Embed Size (px)

Citation preview

Slide 1

PASSENGER CARS

Increasing industry activity dominates this section but let’s start with a review of the North American lubricants market.

Slide 2

P A S S E N G E R C A R S

Conventional API SN/ILSAC

GF-566%

API SL and below

5%

Top Tier9%

High Mileage9%

Mid Tier11%

NA SHOW PCMO4

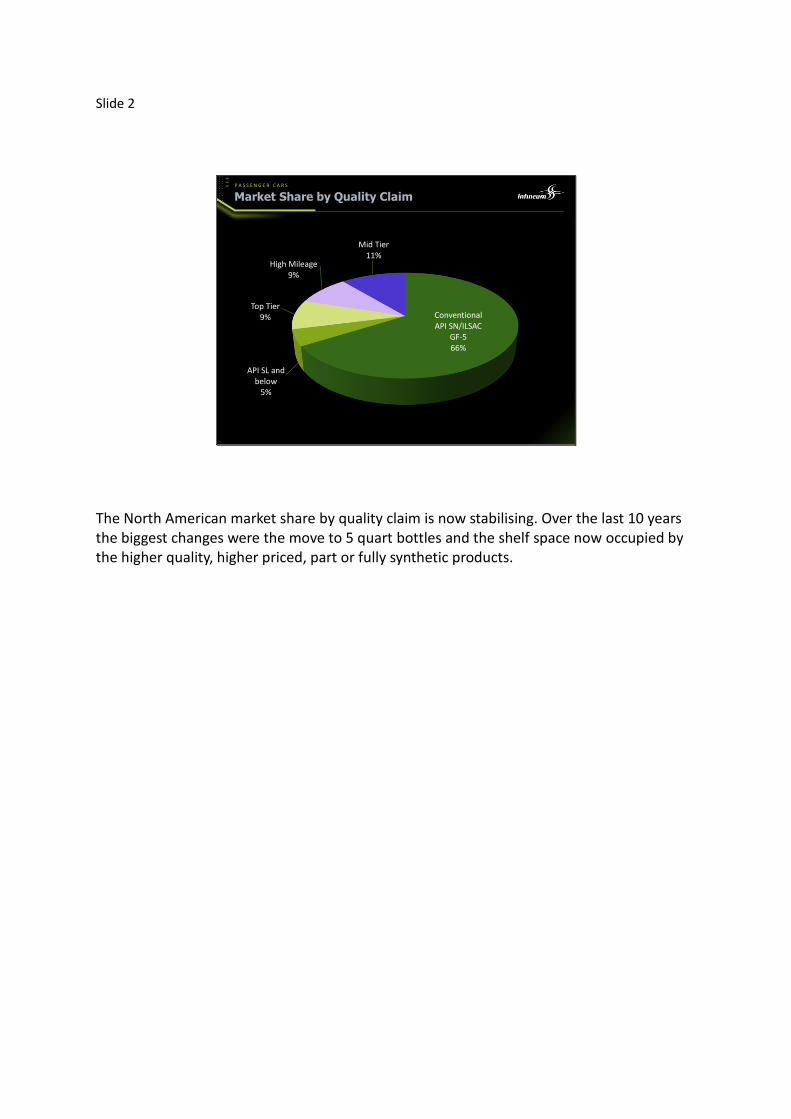

The North American market share by quality claim is now stabilising. Over the last 10 years the biggest changes were the move to 5 quart bottles and the shelf space now occupied by the higher quality, higher priced, part or fully synthetic products.

