Embed Size (px)

Citation preview

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 1/20

ISSUE 2012/12JUNE 2012 WHAT KIND OF

EUROPEAN

BANKING UNION?JEAN PISANI-FERRY, ANDRE SAPIR, NICOLAS VERON AND

GUNTRAM B. WOLFF

Highlights

• This policy contribution discusses in detail how a future banking union could be organi-sed byexaminingseven fundamental choices that decision makers will need tomake:

- Which EU countriesshould participatein the banking union?- To which categories of banks should it apply?- Which institution should be tasked with supervision?- Which one should deal with resolution?- Howcentralisedshould the deposit insurance system be?- What kind of fiscal backingwould be required?

- Whatgovernanceframework and politicalinstitutions would be needed?

• The paperdiscusses how the transitionfrom the currentstate tothefuturebankingunioncouldbe organised andwhat the shortterm steps might be.

Jean Pisani-Ferry ([email protected]) is Bruegel’s Director. André Sapir([email protected]) is a Senior Fellow at Bruegel. Nicolas Véron ([email protected]) is a Senior Fellowat Bruegel and Visiting Fellowat the Peterson Institute forInter-naional Economics. Guntram B. Wolff is Bruegel’s Deputy Director.

This paper benefited from a workshop held at Bruegel on 11 June 2012. We are gratefulto all participants for their contributions to discussions held on that occasion. We thankChiara Angeloni and SilviaMerler fordiligentand effective researchassistance in the pre-

paration of this paper.

Telephone+32 2 227 [email protected]

www.bruegel.org

BRUEGELPOLICYCONTRIBUTION

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 2/20

02

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

WHAT KIND OF EUROPEAN BANKING UNION?

JEAN PISANI-FERRY, ANDRE SAPIR, NICOLAS VERON AND GUNTRAM B. WOLFF, JUNE 2012

ABSTRACT

This paper discusses the creation of a EuropeanBanking Union. First, we discuss questions of design. We highlight seven fundamental choicesthat decision-makers will need to make: WhichEUcountries should participate in the bankingunion? To which categories of banks should itapply? Which institution should be tasked withsupervision? Which one should deal withresolution? How centralised should the depositinsurance system be? What kind of fiscal backingwould be required? What governance frameworkand political institutions would be needed?

In terms of geographical scope, we see the cover-age of the banking union of the euro area as nec-

essary and of additional countries as desirable,even though thiswould entail importantadditionaleconomic difficulties. The system should ideallycover all banks within the countries included, inorder to prevent major competitive and distribu-tional distortions. Supervisory authority should be

granted either to both the ECB and a new agency,or to a new agency alone. National supervisors,acting under the authority of the European super-visor, would be tasked with the supervision of smaller banks in accordance with the subsidiar-

ity principle. A European resolution authorityshould be established, withthe possibility of draw-ing on ESM resources. A fully centralised depositinsurance system would eventually be desirable,but a system of partial reinsurance may also beenvisaged at least in a first phase. A bankingunion would require at least implicit European

fiscal backing, with significant political authorityand legitimacy. Thus, banking union cannot beconsidered entirely separately from fiscal unionand political union.

The most difficult challenge of creating a Europeanbanking union lies with the short-term stepstowardsits eventual implementation. Many banksin the euro area, and especially in the crisis coun-tries, are currently under stress, and the movetowards banking union almost certainly has sig-nificant distributional implications. Yet it is pre-cisely because banks are under such stress thatearly and concrete action is needed. An overarch-ing principle for such action is to minimise thecost to taxpayers. The first step should be tocreate a European supervisor that will anchor thedevelopment of the future banking union. In par-allel, a capability to quickly assess the true capi-tal positionof the system’s most importantbanks

should be created, for which we suggest estab-lishing a temporary European Banking Sector TaskForce working together with the European super-visor and other authorities. Ideally, problems iden-tified by this process should be resolved bynational authorities; in case fiscal capacitieswould prove insufficient, the European level wouldtake over in the country concerned with somenational financial participation, or in an even lesslikely adverse scenario, in all participating coun-tries at once. This approach would require the

passing of emergency legislation in the countriesin question that would give the Task Force therequired access to information and, if necessary,

further intervention rights. Thus, the principle of fiscal responsibility of the individual memberstates for legacy costs would be preserved to themaximum extent possible and, at the same time,market participants and the public would be reas-sured that adequate tools are in place to addressany eventuality.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 3/20

03

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

1. See Cihak & Decressin(2007)and Véron (2007).

2. See Merler & Pisani-Ferry(2012).

3. See ECB(2012) andPisani-Ferry & Wolff

(2012).4. See for example Gerlach,

Schulz & Wolff (2010).5. See Pisani-Ferry (2012).

6. See Angeloni & Wolff (2012).

7. See Véron (2007) andPosen & Véron (2009).

THE CONCEPT OF EUROPEAN BANKING UNION WASRECENTLY ENDORSED by European leaders as a

component for solving the euro crisis. In order to“strengthen economic union and make itcommensurate with the monetary union”, theEuropean Council on 23 May asked president VanRompuy and other top European officials toidentify “building blocks”, among which “a moreintegrated banking supervision and resolution,and a common deposit insurance scheme” – inshort, a banking union. On 19 June the G20leaders expressed support for “the intention toconsider concrete steps towards a moreintegrated financial architecture, encompassingbanking supervision, resolution andrecapitalization, and deposit insurance”.

The rationale for a banking union complementingmonetary union is straightforward. Europe’sEconomic and Monetary Union (EMU) wasconstructed on the basis of two pillars:a monetarypillar with the independent and price-stabilityorientedEuropean Central Bank (ECB), and a fiscalpillar oriented towards fiscal discipline with amodicum of coordination. It has no financial policy

componentapart from the ban on capital controlsand the promotion of a single market for financialservices, bothof which apply tothe whole EU, andit has no banking component, apart from thosearising from the operation of monetary policy andthe common banking regulation and commonstandards on deposit insurance. The ECB itself hasfew financial stability competences.

Even before the crisis there were reasons toquestion whether this bare-bones model was

sufficient. It was known that there was aninherent contradiction between pan-Europeanbanking and exclusive national responsibility forbank crisisresolution1. Recent developments haveexposed further weaknesses:• First, the previously integrated euro-areafinancial market has entered a process of fragmentation. Capitalthat was supposed to moveas freely across countries as across regions hasstopped flowing from North to South, which hasresulted in within-EMU surprise balance-of-

payment crises2

. Banks that were European inquiet times have become national in crisis timesas they depend on national governments forsupport. Furthermore,they have been encouraged

by national authorities to cut cross-border lending.This is understandable from a national viewpoint,

as taxpayers have little reason to pay for theconsequences of imprudentlending to foreigners,but is lethal for the euro-area financial market.Integration of the interbank market is on theretreat within the euro area3. This, in turn, hasincreased the exposure of the ECB that hasbecome a financial intermediary replacing theinterbank market.• Second, there has since 2008 been a strongcorrelation between banking and sovereignsolvency crises. Especially but notonlyin Greece,Ireland, Spain and Italy, sovereign solvencyconcerns have affected banks and bank solvencyconcerns have affected sovereigns4. The reasonsfor this correlation include a strong home bias inthe composition of banks’ sovereign bondportfolios, the sovereigns’ individual responsibilityfor bailing out banks5, and the increasinglyapparent re-emergence of country risk6.Thistwo-way correlation creates vicious circles that theECB cannot quell, because a federal central bankcannot be mandated to assist particularsovereigns and because the ECB cannot address

solvency concerns and stay committed to itsprimary target.• Third, the crisis has made it increasingly clearthat a fragmented approach to banking policyrenders it more difficult to minimise losses totaxpayers. Asset ring-fencing and risk-shiftingresult in coordination failures that increase theoverall public cost7. Furthermore, individualcountries may either be prevented by neighboursfrom imposing losses on bondholders for fear of contagion,as was the case of Ireland in late 2010;

or if they do impose losses, their other domesticbanks risk being at a disadvantage in theintegrated European market, a factor that ledDenmark to amend its policyframework to make itmore creditor-friendly in 2011.

