Embed Size (px)

Citation preview

Strategic Level

SL2 - Corporate Finance and Risk Management

Performance Analysis

Ruchira Perera

CPA (Aus.), ACMA (UK), CGMA, FCMA (SL),

B.Sc. Accounting (Sri J), MBA (PIM - Sri J)

Bond Valuation

Basic Valuation

✓Using time value of money concepts, we realize that

the value of anything is based on the present value of

the cash flows the asset is expected to produce in the

future

2

Basic Valuation

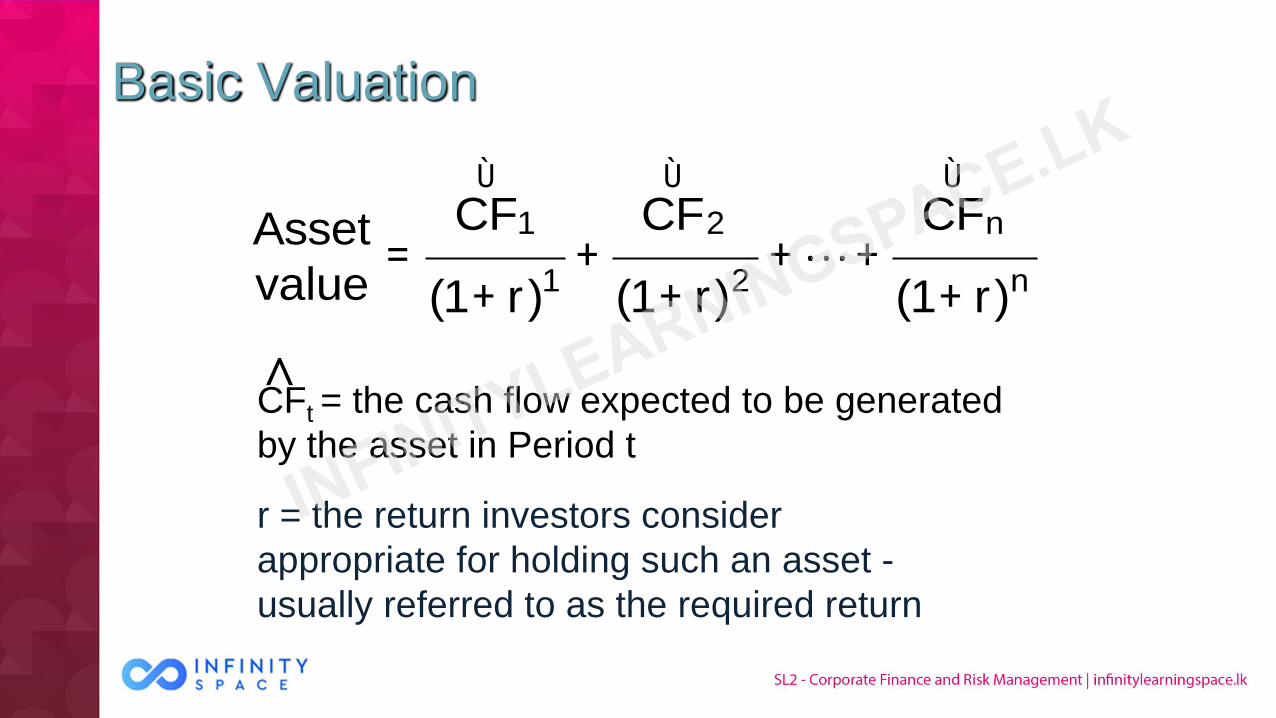

CFt = the cash flow expected to be generated

by the asset in Period t

^

n

n

2

2

1

1

)r1(

CF

)r1(

CF

)r1(

CF

value

Asset

+++

++

+=

ÙÙÙ

3

r = the return investors consider

appropriate for holding such an asset -

usually referred to as the required return

Valuation of Financial Assets - Bonds

✓Bond is a long term debt instrument

✓Value is based on present value of:

