Embed Size (px)

Citation preview

Please refer to Disclosures and Disclaimers at the end of the Research Report.

Pennar Industries Limited Moving up the value chain

MIDCAP | STEEL | Initiating Coverage 29 October 2014

PhillipCapital (India) Pvt. Ltd.

Diversified revenue with vertical and horizontal integration The company diversified its product range within each segment as well as across different segments. It has moved up the value chain — from commodity‐based products to value‐added products, including cold‐rolled‐formed products, precision tubes, profiles, water‐treatment solutions, and building products. Pennar entered the hydraulics business with the acquisition of assets of Wayne‐Burt Petro Chemicals; it will double its capacity over the next year. It is planning to expand its North India reach by setting up a new plant there for manufacturing pre‐fabricated structures. It is also planning to venture into Africa to manufacture pre‐engineered structures (PEBS). Transition from thin‐margin sector to value‐added niches Pennar has progressively evolved its margin profile along with diversification in revenue. The proportion of revenues from value‐added products increased from 15% in FY12 to 50% in FY14. It has enhanced its capacity in the higher‐margin cold‐drawn welded tubes products in FY14, which is expected to improve profitability. Its systems and projects business catering to the railways has high EBITDA margins of 18‐19% and is expected to report revenue CAGR of 15% for FY14‐17. PEBS Pennar’s EBITDA margins are 12‐13% and we expect revenue CAGR of 25% over FY14‐17 to touch Rs 7bn in FY17. Proxy to economic growth recovery Its diverse revenue profile makes it a proxy to overall macroeconomic recovery. It caters to general engineering, auto, white goods, building material, infrastructure, waste water and solar sectors. Its systems and projects business, catering to the railways, expects to ride on demand for wagons, metro rail, and solar structures. It can play a role in setting up warehouses for logistic parks. Pennar Engineered Building Systems provides secular growth It is one of the leading companies in designing, manufacturing, and installing cost‐effective pre‐engineered steel buildings and building components for industries, warehouses, commercial centres, and multi‐storied buildings. PEBS Pennar has reported strong revenue CAGR of 35% over FY11‐14 with revenues increasing from Rs 1.4bn in FY11 to Rs 3.6bn in FY14. We expect revenue CAGR of 25% over FY14‐17 (FY17 revenues at Rs 7.06bn) and EBITDA of Rs 918mn in FY17, contributing to 42% of consolidated operating profits. Valuation Pennar’s valuation is impacted due to economic cycles and steel prices. In the past five years, Pennar has traded at a P/E of 5‐12x and average EV/EBITDA of around 7x. Its revenue profile has changed significantly in favour of value‐added products and the company is in a strong position to capitalise on economic recovery. At CMP of Rs54, the stock trades at 7.2x our FY17 expected earnings and 3.8x EV/EBITDA. We have valued the company at 10x our FY17 EPS of Rs 7.5 to arrive at a price target of Rs 75, translating into EV/EBITDA valuation at 4.9xFY17. We are initiating coverage with a BUY rating.

BUY PSL IN | CMP RS 54 TARGET RS 75 (+40%) Company Data O/S SHARES (MN) : 120MARKET CAP (RSBN) : 7MARKET CAP (USDMN) : 10652 ‐ WK HI/LO (RS) : 60 / 18LIQUIDITY 3M (USDMN) : 1.8FACE VALUE (RS) : 5

Share Holding Pattern, % PROMOTERS : 40.1FII / NRI : 20.9FI / MF : 9.9NON PROMOTER CORP. HOLDINGS : 12.2PUBLIC & OTHERS : 17.0

Price Performance, % 1mth 3mth 1yr

ABS 1.0 40.9 152.3REL TO BSE 1.0 39.1 123.2

Price Vs. Sensex (Rebased values)

Source: Bloomberg, Phillip Capital Research

Other Key Ratios Rs mn FY15E FY16E FY17ENet Sales 13,174 16,110 19,727EBIDTA 1,112 1,563 2,143Net Profit 369 599 907EPS, Rs 3.1 5.0 7.5PER, x 17.6 10.8 7.2EV/EBIDTA, x 7.2 5.3 3.8P/BV, x 1.7 1.5 1.3ROE, % 9.8 14.2 18.3Debt/Equity (%) 44.2 45.3 41.6Source: PhillipCapital India Research Est. Vikram Suryavanshi (+ 9122 6667 9951) [email protected]

0

20

40

60

80

100

120

140

160

Apr‐11 Apr‐12 Apr‐13 Apr‐14

Pennar Ind BSE Sensex

– 2 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Diversified revenue; vertical/horizontal integration Pennar Industries withstood various economic cycles because of its transition from a fabrication company into an engineering company. It has diversified its product range within each segment and across its different segments. It has increased its capacity — in 1988 it manufactured from single location at Isnapur, near Hyderabad, with an installed capacity of 30,000MTPA for cold‐rolled steel strips (CRSS); in FY14 it manufactures in seven locations with a capacity of 240,000 tonnes per annum and is the largest cold‐roll‐formed steel‐section manufacturer in India. Continuous product extension, from cold‐rolled steel strips to fabricated structures and solar module mounting structures helped to increase its addressable market. It introduced products like hydraulic cylinders and pressed components for export and CDW tubes in FY14. It has also successfully acquired and integrated — most notably its acquisition of Nagarjuna Steel, Press Metal, a unit of Tube Investment (TI) near Mumbai, and more recently, its assets of Wayne Burt Petrochemicals, erstwhile Bailey Hydro, for venturing into hydraulic cylinders. It has established a new manufacturing facility at Chennai and set up an assembly unit at Hosur, near Bangalore, to meet the requirements of auto components. Pennar has managed to maintain its existing business well while ensuring that sunrise sectors account for 60% of its revenues. It has developed competence in process by technological alliances with global players like NCI Inc. and Tech Universal. Its major customers include L&T, TATA Motors, Ashok Leyland, ABB, Moser Baer, Schneider Electric, Tata BP Solar, and Reliance Retail. It derived around 20% revenue from longstanding customers (five years or more) in FY14. It invested in capacity addition at its tubes facility, helping grow the division’s revenues. It intends to expand its Chennai operations through capacity enhancements in the manufacture of products and assemblies for its integral coach factory. It is in the process of setting up a new factory in North India to manufacture pre‐fabricated structures. The widened product mix has helped extend the company’s risk profile and cushion the full brunt of the slowdown. Revenue breakup in 1QFY15

