Embed Size (px)

Citation preview

Perekonomian Indonesia Melambat?

Anton H. Gunawan

Chief Economist

PT. Bank Mandiri (Persero), Tbk.

Indonesia Macro Economic Overview: Great Picture, But………

2

3

24.6

7.9

2011 2012 2013 2014 2015 2016 f2017

3

3.02

4.2

4.75

2

3

4

5

6

7

8

1Q15 3Q15 1Q16 3Q16 2017F

Inflation 7 Days RR

4.96 5.04

4.66

5.04

5.18

5.02 5.10

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

20

17

F

14,603

13,173 13,051

13,473 13,400

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 2017F

10-12

GDP growth (% yoy) Inflation and policy rate (%) Loan growth (% yoy)

Currency (USDIDR) Fiscal Balance (% to GDP)

Domestic economic growth will slightly improved this year Inflation will accelerated but still at a manageable level, thus policy rate will be kept at 4.75%

Source : Bloomberg, CEIC, Bank Mandiri forecast

-1.1

-1.8

-2.2 -2.2

-2.6 -2.5 -2.6

2011 2012 2013 2014 2015 2016 2017F

Current Account Balance (% to GDP)

0.2

-2.8 -3.2

-3

-2.1 -2 -1.7

2011 2012 2013 2014 2015 2016 2017F

GDP growth (% yoy) Source of growth (%)

Economic growth was stable at 5.01% in 2Q17 Investment improved but government spending weakened

Source : BPS

25

Components growth (%)

Proportions (%)

5.19

5.01

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

Private Cons Exp NP Inst Cons Exp

Gov exp Investments

Net Export Ch in Stcks, stt discr

2016 2Q16 1Q17 2Q17

Household Exp 5.01 5.07 4.93 4.95

NP Inst Exp 6.62 6.71 8.02 8.33

Gov Exp -0.15 6.23 2.71 -1.94

Investments 4.48 4.18 4.81 5.35

Exports -1.74 -1.52 8.04 0.27

Imports -2.20 30.79 5.74 7.39

Net Exports 0.07 -2.18 16.90 12.33

GDP Growth 5.02 9.13 5.01 5.01

2016 2Q16 1Q17 2Q17 Household Exp 54.35 53.68 55.06 53.65 NP Inst Exp 1.12 1.09 1.14 1.13 Gov Exp 8.21 7.96 5.98 7.44 Investments 32.25 31.55 31.99 31.66 Exports 20.88 20.97 21.89 20.64 Imports 16.55 16.59 17.01 18.52 Net Exports 4.33 4.38 4.88 4.88

Agriculture (% yoy) Mining (% yoy) Industrial Processing (% yoy)

Construction Trading

Primary sectors Secondary sector

Transportation Communication Financial Services

Tertiary sectors

Industries shown mixed performance in 2Q17 compared to 1Q17 Industrial processing sector grew slower in 2Q17. Construction sector growth up but its employment down

Source : BPS 5

1.47

3.44 3.03

5.31

7.12

3.33

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

1.2 1.15

0.29

1.6

-0.64

2.24

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

4.68 4.63 4.52

3.36

4.21

3.54

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

6.76

5.12 4.95 4.21

5.95 6.96

1Q162Q163Q164Q161Q172Q17

4.15 4.1 3.59

3.9

4.96

3.78

1Q162Q163Q164Q161Q172Q17

7.9 6.91

8.26 7.85 8.03 8.37

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

7.58

9.33 8.95 9.57 9.1

10.88

1Q162Q163Q164Q161Q172Q17

9.32

13.59

9.04

4.18

5.99 5.94

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

5.58

5.19 5.01

4.0

4.5

5.0

5.5

6.0

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

5.35

4.95

4.0

4.5

5.0

5.5

6.0

-

2.0

4.0

6.0

8.0

10.0

12.0

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

Investment (LHS) Household consumption (RHS)

9.8

7.9

5.3

3

4

5

6

7

8

9

10

11

Feb

-07

Au

g-0

7

Feb

-08

Au

g-0

8

Feb

-09

Au

g-0

9

Feb

-10

Au

g-1

0

Feb

-11

Au

g-1

1

Feb

-12

Au

g-1

2

Feb

-13

Au

g-1

3

Feb

-14

Au

g-1

4

Feb

-15

Au

g-1

5

Feb

-16

Au

g-1

6

Feb

-17

GDP growth (% YoY) Investment and household cons growth (% YoY)

Unemployment (%) Employment (mn people)

Economic growth and employment absorption (1/2)

Every 1% growth only creates approximately 400 thousand employment

Source : BPS

GDP has only been growing by 5-5.5% not enough to absorb labor force

House hold consumption had been slowing since 2012

89

118

60

70

80

90

100

110

120

130

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Tahun GDP Growth (% YoY) Employment (mn

people) Emplyment addition (mn

people) Employment addition to

GDP (th people)