These developments undermine the foundationsof monetary union and call into question its veryrationale. They explain why the banking uniontheme has emerged as one of the key ways torespond to the incompleteness of EMU.

Centralising responsibility for deposit insurance,bank supervision and crisis resolution wouldcontributeto its resilience by cementing financialintegration and reducing the potential for

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 4/20

04

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

correlation of sovereign-banking crises.

To create a banking union is, however, a step of high significance with major ramifications forfinancial integration within the euro area, publicfinances, governance and, ultimately, politicalintegration. It requires very careful design andinvolves many choices, both as regards the steadystate and the transition to it.

The aim of this paper is to review choices andassess alternatives. We start in section 1 withoverallconsiderations on theprinciples of bankingpolicy. We then draw an outline of what aEuropean banking union would be in section 2,and review in section 3 the key choices andoptions involved. We take up transition issues insection4. Conclusions are presented in section 5.

1 PRINCIPLES OF BANKING POLICY

The central purpose of banking policy is to ensurea proper functioning of financial intermediationexercised by the banking system. To achieve thisgoal, banking policy aims to prevent banking

crises and, when a crisis occurs, to intervene toprevent the crisis of an individual bank givingriseto a crisis of the banking system. To ensure propercrisis prevention and management, a widelyshared view of banking policy describes it asresting on four pillars: regulation, supervision,deposit insurance and bank resolution.• Banking regulation aims to increase theresilience of banks to shocks and, ultimately, toreduce the externality resulting from the fact thatbank failures can impose large losses on society

that may lead governments to bail out bankcreditors. Other aspects of banking regulation,such as on preventing money-laundering orconsumer protection, are motivated by otherconsiderations than financial stability.• Bank supervision allows governments toclosely monitor banks’ activities and risk-takingtoensure that they are managedin a prudent way,and to check the build-up of risk. As withregulation, its ultimate aim is to prevent financialinstability and minimise risks to the taxpayers. It

can involve significant reporting requirements andbe intrusive with supervisors permanentlyembedded in supervised banks’ premises.• Deposit insurance is intended to counter the

threat of a bank run by protecting the value of deposits. Depending on countries, it can be either

pre-funded by the financial industry through adedicated fund, or post-funded as a consequenceof crises. It always has implicit or explicitgovernment backing, because even large pre-funded insurance may be insufficient to covercertain extreme crisis scenarios.• Bank resolution authority and capacity shouldallow for the resolution of banks without severesystemic disruptions and ideally also withoutexposing the taxpayer to losses. The US FederalDeposit Insurance Corporation (FDIC)’s resolutionauthority that has developed since the 1930s fordepositary institutions is an early example. If aresolvability assessment concludes that afinancial institution is no longer viable, theresolution authority should have strong powers tostabilise the core functions of systemicimportance, in particular deposits and essentialintermediation functions; to preserve the value of assets by preventing firesales; to force junior andsenior unsecured creditors to share losses, withdebt restructuring, debt-equity swaps and “bail-ins” among the possible instruments. While the

crisis has spurred increasing internationalconsensus on the desirability of a specialresolution regime for financial institutions and thekey attributes it should include (FSB, 2011),many countries, including some in the EU andeuro area, still lack such a policy framework. TheEuropean Commission has recently madeproposals that would partly harmonise this policyarea across the EU (European Commission,2012).The four pillars are highly connected. To be

effective, strong political authority and executivecapacity are needed. Decisions taken by thesupervisory and resolution authority often implysignificant distributional effects and may alsoimply significant risks to the public purse. Theseauthorities must therefore be legitimised and heldaccountable, which typically involves carefullydesigned governance and active parliamentaryoversight. The division of labour between centralbanks, supervisors and finance ministries differsacross countries, even though the central bank

always plays an important role as the ultimateprovider of liquidity, not only in case of a(systemic) bank run butalso in the periodduringwhich the relevant authorities make an

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 5/20

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 6/20

06

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

required speed. Equally, without European super-vision, moral hazard would undermine the

common insurance scheme and make it prone todistributive biases. It is only by pooling compe-tences in all areas that the banking union wouldbe able to strengthen the system. By the sametoken, such a transfer amounts to a significantdevolution of responsibility to the European level,which makes it imperative to strengthen theaccountability and legitimacy of European-leveldecision-making from a democratic standpoint.

3 KEY CHOICES FOR THE DESIGN OF A EUROPEANBANKING UNION

The creation of a banking union is an ambitiousand complex endeavour, in some respects no lessambitious and complex than the creation of monetary union itself. It will take time to achieveand is likely to require multiple successive steps.The essential choices that will shape its steady-state form can be summarised along seven axes:1. Which countries should participate in thebanking union?2. To which banks should it apply?

3. Which institution(s) should be tasked withsupervision?4. How should bank resolution authority beassigned?5. How centralised should the deposit insurancesystem be?6. How should fiscal backing be organised?7. What governance framework should be put inplace?In what follows we successively review anddiscuss these seven choices.

1. Which member states?

As indicated in the introduction, there is a strongrationale for creating a banking union for the euroarea, as the way the crisis has developed sincelate 2009 has made it clear that a banking unionis indispensable to a lasting and stable monetaryunion. However, there is also a rationale forcreating a banking union for the EU27: a truesingle financial market may be undermined by

incentives for national authorities to restrictcross-border operations by banks headquarteredon their territory out of prudential concerns, or fordifferential treatment or guarantees in the event

would entail the following main building blocks:• European banking regulation. As this area is

alreadysubstantiallyharmonised, changes wouldbe more limited than for the following three items.Even so, progress is needed to achieve the visionof a “single rulebook” (de Larosière, 2009). Oneimportant new element might be the introductionof a European banking charter, which would allowpan-European banks to compete on a truly levelplaying field (Cihak & Decressin, 2007).• European supervision. This is made necessaryboth by the need to effectively supervise bankingoperations that are integrated on a cross-borderbasis, and to counter the incentives for nationalsupervisors to overlook excessive risk-taking bybanks in their jurisdiction if deposit insurance ismoved to the European level. Unlike today’s EBA,the European supervisor would need direct author-ity over supervised entities in order to properlycarry out its duties.• European deposit insurance. The schemewouldbe financed by contributions from the participat-ing banks. This would amount to pooling riskacross banks in all participating countries andincrease the potential for dealing with country-

specific, region-specific or bank-specific crises.However, deposit insurance can never cover allpossible risk scenarios, which is why it must beat least implicitly backed by a second, inherentlyfiscal line of defence. A European deposit insur-ance system would therefore entail some Euro-pean-level fiscal capacity.• European resolution authority. This is neededto prevent the combination of national crisis man-agement decisions from resulting in excessiveand avoidable cost to taxpayersin Europe, includ-

ing as regards burden-sharing with creditors asdiscussed in the previous section.

Once again it is important to realise that in asteady state, the different pillars of a bankingunion cannot be separated from each other, norare they fully separate from parallel advancestowards fiscal andpolitical union. If notbacked upby fiscal support, a European deposit insurancescheme would not help deal with major bankingcrises. It could even blurresponsibilities and make

things worse. Without a centralised resolutionauthority, real-time decisions would be made in adisorderly manner at the national level, as com-mittees based on consensus could not act at the

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 7/20

07

B RUE GE L

POLICYCONTRIBUTION

8. See Véron (2007) andFonteyne & al (2010).

9. In his Mansion Housespeech on 14 June 2012,

UK Chancellor of theExchequer George Osbornesaid: “A bankingunion – in

other words, a union that

stands behind the stabilityof Eurozone banks and their

deposits in return forcommon financial supervi-sion [- is] a natural conse-

quence of a single currency[…].The same level of inte-

gration and common super-vision is not considered

necessaryin other areas of the single marketlike

energy.So we are clear thatBritain will not take part inthis banking union. British

taxpayers will not standbehind eurozone banks.”10. If a “partial” banking

union is adopted, coveringonly the largest banks, thecountriesbelonging to the

banking union would berepresented in the EBA andESRB by both their nationalsupervisory authorities and

the common supervisoryauthority. If it is a “com-

plete” banking union, onlythe European supervisor

would represent thosecountries that form part of

it (see item3 ofthissec-tion).

of a crisis8. The logic of a banking union at 27 isnot to ensure the viability of monetary union, but

to preserve financial integration within theEuropean singlemarket. This is fundamentally therationale behind the proposals for an EUframework for bank recovery and resolutionunveiled by the European Commission on 6 June2012.

