Embed Size (px)

Citation preview

PARTNERSHIPS

Robin MacKnight

Topics for Discussion

• Why use a Partnership?

• What is a Partnership?

• Tax Fictions of Partnerships

• Income, Loss and Gains

• Basis Calculations

• Partnership Reorganizations

• Limited Partnerships

• Tax Shelters

• Tax Shelter Opinions

• Estate Planning using partnerships

May 18, 2011 2011 Tax Law For Lawyers 2

May 18, 2011 2011 Tax Law For Lawyers 3

Predictions

• CCRA will continue to challenge taxpayers who use partnerships as a business vehicle

• CCRA will focus on whether a “business” exists and whether the partners carry it on “in common”

• More taxpayers will realize the advantages of the partnership structure and will increasingly use them

May 18, 2011 2011 Tax Law For Lawyers 4

Thought for the Day

• Anything you can do with a

corporation, I can do better with a

partnership!

May 18, 2011 2011 Tax Law For Lawyers 5

Why Use a Partnership?

• It’s not a corporation!!

• No statutory rules

• No statutory protections

• Flexibility – in governance and changing

member rights and interests

• Conduit for tax purposes

May 18, 2011 2011 Tax Law For Lawyers 6

Advantages to a Partnership

• Rollovers:

• Real estate

• Allocate inherent tax liability to contributing partner

• Governance:

• No statutory minority protection

• Matter of contract

• Anonymity – minimal filing and disclosure requirement

May 18, 2011 2011 Tax Law For Lawyers 7

Advantages

• Compensation:

• Avoids employment issues

• Allows “self correction” based on

performance

May 18, 2011 2011 Tax Law For Lawyers 8

Advantages

• Flexibility:

• Easier to trace performance of

business units

• No solvency tests

• Allows “self correction” of relative

ownership to protect the business

May 18, 2011 2011 Tax Law For Lawyers 9

Disadvantages

• CRA skeptical of partnerships – perception of

tax avoidance vehicle

• Skepticism based on application of section

103

• Notwithstanding, increasing use of

partnerships and conduit vehicles

May 18, 2011 2011 Tax Law For Lawyers 10

What is a Partnership?

• Common law test

• Two or more persons

• Carrying on business

• In common

• With a view to profit

• Codified in provincial Partnership Act

• Artificial statutory creatures – limited

partnership, limited liability partnership

May 18, 2011 2011 Tax Law For Lawyers 11

The Concept of Business

• “Adventure in the nature of trade” is a

business for tax purposes

• Does mere common ownership suffice?

• What commercial activity is required to

meet the business threshold?

• McKeown 2001 DTC 511

• Banner Pharmacaps NRO Ltd. 2003 FCA

367; 2003 DTC 5642

• Hudon 2001 FCA 320; [2002] 1 CTC 25

May 18, 2011 2011 Tax Law For Lawyers 12

Common Law Tests

• “in common” – requires intention of the

parties to create a partnership

• Critical difference between partnership

and other vehicles

May 18, 2011 2011 Tax Law For Lawyers 13

Common Law Tests

• Note that tax motivation is not a common law

test – but query whether it could demonstrate

intention?

• Tax motivation does not expressly disqualify

a partnership under either partnership or tax

rules

May 18, 2011 2011 Tax Law For Lawyers 14

Common Law Tests

• No requirement that partnership agreement be in

writing or be registered

• Consequently, many unwritten commercial

arrangements may constitute a partnership under

common law

• Note that a limited partnership does not exist until

notice is registered

Common Law Tests (cont’d)

May 18, 2011 2011 Tax Law For Lawyers 15

May 18, 2011 2011 Tax Law For Lawyers 16

Common Law Tests• Conflict of law issue – is a partnership

recognized under the law of one jurisdiction

automatically recognized if it carries on business

in another?

• Classification issue presents problems and

opportunities

May 18, 2011 2011 Tax Law For Lawyers 17

What is Not a Partnership?

• Why do we care?

• Co-ownership

• Syndicate

• Joint Venture

• Agency

• Tenancy in common

• Joint tenancy

• Participating debt instruments

May 18, 2011 2011 Tax Law For Lawyers 18

Why do we care?

• Tax consequences:

• Who recognizes income/gain/loss?

• Who is entitled to what deductions?

• Who is restricted in ability to claim

deductions?

• What deductions/expenses are pooled?