Slide 3

P A S S E N G E R C A R S NA SHOW PCMO11

Despite slow market penetration,ultra low viscosity fluids are on the increase

0

20

40

60

80

100

2000 Today 2017 Forecast 2021 Forecast

Viscosity grade trend forecasts in the North American PCMO market

SAE 0W-XX SAE 5W-20 SAE 5W-30 SAE 10W-30

SAE 10W-40 SAE 20W-50 Monogrades Other

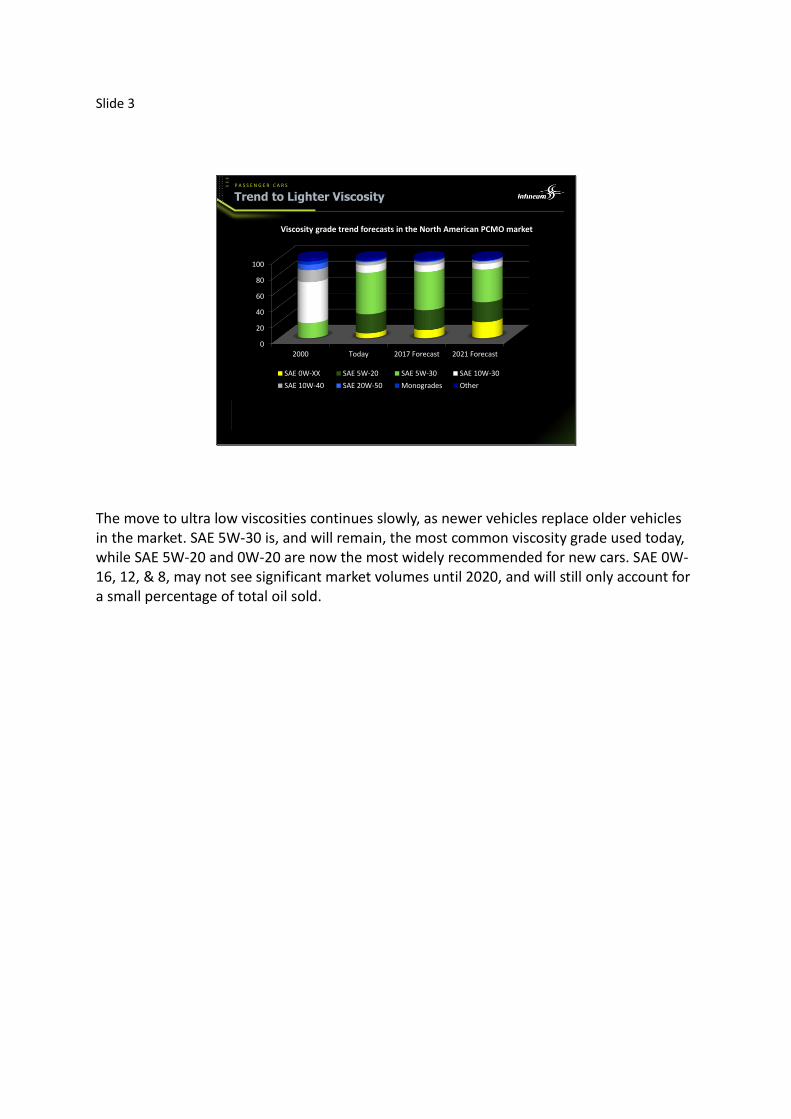

The move to ultra low viscosities continues slowly, as newer vehicles replace older vehicles in the market. SAE 5W-30 is, and will remain, the most common viscosity grade used today, while SAE 5W-20 and 0W-20 are now the most widely recommended for new cars. SAE 0W-16, 12, & 8, may not see significant market volumes until 2020, and will still only account for a small percentage of total oil sold.

Slide 4

P A S S E N G E R C A R S PCMO21NA SHOW

PCMO F-1

PCMO F-2

Bob Proctor from Honda North America followed by Selda Gunsel vice-president of Shell Global Commercial Technology, share their thoughts on ultra low viscosity oils. Bob Proctor: For 0W-16 usage in North America, we hope to consider all engines for applications. We are investigating looking at engine oil applications lower than our current viscosity grades used for turbo engines, which is a 5W-30. So we are investigating a 0W-20 and even further, 0W-16, but of course that technology is a little bit down the road. We believe that we will have to require new tests for the 0W-8 and 0W-12 viscosity grades. Specifically the fuel economy test is one we’re pretty certain will have to be changed. And the other tests, certainly we are investigating, but there probably will be some changes for those grades, for the other sequence testing. Selda Gunsel: We believe that GTL base oils are well suited to make 0W-12 and 0W-8 engine oils, which cannot be made from typical Group III base oils alone. They provide the right viscometrics to make 0W grade, while meeting the demand in performance and volatility requirements of the OEMs.