The preservationof financial integrationwithin thesingle market is a valid economic reason forbuilding an EU-wide banking union. At the sametime, some of the central functions of a bankingunion such as the relationship between theliquidityoperations of a central bank and the fiscalresolution functions, as well as the creation of acommon deposit insurance scheme, are renderedmore difficult by the existence of multiplecurrencies. Moreover, it is a matter of discussionwhether the potential economic benefits of mutualising banking policy outweigh its costs interms of shared sovereignty and mutualisationof risks for the different member states. Ultimately,this is a political judgement, on which differentviews are being expressed. The UK, in particular,

has clearly indicated its unwillingness to be boundby a banking union that it regards as a “naturalconsequence” of the single currency rather thanas the inevitable conclusion of the EU singlemarket. It supports, therefore, the creation of abanking union for the euro area but is againstcreating one for the EU9.

Political reservations may exist within the euroarea, but here they need to be weighed against amuch more powerful argument, namely that the

absence of a banking union undermines thefunctioning, and perhaps the very existence, of the common currency. A s the InternationalMonetary Fund (IMF) puts it, “While a bankingunion is desirable at the EU27 level, it is critical forthe euro 17” (IMF, 2012).

Indeed, ourassessment is that creating a bankingunion that would include all EU member states istoo high an ambition to be practical, at least forthe foreseeable future. Projects for an EU-wide

banking union have no chance of seeing the lightof day. They can only create confusion anddistract from the essential priority of addressingthe euro crisis. A banking union for the euro areaisurgently needed, and the simplest option is one

that encompasses only the euro area.

Onemightalso consider intermediate options thatwould include some countries which are notmembers of the euro area, but (unlike the UK)would be willing to embrace the banking unionwhile staying outside of monetary union. But thiswould create additional risks and uncertainties,for example the coordination of liquidity policiesby different central banks in different currencyareas during a funding crisis. It would also beincompatible with some policy choices, such as if the ECB is chosen as the single supervisor of thebanking union. We view such options as moredifficult and less desirable from a technicalstandpoint than an identity of perimeter betweenmonetary and bankingunions. That said, they arenot impossible, and ultimately subject to political judgment.

Appropriate transitional arrangements should inany case be considered for non-euro-areamembers that have expressed the intention to jointhe currency area and signalled willingness toconsider membership of a banking unionfrom the

outset, giventhe high degree of integration of theirdomestic banking systems with the euro area.

In any event, European banking union should bedesigned taking into account the interests of allEU countries. The goal should be to have a bankingunion that can live in harmony with the singlemarket.

In order to ensure a smooth relationship betweenthe different groups of countries – those in the

euro area and the banking union, those outsidethe euro areabut in the banking union, if any, andthe others – the following guiding principles(based on Pisani-Ferry, Sapir and Wolff, 2012)should apply:• Euro-area countriesshould be allowed to createa banking union that goes over and above thelimited remit envisaged in the Lisbon treatyforthemonetary union.• The integrity of the EU single market should beensured with equal treatment in the application of

common rules. This principle would be enforcedby the European Commission.• The mandate of the EBA and the ESRB shouldbe upheld, with due adaptation of their structuresto the creation of the banking union10.

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 8/20

08

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

11.In the FSB’s terminologyon SIFIs, systemic impor-

tance is recognised eitherat the globallevel (G-SIFIs)or at the domestic countrylevel (D-SIFIs). A Europeanbanking union would needto consider the intermedi-

ate European level, thus E-SIFIs. By implication, all

G-SIFIs based in Europe areE-SIFIs,but there might beadditional E-SIFIs that arenotG-SIFIs; and all E-SIFIs

are D-SIFIs for their individ-ualhome countries with the

EU.

financial stability should go hand in hand, eventhough there may be some instances where the

two objectives may be at odds with one another.The current situation, where the inability of theeuro area to ensure its financial stability has ledto financial disintegration that threatens theentire EU single market, is clear proof of thiscomplementarity. Thus, all EU member statesshould recognise that they share a fundamentalincentive to find cooperative solutions to createthe European banking union.

2. Which banks?

How comprehensive should the banking unionbe? At one extreme, a “partial” banking unioncould cover only those banks that should beconsidered systemically important financialinstitutions (SIFIs) on a European scale, whichmight be termed “E-SIFIs” to extend the nowcommonly used classification of the FinancialStability Board11. Those banks have significantcross-border operations whose resolution isbound to require transnational mechanisms. Atthe other extreme, a “complete” banking union

would entail European-level responsibility for thewhole of banking policy, covering all banks nomatter how small or local. In between, a range of options could be considered.

This choice involves several dimensions:(a) Information asymmetries. Europeanauthorities would have a clear informationaladvantage over national authorities for thesupervision of banks with significant cross-border

• There should be adequate consultation of thoseEU member states outside of the European

banking union in designing the functions of thebanking union.Under such conditions, all EU countries should inprinciple welcome the creation of a Europeanbanking union, evenif it is limited totheeuroarea,since this would help deliver more stability to theentire EU.

It might be the case, however, that even thesefourconditions would not be sufficient to ensureunanimity of EU member states on the creation of the banking union, which is required in order toestablish it under the EU treaty. Specifically, theUK has particular concerns and may ask foradditional guarantees (Box 2).

If the demands of the UK and other countriesoutsidethe banking unionfail to elicit consensus,it is also imaginable that the banking union wouldbe created andorganised outside the EU treaty. Aswith the European Stability Mechanism (ESM) andfiscal compact, however, a compromise should befound to ensure a proper relationship between the

institutions of the banking union and thoseof theEU.

The bottom line is that all EU countriesneed tofinda way to attain two common objectives: topreserve the integrity of the single market, whichmany see as the EU’s most important commonasset; and to ensure the stability of the euro area,for which a banking union has become necessary.In general, EU financial integration and euro-area

BOX 2: THE UK AND BANKING UNION

Although the British government supports the creation of a banking union amongst euro-areamembers, there is concern in the UK that its creation might jeopardise the standing of the City of London as both the main financial centre of the EU, andas a global financial centre. Regarding its rolevis-à-vis the euro area, many in the City are worried about potential regulatory decisions of euro-area authorities which could require certain financial activities to be located within the euro area soas to able to supervise them forfinancial stability reasons. An example of such a decision maybe the2011 announcement by the ECB that the Eurosystem has major concerns with regard to thedevelopment of major euro financial market infrastructures that arelocated outside of the euro area.As far as the City’sglobal role is concerned, there are also fears that, by creating a banking union, theeuro-area countries would act as a caucus on EU single market issues and impose changes to the

single banking and financial rulebook that might reduce the attractiveness of London compared toother global financial centres like NewYork, Hong Kong, Singapore or Shanghai. Those things matterparticularly for the UK because the City, and more generally the financial services industry, contributesignificantly to its GDP.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 9/20

BOX 3: SIZE AND CONCENTRATION OF BANKING SYSTEMS IN EUROPE

Banking systems in Europe differ widely from country to country. On the liability side, deposits-to-GDP ratios vary depending on financial development, wealth and the share of non-residents in totaldeposits. Luxembourgand Cyprus are characterizedby high deposit ratios becauseof thelarge shareof non-residents. At the other extreme deposit-to-GDP ratios are low in Estonia and Slovakia.