✓ Stream of interest payments

✓ Principal repayment at maturity

4

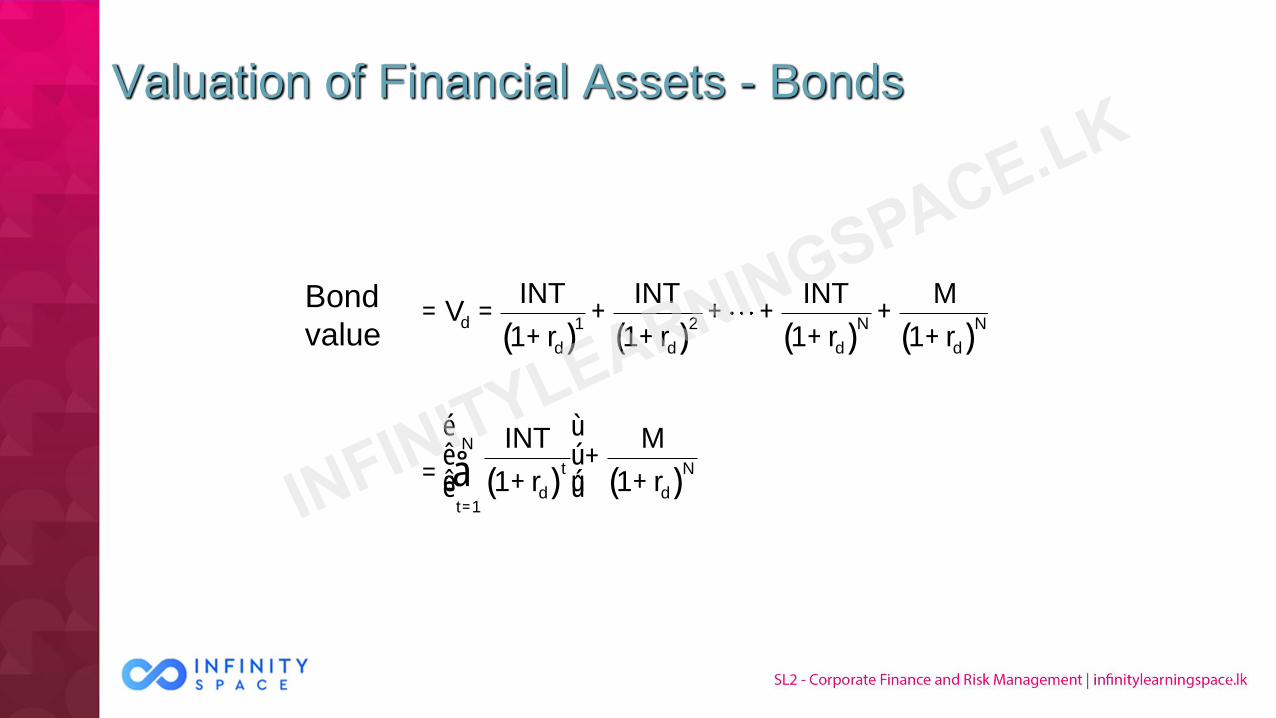

Valuation of Financial Assets - Bonds

✓ rd = required rate of return on a debt instrument

✓N = number of years before the bond matures

✓ INT = dollars of interest paid each year

✓M = par or face, value of the bond to be paid off at maturity

5

Valuation of Financial Assets - Bonds

Bond

value

= Vd =INT

1+ rd( )1