Slide 5

P A S S E N G E R C A R S

General Motors18%

Toyota14%

Honda9%

Nissan8%Hyundai Group

8%

BMW2%

Mercedes-Benz2%

VW + Audi4%

Mazda2%

Subaru3%

Other2%

Fiat Chrysler13%

Ford15%

PCMO12NA SHOW

In 2014, there were no major shifts in OEM market share although Fiat Chrysler Automobiles continued its remarkable comeback since 2008. VW has not gained the market penetration they desired in North America. Japan held the top five best selling cars, but the Ford Fusion did come in 6th place. Detroit OEMs held four of the top five bestselling light trucks. Toyota’s Prius hybrid fell from the top ten best selling cars, as other hybrids gained share. Sales of full electrics like the Tesla, fell in 2014 from their highs in 2013.

Slide 6

P A S S E N G E R C A R S

Vehicle population continues to grow• China accounts for 40% of the increase

• Significant growth in developing markets

‒ India, Indonesia, Brazil, Mexico

Emissions limits tightening in many countries

Tough fuel economy and CO2

emissions limits

OEMs must respond with hardware innovations

1.7 Billion light-duty vehicles by 2040

PCMO1NA SHOW

Rising personal incomes in developing economies is a key contributor to the world’s growing light duty vehicle population. However, this growth comes at a time when emissions limits and fuel economy regulations are being introduced and tightened in many countries. OEMs are responding with hardware design changes to ensure compliance with mandated limits and, in the case of CO2, avoid heavy financial penalties.

Slide 7

P A S S E N G E R C A R S NA SHOW

33%hybrids in global

fleet by 2040.Given the current price of crude this

forecast is likely optimistic.

PCMO2

Fuel economy drives the development of new hardware

0

50

100

150

2010 2020 2030 2040

New Vehicle Sales by Type, Millions

Gasoline Diesel Gas/LPG

Full hybrid Electric/fuel cell

Data so

urce: Exxo

n M

ob

il

Fuel economy improvements of gasoline and diesel vehicles continue: from advanced transmissions, turbocharging and start/stop systems. We expect conventional powertrains will continue to lead in market share for at least the next 15 years. However, some expect hybrids could grow to 50% of sales by 2040 and make up about one-third of the global light-duty fleet. These forecasts could move back if crude prices stay low and consumers are driven back by the affordability of conventional powertrains.

Slide 8

P A S S E N G E R C A R S

Kazuo Yamamori | Toyota Motor Corp., Tribology Material Dept.,

Material Development Division – Project Manager

PCMO13NA SHOW

PCMO D-1

Yamomori-san shares Toyota’s thoughts on emissions and the global vehicle market. Kazuo Yamomori-san: From the standpoint of global environmental protection, it is important to reduce carbon dioxide (CO2) emissions and exhaust gas, such as NOx and others. To achieve CO2 emissions reductions, an efficient power train system with less fuel consumption is important. And to achieve low emissions, it is important to develop a power train system with an exhaust system that is low in emissions.