May 18, 2011 2011 Tax Law For Lawyers 19

Co-Ownership

• May not have the intention to carry on business – eg. Succession on death

• Interest transferable

• No agency between co-owners

• Ability to force partition of ownership

• No lien on property for liabilities incurred on behalf of the venture

• Differences in liquidation/partition

May 18, 2011 2011 Tax Law For Lawyers 20

Syndicates and Joint Ventures

• No clear legal distinction from partnerships

• No definitions for tax purposes

• General commercial difference is scope of

activity – single purpose/transaction or

business?

• Governing agreement may disclaim

intention to create a partnership – but how

do the parties really act?

May 18, 2011 2011 Tax Law For Lawyers 21

Joint Tenancy and Tenancy-in-

Common• Clearly defined legal relationships

• Legal consequences different from

partnership, including:

• Ability to dispose of property

• Ability to demand partition

• Succession to ownership

May 18, 2011 2011 Tax Law For Lawyers 22

Participating Debt Instruments

• Lender may be entitled to participate in the

cash flow of borrower’s project or in the

appreciation in value of the assets

• If participation payments are not interest,

are they a distribution of partnership

revenues/profits?

May 18, 2011 2011 Tax Law For Lawyers 23

Differences between tax and

commercial law

• Allocation of profit and loss

• Status of partners

May 18, 2011 2011 Tax Law For Lawyers 24

Tax Fictions of

Partnerships

May 18, 2011 2011 Tax Law For Lawyers 25

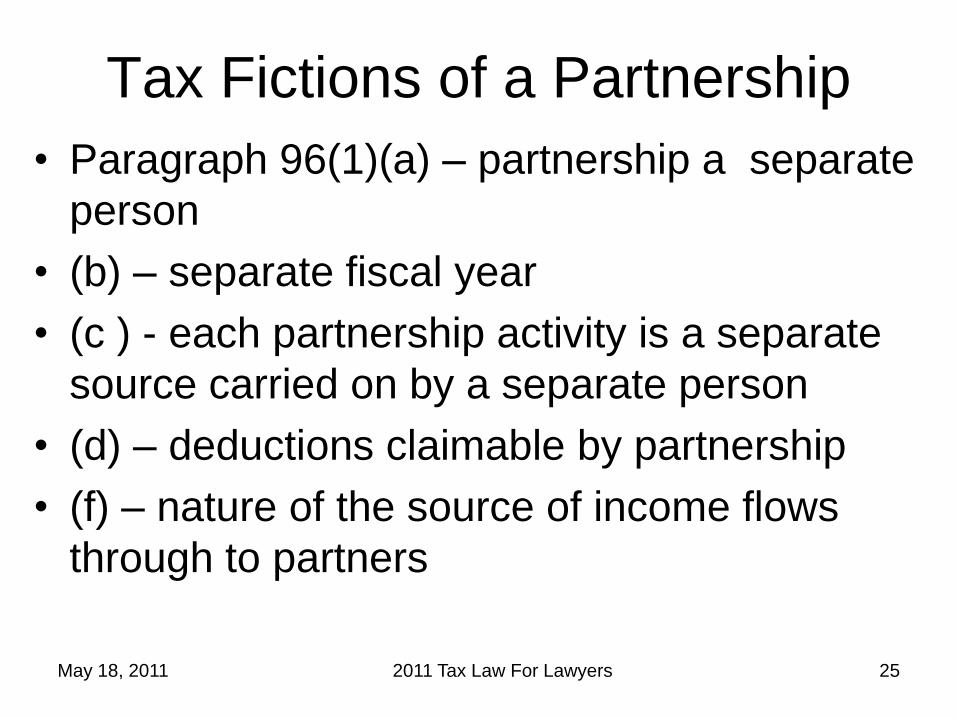

Tax Fictions of a Partnership

• Paragraph 96(1)(a) – partnership a separate

person

• (b) – separate fiscal year

• (c ) - each partnership activity is a separate

source carried on by a separate person

• (d) – deductions claimable by partnership

• (f) – nature of the source of income flows

through to partners

May 18, 2011 2011 Tax Law For Lawyers 26

More Tax Fictions

• Ss. 96(1.1) – deemed continuing partners

• Ss. 102(1) – definition of “Canadian

partnership”

• Ss. 212(13.1) – withholding tax obligations

May 18, 2011 2011 Tax Law For Lawyers 27

Computation and Allocation of Income

• Income computed as if partnership were a

separate person from partners

• Income/gain/loss computed by source

• Income allocation generally set out in

partnership agreement

• Partners recognize income for their tax year

in which partnership tax year ends

• Note 249.1 for partnership fiscal year

May 18, 2011 2011 Tax Law For Lawyers 28

Calculation of ACB

• Bumps and grinds – paragraphs 53(1)(e)

and 53(2)(c)