+INT

1+ rd( )2

+ +INT

1+ rd( )N

+M

1+ rd( )N

=

INT

1+ rd( )t

t=1

N

å

é

ë ê ê

ù

û ú ú +

M

1+ rd( )N

6

Valuation of Financial Assets - Bonds

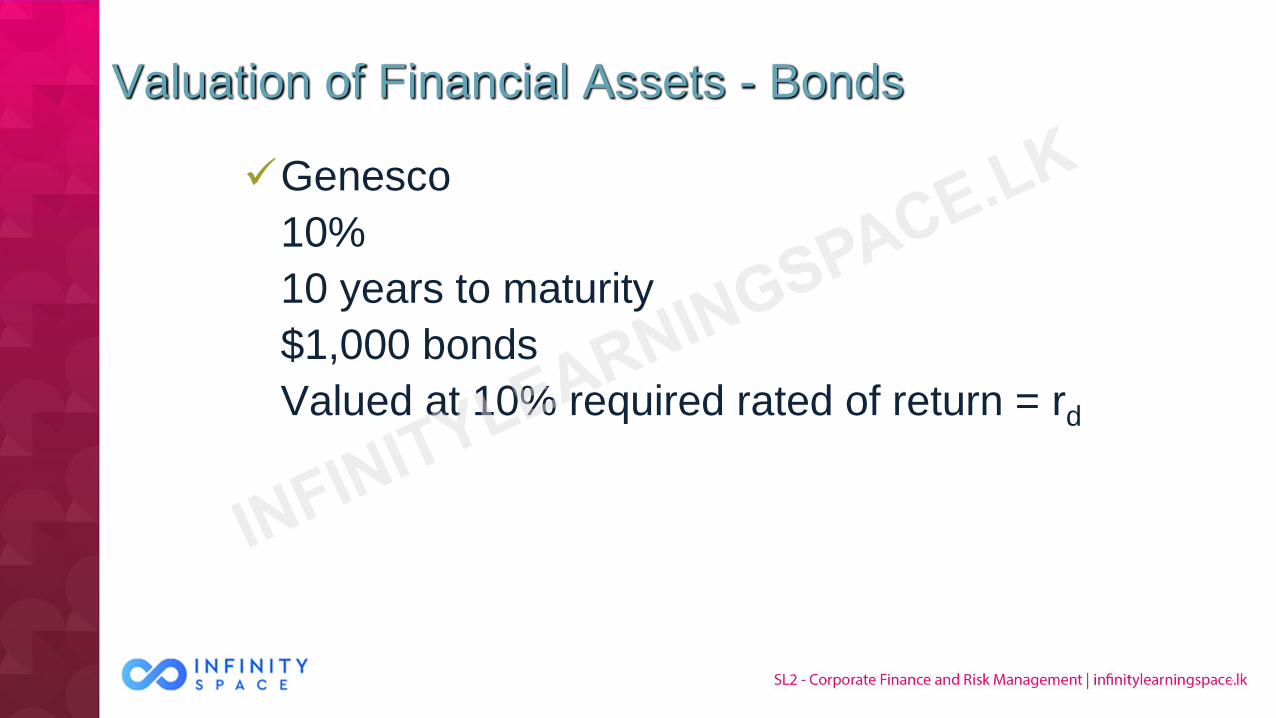

✓Genesco

10%

10 years to maturity

$1,000 bonds

Valued at 10% required rated of return = rd

7

Valuation of Financial Assets - Bonds

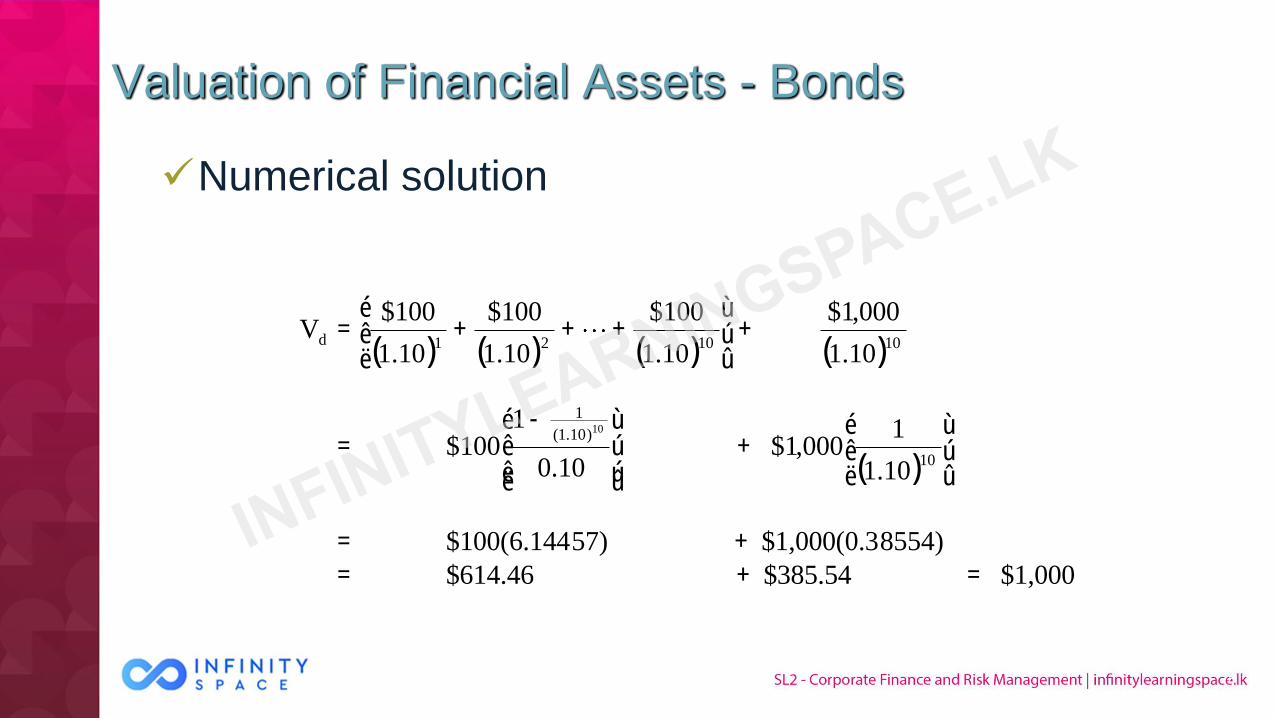

✓Numerical solution

( ) ( ) ( ) ( )

( )