Slide 9

P A S S E N G E R C A R S NA SHOW PCMO3

US new car sales pass 2007 pre-economic crisis levels

5.9% growth in vehicle sales

• Large and luxury brands post biggest gains

CAFE regulations drivehardware change

• Boosted gasoline gaining popularity

• Hybrids sales drop 8.8%

New hardware drivesspecification changes

0

5

10

15

20

2013 2014

Mill

ion

s

US vehicle sales

US OEMs Japan OEMsEU OEMs Hyundai GroupTata

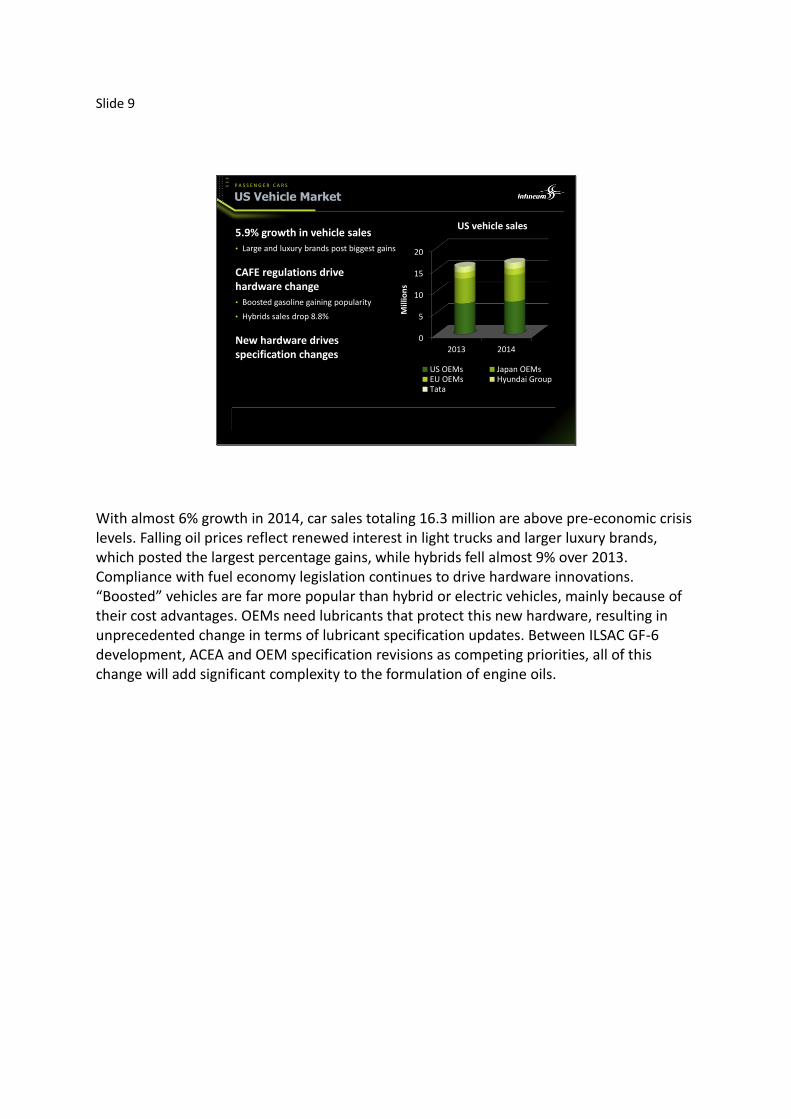

With almost 6% growth in 2014, car sales totaling 16.3 million are above pre-economic crisis levels. Falling oil prices reflect renewed interest in light trucks and larger luxury brands, which posted the largest percentage gains, while hybrids fell almost 9% over 2013. Compliance with fuel economy legislation continues to drive hardware innovations. “Boosted” vehicles are far more popular than hybrid or electric vehicles, mainly because of their cost advantages. OEMs need lubricants that protect this new hardware, resulting in unprecedented change in terms of lubricant specification updates. Between ILSAC GF-6 development, ACEA and OEM specification revisions as competing priorities, all of this change will add significant complexity to the formulation of engine oils.

Slide 10

P A S S E N G E R C A R S PCMO14NA SHOW

PCMO B-1

PCMO B-2

As with all of the new ILSAC GF-x specifications, the role of the lubricant is key in meeting the next series of fuel economy targets enabled by new hardware, as described by Ron Romano of Ford and Angela Willis from GM. Ron Romano: To try and achieve the CAFÉ that will be required in the near future, Ford is relying on Eco-Boost, weight reduction, and 9 and 10-speed transmissions. Angela Willis: GM, like other OEMs, are working on new technologies to meet the upcoming more stringent new CAFÉ standards. Many of the technologies including things like hybrid, especially plug-in hybrids, light weighting coatings, and other new innovations which you will be seeing here in the near future to meet those requirements. OEMs need to be certain that lubricants will deliver sufficient protection to their new hardware – which means we are also entering a year of unprecedented change in terms of lubricant specification updates.

Slide 11

P A S S E N G E R C A R S

Ford Sequence VH

Ford LSPI

Ford Chain Wear

Toyota Sequence IVB

GM Sequence VIE

GMOD*

Chrysler IIIH*Will not be an ASTM standard

PCMO15NA SHOW

With 7 new tests under development, we are undertaking by far the biggest turnover of tests for this new category. ILSAC GF-3 development with 4 new tests was the closest comparison to the current challenge.