Source: Company, PhillipCapital India Research

3%

36%

6%5%

37%

13% Pennar Enviro

Pre‐Engineering Buildings

Systems and Projects

Industrial Componenets

Steel Products

Tubes

– 3 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Engaged in a thin‐margin sector; graduating into value‐added niches Pennar has evolved its margin profile with diversification in revenue. The proportion of revenues from value‐added products increased from 15% in FY12 to 50% in FY14. Its steel business focuses on manufacturing engineering profiles with value‐addition (revenue share of around 55%); steel strips business has less value add. The company has enhanced its capacity in the higher‐margin cold‐drawn welded tubes (CDW) products in FY14, which is expected to improve profitability. The systems and projects business catering to the railways is high margin (EBITDA margin of 18‐19%) and is expected to report revenue CAGR of 15% for FY14‐17. Pennar Engineered Building Systems (PEBS Pennar) has increased its capacity from 60,000MT to 90,000MT, which will drive revenue growth into FY15. EBITDA margins are in the range of 12‐13% and we expect revenue CAGR of 25% over FY14‐17, with revenue increasing from Rs 3.61bn in FY14 to touch Rs 7bn in FY17. It has started offering engineering design services to its US customers, which will improve margins. The improved utilisation in industrial components along with growing opportunities in auto can provide operating leverage. We believe that its focus on creating high‐margin scalable businesses should improve profitability and valuations. EBITDA margins in different segments (FY14)

Source: Company, PhillipCapital India Research

8.2% 8.4%10.2% 10.5%

13.8%

19.3%

0%

5%

10%

15%

20%

25%

Steel Strips Tubes Projects Engg. Profile Industrial Component

Systems

– 4 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

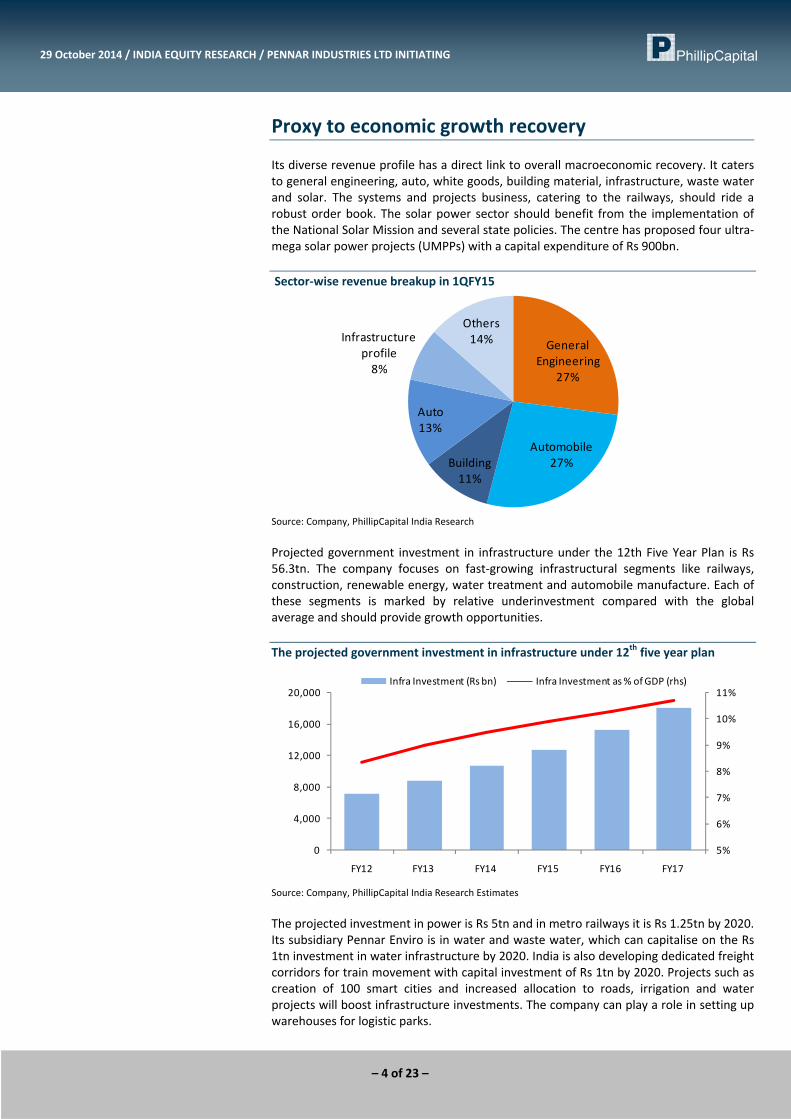

Proxy to economic growth recovery Its diverse revenue profile has a direct link to overall macroeconomic recovery. It caters to general engineering, auto, white goods, building material, infrastructure, waste water and solar. The systems and projects business, catering to the railways, should ride a robust order book. The solar power sector should benefit from the implementation of the National Solar Mission and several state policies. The centre has proposed four ultra‐mega solar power projects (UMPPs) with a capital expenditure of Rs 900bn. Sector‐wise revenue breakup in 1QFY15

Source: Company, PhillipCapital India Research Projected government investment in infrastructure under the 12th Five Year Plan is Rs 56.3tn. The company focuses on fast‐growing infrastructural segments like railways, construction, renewable energy, water treatment and automobile manufacture. Each of these segments is marked by relative underinvestment compared with the global average and should provide growth opportunities. The projected government investment in infrastructure under 12th five year plan

Source: Company, PhillipCapital India Research Estimates The projected investment in power is Rs 5tn and in metro railways it is Rs 1.25tn by 2020. Its subsidiary Pennar Enviro is in water and waste water, which can capitalise on the Rs 1tn investment in water infrastructure by 2020. India is also developing dedicated freight corridors for train movement with capital investment of Rs 1tn by 2020. Projects such as creation of 100 smart cities and increased allocation to roads, irrigation and water projects will boost infrastructure investments. The company can play a role in setting up warehouses for logistic parks.

General Engineering

27%

Automobile27%Building

11%

Auto13%

Infrastructure profile8%

Others14%

5%

6%

7%

8%

9%

10%

11%

0

4,000

8,000

12,000

16,000

20,000

FY12 FY13 FY14 FY15 FY16 FY17

Infra Investment (Rs bn) Infra Investment as % of GDP (rhs)

– 5 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Pennar Engineered Building Systems provides secular growth PEBS, a subsidiary of Pennar Industries, incorporated in January 2008, began commercial operations from January 2010. It is one of the leading companies in design, manufacture, and installation of cost‐effective pre‐engineered steel buildings and building components for industries, warehouses, commercial centres, multi‐storied buildings, aircraft hangers, defence installations, sports stadia, industrial racking systems, cold form steel structure, and solar structure. Pre‐engineered buildings enjoy the advantage of lower overall costs (about 10% lower than conventional buildings) and lower time‐to commissioning (half of conventional buildings). It has manufacturing facility near Hyderabad (29,000 sq. mt.) with a production capacity of 90,000MT per annum. It has set up a 25‐kW solar PV system at the factory in Sadasivpet, Hyderabad, to augment its power supply and reduce its dependence on conventional power. PEBS Pennar has an order book of Rs 3.5bn and has bagged some prestigious projects from companies like Schneider Electric, Ultra Tech, L&T, and Dr Reddy Labs. It has also made a foray into the international markets with some crucial projects in Africa. It has reported strong revenue CAGR of 35% over FY11‐14. We expect revenue CAGR of 25% over FY14‐17 (FY14 revenue of Rs 3.61bn rising to Rs 7.06bn in FY17); EBITDA of Rs 918mn in FY17, contributing to 42% of consolidated operating profits.