09

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

operations. The opposite is arguably true for localbanks.

(b) Sovereign/banking feedback loop. Commondeposit insurance can sever the connectionbetween domestic sovereign and banking risksonly if its coverageis broad enough to mutualise asignificant part of the risks. For instance, theSpanish Cajas have very little internationalbusiness, yet they were collectively large enoughto represent a major fiscal risk for Spain and forthe financial stability of the euro area. Only acomplete banking union canentirelyeliminate thefeedback loop.(c) Distribution of costs and benefits. Bankingconcentration varies greatly across euro-areamember states. For example, most of France’sbanking system is composed of E-SIFIs, whereasIreland and Portugal are home to few suchinstitutions, if any. Other countries combineinstitutions whose systemic importance is at theEuropean, national, or sub-national level, invarying proportions (See Box 3). Hence, differentchoices on the scope of banking union can havevery different distributional consequences.

(d) Potential competitive distortions. Any partialbanking union involves the risk of competitive

distortions and regulatory arbitrage betweenfederally and nationally supervised banks. Aspartial union would not eliminate the sovereign-banking feedback loop, it may also riskundermininglocal banks in countries with weakerfundamentals.

The choice of a scope for banking union should bemade in a way that takes into accountinformational constraints, ensures an adequatecoverage of risks, limits asymmetry acrosscountries, and minimises distortions. A partialunioncovering solely E-SIFIs would mean that theEuropean supervisor would only deal with alimited number of pan-European entities, but itwould address the banking-fiscal feedback looponly partially and would result in a high degree of asymmetry acrosscountries. Conversely, a partialunion might run into less political resistance atthe national (and in some cases, sub-national)level than a complete one. Including only E-SIFIsor E-SIFIs plus large banks would also create

Figure 1:Deposit-to-GDP ratios, 2010

D e p o s i t s ( M F I s e x c l u d e d ) / G D P

Source: Source: ECB and Swiss National Bank, Bruegel calculations

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 10/20

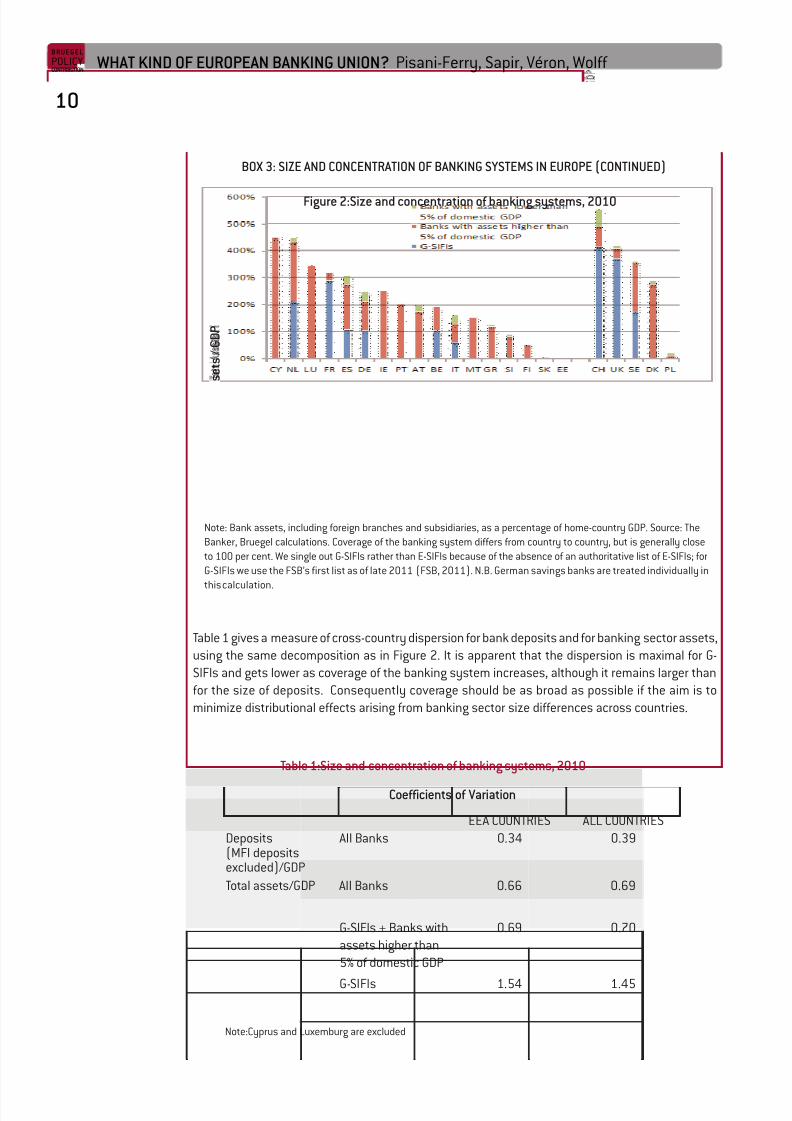

BOX 3: SIZE AND CONCENTRATION OF BANKING SYSTEMS IN EUROPE (CONTINUED)

Table 1 gives a measure of cross-country dispersion for bank deposits and for banking sector assets,using the same decomposition as in Figure 2. It is apparent that the dispersion is maximal for G-SIFIs and gets lower as coverage of the banking system increases, although it remains larger thanfor the size of deposits. Consequently coverage should be as broad as possible if the aim is tominimize distributional effects arising from banking sector size differences across countries.

10

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

Figure 2:Size and concentration of banking systems, 2010

T o t a l A

s s e t s / G D P

Note: Bank assets, including foreign branches and subsidiaries, as a percentage of home-country GDP. Source: TheBanker, Bruegel calculations. Coverage of the banking system differs from country to country, but is generally closeto 100 per cent. We single out G-SIFIs rather than E-SIFIs because of the absence of an authoritative list of E-SIFIs; forG-SIFIs we use the FSB’s first list as of late 2011 (FSB, 2011). N.B. German savings banks are treated individually in

this calculation.

Table 1:Size and concentration of banking systems, 2010

Coefficients of Variation

EEA COUNTRIES ALL COUNTRIESDeposits(MFI depositsexcluded)/GDP

All Banks 0.34 0.39

Total assets/GDP All Banks 0.66 0.69

G-SIFIs + Banks withassets higher than5% of domestic GDP

0.69 0.70

G-SIFIs 1.54 1.45

Note:Cyprus and Luxemburg are excluded

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 11/20

11

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

significant distortions between smaller and largerbanks.

In this debate, centralisation of authority shouldnot be confused with operational centralisation.Even in a complete banking union, the subsidiarityprinciple would apply and there would be adelegation of many supervisory operations tonational or sub-national entities under theauthority of the European supervisor. In noscenario should and would the thousands of banks that exist in the EU be all supervisedcentrally.

These considerations lead us to advocate broadcoverage extending significantly beyond E-SIFIs,and ideally a “complete” banking union coveringthe entire sector if a political consensus can beachieved for it. The choice of scope of the bankingunion has significant implications for the waydeposit insurance should be organised. This isdiscussed below under item 5.

3. Which supervisor?

At the level of individual countries, there is alongstanding debate on whether bank supervisionshould be conducted by the central bank or by aseparate public authority that may have strongerlinks with the finance ministry. A number of dimensions are relevant for this:• First, the central bank is the last-resort providerof liquidity to banks. In times of crisis, it needs tostrongly increase its liquidity provisioning and bydoing so it increases risk on its balance sheets.Therefore, the central bank naturally has to make

assessments about its counterparts, and hasbetter expertise on liquidity conditions affectingbanks than an agency that is more remote frommarkets. All other things equal, this gives thecentral bank a natural advantage in supervision.• A second dimension concerns the potentialconflict of interest between monetary policy andsupervisory action: the central bank may be led tobe more dovish on monetary policy than theinflation objective warrants in order to safeguardcertain banks it supervises, or even in order to

conceal supervisory failures; conversely, it mightbe tempted by supervisory forbearance to preventa crisis happening that could result in priceinstability. All other things equal, this argumentspeaks against supervision by central banks.