Slide 12

P A S S E N G E R C A R S PCMO16NA SHOW

PCMO D-3

PCMO D-4

PCMO D-2

PCMO D-7

Ron Romano of Ford, Bruce Royan, Lubricants Technology manager at Infineum, and Bob Proctor of Honda, share their thoughts on GF-6. Ron Romano: Yes, we feel the present timing is achievable. Most of the tests are nearing completion and development, so we are starting procedure matrix. So we think that we'll be able to meet the timeline. ILSAC feels that all six tests still need to be included in the GF-6 spec. We feel pretty confident that will be able to include them all with the development process that we've made on them. It is very possible that both the GM oxidation test and the Chrysler oxidation test may wind up in GF-6. If we do have to pick between one of them it'll probably be based on the precision of the test, which one is already in time, and correlation to the 3G in field. Bruce Royan: I think from an industry perspective, the two main drivers are the introduction of low-speed pre-ignition as a parameter, and also the increased focus on fuel economy. Clearly the introduction of GF-6B, with high-temperature, high-shears of less than 2.6 millipascals, represents a big challenge for us. Bob Proctor: At this point in time probably the Sequence 3 and Sequence 4 tests seemingly are what we find to be most critical to what will be necessary for Honda’s needs specifically. Regarding LSPI tests, we believe that Honda’s engines will be able to withstand the test conditions established by the LSPI test being created by Ford right now, based on the lower temperatures and operating conditions that we see right now.