$1,000 $385.54 $614.46

8554)$1,000(0.3 57)$100(6.144

10.1

1000,1$

10.0

1100$

10.1

000,1$

10.1

100$

10.1

100$

10.1

100$V

10

)10.1(

1

101021d

10

=+=

+=

úû

ùêë

é+

úú

û

ù

êê

ë

é -=

+úû

ùêë

é+++=

8

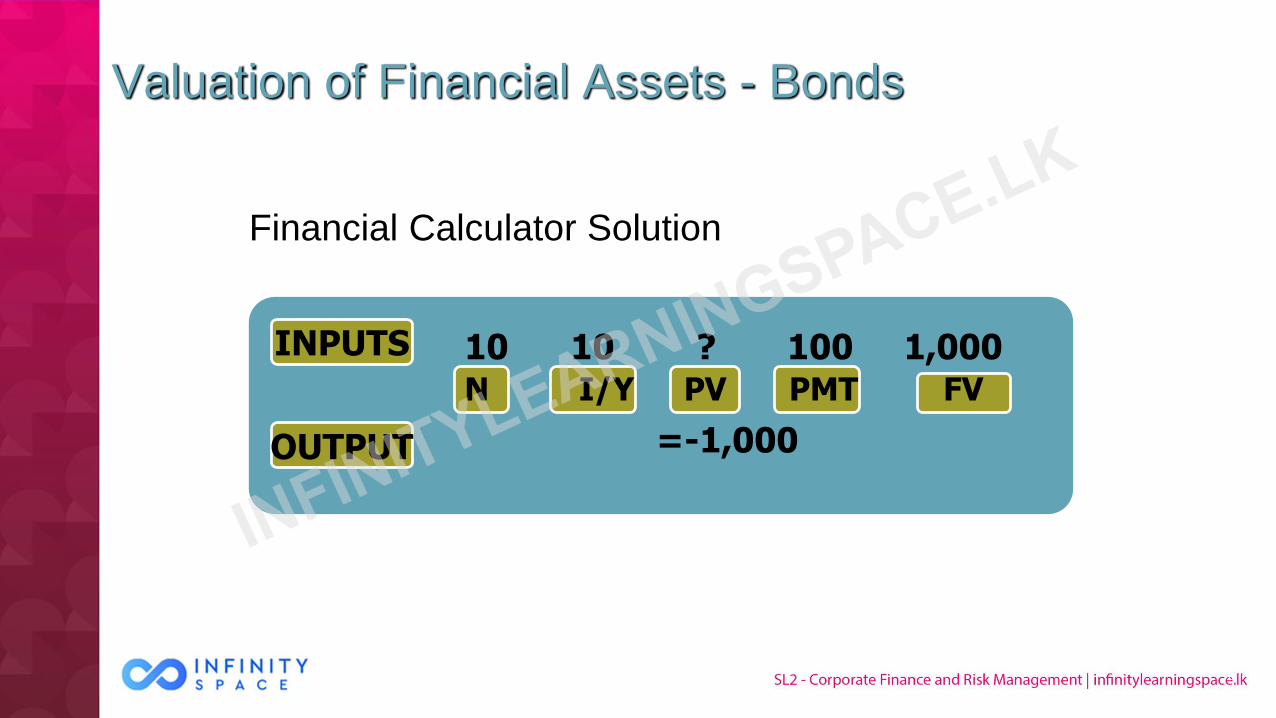

Valuation of Financial Assets - Bonds

Financial Calculator Solution

9

INPUTS

OUTPUT

10 10 ? 100 1,000N I/Y PV PMT FV

=-1,000

Changes in Bond Values over Time

✓If the market rate associated with a bond

(rd) equals the coupon rate of interest, the

bond will sell at its par value

10

Changes in Bond Values over Time

✓ If interest rates in the economy fall after the bonds are

issued, rd is below the coupon rate. The interest

payments and maturity payoff stay the same, causing the bond’s value to increase (investors demand lower

returns, so they are willing to pay higher prices to

receive the same cash flows).

