The inventory of the e-database in the university library is limited.

The library may purchase printed materials upon demand from the academic staff members. The budget for this type of purchases is sufficient. Such demands from academic staff members are generally accepted. However, due to the procedures in the library regulation and the time taking procedure of acquiring printed materials, the process may take a long time.

For this reason, the academic staff members prefer to have memberships in the e-databases so that they can have quick access to the resources they need in their academic work.

Individual purchase of these memberships by many academic staff members in sum reaches a much higher amount compared to the general membership of the university library.

Academic members therefore conduct their work by using the resources and databases outside the library.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

32

# C2B2

Stakeholder group

Library staff

Analysis method In-depth interview

Analysis strategy

Face to face interviews were conducted with the library staff members in consideration of their experiences and job titles.

In this context, 20 out of the 75 staff members were interviewed with.

The responses given by staff members to pre-determined questions were analysed.

Existing situation

Following conclusions were reached:

The areas which may have an impact on the satisfaction of the students using the library and their rate of using the library were analysed during the interviews. These areas are summarized as follows:

Performance indicators of the library staff have not been sufficiently identified. This results in a situation where good performance is not rewarded and the actual performance may vary depending on the sense of responsibility of the staff members.

Due to lack of resources related to the IT services in the library user demands in this area cannot be met at a satisfactory level.

Since the qualities that a library professional must possess, such as experience, command of foreign languages, education level, etc. are not stated in the library regulation, the existing human resources of the library may lack such qualities.

# C2B3

Stakeholder group

Students

Analysis method Questionnaire

Analysis strategy

A questionnaire consisting of 5 questions was prepared for all students.

The questionnaire was published on the web site of the university. 410 students responded via this medium.

Also, face to face interviews were conducted within the library and 140 students answered the questionnaire.

Existing situation

The results of the questionnaire are as follows:

The data sources used by students while conducting a research are listed as follows:

Internet (97%)

Publicly available electronic books and academic studies (90%)

Online databases and resources (78%)

Printed publications available in the library (25%)

The library should focus more on the following resources in its inventory. (The questionnaire allowed selecting more than one option.)

Online memberships (80%)

E-databases (75%)

Printed periodicals (90%)

Printed books (40%)

Only 40% of the students are aware that they can ask the library to acquire e-resources or printed materials. The number of students who know how to place such requests constitutes 10% of the students who have responded to the questionnaire.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

33

# C2B4

Stakeholder group Students

Analysis method

Questionnaire /

Coding

Analysis strategy

One of the questions in the questionnaire asked the students to list the most frequent problems they encounter related to library services.

Coding method was used to analyse the responses. In this exercise, the answers provided were assessed through the below-mentioned scores.

The problems stated by participants were scored according to the ranking provided by participants.

In this regard;

- The problem at the top of the list gets 3 points

- The second problem gets 2 points and

- The third problem gets 1 point.

Existing situation

Using the results of the questionnaire, 10 basic problems faced by library users were identified. These problems were assessed by using the coding method defined in the analysis strategy and the resulting first five problems are stated below.

# C2B5

Stakeholder group Students

Analysis method

Control group analysis

Analysis strategy

Whether the students participating in the questionnaire have taken the library orientation guidance or not was identified.

Regardless of whether they took the guidance, the students were asked whether they visited the library in the first year of their education.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