Slide 13

P A S S E N G E R C A R S

Downsized and boosted engines exhibit irregular combustion• Severe knocking

• Cracked piston ring lands and skirts

• Cylinder head damage

• Increase emissions

• Lower fuel efficiency

LSPI test focus• Development of test

methodologies

• Evaluate new lubricant technologies

• Enable new hardware without compromising performance

NA SHOW PCMO10

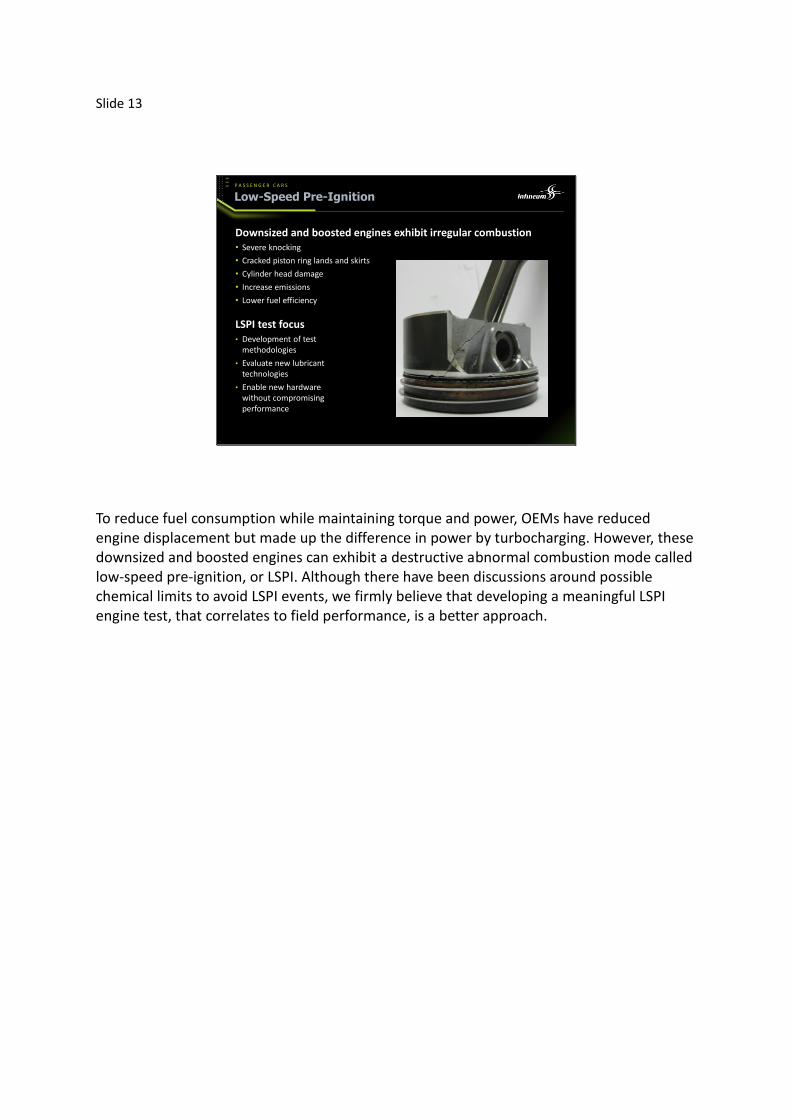

To reduce fuel consumption while maintaining torque and power, OEMs have reduced engine displacement but made up the difference in power by turbocharging. However, these downsized and boosted engines can exhibit a destructive abnormal combustion mode called low-speed pre-ignition, or LSPI. Although there have been discussions around possible chemical limits to avoid LSPI events, we firmly believe that developing a meaningful LSPI engine test, that correlates to field performance, is a better approach.

Slide 14

P A S S E N G E R C A R S NA SHOW PCMO17

PCMO D-6

PCMO D-5

Kazuo Yamamori | Toyota Motor Corp., Tribology Material Dept.,

Material Development Div. – Project Manager

Yamamori-san returns to share his thoughts on lubricant connected LSPI events. Yamamori-san: Improvement of fuel efficiency should be the most important challenge. Durability requirements and reliability requirements continue to be present, as a lowering of standards will not be permitted. In a down-sized direct injection turbo-charged engine, the lower speed, higher torque area is used more, in order to maximize its fuel efficiency. In this area, abnormal combustion called LSPI is a problem. It is known that the oxidation property of an engine oil, in addition to that of a fuel, affects the LSPI phenomenon. The frequency of LSPI can be reduced more in Group III BS, as compared to Group I BS, where oxidation reactions are more likely to happen. ZnDTP and molybdenum additives are also effective in proportion to the contents, due to their anti-oxidation performance. Meanwhile, calcium detergents tend to contribute to the frequency of LSPI occurrence, and therefore, their usage needs to be reduced.

Slide 15

P A S S E N G E R C A R S

June 2015: Tests ready for matrices?

July 2015: Start precision matrices

January 2016: ASTM test acceptance

August 2016: AOAP approval of GF-6

January 1, 2018: API First License Date

PCMO5NA SHOW

Here are the key dates from the current official GF-6 timeline. The hope is that Industry matrices will start in the next few months, leading to ASTM test acceptance of the 6 new tests in early 2016, and AOAP approval of GF-6 in early 2017. January 1, 2018 is the target date for first license of ILSAC GF-6.

Slide 16

P A S S E N G E R C A R S NA SHOW PCMO6

Current dexos™ 1 approvals start to expire 2H 2015

A number of new tests requirements

• Low speed pre-ignition

• Aeration

• Vehicle Fuel economy

• GM oxidation (GMOD)

• Turbochargers

Service fill by end of 2015

Factory fill in 2016

GM will use SAE 0W-20 for the majority of their new engines, replacing SAE 5W-30

General Motors (GM) is looking to introduce its dexos™ 1: 2015 specification in the second half of 2015 when current dexos™ approvals begin to expire. The development of GM tests are critical to meeting this proposed timing. The initial specifications will be a combination of old and new tests. GM is planning to use new dexos™ oils in service fill applications prior to year end 2015, but the deployment of next generation factory fill oils is unlikely before at least 2016. It seems very likely that GM will specify SAE 0W-20 for their new engines going forward.