Revenue CAGR of 25% FY14‐17 Operating leverage to improve profitability

Source: Company, PhillipCapital India Research Estimates

0

10

20

30

40

50

60

70

80

0

1000

2000

3000

4000

5000

6000

7000

8000

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Revenue (Rs mn)

Revenue Growth (%) (rhs)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0

100

200

300

400

500

600

700

800

900

1000

FY11 FY12 FY13 FY14 FY15 FY16 FY17

EBITDA (Rsmn)EBITDA margin (%) (rhs)

– 6 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Financials In standalone, tubes should report higher revenue CAGR of 27% over FY14‐17 to touch Rs 2.67bn in FY17 with an increase in capacity; we expect 14% CAGR in steel products over FY14‐17 to touch Rs 6.25bn in FY17. Standalone revenue CAGR of 16% FY14‐17e

Source: Company, PhillipCapital India Research Estimates The company reported one of the lowest standalone margins (7.1% in FY14) due to a significant decline in profitability of steel, solar, and tubes. Standalone margins have remained volatile in the past with a high 14.2% in FY10 to a low of 7.1% in FY14 and are a function of economic activity and operating leverage. Standalone EBITDA margins are expected to recover to 9.6% in FY17 with higher contribution from railways, components, and recovery in other business. Standalone profits declined from Rs 699mn in FY11 to Rs 126mn in FY14 with slowdown in economy and margin pressure. We expect profits to recover to Rs 418mn translating into standalone EPS of Rs 3.5 in FY17.

New assets to provide boost to top line and earnings

Source: Company, PhillipCapital India Research Estimates

‐20

‐10

0

10

20

30

40

50

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Revenue (Rs mn) Growth (YoY) (rhs)

0

2

4

6

8

10

12

14

16

0

200

400

600

800

1000

1200

1400

1600EBITDA (Rs mn) EBITDA (%) (rhs)

‐80

‐60

‐40

‐20

0

20

40

60

80

0

100

200

300

400

500

600

700

800 PAT (Rs mn) Growth (YoY) (rhs)

– 7 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Consolidated earnings to report CAGR 21% to Rs 19.2bn We expect revenue CAGR of 22% over FY14‐17 driven by 16% CAGR in standalone and 25% in PEBS; consolidated revenue should touch Rs 19.72bn in FY17. Revenue from PEBS Pennar should be Rs 7.06bn in FY17, contributing to 35% of consolidated revenue compared to 12% in FY11. Pennar Enviro should report a CAGR of 90% over FY14‐17 to touch Rs 1.2bn in FY17 due to a low base and strong order inflow.

Consolidated revenue CAGR of 22% FY14‐17 EBITDA margins to bottom out in FY14

Source: Company, PhillipCapital India Research Estimates

The consolidated margins should recover from 8.4% in FY14 to touch 10.9% in FY17. The increased revenue from PEBS Pennar should improve the margin profile. We have assumed gradual improvement in EBITDA margins from 7% in FY15 to 10% in Pennar Enviro in FY17. We expect EBITDA margins of 13% in FY17 for PEBS Pennar with EBITDA of Rs 918mn. We expect depreciation to increase from Rs 188mn in FY14 to Rs 245mn in FY17 due to an increase in capacity. Interest costs should increase from Rs 265mn in FY14 to Rs 352mn in FY17. Gross long‐term debt should rise from Rs 1.52bn in FY14 to Rs 2bn in FY17, but debt to equity will be a comfortable 0.4x. Net profit should see a CAGR of 52% from Rs 259mn in FY14 to Rs 907mn in FY17. PAT CAGR of 52% over FY14‐17

Source: Company, PhillipCapital India Research Estimates

‐20

‐10

0

10

20

30

40

50

60

‐

5,000

10,000

15,000

20,000

25,000 Revenue (Rs mn) Growth (YoY) (rhs)

0

2

4

6

8

10

12

14

16

0

500

1000

1500

2000

2500 EBITDA (Rs mn) EBITDA (%) (rhs)

‐60

‐40

‐20

0

20

40

60

80

0

100

200

300

400

500

600

700

800

900

1000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

PAT (Rs mn) Growth (YoY) (rhs)

– 8 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Valuations Pennar’s valuation is impacted due to economic cycles and steel prices. In the past five years, Pennar has traded at a P/E of 5‐12x and average EV/EBITDA of around 7x. Its revenue profile has changed significantly in favour of value‐added products and the company is in a strong position to capitalise on economic recovery. At the current price of Rs 54, the stock trades at 7.2x our FY17 expected earnings and 3.8x EV/EBITDA. We have valued the company at 10x our FY17 EPS of Rs 7.5 to arrive at a price target of Rs 75, translating into EV/EBITDA valuation at 4.9xFY17. We are initiating coverage with a BUY rating. One year forward P/E chart

Source: Company, PhillipCapital India Research Estimates One‐year forward EV/EBITDA chart

Source: Company, PhillipCapital India Research Estimates

‐10 20 30 40 50 60 70 80 90

100

Apr/05

Sep/05

Feb/06

Jul/06

Dec/06

May/07

Oct/07

Mar/08

Aug/08

Jan/09

Jun/09

Nov/09

Apr/10

Sep/10

Feb/11

Jul/11

Dec/11

May/12

Oct/12

Mar/13

Aug/13

Jan/14

Jun/14

Nov/14

Apr/15

Price (Rs.) 5X 8X 12X 15X

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Apr/05

Sep/05

Feb/06

Jul/06

Dec/06

May/07

Oct/07

Mar/08

Aug/08

Jan/09

Jun/09

Nov/09

Apr/10

Sep/10

Feb/11

Jul/11

Dec/11

May/12

Oct/12

Mar/13

Aug/13

Jan/14

Jun/14

Nov/14

EV (Rs.m) 4X 6X 8X 10X

– 9 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Business Risk Volatility in steel prices: The raw materials cost is significant drivers for company’s profitability and growth and contributed 85% of total cost in FY14. The variation in steel prices increases the business risk for the company. Domestic Steel price trend (Rs/ton)

Cost structure (FY14)

Raw material as percentage of sales

Source: Company, PhillipCapital India Research Estimates

30000

32000

34000

36000

38000

40000

42000

44000

46000

48000

10/8/2010 10/8/2011 10/8/2012 10/8/2013 10/8/2014

Raw material85%

Employee Cost8%

Other cost7%

58

60

62

64

66

68

70

72

0

2000

4000

6000

8000

10000

12000

14000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

RM (Rs mn) % of sales (rhs)

– 10 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Working capital cycle The business is working‐capital intensive and has current assets excluding cash of Rs 5bn in FY14 representing 47% of sales. Its inventory days are around 64 and receivable days are 85 in FY14 vs. 61 and 56 in FY10. Payable days increased from 21 in FY10 to 60 in FY14. Net working capital as percentage of sales has remained 20‐26% over the past five years. High working requirement would put pressure on cash flow and limit growth expectations or increase liquidity risk. Net working capital (ex‐cash) as percentage of sale

Source: Company, PhillipCapital India Research Estimates Debt to Equity remain comfortable at 0.4x

Source: Company, PhillipCapital India Research Estimates

0%

5%

10%

15%

20%

25%

30%

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

NWC (ex cash) % sales (rhs)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0

200

400

600

800

1000

1200

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Cashflow (Rs mn) D/E

– 11 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Company Background Pennar Industries Limited (PIL), which was founded in 1988, is an engineering company. It produces steel‐based products and associated services. It has three strategic business units in its standalone business — steel products, industrial component, systems and projects and tubes. Pennar has two subsidiaries — Pennar Engineered Building Systems (PEBS) and Pennar Enviro Limited (PEL).