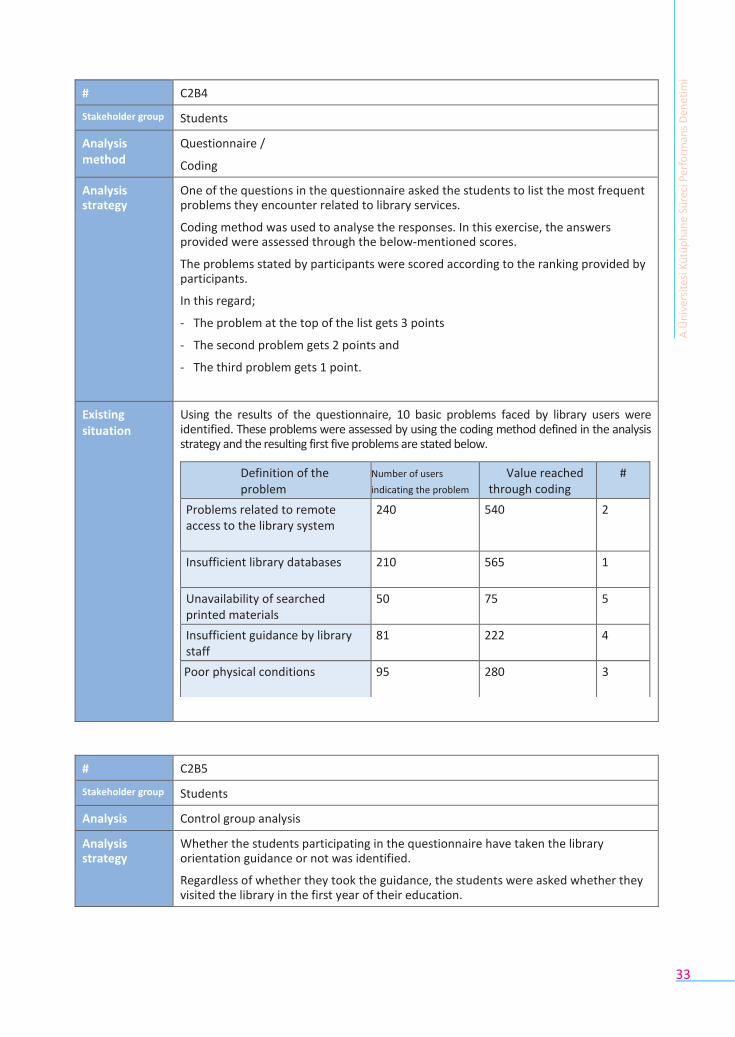

Definition of the problem

Number of users

indicating the problem

Value reached through coding

#

Problems related to remote access to the library system

240 540 2

Insufficient library databases 210 565 1

Unavailability of searched printed materials

50 75 5

Insufficient guidance by library staff

81 222 4

Poor physical conditions 95 280 3

34

Ory

an

tasy

on

Eğ

itim

ine

Ka

tıla

n Ö

ğre

nci

leri

n İl

k Y

ıl K

ütü

ph

an

e

Ku

lla

nım

Ora

nla

rı

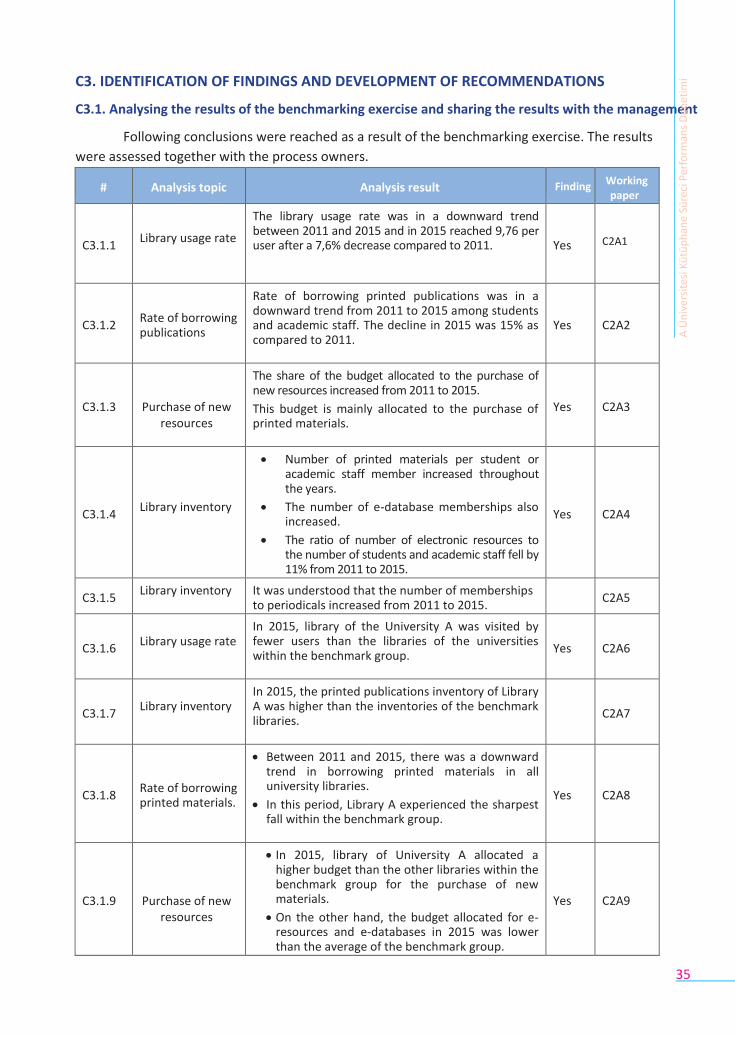

# C2B6

Stakeholder group Students

Analysis method

Bi-variate analysis

Analysis strategy

The library usage rate and the ratio of students who have taken the orientation training to the total number of students were compared to analyse the relationship between these variables. The dependent variable was set as the library usage rate (which is found by dividing the total number of visits to the library to the number of students in the university). Number of students who have taken the orientation training was taken from the library data.