11

Changes in Bond Values over Time

✓Current yield is the annual interest payment on

a bond divided by its current market value

12

Changes in Bond Values over Time

✓Discount bond

✓ A bond that sells below its par value, which occurs whenever the

going rate of interest rises above the coupon rate

✓ Premium bond

✓ A bond that sells above its par value, which occurs whenever the

going rate of interest falls below the coupon rate

13

Changes in Bond Values over Time

✓ An increase in interest rates will cause the price of an

outstanding bond to fall

✓ A decrease in interest rates will cause the price to rise

✓ The market value of a bond will always approach its par

value as its maturity date approaches, provided the firm

does not go bankrupt

14

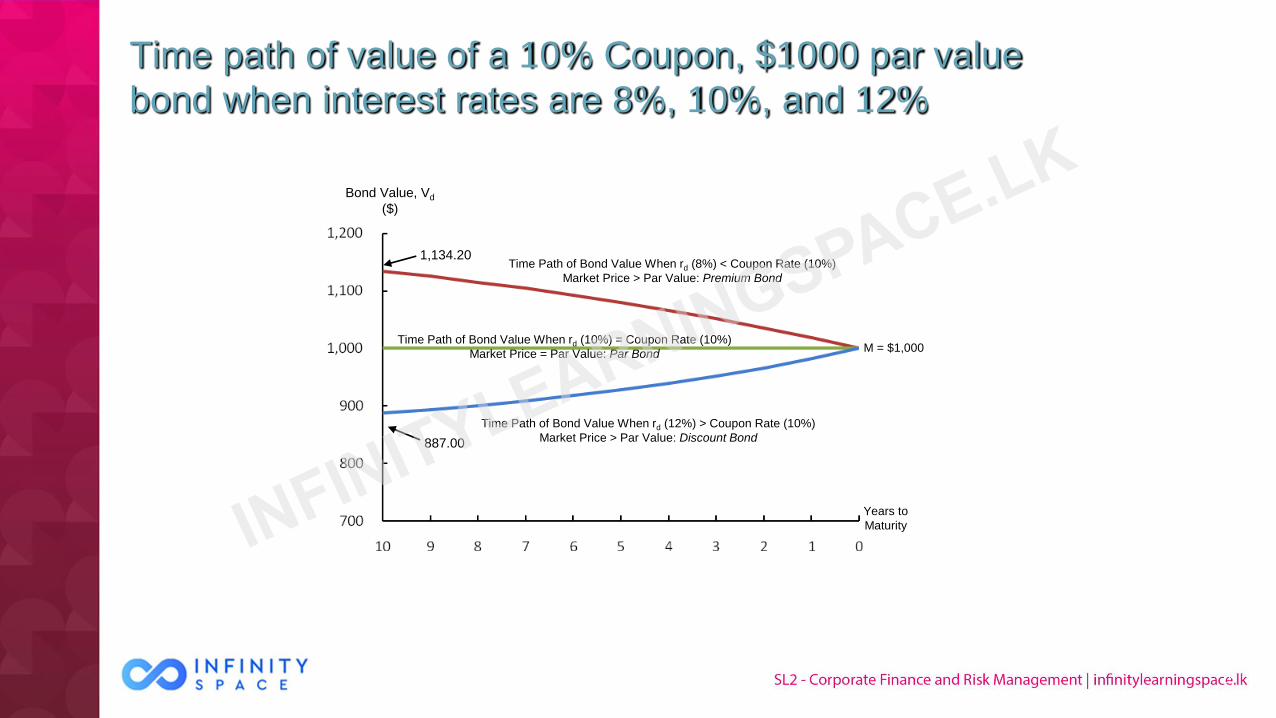

Time path of value of a 10% Coupon, $1000 par value

bond when interest rates are 8%, 10%, and 12%

15

Years to

Maturity

Bond Value, Vd

($)

1,134.20Time Path of Bond Value When rd (8%) < Coupon Rate (10%)

Market Price > Par Value: Premium Bond

Time Path of Bond Value When rd (10%) = Coupon Rate (10%)

Market Price = Par Value: Par Bond

Time Path of Bond Value When rd (12%) > Coupon Rate (10%)