• ITAR 26 for pre-72 partnership interests

• Timing of calculation is critical

May 18, 2011 2011 Tax Law For Lawyers 29

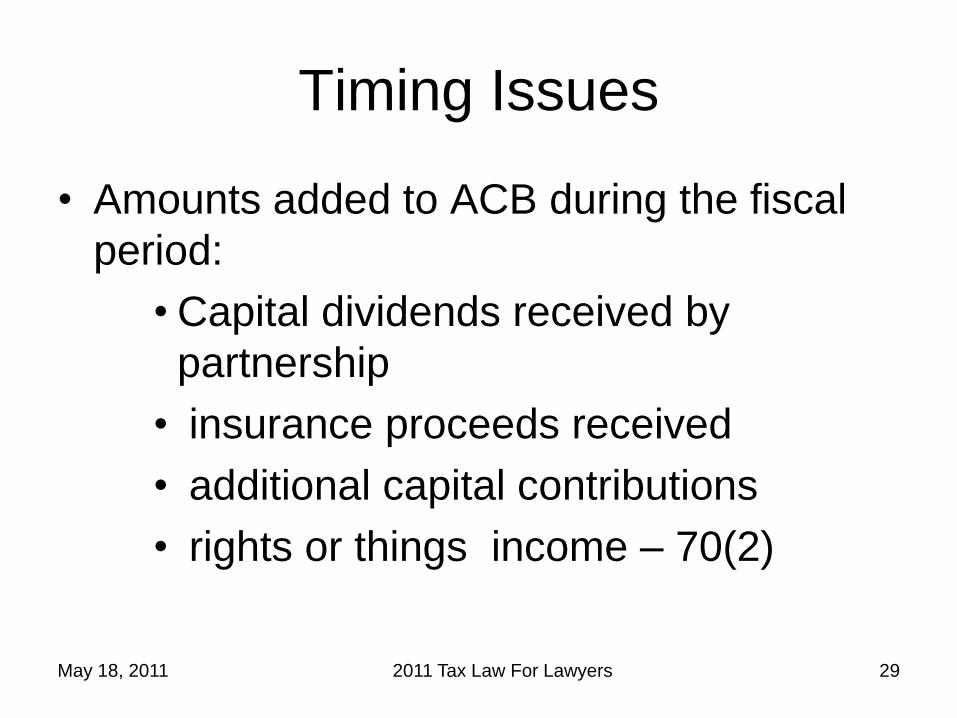

Timing Issues

• Amounts added to ACB during the fiscal

period:

• Capital dividends received by

partnership

• insurance proceeds received

• additional capital contributions

• rights or things income – 70(2)