PIL manufactures cold‐rolled steel strips, precision tubes, cold‐rolled formed sections, ESP electrodes, profiles, railway wagon and coach components, solar structure, storage solutions, pressed steel components and road safety systems. It added hydraulics and warehousing solutions to its portfolio in FY14. Pennar caters to various segments such as infrastructure, automobiles, energy, general engineering, and building and construction. Standalone business segments Standalone business contributed 66% to its FY14 consolidated revenue; PEBS contributed 32% and Pennar Enviro 2%. Within its FY14 standalone revenue of Rs 7.4bn, 58% came from steel products, 16% from systems, and 18% from tubes. Steel products and profiles Pennar's steel products and profiles division is its largest standalone segment — this division manufactures cold‐rolled steel strips (CRSS) from a variety of grades of steel including special steel and cold‐roll formed sections (CRFS). It operates four plants for steel products with an installed capacity of 250,000TPA addressing the needs of customers such as Lloyds Insulation, Alstom Projects, Lanco Infratech, FLSmidth, Thermax, Johnson Lifts, Adani Power, L&T and Ashok Leyland. The company uses in‐house tool room, engineering, and design capabilities. It plans to expand into special profiles and higher‐margin products such as pumping solutions, ESP retro fitting, and specialised sheet piles. Cold rolled steel strips (CRSS): This division’s manufacturing facility is at Isnapur and Patancheru, Hyderabad, with combined annual cold‐rolling capacity of 120,000mn tonnes. The division manufactures steel strips up to a width of 720mm and 0.25mm to 5mm thickness, both in coil and sheet form. The division caters to a variety of industries such as automotive components, durable goods, bearings, and general engineering. Cold Roll formed sections (CRFS): Pennar’s ready‐to‐use cold‐rolled steel has close tolerances, which helps customers minimise wastage. This division manufactures a wide range of sections from simple angles to complex collecting electrodes, precisely profiled to close tolerances using types of raw material such as mild steel, structural steel,

Pennar Industries (SBU)

1. Steel Produts2. Industrial componnet3. Systems and Projects

4. Tubes

PEBS PennarPre‐engineered building Systems (PEBS).

Roof top solar, Solar EPC

Pennar EnvironIndustrial water treatment solutions, water treatment chemicals and fuel

additives

– 12 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

stainless steel and aluminium for a variety of applications. It makes profiles with thickness ranging from 0.3mm to 8mm and widths up to 1400mm. Cold‐roll forming is a continuous process of bending metals in straight line without changing the materials thickness using a successive pair of rotating tools. The products find application in building components and infrastructure, automobile profiles, metal crash barriers, sheet piles and ESP electrodes. It has the ability to mass produce a wide range of complex profiles for the industrial and infrastructure sectors. Structural steel has gained growing acceptance as a preferred construction material in fast‐track projects. Steel Tubes This segment addresses four industrial segments: electric‐resistance welded pipes, cold‐drawn welded tubes, air pre‐heater tubes, and Indian boiler regulation tubes. The tubes are used as structural components for products in the automobile, power, manufacturing, structural, and general engineering segments. The in‐house tool design and manufacturing capability has helped produce designed rolls at low costs with short lead times. The company supplies to prominent automobile companies such as Mahindra, Volvo‐Eicher commercial vehicles, Hyundai, TVS, Tata Motors and Ashok Leyland. In the power sector, it supplies to players such as Thermax, BGR, Paharpur, Cethar, KCP, and Airco Fin. The products are also used by cement plant and sugar plant‐equipment manufacturers. It supplemented the manufacture of electric‐resistance welded tubes with cold‐drawn welded (CDW) tubes in FY14. These tubes are value‐added products marked by precision, dimensional tolerance, strength, controlled mechanical properties and inner surface smoothness. It also introduced a new tubular component to cater to the oil and gas segment — the performance of this component will become visible in FY15. Industrial Components This division, which is a forward integration to provide more value‐added products from steel plates, supplies pressed‐steel components for refrigeration/white goods, automobiles, general engineering, office furnishing components, two‐wheeler parts (disc brakes) and heavy‐vehicle filter parts. This SBU addresses a market segment estimated at around Rs28bn and accounts for 2% of the country’s market share. Over 50% of its business is derived from repeat customers like Tecumseh Products, Emerson Climate Technologies, Endurance Technologies, India Nippon Electricals, IFB Automotive Private Limited, Fleetguard Filters, WABCO India and Brakes India. It acquired the hydraulics business of Wayne Burt in Chennai. Its plants in Patancheru and Chennai are equipped with modern equipment and facilities (press shops and tool maintenance) that ensure the fabrication of high‐precision quality products supported by centralised CNC tool rooms to address the emerging tool manufacturing needs of customers. Systems and Projects Pennar’s systems and project business originated with cold‐rolled steel strips. It manufactures cold‐roll‐formed profiles and fabricated structures for making railway wagons. It developed and supplied stainless steel sections for modern‐day stainless steel wagons and also emerged as a supplier of several sections (including heavy fabrication parts) for railway coaches. It addresses the needs of Integral Coach Factory (Perambur), Southern Railways, Texmaco, and Besco, among others. Pennar’s solar power projects also fall under this segment and had a 10% market share in solar module mounting structures in India, the demand for which is expected to increase following the implementation of the National Solar Mission. Its key clientele for the solar business includes L&T, Tata Power Solar, Navalakha, Lanco Solar, ABB, Schneider Electric and Solaris, among others. Pennar intends to expand its solar business presence from Tamil Nadu, Maharashtra, and Andhra Pradesh to Northern India.

– 13 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Annexure

Annexure – I: Product profile of the company

Roofing: The sheet is formed in mills in Taiwan, dedicated exclusively for roofing sheets. Application in wide range of industries like power plants, cement, industrial sheds, warehouses, institutions etc.

Decking A composite floor deck with a ribbed profile, which binds with a concrete slab and together forms a part of the floor structure. This interlocking between the concrete and the floor deck is brought about through a system of embossment and ribs, which are built into the deck creating a reinforced concrete slab that serves the dual purpose of permanent form and positive reinforcement. Composite decking is one of the most effective methods of constructing floors in steel building and very useful in in power projects, industrial buildings, multi‐storeyed buildings, supermarket / malls, SEZ, silos, storage sites, bridges, walkways and platforms.

Purlins for steel buildings Cold‐formed steel is becoming a basic material for construction. It has a high strength‐to‐weight ratio and the company supplies a variety of sections like c‐channels, lip channels, sigma sections, and Z‐Purlins

Sheet pilling The inter‐locked formed steel sheet piles can be divided in two types — U‐type and Z‐type. U‐type piles are used for support and Z‐type piles are used for heavy weights.