Market Price > Par Value: Discount Bond

M = $1,000

887.00

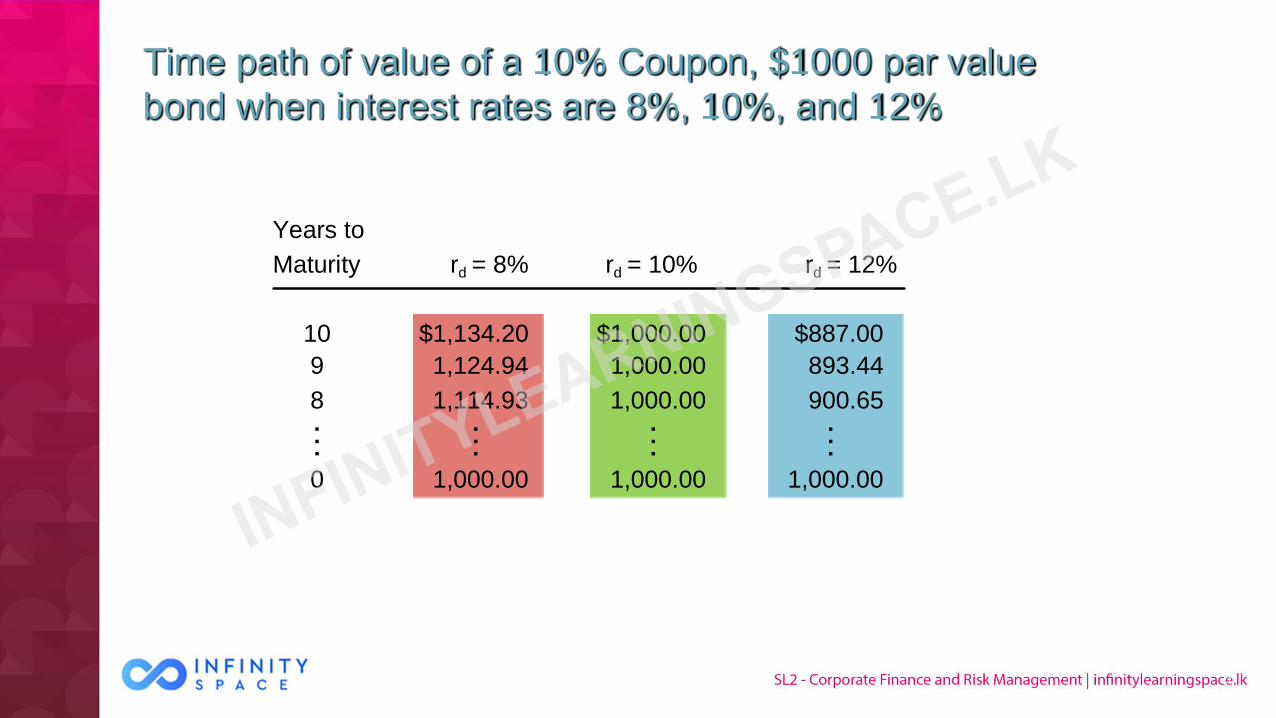

Time path of value of a 10% Coupon, $1000 par value

bond when interest rates are 8%, 10%, and 12%

16

Years to

Maturity rd = 8% rd = 10% rd = 12%

10 $1,134.20 $1,000.00 $887.00

9 1,124.94 1,000.00 893.44

8 1,114.93 1,000.00 900.65 . . . . . . . . . . . .

0 1,000.00 1,000.00 1,000.00

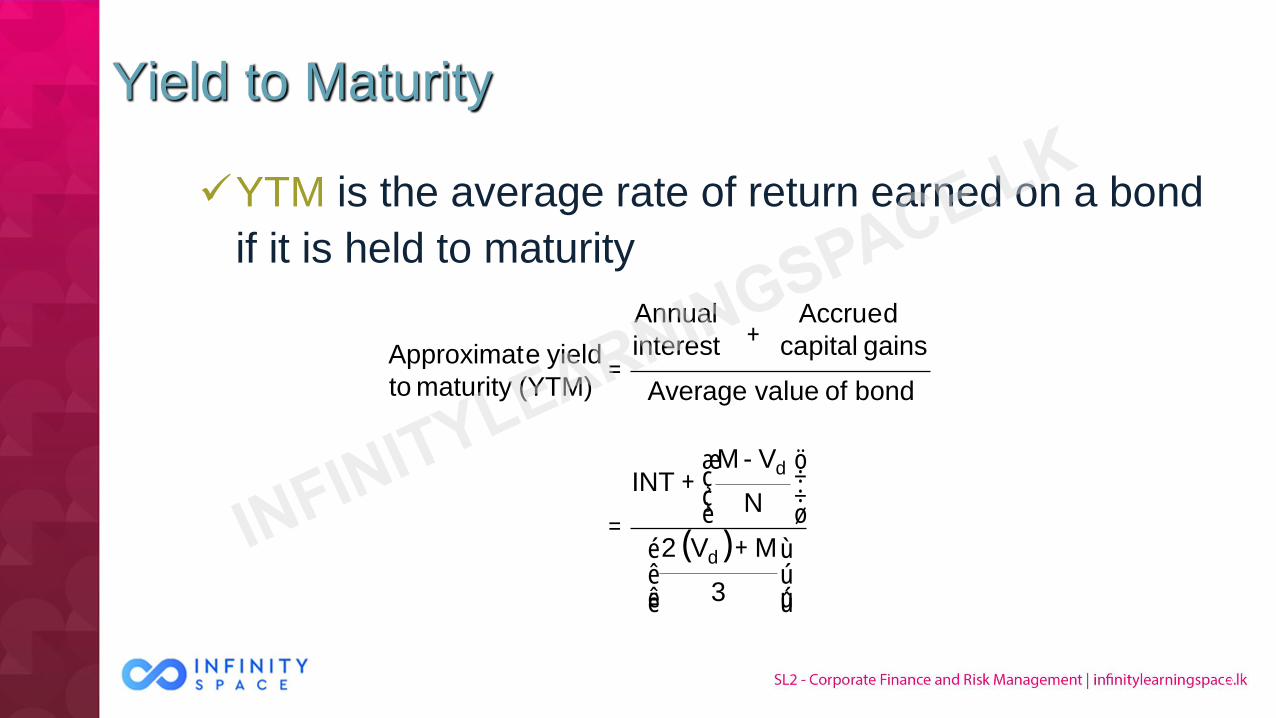

Yield to Maturity

✓YTM is the average rate of return earned on a bond

if it is held to maturity

( )