Existing situation

Relationship between the orientation training and library usage rate

74%

73%

72%

71%

70%

Library Usage rate

69% Projected library usage rate

68%

67%

66%

54,00% 56,00% 58,00% 60,00% 62,00% 64,00% 66,00%

Ratio of students who have taken the orientation training to the entire student population

The analysis shows that there is high correlation between the library usage rate and the participation to orientation training (the calculations result in a rate of 85%).

Existing situation

2014

Students who have taken the orientation guidance Students who have not taken the orientation guidance

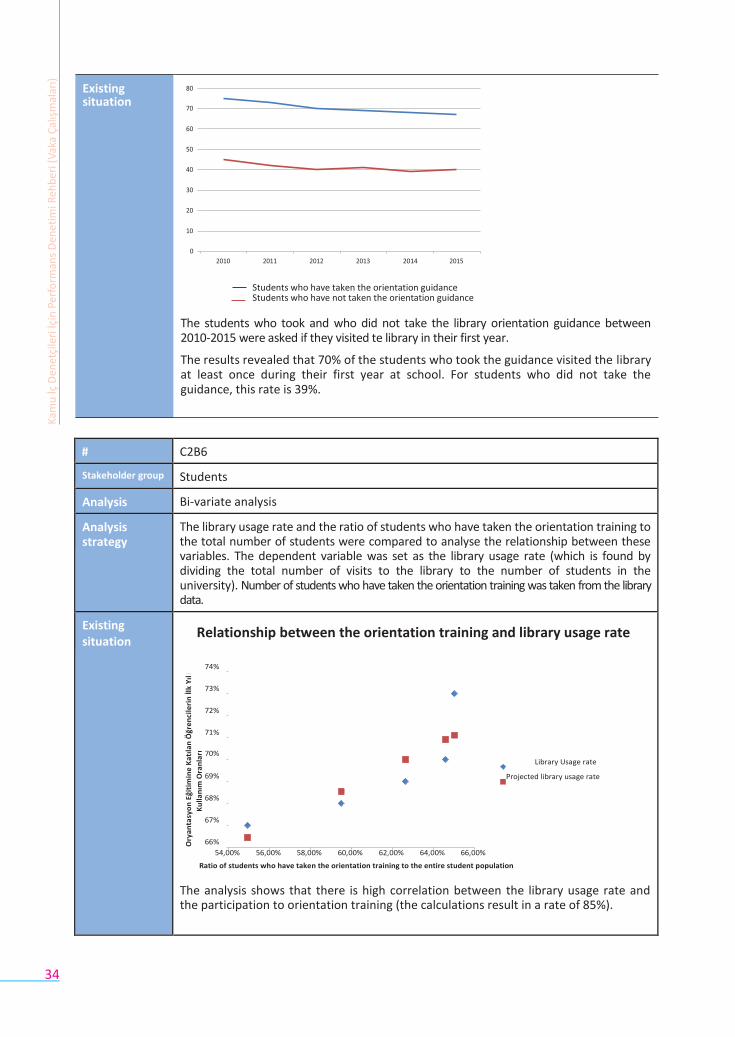

The students who took and who did not take the library orientation guidance between 2010-2015 were asked if they visited te library in their first year.

The results revealed that 70% of the students who took the guidance visited the library at least once during their first year at school. For students who did not take the guidance, this rate is 39%.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

35

C3. IDENTIFICATION OF FINDINGS AND DEVELOPMENT OF RECOMMENDATIONS

C3.1. Analysing the results of the benchmarking exercise and sharing the results with the management

Following conclusions were reached as a result of the benchmarking exercise. The results

were assessed together with the process owners.

# Analysis topic Analysis result Finding Working paper

C3.1.1

Library usage rate

The library usage rate was in a downward trend between 2011 and 2015 and in 2015 reached 9,76 per user after a 7,6% decrease compared to 2011.

Yes

C2A1

C3.1.2

Rate of borrowing publications

Rate of borrowing printed publications was in a downward trend from 2011 to 2015 among students and academic staff. The decline in 2015 was 15% as compared to 2011.

Yes

C2A2

C3.1.3

Purchase of new

resources

The share of the budget allocated to the purchase of new resources increased from 2011 to 2015.

This budget is mainly allocated to the purchase of printed materials.

Yes

C2A3

C3.1.4

Library inventory

Number of printed materials per student or academic staff member increased throughout the years.

The number of e-database memberships also increased.