However, the crisis has also shown that thecentral banks’ functions extend beyond price

stability. In fact, a vivid discussion has emergedabout the best way central banks can reconcilefinancial stability and price stability.• The central bank’s role in supervision also is amatter of a delicate balance with regard to the linkwith the resolution authority. Bank resolution haspotential fiscal implications and thereforeresolution needs to be exercised by an authorityendowed with appropriate political legitimacy.

One way to take into account these divergentarguments is to have the supervisory functionexercised both by the central bank and by aseparate supervisor. As illustrated by Box 1, theUS provides such an example with thecomplementary and overlapping remits of the Fed,OCC, FDIC, SEC and NCUA. Japan similarly hascomplementarities between the respective rolesof the Bank of Japan and the Financial ServicesAgency, each of which supervises banks throughparallel frameworks. However, a longstandingbody of comparative literature generallyconcludes that no single pattern of division of

supervisory responsibilities between centralbanks and other authorities is unquestionablysuperior to the alternatives.

At the European level, a number of additionalfactors need to be considered when deciding onthe appropriate supranational supervisoryauthority. The EBA already exists at the Europeanlevel, and one possibility would be to grant itsupervisory authority. As indicated, however, wefind it unlikely that a banking union could cover

the whole EU, which makes it unlikely that theEuropean supervisor could be the EBA. By thesame token, the ECB could be chosen assupervisor if the scope of the banking union islimited to the euro area.

In legal terms, Article 127.5 provides the treatybase to increase the supervisory power of theEuropean System of Central Banks (ESCB), andthus give prominent supervisory authority to theEuropean Central Bank (ECB). However, a new

institution could also be created by relevantmember states without prior definition in thetreaty, and could possibly be endorsed in a futuretreaty revision.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 12/20

12

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

12. See on this issueAlesina and Tabellini

(2007) or Maskin and Tirole(2004).

A further practical argument speaking in favour of giving supervisory powers to the ECB is the fact

that the ECB is a strong institution with resourcesand significant credibility earned before andduring the crisis. From the central bankstandpoint, risk management would also benefitfrom better access to information derived fromsupervisory authority. Conversely, the democraticand executive deficit of EU institutions createstwo risks if the ECB is made into Europeansupervisor. First, the accumulation of policyinstruments under its authority may make itappear too powerful given the absence of a strongcountervailing elected executive as exists innational environments. Second, in the (in the longterm, inevitable) event of future supervisoryfailures, the political pressure on the ECB couldresult in erosion of its monetary policy authorityand independence.

In both options, governance will be an importantconcern. If the European supervisor is the ECB, itwill be important that safeguards are introducedto reduce the conflict of interest betweenmonetary policy and supervisory action. This

could perhaps be achieved by giving supervisoryauthority to a separate body from the GoverningCouncil (which comprises the executive board andthe national central bank governors), which wouldretain the decision-making role on monetarypolicy. If a “partial” banking union is retained (cf item 2 above), national supervisors will retain arole and may need to be empowered in thegovernance as part of the European supervisor, asis the case of national central banks in the ECB. If a “complete” banking union is retained, national

supervisors will have to derive their authority fromthe European supervisor, and their relationshipwith national governments will need to becomprehensively redefined. Another aspect is thatif supervisory authority is given to the ECB, it willarguably need to be cleanly separated from anyresolution tasks in order to avoid ECB interferencewith fiscal policy. In such a scenario, additionalsupervisory powers should also be granted to theEuropean resolution authority.

Given this last point, and assuming thegeographical perimeter of the banking union islimited to the euro area, we see two options aspossible: either a single supervisor endowed with

resolution authority, which would be a newinstitution; or a combination of ECB supervision

with parallel (and coordinated) supervision by theresolution authority. These two options’ respectivestrengths and shortcomings are markedlydifferent and should be carefully considered bypolicymakers before making a final choice.

4. What resolution authority?

Bank resolution authority potentially involvessignificant choices about the distribution of costsbetween shareholders, creditors, uninsureddepositors, taxpayers, and/or surviving banks, aswell as about ownership and competition in thesector as a whole. The nature of such decisionsexcludes giving this task to an independentcentral bank whose legitimacy derives from thelimited scope of its mandate. Distributionalchoices in principle belong to elected officials andcan only be delegated to an independent agencyto the extent that it operates under clear rules andwith a robust framework of accountability12. In thecase of the euro area, the ECB is even less suitableto perform resolution tasks as it would be drawn

into inevitable controversies as regards thedistribution of losses and banking activitiesacross euro-area member states. In other terms,the ECB should not be the resolution authority forthe European banking union, even assuming ageographical scope limited to the euro area.

The European Commission with its DirectorateGeneral for Competition currently plays animportant role in bank resolution under itsauthority over state aid, as discussed byDewatripont, Nguyen, Praet and Sapir (2010).Granting resolution authority to the EuropeanCommission based on its competition policycompetencies would have the advantage of relying on an existing institution with experiencedstaff. However, the competition mandate is aboutdifferent policy objectives than those inherent inresolution authority. Furthermore, bank resolutionis arguably a less judicial and more politicalprocess than decisions on state aid cases. Finally,the Commission is an institution of the EU as awhole while bank resolution would have to beexercised within a more limited geographical

scope. Thus, we do not see it as practical to opt forthe European Commission as the resolutionauthority.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 13/20

13

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

Another option, again assuming that the perimeterof banking union is identical to the euro area,

would be to give the ESM direct authority toperform bank resolution. It could do so under thepolitical authority of the Eurogroup, extending itscurrent mandate to provide financial assistanceto euro-area member states. Decisions onassistance to member states and decisions onbank resolution are both political decisionspotentially involving the same taxpayers’ money.However, in most countries that do have a specialresolution regime for banks, it is kept at arm’slength from the fiscal authority to avoid excessivepoliticisation of decisions. Giving thisresponsibility to the ESM under the guidance of the Eurogroup would entail similar risks.Furthermore, for such a structure to be effective,different decision-making rules would need to bedefined from the current 85 percent majoritythreshold, which would risk blocking resolutiondecisions.

Ultimately, we think the European resolutionauthority should be vested in a new institutionstill to be created, even though it might have

strong links with the ESM – as is typically the casein national contexts between bank resolutionauthorities and treasuries. As discussed underitem 3, this new institution should also have somedegree of direct supervisory authority over thosebanks that are covered by the banking union. Itcould also be the same institution in charge of thefuture European deposit insurance system, asdiscussed below.

5. What deposit insurance?

As previously argued, there is little question thatthe European banking union must include acomponent of deposit insurance. An importantfurther choice to be made concerns the degree of centralisation of that deposit insurance function.

In national contexts, including those of EUmember states in the current framework, depositinsurance is at least implicitly backed by nationaltreasuries, in other words by fiscal resources.

However, national fiscal resources may be toolimited to credibly back national depositinsurance, and this relationship also contributesto the feedback loop between banking and

sovereign risks. Keeping insurance and fiscalbacking purely national would therefore

undermine both the effectiveness of depositinsurance as a mechanism to maintain trust in thebanking system, and the very purpose of thebanking union.

A first option would be to construct a system inwhich the national deposit insurance schemes(DIS) would subsist but would be partially re-insured by a European deposit reinsurance fund.Such a scheme would need to be only partial so asto avoid free-riding by individual countries. Inother terms, the national taxpayer would continueto back the national DIS with fiscal resources. If the national DIS were to be depleted, itscommitments would be met with a combinationof resources from the supranational fund and of national fiscal resources in a proportion to be setex ante and equal for all participating countries,for example half and half or a different proportion.By doing so, national governments would keep astrong interest in preventing imprudent bankingbehaviour, while the feedback loop betweenbanking and sovereign risk would be attenuated.