– 14 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Product profile of the company (Contd.)

Cold‐rolled steel strips It is produced from a hot‐rolled strip that has been pickled. Strip is reduced to final thickness by cold rolling and also slit to the desired width. Its CRSS unit has a combined capacity of 120,000mt.

Automobile products These are pressed steel products to address the requirement of the automobile sector. Products include tubes for bus body building, floor panels, side panels, and bumpers for LCV, MCV Sheet metal component.

Railway Products: Manufactures stainless steel CRF profiles for different wagon applications. For passenger coaches it supplies stainless steel through floor and sole bar for rail coach under frame and heavy fabrication items, and stainless steel fabrication of side wall / end wall. It also supplies products for metro coaches.

Storage solutions It has forayed into the storage solution market and extended its product portfolio into selective pallet racking, heavy‐duty shelving, Mezzanine systems, pallets and accessories.

Solar PV mounting solutions Supplied mounting structures and structural components to various solar plants of more than 400 MW.

– 15 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Product profile of the company (Contd.)

CDW and ERW tubes • Cold Drawn Welded (CDW) Tubes requiring high precision

dimensional tolerance, strength and controlled mechanical properties.

• Electric Resistance Welded (ERW) tubes are made by forming the steel strips into a tubular round section by progressive movement through a set of specially designed rolls. Used in automobile, boilers and heaters, general engineering

White goods and Auto components Pennar is largest player in the organised sector for industrial component in India. These components used for white goods, market leader in compress shells, automobile

Hydraulic products It has 15 years of experience in hydraulic cylinders. Its product range has applications across industries such as agriculture, construction, mining, marine, ship building and bulk cargo handling, off highway and earth movers

ESP Electrodes Pennar has been supplying various types of collecting & discharge electrodes of all ESP designs (both European & American) to all ESP manufacturers in India for the last 15 years. Pennar manufactures a wide range of ‘Collecting Electrodes’ and ‘Discharge Electrodes’ for Electrostatic Precipitators (ESPs), which are used for controlling pollution in cement, mineral industries and in power plants.

– 16 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Annexure – II: Manufacturing and distribution network

Manufacturing capabilities Pennar has four manufacturing plants — in Hyderabad, Chennai, Mumbai and Bangalore. This has made it possible to effectively address customer needs and supply chain. Its branch offices act as primary engagement points with customers. Its facilities include laser cutting, plasma cutting, transfer presses, and CNC machines. All the plants are ISO certified and follow total quality management. Manufacturing facilities in India S No Location Area Products 1 Patancheru (Andhra Pradesh) 43 Acres Auto components

Profiles Strips Road safety components Building components

2 Isnapur (Andhra Pradesh) 26 Acres Steel strips 3 Tarapur(Maharashtra) 5 Acres Cold‐rolled formed profiles 4 Chennai (Tamil Nadu) 38 Acres Engineering component

Cold‐rolled formed profiles for railways.

Source: Company

– 17 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Annexure – III: Pennar Engineered Building Systems (PEBS Pennar) The company was incorporated in January 2008 and began its commercial operations from January 2010. It designs, manufactures, and installs cost‐effective pre‐engineered steel buildings and building components for industries, warehouses, commercial centres, multi‐storied buildings, aircraft hangers, defence installations, sports stadium, industrial racking systems, and cold‐form steel structures and solar structures. Its major customers are UltraTech Cement, L&T, HCC, P&G, Godrej, Dr. Reddy’s Laboratories, ABB, JSW, Schneider Electric, Reliance Retail, ACC, IOT Infrastructure & Energy Services, Schindler, Volvo and Hyderabad Metro Rail. The pre‐engineered building industry market is estimated at Rs 45bn in India and comprises nine big players and over 35 small players. Private equity firm Zephyr Peacock acquired 26% in PEBS in FY13 with an investment of Rs 500mn, valuing the company at around Rs 2bn. Design and engineering is an important aspect of PEBS’ business and it has eighty experienced engineers in its design and detailing team. It complies with American, Euro, British, Indian, and Australian codes. Its design facility is located near Hitech City, Kondapur, Hyderabad. It enjoys a technical association with NCI Group of USA for knowhow related to the leak‐proof double‐lock roofing systems. It has received tower design approval from RAMBOLL, a leading European telecom tower designing company. RAMBOLL’s tower designs are reputed worldwide and widely used in all SAARC countries. PEBS Pennar is among the four Indian companies to pass stringent checks and attain approval from RAMBOLL, strengthening prospects in addressing the 4G opportunity. It has modern manufacturing facility near Hyderabad 29,000 sq. mt. with a production capacity of 90,000MT per annum. The plant is equipped with high‐precision computer numerical control (CNC) machines to fabricate and supply quality‐replete steel buildings. PEBS has made a foray into the international markets and executed some projects in Africa — mainly shopping malls and warehouses. It intends to set up a manufacturing plant in North India, preferably in Gujarat, to manufacture pre‐fabricated structuresxxx and also in Africa to augment capabilities and local presence by FY16. It currently has an order backlog of around Rs 3.3bn. Its turnaround time is shorter than the industry average. Some of its important projects: • UltraTech Birla White Cement, Jodhpur, Rajasthan: Stacker reclaimer shed of 75

metre clear span, the largest built by any Indian PEB company. • IOT Infra, Dahej, Gujarat: The longest building by a PEB company in India — 1 km

length and 145,000 square metre area • Jayabheri Orange County, Hyderabad: G+10 floor commercial building for Jayabheri • Properties, Hyderabad • Schindler India, Pune, Maharashtra: Factory building covering an area of 25,500 sq.

mt. • Tata Steel Processing & Distribution Limited, Chennai, Tamil Nadu: Factory building

at Chennai • L&T Metro: Building of stations for L&T Metro, Hyderabad • Shobha Developers multi‐level car parking • Nuevosol for NTPL 50MW (solar).

– 18 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

UltraTech Cement: 99 mt. clear span, Rajasthan Bharat Biotech, multi‐story steel building

Typical steel warehouse The pre‐engineered steel building system in itself offers great advantages to the customer as a more feasible, practical, and efficient alternative to conventional buildings. The system has earned acceptance across the world and is gaining rapid ground in India as well. Some of the distinct advantages include: 1. Time saving: Typically delivered twelve weeks after the approval of drawings. Helps

reduce construction time by half, thereby advancing revenues. 2. Cost‐effective: Saves design, manufacturing, transportation and on‐site erection

costs. 3. Flexibility of expansion: Can be expanded in length through the addition of bays. 4. Low maintenance: Supplied with quality paint systems for cladding and steel to suit

ambient on‐site conditions; durable and low maintenance. 5. Energy efficient: Can be reinforced with polyurethane insulated panels or fibre glass

blankets insulation on the roofs and walls. 6. Architectural versatility: Can be supplied with various fascia, canopies and curved

eaves; designed to receive pre‐cast concrete wall panels, curtain walls, block walls and other wall systems.

7. Single‐source responsibility: Complete building package supplied by a single vendor; compatibility of building components and accessories assured.