úúû

ù

êêë

é +

÷÷

ø

ö

çç

è

æ+

=

+

=

3

M V 2

N

V-M INT

bond of value Average

gains capital interest

d Accrue

Annual

(YTM)maturity to

yieldeApproximat

d

d

17

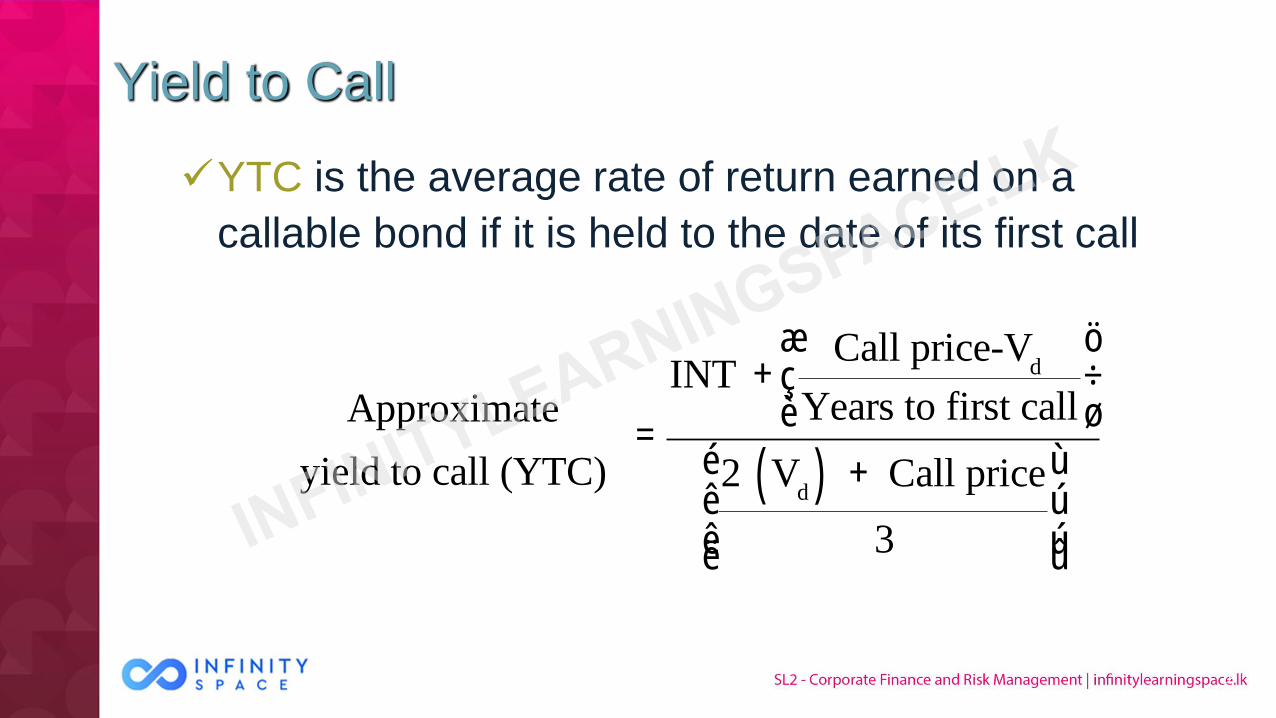

Yield to Call

✓YTC is the average rate of return earned on a

callable bond if it is held to the date of its first call

Approximate

yield to call (YTC)=

INT +Call price-V

d

Years to first call

æ

èç

ö

ø÷

2 Vd( ) + Call price

3

é

ë

êê

ù

û

úú

18

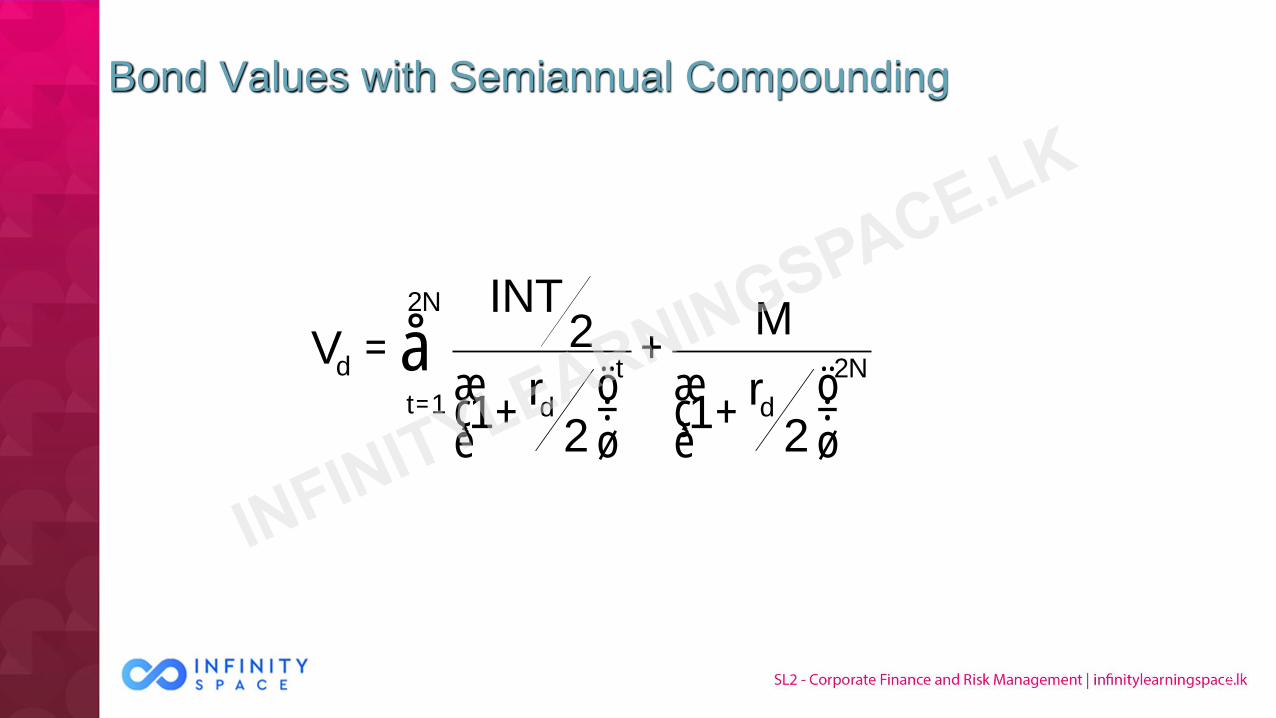