For the system to be fully credible, the Europeanreinsurance fund itself would need to have its ownfederal fiscal backing and the implications of thisfor fiscal union are discussed below.

In a second option, the supra-national re-insurance fund would be prefunded bycontributions from the member states’governments. In case the national DIS was to bedepleted, the supra-national fund would step in. Toavoid moral hazard and free-riding, the annual

contributions to the supra-national re-insurancefund could be made dependent on past drawingson the re-insurance scheme. Such an “experiencerating”, where subscriptions depend on the record,are well established moral hazard-mitigatingmechanisms that exist for example for carinsurance.

A third option would be to centralise the entiredeposit insurance scheme into one single federalsystem, akin to what exists in the US. This however

requires both that member states be entirelydeprived of all instruments of banking policy, toavoid perverse incentives that would lead to theaccumulation of risk in some countries’ banking

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 14/20

14

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

systems, and that a fiscal union be built in parallelto the banking union.

Deposit insurance should also be appropriatelyconnected with the supervision and resolutionauthority. In one possible design, the Europeandeposit insurance fund could be managed by aEuropean supervisory and resolution authority, asis the case in the US with the FDIC (in relation withother federal supervisory authorities).

6. What fiscal backstop?

Moving deposit insurance to the European levelwould amount to transferring a significantcontingent liability. Laeven and Valencia (2012)reckon that the median direct gross cost of anational banking crisis has been 4 per cent of national GDP in advanced economies and 10 inemerging economies, but tails of the riskdistribution are fat, as illustrated by the cases of Iceland (44 per cent), Ireland (41 per cent) andKorea (31 per cent), to mention advancedeconomies only. The pooling of resources atEuropean level would arguably diminish this cost

as more of it could be absorbed by depositinsurance (but it might also increase thefrequency of crises) and the adoption of aresolution framework that puts more emphasis onthe involvement of private shareholders andcreditors would also reduce fiscal costssignificantly. Nevertheless the potential liabilityremains significant.

For this reason a banking union requires somedegree of fiscal union, though it does not

necessarily entail a federal budget. The EU budgetcould remain of the same size as it is at themoment and there would be no need to increasestax revenues as long as a crisis does notmaterialise. But by mutualising insurance, itcreates a common contingent liability and for thisreason requires access to potential budgetaryresources13. To be credible, the ability to draw onpotential resources needs to be assured. Withoutexhausting all dimensions of the fiscal uniondebate that go well beyond the scope of this paper,

one possible way would be for a European fiscalentity (or quasi-treasury) to be given a limitedand contingent taxation capacity for the purposeof resolving banking crises, up to a certain

proportion of GDP and to be triggered only in theevent of depletion of the European deposit

insurance. This would make it possible to convertthe potential income stream into an interventionchest, either through accumulation within a fund,or through borrowing, or through a combination of the two.

Specifically, we do not believe that this fiscal orquasi-fiscal function can be adequatelyaddressed by an ex-ante burden-sharing rule, forexample the ECB capital key or a variant of it,taking into account the size of each country’sbanking sector. As this function would draw onfiscal resources, it is unlikely that this solutioncould be done without making interventiondependent on parliamentary approval in theparticipating states. Experience with assistanceto states in distress has shown the limits of suchschemes and the risks they represent to thecredibility of the insurance. Burden-sharingarrangements are inherently less robust as theyentail the risks that states, which retain theultimate decision, will backtrack on commitments.

7. What governance and accountability?

Resolution of banking crises may involve theclosing or restructuring of financial institutions aswell as the commitment of taxpayers’ money.Often these decisions – whose economic andfinancial consequences can be huge – have to betaken in a context of imperfect information andunder the pressure of time. The assignment of thisresponsibility to the European level thereforerequires the creation of an effective governance

structure, with implications not only for theinstitutions tasked with banking policy but alsofor European institutions more generally.

As discussed above, this structure could not relysolely on existing institutions such as theEuropean Commission, the EBA and the ECB. Thecreation of one or several new institutions at theEuropean level appears inevitable if a functioningbanking union is to be established – even as theEU may still hope to avoid the unnecessary

degree of institutional fragmentation that existsat the federal level in the US, with multiplesupervisors overlapping for different categories of financial institutions. Furthermore, the potentially

13. This is one of the rea-sons why a banking union

would entail the creation of some form of a European

treasury. See e.g.Marzinotto, Sapir, and Wolff

(2011).

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 15/20

15

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

distributional character of resolution decisionsand the potentially large fiscal cost of banking

crises call for political responsibility.

This could entail the appointment of a ministry of finance with responsibility for oversight of banking policy and crisis managementcoordination, as advocated by Trichet (2011). Theministry of finance would rely on the ESM forresolution matters. Equally important is thecreation of an adequate framework of accountability to European citizens through aproperly empowered European Parliament thatwould comply with the principle of equalrepresentation, and also to a properrepresentation of the member states. Ultimately,the creation of a banking union will thereforerequire making progress with political union.

4 A POSSIBLE PATH TOWARDS SUSTAINABLEBANKING UNION

Recent weeks have seen the vision of a Europeanbanking union endorsed by an impressive arrayof European and international leaders. However,

that vision is very distant from the current reality,and the path from here to there is bound to bebumpy. European leaders should avoid four majorpitfalls in their forthcoming discussions on how tocharter such a path.• The first pitfall is to think that a long-term visionis sufficient to stabilise the situation in the shortrun. Lost investor confidence cannot be re-established only by presenting a compellingvision for the long-term future. More immediateinitiatives are needed and they must also be

consistent with the framework envisaged for thelong term.• The second pitfall is to believe that bankingunion can be separated from the other responsesto the crisis. Both in the short term and in thelonger term, banking policy choices areinseparable from those made in terms of fiscalpolicy and of political institutions. One might saythat banking union and fiscal union are mutualcomplements rather than substitutes, and thatboth require a form of political union that goes

beyond the current features of the EU. While short-term decisions must be made to the extentpossible within the framework of current treatiesand institutions, EU institutional transformation

including both more democratic representationand accountability, and stronger European

executive decision-making capability, is anecessary condition for the build-up of a bankingunion that could withstand future financialshocks.• A third pitfall is to think that the introduction of a banking union now can be used as a way todistribute existing debt overhang in a number of countries across euro-area taxpayers in anuntransparent way. Banks in some countries aremuch more vulnerable than in others due toexisting debt overhang. Implementation of measures to stabilise the financial system in theshort term therefore involves decisions as towhether losses accumulated in some banks, andlikely to result in injections of public money,should be borne by sovereigns on a country-by-country basis, or should be partially mutualised,or should be at least partly imposed on creditors of banks. These decisions should not be made in away that hides them from the public. The currentpublic information on banks’ true situation ishighly imperfect, and national supervisors havestrong incentives to retain privileged information

and to hide banking losses in the hope they willeventually be mutualised. The crisis managementand resolution approach should counter theseincentives in a credible manner.• A fourth pitfall is to believe that steps towardsbanking union can suffice to restore trust indeposits across the euro area. Trust in deposits isundermined by two factors: fears about acountry’s exit from the euro area and concernsabout the national-level guarantee of deposits asorganised in the national deposit insurance

system (DIS), assuming no change of currency.The first fear factor cannot be addressed with theinstruments of banking policy, and can only bemitigated by an unambiguous politicalcommitment to preserve the integrity of the euroarea no matter what, including the continuedmembership of all its current member countries.Declarations until now have stopped short of this,often by stating the undesirability rather than theimpossibility of country exits. Ultimately, anunlimited political commitment may be required

to preserve the integrity of the euro area byreplacing deposit withdrawal fully with ECBliquidity.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 16/20

16

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

Against this background, the aim of the transitionshould be to provide a credible path to the new

policy regime, to ensure that there is no vacuum orambiguity in the assignment of policyresponsibilities, to provide total transparency onany transfers resulting from legacy losses, to keepthese transfers at a minimum level to the extentthat this remains compatible with thepreservation of financial stability, and to showcommitment to act early so as to regain trust.

