Embed Size (px)

Citation preview

Paris Europlace, New York : 18 April 2018

France and Europe: economic developments, reforms and attractiveness

François VILLEROY de GALHAU, Governor of the Banque de France

2

EURO AREA: FROM THE RECOVERY TO AN EXPANSION PHASE

Robust growth across countries

Sources: Eurostat

-3%

-2%

-1%

0%

1%

2%

3%

4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

2010 2011 2012 2013 2014 2015 2016 2017

Domestic demand

Net exports

Change in inventories

GDP growth (y-o-y)

Domestic demand to support growth

Sources: Eurostat

88

92

96

100

104

108

112

88

92

96

100

104

108

112

2006 2008 2010 2012 2014 2016

Euro area France Germany

Italy Spain

3

EURO AREA: LABOUR MARKET BACK TO ITS PRE-CRISIS LEVEL

Almost 8 millions jobs added since 2013Q2 Large fall of the unemployment rate

Sources: Eurostat

0m

1m

2m

3m

4m

5m

6m

7m

8m

0m

1m

2m

3m

4m

5m

6m

7m

8m

2014 2015 2016 2017

7%

8%

9%

10%

11%

12%

13%

7%

8%

9%

10%

11%

12%

13%

2000 2005 2010 2015 2020

Sources: Eurostat + March 2018 ECB Projections

4

FRANCE: ROBUST GROWTH SUPPORTED BY BUOYANT DOMESTIC DEMAND AND DYNAMIC NET EXPORTS

GDP growth and its components (%/pp)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2010 2012 2014 2016 2018 2020

GDP growth

Private consumption

Private investment

Public demand

Net exports

Inventories

Sources: Insee + March 2018 BdF Projections

5

FRANCE: IMPROVING LABOUR MARKET

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

2010 2012 2014 2016 2018 20201.0

1.5

2.0

2.5

3.0

3.5

4.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2010 2012 2014 2016 2018 2020

Unemployment rate Wage growth (private sector)

Sources: Insee + March 2018 BdF Projections Sources: Insee + March 2018 BdF Projections

6

EURO AREA INFLATION: PROGRESS TOWARDS THE TARGET

Deflationary risks have disappeared

Sources: Eurostat

-1

0

1

2

3

4

-1

0

1

2

3

4

2006 2008 2010 2012 2014 2016 2018 2020

Phillps Curve Simulated

HICP Headline

ECB Projections (March 2018)

Sources: Eurostat, ECB, BdF calculations

Gradual return to target in the medium term

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015 2016 2017 2018

Headline inflation, Euro area

Core inflation (excluding food and energy), Euro area

Last data: March 2018

7

INSTRUMENTS OF UNCONVENTIONAL MONETARY POLICY: A ‘QUARTET’ OF MEASURES

1. Liquidity provision

Fixed-Rate Full Allotment (since October 2008)

TLTRO-I (launched in June 2014);

2. Forward Guidance (since July 2013);

3. Negative rates on the deposit facility (since June 2014);

4. Asset Purchases Programme (since January 2015), €60 billion monthly, at least until Sep. 2016.

- Extensions -

March 2016: cut of the deposit facility rate = -0.4%; monthly purchases to €80 billion; TLTRO-II (€760 billion as of Sep. 2017)

December 2016 : APP extended at least until Dec. 2017, an additionnal € 60 billion/month.

October 2017: APP extended to end of Sep. 2018, €30 billion/month; reinvest the principal payment for an extended period of time… for as long as necessary; liquidity provision (the main refinancing operations + TLTRO) as long as necessary and at least until the end of the last reserve maintenance period of 2019.

Total APP holdings (March 2018) ≈ €2.37 trillion, will increase up to €2.55 trillion by end of Sep. 2018.