2004 5.03 93.72 2.94 583.82

2005 5.69 93.96 0.24 41.52

2006 5.50 95.46 1.50 272.42

2007 6.35 99.93 4.47 705.01

2008 6.01 102.55 2.62 436.09

2009 4.63 104.87 2.32 500.75

2010 6.22 108.21 3.34 536.18

2011 6.49 109.67 1.46 225.52

2012 6.26 110.81 1.14 181.65

2013 5.73 110.80 (0.00) (0.72)

2014 5.01 114.63 3.82 763.78

2015 4.88 114.82 0.19 39.20

2016 5.02 118.41 3.59 716.33

Economic growth and employment absorption (2/2)

In the past 5 years, every 1% growth increase in GDP resulted in addition of employment of 320 th people

In the past 10 years, every 1% growth increase in GDP resulted in addition of employment of 410 th people

1.13

3.05

3.88

9.27

-8

-6

-4

-2

0

2

4

6

8

10

12

14

16

18

20

0

5

10

15

20

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Jul-1

4

Nov

-14

Mar

-15

Jul-1

5

Nov

-15

Mar

-16

Jul-1

6

Nov

-16

Mar

-17

Jul-1

7

Volatile Food (LHS) Core Inflation (RHS) Headline Inflation (RHS) Administered (RHS)

Source: BPS

(%) (%) Inflation by components

Core Inflation remained subdued a weak domestic demand

(4.68)

(2.4)

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

Goods Services

Primary Income Secondary Income

CAD

16.0%

27.9%

-17.2%

-30%

-20%

-10%

0%

10%

20%

30%

-0.7

-0.2

0.3

0.8

1.3

1.8

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

May

-17

Tho

usa

nd

s

Trade balance (USD bn)-LHS

Export growth-RHS

Import growth-RHS

-0.99 -0.87

-1.9

BOP (USD bn) Trade Balance

CAD to GDP ratio improved since 3Q16-1Q17 from -1.9 to

0.99%

Part of it because weakening imports

Current account deficit improved since 2014, but ….

But the improvement was also because of weakening imports of capital goods

Import Growth (% YoY)

% to GDP

13.76 17.34

(1.93)

(60)

(40)

(20)

-

20

40

60

Jun

-14

Sep

-14

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

Consumption Raw materials

Capital goods

Imports of capital goods and raw materials weakened

sharply

Source : BPS

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

-20%

-10%

0%

10%

20%

30%

40%

Mar

-12

Jul-

12

No

v-1

2

Mar

-13

Jul-

13

No

v-1

3

Mar

-14

Jul-

14

No

v-1

4

Mar

-15

Jul-

15

No

v-1

5

Mar

-16

Jul-

16

No

v-1

6

Mar

-17

VAT Growth GDP growth

629 676 760 752

865 893

Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17

72 79 84 78

139 145

Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17

GDP growth and value added tax growth

6M accumulation of government spending

6M accumulation of material and capital expenditure

Government spending realization (IDR tn)

Value added tax growth is in the process of returning to its normal pattern, and government capital expenditures jumped since last year

Source : BPS

21.2% 22.7%

23.6%

15.1%

27.2% 29.5%

% of budget

% of budget

40.7%

39.2%

40.5% 37.9%

41.5% 42.9%

Abnormal pattern due to “ijon”

Selected Indicators of the Real Sector (some Micro-data)