The ratio of number of electronic resources to the number of students and academic staff fell by 11% from 2011 to 2015.

Yes

C2A4

C3.1.5 Library inventory It was understood that the number of memberships

to periodicals increased from 2011 to 2015.

C2A5

C3.1.6

Library usage rate

In 2015, library of the University A was visited by fewer users than the libraries of the universities within the benchmark group.

Yes

C2A6

C3.1.7

Library inventory

In 2015, the printed publications inventory of Library A was higher than the inventories of the benchmark libraries.

C2A7

C3.1.8

Rate of borrowing printed materials.

Between 2011 and 2015, there was a downward trend in borrowing printed materials in all university libraries.

In this period, Library A experienced the sharpest fall within the benchmark group.

Yes

C2A8

C3.1.9

Purchase of new

resources

In 2015, library of University A allocated a higher budget than the other libraries within the benchmark group for the purchase of new materials.

On the other hand, the budget allocated for e-resources and e-databases in 2015 was lower than the average of the benchmark group.

Yes

C2A9

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

36

# Analysis topic Analysis result Finding Working paper

C3.1.10

Focus group meeting (Academic members)

- Library usage rate

- Library inventory

- Purchase of new resources

It has been understood that a major part of the academic members have subscriptions to e-databases outside the university library.

According to the academic members, the main reasons for this are as follows:

The inventory of the e-database of the university is limited.

The library has sufficient financial means to purchase printed materials upon the demand of the academic members. Such demands are met positively most of the time. However, due to the procedures provided in the regulation of the library and the time taking nature of the acquisition of new books, this process may take a long time.

For this reason, the academic members prefer to subscribe to e-databases which provide the fastest access to the materials they need in conducting their researches.

When the money spent by individual academic members for such subscriptions are put together, the overall sum is much greater than the amount that would be spent by the library for collective memberships.

For the above reasons, the academic members are conducting their academic studies over the databases and resources outside the university library.

Yes

C2B1

C3.1.11

In depth interviews

(Library staff)

- User satisfaction

- Operations

As a result of the interviews, the areas that might affect the satisfaction and library usage rate of students have been identified as follows:

Performance indicators of the library staff have not been sufficiently identified. This results in a situation where good performance is not rewarded and the actual performance may vary depending on the sense of responsibility of the staff members.

Due to lack of resources related to the IT services in the library user demands in this area cannot be met at a satisfactory level.

Since the qualities that a library professional must possess, such as experience, command of foreign languages, education level, etc. are not stated in the library regulation, the existing human resources of the library may lack such qualities.

Yes

C2B2

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

37

# Analysis topic Analysis result Finding Working paper

C3.1.12

Questionnaire

(Students)

- User satisfaction

- Operations

The data sources used by students while conducting a research are listed as follows:

Internet (97%)

Publicly available electronic books and academic studies (90%)

Online databases and resources (78%)

Printed publications available in the library (25%)

The library should focus more on the following resources in its inventory. (The questionnaire allowed selecting more than one option.)

Online memberships (80%)

E-databases (75%)

Printed periodicals (90%)

Printed books (40%)

Only 40% of the students are aware that they can ask the library to acquire e-resources or printed materials. The number of students who know how to place such requests constitutes 10% of the students who have responded to the questionnaire.

For students, the most common shortcomings related to the library services are as follows:

Problems related to remote access to the library system (%88)

Insufficient library databases (%65)

Unavailability of searched printed materials (%20)

Insufficient guidance by library staff (%30)

Poor physical conditions (%30)

Yes

C2B3, C2B4

C3.2. Analysis of the findings, risks and root causes that have emerged as a result of the benchmarking exercise

Several findings have been identified as a result of the analysis. These findings are

grouped under different headings. A fishbone diagram has been used to analyse the causes of the

identified finding.

The analyses and interviews revealed that the proportion of the budget allocated by the

university for library activities within the overall budget increased from 2011 to 2015. In terms of its

inventory and the budget allocated for acquiring new resources, the library is among the top

university libraries both at national and international levels.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