Solar projects: Pennar Engineered Building Systems is leveraging its core capabilities in design, manufacture, supply and installation of pre‐engineered steel buildings to foray into the Solar EPC market. PEBS is one of the leading companies in the field of solar energy with a manufacturing capacity of around 120MW per month. It has set up 25 kW Solar PV system at its factory in Sadasivpet, Hyderabad. PEBS Pennar has worked with leading developers and EPC players for their projects including Moserbaer, Tata Power, Lanco Solar, Schneider Electric, and ABB among others. Solar mounting structures developed by PEBS Pennar are for the following applications: • Solar Photo Voltaic Plants • Solar Roof Top • Solar Canal Top • Solar Car Parks India is building its solar power capacity with its ambitious National Solar Mission, state solar policies, and increased renewable energy focus. The installed capacity of renewable energy touched 32,269.6 MW, or 12.95% of national potential as on March, 2014. With this, the renewable energy constitutes 28.8% of the overall installed capacity in India.

– 19 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

The grid‐connected solar capacity, commissioned under the National Solar Mission, stood at 2,632MW as on March 31, 2014. In FY14, 947MW was commissioned; the company enjoys a leadership position in India’s solar structural market at 10% share. The government allocated Rs 10bn for the solar power sector in its 2015 budget. India receives nearly 3000 hours of sunshine every year, equivalent to 5,000trn kWh of energy. The Indian Railways proposes to harness 20% of its energy demand through renewable sources. Around 500MW of power would be sourced from rooftop solar applications with annual power demand of the Indian railways being 4,000MW.

Annexure – IV: Pennar Enviro PEL, incorporated in 1992, has its manufacturing facility at Mallapur, Hyderabad. Since its incorporation, PEL is in the field of additives, supplying specific premium high‐technology additives‐based fuel‐characteristic requirements and specific performance enhancements. In FY13, it pioneered the launch of premium high‐technology water treatment chemicals and turnkey solutions. The company’s EPC solutions comprise providing turnkey solutions for the water and environment infrastructure. It has also grown its business through annuity‐based O&M services as well as the sale of fuel and water additives and standard packaged water treatment plants. Fuel Additives: It has wide range of fuel additives for treatment of different petroleum fuels in order to enhance the specific performance requirements each fuel like furnace oil (FO), CBFS, light diesel oil (LDO), superior kerosene oil (SKO) and low‐sulphur heavy stock (LSHS). PEL is the authorised manufacturer and marketer of Elf fuel oil additives. It has obtained technical knowhow from Total of France for the manufacture of fuel additives. It has established a strategic alliance with Cummins India for marketing. Water Treatment: For water treatment, Pennar has an extensive range of high‐performance specialty water‐treatment chemicals under the brand “PENNTREAT” for treatment of boiler water, cooling water, raw and effluent water, and reverse osmosis. In water and environment infrastructure business, it provides turnkey solutions such as water‐treatment plants (WTPs), sewage‐treatment plants (STPs), effluent‐treatment plants (ETPs), effluent‐recycling plants (ERPs), and zero‐discharge plants (ZLDPs). In the water business it has an order book of Rs 500mn in FY14. PEL signed an exclusive technology collaboration agreement with Tech Universal (UK) a 30‐year‐old reputed EPC and technology provider. Tech Universal specialises in desalinating water/sewage and industrial effluent treatment, catering to plants throughout Europe and the Middle East. It has an order to commission a 3.2mn litres per day effluent recycle system using membrane technology for a complex textile effluent for the CETP in Tirupur, Tamil Nadu. It has a contract for a 2.4MLD sea‐water reverse osmosis project in Visakhapatnam for a leading pharmaceutical group. JBL Petroleum’s PTA project (worth Rs 45bn) in Mangalore placed an order with the company for two 110 cubic metre streams of de‐mineralised water plants for captive power generation. Equipe, a respected French consultant, examined Pennar’s capabilities in terms of engineering, design and execution capabilities before sanctioning the contract. It is in the process of executing a 30 million litres per day waste‐water treatment project for a leading pulp and paper manufacturer in Assam. The project involves cutting‐edge diffused aeration system and clarifiers of 46 and 50 metre diameters.

– 20 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Quarterly financials (Rs mn) 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15Net Sales 2,855 2,664 2,736 3,051 2,536 2,383 2,732 3,080 2,767Total Raw Material 1,937 1,745 1,602 1,970 1,582 1,491 1,602 2,248 1,802% of Sales 68 66 59 65 62 63 59 73 65Employee Cost 137 142 176 194 164 156 176 208 189Other Expenses 512 500 739 589 608 549 739 324 552Total Expenses 2,586 2,387 2,517 2,753 2,354 2,196 2,517 2,779 2,542EBITDA 269 277 220 299 182 186 215 301 225EBITDA margins 9 10 8 10 7 8 8 10 8Depreciation 44 44 53 49 43 46 53 46 58EBIT 225 234 167 250 138 140 162 255 167Interest 45 69 64 93 63 61 64 76 76EBT 180 164 103 157 75 79 98 178 91Other Income 8 4 11 17 21 16 15 ‐1 5EBT (OI) 188 168 114 174 96 95 114 177 96Tax 70 52 39 72 26 28 39 82 28Tax rate (%) 37 31 34 41 27 29 34 46 29Current Tax 60 50 25 88 25 26 25 59 20Deffered Tax 10 2 14 ‐16 2 2 14 22 8PAT 118 116 75 102 70 67 75 96 68Minority Interest 8 8 11 13 8 8 11 21 10Extraordianery ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐Reported PAT 109 108 64 89 62 59 64 74 58EPS 0.9 0.9 0.5 0.7 0.5 0.5 0.5 0.6 0.5Cash EPS 1.3 1.3 1.0 1.1 0.9 0.9 1.0 1.0 1.0 Segmental Revenue (Rs mn) 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15Steel Products 1,344 1,107 1,066 1,337 1,180 1,020 1,000 1,068 1,014Tubes 274 217 217 285 323 303 345 345 362Industrial Component 187 186 159 195 184 119 130 143 147Systems & Projects 383 469 568 487 236 258 363 342 162Pennar Enviro ‐ ‐ 14 16 ‐ 19 22 104 72Pre‐Engineering Building 673 626 700 883 712 700 979 1,223 1,013 EBITDA Margins (%) 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15Steel Products 9.3 7.7 8.9 6.0 5.2 6.6 5.9 5.0 6.3Tubes 8.8 7.0 7.9 5.3 5.8 4.8 6.0 4.0 6.2Industrial Component 13.5 18.4 17.2 6.9 12.1 12.8 12.7 14.6 14.0Systems & Projects 13.6 14.8 11.7 13.1 8.2 11.7 10.3 12.1 18.9Pennar Enviro ‐ ‐ 6.0 7.8 ‐ 7.1 6.0 1.6 3.1Pre‐Engineering Building 11.8 11.8 10.2 14.4 8.8 9.0 8.8 12.9 8.4