11

Agriculture, Forestry and Fishing

Mining and Quarrying

Manufacturing

Electricity and Gas

Water supply, Sewerage, Waste Management and Remediation

Activities

Construction

Wholesale and Retail Trade, Repair of Motor Vehicle

and Motorcycles

Transportation and Storage

Accommodation and Food Service Activities

Information and Communication

Financial and Insurance Activities

Real Estate Activities

Business Activities

Public Administration and Defence, Compulsory Social

Security

Education

Human Health and Social Work Activities

Other Services Activities

-2%

0%

2%

4%

6%

8%

10%

12%

-5% 0% 5% 10% 15% 20% 25%

12

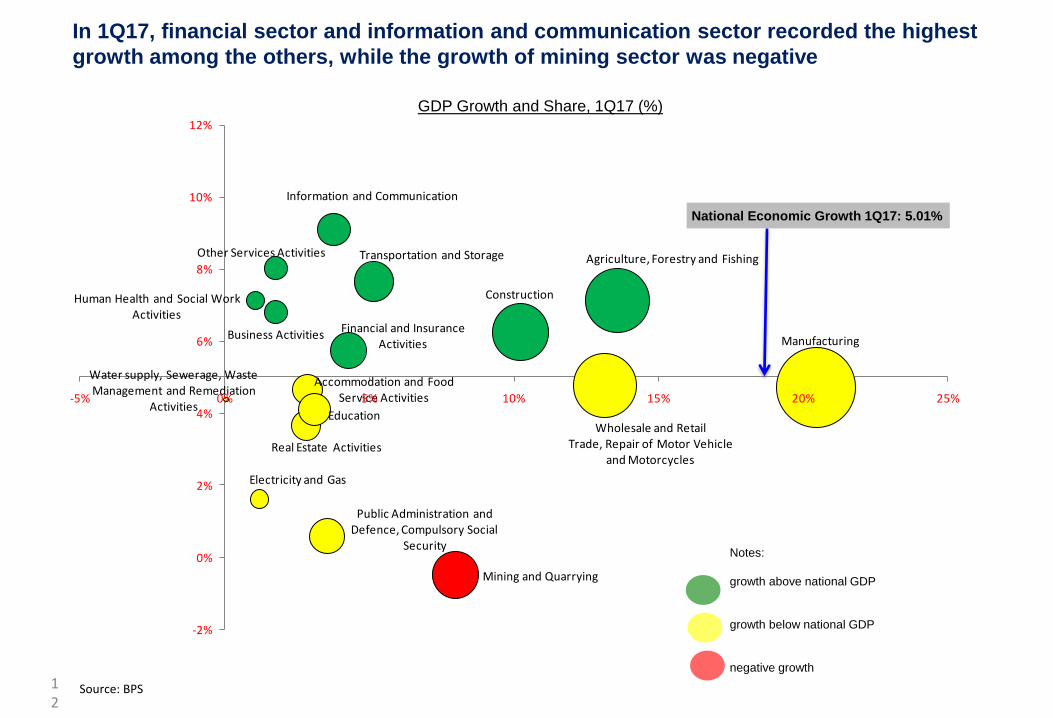

In 1Q17, financial sector and information and communication sector recorded the highest growth among the others, while the growth of mining sector was negative

GDP Growth and Share, 1Q17 (%)

Source: BPS

Notes: growth above national GDP growth below national GDP negative growth

National Economic Growth 1Q17: 5.01%

Agriculture, Forestry & Fishing Mining & Quarrying

Manufacturing

Electricity & Gas

Water Supply, Sewerage, Waste Management & Remediation

Construction

Wholesale & Retail Trade, Repair of motor vehicles

Transportation & Warehousing

Accommodation & Food Service

Information & Communication

Financial & Insurance

Real Estate

Business Activities

Public Adm. & Defence, Compulsory Social Securities

Education

Human Health & Social Work Activities

Other Service Activities

-6

-4

-2

0

2

4

6

8

10

12

14

-5 0 5 10 15 20 25

Gro

wth

, % y

oy

Share Nominal (%) 13

In 2Q2017, information and communication sector recorded the highest growth among the others, while the growth of electricity & gas sector and public administration are the lowest (negative growth)

GDP Growth and Share, 2Q2017 (%)

Source: BPS

Notes: growth above national GDP growth below national GDP negative growth

National Economic Growth 2Q2017:5.01%

Agriculture, Forestry & Fishing

Mining and Quarrying

Manufacturing

Electricity & Gas

Water Supply, Sewerage, Waste Management & Remediation

Construction

Wholesale & Retail Trade, Repair of motor vehicles

Transportation & Warehousing

Accommodation &Food Service

Information & Communication

Financial & Insurance

Real Estate

Business Activities

Public Adm. & Defence, Compulsory Social Securities

Education

Human Health & Social Work Activities

Other Service Activities

-2

0

2

4

6

8

10

12

-5 0 5 10 15 20 25

Gro

wth

, % y

oy

Share Nominal (%) 14

In 1H2017, information and communication sector recorded the highest growth among the others, while the growth of electricity and gas sector is the lowest

GDP Growth and Share, 1H2017 (%)

Source: BPS

Notes: growth above national GDP growth below national GDP negative growth

National Economic Growth 1H2017:5.01%

15

Economic Growth by Sector

Sector (%, YoY) 2011 2012 2013 2014 2015 2016 1Q17 2017F

Agriculture, Livestock, Forestry and Fisheries 4.0 4.6 4.2 4.2 3.8 3.3 7.1 4.1

Mining and Quarrying 4.3 3.0 1.7 0.4 -3.4 1.1 -0.5 0.5

Manufacturing Industries 6.3 5.6 4.5 4.6 4.3 4.3 4.2 4.8

Electricity and Gas 5.7 10.1 5.2 5.9 0.9 5.4 1.6 6.4

Water Supply, Waste Treatment and Recycle 4.7 3.3 4.1 5.2 7.1 3.6 4.4 3.5

Construction 9.0 6.6 6.1 7.0 6.4 5.2 6.3 6.7

Wholesale and Retail Trade, Repair of Motor Vehicle and Motorcycles 9.7 5.4 4.7 5.2 2.6 3.9 4.8 4.2