May 18, 2011 2011 Tax Law For Lawyers 30

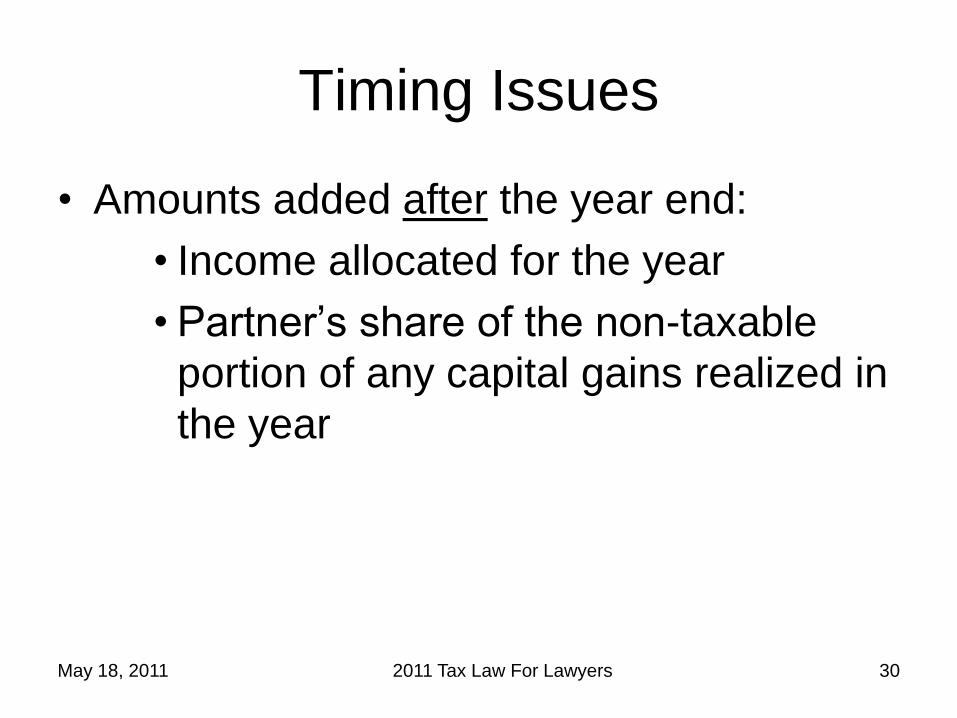

Timing Issues

• Amounts added after the year end:

• Income allocated for the year

• Partner’s share of the non-taxable

portion of any capital gains realized in

the year

May 18, 2011 2011 Tax Law For Lawyers 31

Timing Issues

• Deductions during the fiscal year:

• Partnership drawings and capital

distributions

• Non-recourse debt used to acquire

the partnership interest

• ITC’s claimed by partner during the

year

May 18, 2011 2011 Tax Law For Lawyers 32

Timing Issues

• Deductions after the fiscal year:

• Allocated losses (but “limited partnership losses” only reduce ACB when they are claimed by the partner)

• Allocated share of the non-deductible portion of capital losses

• Allocated resource expenditures

• Allocated charitable and political tax credits

May 18, 2011 2011 Tax Law For Lawyers 33

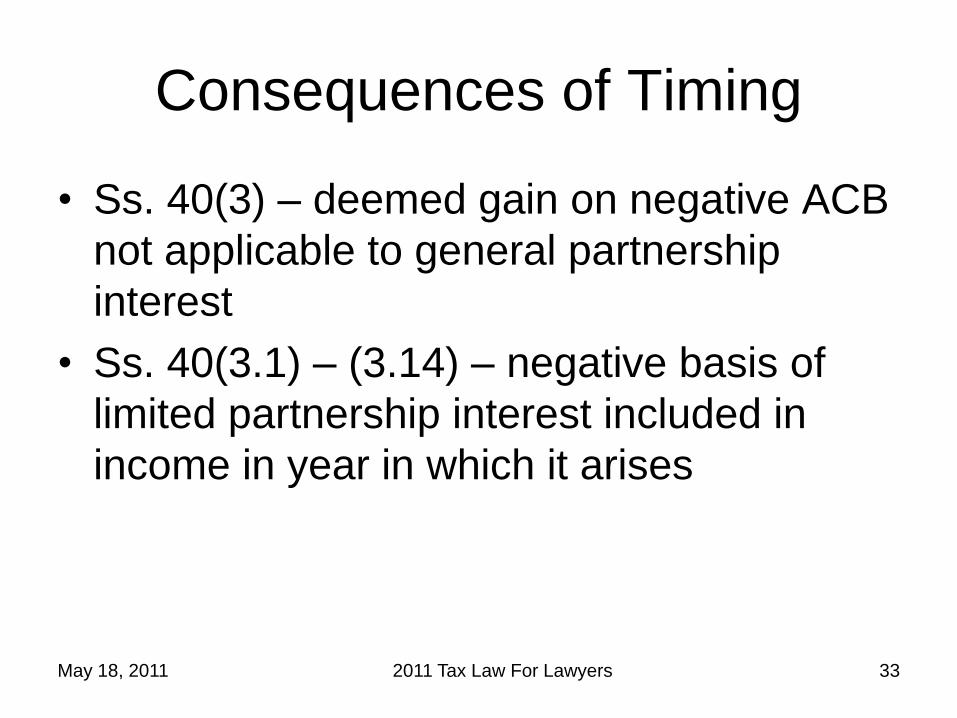

Consequences of Timing

• Ss. 40(3) – deemed gain on negative ACB

not applicable to general partnership

interest

• Ss. 40(3.1) – (3.14) – negative basis of

limited partnership interest included in

income in year in which it arises

May 18, 2011 2011 Tax Law For Lawyers 34

Dispositions of Partnership

Interests Mid-Year

• Proposed ss. 96(1.01) addresses mid-year

dispositions

• Fiscal period deemed to end immediately

before taxpayer ceased to be a member –

96(1.01)(b)(ii)

• Result is that income or loss for stub period

is included in ACB calculation