8

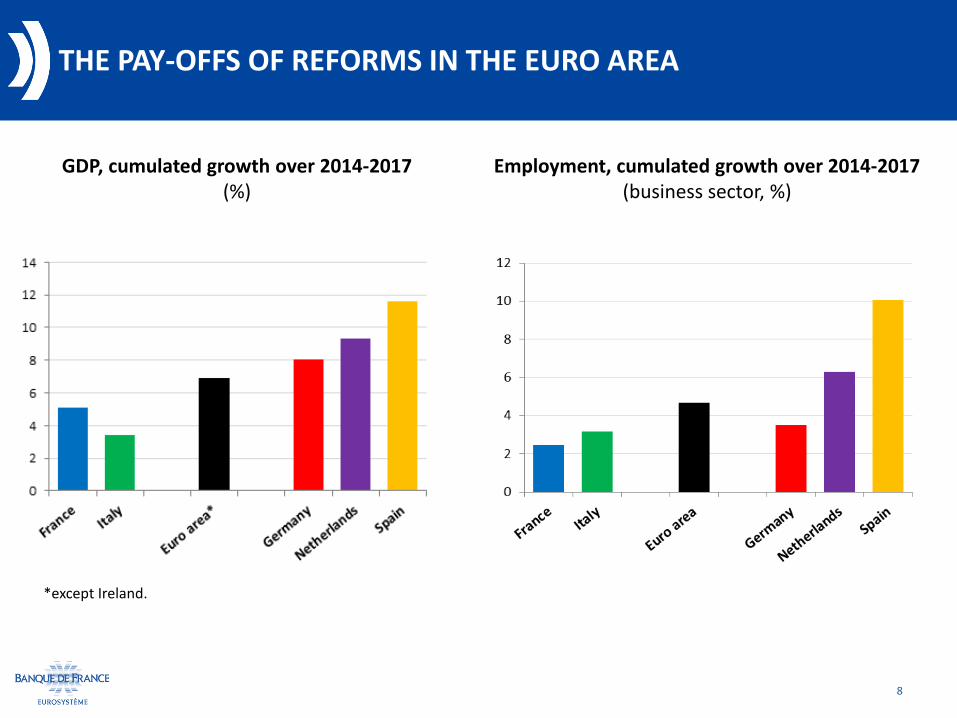

THE PAY-OFFS OF REFORMS IN THE EURO AREA

GDP, cumulated growth over 2014-2017 (%)

*except Ireland.

Employment, cumulated growth over 2014-2017 (business sector, %)

BUT IMPORTANT REMAINING CHALLENGES: HIGH STRUCTURAL UNEMPLOYMENT AND LOW POTENTIAL GROWTH

9

ONGOING REFORMS FOR A BETTER-FUNCTIONING LIFELONG TRAINING AND APPRENTICESHIP SYSTEM

10

Sources: Apprenticeship: Germany: BiBB ; France: INSEE ; Italy: Report Cedefop Italy ; unemployment data: Eurostat.

An ambitious labour market reform was recently implemented: • Widen the negotiation space given to social

partners for decision-making

• Simplify staff-representation obligations: Enlarge the negotiation field and hence ease compromise

• Reduce the uncertainties of labour disputes and better secure labour relations

• Should give more flexibility and reduce uncertainty for firms

Important reforms are also on the way to better adapt worker skills to the needs of firms • A reform of lifelong training (currently inefficient) • A reform of apprenticeship (to make it more attractive for firms and young people) • A reform of insurance benefits (to increase labour force participation)

ONGOING REFORMS TO SUPPORT PUBLIC AND PRIVATE INVESTMENT

11

Private investment rate is expected to remain high:

It has already exceeded the previous peak seen in 2008 and should continue to increase over the projection horizon, reaching 22.8% by end-2020.

The introduction of flat tax on capital gains and dividends and the reduction of corporate income tax should support this positive investment trend 17

18

19

20

21

22

23

17

18

19

20

21

22

23

1995 2000 2005 2010 2015 2020

Corporate investment rate

(% of private value added)

An important public investment plan

Spanned over 2017-2022

In key areas for the future

Energetic transition, digital, infrastructure

Source: BMPE

12

POSITIVE CONFIDENCE REINFORCES FRENCH ATTRACTIVENESS

Source: IPSOS; survey on attractiveness among executives of foreign firms in France

96

98

100

102

104

106

108

96

98

100

102

104

106

108

2015 2016 2017 2018

Business sentiment in manufacturing

Source: Banque de France monthly survey in manufacturing100= long term average

Source : Deloitte