It will be of particular importance to map a credibleway to break the negative feedback loop betweensovereign and banking sector fragility. Against thisbackground, we suggest a graduated approachthat preserves as much as possible the principleof national responsibility for restoring bankingsystems back to soundness before the movetowards banking union, while ensuring that swiftaction is taken where it is needed. If this approachwere to prove insufficient, responsibility forresolving the current banking crisis may be moveddirectly to the European level, either for thosecountries that are in greatest difficulty or, if thisis insufficient to restore confidence, for all

countries committed to banking union.

The premise for the graduated approach is thatthere should be a clean and neat separationbetween legacy problems, which fall under theresponsibility of current resolution authorities –and the sovereigns backing them – and futurerisks, which are to be taken on by the newcommon European banking policy framework –and the funding scheme backing it. Mutualisationof the resolution and its cost should only be

envisaged in the exceptional cases where theactual or potential fiscal cost of resolving thecurrent crisis exceeds the capacity of thesovereign, and even in this case a cost- and risk-sharing arrangement should be devised withEuropean partners.

At the same time a comprehensive, thorough andintrusive screening of all banks which would beincluded in the future banking union should beimmediately performed by a European institution

or delegated to an ad-hoc body under centralisedcontrol. This is because, once the perspective of moving supervision, deposit insurance andresolution to the European level is agreed, national

authorities will have a strong incentive to concealactual losses in the hope that any future cost will

be mutualised.

These considerations lead to the followingscheme, which is intended to minimiseresponsibility overlaps and to address incentiveissues. The underlying principle is that thereshould be clarity of responsibility for crisismanagement, with primary responsibility at thenational level and responsibility at the Europeanlevel only if there is no workable alternative. In allcases, the principle of “he/she who pays, controls”will apply.• Leaders of all euro-area countries, and possiblyalso of other willing EU member states, shouldestablish a European Supervisor, which will act asthe anchoring institution of the future bankingunion even though its operational build-up maytake some time. As discussed in section 3, onepossibility would be to empower the ECB withsupervisory powers, the other alternative being toset up a new institution.• In parallel, a special European Banking SectorTask Force, with an appropriate mix of public

officials and private-sector specialists ontemporary assignment would be created to helpcoordinate the immediate steps of crisismanagement. Posen and Véron (2009)highlighted the relevance of temporary crisis-management entities to address systemic crises,such as the Swedish Bank Support Authority in theearly 1990s; since then, the broadly successfulauto industry task force in the US (2009), as wellas the restructuring of AIG by a special unittemporarily established within the US treasury,

have provided additional examples of theusefulness of ad-hoc temporary bodies insystemic crisis management. The temporary taskforce would work in close cooperation with the ECBand with the new European Supervisor, if separate.• In a unanimous statement, the leaders of participating countries should commit to complywith the steps described below, and should passemergency legislation in their respectivecountries to confirm this commitment and togrant the Task Force full access to banks and

supervisory information. Such legislation mightalso introduce the possibility for nationalauthorities to impose losses on creditors in thecontext of a special resolution regime in those

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 17/20

17

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

countries which have not yet established one. Toan extent this might anticipate the “bail-in”

proposals recently made by the EuropeanCommission (European Commission, 2012).• The Task Force would perform a rigorous capitalassessment of the most important banks whichare to be covered by the European banking union– eg those included in the 2011 stress tests. TheEuropean Supervisor, if already up and running atthat stage, would help in this task and also engagein the complementary task of supervising smallerbanks that would also fall within the scope of thebanking union.• One key feature of the capital assessment isthe value to be attributed to portfolios of sovereigndebt held by the assessed banks. Given currentmarket conditions in the euro-area sovereign debtmarket, we believe these should not be assessedat market value in the context of the capitalassessment, but that a reference value should beprovided for the purpose of that assessment by aconsensus view of the ESM and IMF.• If a bank is found through this assessment notto meet applicable capital requirements, thenational authorities, working in close cooperation

with the Task Force, should take the appropriatemeasures.• If the cost of carrying out such measures in agiven country is found to threaten thesustainability of national public finances or theirperception by financial markets, that countryshould request the support of the ESM14. Theconditionality of such support could includedirections on the specific measures to be taken torestore the soundness of banks found to beundercapitalised or insolvent under the Task

Force’s assessment, the determination of whichmay associate the Task Force itself.• Communication of the capital assessmentsshould be carefully coordinated and should not beenvisaged before adequate progress has beenmade towards defining the approach for eventualbank restructuring and sovereign assistance.Assuming smooth establishment of the Task Forceand sufficient resources and focus, the capitalassessments and corresponding restructuringpackages could be announced publicly at some

point in the first half of 2013.• In parallel, the permanent institutions of thebanking union (supervision, deposit insuranceand resolution authority as discussed in section

3) will be built up and will take over theirresponsibilities in relation to relevant financial

institutions as soon as practical.• The overarching principle should be tominimise the cost of resolution to taxpayers.Creditors should be forced to participate in therestructuring of insolvent banks to the maximumextent possible. The removal of currentuncertainties about banks’ true balance sheetstrength, and the simultaneous creation of thepermanent institutions of the European bankingunion, should result in a marked improvement infunding conditions across the EU that would morethan offset the effect resulting from creditorlosses in banks found insolvent.

Should the above approach run into difficulty,particularly if national authorities fail to cooperateadequately and/or if the banking/sovereignfeedback loop leads to further market dislocation,additional steps might be considered.

This might happen at the level of one individualcountry under assistance from the ESM. If themanagement and resolution of the national

banking situation appears beyond the financialand operational capacity of that country, then itshould accept the direct and early transfer of responsibility for its banking system to theEuropean level in anticipation of the futurebanking union. In such an event, the EuropeanBanking Sector Task Force should be empoweredto be the resolution authority for that country, andwould rely on the ESM’s resources, withappropriate channels of accountability. A limitedinvolvement of national fiscal resources may still

be needed to mitigate moral hazard. This mightentail, in particular, the direct purchase by theESM (or a special vehicle under the ESM) of equityor other instruments issued by banks of thecountry in question, in accordance withrestructuring plans negotiated by the Task Forceon behalf of participating member states actingcollectively.

If even this proves insufficient, leaders mightconsider further expansion of the role of both the

ESM and of the European Banking Sector TaskForce, and consider a move to put all participatingcountries’ banking systems under the Task Force’sresolution authority to address any risk of intra-

14. We assume that theESM will be in place shortlyand will be the instrument

of intervention in the time-frame envisaged for bank

crisis management. If thereare delays in the establish-ment of the ESM, the Euro-

pean Financial StabilityFacility (EFSF) should be

mobilised instead, withappropriate adjustments to

its mandate if needed.

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 18/20

18

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

system contagion. The system-wide approachwould help the Task Force to maximise the

possibility of imposing burden-sharing on theinsolvent banks’ creditors, even though it mightnot be possible to have a uniform approach acrossmember states concerned given differences inlegal frameworks. To the extent that the use of public money might be necessary, the Task Forceshould negotiate a combination of national fiscalresources and ESM, depending on each country’sor bank’s specific situation. This would inevitablygive rise to recrimination about differentialtreatment, but the assumption here is thatcredible alternatives for restoring the Europeanbanking sector back to soundness would bescarce.