Transportation and Storage 8.3 7.1 8.4 7.4 6.7 7.7 7.6 7.8

Accommodation, Food and Beverages Supply 6.9 6.6 6.8 5.8 4.3 4.9 4.7 5.4

Information and Communication 10.0 12.3 10.4 10.1 9.7 8.9 9.1 9.5

Insurance and Financial Service 7.0 9.5 9.1 4.7 8.6 8.9 5.7 9.0

Real Estate 7.7 7.4 6.5 5.0 4.1 4.3 3.7 4.5

Company Services 9.2 7.4 7.9 9.8 7.7 7.4 6.8 7.7

Gov't Administration, Defense, Social Security 6.4 2.1 2.4 2.4 4.6 3.2 0.6 4.5

Education Service 6.7 8.2 8.2 5.5 7.3 3.8 4.1 4.7

Health and Social Services 9.3 8.0 7.8 8.0 6.7 5.0 7.1 6.8

Other Services 8.2 5.8 6.4 8.9 8.1 7.8 8.0 8.0

Gross Domestic Product (GDP) 6.2 6.0 5.6 5.0 4.9 5.0 5.0 5.1

Sectoral sales performance: Slow recovery

16

Sector

Indicator

Growth (% yoy) Growth Jun-17

(%mom) Cum 1H17

Cum 1H16

Jun-17

May-17

Jun-16

2016 2015

Retail1

Ramayana sales (IDR)

14.2 27.0 30.1 7.2 97.7 5.8 -2.0 200.1

Ace Hardware sales (IDR)

17.2 6.4 32.2 17.1 14.7 4.8 4.7 17.4

Automotive2

Total car sales (Unit)

0.3 1.3 -27.4 5.9 11.3 4.9 -16.1 -29.2

Commercial vehicle (Unit)

8.4 -29.0 2.9 46.3 -

32.0 -27.4 -15.8 -32.3

Passenger vehicle (Unit)

-1.7 12.7 -32.7 -1.7 25.1 17.0 -

16.2 -28.3

Total motorcycle sales (Unit)

-8.9 -6.7 -26.9 15.2 -9.7 -8.5 -17.6 -28.6

Property3

Total marketing sales of eight companies (IDR)

1.3 -39.6 -34.2 7.0 n.a. -10.0 -4.3 -41.5

Cement4

Total sales (Ton)

-1.3 2.7 -26.8 7.0 1.4 -0.6 3.5 -31.9

Heavy Equipment

5

Total sales (Unit)

69.6 -24.7 49.4 68.7 16.8 2.7 -39.5 -12.9

Agro segment (Unit)

121.6 -46.8 161.5 473.6 -

58.4 -26.7

-

63.2 -28.3

Construction segment (Unit)

-25.7 19.9 70.8 -55.9 -

10.3 31.2

-

22.3 22.9

Forestry segment (Unit)

61.5 -48.3 49.4 5.4 -

30.7 -31.5 -9.3 -12.9

Mining segment (Unit)

267.6 -45.1 29.1 367.8 5.6 6.2 -

49.9 -18.6

Sea Transport6

Loading and unloading activities in the five main ports (Ton)

2.0 a)

-3.3b)

11.2

c)

9.3d)

-7.3

e)

-1.3 -8.2 7.4 c)

CPO6

Volume of exports (Ton)

5,3 a)

-11,3

b)

4,1 c)

-

15,0d)

-24,2

e)

-14,0 -10,1 7,2 c)

Value of exports (USD)

29,0

a)

-18,4

b)

6,8 c)

-5,1d)

-

18,6

e)

-6,60

-23,2

3,7 c)

Coal6

Volume of exports (Ton)

8,5 a)

-9,7 b)

8,1 c)

16,8d)

-4,1

e)

0,5 -10,1 -5,3 c)

Value of exports (USD)

52,2

a)

-28,3

b)

60,9

c)

67,2d)

-

25,2

e)

-9,3 -

23,2 -3,1

c)

Notes : a) Jan-May 2017, b) Jan-May 2016, c) May 2017, d)Apr 2017, e) May 2016 Sources: 1) ACE Hardware and Ramayana; 2) CEIC and Gaikindo; 3) Mansek; 4) Kementerian Perindustrian, Kementerian Perdagangan, and ASI. The data are still preliminary; 5) United Tractor; 6) BPS

17

Labor & natural resource industries have a down trend growth; Domestic market industries have an increasing trend growth