38

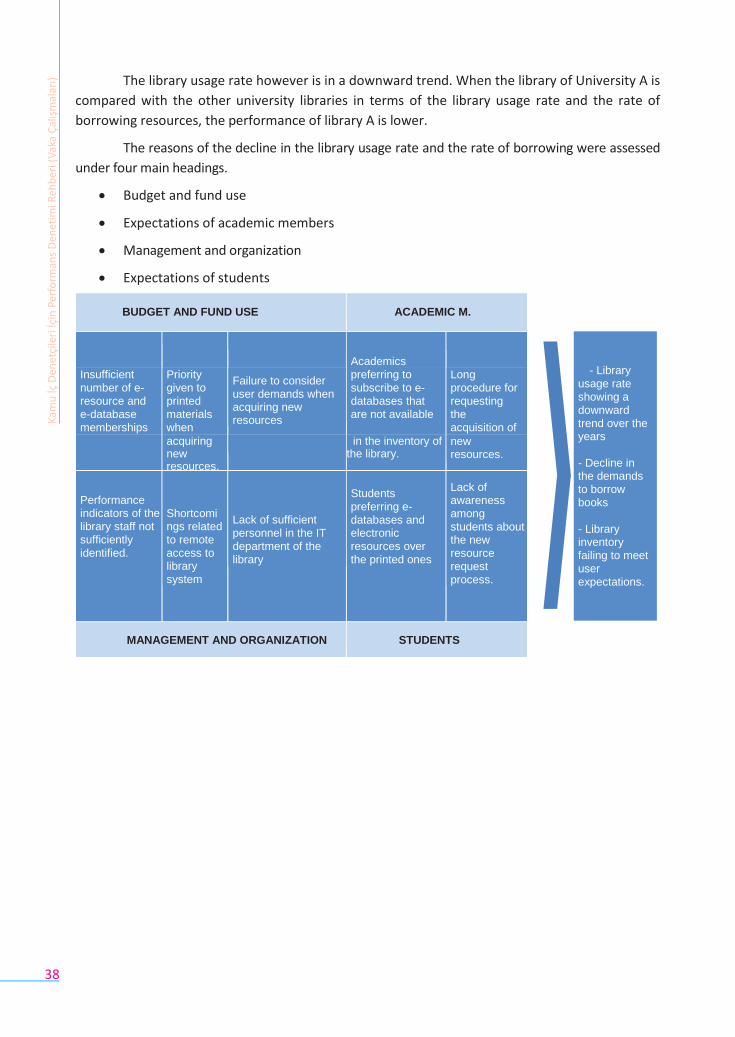

The library usage rate however is in a downward trend. When the library of University A is

compared with the other university libraries in terms of the library usage rate and the rate of

borrowing resources, the performance of library A is lower.

The reasons of the decline in the library usage rate and the rate of borrowing were assessed

under four main headings.

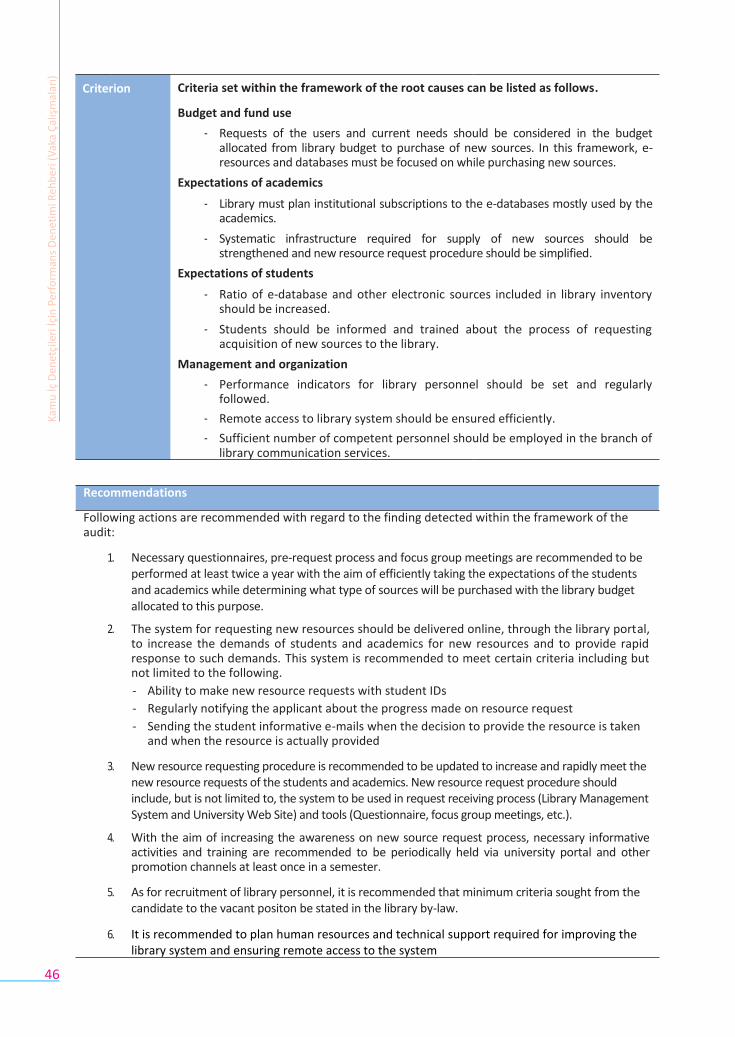

Budget and fund use

Expectations of academic members

Management and organization

Expectations of students

BUDGET AND FUND USE

ACADEMIC M.