Source: Company, PhillipCapital India Research

– 21 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Financials

Income Statement Y/E Mar, Rs mn FY14 FY15E FY16E FY17ENet sales 10,745 13,174 16,110 19,727Growth, % ‐4 23 22 22Total income 10,745 13,174 16,110 19,727Raw material expenses ‐6,923 ‐8,310 ‐10,179 ‐12,428Employee expenses ‐704 ‐844 ‐971 ‐1,146Other Operating expenses ‐2,220 ‐2,908 ‐3,396 ‐4,010EBITDA (Core) 898 1,112 1,563 2,143Growth, % (20.9) 23.9 40.6 37.1Margin, % 8.4 8.4 9.7 10.9Depreciation ‐188 ‐198 ‐225 ‐245EBIT 710 914 1,338 1,899Growth, % (25.7) 28.8 46.4 41.9Margin, % 6.6 6.9 8.3 9.6Interest paid ‐265 ‐301 ‐326 ‐352Other Non‐Operating Income 37 38 41 44Pre‐tax profit 482 651 1,053 1,591Tax provided ‐174 ‐228 ‐368 ‐557Profit after tax 307 423 684 1,034Others (Minorities, Associates) ‐48 ‐54 ‐85 ‐127Net Profit 259 369 599 907Growth, % (38.0) 42.3 62.4 51.3Net Profit (adjusted) 259 369 599 907Unadj. shares (m) 120 120 120 120Wtd avg shares (m) 120 120 120 120 Balance Sheet Y/E Mar, Rs mn FY14 FY15E FY16E FY17ECash & bank 191 161 202 323Debtors 2,498 2,960 3,531 4,324Inventory 1,888 2,274 2,825 3,459Loans & advances 444 498 572 658Other current assets 241 278 333 400Total current assets 5,262 6,170 7,463 9,164Investments 255 263 271 279Gross fixed assets 4,489 4,839 5,239 5,689Less: Depreciation ‐2,023 ‐2,222 ‐2,447 ‐2,692Add: Capital WIP 128 120 120 120Net fixed assets 2,594 2,737 2,912 3,118Total assets 8,111 9,170 10,646 12,560 Current liabilities 3,474 4,113 4,786 5,648Provisions 80 88 96 106Total current liabilities 3,554 4,200 4,882 5,755Non‐current liabilities 640 773 1,025 1,205Total liabilities 4,194 4,973 5,908 6,959Paid‐up capital 658 657 657 657Reserves & surplus 2,895 3,121 3,577 4,313Shareholders’ equity 3,918 4,197 4,738 5,600Total equity & liabilities 8,111 9,170 10,646 12,560 Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY14 FY15E FY16E FY17EPre‐tax profit 482 651 1,053 1,591Depreciation 188 198 225 245Chg in working capital ‐263 ‐291 ‐570 ‐707Total tax paid ‐135 ‐195 ‐316 ‐477Cash flow from operating activities 272 363 392 651Capital expenditure ‐265 ‐342 ‐400 ‐450Chg in investments ‐222 ‐7 ‐8 ‐8Cash flow from investing activities ‐487 ‐349 ‐408 ‐458Free cash flow ‐215 14 ‐16 193Equity raised/(repaid) ‐15 24 25 25Debt raised/(repaid) 109 100 200 100Dividend (incl. tax) ‐145 ‐143 ‐143 ‐172Cash flow from financing activities 21 ‐19 82 ‐47Net chg in cash ‐195 ‐5 66 146 Valuation Ratios & Per Share Data FY14 FY15E FY16E FY17EPer Share data EPS (INR) 2.2 3.1 5.0 7.5Growth, % (37.2) 42.4 62.4 51.3Book NAV/share (INR) 29.5 31.4 35.2 41.3FDEPS (INR) 2.2 3.1 5.0 7.5CEPS (INR) 3.7 4.7 6.9 9.6CFPS (INR) 3.3 2.3 2.5 4.6DPS (INR) 1.0 1.0 1.0 1.2Return ratios Return on assets (%) 6.1 7.1 9.0 10.8Return on equity (%) 7.3 9.8 14.2 18.3Return on capital employed (%) 10.5 12.7 16.4 19.7Turnover ratios Asset turnover (x) 2.0 2.4 2.6 2.8Sales/Total assets (x) 1.4 1.5 1.6 1.7Sales/Net FA (x) 4.2 4.9 5.7 6.5Working capital/Sales (x) 0.1 0.1 0.2 0.2Fixed capital/Sales (x) 0.1 0.0 0.0 0.0Liquidity ratios Current ratio (x) 1.5 1.5 1.6 1.6Quick ratio (x) 1.0 0.9 1.0 1.0Interest cover (x) 2.7 3.0 4.1 5.4Dividend cover (x) 2.1 3.1 5.0 6.3Total debt/Equity (%) 42.8 44.2 45.3 41.6Net debt/Equity (%) 37.4 39.9 40.6 35.1Valuation PER (x) 25.1 17.6 10.8 7.2PEG (x) ‐ y‐o‐y growth (0.7) 0.4 0.2 0.1Price/Book (x) 1.8 1.7 1.5 1.3Yield (%) 1.9 1.9 1.9 2.2EV/Net sales (x) 0.7 0.6 0.5 0.4EV/EBITDA (x) 8.7 7.2 5.3 3.8EV/EBIT (x) 11.0 8.8 6.1 4.3

– 22 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Contact Information (Regional Member Companies)

SINGAPORE Phillip Securities Pte Ltd

250 North Bridge Road, #06‐00 Raffles City Tower, Singapore 179101

Tel : (65) 6533 6001 Fax: (65) 6535 3834 www.phillip.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd B‐3‐6 Block B Level 3, Megan Avenue II,

No. 12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel (60) 3 2162 8841 Fax (60) 3 2166 5099

www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong Tel (852) 2277 6600 Fax: (852) 2868 5307

www.phillip.com.hk

JAPAN Phillip Securities Japan, Ltd

4‐2 Nihonbashi Kabutocho, Chuo‐ku Tokyo 103‐0026

Tel: (81) 3 3666 2101 Fax: (81) 3 3664 0141 www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A, Jakarta 10220, Indonesia

Tel (62) 21 5790 0800 Fax: (62) 21 5790 0809 www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co. Ltd.

No 550 Yan An East Road, Ocean Tower Unit 2318 Shanghai 200 001

Tel (86) 21 5169 9200 Fax: (86) 21 6351 2940 www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd.

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak, Bangkok 10500 Thailand

Tel (66) 2 2268 0999 Fax: (66) 2 2268 0921 www.phillip.co.th

FRANCE King & Shaxson Capital Ltd.

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel (33) 1 4563 3100 Fax : (33) 1 4563 6017 www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Ltd.

6th Floor, Candlewick House, 120 Cannon Street London, EC4N 6AS

Tel (44) 20 7929 5300 Fax: (44) 20 7283 6835 www.kingandshaxson.com

UNITED STATES Phillip Futures Inc.