Source: BPS

No Industri Proporsi (%) Pertumbuhan (%,YoY)

2014 2015 2016 1Q17 2014 2015 2016 1Q17

1 Batubara dan Pengilangan Migas 11.7 11.1 11.0 11.7 -2.1 -1.1 3.2 0.3

2 Makanan dan Minuman 27.1 28.0 29.1 29.0 9.5 7.5 8.5 8.1

3 Pengolahan Tembakau 4.3 4.3 4.2 4.5 8.3 6.2 1.6 2.9

4 Tekstil dan Pakaian Jadi 6.3 5.8 5.5 5.4 1.6 -4.8 -0.1 0.0

5 Kulit, Barang dari Kulit dan Alas Kaki 1.2 1.2 1.3 1.4 5.6 4.0 8.2 7.4

6 Kayu, Barang dari Kayu dan Gabus dan Barang Anyaman dari Bambu, Rotan dan Sejenisnya

3.3 3.1 3.1 3.1 6.1 -1.6 1.8 -2.2

7 Kertas dan Barang dari Kertas; Percetakan dan Reproduksi Media Rekaman 3.8 3.6 3.6 3.5 3.6 -0.2 2.2 4.7

8 Kimia, Farmasi dan Obat Tradisional 8.3 8.5 8.6 8.8 4.0 7.6 5.5 8.3

9 Karet, Barang dari Karet dan Plastik 3.9 4.0 3.5 3.5 1.2 5.0 -8.3 7.5

10 Barang Galian bukan Logam 3.4 3.4 3.5 3.4 2.4 6.0 5.5 3.7

11 Logam Dasar 3.9 4.0 3.8 3.5 6.0 6.2 0.8 -3.0

12 Barang Logam; Komputer, Barang Elektronik, Optik dan Peralatan Listrik 9.6 10.0 10.0 9.4 2.9 7.8 4.3 2.6

13 Mesin dan Perlengkapan 1.4 1.5 1.5 1.6 8.7 7.6 5.1 3.5

14 Alat Angkutan 9.6 9.4 9.4 9.1 4.0 2.4 4.5 2.7

15 Furnitur 1.3 1.3 1.2 1.3 3.6 5.2 0.5 3.9

16 Pengolahan Lainnya; Jasa Reparasi dan Pemasangan Mesin dan Peralatan 0.9 0.9 0.8 0.8 7.7 4.7 -2.9 -0.4

Total 100.0 100.0 100.0 100.0 4.6 4.3 4.3 4.2

18

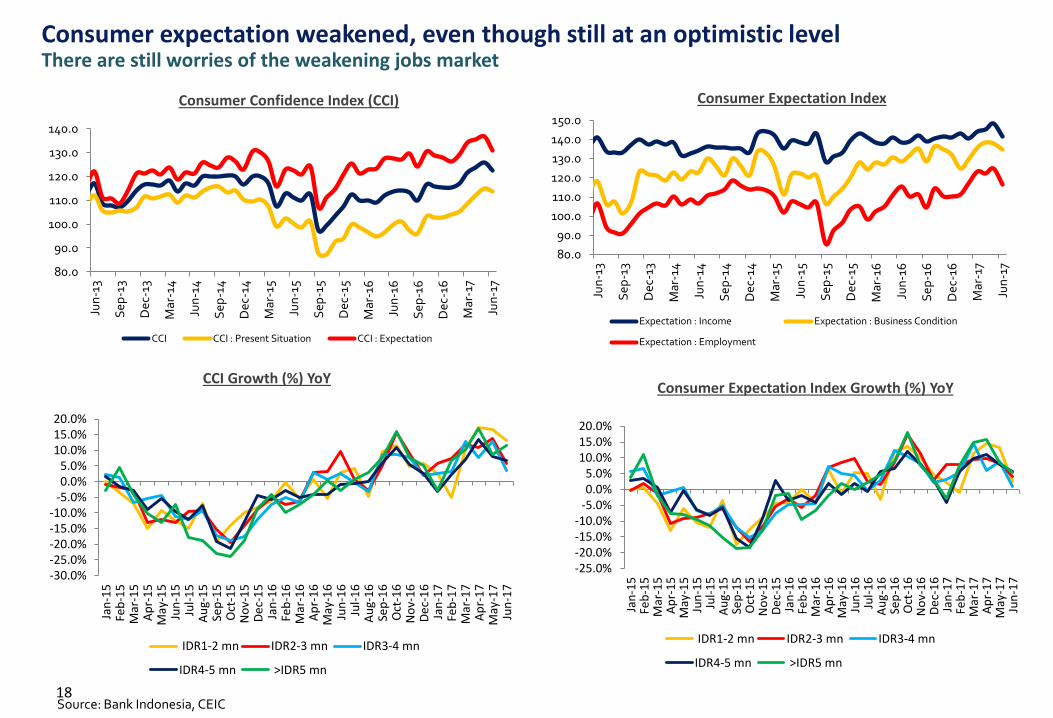

Consumer Expectation Index Growth (%) YoY CCI Growth (%) YoY

Consumer Confidence Index (CCI) Consumer Expectation Index

Source: Bank Indonesia, CEIC

Consumer expectation weakened, even though still at an optimistic level There are still worries of the weakening jobs market