Academics

Insufficient number of e-resource and e-database memberships

Priority given to printed materials when

Failure to consider user demands when acquiring new resources

preferring to subscribe to e-databases that are not available

Long procedure for requesting the acquisition of

acquiring new resources.

in the inventory of the library.

new resources.

Performance indicators of the library staff not sufficiently identified.

Shortcomings related to remote access to library system

Lack of sufficient personnel in the IT department of the library

Students preferring e-databases and electronic resources over the printed ones

Lack of awareness among students about the new resource request process.

MANAGEMENT AND ORGANIZATION

STUDENTS

- Library

usage rate showing a downward trend over the years

- Decline in the demands to borrow books

- Library inventory failing to meet user expectations.

Kam

u İç

Den

etçi

leri

İçin

Per

form

ans

Den

etim

i Reh

ber

i (V

aka

Çal

ışm

alar

ı)

39

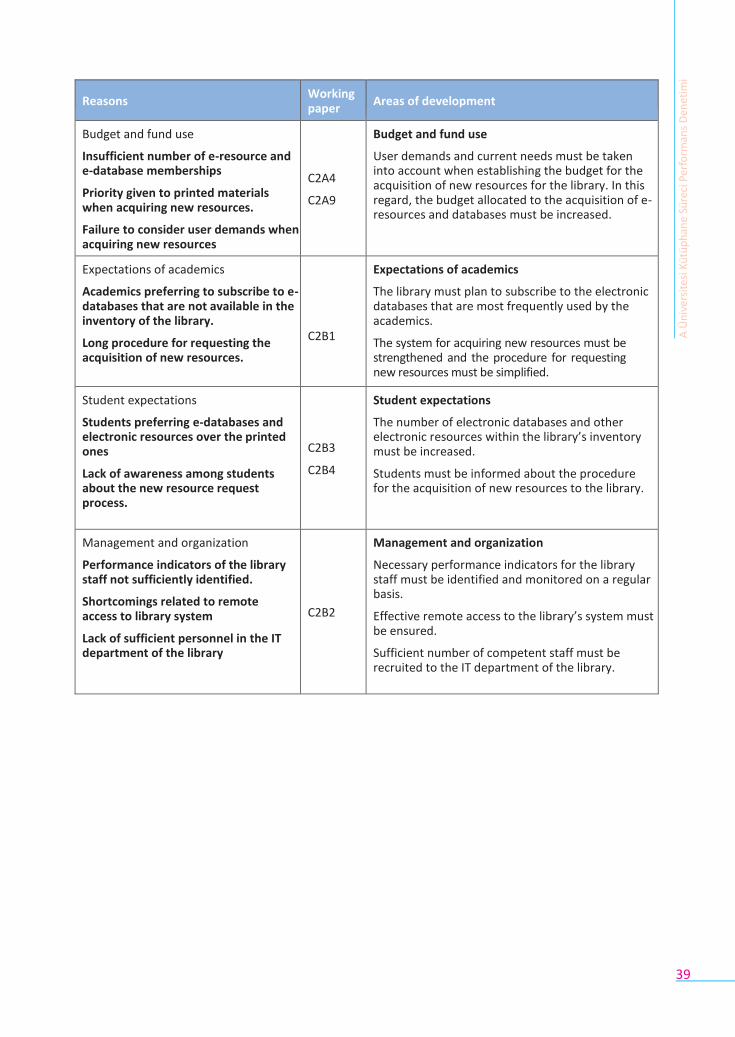

Reasons Working paper

Areas of development

Budget and fund use

Insufficient number of e-resource and e-database memberships

Priority given to printed materials when acquiring new resources.

Failure to consider user demands when acquiring new resources

C2A4

C2A9

Budget and fund use

User demands and current needs must be taken into account when establishing the budget for the acquisition of new resources for the library. In this regard, the budget allocated to the acquisition of e-resources and databases must be increased.

Expectations of academics

Academics preferring to subscribe to e-databases that are not available in the inventory of the library.

Long procedure for requesting the acquisition of new resources.

C2B1

Expectations of academics

The library must plan to subscribe to the electronic databases that are most frequently used by the academics.

The system for acquiring new resources must be strengthened and the procedure for requesting new resources must be simplified.