If circumstances warrant it, a more centralisedapproach may also be applied to restoring trust indeposits and protecting them not only against therisk of failure of individual banks, as national DISsalready do, but also against the risk of the nationalgovernment itself failing to backstop the DIS. Thecurrent financial rescue scheme with theEFSF/ESM does this only implicitly and indirectly

by providing financial assistance to countries thatrequest it. Depositors in the countries in questioncould, however, fear that the national DIS would besubordinate to other claims against thegovernment even though so far bank creditorshave made only modest losses if any, and alldeposits have been spared loss. Moreover, trust inthe willingness to move towards a more integratedbanking union could be increased by introducinga partial re-insurance of DIS that would establisha direct link between the ESM and the national DIS.

Moral-hazard effects could be dampened byrequiring that, if the national DIS were to draw onESM support, then future additional levies wouldbe imposed on banks headquartered in therelevant member state. The advantage of such a“deposit reinsurance” scheme at the Europeanlevel is that it would show that a concrete steptowards a true banking union was being takenwhile at the same time having a mechanism toreduce moral hazard. This could increase overallconfidence in the willingness of Europe genuinely

to move forward towards a banking union, as itwould be strong concrete signal of a move towardsa federal element of banking union.

Consensus on such initiatives is not going to comeeasily, and their implementation is riddled with

numerous major execution risks and moral-hazardconcerns. But these will have to be measuredagainst the downsides of inaction and the risk of further market dislocation, and eventual possibleeuro-zone unravelling. The path towards a bankingunion cannot possibly be smooth, and is likely tobe a white-knuckle ride at times. But for Europe,the alternatives are clearly worse.

5 CONCLUSION

The euro crisis is now in its third year and there isstill no end in sight. The main reason for thissituation is that, although much has been donesince 2010 (in fact since 2007) to quell the crisis,some of its root causes have been left largelyunattended. In particular, no mechanism has beenput in place to address the feedback loop betweensovereigns and banks that plagues a number of euro- area countries. The problem is that puttingin place the necessary mechanism would involvetransforming the euro area into a full-fledgedmonetary union with a fiscal and banking union. In

turn, this would require agreement on sharingsovereignty, mutualising risk and creatingEuropean-level accountability channels that wouldamount to creating a political union.

Although nothing short of such political unionmight ultimately be sufficient to ensure the long-term viability of the monetary union, it is equallyclear that it will take significant time to achieveeven under the most optimistic assumptions.What appears possible, however, at this juncture is

to take a decisive step forward by creating abanking union. This step would not only help toaddress directly the negative feedback loopbetween sovereigns and banks. It would alsodemonstrate that the euro area has the politicalwill to draw the lessons from the crisis and tomove towards a stronger framework thatpreserves the full integrity of the currentmonetary union. In turn this would have majorbeneficial effects on the current crisis bydramatically shifting expectations and anchoring

them on more favourable ground.

We fully realise that, given the currentcircumstances, it will be economically and

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 19/20

19

B RUE GE L

POLICYCONTRIBUTION

Pisani-Ferry, Sapir, Véron and Wolff WHAT KIND OF EUROPEAN BANKING UNION?

politically difficult to agree on a design for thebanking union and even more difficult to take the

necessary first steps that are outlined insummary form above. Yet we also believe that thecurrent circumstances make it imperative that abanking union be created and that concrete steps

be adopted rapidly. Clearly, not all choices can bemade in the short term, but the sequence we have

outlined in this paper could allow a quick start tothis long process. Conversely, failure to take thenecessary decisions could greatly endanger theviability of the monetary union.

REFERENCES

Alesina, Alberto and Guido Tabellini (2007) - “Bureaucrats or Politicians? Part I: A Single Policy Task”,

American Economic Review, Vol. 97, n° 1, pp 169-179.

Angeloni, Chiara and Guntram B. Wolff (2012) – “Are banks affected by their holdings of Governmentdebt?”, Bruegel Working Paper 2012|07, March

Bank for International Settlements (BIS) (2010) - “Core Principles for Effective Deposit Insurance

Systems-A methodology for compliance assessment”, December

Bank for International Settlements (BIS) (2011), “Resolution policies and frameworks – progress so

far”, July

Cihak, Martin, and Jörg Decressin (2007) – “The Case for a European Banking Charter”, IMF Working

Paper WP/07/173

Dewatripont, Matthias, Gregory Nguyen, Peter Praet and André Sapir (2010). “The role of state aid

control in improving bank resolution in Europe”, Bruegel Policy Contribution No 2010/04, May.

European Central Bank (ECB) (2012) – “Financial Integration in Europe”, April

European Commission (2012) – “Proposal for a Directive of the European Parliament and of the Council

establishing a framework for the recovery and resolution of credit institutions and investment firms”,

COM (2012)280/3, 30 May

Financial Stability Board (FSB) (2011) - “Key Attributes of Effective Resolution Regimes for Financial

Institutions”, October

Financial Stability Board (FSB) (2011) – “Policy Measures to Address Systemically Important Financial

Institutions”, 4 November

Financial Stability Board (FSB) (2012) - “Peer Review of Canada-Review Report”, 30 January

Financial Stability Board (FSB) (2012) - “Peer Review of Switzerland-Review Report”, 25 January

Financial Stability Board (FSB) (2012) - “Thematic Review on Deposit Insurance Systems- Peer Review

Report”, February

Fonteyne, Wim, Wouter Bossu, Luis Cortavarria-Checkley, Alessandro Giustiniani, Alessandro Gullo,

Daniel Hardy, and Sean Kerr (2010) - “Crisis Management and Resolution for a European Banking

System”, IMF Working Paper, March

Gerlach, S., Schulz, A. and Guntram B. Wolff (2010) – “Banking and Sovereign risk in the Euro Area”,

CEPR Discussion Paper No. DP7833, May

IMF (2012) - 2012 Article IV Consultation with the Euro Area Concluding Statement of IMF Mission,

International Monetary Fund, June 21Jickling, Mark and Edward V. Murphy (2010) - "Who Regulates Whom? An Overview of U.S. Financial

7/31/2019 Pc 2012 12 Banking Union Policy Contribution v2906

http://slidepdf.com/reader/full/pc-2012-12-banking-union-policy-contribution-v2906 20/20

20

B RUE GE L

POLICYCONTRIBUTION

WHAT KIND OF EUROPEAN BANKING UNION? Pisani-Ferry, Sapir, Véron, Wolff

Supervision”, Congressional Research Service, December

Laeven, Luc and Fabian Valencia (2012) – “Systemic Banking Database: An Update”, IMF Working Paper

WP/12/163, June

De Larosière, Jacques and co-authors (2009) – ”Report of the High-Level Group on Financial

Supervision in the EU”, European Commission, 25 February

Marzinotto, Benedicta, Sapir, André and Guntram B. Wolff (2011) – “What kind of fiscal union?”, Bruegel

Policy Brief 2011/06, November

Maskin, Eric et Tirole, Jean (2004), “The Politician and the Judge : Accountability in government”,

American Economic Review, Vol. 94 n° 4, pp. 1034-1054.

Merler, Silvia and Jean Pisani-Ferry (2012) – “Sudden Stops in the Euro Area”, Bruegel Policy

Contribution 2012/06, March

Pisani-Ferry, Jean (2012) – “The Euro Crisis and the New Impossible Trinity”, Bruegel PolicyContribution 2012/01, January

Pisani-Ferry, Jean and Guntram B. Wolff (2012) – “Propping up Europe?”, Bruegel Policy Contribution

2012/07, April

Pisani-Ferry, Jean, Sapir, André and Guntram B. Wolff (2012) – “The messy rebuilding of Europe”,

Bruegel Policy Brief 2012/01, March

Posen, Adam and Nicolas Véron (2009) – “A solution for Europe’s banking problem”, Bruegel Policy

Brief 2009/03, June

Trichet, Jean-Claude (2011) – “Building Europe, building institutions”, Speech on receiving the Karlpreis

2011, 2 JuneVéron, Nicolas (2007) – “Is Europe ready for a major banking crisis?”, Bruegel Policy Brief 2007/03,

August 2007