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

CCI CCI : Present Situation CCI : Expectation

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Expectation : Income Expectation : Business Condition

Expectation : Employment

-30.0%-25.0%-20.0%-15.0%-10.0%

-5.0%0.0%5.0%

10.0%15.0%20.0%

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-

15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6M

ay-1

6Ju

n-1

6Ju

l-1

6A

ug-

16

Sep

-16

Oct

-16

No

v-1

6D

ec-

16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7M

ay-1

7Ju

n-1

7

IDR1-2 mn IDR2-3 mn IDR3-4 mn

IDR4-5 mn >IDR5 mn

-25.0%-20.0%-15.0%-10.0%

-5.0%0.0%5.0%

10.0%15.0%20.0%

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-

15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6M

ay-1

6Ju

n-1

6Ju

l-1

6A

ug-

16

Sep

-16

Oct

-16

No

v-1

6D

ec-

16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7M

ay-1

7Ju

n-1

7

IDR1-2 mn IDR2-3 mn IDR3-4 mn

IDR4-5 mn >IDR5 mn

Groceries growth has decreased, which may reflect that the low income group has weaker purchasing power

19

20

Again, retail and food industries have a decreasing ternd, which may reflect that the low income group has weaker purchansing power

5.8

27.0

14.2

5.8 5.0

9.7

2016 1H16 1H17

RALS RALS_sa

4.8 6.4

17.2

5.2 5.2

15.5

2016 1H16 1H17

ACES ACES_sa

Ramayana Semi Annualy Sales growth (%)

ACE Hadware Semi Annualy Sales growth (%)

Furniture and householdappliances

Televisi, radio andelectrionics appliance

Computer andcommunication

apparatus

(Rp

Tri

llio

n)

2012 2013 2014 2015 2016 Jun-17

13

2.7

13

3.5

14

5.6

13

5.7

15

8.4

14

1.4

Volume (in Million Transaction) Value (in Trillion Rupiah)

2011 2012 2013 2014 2015 2016 1H15 1H16 1H17

Growth of Consumer Loan for Household Apparatus The use of Credit Card to Purchase

The sales performance of the retail companies for middle and high income groups shows mix results

Source : Companies, Bank Indonesia

-30

-20

-10

0

10

20

30

40

50

60

70

0

200

400

600

800

1,000

1,200

1,400

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1H

16

1H

17

%

Tho

usa

nd

un

its

Car Sales Growth Seasonal adjusted growth

-20

-15

-10

-5

0

5

10

15

20

25

30

0

1

2

3

4

5

6

7

8

9

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1H

16

1H

17

%

Mill

ion

un

its

Motorcycle Sales Growth Seasonal adjusted growth

Car Sales Growth

Motorcycle Sales Growth

Car and motorcycle sales growth weakened in 1H17 Room for motorcycle sales growth in Indonesia may be tighter as 71% households have already motorcycles

Source : Astra, Gaikindo

23

9.5

18.0

6.6

1.4

-3.4

23.9 21.6

2.2

5.3

18.0

37.3

23.7

14.7

21.5

13.6

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

1H13 1H14 1H15 1H16 1H17

MPPA sales growth ACES sales growth AMRT sales growth

MPPA operating margin ACES operating margin AMRT operating margin

More details on the sales growth and operating margin (%) of retail selected companies: weakening

More details on the tales growth and operating margin (%) of food & beverages selected companies: weakening

24

9.5

17.0

3.7 4.4 4.6

24.7

12.7 14.8

5.1

0.9

23.9

29.4

13.6 14.8

-0.8

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

1H13 1H14 1H15 1H16 1H17

INDF sales growth ULTJ sales growth ROTI sales growth

INDF operating margin ULTJ operating margin ROTI operating margin

Sales growth and operating margin (%) of pharmacy selected companies: also weakening