Slide 17

P A S S E N G E R C A R S PCMO18NA SHOW

PCMO A-1

PCMO A-2

PCMO A-3

PCMO D-8

Angela Willis updates us on the dexos 1: 2015 specification, followed by an oil marketer’s view from Thom Smith of Ashland, and Bruce Royan describes the particular challenges faced by the additive suppliers particularly around the timing of these new specifications. Angela Willis: So far, the feedback in terms of the second generation dexos 1 has been relatively positive. We anticipate that dexos 1 second generation oils to be at the dealerships close to the end of this year. In terms of the aftermarket outside the dealerships, we would be looking at possibly first quarter of 2016. In terms of the longtime between GF-6 and second generation dexos 1, GM is not concerned at all with that long period of time. As a matter of fact, GM actually embraces it and thinks it’s a wonderful opportunity in terms of the additive companies and oil companies to get a jump start on the new technologies that would be required for GF-6 by going through and formulating its next generation dexos 1. Thom Smith: It’s certainly going to be a challenge for the next generation dexos 1. Our understanding is that GM is requiring some products to meet the new requirement as early as fourth-quarter of this year, and that all products need to be converted over to the new dexos 1 by August of next year. So this is going to be a real challenge for a couple of reasons. First of all, there’s a lot of testing that’s going to be – have to be done, and there’s a limited availability of engine tests. But on top of all of this, what we’re doing is we’re doing dexos before we do GF-6. Bruce Royan: When GF-6 is introduced, there is every chance that this dexos specification will need to be reformulated at that time. What is often forgotten is that industry specifications such as GF-6 or PC-11 or the European ACEA specification in today’s world are simply baseline performance requirements. Almost always Infineum has to develop OEM claims on top of these base requirements. This adds considerable complexity to the process.

Slide 18

P A S S E N G E R C A R S NA SHOW PCMO7

Proposed new C5 category • SAE 0W-20 and SAE 5W-20 viscosity grades

with HTHS ≥ 2.6 mPa·s

• Opportunity to reassess categories and reduce complexity

Test development influencing release date• DV6 and CEC L-109 oxidation tests complete

• OM646 LA biodiesel and M271 EVO sludge proving difficult

• EP6 gasoline piston cleanliness and elastomer compatibility require additional work

Limits for new tests need careful consideration

ACEA specifications must keep pace with engine technology

ACEA European Oil Sequences

expected in 2015

The European ACEA Oil Sequences are being revised to keep pace with engine technology and to address concerns about biofuels. A new C5 category is expected, driven by OEM requirements for improved fuel economy, and presents an opportunity to reassess the current categories and explore if complexity can be reduced. Test availability is the key factor affecting the updated specification’s release date. Some of the critical tests are still under development and proving to be difficult to complete. The ACEA specifications must be representative of the vehicle fleet they are meant to protect. Replacing tests that are either: coming to the end of life or which are no longer representative, will remain an evergreen topic for ACEA.

Slide 19

P A S S E N G E R C A R S

Bruce Royan | Infineum UK Ltd – Lubricants Technology Manager

PCMO23NA SHOW

PCMO E

Bruce Royan returns to offer us his thoughts on these ACEA developments. Bruce Royan: The new ACEA sequences will bring further complexity to the European marketplace. It is important that we deliver higher levels of fuel economy through lubrication in Europe; nevertheless, the approach being taken will fragment further an already very fragmented marketplace. One of the key challenges has been the development of new engine tests that are both reproducible and repeatable and will serve the purpose required within the ACEA specification.

Slide 20

P A S S E N G E R C A R S

Kazuo Yamamori | Toyota Motor Corp., Tribology Material Dept.,

Material Development Division – Project Manager

NA SHOW PCMO25

PCMO G-1

We finish the PCMO section with some thoughts from Yamamori-san, on the need for better consumer education and the benefits of such an initiative. Kazuo Yamaori: We feel that activities that spread information and knowledge to consumers remain important for the automotive industry and lubricating oil industry. JAMA holds an annual engine oil seminar mainly for the Asia Pacific region – the area in which we wish to further pursue this activity – in order to promote the consumers’ knowledge about high quality oils and to disseminate information to them with the support from relevant industries.

Slide 21

P A S S E N G E R C A R S NA SHOW PCMO7

Unprecedented test development activity

Aggressive timeline to meet GF-6

Intensive activity around new andrevised OEM specifications

In summary, passenger car lubricants are entering a time of unprecedented change in the automotive industry.