Bond Values with Semiannual Compounding

Vd =INT

2

1+rd

2æ

è ç

ö

ø ÷

t+

t=1

2N

åM

1+rd

2æ

è ç

ö

ø ÷

2N

19

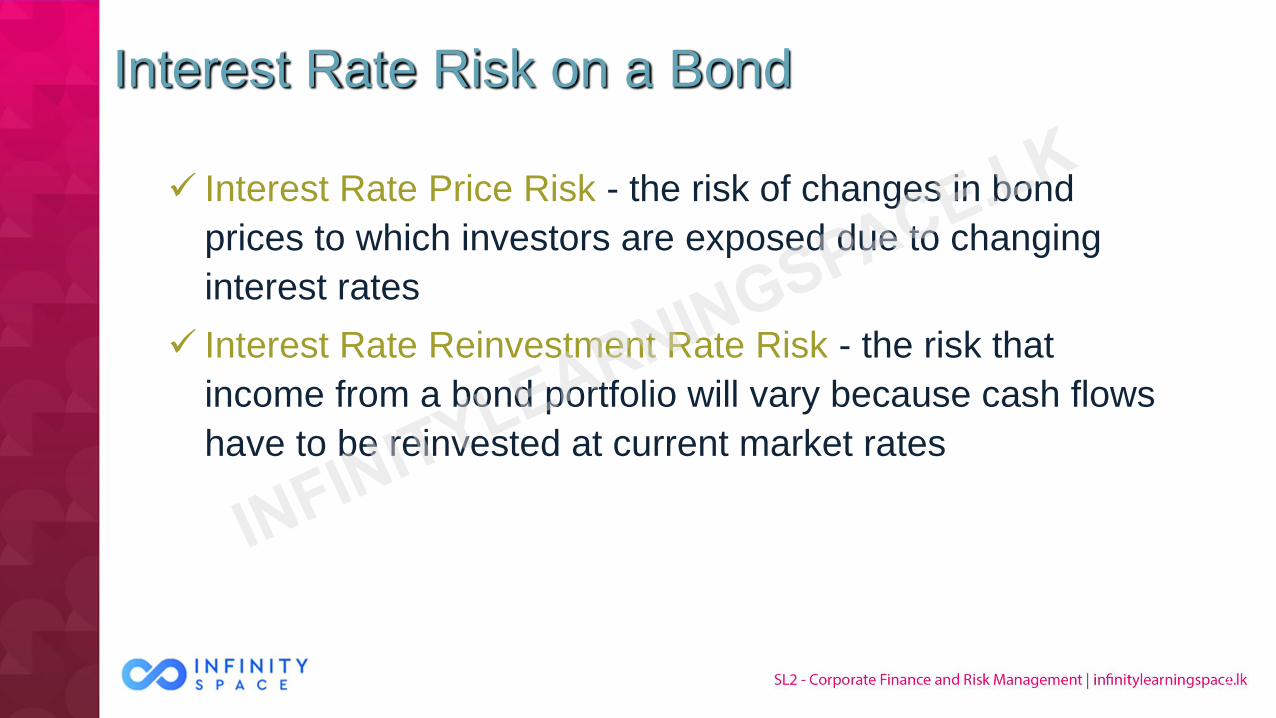

Interest Rate Risk on a Bond

✓ Interest Rate Price Risk - the risk of changes in bond

prices to which investors are exposed due to changing

interest rates

✓ Interest Rate Reinvestment Rate Risk - the risk that

income from a bond portfolio will vary because cash flows

have to be reinvested at current market rates

20