25

18.9

12.9

4.1

9.6

5.3

3.0

8.7

10.6

17.0

-1.9

9.9 9.1 11.0

18.1

5.8

-5.0

0.0

5.0

10.0

15.0

20.0

1H13 1H14 1H15 1H16 1H17

KLBF sales growth TSPC sales growth KAEF sales growth

KLBF operating margin TSPC operating margin KAEF operating margin

26

9.4

16.1

7.7

1.5

-1.0

17.2

12.9

2.4

11.7

4.3

-5.0

0.0

5.0

10.0

15.0

20.0

1H13 1H14 1H15 1H16 1H17

TGKA sales growth EPMT sales growth

TGKA operating margin EPMT operating margin

Sales growth and operating margin (%) of wholesale selected companies: also weakening

2.9

7.0

1.7 1.1 1.5

0.2 0.7 0.7 0.7 0.7

21.0

6.6

4.0

1.8 1.6 1.5 1.0 0.4 0.8 0.4

-

5.0

10.0

15.0

20.0

25.0

PT PP Exelcomindo BCA Indocement PP Properti Ciputra PerdanaGapura

Mayora SawitSumbermas

BumiResources

MNC

Capex 1H16 Capex 1H17IDR tn

Construction Telco Bank Cement Property

Company

Sector Consumer

Goods CPO Coal Media

+ 637%

-6% yoy

+ 6% + 45% + 85%

+ 54% -47% + 20% -47%

Source : Kontan

The realization of private sector capital expenditure remained weak in 1H17 Companies are still cautious as demand is still weak

An Update on Purchasing Power

28

Household expenditure growth has a decreasing trend, while the younger people proportion is also decreasing

29

Real income of low income group decreases, which implies a weakening purchasing power.

30

Source: BPS

Unfortunately, food subsidy delivery is late making the low income group worse

31

32

Meanwhile, the middle up to high income groups are postponing their spending because consumer confidence is declining

Selected Indicators of the Banking Sector

33

Source : Indonesian banking statistic

Loan growth decelerated while deposit growth increased in May-17 LDR and LFR decreased in May-17, suggesting a better liquidity

Loan and deposit growth Loan to deposit ratio (%) Loan to funding ratio (%)

8.71%

11.18%

3%

6%

9%

12%

15%

18%

21%

24%

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

Loan growth (YoY %)

Deposit growth (YoY %)

91.5

89.1

88.3 Ju

n-1

6

Jul-

16

Au

g-16

Sep

-16

Oct

-16

No

v-16

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-17

May

-17

87.6

86.9

Jun

-16

Jul-

16

Au

g-16

Sep

-16

Oct

-16

No

v-16

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-17

May

-17

NPL Stable in May 17 at 3.07%

35

Non Performing Loans Credit quality (IDR tn)

Source : Indonesian banking statistic, as of May 2017

Special mention fell to IDR219 tn (vs IDR234tn in April 2017)

NPL + special mention

3.07%

1.5%

1.7%

1.9%

2.1%

2.3%

2.5%

2.7%

2.9%

3.1%

3.3%

3.5%

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

8.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

234.4 219.8

150

200

250

300

350

400

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Special mention Sub-standard

Doubtful Loss

7.48%

3.39%

4.02%

4.42%

4.97%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

% N

PL

Agriculture

Mining

Manufacturing

Utilities

Construction

Trade, Hotel, Restaurant

Transportation andTelecommunication

Business Services

Social Services

Consumption Credit

NPLs in Mining, Transportation and Trade-hotel & restaurant are still high

Source: OJK

NPLs by Sector

High NPLs found in Kaltim, Papua Barat, dan Papua

13 August 2017 37

NPL (%) Credit Growth (%) Kredit Value (Rp Triliun)