Student expectations

Students preferring e-databases and electronic resources over the printed ones

Lack of awareness among students about the new resource request process.

C2B3

C2B4

Student expectations

The number of electronic databases and other electronic resources within the library’s inventory must be increased.

Students must be informed about the procedure for the acquisition of new resources to the library.

Management and organization

Performance indicators of the library staff not sufficiently identified.

Shortcomings related to remote access to library system

Lack of sufficient personnel in the IT department of the library

C2B2

Management and organization

Necessary performance indicators for the library staff must be identified and monitored on a regular basis.

Effective remote access to the library’s system must be ensured.

Sufficient number of competent staff must be recruited to the IT department of the library.

A Ü

niv

ers

ites

i Kü

tüp

han

e Sü

reci

Per

form

ans

Den

etim

i

43

Kıy

asla

ma

Gru

bu

Lis

tesi

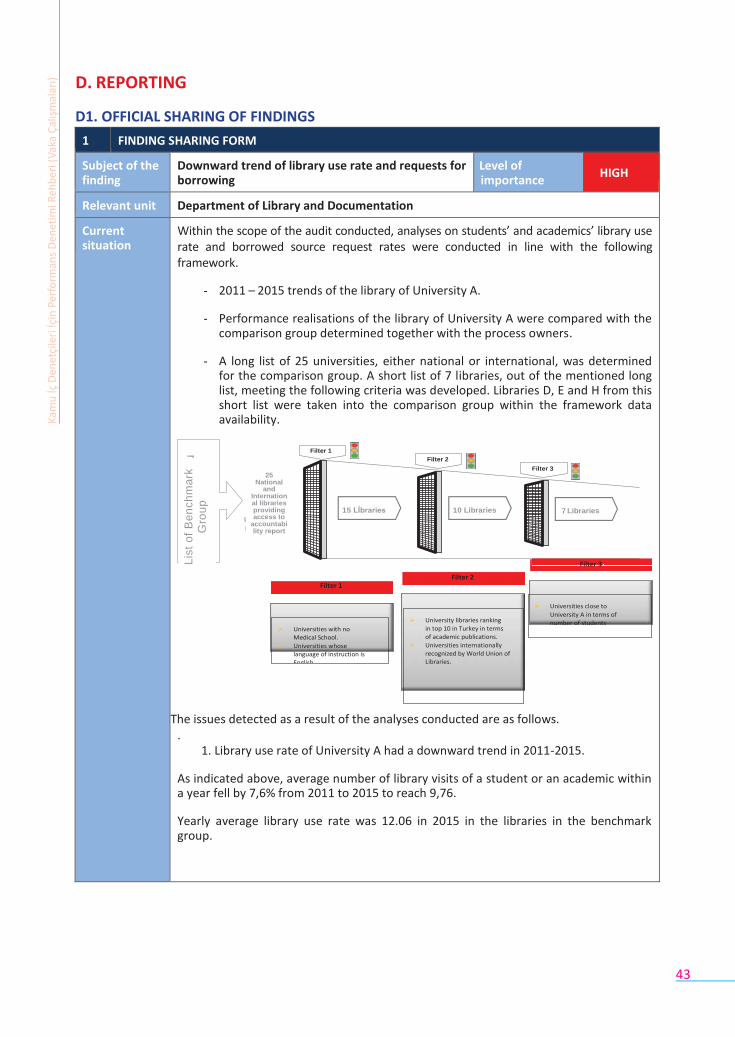

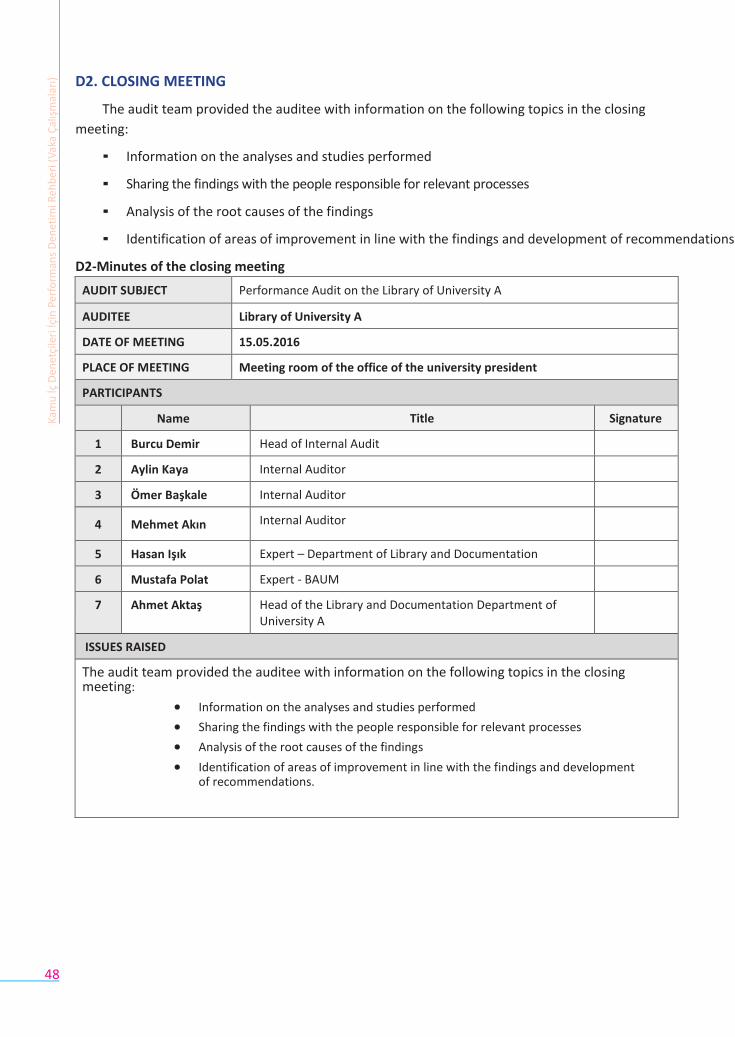

D. REPORTING

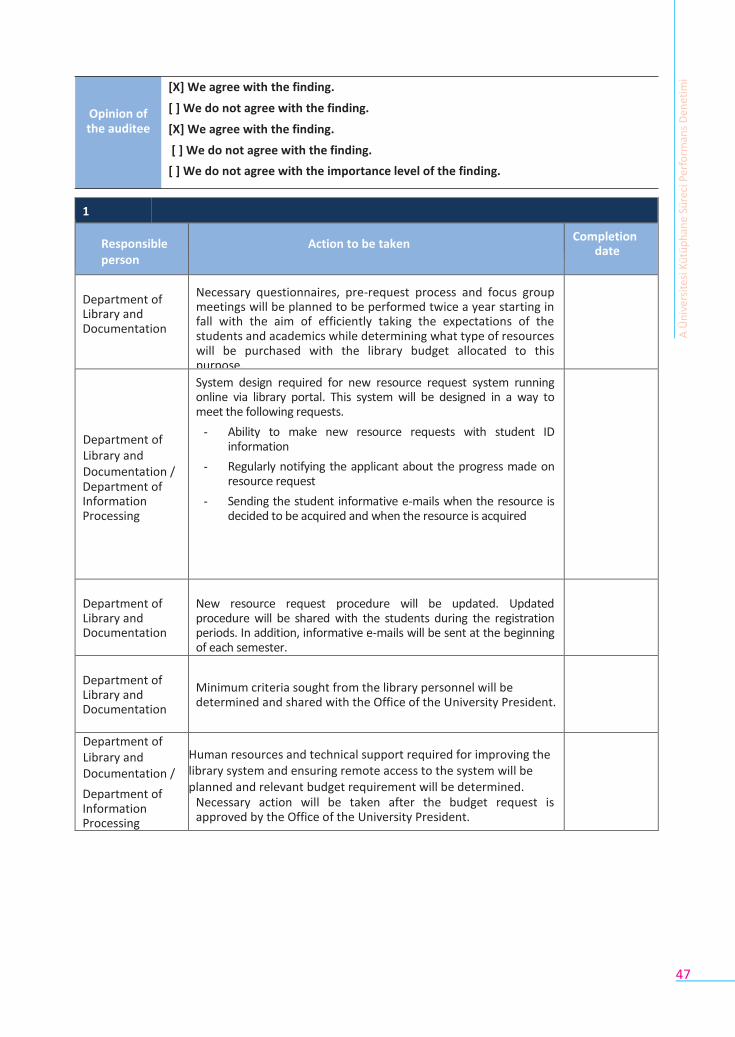

D1. OFFICIAL SHARING OF FINDINGS

1 FINDING SHARING FORM

Subject of the finding

Downward trend of library use rate and requests for borrowing

publications by years

Level of importance

HIGH

Relevant unit Department of Library and Documentation

Current situation

Within the scope of the audit conducted, analyses on students’ and academics’ library use rate and borrowed source request rates were conducted in line with the following framework.

- 2011 – 2015 trends of the library of University A.

- Performance realisations of the library of University A were compared with the comparison group determined together with the process owners.