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel (1) 312 356 9000 Fax: (1) 312 356 9005

AUSTRALIA PhillipCapital Australia

Level 37, 530 Collins Street Melbourne, Victoria 3000, Australia

Tel: (61) 3 9629 8380 Fax: (61) 3 9614 8309 www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

Level 4, Millennium House, 46/58 Navam Mawatha, Colombo 2, Sri Lanka

Tel: (94) 11 2429 100 Fax: (94) 11 2429 199 www.ashaphillip.net/home.htm

INDIA PhillipCapital (India) Private Limited

No. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400013 Tel: (9122) 2300 2999 Fax: (9122) 6667 9955 www.phillipcapital.in

Management (91 22) 2300 2999(91 22) 6667 9735

Research Engineering, Capital Goods Pharma

Dhawal Doshi (9122) 6667 9769 Ankur Sharma (9122) 6667 9759 Surya Patra (9122) 6667 9768Priya Ranjan (9122) 6667 9965 Hrishikesh Bhagat (9122) 6667 9986

Retail, Real EstateInfrastructure & IT Services Abhishek Ranganathan, CFA (9122) 6667 9952

Manish Agarwalla (9122) 6667 9962 Vibhor Singhal (9122) 6667 9949 Neha Garg (9122) 6667 9996Pradeep Agrawal (9122) 6667 9953 Varun Vijayan (9122) 6667 9992Paresh Jain (9122) 6667 9948 Technicals

Midcap Subodh Gupta, CMT (9122) 6667 9762Consumer, Media, Telecom Vikram Suryavanshi (9122) 6667 9951Naveen Kulkarni, CFA, FRM (9122) 6667 9947 Production ManagerVivekanand Subbaraman (9122) 6667 9766 Metals Ganesh Deorukhkar (9122) 6667 9966Manish Pushkar, CFA (9122) 6667 9764 Dhawal Doshi (9122) 6667 9769

Database ManagerCement Oil&Gas, Agri Inputs Vishal Randive (9122) 6667 9944Vaibhav Agarwal (9122) 6667 9967 Gauri Anand (9122) 6667 9943

Deepak Pareek (9122) 6667 9950 Sr. Manager – Equities SupportEconomics Rosie Ferns (9122) 6667 9971Anjali Verma (9122) 6667 9969Sales & Distribution Kinshuk Bharti Tiwari (9122) 6667 9946 Dipesh Sohani (9122) 6667 9756 Zarine Damania (9122) 6667 9976Ashvin Patil (9122) 6667 9991 Sales TraderShubhangi Agrawal (9122) 6667 9964 Dilesh Doshi (9122) 6667 9747 Kishor Binwal (9122) 6667 9989 Suniil Pandit (9122) 6667 9745Sidharth Agrawal (9122) 6667 9934 ExecutionBhavin Shah (9122) 6667 9974 Mayur Shah (9122) 6667 9945

Corporate Communications

Vineet Bhatnagar (Managing Director)Jignesh Shah (Head – Equity Derivatives)

Automobiles

Banking, NBFCs

– 23 of 23 –

29 October 2014 / INDIA EQUITY RESEARCH / PENNAR INDUSTRIES LTD INITIATING

Disclosures and Disclaimers PhillipCapital (India) Pvt. Ltd. has three independent equity research groups: Institutional Equities, Institutional Equity Derivatives and Private Client Group. This report has been prepared by Institutional Equities Group. The views and opinions expressed in this document may or may not match or may be contrary at times with the views, estimates, rating, target price of the other equity research groups of PhillipCapital (India) Pvt. Ltd. This report is issued by PhillipCapital (India) Pvt. Ltd. which is regulated by SEBI. PhillipCapital (India) Pvt. Ltd. is a subsidiary of Phillip (Mauritius) Pvt. Ltd. References to "PCIPL" in this report shall mean PhillipCapital (India) Pvt. Ltd unless otherwise stated. This report is prepared and distributed by PCIPL for information purposes only and neither the information contained herein nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment or derivatives. The information and opinions contained in the Report were considered by PCIPL to be valid when published. The report also contains information provided to PCIPL by third parties. The source of such information will usually be disclosed in the report. Whilst PCIPL has taken all reasonable steps to ensure that this information is correct, PCIPL does not offer any warranty as to the accuracy or completeness of such information. Any person placing reliance on the report to undertake trading does so entirely at his or her own risk and PCIPL does not accept any liability as a result. Securities and Derivatives markets may be subject to rapid and unexpected price movements and past performance is not necessarily an indication to future performance. This report does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax and financial advisors and reach their own regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. In no circumstances it be used or considered as an offer to sell or a solicitation of any offer to buy or sell the Securities mentioned in it. The information contained in the research reports may have been taken from trade and statistical services and other sources, which we believe are reliable. PhillipCapital (India) Pvt. Ltd. or any of its group/associate/affiliate companies do not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinions expressed reflect judgments at this date and are subject to change without notice Important: These disclosures and disclaimers must be read in conjunction with the research report of which it forms part. Receipt and use of the research report is subject to all aspects of these disclosures and disclaimers. Additional information about the issuers and securities discussed in this research report is available on request. Certifications: The research analyst(s) who prepared this research report hereby certifies that the views expressed in this research report accurately reflect the research analyst’s personal views about all of the subject issuers and/or securities, that the analyst have no known conflict of interest and no part of the research analyst’s compensation was, is or will be, directly or indirectly, related to the specific views or recommendations contained in this research report. The Research Analyst certifies that he /she or his / her family members does not own the stock(s) covered in this research report. Independence/Conflict: PhillipCapital (India) Pvt. Ltd. has not had an investment banking relationship with, and has not received any compensation for investment banking services from, the subject issuers in the past twelve (12) months, and PhillipCapital (India) Pvt. Ltd does not anticipate receiving or intend to seek compensation for investment banking services from the subject issuers in the next three (3) months. PhillipCapital (India) Pvt. Ltd is not a market maker in the securities mentioned in this research report, although it or its employees, directors, or affiliates may hold either long or short positions in such securities. PhillipCapital (India) Pvt. Ltd may not hold more than 1% of the shares of the company(ies) covered in this report. Suitability and Risks: This research report is for informational purposes only and is not tailored to the specific investment objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give rise to substantial risks and may not be suitable for certain investors. Each investor must make its own determination as to the appropriateness of any securities referred to in this research report based upon the legal, tax and accounting considerations applicable to such investor and its own investment objectives or strategy, its financial situation and its investing experience. The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as well as by other financial, economic or political factors. Past performance is not necessarily indicative of future performance or results. Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that PCIPL and the research analyst believe to be reliable, but neither PCIPL nor the research analyst represents or guarantees that the information contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current opinions as of the date appearing on this material and are subject to change without notice. Furthermore, PCIPL is under no obligation to update or keep the information current. Copyright: The copyright in this research report belongs exclusively to PCIPL. All rights are reserved. Any unauthorized use or disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without the PCIPL’s prior consent, except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety. Caution: Risk of loss in trading in can be substantial. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances. For U.S. persons only: This research report is a product of PhillipCapital (India) Pvt Ltd. which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account. This report is intended for distribution by PhillipCapital (India) Pvt Ltd. only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor. In reliance on the exemption from registration provided by Rule 15a‐6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, PhillipCapital (India) Pvt Ltd. has entered into an agreement with a U.S. registered broker‐dealer, Marco Polo Securities Inc. ("Marco Polo").Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer. PhillipCapital (India) Pvt. Ltd. Registered office: No. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400013