0.8%

1.4%

1.4%

1.6%

1.6%

1.6%

1.7%

2.1%

1.9%

2.3%

2.3%

2.6%

2.5%

2.3%

2.5%

2.8%

2.6%

3.0%

2.1%

2.6%

2.9%

2.7%

2.9%

2.7%

2.8%

3.4%

3.6%

3.2%

3.4%

3.4%

3.4%

4.5%

4.3%

7.3%

2.9%

0.8%

1.5%

1.5%

1.7%

1.8%

1.8%

1.8%

2.1%

2.3%

2.4%

2.6%

2.7%

2.7%

2.7%

2.8%

2.9%

2.9%

2.9%

3.0%

3.0%

3.1%

3.2%

3.2%

3.3%

3.3%

3.5%

3.6%

3.6%

3.6%

3.8%

3.9%

5.2%

5.4%

9.0%

3.1%

Lainnya

Sulawesi Barat

Kalimantan Tengah

Bengkulu

Maluku

Nusa Tenggara Barat

Maluku Utara

Banten

Kepulauan Riau

Sulawesi Selatan

D.I Yogyakarta

Aceh

Lampung

Nusa Tenggara Timur

Sumatera Utara

Sumatera Barat

Jambi

DKI Jakarta

Bali

Jawa Timur

Kalimantan Selatan

Sulawesi Tengah

Kalimantan Barat

Sulawesi Tenggara

Jawa Tengah

Bangka Belitung

Jawa Barat

Sumatera Selatan

Riau

Gorontalo

Sulawesi Utara

Papua

Papua Barat

Kalimantan Timur

Nasional

Apr-17

2016

13.6%

23.6%

9.1%

10.8%

10.6%

30.9%

12.7%

16.0%

5.4%

9.3%

10.2%

10.0%

7.5%

12.4%

5.4%

7.6%

6.7%

6.8%

9.9%

6.8%

8.6%

11.3%

16.2%

13.5%

9.4%

12.6%

9.1%

9.2%

3.4%

7.5%

6.4%

9.4%

19.2%

0.9%

7.9%

-22.7%

20.9%

17.4%

9.2%

8.8%

24.9%

12.0%

6.6%

3.5%

8.2%

12.8%

11.6%

7.8%

12.8%

10.8%

6.7%

4.3%

11.7%

10.0%

5.8%

11.0%

11.3%

11.4%

10.2%

9.7%

13.1%

9.1%

9.1%

3.1%

7.8%

7.5%

7.1%

13.7%

2.3%

9.5%

55

6

20

16

9

31

6

113

34

104

30

30

45

22

188

44

31

2,117

67

399

43

23

44

18

236

11

364

71

58

10

31

24

10

68

4,377

54

6

22

16

9

31

7

113

33

105

31

31

45

22

191

45

31

2,114

68

389

45

24

44

19

240

10

369

71

58

10

32

24

10

67

4,386

38

579

584

619

717

1,016

1,093

1,744

1,956

4,913

8,175

8,329

9,773

BNLI

BJTM

BTPN

BJBR

BBTN

BNGA

BDMN

PNBN

BBNI

BMRI

BBCA

BBRI

22

6

4

9

86

33

26

14

10

9

7

BJTM

BTPN

BJBR

BBTN

BNGA

BDMN

PNBN

BBNI

BMRI

BBCA

BBRI

Net profit (IDR bn) Net profit growth (% yoy)

Average net profit growth : 16% (yoy)

916

1,023

1,157

1,611

1,717

1,994

2,980

3,106

9,337

10,837

16,015

21,938

BJTM

BJBR

BTPN

BBTN

BNLI

PNBN

BDMN

BNGA

BBNI

BBCA

BMRI

BBRI

4

1

4

11

13

7

3

19

18

1

10

24

BJTM

BJBR

BTPN

BBTN

BNLI

PNBN

BDMN

BNGA

BBNI

BBCA

BMRI

BBRI

PPOP (IDR bn) PPOP growth (% yoy)

Average PPOP growth : 13% (yoy)

112

122

284

320

498

692

848

1,008

1,648

3,143

5,864

10,000

BJBR

BJTM

BBTN

BTPN

BBCA

PNBN

BDMN

BNLI

BNGA

BBNI

BMRI

BBRI

52

-43

-9

5

-65

-20

-33

-60

-10

20

9

36

BJBR

BJTM

BBTN

BTPN

BBCA

PNBN

BDMN

BNLI

BNGA

BBNI

BMRI

BBRI

Provision expense (IDR bn) Provision growth (% yoy)

3.5

4.2

4.3

5.5

5.6

5.6

6.1

6.7

7.2

7.8

7.9

9.6

BNLI

BBTN

PNBN

BMRI

BBNI

BNGA

BBCA

BJBR

BDMN

BJTM

BBRI

BTPN

Net interest margin (%)

5M17 banks performances Weak loan growth and lower NIM compensated by lower provisioning charges

Source : Companies, Mandiri Sekuritas

Policy Recommendations

39

Rekomendasi Kebijakan

1. Penerapan anti-cyclical policy dengan mengefektifkan penerimaan dan belanja negara (APBN) balancing long-run spending push with short-run ones. 2. Mengisi program inter-connnectivity dengan kebijakan meningkatkan industri (industrial policies) yang memperhatikan sisi spatial yang ada.

1. Percepatan pelaksanaan secara efektif sistem voucher untuk program subsidi makanan bagi maskarakat kelompok miskin

2. Menciptakan proyek-proyek padat karya, terutama proyek-proyek yang dibiayai pemerintah (misalnya proyek infrastruktur) agar lebih bisa menyerap tenaga kerja lebih banyak (labor intensive).

3. Tax incentives untuk mendorong sektor industri, terutama sektor industri padat karya dan industri skala menengah-kecil.

4. Penggunaan Dana Desa secara optimal untuk mendorong ekonomi lokal pedesaan sekaligus menciptakan lapangan kerja di desa.

Kebijakan umum:

Kebijakan khusus:

The end of slide Thank you

41